The “Pending Sales Jump” (still -24% year-over-year) was like so January. This is still a frozen housing market.

By Wolf Richter for WOLF STREET.

Funny how this works with the hype-and-hoopla show. The hype about the housing market picking up in January – it should pick up in January, and by a lot, because it’s the beginning of the spring selling season – was just deafening. But it’s already over, just weeks after it started.

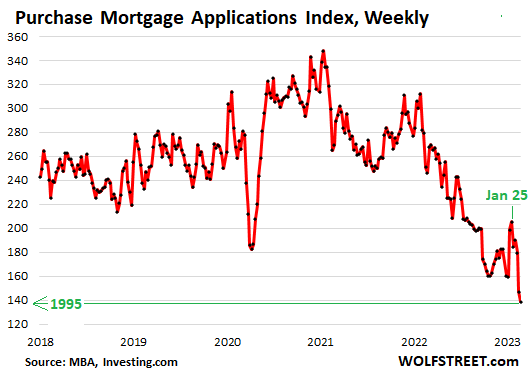

Applications for mortgages to purchase a home plunged every week since late January and now dropped to a new 28-year low. Mortgage applications to purchase a home are a leading indicator of home sales volume. They plunged by 44% year-over-year and by 48% compared to two years ago, to the lowest since 1995, according to data from the Mortgage Bankers Association today.

But note the rise in mortgage applications in January, from the collapsed levels in October through December. It was brief – at the core, just two or three weeks that peaked in the reporting week through January 25. And then it all came apart.

Homebuilders played a big role in the January-hype-and-hoopla show. They’re living off their backlogs because their sales orders in Q4 collapsed by 40% to 60%. Those sales orders, if they’re not cancelled, represent future revenues. Builders’ Q4 revenues and earnings derived largely from completing homes and closing sales from previous sales orders that were part of their backlog. They were eager to brush aside the collapse in sales orders in Q4, which represent future revenues. So they focused on the uptick in sales orders in January from the collapsed levels in Q4. Analysts went for it, and homebuilder stocks jumped, which was the purpose.

Then came the media’s breathless headline about “pending sales” for January a few days ago, by the National Association of Realtors. The media, always eager to hype housing, was all over it: “Pending sales jumped 8.1%,” and similar stuff, the headlines read. Jumped from what?

From the collapsed levels in DECEMBER. Compared to January a year ago, pending sales were still down 24%! But most people only read the headlines.

The 8.1% increase in pending sales from the collapsed levels in December was triggered by a brief and now vanished drop in mortgage rates toward 6%.

Everything bounced in January, stocks, bonds, cryptos. Bankruptcy equities and collapsed post-SPAC and post-IPO stocks doubled or tripled in days. As bond prices jumped, long-term yields fell, and mortgage rates too fell toward that 6%. And it caused a brief uptick in home sales from the collapsed levels in December.

But all that reversed in February. The 10-year Treasury yield is back at around 4%. The average 30-year fixed mortgage rate is now near the magic 7% again. Markets are finally starting to see ever so gradually that this inflation is sticky, that it re-heated in December and January, and that interest rates are going higher and staying there for longer.

And the spring selling season already fizzled. All this hype was based on what amounted to a two- or three-week period in January when activity perked up from the depressed levels late last year. But even at the peak toward the end of January, mortgage applications were still down by 32% from a year earlier and by 38% from two years earlier.

This is still a frozen housing market, that’s what these mortgage applications tell us. For sales volume to rise to normal levels, prices need to come down, and by a lot, to make sense with 7% mortgages.

There is a stand-off in the market, with many potential sellers, confused by all this hype, still thinking that this too shall pass, namely these mortgage rates, and that somehow the sub-3% mortgages will return to make their aspirational prices possible, even as inflation is eating everyone’s lunch, in some cases literally. And so they cling to their aspirational prices, or hold their vacant properties off the market, waiting for the return of the 3% mortgage rates.

A healthy – or at least a thawing – housing market needs to have sellers and brokers that are in touch with reality, and the reality is set by potential buyers.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If you need a house, time to start thinking about making lots of lowball offers. Somebody will bite.

At some time, gov’t will pull out all the stops to prevent more downside. In 2008 they enacted a foreclosure moratorium, forced mortgage refinances, short selling ban, etc… The banks kept their inventory off market and sold it all to corporations.

If you get into trouble, do not mail in the keys. Just stop making payments and save your money. In 2008 gov’t made it impossible to evict people, they lived payment free for a couple of years. Also, be very wary of taking a mortgage refinance because they turn no recourse loans into recourse.

Good luck out there.

Patience – a lowball offer is probably only 10-20% lower than a seller’s dream price. Why pay that much?

Just wait. Let all the momentum turn upside down. This will likely be a very long downturn in the housing market. A whole lot of equity needs to be destroyed before distress hits the market and it bottoms.

I agree. This is not the time to even make a low ball offer considering how much prices have run up in last 3 years.

+1

+1

It’s best to sit out this spring and let it crash and burn!

In Seattle, with price falling ~2% every month, buyers are saving ~ $20K every month that they chose to delay a full cash purchase. Add the 30 year 7% interest to that $20K, and it becomes $48K per month savings.

That’s more than twice the earning of most households in this region. So why sweat?

+1

A personal opinion and “quick math” solution to setting a lowball offer… look at the 2017-2018 market and use that as a baseline for the lowball – eventually the current market will find you.

You must get a good real estate agent who can write offers at 2018 prices.

A lazy one will avoid work of writing offers and you are best filing him.

It’s best to sit out this spring and let it crash and burn!

In Seattle, woth price falling ~2% every month, buyers are saving ~ $20,000 every month that they chose to delay a full cash purchase. Add the 30 year 7% interest rate to that $20K, and it becomes $48,000 per month savings.

That’s more than twice the earning of most households in this region. So why sweat?

Even before the recent 2 year run up, prices were high and buying was irrational driven by investors with owners becoming landlords increasingly because they could not part with something appreciating that fast, not because they want to be in the real estate business. If one is to buy because they actually need house housing, don’t just rent and protest this market!

One can only hope.

Wait

Wait…

But

Muh

Real Estate Agent ™

Who is an experienced Professional, and all..

And knows the markets inside out, (She graduated summa-cum-load

She ran my financials, took my credit cards…

And she says..

Wait for it….

“IT IS ALWAYS A GOOD TIME TO BUY”!

So all you loser commenters don’t know squat!!

So there…

Morty..

Time for meds…

Pay a financial advisor to be your fudiciary to give you the right financial advice without conflict of interest.

The real estate agent is not paid by you and is not expected to be your fiduciary. They are governed by the most corrupt “National Association of Realtors”.

YouTube is loaded with testimonials from Seattle area realtors talking up recent sales. Most look to be too young to have weathered the before and after of the last bubble. It’s just sad.

It’s wild, people’s faces and professional reputations are going to be stamped all over this collapse.

They would just delete their YouTube videos.

Pay a financial advisor to be your fudiciary to give you the right financial advice without conflict of interest.

The real estate agent is not paid by you and is not expected to be your fiduciary. They are governed by the most corrupt “National Association of Realtors”.

“Lived payment free for a couple of years.” Next door neighbor took 8 yrs. That is not a misprint. BTW I’m in the Escrow biz. People have no idea how jacked the market was and the nonsense blessed by the real estate industry and also lenders. People only know what they read in the media. Being in the trenches daily was just nuts. My signature is on proceed checks for $10K to sellers as an “incentive” and to help “defray moving/closing costs,” who hadn’t made payments in years, collected rent payments and laughed all the way to the bank. It was a shit show like no other. There is a large cohort of owners today that are “walk away” veterans who will easily do it again. And the real estate industry will hold workshops again on how to stop making payments, collect rents or Airbnb rents and wait until their “investment home” is finally foreclosed on, taken back by the lender and put on the market as and REO. Agents should look into their closet and dust off their “short sale” hats.

Thanks for your comment. I remember some of your experiences from other sites like seattle bubble.

I would imagine the 10k payment was to make sure they move out without doing damage. Otherwise some of these people would strip out anything that can be sold, leaving the place as a tear down.

Great post. The “cash for keys” Deed in Lieu of Foreclosure is actually my favorite way of avoiding a foreclosure. But why would you wait years to present the offer?

Last month I presented the offer (after his 3 month incarceration for a bar fight) while he still had a small portion of his downpayment remaining in equity and he found the money to come current.

The note is at current rates. No requirement for any insurance: wind, flood, hurricane, fire, theft, damage, nothing. Replacing insurance companies is the key to success in banking.

I don’t think that there will be ANY relief for homeowners this time. 2008 wasn’t really a real estate crisis – it was a financial, banking, and derivatives crisis.

The danger was that the derivatives would blow up the financial system. Houses were simply the mechanism through which the derivatives were created and got caught in the crossfire. Yes, there was a ridiculous amount of speculation (and if you don’t remember or were too young to live through it, watch “The Big Short” – or google “Casey Serin”) and more crap derivatives created than could be believed (CDO squared, anyone?). Slowing foreclosures and all of the other activity was to help the banks and the financial system unwind the toxic positions without destroying the entire system. Homeowners were used to “foam the runway” and if homeowners in some minor way benefited, that was incidental to “saving” the financial system.

But as Wolf and others have pointed out, the financial system today is largely immune to the fallout from declining house prices. And the FED only cares about the financial system; any relief from the FED will not be to help individuals directly.

The short selling ban, by which I presume you mean short selling stocks, not houses, was, as I recall, restricted to shorting financials. I remember it vividly: I was short a meaningful position on WF and my 25% gain evaporated into a 10% loss the day the ban was put into effect. That was another way to help the banks (I think that Citi was insolvent at the time). Again, no short selling ban in financials (or anywhere) if the impact from a general house price decline doesn’t impact the financial system.

On making lowball offers – it feels really early. I have a few select markets I watch in both the west (ID, MT) and the east (NH, VT) and the majority of houses are listed at prices equal to or greater than the peak a year or 18 months ago. Too many listings that were bought in 2018/19 at a (hypothetical) 400k now asking 725k. Offering the 2018 purchase price as a “low ball” may even be too high; on a monthly payment basis the SAME purchase price as 2018 is 60% more. Sellers need to have the reality check of a spring with no viewings, let alone offers, to get the message.

Finally, accept that there will be continuous and ongoing anecdotes about “bidding wars”, “all-cash offers”, “four offers in a day”, etc. Again, as our esteemed host mentions frequently – a well priced property in good condition will sell (and probably sell quickly).

A house built when Clinton was president (and untouched since) and priced at 60% over a 2019 price will sit.

And sit.

And sit.

How do you feel about Kalispell? I’m hip to MT (Lived there six years) but dipped in the Covid frenzy. It just got INSANE, carpet baggers with war chests of gold moving into small mountain towns.

I’ve recently been watching Kalispell and noticing their market is stabilizing quite a bit, but considering how the smoke sits in that valley in fire season IDK.

I’m finally starting to see these people who moved in getting the picture that it’s not Yellowstone on paramount. It’s a desolate harsh climate you need to be prepared for, even if it does have its treasures.

You can not compare residential property prices in 2018 with asking prices today. The FED has $2.8 trillion of MBS on their Balance Sheet all added since 2010 and maybe 90% under 4.5% with nearly 1Trillion under 3.25%. Us Boomers may still have mortgages because we have been forced to refi since the early 80’s as we upsized from starter homes and road the declining interest rate wave. With kids and college expenses and sometimes access to 401k’s until mid career that was your only improvement to cash flow you could get.

Everyone of my sisters and BIL, our millennial children refied during 2020 who had a home or could afford to buy one. With rates as low as 2.45%. I did I cash out and full house renovation in a highly desirable part of the country with D/E of under 30%. Everything new. None of us are going anywhere. This was a window of opportunity created by a foolish fed to protect big banks. We have vivid memories of the 80’s and entrenched inflation. At least our millennial children are receiving great raises. Their problems are childcare.

Now this economy and the housing sector is locked up. The only people selling are those that have too. Those that are buying are those downsizing with cash or cashing out declining Stock Options.

My property will become rental property before being sold. My Million dollar highly desirable family neighborhood with no buildable land in town. JMO

Wolf how many individual residential mortgages do you think the FED is holding and will they roll over much in the next decade?

In terms of your question: The Fed holds zero individual residential mortgages. It holds MBS that are each backed by a pool of residential mortgages.

In terms of your point of “not selling” your home: Whether a live-in homeowner sells or doesn’t sell is irrelevant overall for housing inventory if the homeowner buys another home. It’s only relevant for Realtors because they make a commission. When you sell your home that you live in, and buy another home, you put one home on the market and take another home off the market, and the net effect on inventory is zero.

What will increase inventory is when people put their vacant homes on the market, or when people die or move into a nursing home and their home gets sold, or when they sell their home to move into a rental.

Home many vacant homes are there? Lots. Of them, 11 million are vacant year-round. Of them, 3.5 million vacant homes that are being “held off the market” for a variety of reasons including that the owners don’t want to sell at this point. If just 20% of the 3.5 million held-off-the-market homes show up on the market, you’ve got a glut.

https://wolfstreet.com/2023/02/02/what-is-the-actual-housing-vacancy-rate-census-bureau/

Feckless boomer slim got housing upside. Rental nightmare to capture your time for pennies on the dollar. They brought in the amigos to build at $15 per hour for the last 20 years, zero benefits, while the tax ships of gringo go round and round. They frame, shingle, nail till they die never mind any education, we got investment backed by bs money on the line. No GOLD, no HOUSING, no FOOD! The sellout grand-fraud parents have pensions to be guaranteed for their warmth and comfort. They sell your future like their own grandkids future thru 401k, Moar is all they ask, now 50 year advantage to rob and steal, fall inline and pay inflation then add tax and regulation theft for the old worthless slim. Our money not yours, you obey, while they erase your time.

Translation needed. Is this even written in English?

Slim means slender. Is your word missing an “e”?

I’ve been looking since before the pandemic and have been outbid. At this point the rent is cheaper than the mortgage. I’m in Chicago. The broker said ppl are still paying over asking and bidding wars. He thinks it’s really not going to slow down as long as the inventory is low. Looks like I’ll be a permanent renter

Patience is a virtue and this unwind as your charts show is just starting.

Late Spring after realizing buyers are still not buying may be the real noticeable start of the turn for real estate south…

Why are people thinking in terms of months? This is years of downside to the bottom.

Absolutely many years.

Lately I’m of suspicion that the bottom of this everything bubble bust might never be reached, but it will be the endless asymptotic drift lower – Japanese style. Demographics are ruthless.

Nah, prices will eventually drop enough for smart money to buy again. With the speed of the decline so far I think it’s possible the bottom might occur in 3 years instead of the 4 or so in the last bubble.

Reits look to be breaking down here. Investors apparently just woke up out of a deep slumber to realize 6 month tbills are near 5%.

It’s not demographics, it’s manic psychology.

Artificially cheap money and basement level credit standards which some think are “strict”.

I’m guessing 2 years.

I just read an article recently that said 8 quarters.

:(

I need more patience.

Smile, you will be saving money!

My point was do not expect market forces to overcome market manipulation, which I did not make clear.

Not that Wolf needs any validation, but I can tell you all that this spring is going to be rough with a capital R on the housing market. As an LO in the DC Metro area, normally, by March 1, I have 20-30 pre-approved borrowers ready to go out and buy a home. This year? 5. I might have to dust off my flashlight and go back to working the door checking IDs at the local pub if this keeps up.

5 is A LOT in this market… My buddy (in the same position but in Orange Cty CA) has 1….

I got a pre-approval from a broker I used in times past… have been waiting to purchase forever and finally saw something i was interested in.

Of course, it was overpriced and some idiot bit on it and seller took it. But point is- just that one lousy pre-approval letter I got has literally generated 25+ random texts from across the country and 15+ calls for me to mortgage with a bunch of people I have no clue who they are.

I know it’s just me, a random dude, but it did strike me as real desperation to be blowing up my phone for a lousy pre-approval.

All Good you can thank “trigger leads” and a desperation for business across mortgage land. Mortgage lenders, especially broker chop shops, purchase leads from the credit bureaus. The credit bureaus sell them your information as someone who recently had their credit pulled by a mortgage lender.

I know Wolf does not like links, if you google optoutprescreen you can get your name off these lists in the future.

DR J 2022 into 2023 has been a major reality check for even seasoned pros in this line of work. I’ve been doing this for 10 years and I’ve never seen a freeze quite like this. Hope your buddy hangs in there.

I wonder how many people in the mortgage biz were in it through the last big bust in 2008. A lot of short memories.

Why not think “what does my local economy actually need?”

Cuz being a Realtor serves no purpose that people need. It’s basically a smiling face attached to a fee.

Find a real niche. Entrepreneur Magazine might be a place to start looking?

In my market (Reno-Tahoe) the pending and sold numbers are up leaving not much in the way of inventory. This bump in activity is from 30-60 days ago but new listings are few? May not matter as the new rates will kill traffic. This low inventory situation may have just enough buyers to keep prices from falling further. At some point listings have to move up? The big news here is the announcement Tesla will be investing billions more in my area. This will not help reduce pricing so what will happen next is not clear.

Can you provide a reference to “pending and sold numbers are up”? I just looked a Redfin for Reno:

“In January 2023, Reno home prices were down 15.3% compared to last year, selling for a median price of $468K. On average, homes in Reno sell after 78 days on the market compared to 41 days last year. There were 186 homes sold in January this year, down from 305 last year”.

South Lake Tahoe CA (96150) is comparable (although median is up but have to consider mix):

In January 2023, 96150 home prices were up 5.1% compared to last year, selling for a median price of $652K. On average, homes in 96150 sell after 81 days on the market compared to 23 days last year. There were 99 homes sold in January this year, down from 184 last year.”

And per my earlier comment, the first house (listed 60 minutes ago) on Redfin in Reno is:

13382 Travertine Ln, Reno, NV 89511

Sold April 2017 for $675k

Listed March 2023 for $1,499k.

Reno: Sales down, DOM up, Median Price down

SLT: Sales down, DOM up, Median Price up.

Take sites like Redfin with a grain of salt. My folks home has some really bad pricing data listed on their and Zillow, eg. How do I know? because it hasn’t changed hands in two decades.

The sites are artificially inflating the value of the home to something I can tell you is very unrealistic. Fact is, the home has lost value in the last 20 years.

My buddy, an MLO in NE Maryland, is the last one left in an office that held 12 of us a year and a half ago. He has 2 pre-approvals sitting right now. Two.

It’s a freaking massacre, and the bullets haven’t even begun flying.

Zaridin,

That is pretty scary. I hope your buddy has some savings built up from 2020 and 2021.

Zaridin-

Thank you! Fantastic information!

The Fed pulled the plug on supporting the residential real estate market – they ceased buying RMBS in Sept 2022, permanently . RMBS was historically not an asset held by the Fed but, as an accommodation to gov’t IMHO, the Fed bought RMBS to repress mortgage rates while housing recovered from the 2006-8 debacle. It took 15 years. As the long term housing curve (4% appreciation) caught up to the 2005-8 numbers, the FED leaving it to the market to find its equilibrium post-Covid.

“they ceased buying RMBS in Sept 2022,”

Yes.

“permanently”

No.

If passthrough payments increase enough to hit and exceed the “cap” in any given month (so far this hasn’t been happening), the Fed will reinvest the excess, just as they said they would.

Speaking of astronomical future fizzle

“For most businesses, a recession is not a good thing, and I would never wish for something that is not good for others,” Blecharczyk tells Quartz. However, he says, “I think actually we would thrive in a recession.”

Airbnb, after all, was founded at the dawn of the Great Recession in 2008—a time when many people were losing both their jobs and their homes.

Hewlett-Packard, considered the granddaddy of Silicon Valley, was founded during the Great Depression.

Wonder what kind of BS the MSM is going to come up with now to tell us thr turnaround us right around the corner?

All hopes pin to Spring miracle I guess…good luck

But, but, but …. the main stream media is always right…. right?

We are already in the spring selling season, and there is no miracle. 10 year is over 4% today.

Yun replaced David Lehrea as NAR economist. I recall he took a lot of abuse and made a statement “My mother reads this stuff”. Maybe Yun will crack some day.

Stop making fun of my Larry.

Hurricane wind speeds and wave height increasing, as imminent category 5 storm heads towards paradise

Total short-term rental supply in the U.S. reached 1.38 million listings in September, up 23% compared with the same time last year, according to AirDNA, an industry analytics firm. A whopping 62% of active listings have been added since 2020.

The next downturn in travel and tourism will whollop this hard. Properties will go back to regular rentals or get dumped on the market. Owning an Air B&B has become a way too trendy quick-buck venture among people who know little of the housing market.

Mike G,

I sincerely hope so!!!

When you live in a vacation spot, all the AirBnbs trying to make a quick buck really suck.

Locals can’t afford any nice houses and are pushed to the fringes/outskirts.

All my neighbors are leveraged out the wazoo riding the AirBnb train.

If they lose income it will be cascading foreclosures.

I find it amazing so many investors have not factored in possible severe, prolonged unemployment in their investing decisions. Excess jobs narrative scam blinded people to extreme greed and riskiness, again. Only worse. Substantially worse. I remember in normal times a rental could sit 3-6 months before being leased. And that was at 70% less than today. Bubble psychosis leads to blindness and memory loss.

Dr. Duration – where did you get these stats? I believe you, but this is NUTS. Have to see it with my own eyes.

This is exactly what the Fed THOUGHT they wanted. Now watch it spill over into all the ancillary industries from construction to furniture to home services. The real blood bath will start this fall. Incomes will drop. Jobs will be lost, and the long-awaited recession everyone thinks we’ve avoided will finish off the economy.

Panic first and sell now while you still can.

Kashkari has it right for once. Wages are rising. If the Fed reverses course, markets and inflation will shoot up like a rocket, and they are back to square one, with even lower credibility (if that’s possible).

I never imagined Kashkari (The Dove of Doves) would see the light.

And there is no reason for Kashkari to worry. Continued and steady asset price drops will not impact the real economy in any significant way, just like the rise in stock and RE markets over the past 10 years had no impact. The reversal of stock market and RE market wealth will be silent as a mouse pissing on cotton.

The wealth effect is concentrated in the top 5% to 10% of the wealth distribution. This combined with artificially low interest rates, sub-basement credit standards, and the loosest fiscal policy in history have supported the mediocre US economy since 2009.

It’s going to be a process, not an event, but the end means the majority of Americans are destined to become poorer or a lot poorer over the indefinite future. This has been a multi-decade asset and credit mania.

I agree! Americans will live a lower life style going forward as they won’t be able to afford or obtain lots of “stuff” they have been accustomed to enjoying. In the Depression you could not afford these discretionary items or services. I ask you what is the difference if you go without because you can’t afford it or it is not on the shelf? Well none. The result is you just don’t have it.

The Fed has credibility? When did that happen?

Yes, I’m beginning to like him.

Or as Harold say, just stop paying. If the housing prices go to free fall a non performing mortageg may be better to the bank than a worthless asset.

Exactly! In 08 I would battle a bank on a short sale and the bank would continue to deny the sale. The logical move for the bank would be to get out before the home dropped further and the bank’s loss would be even bigger right? No. Two things kept banks from approving short sales.

1. The sale would force the bank to log the loss in that fiscal quarter. It’s not a loss until it is sold.

2. The loss mitigation department bonuses were at risk if the losses were too great. So a larger staff bonus was the call. Result “your short sale was denied”.

If banks had to mark to market the asset this would change everything. But until then they will continue to tell the share holders “your money is safe. We still have the home as collateral”. No one really asked what the true value was until much later when the housing crash was all over the news.

If you think the banks were slow in 2008, now you will have to deal with Fannie, Freddie, and FHA which are all the slow moving Federal government.

If it becomes overwhelming for them, their will be a moratium on paying mortgages just like during the pandemic.

I am an optimist. As long as we don’t have massive unemployment, the majority of people will still be able to pay their mortgages on an overvalued house due to them holding 3% loans and wage inflation. It will be a soft landing and I will declare the Fed to be geniuses even though they got us into this mess in the first place.

I mean, what alternatives are there? Leave inflation to eat all that stuff up on its own too?

Should we pay 100k for a couch? Hello Venezuela!!

You have to reset the machine sometimes. It’s eating our money. Hit it with a stick!

High real estate prices have destroyed more businesses than they have created.

Houston, we’ve located the problem for that fuel dump, and confirm we’re entirely out of fuel, and oxygen almost exhausted.

Over…

AZ Family Investigates examined data from the Maricopa County Assessor’s Office, which contained information on every residential property in the county. We found hundreds of investors have bought tens of thousands of properties. The 700 largest investors own more than 71,000 residential properties.

That’s less than 10% of all houses in the county. I thought it would be a lot more, LOL. There are 1.63 million households in the county, including a portion of renters. It’s a big county.

Most of those were bought by investors out of the financial crisis. There are also thousands that were “built to rent,” which was super hot over the past few years, and that were sold by the builder as rentals with tenants, whole subdivisions of them with their own rental offices, to fixed income funds, etc. I’ve covered some of that here.

You cannot just throw out some number that you fished out of the internet somewhere without context. Without context, it’s manipulative BS.

Something smells rotten, besides the jet fuel

Invitation Homes owns and rents out more than 80,000 single-family homes in 16 markets, primarily in the Southwest, the Southeast, and Florida

Rotten? They bought 40,000 of those houses in 2012 out of foreclosure. They bought more in 2013 out of foreclosure. I covered this stuff at the time. It’s not new. Recently, they’ve been buying mostly built-to-rent subdivisions. There are about 150 million homes in the US. It’s a big country. People rent those houses because they WANT to rent them. If there’s demand, there will be supply. If people don’t want to rent the houses, they sit vacant. Other people want to rent apartments in city centers, often expensive apartments, and landlords provide that service. What’s your beef with people who want to rent instead of dealing with the hassles, risks, and costs of ownership? And what’s your beef with landlords trying offer them this service?

“There are 1.63 million households in the county, including a portion of renters. It’s a big county.”

163 million? But agree with your points. I hope you will publish something on Airbnb homes. They will take a serious fall and add to distressed inventory. I see lots of them practically begging for customers

I wrote “There are 1.63 million households in the county,” county without R, and you copied-and-pasted correctly “There are 1.63 million households in the county,” without R, into your comment.

I think you’re seeing an R that’s not there, so you think it must be, “163 million” in the countRy with an R.

All this was about “Maricopa County” not the “country” with an R as in the U.S.

Thanks Wolf for another great report. It further confirms that now is definitely not the time to buy a home.

Whether you favor the market or not, the heightened risk level tells buyers to wait a year to see what happens. Savvy buyers realize this.

The emotional buyers are like gophers running onto the open field, where observant eagles stick claws in their back and carry them away. When the eagle has a stock of bones in his nest, it may be time to buy.

Great analogy!

QUICK! GET DAVID LEREAH ON THE HORN!!

Thanks for the info. I follow the residential real estate market in Utah and New Hampshire. It seems like the market in Utah is pretty much frozen as Wolf has described – big standoff. A condo listed for $290K in 2019 is now listed for $480K, down from $500K 6 months ago.

The part of New Hampshire I follow is more active – some low end properties even going up in price. A condo that went for $90K in 2019 is now $240K and under agreement.

In both places inventory is super low.

The “hype-and-hoopla show” doesn’t bother me when it snookers investors. Investors are supposed to be savvy. But when the hype-and-hoopla show cheats home buyers, many of whom are investing their life savings and many times making the only “big” investment they will ever make, then (then) it’s criminal, and those that participate are guilty of heinous crimes against humanity.

True, but it’s up to buyers to educate themselves about the market and read Wolfstreet.

This mentality, that a home is an asset and homeownership has no downsides, is precisely why we’re in this situation.

I always thought that an asset puts money into your pocket. So unless you’re sub-letting some rooms, I don’t see how any house is an asset.

Just sayin’

Agreed

With mortgage applications in such a low level, it’s impossible for demand to recover over the next several months, unless cash buyers come to rescue, but cash buyers are likely to be happy with zero-risk 5% treasuries.

Further RE price drops are locked in.

Thanks to Wolf for highlighting these important statistics, amid all the fluff we hear in the general media.

I hear the phrase “This too shall pass” used frequently in the last few posts. Who was the author of this famous quote?

Hint – Was this a WWI French General from the Battle of Verdun?

“This too shall pass” – Yep, it’ll pass…maybe like a kidney stone, but it will pass.

“And this shall pass”

It will surely pass as everything passes and then it happens again, BUT

the question of the day is how long will it last, because it seems to me that the thing is here to stay for a long time

I always thought it dated back to King Solomon (in Hebrew).

From what I read, in more recent history, it was one of Lincoln favorite sayings. He predates the Battle of Verdun.

Now it’s home sellers’ favorite saying, LOL

It is also a saying popular with “Friends Of Bill”

Why buying a house when you can live “rent free”?

There is a landlord on hunger strike in SF Bay — his tenant won’t pay rent and he can’t kick them out. Wolf should know :-)

Some smart lawyer needs to sue cities that do this. It’s an eminent domain taking by another name, and without the compensation. Gov’ts can take your property rights but it has to be done legally.

There are many landlords that skirt laws and then complain when they end up in situations that leave them no options.

Why do people like you come out of the woodwork whenever the word “landlord” is used, and throw every nasty accusation you can think of?

The vast majority of landlords are law-abiding, and are providing housing to folks with lower asset levels at a monthly cost below an equivalent mortgage (in most metro areas), and do so in a way that presents very little risk to the tenant, but very much risk to the landlord. Most landlords make little profit, and a decent number lose money every month.

Meanwhile, the vast majority of tenants choose to rent because they simply don’t have enough saved for a down payment, they don’t want the commitment of a 30yr mortgage, they don’t want the responsibility of maintaining a property, or they don’t want to commit to a particular location.

I’ve rented close to a dozen properties over the course of my life and none of my landlords have been deadbeats or law-evaders. Stop with this anti-landlord propaganda. They’re too important to our housing market to throw out under the false pretenses of a socialistic fever dream.

Zest,

The 3 of the last 4 places I have rented, the landlord has skirted laws.

1. Illegal conversion of single family house.

2. Applied for demolition permit and withheld information of application upon leasing.

3. Unbrokered property manager handling lease and financial aspects of the property.

It a plague. That’s why we come out!

I’ve rented from Property managers 6 times in my life. In every case I wound up in a lawsuit with the property manager. Need I say more.

Six times? Then the problem is you.

Along Lake Superior where I-35 stops and then connects with Hwy 61, MnDOT is going to resurface the 5 km stretch of London Road.

But they’re going to put in a few roundabouts. Five residential homes will have have to be demolished to do this.

“MnDOT will offer to buy the five homes needed to make room for the project, but could use eminent domain for the project if necessary.”

That was in the local newspaper two days ago. It’s part of a $17 million dollar project that will be decided upon in a month or so & construction should begin in 2025.

“Our life is on hold,” Elizabeth Johnson said. “We just love our house and location and can’t imagine a better place.”

Minnesota will probably bulldoze her house despite the fact that she owns it and does not want to sell it.

Prairie Rider, I’ve been up to Duluth/Lake Superior a fair number of times when I was younger, and I have to agree with MnDOT on this one. Yes, it hurts the soul to lose cherished heirloom homes…but with tens of thousands of cars speeding through the area daily with all their attendant safety issues it’s clear to me multiple roundabouts are appropriate for the situation.

At least the homeowners will likely receive above market value along with moving logistics and expenses assistance.

There are other times I would side with the homeowner, such as with the Vera Coking case in Atlantic City.

It’s way too far gone for the legal process to fix most of our problems. These types of things will eventually end in guerilla terrorism.

There were plenty of programs that made unpaid landlords whole again. Many, many more of those stories, but oh, “Those poor landlords.”

You don’t know much about those programs do you? Hint. It usually requires the tenant to cooperate and prove a loss of income. If they’re just deadbeats, they won’t be able to do the latter and they won’t agree to do the former.

It was a 1.95 billion dollar program in the California. I know plenty about it and the requirements needed from both landlord and tenant.

We would all be better off if the FFR had stayed at 2% and 30yr mortgages at around 5.5%…for the PAST 14 years.

And, I suspect we wouldnt have the inflation, nor the 31.5 national debt.

The Fed, trying to “make things better”, actually made things worse for most of the citizenry. But there is a tranche that did quite well.

Those aren’t normal interest rates, not with the stable rags that pass for balance sheets in the US, at all levels.

“Everything government touches turns to crap.”

–Ringo Starr

Good report. Glad to have found your site and subscribe.

I am a Realtor in a resort ski town, In 2007 when we first heard the words “sub-prime”, and in 2008 the word “short sale”, everyone in the real estate community around here said “Our market is different.” Fast forward to 2010/11, and ski-in/ski-out condos were forced to an auction by the creditors, who were tired of waiting; the developers were holding their prices. The market spoke, and the unsold units (about half) sold for 40% off. The developer of the building next door then let us know THEY would accept 40% off as well, but not lower the prices on the MLS. Such pride. They all sold too. So you had half those buildings sell for say, $1.8mm for a 3 BR unit, while the neighbor paid $3mm a couple years prior.

So it turns out our market was not so different in the end.

Now, it’s like an echo chamber again. The local franchise owner of my large, national firm keeps sharing ‘data’ to show how well our market is doing, and not to listen to the negative ‘media’.

Our prices increases 60 to 120% during the Covid boom. Some buyers even made money when they bought in 2021 and then sold for a 40 or 50 percent gain in 2022. Every day for two years I would look at new listings, new sales, etc, and say “this is ridiculous.” The desperation was real. Residential listings across our MLS went from a normal 1300 or so, to 245 last February. By late summer 2022, they were back up to 950; and now back down to about 750. Transactions are down 40 percent. I keep waiting for prices to dive, but they are surprisingly sticky. I would love to see a massive correction…I have how ridiculously unaffordable this formerly little ski town has become. In 2019 there were 4 sales over $10mm. 19 in 2020, 28 in 2021, back to 18 or so in 2022. But good high end stuff is still selling to those cash buyers. Middle market mortgage stuff is what seems to be slowed the most right now. It’s obvious why, of course.

Wolf, I’d love to read a deep dive on your thoughts about higher-end real estate in resort areas like ski or beach towns. And what you think will put a significant damper on prices. What will make the wealthy stop buying? The founder of Rock Star Energy bought a new spec home in October for $39mm. Biggest sale ever. Four months later, it’s listed for $50mm, supposedly never slept in it. When I say that price, I laughed. But during the pandemic boom, I laughed many times….and it turned out, I was wrong, things just got dumber and dumber. I wonder if I’ll be wrong again and someone will bite on a $50mm home? (The town is Park City, UT, by the way…not Aspen or Jackson.)

From the Deseret News this last summer- Summit County 23.3% of the housing units were now short term rentals- over 6,000 housing units. So, what happens when the consumers stop spending at a torrid pace? Costs keep running and shooting up while income dries up. How many inwestors have the deep pockets to feed the alligator? Say 10 percent throw in the towel to sell or try to convert to long term rental? 600 houses, condos, etc on the market….

But first the consumer needs to pull back in your market. And not crash, just pull back. These prices are also based on cap rates, which is how so many of this “investments” have been sold in the last three years. Vacancy rates will tell the tale. There will be no “affordable” housing for a long time as this market adjusts. And adjusts, and adjusts. How many properties are dark every night because so few units are rented? Investors are fickle. The homeowners of yore were much more committed to the idea of ownership and living in the property. Now it becomes just another investment. And with a bazillion LLCs, there will be no desire to feed that alligator when things get real. In short, it won’t even be jinglemail, just pffft.

I have to wonder how many people who could be potential move up buyers are locked with low rates. How many people would sell and move up if they didn’t have to trade their 3% mortgage for a 7% mortgage? There’s so much demand for houses and I think for prices to meaningfully decline first inflation has to come way down and then mortgage rates will follow. From there I think it’s likely more people will list and move up once mortgage rates are below 5.5% and we will see pricing come down.I know Wolf talks about the shadow inventory also potentially hitting the market. Hopefully something happens to thaw out this frozen market.

I was thinking who else profits from the doubled housing prices in certain areas, is it possible that the local municipalities and counties are the biggest winners since they will and probably already raised property taxes based on the increased house prices?

I think we’re in store for continuing thin inventory in SoCal this year (yeah really going out on a limb here). Hard to call much further out other than inventory will increase next year (nowhere to go but up). Rates likely to stay 5.5 – 8% range for a few years, prices down more noticeably in ’24-’25, maybe finding a bottom in ’26 or thereabouts. Recession in there somewhere. RE and stock markets fighting it all the way down.

History doesn’t repeat itself but it sure does rhyme. Half my neighborhood inhabitants did not get whacked in ’07-’10, they were too young with no RE and no significant financial market exposure then. They’ll get their taste soon enough.

I’ve just ran across a sales contract on a condo in the DC Swamp with VA financing which I will call the “Sales Contract from Hell”

1. The $100,000 loan includes over $10,000 in lenders fees, closing costs, underwriting fees, title ins, miscl financing costs, VA funding fee, survey, home inspection fee, appraisal fees etc.

2. The actual interest rate on the $100,000 loan are not even listed anywhere in the contract except listed as “Market Rate” whatever the f.ck that is.

3. Sales contract was 30 pages in fine print that you had trouble reading with a powerful magnifying glass.

How could any honest Realtor dupe some Veteran into signing such a piece of trash as this just to make a commission and call this a benefit to the Veteran who have served or are serving honorably in the US Military. The whole RE industry here is corrupt beyond repair.

The seller pays all closing costs, fees and appraisal costs in a sale with a VA loan.

Not sure about the remainder of the contract … you might get out the magnifying glass and take a closer look.

Josap

Total BS. What about home inspection fee, state transfer taxes, appraisal fee, loan origination fees etc. You must be a Realtor.

Who is paying the seller ?

The seller does not pay the fees. It’s the buyer who pays the fees although indirectly. Buyer pays the price for the home to the seller and then seller pays from it.

Hope you get the bigger pic.

This remnds me of real estate agent in so cal.

I wanted to buy a specific home for 1 million and asked agent if she can reimburse some commission back. $30K for few hours of agents time was too much. she said she cant because it is not ethical and sellers pay this to buyers agent,

Maybe the lender really doesn’t want to make a 100K loan?

What is the interest per year on 100K at 6%? 6K the first year and then it drops, which has to cover all of the loan servicer fees in this low unemployment environment plus legal staff, plus pay for the fees when this is rolled into an MBS…… There is high overhead in a home loan.

I have heard cases that conventional loans values have a lower limit since the fees to process and maintain them are high.

I heard this when conventional loans were at 2.5%. At 2.5%, a conventional 100K loan would only generate 2.5K/year at a peak. You couldn’t make any money at $200/month in interest and pay all of your expenses. Now at 6% and $500/month in interest, maybe it is worth rolling it into an MBS again.

Hoping someone can fill me in on the mortgage rate buy downs. As they are temporary, I am surprised they are legal. Seems subprime like. Per my understanding the spec builders are buying down the mortgage rate by 2-3 percent for 2 or so years, and then they revert. 2% down from 7% decreases mortgage by 20%. 3% down from 7% decrease it by almost 30%.

Do the buyers have to qualify to be able to pay the full mortgage amount once it reverts? Does government still buy these loans? Can’t imagine a competent bank would want to hold these. Assume if rates don’t drop by 2 -3 percent by the time the mortgage reverts it will lead to foreclosures. Also assume this is what is allowing Tol and other builders to make the the majority of their sales, and also keeping prices elevated. Is this also being used by realtors outside of the spec home market? Smells like moral hazard to me.

Who is holding these adjustable loans and what is the qualification requirement? These are essentially adjustable rate mortgages but someone is holding the loan and the risk.

Is it the US government? The US government currently holds the majority of conventional fixed rate loans now. Unlike 2008, the banks no longer hold these loans. If so, the taxpayer is in trouble.

If it is the builder, then they are accepting the risk and counting on the future rates to be lower in order to make money now.

Generally, buyers have to qualify for the mortgage based on the full rate with zero points. The 2-3 years of lower payments is really just an incentive being offered by builders, rather than just lowering their prices.

Wolf – I actually think mortgage appps would be much higher if there was any decent existing home inventory for sale! I am a frustrated buyer in norcal area and our market saw a big bump in buyer activity in /Dec/Jan. Prices are still extremely high and sticky, and home still still here very fast! No crash here other than sales transactions

Have you not read anything Wolf has been writing?

Get control over your emotions. Trust your instincts. You are FOMO’ing at the mouth. Consider this an intervention from a Wolfstreet buddy.

Yes prices are still high… but they HAVE come down. Last housing bust took 5 years to play out. Housing Busts are measured in years. We’re less than a year into it. So be patient.

Here is Sacramento County, median price down 11% from peak and down 5% yoy (data from the California Association of Realtors):

Very true. But prices have now gone up a net 35% in your graph. You can see how high they went up, as well as the recent bounce higher in DEC2022 and JAN2023. Still a long way to go down (I hope). I’m just not confident the FED is going to see this through and let prices correct very much more. Existing home sellers remain quite confident, and just are not selling, nor do they “need” to sell. Inventory is non existent. The FED is so weak and has done very little with MBS, already declaring a “disinflation victory”, etc. WOLF, in your opinion, where do you see house prices settling at in this cycle? Maybe 2020 levels at best? Other than high crime/homeless (SF Seattle) and/or large homebuilder markets (Phoenix, Vegas, Austin), I just don’t think a lot of other markets will drop that much in price after having gone up 35%-50% in the last 2 years. Thank you WOLF!!!

As long as inflation remains an issue i am sure Fed would keep hiking and tightening.

Its not not rate hike but also qt.

A lot of people said fed would never ever come this far but here are we today

There has been a paradigm shift for all asset classes in last year

The process of raising interest rates in real estate is similar to heating up popcorn in the microwave. The results take some time to deliver.

You wait a long time. Then a few pops trickle in, then a little more, then suddenly the whole bag starts rumbling with action. You try to pull it out before everything burns.

Then you die of cancer after partaking of the mess in the first place

According to the Trading Economics website chart, the U.S home price to rent ratio reached a 50 year high in 2022.

This is further evidence backing my thesis that home prices must come down, and/or rents must come up.

I just don’t see how it makes sense to be a landlord with this kind of home price:rent ratio, and risk-free T-bills yielding 5%

Thank you Wolfstreet. I just found your website few days ago. It is much better than regular news (better than constant negative news (cnn) and fox). I did not buy a home in 2020 (when I was looking), I am still living in an apartment in Northern California near Sacramento. I really hope the home prices drop by $100,000 by the end of this year so that I can buy a home. So for now, I keep living on bad rugs of this apartment and continue to save.

The last housing bust took FIVE years to play out. Houses are NOT cryptos.

Did someone unplug Engel?

Well I found something very interesting in the house hunting realm. Went way out of our footprint, where you can pick up a decent home cheap, and saw most houses empty not for sale. This is no dream place or vacation spot. I asked what happened to all the neighbors. It turns out that if you go into a nursing home, and do not have your home in a trust, it sits vacant per Medicare requirements. It’s not even allowed to be sold to family. Has anyone ever heard of this law? Could this be why we have a weird market?

Medicaid perhaps is what you’re thinking of. Medicare only covers skilled care (sub acute rehab) for a limited # of days, the details of which don’t matter in a Cliffs Note-y discussion of long term care (LTC).

The poor old duff likely has Medicaid if going into LTC, as LTC is ungodly expensive, and he must be meeting the state’s Medicaid income and asset limits for a spend down to stay on Medicaid services — this limit is basically set by the individual states. A person may be able retain certain assets, such as their modest residential home, when going into LTC under Medicaid benefit, they’ll just tell Medicaid they plan on returning to the home someday, and even with one foot in the grave and no chance they’ll leave the facility alive, they’ll retain the home in their name.

If they sell the home before they die, well, now they have $ which can punt them off Medicaid and out of LTC, so why sell to the kids?

After they pass on, things can get ugly as some states have Medicaid Estate Recovery. Medicaid can go after the estate recouping the money it spent keeping Pops in the facility, and then the house can/will be taken.

There’s much more to it, but it shows why you want to plan ahead, at least 5 years ahead. Set up a trust or shuffle things around in other ways. There are creative attorneys out there who can set you up so you can cleanly qualify for Medicaid some day and still be comfortable, and your heirs won’t get the shaft. Just don’t wait until its too late to buy green bananas to try to get your affairs in order.

As far as weird housing market, eh, I’d defer to Wolf. But from what I can see from my perch in geriatric medicine, by generation, The Greatest Gen are mostly gone or well on their way. Boomers are starting to get up there in age, but LTCs aren’t busting at the seams with them just yet.

Boomers are largely just starting to experience US geriatric healthcare for themselves in all its miserable glory. Yes they probably watched their parents in the Greatest Gen move on up, but those folks were somehow much better off in retirement (if you can believe it). The most I can deduce is they may be getting a tad desperate to pad their retirements knowing how horrible things are looking financially up ahead, and that’s why they’re going for gold with the listing prices as they downsize or whatever. But what seller of any age isn’t aiming high right now.

Wolf, Do you think that there can be any good deals in the current market? We had been looking for about a year in the Catskills area. In the specific ski town, there were never any houses below 300K. Most were significantly more. We finally found one listed from an estate sale by a non profit. They couldn’t afford to turn on the sewer, well, furnace, electric, or anything else. Nice lot in nice neighborhood. House is smaller and interior in rough shape BUT strong bones and a solid house that we can pretty easily renovate. We aren’t positive but pretty sure based on circumstances that everything will be working. They just couldn’t turn things on so the agent listed for a quick sale (we used the selling agent). Price was 127K and we were told that there were 20 other offers, one of which we reviewed ourselves (escalation clause). Agent was even hesitant to sell to us bc there were so many other offers and we were out of state, making offer site unseen. (We have since inspected the property and we love the house and neighborhood.) This just seemed like an exceptional deal despite the fact that we were aware of your warnings. Also, this house is for pleasure not income. We will be taking our RV in the summer to vacation mainly at this house but also using this as a base camp to visit other areas of NE. We aren’t ultra wealthy but we are comfortably middle income with 20 rental properties we own free and clear, purchased around 2011-2012 mostly. Maybe a couple a year or two later. Great deals though, compared to anything recent. Anyway, this is a pleasure home and our feeling was that we are only going to live so long. We are 53/60. Still, we are really hoping that we didn’t just buy a house that will only cost 50-75K in the next few years (and other houses for what we paid will be twice the size and in excellent condition, similar to 2008-2012). I know this isn’t a huge amount of money but it is a decent percentage of our cash. Do you think we’ve made a terrible mistake? Just in terms of price paid in this market but maybe with a uniquely low priced listing? Or was that wishful thinking. Realtor could be FOS but he said this house with functioning utilities and just minimal / basic renovations would be 300K.

Why sell at all? 99% of mortgages are under 6%, saving great money not paying inflated rents, and a deflated dollar will prop up asset prices eventually. Re is a traditional inflation hedge, look what happened through the 80s.

This will pass in the future and unless you’re swing trading houses, there is no pressure to sell

I’ll take a run at a little prognostication.

I’d say as the leading edge in home prices continue their declines and equity begins to evaporate, we’re going to see single family homes owned for investment become the accelerant to the declining market and prices.

The new GREY MARKET which drives real estate values will be the Blackstone’s et al. This unique PE – Corporate ownership in single family homes is going to experience first hand the horror of illiquid assets in declining markets. These entities don’t own single family homes for their habitation, when their balance sheets start to be torn to shreds and there lenders force them to mark to market for there presumptive collateral valuations it’s a feit compli.