It just keeps getting funnier with this crypto stuff. Shares crush dip buyers after hours.

By Wolf Richter for WOLF STREET.

Silvergate Capital, a small bank holding company that owns crypto bank Silvergate Bank, disclosed today after hours in an SEC filing:

- That it would restate its financial statements for 2022.

- That the shocker net loss of $1.05 billion for Q4, disclosed on January 17, would even be a bigger loss.

- That it was unable to file its annual report (10-K) by the deadline, March 1, and even after the 15-day extension, because it “requires additional time to perform analysis, record journal entries related to subsequent events and to complete management’s evaluation of internal controls over financial reporting.”

- That it sold even more securities, with even bigger losses, in order to repay its loans from the Federal Home Loan Bank of San Francisco.

- That “these additional losses will negatively impact the regulatory capital ratios” and “could result in the Company and the Bank being less than well-capitalized.”

- That it “is evaluating the impact that these subsequent events have on its ability to continue as a going concern” for the next 12 months.

- And that it “is currently in the process of reevaluating its businesses and strategies in light of the business and regulatory challenges it currently faces.”

Oh dude.

“Evaluation of internal controls over financial reporting” is not what you want to hear after you dip-bought the shares after they’d collapsed. It speaks of funny accounting and leaves everything up to your imagination.

You also don’t want to hear “will negatively impact the regulatory capital ratios,” and you never-ever want to hear “less than well-capitalized” – a key term because you can imagine that bank regulators are getting nervous and might swoop in one Friday evening and take over to “resolve” the bank.

You never-ever want to hear any kind of language from a bank about “continue as a going concern” because it shows that its auditors might see issues that would shed serious doubts on the bank’s ability to make it through the next 12 months.

You also don’t want to hear “reevaluating its businesses and strategies in light of the business and regulatory challenges it currently faces.”

These “regulatory challenges” refer to it being investigated by the Justice Department’s fraud section, according to Bloomberg earlier, and being hounded by Senator Elizabeth Warren and other lawmakers over of its relationship with FTX and Alameda Research, which collapsed amid a huge mess into bankruptcy.

Short sellers are all over it, sending letters to Silvergate’s auditors Crowe LLP and to regulators, that, according to Bloomberg, detail a laundry list of alleged misconduct, including money laundering.

If you caught Silvergate Capital [SI] on the dip, by about right now you realize that your fingers got cut off.

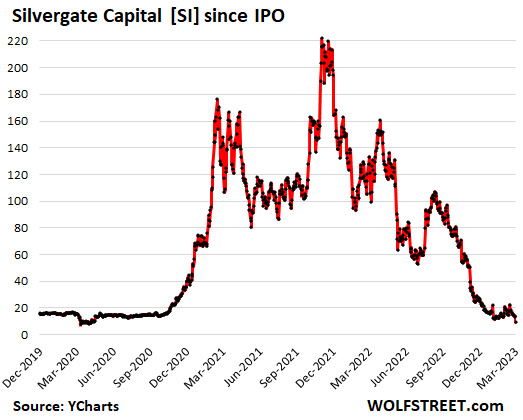

Silvergate is one of the many shining heroes in my pantheon of Imploded Stocks. In after-hours trading today, its shares plunged another 31%, to $9.24, but you can barely see today’s plunge on the chart because it has already collapsed so far. It’s down 96% from the consensual-hallucination peak in November 2021 (price data via YCharts):

Tiny Silvergate Bank became a crypto bank and then ballooned. It didn’t lend to crypto platforms, but it took their US dollar deposits, billions of dollars of them. With this cash, it bought Treasury securities and earned interest. Sounded like a low-risk approach.

But when its customers, crypto platforms such as FTX, began to collapse in the second half last year, they withdrew their deposits from Silvergate, triggering a massive bank run.

Total deposits from “digital asset customers” plunged by 68% in Q4, or by $8.1 billion, from $11.9 billion at the end of Q3 to $3.8 billion at the end of Q4, it said on January 5, when it announced the preliminary results, and we walked through the details at the time. It reported the actual results – now reduced to fake results – on January 17.

In order to be able to repay these depositors their $8.1 billion that they withdrew, it started selling Treasury securities and it borrowed in the wholesale market by selling FDIC-insured brokered CDs and by borrowing from the Federal Home Loan Bank of San Francisco (Silvergate is a California company).

The Treasury sales occurred as yields were shooting higher, and it lost money on the sales, and given that it would have to sell more Treasuries at losses, it marked to market more Treasuries it would have to sell at a loss. And now it sold even more Treasuries to pay off the loans in full that it had received from the San Francisco FHLB.

All in all, when it reported Q4 results on January 17, it said it lost over $1 billion. And those results have now been reduced to fake results, and the corrected results with bigger losses will be reported sometime in the future.

And folks back then thought that was it, that the bad news was out, and they bought the shares on the dip. And the shares nearly doubled, from $11.55 after the plunge following the first disclosure to $22.32 on February 15, along with all the other crazy stuff that doubled or tripled, the assorted penny stocks and bankruptcy equities out there. So now, this evening, they’re suddenly at $9.24.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The FED created a fictitious economy full of fake businesses, like this one. And yet I keep hearing the FED is going to pivot very soon and go back to zero interest rates and QE, like more poison is the cure for the rot that is festering, like this filthy excuse for a “business.”

The pivot story got taken out the back and shot in February. The 10-year yield is back at 4%, the average 30-year mortgage rate at 7%, stocks are skidding, bonds are skidding, housing is skidding. Folks are now seeing higher rates for longer, driven by sticky inflation. It just takes a while to sink in, interrupted by bouts of denial.

I agree with you, I am just saying that these pivoteers or whatever the hell you call them are still out barking about some miracle pivot that’s coming. They’re like Linus waiting for The Great Pumpkin.

And then I just about choked on my coffee this am as I read something that said “housing has bottomed and is now recovering.” This stuff is so absurd that it defies logic.

It’s speculation, it’s been around since the 17th Century with the Tulip bubble!

When people are flush with cash they make horrible decisions.

I don’t claim to know about the future of a “pivot” from Powell.

I just think it’s way too soon to be taking “victory laps” at this point , when nothing has broken yet. Not housing prices hugely, not unemployment, and not the stock market.

If (when?) Powell redefines the target interest rate to 3-4% when things start breaking, that will be a huge pivot in my book. (Hopefully Wolf would admit it also).

Now about those electric cars with 2% of the market , and testifying against you in court with recorded driving parameters, and no range to really take a comfortable long trip, no towing capacity, frozen batteries in the cold, etc etc etc. Hahahah

(Want to race my 2003 CRV ($3,000 blue book) from East Coast to California in a 70,000 Tesla? Have fun at the charging stations …

Depth,

I’m not going to defend the dummies who invested in various forms of garbage…but you need to reserve some obscenities for the Fed/DC which made the garbage saleable/”necessary” through 20 years of Treasury rate destruction (in the service of exactly what, in the inevitable end?)

ZIRP was put in place and kept in place (for decades) because DC absolutely and totally refused to address the deep and horrible problems the US has had with its lack of intl competitiveness (phony RE bubbles being used to obscure manufacturing collapse relative to consumption).

“If (when?) Powell redefines the target interest rate to 3-4% when things start breaking, that will be a huge pivot in my book.”

Fantasies don’t mean jack sh!t.

Mark,

LOL, you’re way behind. EV sales of new cars in the US in 2022 were 5.8%, up from 3.2% in 2021. Worldwide, sales were 10% of new vehicles. As for your other concerns, most people rarely, if ever, tow anything. Many people don’t live in climates that freeze very often, and those that do can account for the reduced range. Most trips aren’t across the country, but often families, like mine, have both a gas and electric car so it’s not an issue.

If an EV isn’t practical for you, don’t buy one. However, millions of people obviously don’t share your concerns about EVs.

Don’t be fooled. It’s actually a very well-designed and executed business, focused on the transfer of wealth from the public to the organizers.

Ohhh, so these guys are related to the people who “have a bridge they can sell you”. Gotcha Gotcha ;)

Guys,

I just figured outh the next big thing. It’s called “AI_Coin”.

It combines both AI and crypto, two of the hottest words in speculation market.

While AI is once again being touted by our tech companies and chip companies as a gamechanger, crypto is the touted replacement of central bank control on future currency. In this setup, AI will be the only regulator of “AI_coin”. Bitcoin lacked this.

Even, Wolf will agree that this can be the perfect scam. /s

Once it catches on, I would feed this AI logic to move your money to my accounts. Muhahahahahahaha!

:-) “All our Smart Contracts are written by ChatGPT!”

Fed member Bullard said wage growth to high to get 2% inflation(I mean devaluationx10)

he thought 5.4% rates now thinking 7%

The implication is that Silvergate was dishonest and I’m not so sure whether that’s true or not. Isn’t it to be determined? It appears they were trying to do the right thing by taking a loss and paying back their depositors when there was a bank run I know there is ambiguity in terms of their intent or how it played out but no one really knows exactly yet.

They’re being investigated by the Justice Department’s fraud unit, as I pointed out. That’s not an “implication” but a fact.

They’re being looked at by Lawmakers for their dealings with FTX, as I pointed out, which is also a fact.

The short sellers have detailed all kinds of alleged misdeeds, including money laundering, and have sent that info to the auditors and regulators.

So I should buy dogecoin, right? Is that what you’re saying?

If you mean, “Let it All Burn,” then yes.

???? did politicians return any of the $40,000,000 FTX gave away

Looks like a Duck, Quacks like a Duck, Must be a Duck.

Who was supposed to be the regulator for this sweetie?

Oh.

The Fed.

Mr. Powell is Not available due to a conflict of schedule. But we have this new ChatGPT hotline. You’ll always get an answer.

20-20 hindsight. No, I say, all the libertarians were in this to escape regulation. They were constantly on the prowl for touch-points into the legit financial system. Maybe regulators could have prodded a little more and earlier, but that wasn’t the source of the problem. The source of the problem was very busy and sneaky regulation haters and avoiders/evaders. The easy, cheap shot is to lay absolutely everything at the feet of Powell and the Fed, but past a point, this blurs the picture. There is always a dance between innovation and regulation.

The whole point was to circumvent the classical time-honed banking and regulatory system. It was lucrative to build hookups between that and crypto. These broke quickly and the right speculators lost their money, which is the right outcome, without cumbersome and expensive new regulatory action.

Well, ….. No.

A bank is a bank is a bank. Whether it deals in rotten tomatoes, tulip bulbs or “crypto currencies”: it’s a bank and the Fed should have regulated it. And it certainly has ties to other banks and financial institutions that make this thing a systemic risk. Let the libertarians be libertarians, but when a bank with ties to the real world goes bust, pretty soon these libertarians will come asking to be bailed out, and if they are big enough, they will be.

Powel is asleep at the wheel. And it’s too late.

Looks like maybe this “bank” made the classic mistake of accepting large deposits on an on demand liquid basis from one sector and then used the money to buy longer dated bonds and paper in an environment of raising interest rates and meanwhile the one favored sector crashes and needs their cash. And then looks like no protective hedging.

Have to wait and see and hope taxpayer’s don’t have to bail em out

This.

The bank may have engaged in actual crimes (we’ll see) but the huge losses so far seem to mainly come from the funding mismatches Rodolfo did a good job describing.

Even if a bank is keeping things very, very simple,

(taking in deposits – to pay pretty low interest on…and using those funds to invest in impossible-to-default Treasuries…those “riskless” Treasuries still see their *market value* fall as rates rise…so if forced to sell, the bank can lose a lotta money on “riskless” Treasuries)

things can go south quickly.

Borrow long, lend short: result happiness.

Borrow short, lend long: result misery.

But they all do it, based on projections, i.e. models/forecasts.

Who knew demand deposits could vanish so quickly, as in ‘nobody saw it coming?’. By ‘nobody’ is meant all the experts doing linear projections until everything falls off a cliff.

SI was described by advisors/analysts as a can’t-lose money machine in a rising-interest environment.

The bank was just fine until it decided to suddenly get big and pump up its stock price into the stratosphere (IPO in 2019) by riding up the crypto craziness by doing business with companies that are scammers and fraudsters (crypto platforms) in support of their scams and frauds. And when the scammers and fraudsters collapsed, Silvergate got what it deserved.

No, Wolf you are wrong, “Fortune Favors the Brave!” Matt Damon never would have said that if it weren’t true!

Heading to 100 billion $$$$ plus interest payments on federal debt this year while revenues are falling! Easy-money Janet is in panic mode!

This year marks the centennial of the final collapse of the old German Reichsmark. And to think that 10 years earlier, Germany was still on the gold standard. I still have a 20 milliarden (German for billions) stamp from my stamp collecting days over 60 years ago. It was my first lesson on inflation and I hadn’t even reached my tenth birthday. I wonder if Janet has even read the first few chapters of “The Rise and Fall of the Third Reich”. If she is not in a panic, then she should be.

Hey Wolf, you should do an article on the soon to collapse stablecoins, not if but when there is a bank run as their value is linked to under-water treasuries and corporate bonds like SI. Will be hilarious when those scams collapse and bring down the whole crypto ponzi scheme!

Fraud Money Laundering and Risk Controls as Wolf pointed out. Crypto in my option though not intended when created out of then air is the home for the criminal element to transfer money across the globe and now even deposit in an FDIC insured bank . I hope that any criminal element never sees their funds again . FTX had deposits at the bank. China was a crypto king for minting coins and even banned the use of crypto in their country. Freedom is wonderful but there are rules of society that have to be enforced and unfortunately i see little enforcement of the weak regulations on the financial industry we have in place today . Oh and as Wolf had said many times and I think I raise my text with all caps SOMETHING HAS BROKEN INFLATION.

These “Federal Home Loan Banks” are truly inteesting institutions, to say the least. If one looks at what they’re doing on FRED, it’s truly – interesting, especially the Timing of it.

One could spot a certain pattern there. I’m not sure whether they were created to bail out a failed Crypto Bank, but hey – whatever gets you through the night – it’s all right.

Nah. That’s related to spiking interest rates paid by money market funds, Treasuries, etc. And depositors shifted their funds from banks to those higher-paying instruments, including many commenters here. So some smaller banks, which wanted to continue to pay 0.01% on their deposits, lost deposits that shifted to money-market funds, Treasuries, brokered CDs, etc. For funding to replace those lost deposits, they borrowed from the FHLB. Some also went to the discount window, as we saw. Once they raise their deposit rates, deposits return, but that increases their costs across all deposits. So it’s cheaper for them to borrow smaller amounts from the FHLB and the discount window than having to pay ALL their depositors more.

The New York Fed published a study about that a while ago. The crypto banks are too minuscule, and there are only a couple. Silvergate paid off in full its loans from the FHLBs, as I noted in this article.

After the horse has left the barn… “JP Morgan analyst Steven Alexopoulos downgrades Silvergate Capital (NYSE:SI) from Neutral to Underweight.”

Was JP Morgan one of the underwriters when SI went public?

No, not this one. The underwriters were:

Lead book-running managers: Barclays and Keefe, Bruyette & Woods (Stifel).

Book-running managers: Sandler O’Neill + Partners, L.P. and Compass Point.

Co-managers for the offering: Galaxy Digital Advisors LLC and Performance Trust Capital Partners.

Federal Reserve/Treasury.

Speculation Nation.

Silvergate Capital IPO’s at $13/share in the Pre-Pandemic November 2019 as a regular family bank.

Somebody at Silvergate get irrationally exuberant and goes all-in with crypto in 2021 and the stock soars to $220.

Just another rags-to-riches-to-rags crypto story and the stock is now at $6.50 today.

It might be a good buy if they go back to their roots and become a regular family bank again. Unless they go bankrupt.

Thanks. I am more enlightened.

Over at Brian Romanchuk’s there was a little discussion on whether money and Treasury Bonds were exactly the same thing. In this case, evidently not. If they had been, Silvergate could have satisfied FTX’s withdrawal “Here are the Treasury Bonds your money bought. They’re yours; take them and be happy.” But no, Silvergate had to turn the bonds into money in the private market, and got slaughtered.

Argent provocateurs in trouble…

Can anybody explain why Bitcoin has actually gone up in value since the FTX downfall and other events?

Paxos is shutting down BSUD. It’s about $13 billion notional value. It’s trying to manage an orderly redemption process. They won’t redeem your BSUD if you can’t pass KYC requirements. Also they won’t redeem Binance issued wrapped BSUD. So for those that are stuck their only option is to use their BSUD to buy bitcoin, eth, or any other stuff. So bitcoin goes up. It’s not new money pouring into crypto. In the dark crypto underworld it’s all interconnected as Wolf has said many times.

Low volume moves bitcoin. I read only 4% of bitcoin actually trades. It is like a low float stock. All the rest is sitting in some ones wallet waiting for it to go up.

> why Bitcoin has actually gone up in value since the FTX downfall and other events?

Last man standing in Ponzi-land. Last venue dealing hopium.

I think the government generally hates crypto because of its anonymity and will always want to regulate it, but, as mentioned above, isn’t crypto like tulips? There’s nothing there there. Even a bankrupt company has intrinsic value, crypto only has electrons.

I just read an article:

(Kitco News) – Daleep Singh, the former deputy national security adviser for international economics in the Biden administration, has suggested that the creation of a U.S. central bank digital currency (CBDC) would “crowd out” the private cryptocurrency ecosystem and serve as a protective measure for the national security of the U.S.

Singh made the comments on Tuesday during a Senate Banking Committee hearing, taking an oppositional stance towards the nascent asset class by highlighting his view that cryptocurrencies facilitate ransomware attacks and contribute to the evasion of U.S. sanctions.

For that reason, Singh believes it would be in the best interest of the U.S. to release a digital dollar, saying it’s the “single best step that we could take [to protect the national interest] because it would crowd out the ecosystem of crypto.”

….“could result in the Company and the Bank being less than well-capitalized.”

A bit like saying the plane’s wings have sheared off, and could result in less than optimal flight characteristics.

Well, maybe not both wings. Just one wing. Involving unusual spiralling manoeuvers and whistling noises?

+1

The Federal Home Loan Banking system is going to come under immense pressure because of this from Congress. If the bank fails, the FHLB gets paid back first before the FDIC’s deposit insurance fund gets paid back.

The optics are bad for the FHLB because they have gradually strayed away from the original mission and become more of a banker’s bank.

The optics are bad for a lot of Federal institutions. Imagine a bank making a 30 year loan to someone with a poor credit history and only asking for 3% or 5% down? In effect, these were the Federal guarantors’ lending standards before the Great Recession and may well be still in effect.

Part of the story here is that Silvergate (perhaps under pressure) paid back in full its loans from the FHLB, which is why it had to sell more securities to come up with the funds to pay back the loans, which caused further losses.

Do we know whether the loans paid back at Silvergate’s peril, had unfavorable clauses or security agreements for any of the insiders or other favored folks?

Being in the recovery business for decades I used to find that in post bankruptcy analysis that at times, credit lines and loans containing ties to principals, such as personal guarantees, or personal asset security agreements, were most often paid off first.

Trick for debtor is to be sure it happens outside the preference period and does not attract attention of the creditors. Trying to prove and claw them back is a very expensive endeavor. The ‘insovlency’ is sometimes sucessful albeit still expensive for creditors already facing loss via the bankruptcy.

What sticks out from a Canadian perspective is that this Sivergate thingy is bank of some kind? It has some connection to the FDIC? Does this mean that even if indirectly, the FDIC is guaranteeing crypto ‘assets’ which consist of zeros and ones stored in a computer?

OK, two very large Canadian pension funds lost a bit of money in crypto ventures of one kind or another. Small amounts relative to their size. But they aren’t banks.

If you re-read Wolf’s article, you will notice the letters FDIC (Federal Deposit Insurance Corporation). So yes, SI is a bank and its deposits are insured by the FDIC up to certain limits. FDIC is the American version of CDIC (Canada Deposit Insurance Corporation).

“…even if indirectly, the FDIC is guaranteeing crypto ‘assets’?”

It doesn’t mean that.

The FDIC insures US dollar deposits of up to $250,000 per account type if the bank collapses.

Each of the crypto firms had large amounts of dollars on deposit there, far exceeding insurance limits, so most of their dollar deposits would NOT have been insured in the first place.

But the crypto firms when they collapsed yanked out their dollar deposits, and some that didn’t collapse yanked out their money, and in total $8 billion was yanked out in the second half of 2022. I’m not sure how much in deposits from crypto firms is left at the bank, maybe not much.

To get new funding, the bank sold regular CDs to retail savers/investors via their brokerage accounts. Those CDs are FDIC insured up to $250,000 per account, but they’re held by retail savers/investors, not crypto firms.

Even if a crypto firm still has US dollars on deposit at the bank, and the bank is taken over by the FDIC, the FDIC only guarantees the first $250,000. In other words the crypto firm will get back $250,000 of its own dollar cash deposits at the bank, and the remainder of its dollar cash deposits is lost. So that FDIC doesn’t back any kind of crypto assets, not even indirectly. It’s backing US dollar cash deposits.

Got it. Thanks

I view this as a warning sign for people who have bank accounts or CDs with Silvergate.

If you only have one bank that you work with and your entire life savings of greater than 250K are deposited with Silvergate, you are in extreme danger.

As Wolf pointed out, FDIC insures up to $250K. If your life savings are beyond this deposited at Silvergate, you need to rebalance elsewhere to a more secure bank. Or, invest in US Treasuries.

The problem with FDIC insurance is that it is only used if a bank fails. FDIC can bail out the depositors up to 250K. It has worked well in the past. If you are unlucky/greedy and have deposits in multiple failing banks due to unrealistic interest rates over 250K, you will likely lose.

If Armageddon ever happens and ALL of the banks fail, the FDIC will be overwhelmed and you will lose on deposits. Definitely if you have over 250K in bank accounts. US Treasuries, IMHO, will be the last to fall.

If the full faith in the US government fails, we are all in big trouble. Bank accounts, CDs, Treasuries, pensions, US corporate bonds, and US stocks will all plummet.

This would be a QAnon scenario. Not likely and I wouldn’t bet on it other than have a well-stocked pantry. I like midnight snacks.

As a side note those financial biz-blab lines are also great for dating:

Sorry can’t meet you for dinner I’m “less than well-capitalized”

Well Susan I’m “evaluating the impact that these subsequent events have on my ability to continue as a going concern”

Wow. Nicely done.

Interesting action with the stock, as so often happens when the dreaded “going concern” language appears. Massive drop, followed by eager bargain hunting, before swirling ever lower.

Also watching CREDIT SUISEE saga in real time

i dont understand why bitcoin is still work 23K each. the core concept of digital currency that could eliminate the hegemony of banks on currency is a good one, but bitcoin has so many problems in actually becoming a core part of everyday commerce.

Money laundering

Your graphic of the price of Silvergate since it’s IPO is worthy of being an exhibit of the power of monetary policy to juice the economy when necessary. Which begs the question; why are they having so much trouble in reversing said policies.

The picture that comes too my mind is a portrait that questions one of the foundational rock firmament that underlies the basis of economic and it’s cousin finance which is the concept of “imagine a rational consumer”.

For crying out loud, the portrait reflects an inherent animal spirit, in this case, the bull. Anyone who has seen a video of the Pamplona bull run will understand the essence of what that means.

Would I even have ever known of the event had not Hemingway captivated the world with his lurid descriptions of reality.

The other animal spirit is represented by the bear. In particular, the grizzly bear who live up to their representation and a lot worse.

An alternative view occurred to me that the world has been engaged in a currency war in which currency issuance was practiced to support imports into the US, making American exports more expensive.

A domino chain of stupidity or genius promoting a new economics, zero interest rate policy made possible by a program called quantitative easing, QE, available to all countries with a sovereign currency.

The honest diagnosis of the economic and political conditions that led to such an absurd course of action in the first place is not a pretty tale.

What was the objective, assuming their was no reasonable purpose to veer so violently from an established system of rigorous financial statements into an era of grift in which the financial statements no longer accurately represent the financial condition of the firm issuing the statements. Audited statements are better than unaudited, although the chasm has closed rapidly and sometimes seems like a gap between being a clueless dumbshit and an organized pain that gets swindled.

It’s not as if the Fed hasn’t been an organization of fools making terrible decisions about monetary policy for most of it’s existence. In fact, it’s pretty hard to find an instance when they weren’t doing opposite which eventually needed to be done.

I recommend they start right now and talk about terminal interest rates above the rate of inflation, which would currently be between 6 and 7 pct or more.

I must be very old. I’ve seen quite a few comments and articles about Crypto’s “settlement speed” but I think I must be missing some major point.

Other than international financial transaction settlements, for the man on the street, is there really a “speed” problem? I keep thinking of me ordering stuff on line with my CC and it never has a delay, and I pay it off monthly.

Must be missing something.