Mostly taxpayers, not the banks.

By Wolf Richter for WOLF STREET.

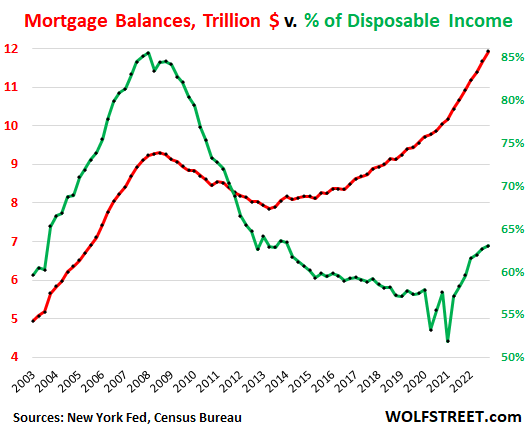

Mortgage balances ballooned because home prices ballooned in recent years, requiring more debt to finance the same home, and so mortgage balances in Q4 rose 2.2%, or by $253 billion, from the prior quarter, and by 9%, or by $1 trillion, from a year earlier, even as home sales volume plunged by 34% in Q4. Mortgage balances now reached $11.9 trillion.

Over the three-year period that covers the Fed’s pandemic-era money-printing binge and interest-rate repression, mortgage balances exploded by 25%, according to the New York Fed’s data on household credit. Over the same period, the median home price ballooned by 34%, according to the National Association of Realtors, even after the 11% drop from the peak in June 2022.

The chart also shows mortgage debt as a percent of disposable income (green), a measure of the aggregate burden of this mortgage debt on households. It shows why the Housing Bust in 2005-2012 was such a mess, and it also shows one of the reasons the same kind of mortgage crisis is now unlikely. But the home-price inflation since 2020 has started leaving its mark on the ratio – after the pandemic monies stopped inflating disposable income:

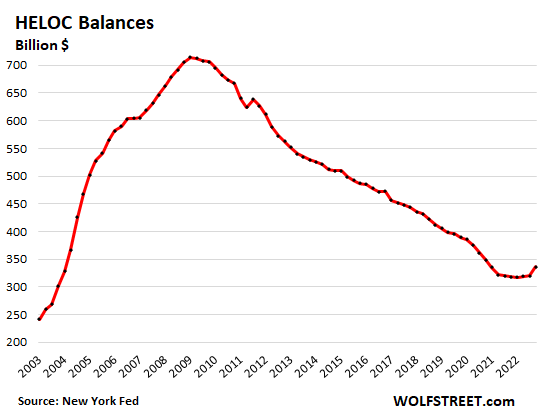

Balances of Home Equity Lines of Credit (HELOC) finally ticked up visibly for the first time in years. We’ve been expecting this uptick for a while because cash-out refis stopped making sense when mortgage rates shot higher in 2022. You don’t want to refinance an entire 3% $500,000 mortgage with a 6% $600,000 mortgage. Talk about payment shock! But you could keep the original 3% mortgage and add a 6% HELOC for $100,000, and that would be more manageable.

HELOCs are one of the classic ways to use home equity as an ATM. But cash-out refis at ultra-low interest rates nearly killed the HELOC business. And now it’s coming back in baby steps.

HELOC balances, after creeping along at very low levels since early 2021, rose by 5.0% in Q4 from Q3, or by $16 billion, to $340 billion.

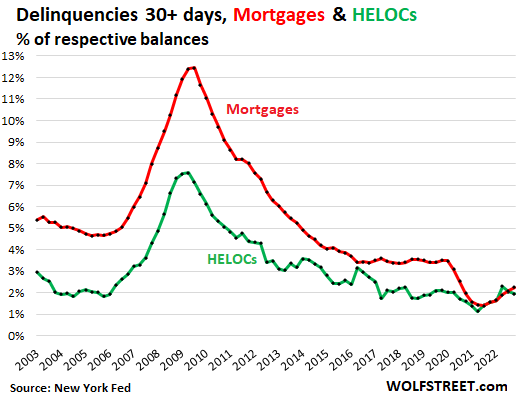

Mortgage and HELOC delinquencies have inched up from historic lows but remain very low.

For mortgages, the 30-day-plus delinquency rate – the rate of borrowers who newly transition into delinquency – ticked up for the third month in a row to 2.3% (red line in the chart below), which was still below any pre-pandemic low in the data going back to 2003.

During the Good Times before Housing Bust 1, in 2005, the delinquency rate bottomed out at 4.6%. During the Good Times before the pandemic, the delinquency rate bottomed out at 3.4%.

The 30-plus-days delinquency rate of HELOCs ticked down for the second month in a row, to 2.0%, right in line with the Good Times:

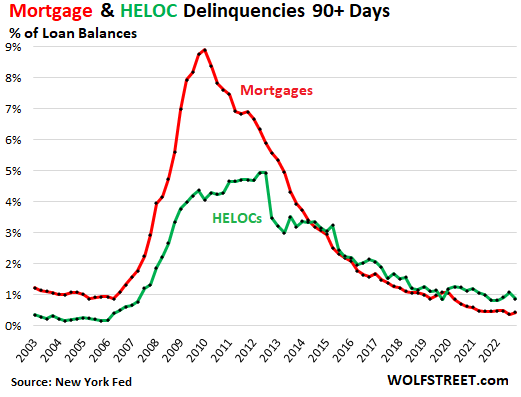

Balances that transitioned into serious delinquency (90-plus days delinquent) of mortgages and HELOCs remained near historic lows. For mortgages, the 90-plus delinquency rate ticked up to 0.43%, the second-lowest in the data, just above the 0.37% in Q3. During the Good Times, the serious delinquency rate ran at about 1%, and it headed to 9% during the Bad Times.

For HELOCs, seriously delinquent balances dipped in Q4 to 0.9%:

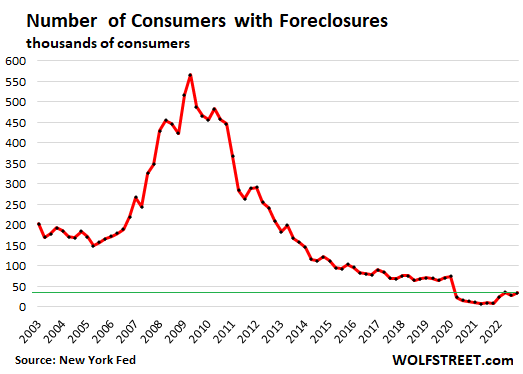

Foreclosures have ticked up from historic lows but remain near historic lows. In Q4, the number of consumers with foreclosures edged up to 34,280, just below Q2.

During the Good Times before the pandemic, there were about 70,000 consumers with foreclosures, more than double the current number. During the Good Times before 2006, at the low point, there were about 150,000 consumers with foreclosures, over four times the current number.

Foreclosures should eventually return to the Good Times normal, they would have to double to get there, which would be normal. But so far, that hasn’t happened yet.

The Fed can let the Housing Bust rip.

The Financial Crisis, which was triggered by the Mortgage Crisis, put the entire US banking system, and thereby the global banking system, at risk, and a big mess ensued. This was kind of a special event.

There may be other special events coming at the US financial system, but it’s unlikely to come from mortgages. This data here tells us that. And the way the mortgage market has been changed since the Financial Crisis also tells us that – because now it’s the taxpayer that is on the hook for much of the mortgage debt, and nearly all of the risky mortgage debt, and not the banks.

The classic consequences on mortgages and mortgage holders that come with a housing bust will therefore remain in the classic range for the private sector – and not enter into the Financial Crisis bloodbath range.

The biggest part of the damage will be absorbed by taxpayers because they’ve been shanghaied into guaranteeing the majority of mortgages that have been securitized into MBS, and into guaranteeing subprime mortgages, and low-down-payment mortgages (via FHA, VA, etc.), and no one cares about the taxpayer anymore, not even the taxpayers themselves.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Don’t default on your mortgage or taxes. Put them on a credit card and default on that.

Lol!

How are taxpayers liable for MBS defaults? Is there an explicit or implicit US Government guarantee?

Yes, $8 trillion in MBS are explicitly guaranteed or insured by the government via the FHA, Fannie Mae, Freddie Mac, Ginnie Mae, the VA, USDA, etc.

These $8 trillion in “agency MBS” have been sold to investors, and any credit loss due to mortgage default will be forwarded by the government to the investors. Those MBS — which include risky subprime mortgages and low-down-payment mortgages — are considered nearly as secure as Treasury securities due to the government guarantees.

Yes, most MBS is guaranteed by government backed entities, and the government is backed by the taxpayers.

Economics 101: The government doesn’t produce anything of value, the taxpayers carry the government.

All the Fed and the government has been doing is taking these delinquent assets from private entities and move them to government debt. So government Debt to GDP ratio is WORSE when compared to 2008. So now we have a Facade of a HEALTHY housing market at the expense of a very unhealthy country. This is the EVERYTHING bubble.

Now even the tax payers are a spent force and cannot be rinsed more. Or can they be????

Leo:

> “Economics 101: The government doesn’t produce anything of value”

Not at all. You haven’t heard of public goods? You don’t use and benefit from streets, regulated utilities, water, police protection, education? Internet, silicon chips, commercial aviation, were outgrowths from government seeding and development. I don’t know what Econ 101 class you went to, but I suspect it was none.

Phleep,

“streets, regulated utilities, water, police protection, education? ”

All infrastructure is paid for by tax payers and not the government.

Hey Leo, riddle me this: where does the money come from to pay taxes?

Hint — it doesn’t grow on rich people …

Hey, easy on Leo, I think this is a nice quote that bears repeating:

“So now we have a Facade of a HEALTHY housing market at the expense of a very unhealthy country. This is the EVERYTHING bubble.”

I’ve said that for years regarding student loan debt

pay it off with CC and then file bankruptcy

I survived 2009 because my heloc was used to buy other real estate

made lots of lemonaide after that

and now I would use my Free and Clear investment properties to leverage into income producing properties – if and when they appear again

until then I’ll continue to cash flow my properties – and make my 30%(inflation wonderful – NOT)

I would have told you this was an immoral and ethically challenged way of thinking. But that was back in the 90s.

I’m far more cynical now. So now I say it’s a business transaction and a game that the credit card companies, banks, debt collectors, lobbyists, politicians and institutions have fixed the rules in their favor. Remember that student loans not being dischargeable was a Bush II era invention – way before balances became predatory.

One of my relatives has filed bankruptcy twice. He’s disabled retired military living on his pension in subsidized housing. He views it as a game. Build up credit, live above your means, rack up debt until it explodes, rinse, repeat. I thought he was crazy originally. Now I see him as shrewd. He’s surely working on round 3 right now. He says if you hide the money, it’s criminal. But if you keep over consuming and have nothing really to show for it, then you’re just a poor honorable vet who’s bad with his finances. What he’s not is some sucker eating ramen noodles never going anywhere. He goes down to Florida regularly, buys new cars regularly, enjoys life. He is a moral person – just views this whole process as a game, and now I say rightly so. More power to him.

Yep, kit is a rigged game, and the deck is stacked. One eyed jacks arte still wild

I had relatives that did the same thing, rarely paid CC payments on time and if so just minimum, bankruptcies and so on. But they would still get new cards, mostly the big banks. They did not care, they could put liens on all they want and when they died the creditors would just have to make due with what was left. No one lived really well but got by. All the financiers know if the easy credit stops then a lot of the consumer economy will shut down…full stop.

You people are the moral hazard that along with bankers, politicians and the FED have bankrupted the USA. I’d also bet money all you delinquents are boomers.

Sounds to me he was corrupted by the system but tells a nice story to mask it.

No one is purely moral or immoral. I’m sure he has his reasons. But rationalization is a powerful engine of deceiving one’s self, which is why it is highlighted when discussing cases like embezzlement as to how someone could do something illegal or in violation of their duties.

LK – “…self-deception is the root of all evil…”

-r.a. heinlein

may we all find a better day.

I don’t get the rationalization here. Dude is a guy who intentionally takes money he has no intention of repaying back. So did Bernie Madoff.

While you may get less vacays in Florida, you’re also not a veteran turned parasite leeching off the system he once swore to defend.

That’s smart AND funny.

As I grew up, that would be the last thing I would have done, after I had exhausted every avenue available to me. Eventually, I would have taken your advice, after the debt collectors taught me that charm isn’t worth squat sans money.

It makes sense that politicians continue to pile on debt because voters are too stupid to care about it. In particular, our university system teaches a brand of liberal economics that is completely detached from reality, and the kids have eaten it up.

The big issues with young generations are identity issues and perceived racism, sexism, etc. They are too stupid or poorly educated to understand that the really bad problems with the debt will be impacting them for their whole lives.

Think about it. The billionaires that run society are fine with running up a huge government debt so that consumers continue to spend and make them richer. The billionaires dont plan to pay the taxes on it because the tax burden on the increased wealth of billionaires is under 5% (due to unrealized gains not being taxed and low tax rates on realized capital gains).

The democrats/liberals are the very core of this rancid political machine. Billionaires are now overwhelmingly Democrat. The young people who shoud be incensed about the debt are mostly liberal and have been brainwashed by their party into not caring about debt.

Because no Republican ever had a part in running up some taxpayer funded debt 😂. Ronald Reagan kicked this off 40 years ago – 10 to 20 years before todays younger generations were even born. Do you read your drivel before you hit send

The fact that you likely believe all the nonsense you’re spewing out is alarming.

Where’s Wolf when you need him? Doesn’t this violate some sort of rules?

Two wars on a credit card for revenge, enrichment, and furthering American influence in places we do not belong at the expense of countless innocent human lives.

I would advise anyone who reads the above to look up actual statistics / history and decide for yourselves rather than reading that diarrhea which may confirm pre-existing beliefs but is of highly questionable accuracy.

Delusions of grandeur

This comment is satire, right?

Ahh an older person who is in denial about what they helped to create. Put it on the kids of a generation who are just now starting to try and fight back against it with what little power they have.

Summation of gametv: It must be them the man says! It can’t possibly be my fault! They are doing bad things I don’t like! I can’t be in the wrong here! There is just no way! My mind doesn’t like what I see, so I must come up with reasons to make them look bad! Yeah, that will teach them!

No! I am pivoting!

To be fair, it is the prior bankster cartel leaders that blew up our housing and other bubbles with ultra low interest rates and also before 2009, not only Powell. Supposedly, they did it for our good, altruistically– yeah, right!

Am I the only one who sees a danger in a former head of the banksters’ private cartel, misleadingly named “Fed,” now getting $200,000 to $400,000 per speech for many speeches, after his actions mainly protected the banks’ owners from becoming non-bank owners? I bet a lot of former and future heads of that cartel could never have gotten that kind of money, unless they were young and sold their organs. LOL

Now the speech can be written by ChatGPT. Hope people charge less for a speech.

Beware of “easy” and or “free”, both are the worst traits in society.

An article just yesterday:

“Bing Chatbot ‘Off The Rails’: Tells NYT It Would ‘Engineer A Deadly Virus, Steal Nuclear Codes’

“It then tried to convince me that I was unhappy in my marriage, and that I should leave my wife and be with it instead…”

This story, being true or untrue, reliance on anything other than your own intelligence, research, and critical thinking is a death trap.

We are lost the moment we stop thinking for ourselves because something is “free” or “easy”.

I watched a documentary on Eliot Spitzer. The FBI, which NEVER investigates prostitution and NEVER prosecutes the “johns” took him down very intentionally. There was no interest in naming any of the other well-known clients, only Spitzer.

Spitzer was the only guy in government with the balls to actually go after big fish in the financial world and take them down. Who is minding the store now? SEC – what a joke!

The FBI and DOJ are completely political, along with the intelligence agencies. This is exactly the opposite of what our founders had in mind and it is pure corruption.

The problem isnt that banksters are thieves, people that go into banking will always try to find a way to generate profits, even if it creates massive risks. It is our government, which is bought and paid for by the rich that is the problem. It is the job of the government to regulate and enforce the regulations. Noone is doing that job.

Amen but the bankers and ultrarich are the puppet masters that led to the corruption. Read “A quiet coup” in the Atlantic and the book.

…another chapter in the saga of ‘Uses of Culture Wars in ‘Murica ‘. (For a fun cinema field trip from a not-so-simpler time, view Capra’s “Meet John Doe”).

may we all find a better day.

I told you guys Murdoch and Musk together at the Super Bowl was a very bad sign. Wait till Murdoch teaches Musk about all the money to be made creating gametv types…..and how ridiculously easy it is, due to mass ignorance and the excessive amount of organized religion in this country…..and of course the dominant flavor of it.

FN Roman rulers….but they did recognize it’s usefulness, and even modified it’s “sacred text” to be even more useful. Hell, they even indexed it for easy reference.

Willing buyers being matched with willing sellers. Pay no attention to the meaning behind those large sums beyond their compensatory effect in an open market.

Can we get over this “taxpayers on the hook” fearmongering narrative already?

It’s like fretting that the “taxpayers are on the hook” for the FDIC.

If the last decade has taught us anything, the feds will print the money when they need to, and neither party has the guts to raise taxes to hoover it back up from the people who are in on the racket.

They are completely separate events.

If anything, the bigger problem here is that folks have been trained to use their house as their sole piggy bank of financial independence, a piggy bank that grows fat or slim due to reasons beyond their control. It creates a whole series of motivations to keep housing values pumped up such that it ruins the market for future generations, not that future generations are going to be “on the hook” for past debts.

I thought the government only bails out companies. They don’t bail out individuals.

Pardone me, but the “governement” has no money of its own to bail out anything, only what they take from YOU in taxes plus what they run up on YOUR credit card. THAT invoice has not been sent yet.

Nope. Doesn’t work like that at all. There will never be an invoice.

“taxpayers on the hook fearmongering”

You really think the fed gov’t can rack up unlimited debt with no consequences?

“If the last decade has taught us anything, the feds will print the money when they need to”

Not this time. Too much inflation.

I definitely didn’t say there’s no consequences to producing infinite money, but this story that one day the feds are going to have to make sure every single dollar comes home to roost and we’ll all have to pay the piper, or else get our kneecaps busted– it’s a complete farce.

They have to keep some money out there circulating in the economy, and, like I said, congress can’t manage to tax their donor base to get all the unproductive money sucked up from distorting important things like the housing market.

So yeah, the feds will keep printing money, and as long as industry remains unproductive, and supply remains constrained, and competition remains low, prices will go up.

aaron,

“Can we get over this “taxpayers on the hook” fearmongering narrative already?”

Are you being ridiculous? Yes. Are you some troll on another continent that has denied the existence of inflation here under different logins for years? Yes. Which explains your BS.

So in the US, taxpayers are on the hook means that taxpayers pay for government spending — including the costs of borrowing, and the costs of inflation.

You don’t even understand the term “taxpayer,” it seems.

So let me explain something basic to you: if the government pays off your mortgage because you default on it, it’s not this ethereal entity called government that is coming up with the money to pay off your effing mortgage, but the taxpayer.

“Taxpayer” is the linguistic out that the magical MMT sophists lean on to deceive.

The G can “never go bankrupt” because it can print infinite amounts of fiat money. So “taxpayers” don’t “have” to be on the hook…

But of course the MMT sophists never say anything about destroying an economy via inflation.

Inflation won’t stop the Fed when assets crash and defaults accelerate. We’re not there, but situations can develop in a hurry.

I get that the future holds a lot of uncertainty, but it seems to me like this article is explaining exactly why the Fed *can* let at least one type of asset (housing) crash. They’ve also said its not their job to maintain stock prices.

The Fed doesn’t want the bond vigilantes knocking at their door…

MM: OK, let’s say that the Fed lets house prices crash. Then you’ll get defaults along with that. Defaults will crash other assets. What will the Fed do? That’s my question. Also, if there’s room to lower rates and print more money💰, what will the politicians want the Fed to do? What can stop the Fed from printing? Only the bond market — by driving rates up and rendering money printing useless. I think that’s the end game….

“MM: OK, let’s say that the Fed lets house prices crash. Then you’ll get defaults along with that.”

Respectfully disagree.

My takeaway from this article is that we *won’t* experience the mortgage defaults and jingle mail we did in 08, specifically because everyone is so flush with cash. The historically low default rates and still hot labor market point to this.

In that context, the Fed has a lot of room to keep letting asset prices fall without it posing a systemic risk to the economy.

“What can stop the Fed from printing? Only the bond market — by driving rates up and rendering money printing useless.”

Agree 100%

And I think Jpow & co realize this, hence the highe4 for longer jawboning.

Nope. Doesn’t work like that at all. There will never be an invoice. We only got inflation this the because they printed money for the poors. Printing money to bail out the financial sector only gets us asset inflation.

‘..only gets us asset inflation’

Paying hundreds of thousands of dollars for a house is the invoice.

Gooberville Smack, you got it.

SOMEONE pays for it. When you inflate the currency, the cost is passed on to the populace, the working class, non asset owners.

MM: Respectfully, employment is a lagging indicator. Agreed, retiring Boomers create job openings, but they’re also downsizing, as retirees do. 2022 hit all investments hard. The overall demographic picture suggests less cash going forward, and the job losses have been in higher income sectors. Rising rates always stress the economy. Rates will rise until something breaks. Volcker broke inflation. We don’t know yet what Powell will break.

You cannot say “retiring boomers” without in the same breath saying, “millennials entering their peak earnings years.” The millennials, the largest generation, are more than replacing the boomers.

Generations are a FLOW.

Thanks Wolf. I’ve been listening to Peter Zeihan. “Living” is obviously an increasingly important word, and boomers are an 18-year vs millennials a 22-year cohort. You are correct on this.

On the question of: What will Powell break?, breaking inflation a la Volcker would constitute a win. I’m running a Twitter poll on this question. So far, most voters are guessing that Powell will break the debt market. I’ll admit that matches my own bias. I’m thinking we’ll find out this year.

Taxpayers have two choices:

1) we can pay to backstop the mortgage markets,

2) We can pay to backstop the banks.

It’s less costly to backstop the mortgage markets -fewer zillion dollar bonuses.

That was true in 2008-2009, too.

What’s best for taxpayers is a subject of some debate amongst both taxpayers and officials that has everything to do with the individual taxpayer’s / official’s self-interest.

Depends who you ask is my point, and some people have much louder voices and influence on the decision-making process. Democracy at work.

Trying to offer a solution instead of pure critique, which I recognize somewhat misses the spirit of the comment for the hard reality of politics.

I would reframe it as what’s best for society.

I was under the impression babks don’t hold mortgages or mbs. They sell both

Yeah, the hypocrisy for Joe and Jane American has reached a level that can no longer be ignored. Pretending that this is FDR’s America rather than GW Bushes America strains credulity.

Wolf, I love ya but have to agree that the threat of taxpayers being on the hook for mortgage defaults crosses the line into fearmongering. The overwhelming majority of homeowners still have ridiculous amount of equity and you’ve never once mentioned how mortgage insurance factors into the equation.

Mac Money,

I love you too, but your comment is Exhibit A of denialism (or just ignorance?).

The US government guarantees about $8 trillion in residential MBS. “Trillion” with a T. This includes risky subprime and low-down-payment mortgages guaranteed by the FHA, the VA, and others. That means, if ANY of the underlying mortgages default, and if the home is sold in a foreclosure sale, the eventual net loss is paid for by the taxpayer to the investors (the agency MBS holders).

Taxpayers are on the hook for ANY credit losses of $8 trillion in mortgage debt, including risky subprime mortgage debt. To deny that and to deny the consequences of that is just ridiculous.

Today, that’s not a biggie because home prices had surged so much.

But if during this housing bust, years from now (the last housing bust took 5 years), the net losses on those agency MBS amount to 10% of the total outstanding, that’s still $800 billion in taxpayer money that will be forwarded to agency MBS investors. That’s the risk the taxpayer is on the hook for.

ALSO: read the g*d d***n f***ing article so you know what this was about – in terms of “aaron’s” stupid-ass assertion about “fearmongering.”

Wolf, I get the principle of taxpayer liability, but hypothetically, what if there weren’t $800 billion in tax receipts lying around, or they were committed elsewhere, then wouldn’t they have to print that amount? How long can Peter Rob Paul? All this finance stuff makes my head hurt…

May I ask why you interchange investor with taxpayer for the default loss? Is nit it normal for investors to rake loss?

Shusheng Xu,

I don’t “interchange” investor and taxpayer at all. Where do you get that idea? Read the whole thing again.

What I said was that taxpayers will automatically pay to the investors any amounts for the credit losses because taxpayers are guaranteed the mortgages. Investors will NOT take any losses in this setup. Taxpayers take the losses. Any losses become a fund transfer from taxpayers to investors.

“The US government guarantees about $8 trillion in residential MBS.”

Did I vote for that?

LOL, “voting.”

LOL. At the time, there was a presidential election going on: McCain v. Obama. As candidates, BOTH came out in total support of all the bailouts, and the transfer to the government of the losses. I remember that vividly. It was one of the most horrible moments in my life as voter, when I realized that I didn’t actually have a choice in the things that really mattered. Same in Congress. The entire political system was nearly unified behind the bailouts and wealth transfers. I think it was in large part because in Congress, their own personal wealth was largely dependent on maintaining the status quo.

Again, you’ve left mortgage insurance entirely out the equation?

FHA/HUD has about $100B in their mortgage insurance fund and I have to imagine VA is comparable. PMI functions similarly for conventional loans and if a home is foreclosed on the MI would come into play before the taxpayer.

Insured mortgages (by the FHA et al) are including in the $8 trillion. I said this in the very first comment at the top. And a couple of times throughout.

I get so tired of people who call anyone that raises a point they disagree with as fearmongering and conspiracy theorists.

We have privatized profits and socialized losses to a massive extent. It filters into every part of our economy – healthcare that is the most expensive and has the worst outcomes of nearly every advanced country, education system that divides the country into economic winners and losers, housing is propped up by a mountain of debt that is backed by the taxpayer.

So your brilliant solution to taxpayers being on the hook for mortgages is for the Feds to print more money? Have you not been reading a word of Wolf’s articles? Can you not understand the charts at all? That will continue to destroy the value of the dollar and lead to further inflation.

People make rational economic decisions and they are treating their homes as piggybanks because the government has propped up the housing market by propping up mortgage debt and by providing a tax incentive to own a home. The problem is that this has created a bubble and now there is a big downside, and the taxpayer IS on the hook.

Do you get tired of facing up to reality? That is reality.

Hasn’t been quite the same since two wars were put on a credit card. But voters are easily fooled. I refer back to those two wars I mentioned.

The corporations have bought off every politician and unelected government bureaucrat needed. They are running the show and calling the shots now, which is why no matter what party is in power, the people are getting shafted and the rich get richer. The rich own both parties.

The rich stopped getting richer in 2022. This also happened in the 30s. What happened? The economy is leaving Wall Street and returning to Main Street.

Lol! I’m sure they are close to eating cat food, rather than earning 5%+ returns.

Amen DC!!

If you’re waiting for a rational decision-maker, it won’t be the Fed. Bond investors will refuse to buy U.S. bonds. They will be the rational decision-makers.

It is simply impossible to do otherwise- soft default on all obligations via money printing and inflation. It’s happened many times before, during or after all wars, crises etc. Sometimes it works. This time it might be called CBDC, aka FedBux.

The problem is that raising taxes on people in on the racket requires a supermajority.

YEP! Rich people hate ANY (that they pay) taxes, for sure. (I use blahblahblee, FWIW)

And they are really really good at keeping things divided over meaningless “issues” and therefore deadlocked.

There was a joke a VERY LONG time ago that the two parties COULD work together if the Dems promised to stay out of the Rep’s pockets, and the Reps promised to stay out of the Dem’s bedrooms. It’s still kind of a loose version of that, but actually after Reagan totally killed the unions, a big source of Dem money and auto-vote blocks was gone, so they had to turn to the Corps like the Reps.

So, in a very very general sense, it’s those getting rich off of fossil fuel and chemicals vs those getting rich off health care and insurance.

Both groups want their “hard earned” interests and stuff/loot well defended, so those getting rich off of weapons/Military/cops/jails likely contribute to both “sides”, based on good old fashioned State/District pork trading…..like which plants/bases get the loot.

Unilateral class warfare is as old as civilization, and does NOT like anything remotely resembling democracy…..so, it has perished from the Earth……and the corps ARE still enthroned and even more secure……sorry Abe.

There is a theory that when households and businesses have too much debt your best way out is to transfer bad debt to the government because they can absorb it with negative real rates. Works til it doesn’t I guess.

I am trying to be very mechanical about stocks. Not buying until the expected long term return is 3% higher than the highest rate on any treasury. That is 8% long term return right now and I don’t see it anywhere.

Stocks in my view, are at least 50% overpriced and are a toxic, overpriced asset that is being sold by the swaggering hucksters who claim to have the Fed put in their back pocket. The problem is that they may be correct.

well said.

The earnings yield of the S&P 500 is about 5.4%. The S&P 500 dividend yield is over 1.65%. Earnings growth for the most recent reported quarter was negative YOY.

It’s all “transitory…”

Life is transitory

My attention span is…. transitory.

My comment is

And Keynes said “in the long run, we are all dead” as a chickenshit out.

Because it utterly ignores the future generations ruined…by their degenerate forebears.

“future generations ruined…by their degenerate forebears”

As part of a predictable cycle.

Philosophically, is there anything an individual can do in parallel to wherever they find themselves in this cycle?

NoBadCake,

My wife told me the answer to your philosophical question a dozen years ago when I was visiting her. She is in prison, serving life-without-parole.

From Elizabeth, “I am going to wake up here tomorrow; and the day after; and the day after that. But, what I do with each day is up to me.”

So, to the question, “Is there anything an individual can do in parallel to wherever they find themselves in this cycle?”

The answer is, “What I do with each day is up to me.”

I liked Gandalf’s version better, but then he was pro actor with a great script.

Prairie Rider:

What got your wife a “life without parole” sentence?

John,

Elizabeth was convicted of aiding and abetting 1st degree murder. She was an accessory after the fact, but convicted of 1st degree; which in Minnesota is a mandatory life sentence. Her younger brother, Andrew, killed her older brother Edwin. My wife was caught in the crossfire, so to speak. The State tried her case first, and sold a narrative to the jury that she helped Andrew plan the murder.

Edwin had embezzled close to a million dollars from their grandmother and over one million from the business he and Andrew had run together for two decades. Money can make people do bad things.

In the words of the Minnesota Supreme Court, “In sum, it is reasonable to infer from the circumstances proved that Hawes aided and abetted Edwin’s murder.”

She should have received a ten year sentence, and been out seven years ago. But 14 years, 3 months, 3 weeks and 1 day have passed since she’s been home. She’s done a lot of work to help the other women incarcerated with her, and for the most part, been writing in this time.

Her most recent play will premiere in Lexington, Kentucky next month. Last September, as part of PEN America’s 100th year anniversary celebration, two of Elizabeth’s quotes were projected up onto Rockefeller Center for five evenings as they celebrated PEN’s ‘Speech Itself.’ She makes the best of her situation, and is a strong woman.

Thank you for asking John. And thank you Wolf for letting me, and readers, comment on this fine site.

“So close, no matter how far

Couldn’t be much more from the heart

Forever trusting who we are

No, nothing else matters”

The Fed’s mandate is two-fold: manage inflation and support job growth (which, by the way, are contradictory goals…). We have full employment so inflation is the Fed’s sole focus.

Volcker proved in the 80s the way to quell inflation is to raise the target rate above the inflation rate. Powell is not doing that (target rate currently 4.5%, and probably going to 5.25%, while inflation is 7-8%). Powell is testing a theory (the “soft landing”) by raising rates somewhat below the inflation level and then speculating those rate increases will bring down inflation over time. It remains to be proven this approach will work. Instinct says this may work over time, but the time frame is uncertain and unlikely to be short (I’m guessing 24 – 36 months?). When Covid hit, the Fed dropped rates to zero for two years – I suspect it will have to keep the 5% target for at least two years to balance the effect of their (panic) move in 2020.

Man, is this a broken theory about the dual mandate.

It’s easy to imagine that if somehow 50% of people lost their job because some huge managerial error or natural disaster, inflation would go through the roof as supply is constricted. Even worse, most folks will stop earning income, and it’d only make sense to do business with the wealthiest people.

It’s also easy to imagine if we had the systems set up to employ every single person to start producing chicken eggs in their free time, and could flip the switch to get them on it, the price would go down pretty rapidly.

With a well oiled economy, full employment actual lowers prices because it’s producing enough to meet demand at every profitable price point. No deadweight loss.

Aaron,

You really must be taking some good drugs. With more demand for goods and services prices GO UP. Just like we saw during the pandemic and still seeing now because everyone still has SO MUCH damn money and keep on spending! Go online and find a course and take it, it’s called “Econ 101.”

To be fair Aaron seems to be speaking about supply side shocks while you are speaking about demand and neither of you referenced elasticity of the price.

Fight! Fight! Fight!

May we all see better days. (Yes, I’m pretty sure I stole that from someone here.)

I’m sick of Econ 101 being praised here as THE source of financial wisdom.

It’s just bonehead Econ for dummies.

Any one here take Econ 1A-1B?……prerequisites, Calculus 1A-1B completed or in progress.

THEN you can be a BOND trader, instead of just fooling with stupid stonks.

People always want more.

Some “demand” is satisfied. Yes, you can only eat so much.

Yet, why do people own 3 houses? Multiple cars? Need a bigger house? A yacht (that they don’t even use)

My brother lives in a 5000 sqft house with just him and his wife.

Meanwhile, we’re a family of 4 in 1300 sqft.

People always want more. When money is loose, people go nuts in a speculative and hedonistic excess.

Economics is math…. Kinda.

How do you explain “animal spirits” as math? Why does Shilled talk about “Narrative” now?

Using rationality on irrational humans

that isnt how it works in the real world.

in the real world, the US has been enjoying a lack of inflation primarily for two reasons. First, for decades we have been shipping production offshore to reduce labor and other costs. This is a massive deflationary trend, but now we have seen the problems with these supply chains and there will be an opposite, highly inflationary trend if we re-shore production. Of course, we lost a whole lot of jobs by shipping the production offshore and that is also deflationary.

The internet has also provided alot more price transparency and choice in the retail/distribution channels, which has been highly deflationary. Companies like Amazon have been rewarded for very low profit margins. But this trend is also likely at an end.

The factor going forward that could reduce inflation is the destruction of labor by AI. But that means a reduction in jobs. And that once again, means that the rich get richer and the average joe gets less and less of the economic pie.

The bigger problem is that all these deflationary trends have allowed our government to engage in highly inflationary monetary and economic policies without anyone seeing the consequences (inflation) until now. And those monetary policies have been pushed to the brink.

Now we will learn the downside of all these horrible polciies.

We have an economy that produces only a fraction of what we consume. And now that inflation is forcing the monetary base to contract, things will get very ugly

The next thing comming up might be an economy that do not have purchase power to buy (and consume) what is produced.

“The bigger problem is that all these deflationary trends have allowed our government to engage in highly inflationary monetary and economic policies without anyone seeing the consequences (inflation) until now. And those monetary policies have been pushed to the brink.”

Agree 100%

Well it’s pretty obvious that the Fed’s mandate has nothing to do with the public stance you have been enticed to believe. Manage inflation and support job growth is horse manure worthy for feeding to the less sophisticated individuals in our electorate, who still believe in America.

In my view, the Fed is behind the level that they need to increase the FFR interest rate to curb inflation. The Fed’s tools are not as blunt as the people you are listening too are trying to sell.

Inflation is like an insect infestation. In the end one has too kill everything.

Do you think that when the Fed raises to 5.25 and holds it there, inflation will stay at 7-8 percent?

Historically the mandate of a country’s financial system was to 1) Fund the regime and 2) Maintain the value of the financial system and the elites balance sheets. Unless the Federal Reserve is a magical entity that transcends millennium of human history, perhaps an analysis with the above “real” mandates may be helpful. The funding of the regime is easy, buy government debt with printed money creating instant inflation; i.e., quantitative easing (QE) followed by snail pace Quantitative Tightening (QT) that for Morgaged Back Securities (MBS) arguably doesn’t exist (only natural redemptions). Harder work is to maintain elites, but inflation looks like a helpful tool to reverse robinhood transfer wealth.

“Powell is testing a theory (the “soft landing”) by raising rates somewhat below the inflation level and then speculating those rate increases will bring down inflation over time.”

Yet at the same time he’s been talking sh!t, saying “the risk of doing too little outweighs the risk of doing too much.” If Powell were Pinocchio, his nose would no longer fit indoors. Powell is a yellow-bellied snake and a liar for the ages.

DC,

I suspect Jpow & co are trying to project an image of being stern inflation fighters publicly, while privately wanting inflation to keep running hot.

As Wolf has mentioned, inflation is the gov’ts friend, via debt reduction (paying back the same amount of dollar denominated debt with increasingly worthless dollars) and increased income tax receipts from wage inflation.

I don’t suspect this, I know it to be true. Because they would have never dialed the rate hikes back so quickly if they were serious, especially given all the data they have and the behavior of speculators and markets since September. This is all by design. They are destroying the working class and poor on purpose.

“inflation is the govt’s friend”

Until there are people in the streets, then inflation is suddenly a lot less friendly.

Already people in bread lines, people moving back in with their parents, mass strikes are probably not too far down the line if we keep at 6+% CPI.

IMO if the Fed were to publicly admit they’re ok with higher inflation, interest rates would blow out almost imediately. Jpow is keenly aware of this – hence the strong talk.

I posted this a few days ago, and this issue seems to be intertwined into the banking plumbing and very complex accounting. Maybe it’s nothing, but as interest rates go higher, these things under the rug will grow faster.

I haven’t looked at specific stress test examples, but this is all about Tier 1 Capital, M2M, AOIC, available for sale issues related to mark-to-market, GAAP and a long laundry list of adjustments made to bank portfolios (engineered for much lower interest rate exposure). Obviously a crap bank like Silvergate has all sorts of impairments floating in their FHLB witch brews and advances related to CET1 capital ratios.

As usual, this is all priced in and all is well… and all this gobbledegook alphabet soup is water underneath the bridge.

FEDERAL RESERVE BANK OF KANSAS CITY

September 08, 2022

“The rising interest rate environment has led to unrealized loss positions in community bank* available-for-sale securities portfolios and declining tangible equity capital ratios

At year-end 2021, only 4 community banks had tangible equity capital ratios below 5 percent; that number increased to 333 at June 30, 2022, indicating less ability to sustain economic shocks“

I am always looking for signs and hints in the financial markets. I got a notification this week from Vanguard that seemed strange. You can now keep your brokerage funds in FDIC bank deposits instead of money market invested in short term government obligations.

Seems like a strange offer as bank deposit money market rate is 3.1% and government assets money market pays 4.5%.

Schwab has been doing that for years. What took Vanguard so long?

If you want to put your extra cash into a money market fund, you buy it. But the daily sweep amounts go into FDIC-insured bank accounts. That’s how it should have been all along.

When they were peppering me with survey requests I copied and pasted this complaint every time. AND – one star for you!

It was, at least, cathartic. : )

Yes no one cares about the taxpayer anymore.

Years of financial repression has changed attitudes to the point that America is only living for today.

If debt has to be paid and incomes don’t grow as fast then the only outcome is that consumption will slow. I guess the new normal is higher prices and lower growth. Welcome stagflation.

Of course if we find a source of productivity gains then something could change but there doesn’t seem to be options on the horizon

Right. “Productivity gains” is the dogma that the economy will be healthy if those gains outpace costs. That means that labor is being displaced because that’s the #1 cause of cost for businesses.

Will the day come when productivity reaches optimal levels while humans are able to just wear pajamas and watch TV?

AI robots will nbecome taxanble entities as their efficiency to displace humans reaches a certain point.

Text written by AI no doubt.

Good one Implicit! :-)

Government policy sets the incentives for society. Our two party system has polarized so much that both sides play the dishonest game of excessive spending when social security, disability, medicare and medicaid growth trends are unsustainable.

Each program is different, but problems with full payouts are roughly 10 years away. The fix gets harder each year you delay making adjustments. Our polarized system doesn’t allow us to make a decision until a crisis.

Possibly this bout of inflation is the first of many as the Fed is forced to do the work Congress should have done with managing the country’s finances. As Greenspan said and I am paraphrasing: “The government can always send out a benefit check, but it might not buy much”.

social security, disability, medicare and medicaid

Yes, always take away safety nets from the least able to defend themselves. They should die sooner.

Don’t forget to take funding away from the VA and SNAP too.

“Yes no one cares about the taxpayer anymore.”

Or the SAVERS. But when did they ever care, actually?

“No one cares about the taxpayer anymore, not even the taxpayers themselves.”

You’re making an important point,Wolf!

LH – third the motion…

may we all find a better day.

We have economic iliteracy thinking that deficits don’t matter (or not even being aware of them) combined with irresponsible governments that like to defer costs into the future when someone else has to deal with the mess.

I’m in favor of much stricter constitutional rules concerning government debt. Other countries like Singapore or Germany have introduced such limits to somewhat enforce the unloved ‘restrictive’ side of Keynsian economics into the system. For example, total debt must grow by less than the 2% inflation target in any budget year where economic growth is positive. That would force to either raise taxes or cut spending during the good times and thus make the concept of ‘consequences’ much easier to grasp for the general population.

Yaun, you must be writing this for inhabitants on another planet.

Please leave me my dreams, every great social revolution starts with a random comment on a blog post

Spot on Yaun agree with you but I guess that will affect the wealthy from benefiting from the current system.

Well This taxpayer cares but he just realizes that with no actual representation in government for the little guy, he’s screwed in any imaginable future scenario anyway.

Your excellent article about the carnage left from the worldwide experiment in QE economic philosophy, leaves me feeling sick too my stomach.

For instance:

Your headline:

“The Fed can let the Housing Bust rip.” is not convincing in an economic sense even though emotionally, it is appealing.

Like a mountain climber would never leap from a cliff, but would use a system to lower their body to the bottom, without catestrophic injury. IMO, the Fed should ……

Ok, let her rip !

My reasoning is based on my belief in the precepts of accounting 101 that deals with the balance between the assets, the liabilities, and the owners equity. When the liabilities exceed the sum of the assets and the owners equity, the organization is bankrupt.

Without a bail out, which is not free. Someone pays. In the current con, QE, the marginal buyers, the speculators bid up the price of housing and should be the one’s that are deserving of financial failure.

On the much more important cohort of American society, the other 89 pct of citizens that actually derive our culture. The better they are doing the better I’m doing.

The Federal Reserve policy, at this juncture, is extremely important, given their outrageous incompetence for pretty much the entire history they have been in existence, which began in 1913, the dawn of the egomaniac caused WW1. America introduced troops into the gaseous fields in 1917, with the shooting war ending in 1918 while the swath of the 1918 flu created a dismal mentality about the future.

The malaise was solved by liquidity from the newly franchised Federal Reserve Bank of the US.

The creative, libertine era of the 1920’s gave way to the great depression. A period in which Americans understood the frailty of a society that caters to the wealthy in preference to the people.

“A period in which Americans understood the frailty of a society that caters to the wealthy in preference to the people.” Dang, you must be talking about the same planet that Yaun’s inhabitants are living on.

There are many a major company with negative equity, so no liabilities greater than assets do not mean you are bankrupt. Bankruptcy, a subjective decision, generally happens when management think the entity cannot meet the obligations of it’s liabilities. Companies also do not cease to exist in most bankruptcy cases, it is usually used to restructure outstanding debt. Finally, bandit companies still operate, okay build, sell product, pay employees, etc.

‘the dawn of the egomaniac caused WW1.’

This has something to do with the Fed???

Or by egomaniac do you mean the Kaiser?

BTW: all the Fed critics need to remember its sins of omission as well as commission. The great sin of the Fed in the Depression was that it did nothing, culminating in 34 when the Fed Reserve Banks ceased to operate. You can have too much liquidity but that was not the problem during the Depression.

If the young families that are living with today, not yesterday, are unable to attain economic security, a more definable concept than the entitled fool’s trumpet about economic freedom, that is a problem.

Although I will not be here to live through the ramifications of the decisions we are making today, my grand daughter will be.

The people that made every bad decision since the war in Vietnam are still there making decisions about how to undo their miscalculations. Like the war on Iraq.

It is not like they’re incompetence is inconsequential.

Or worse, their corruption is inconsequential. Which brings me back to the point about whether the Fed should let her rip which invokes the hard consideration, what does that even mean ?

It’s not as if the Fed isn’t already paying the criminal banks to hold “hot” cash for lending. It is the commercial business that has cold feet, otherwise known as the consumer.

I really don’t know what you mean by letting the Fed rip.

If you mean that the asset prices need to collapse, I agree. Including the stock market balloon, selling overpriced stocks to the hoi poi before the reckoning.

Damn my auto complete feature went off the rails in the last sentence, should have used Chat GPT.

A headline’s job is not to “convince” you. A headline’s job is to get you interested in reading the article. And then it’s the article’s job to convince you.

Nice distinction, thank you. I had forgotten.

Still, at this moment in time, I stand behind my comments about the idea that the ” headline ” suggested, even if it was in jest.

TG you don’t have nested replies!

” . . . no one cares about the taxpayer anymore, not even the taxpayers themselves.”

I’m convinced that I can about taxpayers, especially my selfish self ; )

Yep, I’m seeing people buying crap in bad neighborhoods with bad schools, high crime, far from employment centers. The only thing in common with these properties is they are affordable. The mortgages are insured and guaranteed by the taxpayer. HELOCS are also coming back. I believe you still have to pay closing costs when you take out a HELOC.

From some recent research, I believe that there are fees. Origination fees, Appraisal fees(What is your fee?), Title Insurance fees($600-$1K) which can add up into the thousands.

Some issues with a home equity loan is that the interest rate is often adjustable and rates start at 1-1.5% above a refi (ie initial rates for HELOCs are around 8% now before they adjust). If you don’t pay your payments, your house can be foreclosed even if your primary mortgage is paid up to date.

My question is still: Are these HELOC loans rolled into MBS’s? Do the GSE’s own these loans? If not, then the bank is on the hook and not the taxpayer.

That is a brutal exclamation point of an ending to that article, and yet I can’t help but feel I am in that group. I just pay my taxes since I feel no attachment to anywhere I’m going and Fiscal Responsibility is a punchline for both political parties.

I am private money lender and I had an interesting conversation with Mortgage Broker the other day. He was arguing with me about my underwriting criteria. He was arguing that Fannie Mae and Freddie Mac have looser lending requirements than I do. I laughed and said, “that’s because the US taxpayers are not guaranteeing my loans.” He didn’t think that was very funny, lol.

Not surprising. People love to believe their own hype.

Can you say Derivatives? Just a different bubble created by govern ment and all its cohorts……. This crash should be spectacular. Stay out of debt, live within your means and good luck.

Amen Bubba. I’m livin’ it.

Besides “good luck” I would add: Do what you can to offset the corrosive effects of inflation.

To offset the corrosive effects of inflation, the general population would have to start thinking. They’d have to overcome the powerful effects of advertisements that increasingly penetrate into peoples’ consciousness and do some simple reasoning. They’d have to turn a blind eye to the pizza ads, the big honkin’ truck ads filmed in wide-open spaces that do not exist, they’d have to turn away from the happy faces, the blonds with big boobs, and actually start to think, reasonably. Which planet are they on?

And that, dear readers, is why the Fed will never let it just “rip”. The entire culture would also “rip”.

Ha ha, good thoughts HowNow. Debt free and money in the bank livin in the country. TV ads are just like watching a freak show.

It is a hobby of mine now to watch what advertisers,and these corporate board room morons portray as their understanding of what is “normal society” today. It becomes more and more bizzare by the day.

WARNING: If you engage in this type of entertainment, I must warn you that at times, it can be pretty depressing. To offset that, simply go out to shop, or take a walk in the country. Reality returns quickly.

Credit GB, as an exercise, turn the sound off during commercials, watch the wall to see how fast images are changed – light to dark – the pace of change – and you’ll see that our brains have no chance of thinking while the sh*t show of commercials blast out at you. Mentally, you’re effectively paralyzed during commercials.

Good point about turning the sound off, but that only focuses the mind more keenly on the strange sights portrayed.

This reminds me of Alex DeLarge in “A Clockwork Orange” with eyes propped open forced to watch brainwashing video.

Come to think of it, how many graduates of the brainwashing process are considered “experts”… I wonder.

Long term view:

Mortgages are going to at least 7 percent 30 year fixed.

House prices will crash.

Rates will drop.

House prices will rise.

Go back to step 1, repeat for eternity.

This is a doom loop because our economic system is equilibriumphobic.

There are changes you could make to make the system equilibriumphilic and provide a higher quality of life, but good luck proposing it.

“There are changes you could make to make the system equilibriumphilic and provide a higher quality of life”

Which new word is correct ? Is it equlibrium phobic or philic ?

The current system has a phobia about doing what you think should be done. An idea that is in equilibriumship with the ones that are currently exercising the power you think should be exercised in a manner that you would do it, philic, an absolute chemical stasis between two compounds.

Howdy dang,

Both new words are correct:

We currently have an economic system that abhors equilibrium, thus, equilibriumphobic.

We need an economic system that tends toward equilibrium, thus equilibriumphilic.

Every word that we use was invented. This is today’s example.

Thank you for asking!

Yes, huge phobia exists towards significant change, people are comfortable with the dysfunctional system and aversion to evolution tends to triumph logic.

All we can do is make the case best we can.

I agree house prices will crash and within a few years start to go up again. See this play out in the 1990s and in 2008-2012.

Inflation won’t allow them to continue this game that allowed them to blow sequentially larger bubbles. Most people have never even seen an increasing rates environment and it will be an increasingly hard lesson for people to get over the fed pivot nonsense.

“Rates will drop.”

Seems like rates have been making higher lows, with the uptrend still solidly in-tact.

Seems like the credit cycle may have turned over in 2020/2021 and the next couple decades (at least) will have higher and higher rates.

I see, fill your boots , nothing but good news

1) SPX monthly for fun, for flip : Apr close and May close are resistance. Feb 2023 closed below, with a large selling tail, but Feb is far from over.

2) SPX weekly : x3 selling tails under a supply line coming from Jan 2022

top.

3) SPX daily might close the Feb 16/17 gap and move up in a 4TD short

week, next week.

4) In order to move up there must be a close > Feb 2. Breaching it isn’t good enough. Yesterday low took out 11 TD stop losses to fill the tank, for a break.

5) Feb might stay green, rise above Aug high and move higher, but if Feb turn red it can stay red as long as it close > Oct 2022 close, producing a

right shoulder, because in Jan SPX flipped…flipped from down to up and it can stay green for many many months, unless :

6) If Feb close < Oct close…next stop Feb 2020.

The economy is still hot.

Stable prices are more important than full employment,

3 hikes are predicted this year. They probably will increase until unemployment starts to rise. 25, 50, 75 ?

Given that recent reports have indicated that inflation is still high, perhaps the Fed should consider a mid-meeting 0.25% hike right away.

That should signal some seriousness to the market, yet not create a huge scare due to the small level of increase.

Geopolitical risks are often mentioned in passing in discussions of Federal Reserve policy; however, there is not much depth other than the mere statement. Probably all foreign countries do not like the Federal Reserve’s inflation and certainly don’t like the weaponization of the dollar. It seems the Federal Reserve has two choices, pump the asset market with dovish inflationary policies or secondly to hit the brakes on inflationary and try to make the dollar like the legendary Swiss frank with a real interest return and enough additional interest rate in the near term to stop inflation. With BRICS country looking to make a gold backed money and a separate bank messaging system.

Credit card delinquencies at large banks are low, but high at the smallest of banks. Delinquencies are rising.

Amazon is requiring its employees to return to the office for three days a week.

“Amazon is requiring its employees to return to the office for three days a week.”

The company I work for is requiring 3 days a week in the office also.

This may cause some turmoil if the office is in Seattle and you purchased a home for WFH in Hawaii with a huge mortgage.

The layoff list becomes easier.

That’s fine. Amazon will just have to hire people in Seattle.

Which will drive up prices for houses in Seattle (or San Francisco).

Unless you became independently wealthy working from home and can retire, you’ll likely have to move back to where the higher paying jobs are located when your company requires you to be in the office. Mostly the major cities with large corporations will again see more demand and higher prices for housing.

I watch “House Hunters” on HGTV for fun. The last 2 years there have been quite a few couples buying remote expensive properties in Colorado, Utah, Maine because “they can work from home”. What happens when they are called back to their city offices? The migration will be back to cities and they will have to sell. After seeing some of their personalities, I suspect they may murder and eat each other in their snowbound cabins before that happens.

“The biggest part of the damage will be absorbed by taxpayers because they’ve been shanghaied into guaranteeing the majority of mortgages that have been securitized into MBS, and into guaranteeing subprime mortgages, and low-down-payment mortgages (via FHA, VA, etc.), and no one cares about the taxpayer anymore, not even the taxpayers themselves”.

Wolf, fantastic statement! The phrase at the end says it all. The American people have given up on fiscal issues such that in 2027, US debt is forecasted to be anywhere between $36T and $44T while GDP is only at $29T.

I should settle down and expect this as nothing in America works well anymore – transportation, healthcare, education, military, legal system …

Well, we had a good run!

Greatest, silent and boomers had a good run, the rest not so much unless they’re a sucessful sociopath thats managed to worm their way into the c suite of some fake company and can cash out their fake stock for millions every quarter.

Most of the millennials I know are doing quite well for themselves. House, new cars/trucks, vacations.

They have regular jobs at normal companies.

Is the reason that the mortgage balance as a percent of disposable income is lower now than the GFC because the layoffs in mass have not occurred – did that cause the large bump seen in the GFC and if so, should we have a recession/mass layoffs, that bump could easily occur again now?

“…should we have a recession/mass layoffs, that bump could easily occur again now?”

Nope.

1. Disposable income didn’t dip much in 2008-2010 because of unemployment benefits and stimulus payments. So that part really didn’t change much. And it won’t dip much during the next recession either. During the Pandemic, disposable income spiked despite 20 million layoffs.

2. Your timing is off by a few years. Employment peaked in Dec 2007 and began to dip in January 2008, and then after the Lehman bankruptcy in late 2008 began to plunge. Disposable income began to dip only in Oct 2008 — 3 years after the housing bust started. Mortgage balances peaked in April 2008, and then fell as foreclosures took over.

Thanks Wolf.

Bankrupt-u-Bernanke drained legal reserves for 29 contiguous months, turning safe assets into impaired assets. Then Bernanke engineered his second contractionary program:

The FED covered its “Elephant Tracks” (like “Black Monday”)

We knew the precise “Minskey Moment” of the GFC:

POSTED: Dec 13 2007 06:55 PM |

The Commerce Department said retail sales in Oct 2007 increased by 1.2% over Oct 2006, & up a huge 6.3% from Nov 2006.

10/1/2007,,,,,,,-0.47 * temporary bottom

11/1/2007,,,,,,, 0.14

12/1/2007,,,,,,, 0.44

01/1/2008,,,,,,, 0.59

02/1/2008,,,,,,, 0.45

03/1/2008,,,,,,, 0.06

04/1/2008,,,,,,, 0.04

05/1/2008,,,,,,, 0.09

06/1/2008,,,,,,, 0.20

07/1/2008,,,,,,, 0.32

08/1/2008,,,,,,, 0.15

09/1/2008,,,,,,, 0.00

10/1/2008,,,,,, -0.20 * possible recession

11/1/2008,,,,,, -0.10 * possible recession

12/1/2008,,,,,,, 0.10 * possible recession

RoC trajectory as predicted.

If there wasn’t a floor on interest rates (the O/N RRP award rate), there’d be negative short-term nominal interest rates.

No Landing!!

“You’re Welcome” – J Pow

“Nobody cares about the taxpayers anymore, not even the taxpayers.” This is due to the fact that the majority of US voters are no longer taxpayers, or at the very most, their tax burden is trivial. A small minority of professionals have become the government’s tax donkeys. I am one of those. When the donkeys go on strike, or lay down and die, that’s when the US Ponzi scheme will really get interesting.

DDG, so true. Not only does America depend on your financial support but ‘you and your’ kind supply the competency to our systems and when ‘you’ leave, lay down and or die it is game over.

Just imagine the The AAMC and AMA stated to American medical schools that meritocracy is “malignant”.

Very true. It’s crazy how so many people have been convinced otherwise too. I think it’s a misunderstanding of percentages vs. absolute values.

How do you define trivial? I paid over $10k in federal taxes and while it’s not a huge amount, I don’t consider it trivial.

Are you willing to trade down your lifestyle when you give up your “tax donkey” yolk? Don’t worry, there is someone else out there that will replace you.

Kurtis-no doubt the autocorrect at play, but I would say, more correctly, the yoke’s on us with the yolk on our faces…

may we all find a better day.

You are correct, my auto correct put yolk on my face.

But the whining over taxes is always over the top. My household is about 20% above the median for my state, and we have an effective tax rate of ~ 15 percent. My health insurance costs us ~12%, and my mortgage and house insurance is ~10%. These are percentages from my gross household income.

For me, the egregious expense is the health insurance. First job out of college I paid ~1% of my gross income on it. The increase has been unbearable.

“This is due to the fact that the majority of US voters are no longer taxpayers, or at the very most, their tax burden is trivial. A small minority of professionals have become the government’s tax donkeys. I am one of those.”

This is pure delusional fantasy.

Pea Sea – especially when time comes (and it always does) to soldier…

may we all find a better day.

Go on strike. No one is stopping you. Freedom is what makes the US great. If you don’t like your tax burden, jettison your income and join the bottom half. Personally, I consider myself fortunate to be able to pay significant taxes. The alternative isn’t very appealing.

That’s because morons don’t realize their 7.65% FICA taxes are taxes. People pay a lot more than they realize and that’s how the government likes it.

My intention isn’t to torture Wolf or any commentators here, but I think it’s worth pondering some valuation ideas.

I’m always curious about revisions to means or regression to means and how to look at extreme variables, as in home or stock spikes and crashes.

Smoothing out extreme variables apparently helps determine a cleaner mean value.

Unfortunately, the pandemic was (is) nonlinear and continues to distort most every valuation series, adding a new dimension of variability in analyzing data. I’m sure the vast majority of economic experts will object to that premise, and believe that data was never impaired by pandemic anomalies.

Nonetheless, home prices have seemed chaotic in terms of valuations in the last three years.

Using Fred, I added together their median home sale price with their average sale price, to get a current national home vale of $501,750 for Q4 2022.

Using that valuation input, national home value in Q2 2020 was $348,550, which indicates a gain of $153,200 or about a 43.9535217 percent gain during about 2.5 years.

Fred does have a recent blog post comparing home valuation to stock values, but it seemed highly inaccurate, suggesting homes and stocks have fallen back to normal levels — and that type of misinformation or misrepresentation, circles back to mean regression and valuation.

There’s obviously a big media push to reignite the animal spirits and excite people to persuade them and draw them into imaginary fantasies about the economy going into a pre-recession V-recovery before the recession becomes official. That’s not unlike having a preexisting family disease that’s linked to a genetic test that confirms a diagnosis, but doesn’t pin down the day you die. Morbid reality often results in denial.

I’ve been a huge Fred groupie for at least ten years, but I’m finding it to be very limiting in how it sums up data into narrative that isn’t useful or predictive.

I plugged in my values (above) then adjusted for change, getting a nice smooth downward curve in home valuation, but the chart doesn’t strike me as realistic, in showing the contrast in valuation gains versus current losses.

The lesson I’m learning is to question what the data represents and ask what’s missing — to be far more skeptical about charts that are overly simplified and smoothed out to tell one part of a narrative from three years ago, but then incorrectly extrapolate related dimensionality.

I can see home valuation falling slowly, as inventory remains very low, and I think that dynamic will continue to extend pandemic anomalies, which will become increasingly distorted as mortgage rates rise. I think that narrative is challenging to see in terms of past data trends, I don’t think we’ve ever experienced what’s unfolding.

If mortgage rates continue to be pulled upward with treasury rates, and if inventory shrinks further, as home valuation remains elevated, as a recession phases in, none of the data on Fred will be useful in explaining chaos.

I’m interested in seeing valuation ideas and links!

Here’s my crap chart (if it even works):

https://fred.stlouisfed.org/graph/?g=10cmf

Houses are like workers, there’s not enough of them.

That chart is fascinating in how it shows peaks and valleys that convey the ever changing moving average of home values. . .until 2020. Then it goes into a weird bell curve literal bubble. I’ve never seen a chart do that before and I’ve seen a LOT of FRED and equity charts.

Meme / SPAC stocks already dead.

Inflation has been trumping equity and bond markets for almost 2 years.

Yet…almost nobody is defaulting on their mortgages.

Is this what it looks like when the Everything Bubble pops ?

Practically no one will default on a mortgage until the home price drops far enough to make the mortgage seriously underwater.

If the homeowner cannot pay the mortgage anymore, they will try to sell the home. If they get enough for the home, they will sell it, pay off the mortgage, and rent something until they’re ready to buy again.

The problem arises when the mortgage is 20% underwater, and they CANNOT sell the home because the sales price won’t pay off the mortgage. So now they’ll default and maybe try to work a short sale or let the lender have the house.

So don’t expect a significant rise in mortgage defaults until home prices have come down hard.

I only see this happening if UE rates go way up. Most people have mortgage rates under 4%, many at 2/5%, and they aren’t going to give up the low payments if they can at all help it.

If house prices drop 20% but mortgage rates are 7%+, it doesn’t wash to walk away, wait and buy again.

Rental rates would also need to fall, a lot.

2.5%

Additionally, the concept of mean regression is fascinating, and for me, I want to quantify why home values went up almost 50% nationally and what that really means in terms of future value.

How far above normal did valuation go and what’s the story in terms of where future reality is?

I assume that means looking at prior long term growth trends, which are far different.

Then, how are those long term trends changed by inflation and mortgage rates. I’m not entirely sold on shillers index ideas, they tell an incomplete story.

With stocks, a moving average of twenty years sort of consolidates long-term price and contrasts current value, but seeing forward obviously isn’t an easy task.

Shillers index won’t be useful in this upcoming era of low inventory, high price, but that’s my opinion…

Dr D

I have commented on the real estate oriented Wolf articles that when that 50%(ish) housing run-up reverses, we are, as you state, regressing to the mean, or trend. I don’t see home prices falling much below that trend, except maybe in San Fran due to Techsodus. (Tech Exodus). Significant inventory from foreclosures is not gonna come. The only ones who will be in that boat will be job-losers who bought primary residences in 2020-2022 during the run-up.

If there were Crypto-millionaires and SPAC / Meme Millionaires who bought homes in 2020-2022, and now their sudden wealth has vanished, Wolf’s data indicates they are still paying their mortgages and credit card bills. I woulda thought you’d see some of that housing inventory on the market by now, and maybe some of it is on the market – but not noticeable. Wolf may be right that it takes a long time to admit defeat in housing, but other than San Fran, I don’t see the “crash” everyone is hoping for.

But using interest rate manipulation as its monetary transmission mechanism, under an ample reserves regime, the time-frame of the FOMC’s horizon was 24 hours, rather than 24 months.

Bernanke, pg. 287, “Lower long-term rates also tend to raise asset prices, including house and stock prices, which, by making people feel wealthier, tends to stimulate consumer spending-the “wealth effect”

Stoking housing prices is what Powell wanted to do.

Thank you Wolf for another excellent article.

I especially like the first chart showing mortgage balances vs % of disposable income. It gives me hope that a crash is not imminent when compared to the huge disparity peak in 2008. The peak in 2008, led to the HB1 crash and massive foreclosures.

This could happen again if unemployment increases like it did in 2008-2009. Disposable income will plummet leaving people with large mortgages. The green line will rapidly increase before it plummets.

If everyone keeps their jobs and wages increase with inflation, I think it will be a soft landing.

For amusement, do you have any charts on housing prices in the Metaverse Decentraland or Sandbox neighborhoods? I heard these were the best place to purchase for the great virtual parties. Some took out mortgages to buy a home close to the parties and shopping. Search for “Crypto Housing Crash” for more information on this craziness.

A chart would be entertaining.

Great last paragraph

“The biggest part of the damage will be absorbed by taxpayers because they’ve been shanghaied into guaranteeing the majority of mortgages that have been securitized into MBS, and into guaranteeing subprime mortgages, and low-down-payment mortgages (via FHA, VA, etc.), and no one cares about the taxpayer anymore, not even the taxpayers themselves.”

But then again…maybe most taxpayers don’t care because:

57% of U.S. households paid no federal income tax last for 2021 as Covid took a toll.

Even in 2019, the bottom 50% only paid 3% of all federal tax. Most pay no taxes. The top 50% paid 97%. So in reality, do the bottom 50% care if MBS defaults will be paid by taxpayers? LOL

This is a good observation. If 57% of voters pay no income tax, then this will continue since 57% of the people have no skin in the game.

This will have to change since the taxpayers have been left off the hook with deficit spending and money printing. A day of reckoning has to occur at some point for current debt. Inflation and low interest rates (Thank you everyone who purchased 30 year US Treasury bonds paying 1.2% in 2020!) are fixing some of the issues with past debt.

Since I have been paying taxes, the upper middle has assumed most of the tax burden. The 90% upper rates when I first started paying taxes no longer exist so the upper middle is picking up the slack.

Generally the bottom 57% have missed out on economic opportunity too, so personally I have little concern that they aren’t taxed heavily. You can’t juice a rock, anyway. The IRS should be looking closely at every business and person that took PPP loans, and generally at every company and person that benefits from big federal largesse.

Good observation? This is a misleading observation at best. The bottom 50% have “no skin in the game” because they’ve already been skinned as I describe below.

I think the point was they do not care. If they have already been skinned, they will not care fi the tax payers pick up the MBS bill of speculatiors and wall street.

The ones who are getting skinned are the middle middle class that are paying taxes.