It just keeps getting worse.

By Wolf Richter for WOLF STREET.

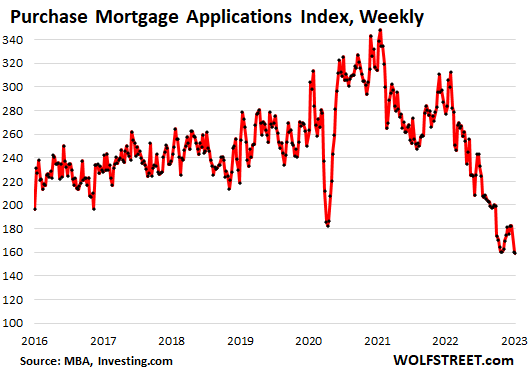

Mortgage applications to purchase a home are a forward-looking indicator of where home sales volume will be. Existing home sales that closed in November already plunged by 35% year-over-year, the 16th month in a row of year-over-year declines, making for a historic plunge. And mortgage applications went into the wrong direction from there, despite the dip in mortgage rates.

Applications for mortgages to purchase a home fell to the lowest level since the Christmas week of 2014, and beyond the lows of 2014, we have to go back all the way to 1995, according to data from the Mortgage Bankers Association today.

Compared to a year ago, purchase mortgage applications have plunged by 44%. Even during Housing Bust 1, mortgage applications didn’t plunge that much year over year.

That little dip in mortgage rates had no impact. This drop in mortgage applications came despite the dip in mortgage rates that started in mid-November from the 7.1% range and hit a low point in mid-December at 6.28%. In the latest reporting week, the average 30-year fixed rate was at 6.42%, according to the Mortgage Bankers Association today.

The drop in mortgage applications indicates that it doesn’t really matter to the volume of home purchases whether the 30-year fixed rate is 6.3% or 7.1%. The difference is just cosmetic. The current home prices – though they have come down in many markets, and have come down hard in some markets – are still simply way too high.

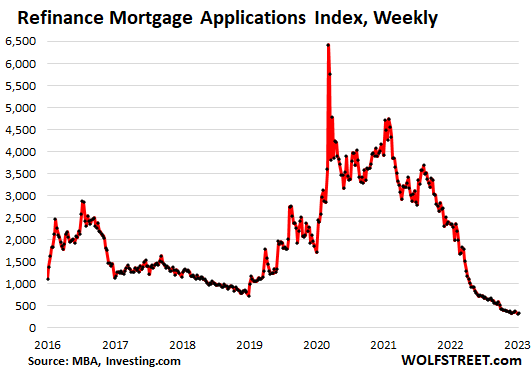

Refinance mortgage volume has died: Applications to refinance a mortgage have collapsed by 86% from a year ago, despite the invisibly small uptick in the latest week. Since October, refinance applications have hovered at the lowest levels since the year 2000. And this makes sense because hardly anyone would be refinancing a 3% or 4% mortgage with a 6% or 7% mortgage, except when under duress to extract cash.

Mortgage lender woes.

Mortgage lenders, whose revenues have collapsed as mortgage applications volume has collapsed, have spent the last 12 months laying off people and shutting down divisions. Some smaller operations have shut down entirely.

Wells Fargo, once the largest overall mortgage lender and then the largest bank mortgage lender, is the latest to make the news with its additional efforts to step back from the mortgage market, on top of the steps it had taken in 2022.

CNBC reported yesterday that it had “learned” that the bank will now re-focus its mortgage business only on its existing bank and wealth-management customers, and borrowers in minority communities; that it is shutting down its business that buys mortgages that had been originated by third-party lenders; and that it is “significantly” reducing its mortgage-servicing portfolio through asset sales. All this will entail a new round of layoffs, on top of the layoffs in its mortgage business that started in April last year.

Wells Fargo only had about 18,000 mortgages in its retail origination pipeline in the early weeks of the fourth quarter, which was down by as much as 90% from a year earlier, according to CNBC, citing people with knowledge of the company’s figures.

Wells Fargo shares are down 29% from their recent high in February 2022, and down 36% from their all-time high in January 2018.

The mortgage lenders that surpassed Wells Fargo a few years ago are non-banks – they were aggressive in getting the mortgage business during the Easy Money era, then got crushed, and in 2022 made it into my pantheon of Imploded Stocks. They have all shed large numbers of workers, and some have shut down entire units in order to survive.

Their stocks have collapsed from their highs:

- Rocket Companies (owns Quicken Loans): -81%

- United Wholesale Mortgage (owns United Shore Financial): -73%

- LoanDepot: -94%

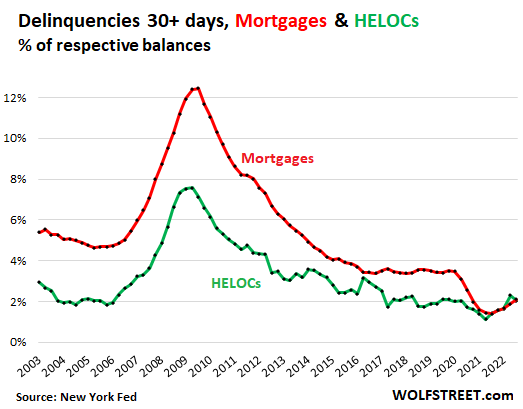

But mortgage delinquencies and foreclosures are still near record lows.

What the real estate and mortgage industries are lamenting is the plunge in volume of home purchases and the plunge in volume of mortgage originations, which have caused their revenues to collapse.

The issue is not the credit quality of the existing mortgages. At least not yet; that phase may come later if and when unemployment reaches high levels, which is just not happening yet despite the layoffs in tech, social media, and finance. Mortgage and HELOC delinquencies, though they have ticked up from the record lows during the pandemic, remain very low.

The HELOC 30-day-plus delinquency rate ticked down to 2.0% in Q3, 2022, in line with the lows during the Good Times, according to data from the NY Fed (green line).

The mortgage 30-day-plus delinquency rate ticked up to 2.1% (red line), still far lower than before the pandemic.

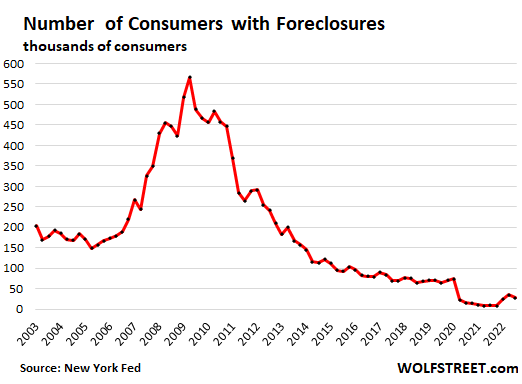

Foreclosures ticked down again in Q3 to just 28,500 mortgages with foreclosures, and remain well below the number during the Good Times before the pandemic, when there were about 70,000 mortgages with foreclosures:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

One day…folks with student loans will have to start making payments again.

And those funds will come out of somewhere…maybe even from an underwater mortgage payment.

Will they though? the Biden administration is now pivoting and trying to make unpaid student debt dissolvable for many just 10 years after the loan commence date starts, regardless of how much has been paid back or if payments were even being made.

There’s no reason to believe tons of this debt won’t just be written off.

If I were a smarter person, I would get myself into Stanford, max out student loans to the hilt, leverage the hell out of that degree/those contacts/a dazzling CPA, then let the government and the tax payers pick up the tab.

Enlist in the military, test into a cushy desk job with the ASVAB, spend 3 years doing f-all (possibly getting valuable certs), apply to Stanford, pay with your GI Bill/yellow ribbon benefits, collect BAH while going to school. Leverage your contacts as well as a veteran and disabled (let’s be honest, if you leave with a 0% rating, you deserve at least one for being too mentally deficient to document one of the hundreds of things that gets you a 10% rating that you no doubt developed over your 3 years). Easy. Also, now you get VA backing of your mortgage and various other goodies.

Heck, this is easy! And recruiters are saying they’re having a tough time meeting quotas? I’m not willing to go back in, but if they pay my consultancy fee, I’ll happily tell kiddos the good news about the military (while not talkin about the bad/dumb stuff). Service guarantees citizenship!

Grant,

“service guarantees citizenship”.

I believe that quote comes from Stormship Troopers.

Grant,

“service guarantees citizenship”.

I believe that quote comes from Starship Troopers.

It’s a good question, as practical matter it’s hard to see how student loan repayments really get restarted again. The amounts due have grown during the moratorium but the economy in general and esp the finances of grads have come to depend on the de-facto forgiveness since the pandemic. Any student debt payment re-start, at least with the pre-pandemic policies would tear another huge hole in spending and the broader economy. And with all the uncertainty, lots of students and grads with debt are honest wondering if it’s financially smarter to put their money elsewhere instead of towards debt repayments–and these are often huge debts, even public universities are more expensive these days, Ivy League tuition costs are out of control and professional schools like law, medicine or business can easily be $100K to $150,000 for a year. The mistake was in using a debt-funded higher education model to begin with. Whatever their flaws, European universities had the right idea with the tuition free model, but tougher entry requirements to show a student is college material, and a bigger focus on apprenticeships and practical training even before middle school.

As unfair and bad as the student loan system is, people like me who went to modest schools and worked while we were there and managed to pay the loans off (if we even qualified for FAFSA) rapidly upon graduation feel pretty chafed that others who threw caution to the wind might walk away without a scratch. I’m by no means a boomer who paid for his education, a nice car, and rent on a job flipping burgers. I’m a mid-millennial whose school cost around $60,000 for 4 years. I was able to shave a few thousand off with scholarships, etc. I could have gotten into, or at least transferred to, much more elite (and expensive) institutions, but didn’t because of a combination of frugality and a determined belief that merit could outweigh connections and the name-brand sheen of an elite college. Forgive me; I was young and dumb. I’m fine now and could easily go back to college for free with the GI bill or my company. I just have no interest. The point is, the notion of the money and opportunity cost I surrendered in order to be financially responsible at a young age getting mitigated for other people perturbs me. I know the system is a scam, and I know that decent people suffer under the odious college loan 5-sided-5-pointed-egyptian-architecture scheme. That doesn’t change the way that I and a lot of Americans will feel about loan forgiveness if the topic is ever broached.

Grant – even under the old GI Bill that i returned to college with, it fell well-short of a ‘free ride’. I still found it necessary to minimize my course load to give me time to work while completing my degree (over ’76 – ’80, I had a year-and-a-half of credits when I received my draft notice), even allowing for the bargain rates of the CSC/US at the time.

I had them, and share with you now, those chafing feelings. The issue, as alluded to by the references here to R.A. Heinlein’s classic SF novel ‘Starship Troopers’ is the one we’ve yet to work out among the citizenry except in times of war (US Civil, WWI, WWII, post-WWII/Korea/VietNam), or economic disaster (FDR’s ‘New Deal’ employment programs) and that is the one of how seriously do we, as a people, take the idea of ‘national service’ beyond that of simply paying taxes (see Justice Holmes’ quote on that) when, given human nature, avoidance of same (and general ignorance/avoidance by the citizenry in performing their oversight of their Congress in terms of the budget and taxes, among other policies) might be termed a major national sport.

(In my reference to ‘national service’, I wish to be clear that I think it can exist honorably and respectably in forms other than military, as well as. In any case, given human history, it will only be successful in proportion to a people’s belief and faith in their polity).

Rant over. Thanking you for your patience, and-

may we all find a better day.

“Whatever their flaws, European universities had the right idea with the tuition free model, but tougher entry requirements to show a student is college material, and a bigger focus on apprenticeships and practical training even before middle school.” You nailed it, Miller!

91B20 1st Cav: I agree with your rant, especially the need for the U S to have some form of “national service”.

Valerie and Miller: the idea of “free college ed.” as in largely homogenous European countries, would be a bad idea here. Unless there are some very, very stringent rules (how many units are taken, how many semesters to attend, what kinds of curric. are included, is attendance required, etc. etc.), it will be abused by students who don’t have “skin in the game” or are there because of welfare support, free books that can be sold back to the stores, etc., etc. And professors who have 20-hour work weeks (lectures) and skip their 10 hours of office time and only work 8 months/yr. will further a bloated system of faculty and increase the “lecturers” who get minimal wages, no benefits, and zero job security or longevity.

And the notion, Valerie, that there should be “tougher entry requirements to show a student is college material” is fanciful in fact, and exclusionary for many minority students. Many, many poor kids aren’t prepared for college work regardless of having gotten good grades at piss-poor K-12 school districts. They will be attending in such small numbers that it will be akin to racial segregation. The college material notion – well, what can you say about private colleges where wealthy alumni will get their kids enrolled by hook or by crook regardless of capabilities or motivation.

K-12 is paid by taxpayers and the system turns out many successes and lots of failures. No need to extend “free education” beyond high school!

Rant over.

@2banana, yes and no. The newest resolution in the world of student loans is to reduce the income based payment amount to a lower percentage of discretionary income, so if someone’s in bad enough shape to be behind on the mortgage the student loans may not sink them anymore. They also might have deferral time left and the servicers have other options. The private loans are much less forgiving, of course, but I’m not sure we’ll see much cause and effect here. It takes more creditworthiness to get a mortgage these days, in the shadow of ’08.

This just means more layoffs for the Dept of Education as funding from unpaid loans dries up.

Does the federal government actually lay anyone off?

Or are you referring to contractors?

How about some common sense,quit paying football coaches 8-10. Million a year . That money should go to student education

Football coaches are the highest paid state employees in many states.

Athletics is easy to point your finger at but it’s a common misconception that they are taking away from other areas. Universities (particularly state universities) are generally set up so that each unit is self-supporting. Parking garages are built with money from parking fees. Coaches are paid from TV contracts and ticket sales. Not from tuition.

We should let the bankruptcy court sort who can pay and who cannot.

No, actually these institutions of supposed higher learning should underwrite these loans at their own risk. More moral hazard on steroids.

The federal student loan program should not exist at all. Predictably, it’s turned into another welfare program.

Too many institutions have no business issuing diplomas and shouldn’t even exist. Too many of their students have no business being enrolled.

It’s substantially a disguised form of day care.

Why aren’t the schools liable for say 50% of loans not paid??

not like their tuition isn’t enough to cover it

Plus…

A lot of that money went to commercial landlords — “student housing” is an asset class, and “luxury student housing” is a segment within this asset class; and these mortgages have been securitized into student housing CMBS.

A lot of it went to tech companies, such as Apple.

A lot of it went to the scam that are textbook publishers.

Etc.

They all should surrender some of their ill-gotten gains.

Wolf,

Everybody in HE should pay…but the colleges have profited the most and been the indispensable actor (purveyor of fraud).

Not to mention that they are the only ones with billion dollar endowments (more than many might think) that can (finally) be reasonably taxed or expropriated.

To the best of my knowledge, student loans are exempt from bankruptcy. That is the problem. One can buy a boat, an SUV, run up credit cards and claim bankruptcy, but something that benefits the citizen for life – or society as a whole – can be claimed. I reckon all those real estate developers have a golden road to bankruptcy should their gamble not pay off.

Wait for the realtors to suddenly flock this article with following stupid comments:

1. The inventory remains low.

2. The inflation has been defeated and Fed Pivot is just around the corner.

3. Here in socal, the sun never sets……

4. My neighbor just sold his house at twice the 2019 price! So there is no price correction.

5. Housing remains a great investment, the rent will offset the fall in prices.

6. My own data shows that the puny drop in mortgages have made housing market healthy again.

7. Buy now or Miss out forever.

Yes. The predicted recession, along with supply chain changes may be taming or have tamed inflation, maybe temporarily. However, it has dramatically reduced the poorer, 90% of Americans’ disposable incomes and expectations (the Americans who pay taxes), so fewer large, white elephant houses will be built and sold.

This is particularly so because baby boomers have to sell their family homes given their reported, meager savings. Pity the ultra rich and bankers, who thought inflation would reduce the real value of their liabilities and wages paid to employees more. LOL

Exactly. I’d love to get rid of the realtor business model.

I’ve used 2 flat fee brokers to sell in metro Chicago burbs, $400 to $600, they list in the MLS, etc, includes photos (yours or theirs) and you do the showings. Up to you to include a % if buyer shows up with one, however.

How you would do that?

Funny, but True!!!

Biden is looking to either minimize or wipe out those loans for select people so I wouldn’t count on that.

Those funds will come from brrrrrrr.

Regarding housing, as a landlord of several homes, I monitor this stuff for the zip codes my properties are located. Price on a few places have dropped, but these are fixers. Anything somewhat together (meaning I don’t have to spend several grand per item to put in an AC/Furnace, new windows, roof) is still pricey and WAY ABOVE what was going on during the Great Recession. Back then, I got homes below 100 grand So, I see NO DROP IN INFLATION. I went to grocery store yesterday and prices still up. Sandwich meat that used to be 7.99 to 9.99 a pound is 12.99 to 14.99 per pound. Four blueberry muffins that used to be 3.99 are 5.99. Same for a little slice of various cakes, I’m talking small squares. Those too used to be 3.99 and now 5.99. You will be hard put to find a decent frozen pizza below 4 bucks like the old days. The better ones below 5 bucks or even 9 bucks is difficult.

The great Peter Lynch years ago taught me years to use your own two eyes regarding financial conditions because many times the financial pundits totally got it wrong.

JK,

“Those funds will come from brrrrrrr.”

No, those funds have already been borrowed long ago by the US government were handed to the students who then spread it around to the education-industrial-RE complex. That money is gone and doesn’t need to be printed, and won’t be printed.

But those student loans are the biggest financial asset on the US government’s books ($1.65 trillion of “loans receivable”) which, under this program will have to be written off as a loss at least partially because at least part of them stopped paying interests and will be forgiven. So taxpayers will come to grips with the fact that they’re $1 trillion or so poorer than they’d thought. But then on the other hand, those students whose debts will be forgiven will be richer by that same amount, and so it all balances out, at the taxpayers’ expense.

Grisham does a thorough job of describing the student loan scam biz as applies to law schools particularly in ”The Rooster Bar” for anyone interested Wolf.

The ”story” is entertaining as usual, but the extent of the scam, apparently based on reality, is really sickening, especially for folks who save and slave to work their way through college without massive debt.

Unfortunately, this GUV MINT program has made college, in general, extremely disproportionately expensive these days, to the very clear detriment of our society in general, and particularly to folks serious about obtaining appropriate skills that our society seriously needs.

Wolf, what is your thought on having zero interest and a flat “administration charge” to cover the cost of providing a student loan, rather than the significant rates students are charged currently?

After speaking to many young borrowers, for many of them, it is the interest that makes repayment difficult.

If we want excellent affordable higher education, we need to gut the educational-industrial-RE complex and hang it up to dry. And start anew with a different model. The problem is not who pays for it; the problem is that the educational-industrial-RE complex is sucking the lifeblood out of everything.

What’s another 1 trillion at this point, know what I mean?

College costs are massively overpriced. Why does a Chicago retired Prof get a $76k per MONTH pension? My degree cost $20k for four years, paid it working weekends. Go to a State school, stay away from Ivy league trash.

Does anyone have a good sense on where rates and prices go from here? I’m hoping to buy a home this fall and I’m wondering whether…

a) Rates will stabilize around 6-7% and house prices will come down moderately during the spring/summer, since few places will sell at current prices? Or…

b) Mortgage rates continue to climb, driving prices down further?

I’m hoping to buy near Dallas, and I’m truly grateful for any insight from you guys.

You cannot look at mortgage rate independent of house price. When you look at ot in combination, here is the most probable scenario.

1. Fed won’t Pivot soon!

2. House prices will come down significantly.

3. Mortgage rates may remain steady or go up slightly.

4. Overall, it will be very beneficial to wait as house price decrease with outweigh the small rise in mortgage rates.

5. If layoffs spread, expect even more serious corrections in House prices irrespective of mortgage rates.

Just go on the various real estate platforms (Realtor.com, Zillow, etc) and monitor those zip codes that you are interested in moving to. Do you know this? If not, I’d suggest do a trip there a look around where you’d like to live. You will see with you own two eyes if you monitor the real estate for those zips. These people don’t know. Those charts mean nothing to me unless I’m watching myself. This doesn’t require big, brain power. :)

All I do is I follow the prices on a daily basis. The websites will note when prices drop. You can usually see the sales history of the property and monitor price per sq ft per condition of the property you like. What’s interesting, the phone texts are starting to come back with people looking to buy my properties. They somehow get the info publicly. I’m not the only one. So, investors are still buying. I’m sure a lot of these guys have or work for investment funds that buy houses for cash so they give you a lower than average price to seduce you to unload. That’s what a guy told me years ago when he was curious to see what someone wanted for his house. Lower ball cash offers.

You can either pay high rent to someone or pay a mortgage for yourself. Your choice. I’m older and years ago, a house was an investment, but not a get rich quick scheme. it was a place to hang you hat. Even if you got a higher mortgage, you can refi if rates drop. I would make sure you can avoid a prepayment penalty as that’s what I did. Good luck.

It is real important to be flexible with your investing approach. There are good times for different investments and bad times.

It is clearly a horrible time to purchase a home. Prices are still very high because the inventory has not built…yet. Give it time. The demand is remaining low and I believe will get even lower as declining prices continue.

There are always people who try to catch a falling knife. In real estate, where buyers are leveraged, another 10-15% decline can force many people underwater and combined with the potential for a recession, this is not a time to be buying exposure to the single most leveraged asset class in the world (I think).

count me in..I waiting here like a patient vulture in the Collin County are..I’m a first-time buyer and I’m scared to dip my feet right now ..although I could make a substanial downpayment..All the money is losing purchasing power with inflation..It’s like I’m stuck between a rock and hard place.

There are people who think that if they can continue to make payments on a home they can ride out the downside. The problem with that theory is it might take decades to get back their equity if prices drop for the next 2 years (which is the typical real estate cycle).

I have heard that as baby boomers go into retirement and downsize housing needs, there is going to be a demographic decline in the need for housing. Maybe that is why certain people want alot of illegal immigrants to fill up the housing. I cant believe many of those illegals have the money to pay top dollar for housing.

“all the money is losing purchasing power with inflation”

well, I look at it differently. If you can buy the same house with fewer dollars in the future, then money is gaining real estate purchasing power. just looking at the bright side I guess.

@yubeie

Collin County is where I’m looking too. It seems like a very nice place to live.

Best of luck to you! Maybe we’ll run into each other someday.

I think you are looking at it cockeyed. You shouldn’t plan to buy at a certain time. You should buy when the time is right, and you don’t have control over the timing . Let the market come to you. Have patience. That’s how to build wealth.

Don’t listen to most realtors, who like to say it doesn’t matter when you purchase. They say, if you live in a home for 10-20 years, you won’t lose money. What their incapable minds fail to understand is that you’ll lose out on gains. Who in their right mind would put a huge wad into an asset that won’t appreciate, and might depreciate? Better to put that money in something safe, so it’s available to capture gains when the time comes.

In other words – buy low, sell high. Don’t buy high, and hope to break even after 20 years.

You have to live some where though.

Rent.

Like Tesla, Facebook, and Bitcoin.

I have never-ever-ever found anything to buy low and sell high-ever! and I’ve been looking for a long, long time….Will someone please tell me what do you buy that is low and sell when it is high so I can make money from it…Thank you very much.;

Been in the buying and selling home market for 40 years with many purchases in markets like this one . Wolf is right this takes several years to work the inventory through the speculators washouts. Unfortunately for you but the good news is short term tbill rates are 4.35 percent so be patient keep building equity from your downpayment and wait for a market value to come to you. Buffet sat on cash for a decade before he bought OXY deep value.

6-month T-bill is 4.8% today.

I wouldn’t go much further than a 6-month T-bill because the radicals in the House are not going to let the debt cap be raised which should crash the markets, sink gold (not raise its price because a default with be so deflationary), spike interest rates, furlough govt. workers and social security, and possibly destroy the reserve status of the dollar.

They want to destroy the government and bring chaos to a theater near you.

Yes, radicals, what are they thinking, the debt limit must always increase, and faster than GDP or anything else.

Be careful what you wish for… I’m sure that China, No. Korea, Putin, the mullahs are salivating right about now.

You only need a few Republicans to break with the radicals, and the debt ceiling will be raised.

Oh, the ol’ debt ceiling ruse. You’re still falling for that one? It would appear so given your alarmist last sentence. Are you cowering in fear under your bed covers? Get a hold of yourself and stop the paranoia.

Might want to call the nurse to change your soiled britches, lol!

So trying to restrain out of control self destructive government spending now makes you a radical? Orwell would hang his head.

Such a false narrative that not raising debt ceiling creates default. Gov is still receiving tax revenue; it simply will be prioritized. Clearly you make interest payments top priority. The fear mongers keep this misinformation alive.

Hi Captive,

The first place to start is Wolf’s 12/27 article, “The Most Splendid Housing Bubbles in America, December Update”. Look at Dallas. Prices up about 50% from 2011 to 2019 (tracking the unwinding of the earlier bubble and the ongoing decline of mortgage interest rates). During the COVID housing blowoff, (roughly mid-2020 to June 2022), the index went from roughly 190 to peak at 310. By my eyeball calculations, that’s 60%+ in two years. Per Wolf’s calcs, the index is down 5.6% in 4 months. And 2.1% in the last month. Looks like a textbook “blowoff top”.

Now also consider that interest rates have moved from roughly 3% to roughly 6.5%. The interest rate increase translates to a monthly payment increase of roughly 50% (e.g. $100k loan is $421/month @ 3%; $632 @ 6.5%). This is one (but not the only) driving factor in the decline in prices.

The vast majority of individuals finance their home purchase and the driver in purchase is NOT the price of the house but the monthly payment (note – I’m not saying that the house price isn’t a factor, it’s just not the prime factor). So if the most I can afford is $421/month, the house price will need to drop from $100k to about $66.5K for the same monthly payment. That’s the interest rate factor only.

This is a very basic analysis: you can make it more complicated if you want (wages are up, if the house price is lower PMI and Insurance may be less, RE taxes will be less, so maybe the monthly payment can move by a bit). But I think that a retreat to a 2017 price (or possibly even lower) is likely. And don’t forget that these things tend to overshoot on the way down as well as up.

I’d take any comments about rate reductions, pivots, etc with a huge grain of salt. Chairman Powell has clearly said that rates will be higher, for longer, than he originally anticipated. Since he started raising interest rates he’s done exactly what he’s said and I would hesitate to go against him (and the FED) right now (remember the old saying, “don’t fight the Fed”.

I hope this is helpful. I’m not sure what percentage decline you consider moderate, but if I had to guess I’d say that Case-Schiller will be down about 20% from it’s current level by next fall, and maybe back to 2018 by 2024.

Thanks Eddie (and everyone else who responded). I’d be happy as heck if prices dropped another 10% between now and October, let alone 20%. I’ll keep my eye on the markets and on this site, and if houses are still too pricey by the fall I’ll probably rent for a while when I get to Dallas. I’m looking for a house to live in, not just an investment , and I don’t mind being patient 🙂

Captive-

My brother runs a mortgage business in Dallas and at Christmas he didn’t seem to have a clue where rates were going. Generally up but not tremendously so was the impression that I got from him.

That said, the COVID overhang is going to put pressure on housing prices over the coming two years. A lot of people who weren’t making payments for the last couple of years are going to have to exit their houses when they can’t work something out with their current lenders. THAT will pull the entire market down somewhat.

I have never gone wrong with what I call the “3 D’s” of real estate investing. The best deals come from Death, Divorce, and Dislocation… when sellers are just unloading their houses for whatever they can get for them at the moment.

Good Luck to you!

nailed it.

Look at Accuweather monthly temperatures for Dallas this past year (unless you’re already from Texas or Arizona). All of 2022 is there (“monthly” tab). Dallas had approximately 50 days with highs 100 or above and 120 90 or above.

I lived near Dallas for 11 years. I liked it except for the very long summer and a few other things.

Good restaurants as with any major city.

Housing was affordable there then mid 80s to mid 90s. Ambiguous sentence.

Timeframe and new house prices !

Lost $ on mine though.

I had some bad experiences that aren’t relevant here.

Check out AccuWeather though. Its pretty humid April thru June but when the extreme heat hits the humidity backs off.

November was my favorite month…oh how I yearned for November.

Thanks for the heads-up, but I’m actually moving to Dallas from Canada because my wife gets very depressed during our winters here. She needs to be somewhere with more heat and, especially, more sunlight, and I’m willing to handle long, hot summers if it means things will be easier on her.

(She’s already an American citizen and immigrated to Canada to be with me many years ago. I’m now waiting on my own immigration papers to clear so we can move back for her, which is why we’re looking to buy this fall).

I won’t miss six months of snow shoveling every year. Scorching summers could be a nice change of pace. At least it’s a new problem LOL.

I’m originally from NE Ohio… know about dreary winters. Lived near Seattle. Ditto. Surprisingly….

Spokane – maybe its just where I live nestled between hills – seems even more dreary than Seattle in the winter.

You might try Colorado Springs or some other southern RRocky Mountains destination. Good amount of sunshine year around… minus the extreme heat.

I think they average 35 to 40 inches snow. Probably varies a lot by year and exactly where you live. Supposedly the snow often melts fairly quickly since it warms up in the day w/ sunshine.

Cold nights though.

Housing is quite expensive though not as bad as Denver.

I moved from Seattle (Lynnwood) not because of the dreariness or chilly weather (annoying in June) but cost of living and being harassed.

Good luck with Dallas or wherever you move to. B.t.w. I do not like the climate in Spokane either. May and June good months… the rest not good (i used to like September but now too much wildfire smoke).

Fed interest rate policy really affects housing and there is a pretty substantial delay. Now is the time to do your homework about where you want to live and what price will make you pull the trigger.

Some say don’t catch a following knife and the safest thing to do is let a market bottom and then start the upward climb. It’s ok to be 6 months late on a true bottom.

Good point OS re six months late,,, or even later.

We had to move to saintly part of tpa bay and sold out of the farmstead in flyover in ’14; buyer reneged, and we ended up moving in 2015.

Many houses in the desired area of Saint Pete were in the $50K range in ’14, but had only gone up $20K or so by ’15.

IIRC, houses in our target area had bottomed in 2012-13, but not much lower than ’14-’15…

IF you absolutely ”need” to move sooner, per the very clear instructions of JP Morgan, buy on the way down IF AND ONLY IF you KNOW you can hold through the bottom…

This economy cannot survive without the printerrr. It will come out by the end of the year, driven by some financial or geopolitical crisis. The scheme is global now, there’s no going back.

Just wishful thinking. Enjoy while you can.

For now, the trajectory of mortgage rates is down. The Fed will slow its FFR increases to 25-basis points in the coming months. The economy will continue to slow down, slowly.

Once the 30YFRM reaches 5.5%, housing will begin to stabilize. Once it gets to 5%, prices will begin to creep back up.

What is concerning is what happens in 2024, since there’s a good chance that a soft-landing leads to a reversal of inflation next year, although not back up to 9%. But a reversal from 4% back up towards 7% is a very real possibility.

Until there’s some reasonably constraints placed on government spending or a real recession, core PCE inflation isn’t going below 3.5% anytime soon.

You should Google “case shiller dallas” and consider that it may take years for prices to come down. It updates monthly

Just thinking out loud going forward.

-The longer we have this collapse in mortgage originations the bigger the queue of future home buyers becomes. Even though sales have dried up does not mean people do not want a home. They are just waiting for prices to bottom or interest rates to drop a lot so they can hit their monthly mortgage payment target.

-Inventory is still low in my area. Inventory has increased but it is still down 50% from the average. At the peak it was down 70%.

-A Realtor in my city said there are plenty of home buyers looking to buy but there is no inventory. Maybe that could mean no affordable inventory.

Going forward, when housing prices drop or interest rates drop or a combination of both, there is going to be a rush of pent up home buyers?

“but there is no inventory”

This lie never dies.

ru82,

Item by item:

1. Nah, that’s never how it works. The selling hasn’t even started yet. There is a huge overhang of potential sellers that are still waiting for this to go away, they’re still waiting for the return of 3% mortgage rates. At some point, they’re going to get washed out; happened during every housing bust. He who panics early, panics best — but they haven’t learned that yet.

2. “Inventory” is low because potential sellers with multiple homes, money-losing vacation rentals, vacant rentals, etc. that they want to sell are still waiting for this to go away. I know several of those myself. The overhang of this “shadow inventory” is HUGE. Eventually, every housing bust brings out the shadow inventory. But it takes time.

3. Realtor in your city is a sales person, will say whatever. See item #2.

4. Not any time soon. House prices will have to drop a WHOLE LOT, and that takes time, and mortgage rates won’t ever go back to where they were — that was a once-in-ever opportunity that is now gone because it led to the worst inflation in 40 years.

##1,2,4 are right on.

#3 is the most SPOT on.

2banana,

From personal experience, you’re absolutely right.

All of a sudden, one week or less, there are now several homes for sale in the hood we walk daily. Mushrooms!!!

Last week only one rental, (nothing for sale,) and it’s rent reduced twice and owners throwing tons of $$ to bring it up to modern at least somewhat, though it needs a ton more IMO to be at current average standards…

“Mushrooms!!!”

The fun kind, or just…?

Wolf,

Is there any data on the % of Single Family houses that are primary homes vs second, flipper, or investment properties? Tax data must have this information.

That would be good data to determine the overhang you mentioned above.

I think the overhang is large and many took their Pandemic money and invested into a rental property or second home.

I keep hearing anecdotal stories of entire streets of houses turned into AirBnB’s during the last few years. A few co-workers bought houses in the suburbs but kept their original house/condo in case they wanted to come back. They are renting their old house/condo.

There are a couple of places to check AirBnb stats such as how many in your area, vacancy rate, rent rate.

airdna It will tell you how many, daily rent, and all kinds of stats. I think the other is mashvisor

Thank you Ru82,

I did a quick check on AirBnB for my area. There are 1500 houses listed as short term rentals. Since my area only has about 15,000 houses, this is significant (10%). I didn’t look at VRBO.

It is true that some of the AirBnb’s are ADU’s or spare bedrooms on primary homes.

I have no idea if the AirBnb properties are highly leveraged houses purchased since 2020. If AirBnB booking rates crash and 10% of the houses in this area are listed, prices may fall quickly. However, everything moves slowly in RE.

An AirBnb booking drop would cause mortgage holders to initially offer the properties as a LT rental. This would drive LT rental rates down first. When LT rental income doesn’t pay the monthly expenses on a leveraged house, then prices will start falling. LT landlords will see this hit first. Price drops may take awhile.

Anyone who purchased before 2020 has at least a 30% cushion and an extremely low mortgage rate.

Thanks for for the feedback. I like to throw out stats out to see what people think.

ru82, if the momentum of price deflation gets real traction, then we’ll see the mirror image of the housing boom heading in a southerly direction: great reluctance to buy if you think it’ll be cheaper next week.

Many of the people who refinanced during the pandemic and spent all the money of personal consumption are going to pay for this decision. When prices decline 20 to 30% on their home and they are underwater and lose their job in the next recession they will be SOL (S$it out of luck).

#2. Also of impact: Wolf, Reventure Consulting, and others have sptly demonstrated that apartment construction is as great as it has been since the 70s and 80s. If rents fall this too pressures house prices.

#4. But then pandemic free money and external supply constraints also contributed to the inflation spike… so I’ve been lead to believe. Minus those two one can only speculate (it seems) how bad inflation would have been if rates had been at 3% w/o those 2 inflationary causes.

sptly => aptly

yes, multifamily construction has been booming close to the record levels in the early 1980s. But now the population is growling a lot more slowly than back then

Multi unit construction is a huge factor, and will eventually impact single family prices as well. A glut of apartments, would result in lower rents putting pressure on SFR rentals.

While large commercial landlords can afford multi year losses, most small landlords cannot. Once rents drop enough to cause negative cash flow, many will need to sell.

What I am seeing in my area, is a lot of vacancy in newly completed apartment projects, but because of the long term nature of these commercial projects, they are still breaking ground for new ones. It seems as if commercial apartment developers are much slower to react to changes in the economy than the home builders who are already in clearance mode dropping prices to unload inventory.

There is another possibility when it comes to #4. Low rates, but limited supply.

A switch to a finite money volume without interests may enable central banks and governments to kick the can down the road for a while longer.

Side effects can be interesting.

I don’t understand the new companies like Arrived Homes. People are putting their money into houses (crowd funding) that are overpriced and expecting return from renting out these properties at $3,000 a month or higher. Folks don’t understand, they file bankruptcy and you don’t get your money back.

It seems like a lazy way to try to jump into the housing investment boom. Treat it like buying any stock. Buy it and forget about it.

Like stocks, if the company goes under, there are thousands of lawyers and others collecting their share before you receive what is left. If anything is left.

Wanted to post the financial I found to back up the comment – ie be like WOLF: Crowd Investing in Arrived Homes.

AS of June 30,2022

Consolidated

Rental income 723,399

Operating expenses:

Depreciation 332,889

Insurance 51,685

Management fees 122,269

Repair and maintenance 151,710

Property taxes 92,593

Other operating expenses 229,990

Total operating expenses 981,136

Loss from operations (257,737 )

Other income (expense), net

Interest expense (377,303 )

Total other income (expense), net (377,303 )

Provision for income taxes

Net loss (635,040 )

Gotta love that one track mind of FOMO only works like a one way street, when in reality and has been proven in history both in housing and other things, it works both way…

Then again I wouldn’t understand any house humpers or RE shills to understand or say it out loud. Some house humpers treat it like a religion, others probably know what’s on the other side and their paycheck is dependent upon them saying the opposite, just like all those “Finance” YTubers shilling for FTX..

In response to your first item, keep in mind that the majority of people finance their house with low down payments and 30 year terms. If their current house value is dropping alongside their target house value then they will still be hard pressed to move homes, especially if interest rates are higher than their current mortgage.

Please define “Majority”. The volume of home sales during the past 4-5 years has been low, and 40% of homes are paid off.

“The longer we have this collapse in mortgage originations the bigger the queue of future home buyers becomes.”

Unless of course, interest rates “blow out” later which will happen if the interest rate cycle turned in 2020.

The demand inferred by your comments is a side consequence of the debt mania and cheap rates. How badly they want to buy is irrelevant.

“A Realtor in my city…”

Believing any realtor is a huge mistake.

What makes you believe that the rush of pent up demand will come before the rush of pent up supply? Many people have not been willing to sell their homes because they believe that home prices will only rise. That is the big fallacy. As home prices fall month after month, the incentive to sell will increase, not decrease. The lie that home prices always move higher will finally been evident and then people will once again look at the relative costs of ownership and renting, and make smart decisions.

Just wait for Spring and Summer for the homes to pile up on the market. People who pulled their home off the market when they didnt get their dream selling price will be coming back to compete with new sellers.

A Realtor is a housing shill, nothing more. Well, they’re also a leach which attaches itself to the transaction to take a cut of the proceeds, so there’s that.

*leech (who leaches the profits)

I may not disagree with this comment but this specific realtor is a longtime friend and has been in the business for over 20 years. Nothing to gain. I was just asking how business was going.

Her client list looking to buy is close to an all time high. Yes, she says inventory is low, but I think it means affordable housing (3x salary) inventory is low. She had an affordable open house in December. 56 people showed up. She was expecting 10.

I am in the midwest so things might be skewed. Prices have only dropped 2% from the ATH. Inventory is low. It is still about 60% lower than average. There are no vacation homes or 2nd homes in this area to sell as this is not a vacation spot.

“People who pulled their home off the market when they didnt get their dream selling price will be coming back to compete with new sellers.”

It depends why they are selling. Did they initially want to sell for million dollar gains so they could buy a cheap house in Mexico or a smaller, cheaper house in the US?

Or, are they selling because they can’t afford their current house due to cash-out refi’s, HELOCs, and job losses?

In case number #1, greed will subside and they will keep their house and continue to pay their low mortgage.

In case #2, they will sell in desperation (or foreclose).

My Sister In Law, was looking for a house in 2019 during the short housing dip. They looked at one short sale that made me lose faith in lending practices. This house was initially purchased in 2009 for an incredibly low price. The owners were able to Refi/Heloc the house to full value in 2018. When the short dip occurred in 2019, the owners threw up their hands and went to the bank and asked for a short-sale. They threatened to foreclose. I have no idea what happened to the 500K+ in money pulled out of the house. It was irresponsible lending.

“Going forward, when housing prices drop or interest rates drop or a combination of both, there is going to be a rush of pent up home buyers?”

I think you also need to consider that the status of buyers will most likely evolve going forward. Maybe someone who would like to buy now, loses his/her job in the coming year.

…when FOMO turns to FOLMJ (fear of losing my job). Has about the same effect as actually losing the job.

Good point.

Realtor said lol. Stopped reading after that.

Yep,the cue of future buyers is growing and inflation has reduced their savings and ability to purchase. So as inflation is still outpacing wages and draining the pocketbooks of those pent up buyers they’ll have to resort to credit cards to pay for groceries and they’ll slowly but steadily see their fico scores go down and their mortgage rates go up.

There is no little or no affordable inventory. Anything decent here is selling for top dollar, as if there were no interest rate increase.

We just did a 1500 sq foot brick ranch style just renovated top to bottom house in a good neighborhood, with good schools, access to transportation, and Metrorail just sold for 1.2 million. That’s over $800/sq foot The buyers were grateful to get the deal. The junk is sitting. Soon signs will be going on the undesirable properties like back in 2005/2006/2007. The rich are doing fine. the lower middle class are getting screwed. It’s a two tiered market.

Good, let it crash hard… still a long way to go in SoCal..

If nothing else, seeing this unfold as predicted by non RE shills is all the joy I need for 2023

I am actively looking for the right property for me. Small, rural, in good condition and close to family. With interest rates going up I can save about $3,000 per month toward the house price. They are just rolling over in my area, so if they start dropping at about $3,000 per month I think in a a year or two the savings curve and house price could intersect and I will be a cash buyer.

The payment never goes away ,taxes and insurance in Nebraska are about to make me move to low tax state = wherever that is

My sentiment exactly.

According to the last chart shown “Number of Consumers with Foreclosures”, I would say that these are the good times for existing mortgage holders. Going forward, I can’t imagine that chart looking any better than it does right now.

Ah, federally subsidized mortgages for 30-year fixed terms at criminally low interest rates. A gift that keeps giving. There’s almost no incentive for these people to sell now. Combine it with boomers dropping out of the workforce and unemployment staying stubbornly low. Sounds like house price drops will be a long slow process unless some other economic fundamentals change dramatically.

Yes, and I think inflation will stay high for a long time.

Escalating property tax increases,and insurance premiums will eventually force you out of house, told my kids we would all be living in one house laughed at me ,ask my grandma as this was her circumstance during depression.But they had a 80 acre farm on which 15 family members survived.

Actually, it doesn’t make sense to own a leveraged asset if it is dropping in price, no matter what your finance rate is.

When rates were low, chances of home price drops were also low. When rates are high, chances of home price drops are high. People getting the benefit of low locked mortgage rates may be influenced to ride the housing price downturn – to the bottom. That would be a big OUCH!!

Wolf, you have a typo of a missing word. you can delete my post

that it IS shutting down

With housing prices still in the stratosphere, the slight decline in mortgage rates we’ve seen clearly are not enough to slow the decline in housing prices. Unless we actually dip into a recession, mortgage rates likely won’t fall much further, allowing for sustained pressure on prices.

With that being said, there are still buyers out there (huge number of people in their 20’s and 30’s still at prime buying age). Demographics and a strong job market should provide a floor under prices. Until we see a dramatic increase in the number of distressed homeowners (Which Wolf proves to be near historic lows) I don’t see this correction in housing prices deepening too much further. Those rooting for a housing market collapse need also to be rooting for a major economic recession. At this point a collapse in employment and wages would far outweigh any subsequent decline in mortgage rates.

My only comment is that home prices mainly went up astronomically in the last 3 years so people, once resigned to the new reality, will drop down to the prices of 3 years ago. I don’t think it will be that sticky.

Good points JoshWX.

The FED would like housing prices to go down but they do not want a crash like in HB1. HB1 was not caused by the FED and cheap money. It was caused by Cheap money from the banks and investment banks who could sell the MBS to investors who thought they were buying a no fail investment because of CDS and tranches.

IMHO…I think the FED would be okay with up to a 20% in housing decline but will pull out the stops to prevent anything further and prevent jingle mail and a downward spiral.

Stonks have to drop substantially for the selling to accelerate. Same people own stonks and multiple homes. As long as stonks/cryptos are stable, they can manage without having to sell their second or third homes.

Waiting for Godot

Oh.

As long as cryptos are stable???

Lol, caught that too. Wonder what color the sky is in his world!

Even with all thats happening btc is hovering at 17k. That’s pretty stable isn’t it?

Only if your timeframe is 2 months. BTC’s 52-week range is 15,599.05 – 48,086.84. That’s not so stable.

QT has a looong way to go if you expect the party to end and it’s happening slowly

Bitcon down massively and that’s the best out of the 10k or so garbage coin scams . Gotta love it

Just looking at stocks I can value and houses I see, prices need to come down by roughly 20% – 35% for both to reflect current rates.

Depends HUGELY on location OS:

If prices here in our hood in the saintly part of the TPA bay area drop 20%, ours would still be approximately FOUR times what we and several now friends/neighbors on the same block paid in 2015-16.

FWIW, all the houses were built in 1950 with exact same floor plan, though some ”blueprints” were upside down, so mirror image.

I’m guessing about 50% down from peak around here is very likely, though also likely to take couple or more years.

More like 50%. Need to go back to 2015/16 level.

But the Corona gain has to drop as fast as possible. Other can take some time.

This is true. Stocks need to drop another 30% and inflation needs to remain relatively elevated for some time. Hitting the working class does NOT solve the housing problem as the pressure needs to get to those currently holding said inflated assets to get them to “give them up” at a lower price (homes, stocks, etc).

Alternative to housing, US stock market:

I realize there are the economies to consider and other metrics but many international mutual funds sport P/Es in the 8 to 12 range. And 10 year returns of only 5 to 7 percent. Both historically low.

They have had a good 3 month run perhaps due in large part to currency fluctuations (?) but still may be cheap.

Inflation is eggs at 4.00$ a dozen =hyperinflation

Nah little bug:

Inflation is eggs for $1.00 EACH,,, possibly coming soon, as it has been many times in the past when a dollar then was worth about ten today…

Clearly documented in various places over the last century…

Many folks doing the city chicken thingy once again, at least around our hood, where no chickens were seen until recently???????

I agree with you Wolf. Be careful with agents. I haven’t found one that had my interests truly at heart. They’re just showing you the property and they “might” mention something to bring to your attention. Something out of 100 things. haha. Also, property inspectors for the sale can be good, bad or ok.

I’m sure YouTube has videos how to look at things yourself and if you got a friend that has some construction experience or handy man then bring him along for the house you desire and treat him to a nice lunch for the effort. Sometimes things are missed by everyone.

Spot on, jk. You need multiple inspectors.

Rudimentary knowledge of hydrology helps as well.

Most are liars. I’ve got a complaint against one now with the real estate board. They are worthless. Time to change the business model to one that eliminates realtors.

My realtor colluded with the selling realtor, and then paid off the inspector she recommended, who wrote a phony report. The sellers were an older couple paying the full 6% commission (they didn’t know any better) for a 1.5M home, and both realtors saw dollar signs.

By the time I figured it out the inspector had shut down shop (I assume to reopen under another name). I looked into suing the realtor but didn’t really have proof, and figured the cost and time of litigation were more than the cost of fixing the house’s problems.

So I learned:

– Never trust a realtor

– Will be using Redfin or other fixed salary realtors in the future

– Hire my own inspector – don’t let realtor “make a recommendation”

Yeah i think this happened to me also. Must be fairly common. My agent likely colluded with the sellers agent AND the inspector i choose at random to hide a slew of issues. Notably a horrible pest problem among many others. I suspected this even before closing but didn’t really care since the house was well under 200k and has a great views of the mountains. The pest problem took YEARS to get under control. Will be more careful in the future…

100% agree. Many realtors are fraudster, not all. We need to change the business model and eliminate the realtor business license scheme. I don’t need them to sell or buy a house.

The Realtors who handled the Sale and Purchase of my home 2 decades ago committed 26 ethical violations. I will never trust a Realtor again.

How about let’s get rid of car dealers too? Tesla has proven that the manufacturer can sell directly to the consumer whether new or used. All these 20th century middlemen need to go the way of the dinosaur. They are just extracting wealth from the working & middle class

A town I’m looking at to live had fifteen to twenty homes for sale just a couple of weeks ago. Now there are only six.

I suspect people are taking the homes off the market in hopes that sales pick up, rather than sell them for a loss?

Yes, a ton of inventory always leaves the MLS around the holidays. Nothing unusual there. People are taking vacations, traveling, visiting with relatives, etc.

Expect to see all this shadow inventory relist in months ahead, AT LOWER PRICES.

Thanks! Still learning.

Jon,

This ALWAYS happens over the holidays. Right before Christmas, many sellers pull their homes off the market and relist them during selling season in the spring.

Thanks, Wolf. That makes a lot of sense now that you and Bobber have explained it.

I’m in the process of buying a house, for better or worse. I feel a bit insulated from the market dangers as I sold my house last fall close to peak freenzy. The house I’m buying belongs to a real estate agent who bought it in ‘19 as an investment. He put it on the market two weeks ago just over the analytics pricing. In a week he reduced it to just under and a few days later took the first offer on the table without countering (actually the offer was through another broker and he gave me the option of matching it as I’d looked at the place three times). That’s indication enough to me the market is indeed going south and the pros know it.

Back just before the GFC, 30 year rate was around 6.7%, then drifted lower and lower. I think we’ll see that again, in conjunction with falling home prices and crashing equities. A Fed pivot towards September will move glacially into 2024, as more and more people feel consequences of illiquidity.

Nostradamus

This is for you, Aficionados of Mob Memorabilia, Paraphernalia, Trivia and Substantivia – peppered up with hard RE facts.

During the early ’20s things in Chicago were sizzling hot. Johnny Torrio moved all his 401(k), amounting to $40M gold dollars, to Italy and escaped thereto. Big Jim Colossimo was gunned down. Irish gangs were attacking from the North Side…

On one of these wonderful Manhattan evenings somebody passed Al Capone (who was perfectly happy in Noo Yawk) a message: “Al ! You wanna drag yo’ fat lazy a$$ to Chicago and straighten things out ? BTW we are not asking…”

Al chose long 800 mile ride to Chicago over short one-way ride to Hudson River.

Nobody met him at the train station in 1923 because, as they say, “Curiosity killed many a Chicagoan Cat”. The only exception was wildly enthusiastic realtor Kunal who sold him 2,860 sqf solid brick 2 story house for $5,500 – the very same day of Al’s arrival:

7244 S Prairie Ave, Chicago, IL 60619

After 92 year long hiatus it was listed on MLS for $176K. From 2016 to 2019 there were no takers. Then it was re-listed for $100K and EVENTUALLY sold…

Oh, and Al’s favorite toy – Colt M1911 .45cal semi-auto – was sold for $800K+ at about the same time. 8x times more than Al’s house…

Newsweek: “Al Capone’s Favorite Gun Sells for $860K at Auction”

Food for thought my friends.

And we need Kunal and his ruthless RE cheer more than ever !!!

Now, demand for mortgages have plunged, but prices (interest) do not drop? It look like the market is not working here, if demand drop should not prices also do so to keep sold volume up?😉

Other industries are expected to lower prices if demand fall, so why not the lending industy?

Or is that part of economic theory not quite well founded? Could it be that cost to the provider carry more weight than volume sold?

There is no price discovery in mortgage lending. The government has distorted the price of mortgage credit entirely.

If there was a real mortgage market where lenders actually took full credit risk as they should, mortgage rates would be much higher.

No one would ever lend their own money at fixed rates for 30 years to so many actually marginal borrowers on such inflated collateral, especially at recent rates.

You hit the nail on the head. We should ban disband Freddie and Fannie.

Another nice idea would be to cut the maximum mortgage term to 15 years. That would allow people to pay for their home in 15 productive years and prepare more people for a solid retirement. After 15 years people could save more money for retirement, instead of paying for an overinflated piece of property.

g.tv: check the history of mortgages in the U.S. You were born in the wrong era. You’re dream came and went: mortgages were renegotiated annually, they were adjustable monthly, the homebuyers would have to put in more than 50% for the downpayment. The Great Depression changed the nature of mortgage loans. And that was changed again, dramatically, after WWII.

Get yourself a time machine. Houses for the average citizen in SoCal were about $2000 near Santa Monica.

You may not have had a refrigerator though…

Hell, we don’t even have to start out with anything remotely radical – just lower the maximum loan that can qualify for conforming status.

Fannie, Freddie, etc. ratify and perpetuate the insane asset price inflation in housing by always/always/always ratcheting the qualifying maximum up.

*That* is insanity personified (everybody at those institutions knew exactly (*exactly*) what would happen if the Fed ever (*ever*) let rates anywhere near a natural level. => price collapse, ultimately a foreclosure wave, and inevitable huge taxpayer losses/ZIRP driven inflation round #17…

The interest rate repression that we saw after the GFC was very similar to the GI bill when the fear was that returning Vets of WWII would cause a massive depression. So, in effect, mortgages were no-money-down and exceedingly low, long-term to stimulate the economy. Unprecedented at that time.

You’re right AF that there isn’t true price discovery, but, unless the Fed has to jimmy the rates to prevent an economic collapse, the bond market will keep mortgage rates somewhat honest.

Currently, the majority of all 15 and 30 year fixed rate loans are owned by Freddie and Fannie and are backed by the US Government.

The government/Fed sets the rates and accepts the risk.

I think if the government let the rates follow the free market and didn’t back loans, Augustus is correct the risk would be too high for lenders and rates would be very high.

Home loans would likely switch to an adjustable model where the lenders would not be locked in at a fixed rate for 15 or 30 years.

All mortgages would be adjustable (I believe this is the model Canada and Europe use).

In Canada there are variable rate mortgages but also fixed rate mortgages for relatively short terms by US standards — generally between 1-7 years with 4 and 5 year terms being the most common.

The real customers of mortgage lenders are the purchasers of MBS and the product sold is the mortgages. They have to raise interest rates on mortgages to get investors to buy. Rising interest rates reduce the number of mortgages they can package and sale until prices normalize and they still have to compete with 10 yr bonds. They’re between a rock and a hard place.

I hadn’t read your post, M, before I replied above.

Is it really possible for anyone to earnestly conclude that Mortgage Delinquency and Foreclosure rates falling well below the levels seen at the apex of Housing Boom 1 are positive market indicators.

They clearly display the scale of the problem. They are not markers of stability.

A fool’s paradise, courtesy of easy money.

It’s another government induced distortion.

I think the low foreclosure rate now means this time is different than the 2008 GFC. So far…..

I think Wolf’s chart on foreclosures is very interesting. Note foreclosures started to ramp up in 2006-2007. This was when HB1 was inflating.

We don’t see that yet this time. Possibly because people have very low fixed rate mortgages this time with 20% down. 2006-2007 was notorious for no down, no-income, adjustable rate mortgages. Adjustable mortgage rates were also increasing from 2006-2007 squeezing people with these loans. It is different this time. People are more secure with more down, more income, and a low fixed rate.

I could argue that anyone who purchased a house before 2020, has at least a 30% equity buffer and if they refi’d in 2021, they have the lowest fixed mortgage rate ever recorded in US history. They will likely not foreclose as long as they keep their jobs and housing does not plummet more than 30%. This time is different than 2008.

It is different this time “so far”.

Fixed rate mortgage holders understandably believe they are insulated. They are on the right side for now of loss-making terms but they haven’t escaped the eco-system in which those losses manifest.

The 30% you refer to is vaporous mist.

The brief phenomenon of the delinquency rates of HELOCs exceeding mortgages, foretells a corrective spike in mortgage delinquencies.

It is different. Maybe it rhymes.

Housing inventory and vacancies were rising from 2005 to the peak in 2007 at the same time house prices were rising. Inventory for sale rose from 2.4 million to 3.9 million during this 3 year period. Rental vacancies also went up about 30% during that time

This time housing inventory dropped from 2.4 million in 2015 to 800k in 2023 while house prices rose. Rental vacancies have also dropped. Those are two interesting differences.

The one constant is price rose faster than income making home affordability drop. Dropping interest rates meant income did not have to increase for one to chase higher prices. But that is over. HB1 was from loose lending to subprime borrows and speculators. This time it is the FED providing the liquidity via GSEs artificially low mortgage rates. Both periods are bubbles. It will be interesting to see how this bubble pop plays out. How far does it drop? When does the FED help to stop it?

The FED could not stop HB1 but they mopped up the old debt with QE and provided cheap money to help buy up the houses. They now have open funding tools since 2010 to purchase anything as needed.

I am not sure the FED will want a housing crash like HB1. They want prices to come down but not crash and cause jingle mail.

Grab the popcorn.

Since Wolf’s data only went back to 2016, I went online to see how things fared previous to that, particularly during the 2008 bust and found that during 2007-2008, there was not the same type of bubble in applications that we saw in the recent past. But the applications also didnt fall down to the level we now see.

My hypothesis is that last time around prices quickly fell and lots of distressed homes were being sold. Interest rates were also being suppressed, so that made the mortgages even more affordable.

Last time around originations saw a spike in 2009, as the low interest rates and low prices and ample supply of distressed properties gave buyers an incentive to purchase.

Dynamics are very different this time. Demand will remain low for quite a long time until prices are much lower.

ignore what i posted above, i was looking at the refinance index, not the mortgage application index.

gametv,

This is the only comment section I visit where people are quick to self-correct. I think it’s about fixing it before Wolf does ;)

I really appreciate the comments here. Many knowledgeable and articulate posters.

Can’t wait til tomorrow morning, when inflation figures come out. If memory serves me correctly, December service prices were through the roof, fuel was down, rents were down slightly and everything else stayed about the same.

The fed thinks they can slam on the brakes and stop the front of the car (housing) while the back end (the rest of the economy) keeps rolling along at 70mph.

All hell breaks loose tomorrow, along with pivot hallucinations.

Current expectation is 0.0% MoM for CPI and 0.3% MoM for core CPI on Bloomberg. Cleveland Fed inflation nowcast has theirs at 0.12% CPI and 0.48% core CPI (both month over month).

Anecdotally when shopping after Christmas I saw noticeably higher prices than Thanksgiving week and cyber week. Manheim wholesale used auto prices were up 0.8% month over month in Dec from Nov. If CPI comes in at 0% MoM or negative I’ll be shocked.

January has a lot of price increases kick in. Both wage adjustments and retail from what I’ve already noticed less than 2 weeks in so Jan #s should absolutely be way higher than Dec in next month’s report, too.

The CPI for eggs is going to be a hoot tomorrow, for sure.

Did you mean “cluck”?

Pretty soon, eggs will be sold on an individual basis. And if you want bacon….by the individual strip pricing.

Still couldn’t find any of the free range grade AAs in the store. Too weird, this economy. Can’t tell the chickens from the owls

Late last summer, a neighbor on the alleyway built a chicken coop and has five chickens. It’s a nice set up and it works well.

But for years, there’s also been one a few houses up the alleyway, and it too works well.

Sort of crazy, but on my block in Longfellow, south Minneapolis, two families have chickens in their back yards to get fresh organic eggs — the old fashioned way — straight from the hen.

One detail: there is a requirement for a permit in order to do so, and the city sends out an inspector to give a license to the owners for approval.

Just stocked piled on eggs! LOL

WOLF, thanks as always. I know you are working on the CPI analysis. Wanted to say thank you and looking forward (excited) to read your CPI analysis.

An apt description in your second paragraph which illustrates the limitations of monetary policy when discord breaks out.

In fairness to the Fed, they will know a soft-landing is a fallacy. Saying it would hardly serve their cause. Who ever ran the plank?

I have no idea what inflation will reveal today but it will kickstart the market for 2023.

Housing in Canada is a religion. 500k for a 1200sf teardown where I live in Nelson British Columbia. Asking prices have not budged but very few sales happening. It will take defaults to get the ball rolling.

Religion sounds about right but not exclusive to Canada, also a cult in US and China and many other parts of the world…

This housing religion kind of reminds me of sciencetology, both cost you a lot of money and have you believing in silly things..

The core belief of that religion, is that you can borrow your way to prosperity. Never quite understood the math on that…….

Let’s hope it continues to crater. We can’t have these high house prices be the new floor.

HELOC’s will be making a comeback. My credit union is pushing them big time. No need for an appraisal, No issues with massive closing costs, No disturbing the low rate on your 1st Trust loan, interest is tax deductible if you use the money for home improvements. You can’t go wrong and you can’t get hurt.

that is how bankers get in trouble. mortgage originations are down so they push the HELOCs at a time when they should be tightening up the lending restrictions on them. this will end badly. I believe HELOCs are generally retained by the banks that originate them???

You’d be surprised by how many people are struggling with higher HELOC rates as it is. They are typically pegged to the prime rate (with a plus “factor” depending on CLTV and credit score), and depending on the amount of the HELOC balance, payments may have jumped several hundred dollars a month since the Fed started raising rates again.

Then again, this is primarily affecting people who had HELOCs in place before the rate increases kicked in.

Yep. That is always the next phase of a housing bubble. Tap the inflated asset (free money) equity.

IMHO….Banks typically put up blinders on how far the price of a house can drop regarding their LTV in giving out HELOCs. Thus making fees now on the HELOC is revenue that replaces the refinancing income stream.

Home prices will fall and yet the job market will remain strong.

Ridiculous.

Employers, except Govt. employers will be forced to adapt or die.

In tech, the adage was always, those cannot do the work manage.

And along came project management and the managing of boxes.

I have no idea what is in box A, but I do know that what is inside box A needs to be completed by X Date. I need to summarize this complex information so my boss who understands none of it can get his bonus.

2000, was brutal for tech workers, 2008 was even worse.

The Fed was able to lower interest rates and implement QE to combat both downturns.

As home prices fall people are still going to need a decent job to qualify for the available homes. The job market will remain strong, until it collapses, like it always does.

Here we go again. Doomsday real estate collapse talk here after 1) a stock market correction where the bottom is probably already in (at least for a while), and 2) where inflation has likely peaked and is on the way down. So there is NO guarantee that we will get the housing collapse that everyone here wants any time soon. And Powell could pivot when/if the data warrants it. So, yes, this collapse could possibly occur, but it’s not a done deal.

The “collapse” discussed in the article is of mortgage origination volume (home sales volume), and what it did to the mortgage lenders, and this HAS ALREADY OCCURRED and is in process. That’s not a prediction but a reflection of past events.

Yes Wolf I understand. I’m referring more to price, not volume. The thesis here is that further price collapse will be inevitable and will follow (lag behind) the volume collapse. I’m not sure it is.

How do the prices survive when people can’t get mortgages?

It’s curious to me that no one seems to be considering the impact of climate change on values rising or falling, and where.

On an unrelated note, I had a realtor tell me, and I’ve personally observed in several markets, that well-priced houses under 200K aren’t being affected as much by the mortgage situation. And I’ve seen many houses at this point, under 200, that look like excellent deals based on recent prices recently go pending very fast. Meanwhile, houses over 200 are just sitting.

I’m not a new RE investor but I’m fairly new to this level of analysis. What could be the reason that houses under 200 (again “well-priced,” based on recent prices, are still flying off the shelves? Maybe those with cash are worried that the lower priced houses will continue to rise somehow?

But it also seems to me that if a house “worth” 300+ sits and sits… Eventually they will reduce the price, therefore driving down the 200 and lower houses even further.

Is there something about house prices under 200 that would insulate them from this mortgage situation? 🤔

And that’s actually been consistent for several months in what I would consider good and bad areas as far as climate impact is concerned. A “good deal” (again based on recent prices) for 80-175K? Gone in a few days. I’m never sure whether to believe “we have multiple offers.” But they have something because they sell.

But many of these look like they’ve already reduced at least 20% before listing.

Haha..must be Kunal from another mother..or Dr Yun in dusguise

Good comment; I would not count on a real estate collapse. Might just be downward bias of prices or price reductions of 25-30% and prices would still be high, especially with higher mortgage rates. Sellers can’t sell, many have great (low interest) mortgages, and buyers can’t buy, because of affordability. We might just have very low volume for a long time. I would think realtors may have it very tough, and many will be have to find other work for income.