Services are nearly two-thirds of consumer spending. That’s where inflation is now raging. The Fed has been talking about services for months.

By Wolf Richter for WOLF STREET.

Nearly two-thirds of consumer spending goes into services. Services include housing, insurance, healthcare, education, travel and hotel bookings, subscriptions, streaming, telecommunication, haircuts…. And this is where inflation is now raging. This is where inflation has gotten entrenched, while prices of durable goods are unwinding the pandemic spike, and while energy prices plunged, and food prices slowed their increase, according to the CPI data released today by the Bureau of Labor Statistics. Month-over-month and year-over-year:

- Services: +0.6%; +7.5%

- Durable goods: -0.8%; -0.1%

- Food: +0.3%; +10.4%

- Energy: -4.5%; +7.3% (gasoline: -9.4%; -1.5%)

- Core CPI (without food and energy): +0.3%; +5.7%

- CPI overall: -0.1%; +6.5%.

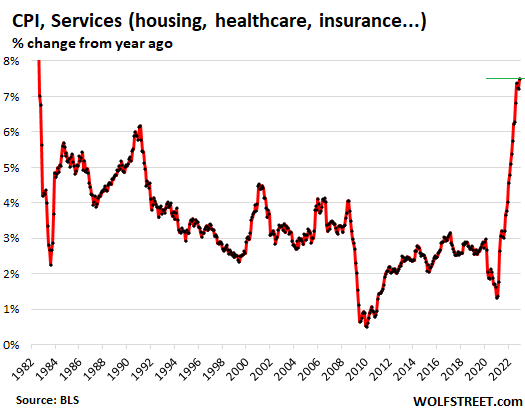

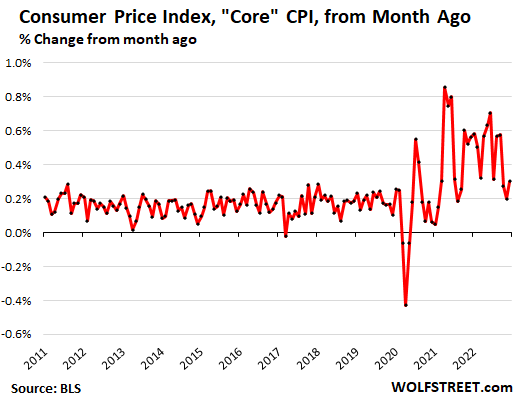

Inflation rages in services.

We’ll start with services because services are such a big part of consumer spending and are therefore so important to consumers. The Fed has been talking about inflation in services for months. I have been talking about it for nearly a year. The CPI for services spiked by 0.6% in December from November, and by 7.5% year-over-year, the worst year-over-year increase since 1982. And it was the fourth month in a row over 7%:

Services by category.

The health insurance adjustment. The spike in the services CPI occurred despite the ongoing massive mega-downward adjustment of health insurance. Without that adjustment, services CPI would have been even worse.

The BLS undertakes annual adjustments in how it estimates the costs of health insurance and then spreads those adjustments over the following 12 months. December was the third month (I’ve discussed this in greater detail here). Due to this adjustment, the CPI for health insurance plunged by 3.4% in December from November. These three months of mega-adjustments reduced the year-over-year rate of the CPI for health insurance from 28% in September to 7.9% in December.

Health insurance is part of medical care services, and so that adjustment knocked down the CPI for medical care services as well. In the chart below, both are indicated in red.

| Services | MoM | YoY |

| Overall services | 0.6% | 7.5% |

| Airline fares | -3.1% | 28.5% |

| Motor vehicle insurance | 0.6% | 14.2% |

| Motor vehicle maintenance & repair | 1.0% | 13.0% |

| Pet services, including veterinary | -0.4% | 9.1% |

| Rent of primary residence | 0.8% | 8.3% |

| Owner’s equivalent of rent | 0.8% | 7.5% |

| Recreation services, admission to movies, concerts, sports events | 0.3% | 5.7% |

| Other personal services (dry-cleaning, haircuts, legal services…) | -0.2% | 5.5% |

| Water, sewer, trash collection services | 0.3% | 4.9% |

| Postage & delivery services | 0.2% | 4.6% |

| Video and audio services, cable | 0.9% | 4.2% |

| Hotels, motels, etc. | 1.7% | 3.2% |

| Telephone services | 0.3% | 1.9% |

| Car and truck rental | -1.6% | -4.9% |

| Medical care services | 0.1% | 4.1% |

| Includes: Health insurance | -3.4% | 7.9% |

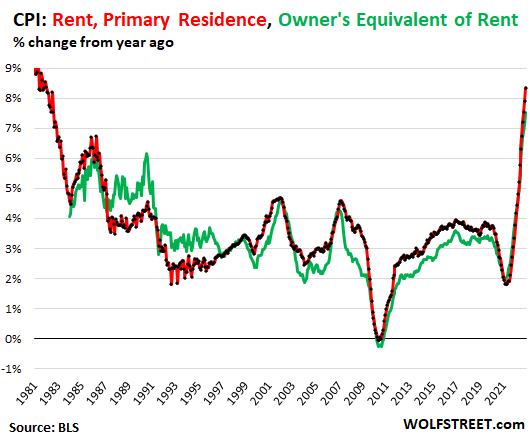

The CPI for housing as a service (shelter).

The CPI for “rent of shelter,” which accounts for 32.6% of total CPI, tracks housing costs as a service, not as an investment, and is based on rents:

“Rent of primary residence” (accounts for 7.5% of total CPI) spiked by 0.8% for the month and by 8.3% year-over-year, the highest since 1982. It tracks actual rents paid by a large panel of tenants, including in rent-controlled apartments (red in the chart below).

Other rent indices, including Zillow’s rent index, track “asking rents,” the advertised rents that landlords wish to charge future tenants. When asking rents are too high to fill the units, landlords may lower the asking rent. There was a boom in asking rents during the pandemic as landlords got a little crazy. But rentals don’t turn over every day, and proportionately not many people actually ended up paying those asking rents, and these sky-high asking rents never fully made their way into actual rents. They were mostly a landlord wish list, which is now getting trimmed back to reality.

“Owner’s equivalent rent of residences” (accounts for 24.2% of total CPI) jumped by 0.8% for the month and by 7.5% year-over-year, the worst in the data. It tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for (green line).

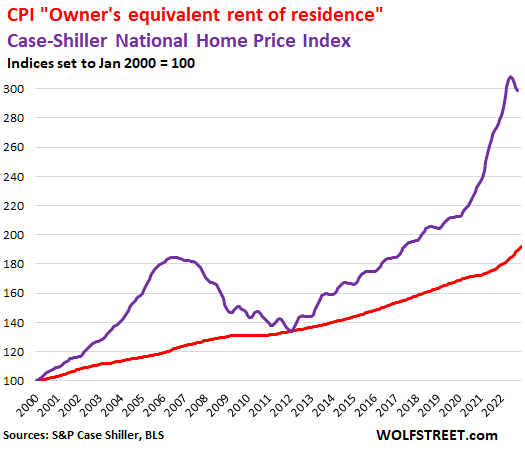

Home prices started to decline in 2022, according to the Case-Shiller Home Price Index [see The Most Splendid Housing Bubbles in America]. The most recent data point available is the three-month moving average of September, October, and November (purple line in the chart below).

The red line represents “owner’s equivalent rent of residence.” Both lines are index values, not percent-changes of index values:

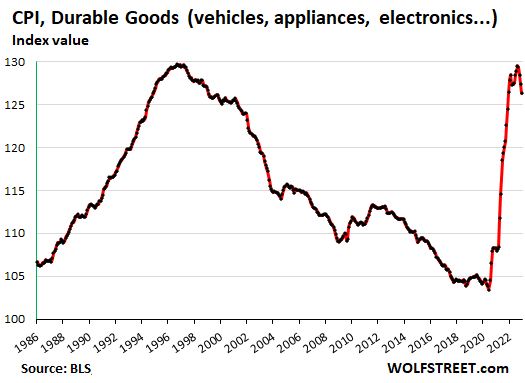

Durable goods prices dropped.

The CPI for durable goods fell for the fourth month in a row, -0.8% for the month, after the ridiculous spike that started in late 2020, extended through 2021, and part of 2022, before unwinding. This whittled away the remainder of the year-over-year gain and turned it negative, if barely: -0.1%.

The CPI for durable goods, expressed as index value, not as percent-change of the index value, depicts how ridiculous the situation had gotten in 2021 and through mid-2022, and how prices have started to drop from the ridiculous spike. The largest categories in this index are new vehicles and used vehicles.

In normal years since the 1990s, after “hedonic quality adjustments” were incorporated, the CPI for durable goods tended to be negative. Inflation is supposed to measure prices of the same product over time. But due to constant improvements of motor vehicles (for instance the move with F-150 trucks from a three-speed automatic transmission back in the day to the now standard 10-speed automatic), adjustments are made to remove the costs of these improvements from the index, which causes the index to decline in normal times:

| Durable goods by category | MoM | YoY |

| Durable goods overall | -0.8% | -0.1% |

| Information technology (computers, smartphones, etc.) | -0.9% | -11.8% |

| Used vehicles | -2.5% | -8.8% |

| Sporting goods (bicycles, equipment, etc.) | -0.5% | 3.5% |

| New vehicles | -0.1% | 5.9% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.2% | 7.3% |

Food inflation.

The CPI for “Food away from home”– prices at restaurants, vending machines, cafeterias, sandwich shops, etc. – rose by 0.4% for the month and by 8.3% year-over-year, the fourth month in a row of around 8.5%, the worst since 1981.

The CPI for “food at home” – food bought at stores and markets – rose by 0.2% for the month and 11.8% year-over-year, the 10th month in a row with double-digit year-over-year increases.

Overall, the increases are slowing. Some prices have started to retreat, while others still spiked, such as eggs, which spiked 11% for the month and 60% year-over-year, due to issues triggered by the avian flu:

| Food inflation by category | MoM | YoY |

| Overall Food at home | 0.2% | 11.8% |

| Cereals and cereal products | 0.0% | 16.1% |

| Beef and veal | 1.3% | -3.1% |

| Pork | -0.2% | 1.5% |

| Poultry | -0.6% | 12.2% |

| Fish and seafood | -0.7% | 5.0% |

| Eggs | 11.1% | 59.9% |

| Dairy and related products | -0.3% | 15.3% |

| Fresh fruits | -1.9% | 3.4% |

| Fresh vegetables | -0.1% | 9.8% |

| Juices and nonalcoholic drinks | 0.0% | 12.2% |

| Coffee | 0.0% | 14.3% |

| Fats and oils | 1.5% | 23.2% |

| Baby food | -0.2% | 10.7% |

| Alcoholic beverages at home | 0.6% | 5.3% |

Energy prices plunged in December:

Gasoline prices plunged further in December and were down 1.5% year-over-year. This, and the plunge in heating oil in December, pushed down the overall energy CPI for the month to -4.5% and slashed its year-over-year gain to +7.3%. But natural gas still rose:

| Energy | MoM | YoY |

| Overall Energy CPI | -4.5% | 7.3% |

| Gasoline | -9.4% | -1.5% |

| Utility natural gas to home | 3.0% | 19.3% |

| Electricity service | -0.2% | 13.7% |

| Heating oil, propane, kerosene, firewood | -11.9% | 26.0% |

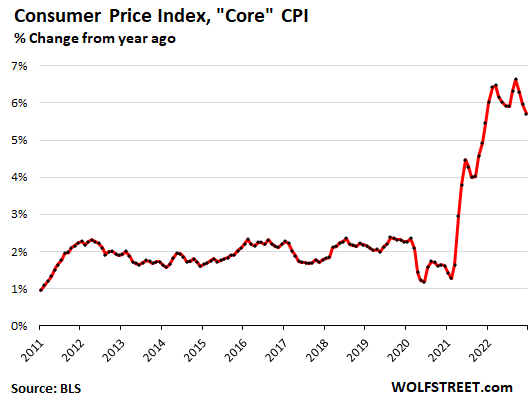

“Core CPI.”

The core CPI, which excludes the volatile food and energy products, rose 0.30% for the month, an acceleration from November (+0.20%) and from October (+0.27%):

Year-over-year, core CPI jumped 5.7%:

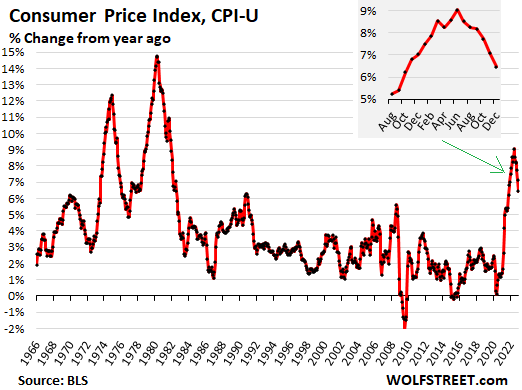

Overall CPI.

Pushed up by services and pushed down by plunging energy and durable goods, the all-items CPI-U dipped 0.1% for the month, which whittled its year-over-year increase to 6.5%:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The fact that medical services are 4.1% inflated while medical insurance is 7.9% inflated should get a double-take from anybody with an above-room-temperature IQ and was the first thing that leapt out at me. I know there’s overhead, but there’s no way there’s THAT much overhead.

Medical care services CPI would have been MUCH higher if there hadn’t been this huge mega down-adjustment to health insurance, as explained in the article.

This was now the third month in a row of this mega-massive adjustment to health insurance. This is the month-to-month plunge due to the adjustment. This replaces what might have been a 1% month-to-month increase:

Wolf,

The treasury yields across the board are retesting December lows today. And in some durations setting lower lows. Starting to look like more than just a technical bounce in treasuries. Almost as if market is trying to call Fed’s bluff.

“Almost as if market is trying to call Fed’s bluff.”

Um that has been the case since last summer. Wash, rinse, repeat. We’ll see who has the last laugh

Laughing in the Fed’s face, as markets have been doing for most of the last eight weeks or so (after doing it for most of last summer).

The Fed is not bluffing. The market is bluffing, and the Fed is going to call its bluff.

I agree with Wolf. The market is bluffing and the Fed is not. I’ve thought this for a while, and there are benefits received on both sides playing it out this way.

If the market is going to call the Fed’s bluff, it should wait for some softness in the labor market. Doesn’t the Fed hold all the cards until that point? The question is what will the Fed do in the face of labor market weakness and how weak will the Fed let it go without responding?

I sold quite a few calls on TLT. Let’s see if the 20 year can drop below 3.55% and stay there. I hope not.

Its very inconvenient that BLS fails to clearly report the effect of “mega-massive adjustment” to health insurance, and provide a number without these one time adjustments, and then mainstream media conveniently ignores this adjustment in favor of wallstreet pivot narrative.

> Medical care services CPI would have been MUCH higher if there hadn’t been this huge mega down-adjustment to health insurance, as explained in the article.

What % of the US population is exposed to these increases in healthcare though after removing those on Medicaid, Medicare, VA, public sector employees, politicians. and ACA with subsidies?

Medicare copays increased by about 30% for 2023. CPC copays stayed the same, but any tests like MRIs went way up if done at the hospital.

For some tests I can have them done at the specialist office. For others I have to go to a hospital to get quality readings. The ultrasounds I need went from $125. to $175.

On a personal level I look at my cost of health insurance and know that the ‘adjustments’ are pure BS.

What is hard to get your head around is that they say healthcare is 18+% of GDP. That is staggering.

actually low for coming additional 10 million soon to be retirees(about 3 years worth)

these boomers – of which I’m at end will soon need medical services with fewer providers

time has come to have 1 PRICE FOR ALL – no more biggy insurance pay 30% RETAIL while medicare pays 80% and patient gets bill for balance(even with insurance)

That summary appears backward from the reality of payments as I understand it. Private insurance is what bears the most weight of American healthcare . Medicare reimbursement for services is far lower than most private insurance. Drugs may be the other way around, as insurers negotiate big discounts on drugs, but gov’t isn’t allowed to negotiate.

Either way, medical pricing is deliberately opaque and a total scam. We are self-insured as a mid-sized employer and some of the numbers that come across my desk for healthcare just make me shake my head and laugh.

zillow tracks “asking rents,” the advertised rents that landlords wish to charge future tenants.

no wishing – it is what I get – sometimes higher

then again I’m not in PITA(price picked from thin air – nyc, san fran, chicago)

lowly Tucson – were we are finally making few bucks and big $$$ investors keep building class A – while us class C guys are 97% occupied

> What is hard to get your head around is that they say healthcare is 18+% of GDP. That is staggering.

Not only that. The 3 groups that do the best healthcare outcomes wise and longevity-wise in the US are the 3 that use the LEAST amount of healthcare: Asian women, Latina women and Catholic nuns.

Malpractice being the third cause of dead after cardiovascular and all cancers combined has something to do with this.

To be fair, you may hav shorten this backwards— healthy people use health care less. So healthy Asian women will not hinting the doctor as often.

Time to limit Medicare to 10 year term. If people live longer they will need to figure out some other way. Or maybe won’t live longer 🤔

Or just stop spending nearly a Trillion a year on “Defense” for the Military Industrial Complex bros, eh?

Don’t try to love me your just in the way.

Because out here it is summer time.

Milk and Honey days and those San Francisco ways

Cause out here it is summer time.

Fever Tree

Wallstreet lowered estimated earning growth for past quarter to -4% in a 7% (official avg) inflation environment. That’s a pathetic 11% decline in real terms. Now Wallstreet is building up expectations of a rally on expected 0.25% earnings beat (real 10.75% decline).

Wallstreet thinks that its investors are either foolish enough to allow this pivot bluff, or that they lack the balls to punish these companies for not cutting costs as earnings decrease.

Also, our new corporate leaders feel that they are no longer accountable to investors and can keep waiting on Pivot as stock prices keep declining.

Time for investors to hit back starting tomorrow with big bank earnings.

Wolf – I read the headlines and inflation reports on the major finance sites and then headed to WolfStreet to get the REAL info. The markets are screaming about how inflation is coming down, but the Fed sees entrenched services inflation.

Plunging energy and auto inflation and the adjustments in medical service inflation is really hiding the fact that service inflation is really still on fire and this report will cause the Fed to actually increase their expectations for interest rates, not decrease them.

All I can say is that we are in a new bubble of hope right now and it is going to get trashed at some point in the future.

What I am wondering is whether the Fed will be forced to move to outright selling of their bond and MBS portfolios (taking losses) in order to quell inflation. With the Federal government spending money like a drunken sailor and a still very large Fed balance sheet, will services inflation really subside?

I think that is really the question for the central banks around the world. They have all acquired large balances of debt that were purchased at very low interest rates. Now, with higher rates, they must take losses on their portfolios if they need to increase the rate of selling debt to quell the inflation fires.

Maybe it never gets to that. Maybe the drop in durable goods prices and energy prices is really doing to bring down inflation. Or maybe not. As I recall from the data on the 70’s, inflation dropped once and then shot right back up.

A question for Wolf. Does raising short term rates versus selling off the balance sheet of Treasuries and MBS have a different impact on inflation?

Is it possible for the Fed to quell inflation with increases in the short term rates if long term rates remain low and the yield curve just gets more inverted?

I just wonder if the huge balance sheet is what is preventing long term rates from moving much higher?

I think the Fed is on the right track to get inflation down, with QT rumbling along in the background, and rate hikes on the front end. It will eventually pause the rate hikes (at 5.5%?), while QT will keep rumbling — and the Fed will watch what is happening. Maybe it will do the job.

But I have reasons to think that core PCE (the gauge that the Fed uses) will head higher over the next few months; and that core services PCE will head higher, and if it does, Powell is going to be very frustrated and make a big deal out of it. And then they might pause later at a higher rate.

Care to give a summary reasoning for your comment about

But I have reasons to think that core PCE (the gauge that the Fed uses) will head higher over the next few months; and that core services PCE will head higher ?

I think the PCE will track higher because of rent increases . Mother in law in Tyler Tx just received a 10 percent increase in rent for her apartment in a retirement community. Several folks said they would look to move out.

The rent was all bills paid including maintenance (no meals). I just paid an appliance repairman 180 usd for installing a computer chip in microwave for less than 1 hr work . Two years ago bill was 80 usd. Plumbers are now pricing work by the task. Accounting and tax prep increasing 10 percent . So these annual increases may hit all at the same time in the monthly actuals. Month to month rent can be an annual increase

From the stock charting perspective we use, this lines up from what we expect to see in both the stock and bond market this year. There looks to be a rally setting up that will take at least a few months to play out (bonds seems like it could take longer). It’s possible stocks hit a new all time high, but unlikely.

The probabilities are heavy on the side that once this rally tops there will be a crash-like move in both stocks and bonds (though probably not simultaneously) that will make last year’s move feel tame.

I simply don’t believe the CPI stats anymore. I think they are torturing them to death to try to give the impression that inflation is falling. What they’re doing with Healthscare, for instance, seems shady to the point of completely disingenuous.

The Fed is finally doing the right thing. Way too late, but better now than never. Now we’ve got to get Federal spending under control to help the Fed do its job. That’s where the problem is. Spending. Start impounding allocated funds like Nixon did back in 1972/1973. No increase in the debt ceiling. Have a government shutdown if necessary.

Excellent question! The fed is picking who feels the most pain. Reducing the balance sheet as fast as possible verses small spread out rate increases, who is getting their pockets picked? As for long term treasuries, what entity is purchasing them, forcing the rates down? Maybe something caught in a corner, but trying to keep the game going?

It’s always the dowtrodden, the working poor and the middle class (what’s left of it) who feel the most pain. That’s no different this time around. The FED will ensure the duration of the pain is stretched out as long as possible.

It’s not the Fed’s job to make the economy more fair. It has no control over that and only blunt tools to address inflation. Consolidation, union-busting, SEC’s blind eye towards corporate malfeasance, stock-buy backs and things like that, which have given a raw deal to the working class are failures on the part of the thee branches of government, not the Fed.

Digger Dave,

You’re correct on the raw deal given to the working class by other branches of government, but the Fed has pursued a policy of negative real interest rates for years. That is a decidedly unfair economic policy for savers to the benefit of some borrowers and speculators. I say some borrowers because any borrower who paid an inflated price for a home or other asset, rather than simply refinancing at a lower rate, was also damaged by Fed policy in a different way. Since the Fed’s policies can and do actively favor one group of economic actors over another, the Fed does have some control over fairness in the economy.

@rojogrande – No doubt that the Fed has some culpability, but the slash and dry timber was already laying around in ’08. Fannie Mae started the fire. The Fed poured gas on it.

I agree, saving the “system” required burning a lot of workers.

“All I can say is that we are in a new bubble of hope right now and it is going to get trashed at some point in the future.”

Seems to be a cyclical thing with financial media, rates go up they run a bunch of negative news, S&P500 falls to touch bottom of the trend line, financial media run stories about inflation coming down, S&P rallies to upper trendline, FED meeting, bad inflation stories again… so on and so on. So strange to watch it play out. I’m am amateur though so maybe this is normal and I’m just noticing it now.

Keep in mind SPR is still being drained. Once they start getting refilled, along with China getting over the first COVID wave, I anticipate much higher oil and gasoline prices by end of this year.

Somewhere I read that the Biden administration chose not to refill the reserve because the prices were too high. Might be BS, but… what in this day and age isn’t?

It’s not BS but I believe the bids from oil companies or refineries or whomever were too high so they choose to wait. I read the energy departments budget is compromised and it’ll be hard for them to buy back enough oil unless it crashes below $70…. I’m not sure if that’s true but 🤷

Traders seem to be putting a floor in prices just above that knowing the government will step into buy around 70 so not a ton of downside.

Seems to me like oil should go up since we’re not near a recession based on jobs market among other things

Last week the price of gas at our 2 local stations went up 60 cents in one shot.

I had believed the reports of reduced inflation, because China and even the EU (due to its fossil fuel issues), were going into or in recession for varied reasons. However, this data contradicts the reports, particularly since the services/goods, such as food at home, that the less wealthy 90% of Americans will consume seem to mostly still be going up.

Apparently, the “Fed” is not “succeeding” in its alleged efforts to tame inflation. Cynics would claim that the way that inflation reduces the real value of banks’ and ultra-rich persons’ liabilities (such as bank deposits of their customers-depositors) creates a big conflict of interest against taming inflation. The derivatives liabilities, which may play a role here, which allegedly amount to trillions are also “coincidentally” getting reduced by inflation.

Of course, maybe we should just trust the bankers and the ultrarich and just believe that they will take care of us. After all, it is not as if they are greedy or immoral, is it? See Investopedia: “The Panama Papers Scandal: Who Was Exposed & Consequences.”

Maybe, all persons that criticize them are just sore losers because of the ultra-low interest rate loans and effective guarantees that the “Fed” and other central banks give their blessed cronies, who are our new aristocrats and are above our laws, since they can pay money to elect our judges, who then rightfully cherish them: e.g., a lawyer I know just had a case in which a wealthy company suing a group of poorer doctors, who had refused to produce documents as discovery rules require, was effectively excused by a corrupt, soon-to-be wealthy, CA judge. I laugh at world corruption indexes that usually ignore that kind of thing.

To clarify, the wealth (quasi-insurance) company was the one who arrogantly just refused to produce any documents in a long case for years and just invented a procedure (which was not agreed to) in which it required the financially-poor defendants to download the documents from the insurance company’s websites directly, then refused to allow the downloads or provided files that could not be opened with either defective passwords or maybe garbage in them, and claimed it was the fault of the defendants for not being able to get them. If a financially poor defendant had done that, he would have lost his case in one minute. It pays to be rich and be able to give enough to elect your own subservient, CA state court judges. The ignorant still claim that our legal system is not like the CCP-controlled one in China in which corrupt cronies are protected by judges who are being controlled by those in power! LOL

Inflation still raging, as expected. Just when long-bond holders flapped their faces back on, it appears their faces are going to be ripped off again. Persistent elevated inflation is NOT priced into long-bonds.

They were right before. Don’t fight the Fed.

Wallstreet lowered estimated earning growth for past quarter to -4% in a 7% (official avg) inflation environment. That’s a pathetic 11% decline in real terms. Now Wallstreet is building up expectations of a rally on expected 0.25% earnings beat (real 10.75% decline).

Wallstreet thinks that its investors are either foolish enough to allow this pivot bluff, or that they lack the balls to punish these companies for not cutting costs as earnings decrease.

Also, our new corporate leaders feel that they are no longer accountable to investors and can keep waiting on Pivot as stock prices keep declining.

Time for investors to hit back starting tomorrow with big bank earnings.

Thanks wolf!

New car prices still insane. Maybe the official used car prices are declining but in the real world they are still ridiculous and the inventory is shite. Take a look at Carvana today. Nuts

Carvana? I don’t think I would use them as a yardstick.

Retail prices are sticky. I reported on used asking prices — what dealers want for their vehicles. And they had barely budged, compared to the spike they had. I’m going to get the December used asking prices in a few days. Maybe I’ll cover it. Wholesale prices are down quite a bit though.

@Wolf

Ran into a local new/used auto salesman last week.

Not much new inventory arriving. He said the used market is a dead zone, they overpaid at the wholesale auctions the past few months and are priced way too high to try to sell at a profit. No foot traffic.

They are not planning on selling anything until after winter and salespeople have been plowing snow with the shop trucks for extra $ into the door.

Pretty small market though, and imprecise research on my part to say the least.

Appears to be a sort of standoff between consumers and dealers.

The dealer will lose. I can do without buying a car for far longer than they can do without selling a car.

Inventory is constantly “eating hay”. Floorplan (or lost opportunity), lot rot (repairing dents/acid rain/etc.,) is expensive.

100 years ago… when I did a short stint in retail, we had major snows in Chicongo. I, along with my fellow salesmen, took on plow duty. One guy revved up the GMC 4×4 he was driving (plow down) and hit a snowdrift to widen a lane. Our of the snow flew several pieces of blue plastic… which used to be attached to a car. Enterprising lad that he was, he got the end loader to bury the evidence. They found it about 3 months later. Totaled. The trunk was pushed up to the rear window. Whoops.

Funny how disgusting greed works and they all behave the same. These dealers are just like stubborn home sellers not wanting to lower price to move inventory..they rather die on that hill…and for that when they do die on that hill I say good Fing riddance.

Bought my F150 in ’09 25k cash, my Tacoma in ’08 16k cash. My ‘022 Ford Escape Cash 60k. Holy geez. Just about fainted. Oh well got all three in good running order maybe you somehow amortize that mess.

You paid 60 grand for a new Ford escape? Good lord you can’t be serious

Please correct me if I am wrong but I see even more money entering into the economy with no end in sight as well as no large increase in productivity within the US economy. These are traditional Econ 101 inflation signals and this leads me to believe inflation is not going away anytime soon.

I am I missing something?

Compare the amount of Government deficit spending each month to the amount of monthly roll-off from the Fed’s balance sheet. That will tell you something about whether inflation will be going away anytime soon.

The U.S. government spent $85B more in December 2022 than it collected in revenue so I think I have my answer, thanks!

The government spend/collect numbers are not the same each month.

As Schiff said recently “To use a favorite Fed term, any cooling of the CPI is likely to be “transitory”.”

Same comment as other(s)… headlines everywhere else suggest big positive today.

Data didn’t look good to me yet saw these headlines:

“Biden moves quickly on Thursday to tout good inflation news” Yahoo Finance

“US inflation cools again, putting fed on track to downshift” Bloomberg

“Inflation is easing, even if it may not feel that way” NPR

… wtf.

Many thanks, Wolf, for the light of reality in the dim jungle of misinformation out there.

The problem with services inflation is that it is tied to service salaries. Salaries don’t go down; they only go up. A company can reduce aggregate wages through layoffs, which means we should be seeing an increase in the unemployment rate, which is likely what the Fed intends as well.

Inflation wouldn’t be so bad if people exercised some caution and common sense, but we’re learning that many people refuse to voluntarily cut back spending. They’ll keep spending every penny until they lose their source of income, or their assets drop 50% in value.

Shame on the Fed for not understanding all of this. It was very obvious to thinking persons that the wealth effect was inevitably going to show up in CPI. The Fed is supposed to act prudently, with consideration of the long-term consequences.

I’ll play devil’s advocate here. People keep hearing about inflation and their dollars having less spending power if they hold on to them. Things keep on going up in value, money keeps on going down. Telling that to a shopaholic is like telling al alcoholic that gin is medicinal. American advertising has centered around the notion that buying things and experiences will make you happy. The country has been pretty miserable since 2020. Amazon made a lot of money during the pandemic off people attempting retail therapy. Once the restrictions lifted, the hospitality side of the service industry got the same sort of treatment. Now many people have unrealistic spending habits. My generation (millennials) always had a “carpe diem” philosophy towards spending vs. saving, but now most have stop bothering to try. I think only a fraction (25-30%) of my high school class actually have homes, and most of us were first time buyers within the past 5 years.

Most seem to feel like there’s no point in saving because all of the things you are saving for are hopelessly out of reach financially. Couple that with the fact that they watched purchasing power erode in front of their eyes last year, and you have a relatively simple explanation for why money keeps on flowing. I have no idea what the boomers are up to. My parents have been exceptionally tight-wadded in the past 2 years. My wife’s parents spend like drunken sailors, but they’ve been doing that for 15 years because her dad grew up poor and can now afford all the toys he never wanted.

What a terrific comment, Grant. Thank you.

And you’re right, I think — there is what seems like a fatalism underscoring the spending habits of Americans today. That said, I don’t think it’s entirely unreasonable.

Living under self-imposed austerity/poverty effect in the short-term in support of saving for a brighter future — what I once did — always contained more than an element presumptuousness. Combine that with the sinking feeling of knowing that the buying power of the earnings you’re so earnestly socking away is being perceptibly eroded from one quarter to the next and you have a very attractive argument for getting at that gravy while it’s still hot. Maybe the ants got it wrong!

The value in sites like Wolf’s here is that they serve as a sort of de-fogging agent; cleaning the rearview mirrors so that we can enjoy a really detailed look at who’s giving it to us over the barrel. Horribly, there are times when the face in the mirror ends up being our very own.

Totally agree with both of you but wanted to impart this… Sometimes one just has to be a ‘freaking jerk’ about stuff.

My auto insurance renews soon. Always have paid full premium in advance to avoid finance charges. I have been with the same company for four years and am a ‘diamond’ bs moniker whatever with them. Of course my rates went up (knew it was coming cause I read this site) and so I cussed them over it and went shopping for new rates. It was only $70 bucks over the 6-month period but it’s like Big Worm told Smokey- Principalities involved, Smoke!

No joke- I got way lower rates from the same exact company for the same level of coverage by going through one of those ‘insurance comparison sites’ which ultimately redirected to theirs. Bought the new policy in full. Could care less about insurance as it’s a freaking scam that does nothing but generate leads for trial attorneys. Would have no problem going without it. None. Only reason I have it is not to be hassled by the state.

Point is- sometimes you just have to say ‘screw you’ because I can and to hell with your crap. That’s how some of this ends. And even if it doesn’t help end it, it’s nice sticking it to the man.

AGHM:

All insurance is a waste of money until you need it. Had some moron hit me and then sue me for his injuries. The dope sued for too much, the insurance company balked, gave me full indemnity (they have to if they refuse to settle) and the plaintiff walked out with his wee wee in his hand and the ambulance chaser attorneys got bupkus. I’d hate to see the lawyer/expert witness/etc. bill on that puppy.

Grant/Bul – my observation confirms yours, but I noted this trend occuring with the stagflation/explosion of easy consumer credit of the late ’70’s-early ’80’s…

may we all find a better day.

“I have no idea what the boomers are up to”.

Aged between 59 and 77, they are retiring and dying.

They are also followed by a bulge in the US Population Pyramid for those aged 50 to 60.

It will take time, but their houses and toys will re-enter the market with countervailing price pressures … maybe.

Dying indeed. As one who winters in a retirement community I can attest to the horrible health of boomers. The vast majority are out of shape and get zero exercise. It’s like they are on a suicidal mission.

Grant – Does the classmates who do not own a home want to own a home? If so, why do they not want a home?

You own something, and it owns you. Rent and you can just take off anytime you pleaseusing the dough you got from selling your home.

They certainly do want to own homes. The problem is location. I grew up in a suburb of Philadelphia. My parents bought their split level in ’90 for around $175k. It’s now valued at around $450k. Wages in the area have not risen nearly to the level that property has. Most of us who do have homes were either tradesmen or in the military. A lot of the people who now could, theoretically, save for a down-payment to avoid PMI, are so downtrodden that they have convinced themselves they like renting apartments.

Spot on Bobber,

Except for the “Shame on the…. understanding “

They don’t like us and never did. As always a they are professional thieves in the night.

Everyone should take lessons for hedging alongside.

Great observation I needed this

No Quarter

I see the YoY markup for eggs is 59.9%. Somebody is getting a good deal. I paid 1.77/dz for eggs in Jan 22 and 5.28/dz yesterday. Since the family eats a lot of eggs, that price increase is eye-catching, but as with a lot of spending throughout the economy, we pay it and keep on eating. If the price gets to a dollar an egg though (the egg price in the gold fields of 1850), I’ll probably be looking for a change in my diet.

Saw $7 for a dozen brown eggs…

My doctor will be happy…. because I passed. Low cholesterol here I come!

Where do you live that eggs are that much!? Today I bought two dozen brown organic eggs from Costco for $7.99.

This week 18 eggs cost $10. There were no eggs available in the 12 packs.

If we lived in a house with a yard, I would get chickens.

Here in NE Wisconsin my local Aldi has been out of eggs for about 2 weeks now. On my last visit, a sign on the empty case said $5.09 doz for large.

I went to the Woodmans, and they had a local off-brand, 12 med for $2.69, and large $3.79 doz, also a 75¢ off coupon if you bought 2 doz. A lot of the eggs are brown, not the usual white.

That might bother some people.

Going off on another tangent. The local paper reports that a large RE SFH is mostly sold, but that only 30% are occupied by year around residents. Since tourism is very big here, I am not surprized. But wow. I wonder how many people have 2 or 3+ homes???

My local grocery store – no eggs at any price for a at least a week now.

It’s obvious you are not a connected guy. A lot of us have been getting our eggs direct from the nation’s Strategic Eggs Reserve.

Seems pretty clear to me that the Fed is especially targeting housing costs. The sooner they can force residential real estate lower, the faster services inflation will come down.

The rent was raised 0.8% according to this report. That is 9.6% annualized. Not sure the Fed can lower the rent. Home repair costs have risen. There is a shortage of sober workers.

By allowing mortgage rates to increase as a natural result of the rising FFR, the Fed is trying to deflate Murica’s housing bubble.

‘Sober’ workers? I’ve known more white-collar alcoholics who ‘worked’ while loaded than blue-collar guys drunk on the clock.

There is a shortage of workers that can afford to work for the pay being offered. So they look elsewhere.

China cannot “lay flat” for long. Wait until they decide to heck with their people and the virus, back to work!! Oil supply will be pressed and prices will again be in the clouds. Gas will be in short supply and very expensive since we don’t have any way now to boost our home production.

China, just like the US, will see a spike in oil consumption as a result of the imposed lock-down. People who have had to put off seeing family and such will book flights, and jet fuel will start being burned in mass. There is a lot of speculation about what that is going to do to world markets.

YoY Eggs up 59%. I’m going to buy beef for my protein – YoY -3.1%. LOL

I hardly eat out, but I get these coupons mailed and occasionally I use them as I’m a bachelor and sometimes after work, I don’t got energy to make something. Again, rare.

I went to Carl’s Jr. Had a mailer coupon (These younger gals at my work laugh their butts off when I tell them I used a coupon) and ordered 2 Angus Burgers (2 for 9 bucks), and order of small fries and order of onion rings (one side only). Almost 18 bucks with the coupon for the burgers. No drink. Had the meal with beer at home. Burgers go for almost 8 bucks apiece without coupon. I ate the other burger the next day which these same gals say is gross. I put the 2nd burger in the fridge, and nuke it in the microwave the next day. I tell ’em almost everything is edible when your a bachelor. They just laugh.

Years ago, under 10 bucks got you a burger, fries and soft drink. Then, the prices for same went to 12, then 14-15 and now we are 16-18 bucks. This is just one person, an adult. I don’t how you guys eat out every day and buy coffees at Starbucks daily, and you guys with the families! You must be rich people. :D

Fast food is disproportionately of low quality, in many places the service was not fast (when I went), and now it’s not even cheap (just the cheapest option).

Sounds like a great reason to avoid it.

Lots of people eat out and go to Starbucks every day and they’re NOT rich. But, they are quite instructive for those who grasp the connection.

All’s well until the credit card is declined. Saw that at Costco where the woman started taking things out of the basket to get to what was left on her line.

In Scottsdale, AZ…. with a large rock on her hand and a Louis handbag.

That’s the husband’s way of controlling her out-of-control spending habit, most likely. I have firsthand information.

I was like that woman during the GFC. She is falling out of the middle class but doesn’t know it yet. First the credit goes, then they take the car, then she will sell all those nice things to pay the electric bill and eat. The house will go too and probably forever. If she is young she may recover someday but otherwise she will live in poverty going forward.

@JK

Showing my age but in the late 1960s a burger, fries and drink were 99 cents. Minimum wage at the time was $1.15/hr. Thank you FED. (for destroying the dollar). I hope to live long enough to see the end of the FED.

Wow that hits

I was just got notified that my Blue Cross/Blue Shield insurance premiums are going up 9%. The figures in Wolf’s article may be dated. This year look forward to double digit insurance premium increases across the board.

Wells Fargo just charged me a fee of $32 to stop payment of a check that was lost in the mail.

“The figures in Wolf’s article may be dated.”

READ THE ARTICLE!

Right after the first chart. Here is what it says verbatim (I hate having to repeat portions of the article in the comments because people refuse to read the article and then post nonsense it, LOL):

“The health insurance adjustment. The spike in the services CPI occurred despite the ongoing massive mega-downward adjustment of health insurance. Without that adjustment, services CPI would have been even worse.

“The BLS undertakes annual adjustments in how it estimates the costs of health insurance and then spreads those adjustments over the following 12 months. December was the third month (I’ve discussed this in greater detail here). Due to this adjustment, the CPI for health insurance plunged by 3.4% in December from November. These three months of mega-adjustments reduced the year-over-year rate of the CPI for health insurance from 28% in September to 7.9% in December.

“Health insurance is part of medical care services, and so that adjustment knocked down the CPI for medical care services as well. In the chart below, both are indicated in red.”

In addition, you might want to look at the chart I posed above into the comments about the health insurance adjustment.

This is what I said in that comment that might shed light on your point:

“This was now the third month in a row of this mega-massive adjustment to health insurance. This is the month-to-month plunge due to the adjustment. This replaces what might have been a 1% month-to-month increase”

My health insurance is now running about 12K a year. I went to a doc-in-the-box exactly once last year. Kinda hard not to want to just wing it next year when open enrollment comes around. Short of major stuff, out-of-pocket for most things is just ba better deal in my experience.

My family of 4 is now at $20k/yr including dental. $250/mo increase this year. We are seriously considering leaving the country, not just because of this but certainly in part.

That’s about 3x my max out of pocket for my entire family.

Went without coverage 4 years after O’care, I got pounded with 6X increase for coverage. Fortunately I moved to another country. It’s not worth your life to get beaten down like that.

The bad news is the cost of your health care is going up. The other bad news is despite paying more, you have a 5% higher chance of dying from all causes than when you were paying less….. LOL it just keeps getting better.

Worse news is that it’s not “health care” but sick care. With all the money thrown at certain ailments, you’d think a “cure” would be found.

But it likely won’t be because it’s become big business where the CEO makes multi-millions. He’s going to find a cure and put his enterprise out of business? Are you nuts?

“Health care” would be: “You’re a fat a$$. Strip naked. If you can’t see your *junk*, you’re too fat. Don’t lose the weight and you’ll die. There’s no pill available to cure stupidity” $200 please..”

“Sick care” is: “Take two of these… and these… and these…. Oh, by the way… don’t read the sheet that comes with any of them so you know the risks associated with taking them. That’s $200 plus the $500 for big pharma.”

Blue Cross/Blue Shield insurance premiums didn’t go up much last year. They are a non-profit I believe so they are anticipating some big increases in the future. That’s why the premiums went up. That ate up a lot of my COLA.

Oh boy, the silliness is coming back to crypto! Those were some pretty nice gains today. I even found out the Coinbase is extending existing and opening new contracts with a very expensive big 4 consulting firm. Party on Wayne!

All the signs of a rope-a-dope scheme to me.

It’s because the FED is too scared to get real with rate hikes and QT. They have decided to try to engineer some fantasy “soft landing” which means they slow their inflation fight well before inflation is under control, rather than after. They already cut back their rate hikes to 50 basis points – PREMATURE – and the talk is now 25 basis points at the next meeting. Then no more rate hikes following that, where they sit around and wait for The Great Pumpkin of Magically Falling Inflation.

So, the guy who supposedly channels Volcker is going to pause rate hikes at a much lower rate than CPI even though, as Stanley Druckenmiller has pointed out, inflation above 5% has NEVER IN HISTORY come down without a fed funds rate above CPI. THAT’S why everything is taking off again and people are calling the FED’s bluff, because the FED is signaling a BS strategy to begin with. So yeah, it’s party on again. The DOW is barely off its all-time highs.

Crypto has very little to do with the Fed. It’s a purely sentiment driven thing (so is most of the market but Crypto is worse because there basically is no “fundamental” aspect to it).

From a sentiment charting perspective, BTC and ETH may be close to a major bottom (by close I mean they could still drop 30-50% or more) but the upside once they bottom is ridiculous.

It may be many months before a bottom hits but once it begins the next bull market you will want to have some money there even if you hate it (not more than you are willing to lose, because you might lose it all).

Take your crypto shilling to somebody who gives a f***. I don’t.

I honestly don’t see how crypto recovers from this.

I would have considered myself a believer that BTC had potential for changing global money 12 months ago but trust is broken.

Now I see it’s something that is so far off it’s original mission that it’s a joke and will only have value if free money has no where else to run to

I will simply give this comment the reply it richly deserves: lmao

DC

Good response to the Crypto shill. I couldn’t have said it better.

Depth Charge

Overall CPI (year-over-year), which sensibly includes the very relevant components of food and energy, peaked at 9% in June 2022, interestingly, that’s when QT started. It’s at 6.5% six months later, a 2.5% drop, and only 1.51% away from appearing below 5% and that’s in the face of raging Services inflation.

As Services inflation involves an outsized contribution to consumer spending on the way up, we will have to accept its outsized contribution on the way down – whenever that may be.

QT and rate hikes continue. I have read quite a lot about policy lags in the Comments sections on Wolf Street, which if true, the corollary is they have yet to take effect.

This is not looking like a repeat of the 1970’s at all. I note the spectacular implosion of Volcker chatter.

My suggestion has always been to follow QT. This remains unchanged.

The idea that the peak month of inflation and subsequent decline is directly related to the start of QE at that very same juncture is not something I believe in.

Coming back? Crypto is about as silly as investing in Tulips. At least tulip actually exist…..

Ordinary people must worry first about rent, food, and transportation to work. As long as these keep rising, they will demand increases their wages. Inflation will be sticky until primary expenses fall. Used car prices returning to sane levels will be a one-time benefit only. Although discretionary consumption will continue to be pushed into the future, I don’t see a quick return to 2% inflation.

Increases in wages are not tied to inflation in prices, but to availability of labor. I think this will change very soon. As companies start to see tough times ahead, they will put off hiring more workers.

Employment at the state and local government level has also been propped up by all the government spending, which is going to be reversed as Republicans try to bring a little fiscal discipline (just a little)

Only because they aren’t in charge. No fiscal discipline when they have been, for a long time.

Growth in federal government spending will decrease due to gridlock, not fiscal discipline.

Excellent- exactly as the founding fathers intended.

The trend is still moving towards a ‘looser’ Financial conditions in the NFCI.

So I’m thinking another 50 basis points at the end of Jan. That will kick the markets in the gonads!

Index Suggests Financial Conditions Loosened in Week Ending January 6

The NFCI edged down to –0.27 in the week ending January 6. Risk indicators contributed –0.07, credit indicators contributed –0.10, and leverage indicators contributed –0.10 to the index in the latest week.

The ANFCI ticked down in the latest week to –0.26. Risk indicators contributed –0.03, credit indicators contributed –0.08, leverage indicators contributed –0.07, and the adjustments for prevailing macroeconomic conditions contributed –0.07 to the index in the latest week.

Markets are now slam dunking 25pts on Feb 1st.

I’m with you though looser conditions could push Fed towards 50 bips.

To me when the report dropped it said no progress in service inflation and rates need to be higher. The initial market reaction was the same so we’ll see where we go from here.

Earnings should be interesting. Last quarter it felt like the big boys were hanging on by a thread so we’ll see there.

Oh and Bitcoin, carvana, Bed bath and beyond all popped today..

Apple down 8 cents…sustainable rally? We will find out

If the FED were serious, they’d hike 75 basis points next meeting to send a message. Period.

It’s gonna be 25 unless earnings show over heated consumers

Of course it’s going to be 25. There’s zero chance of 75. I’d say there’s less than 10% chance of 50. Because these guys are frauds.

Why did the stonk market, the NYSE and TSX go up in value while the American and Canadian five and ten year bond go down in tandem?

Rising interest rates are a drag on the stock market for a million reasons.

Right now, the mainstream financial media is reporting low unemployment combined with low wage inflation + some decent (cherry picked) inflation numbers… and so according to the mainstream financial media, we have good reason to assume a more dovish fed – in other words, maybe lower interest rates in the future… which is all good for stocks.

Anyway, I don’t buy what the mainstream financial media is selling. You just have to read this article to see why.

CPI blog posts often exclude complaints about methodology or data bias, but thankfully, I’m willing to put an end to that.

As everyone knows, Nelson, the survey company helps collect barcode data for a consumer inflation panel, but my complaint is, they pay people to participate in that program. In a nutshell, I think it adds extra dimensions of chaos, into complex and confusing aggregate data, which compounds inflation dynamics.

It is what it is, but obviously inflation data is mystical and filled with loud noise.

FYI, not that it matters

Nielsen Homescan Consumer Panel

A challenge that has hindered incorporating high frequency chained indices into CPIs is that they can suffer from the chain-drift problem, whereby a high frequency relationship between prices and quantities leads the inflation index to become increasingly biased over time.

“an unintended consequence of chaining is that the index does not return to its base even when item-level prices go back to their base levels (Forsyth and Fowler 1981), a phenomenon known as chain drift. This can be particularly prominent in high frequency, such as weekly, data where temporary price cuts and the resulting stockpiling behavior by shoppers are more pronounced. “

Stupid rabbit holes!

Jesus!!! Nielsen has ZERO to do with the data here. That’s just BS to drag a private outfit into here and draw stupid conclusions from it.

And the CPI here (from the BLS) is NOT CHAINED, for crying out loud. Don’t you know ANYTHING about this?

Nielsen has its own CPI measure that it gets from supermarket scanner data. This has nothing to do with the BLS data.

I should have deleted your effing crap.

Wolf the previous comment and the one following appear to be ChatGPT or equivalent AI generated garbage.

Sorry John , the one following labelled Brent.

good observation TX! agree.

On the contrary, it’s all too human. Wolf’s comments section attracts some people who are clearly…wired a little differently.

All good points, but the Fed has trained the gamblers to focus on “core inflation” and the market was again happy today and ignored the services inflation.

Services inflation will probably kill the economy this time around: 50% of the population may soon be unable to afford much of any services at all. For example, some mothers have given up working due to the cost of daycare/babysitters and commuting to work.

I wonder when was the last time Powell and his minions pumped their own gas, bought groceries, or went to a dealership.

Core CPI accelerated (MoM, it bounced off the low in the prior month).

Yes, but now they keep saying “CPI was not as bad as feared” or it was “all priced in.” So infuriating how these markets are being manipulated. DAX might hit an all time high soon.

Financial conditions are easing again due to the CPI circus rallies, and the Fed is planning to stop at 5.25 according to Bullard. We may never get a positive return on our savings again.

My 2 cents is the market has been marking up a lot of garbage to get in front of what will be a lot of selling due to disappointing earnings. They do this manipulation often around options expiration and prior to earnings. The stuff that doesn’t get ramped is probably worth looking at on the long side. Carvana is a great example, as is a lot of RE related stuff, especially given transactions have fallen off a cliff and we will likely see a lot of inventory come to market in the spring.

And the “surrender” of one of their dealership licenses in Michigan….

John-

Today I actually felt like the murmurs we’re that CPI wasn’t as big of a miss as they were hoping for on wall street.

Markets struggled in early trading and finishing 35-60bips in the green is not anywhere close to fireworks. Remember that 7% nasdaq day a couple months ago!!!

Yields got whacked but maybe Japan ycc uncertainty has something to do with that. Yields falling so much is the thing that really didn’t add up to me but let’s see where we go from here.

“CPI for Gasoline & Durable Goods Plunge”

CPI for one food category plunged even more

I am tracking Amazon section “Edible Insects” which, according to 1000’s of raving 5 star reviees, are all the rage, and Food of the Future too.

Grasshopper Powder (Oxya Yezoensis Sp) $9.90

Locust Powder (Locusta migratoria) $13.50

Silkworm Pupae Powder 100g $6.50

Silkworm Pupae Powder 1kg $55.00

Giant Cricket Powder 100g $6.50

Scorpion Powder – 100 $29.90

Earthworm flour (Eisenia foetida) 40g $10

YoY the average price of such delicacies went down 29% – I designed my own Food of The Future Index (FTFI) patent pending

I like fried eggs with bacon and REAL butter…

I like fried pork dripping with fat…

I like barley or buckwheat or rice cooked with lard…

I like cabbage soup with suet…

I like many other foods considered good & nutritious in the 60’s but recently proclaimed bad…

But Edible Insects appear to be the Future. And it is unstoppable.

Lets not forget Roman proverb:

Ducunt volentem Fata, nolentem trahunt

(Seneca)

I understand that Scorpion Powder is not for the faint-hearted. Silkworm Pupae Powder on the other hand is smooth and silky, just like NPR radio voices.

State Provides Quality Ramen

Soylent green!

EK

Liked your comment above. Dealership I’ve traded with for 30 years retired. Sold out lock, stock, and barrel to the largest dealer in the area and retired.

Mark Zandi had some inflation zingers today on CNBC. Zandi reminds me of Tommy Lee on CNBC, the guy who throws out ridiculous future asset value targets, which usually never materializes. Good for a laugh always, yet curious…are such individuals just too rich to get it or too dumb to understand or too manipulative to care?

Per CNBC:

“Inflation is on its back heels,” said Mark Zandi, chief economist at Moody’s Analytics. “It’s moderating steadily and, at this point, quickly.”

“I don’t think people will be talking about inflation this time next year,” Zandi added. “It just won’t be at the top of their agenda when thinking about their own finances.”

I used to follow Mark Zandi’s career when he was a “fellow traveler” on the Fannie Mae perpetual conservatorship debacle, and he appeared to be a tool, and a tool only. Therefore I don’t usually trust a word Zandi says. He gets paid good money for lying.

So do most politicians.

Most?

I love watching Tom Lee on CNBC because he has the most peculiar way of contradicting himself sometimes even in the very same sentence. It’s like he does these somersaults in his head to come up with the most bullish scenario possible but manages to do it in a stunningly convincing way. He is literally made for that channel

In the real world rents are going down, the data Fed uses for rents is lagging by more than 6 months and so inflation showing now is already well past!

Red herring alert. In the actual real world, not your “real world,” tenants ARE PAYING rents, and the amounts tenants ARE ACTUALLY PAYING are the actual rents, and they’re reflected in the data here.

Your “real world” is asking rents, which is what landlords advertise their vacant units for. That’s a landlord’s wish list. Very few tenants are actually paying those asking rents because there isn’t that much turnover.

That’s why the spike in asking rents last year and in 2021 never made it into the index, and that’s why the decline from that spike in asking rents won’t make it into the index because the spike never did.

ACTUAL rents are NOT coming down. People are still getting rent increases when the lease renews.

It’s the age old Two Card Monte being forced upon baffling audience of the renters.

Wolf,

Agreed. Rent increases show no signs of slowing down…except here in LA where they’ve been frozen for nearly three years. Yes, rental housing ’emergency measures’ remain in effect here in 2023. Were supposed to expire Dec 31 but they kicked the can out to Jan 31 and both the city and county hinting these will be extended out to June 30.

Eviction moratorium remains in effect and rental increases have been outlawed until these emergency measures are officially rescinded.

Here’s the kicker: once the city and county authorities officially end these emergency measures, landlords must still wait another 12 months before they can raise rents.

Local property management companies have laid off nearly everyone. No one around to even answer the phones.

Wolf,

“People are still getting rent increases when the lease renews”.

Agreed. In fact, it’s worse than what you reported. Landlords here are throwing tenants out of their houses to get gigantic rent increases that are not allowed according to local laws. They use the BS that they are selling the home to get the tenants out. Then they don’t sell and re-rent the same property to 20% to 30% above the previous rent. I wonder if this rent price gauging is being captured in the data provided.

I for one have not seen any rentals I look at it going down or anybody that I know taking about there rent going down or them being able to move to a cheaper lease. Not sure why you would think this.

I have heard multiple stories of houses not selling for the price they want and them pulling it off the market and renting it out because it can currently rent for enough to cover the cost as they try and wait this out.

Once again, your excellent deadpan analysis of the numerical facts, left me with uncertainty about what it all means.

First question of all, is the yoy measurement of the decline in inflation even statistically different than zero ?

I think, that a zero, average change in inflation lies within the plus or minus range of one standard deviation. More likely than not that all the chaos of the last year has failed to reduce the rate of general inflation, an insidious poison for at least 90 pct of the population.

What I currently think, which could change tomorrow, is that the FOMC are not only not hawkish, but they are doves, lulling we fools into accepting their pandering to the wealthy that own the four asset bubbles that have yet to implode:

housing, stocks, bonds, and the military budget.

Meanwhile the cost to the paycheck society increases 7+ pct per year and their cash flow only increase 4 pct.

The Fed needs to step up their game and raise the FFR rate to > 6 pct. Pronto.

Inflation is, obviously, anchored.

The second question I asked myself was initiated by your bombshell reveal about the potential maladjustment to the measurement by the estimated health care effects, which, if I understood correctly what you were saying, reduced the reported inflation datum by a couple of pct.

Think what ya want, the concentrated corporations are raising prices with reckless abandon, because they can. And we’re paying for it.

Government spending is the largest component of the Keynesian calculation of GDP. The military budget has become the largest component of Government spending.

While I understand the emotional gravity that military service connotes for the generations that remember WW2, I also abhor the crass financialization of our current gross waste that the current military represents.

Rents are through the roof in the Phoenix area.

The inside joke is who would ever pay to live in Phoenix, must have been a young job applicant willing to not drink the water so as to obtain a paycheck. An engineer perhaps.

The Fed will remain hawkish not because they want to but because they have to for the sake of there own existence.

Don’t panic

Low-quality stocks (BBBY, SPCE, etc.) have been rocketing higher. Wall Street is going crazy.

Most economists agree inflation has peaked. The broadest measure, headline CPI, peaked in June 2022 at +9.1% TTM. The narrowest measure, Core PCE, peaked in Feb 2022 at +5.4% TTM.

The Federal Reserve hasn’t given much clarity on the necessary conditions for lowering rates. Is it just lower inflation, or does unemployment need to rise as well? If, later this year, inflation drifts down to something near 2%, but the job market remains solid, do they still cut rates?

” The Federal Reserve hasn’t given much clarity on the necessary conditions for lowering rates.” That POV mystifies me because inflation seems out of control and the FFR is too low to blunt it.

The stock market, in the short run, is not what the economic theory would categorize as a competitive market, especially now that the Fed engorged the criminal banks with $5 T dollars of interest earning reserves.

The house always wins.

What too me is the most disturbing part of this pantomime about the so called “free market” is that it is less than 35 pct of the economy, controlled by a pseudo aristocracy who, obviously, have been painting the tape.

Like Bernie Madoff, unquestionably, legite.

Naivete is a necessary quality of beauty.

I learned a funny new term today with regards to Bed Bath & Beyond, Carvana, etc.: “bankruptcy equities.” All the bankruptcy equities were spiking today, LOL

just computers playing hot potato with each other … that’s the wolves going at it. if retail thinks they’re smart and fast enough to play that game they become wolf food.

that game is great click bate. just look away.

Janes – speaking of potatoes, I’ve heard a few of them muttering about the possibility of dyeing those for the kids this Easter…

may we all find a better day.

“heard a few of my neighbors…” (not potatoes), that is. Apologies, and-

may we all find a better day.

What’s so funny about that? It’s in my opinion a thieving continuation.

You just laughed at the wipe out of kids that had no way to escape this financial carnage.

What do you mean kids that had no way to escape this financial carnage.

They could have not invested in bed bath and beyond and Carvana and not found jobs there in this job market…

I am confused as to how these kids couldn’t avoid the wipe out…

Peaks are relative. If say the Fed did pivot, and say they did pre maturely cut rates or say something else happens like China into Taiwan or Russian nukes or whatever there could be another peak… See the last inflation outbreak

They’ll cut rates when a recession forces unemployment up and kills inflation.

The question is how long will that take and how far are they going to have to push assets down in order to get this done

Rent up 8% for the new year, up 7% last year. Car insurance up 30% last year due to fender bender, we have a $1K deductible. Phone bill up $50 a month because we had to upgrade to 5g, at least I got my phone as a gift. Water bill up, gas bill up, electric bill up, food bill up.

If BCBS increases their medical premiums, we have no choice but to drop them. The dental will go as well by next year.

I had to put in for SS early because we really needed the money. It has kept us afloat, but it won’t in the future at this pace.

> Phone bill up $50 a month because we had to upgrade to 5g, at least I got my phone as a gift.

Mint mobile $15 / month, great coverage.

I killed housing by fixing a REO that became available thanks to the mortality of its 4 previous occupants. The increase in mortality rates of older homeowners with reverse mortgages will allow for this type of access to affordable housing in more substantial numbers.

Housing affordability will get better imho thanks to this. Not romantic, but still helpful.

lean,

Husband and son use their phones for work and need 5g and high data plan. They had to upgrade their phones for 5g and my son gifted me a new cool phone. The downside is expensive phones and high data plans are not cheap. Plus insurance becomes necessary.

Just posting for the rest who are considering lowering phone bills when not using that much. My $15/month plan with mint is 5G up to 4 GB per month. You can buy more if needed.

Google pixel 5+ are 5g, bought mine for under $300.

No one needs 5G. In a few years everyone will because the carriers will sunset their 4G network, but we’re nowhere near that point yet. In real life, 5G isn’t noticeably faster than 4G and is sometimes slower–when the 5G towers in your area are swamped, try manually forcing your phone to prefer 4G and sometimes you’ll get your speed back.

You are a data point indicative of those for whom I am calling out the recalcitrant Fed who are feeling good about their policy because their controllers patted them on the head and said, good boy.

Meanwhile, the people we need are suffering from the curse of inflation.

Funny but when I was a kid, we had one landline phone for maybe $20 a month. Now I have 5 cell phone plans for the family.

I think I can get a landline for $25 or $30. But cell phones plans are $40 a person before tax. So because the invention of cell phone I am paying $230 a month.

I am not sure how these cell phone companies are not rolling in the dough. They really do not have to support the copper lines to the home anymore. The last mile is all wireless.

I think ATT is now charging $5 every time you need to talk to a customer service rep. I use to have them, now glad I don’t.

AT&T deliberately sends the bill late so they can hit you with late charges. They are a fascist organization.

I suspect when you were a kid has was $0.30 a gallon and a nice Buick was $5k. And $15k/yr was a princely salary. So now for the kid-era equivalent of $23 you have 5 wireless phones integrated with powerful computers, cameras, an encyclopedia at your fingertips, email, etcetera etcetera.

“gas”, not “has”

Because they have enormous capex like spending billions on new spectrum and fiber for 5G rollouts. Most are in heavy debt in the 100’s of billions. Plus excluding tmobile they made stupid aquisitions in the past they had to write off or way down.

“I had to put in for SS early because we really needed the money. It has kept us afloat, but it won’t in the future at this pace.”

I feel very badly for people like you. This didn’t have to happen. It never should have happened. The FED destroyed pricing. Now there’s hell to pay. But of course Jerome Powell with his hundred million dollar fortune won’t be the one enduring the hardship.

Analysts keep wondering why so many people are retiring early. Now you know. It’s mostly the lower earning spouse retiring because the family needs the money.

Since the lower earning spouse is usually the woman, this is pushing more and more older women into poverty. I guess they don’t have to wonder about all the homeless old woman anymore.

Petunia

You are not alone,

Ms Swamp had to put in for SS early because she needed the money. In addition, she couldn’t retire because the SS payment was inadequate to pay fixed expenses to live here in a high cost area like Washington D.C. So she continues to work. Actually, she like to work, so its’not all about the money.

> These three months of mega-adjustments reduced the year-over-year rate of the CPI for health insurance from 28% in September to 7.9% in December.

Great work WS untangling all these mega-adjustments!

This is brutal. My goal of not spending anything on US healthcare feels even more relevant. IMHO most OECD countries healthcare systems were on the collapse trajectory way before COVID, driven mostly by demographic aging, regardless of how they are structured.

Hence, focusing on quality of time NOW versus longevity is the way to go, even more so with Climate Change.

My auto insurance went up over 150%. I’m still pissed about it. They cited labor costs as one reason. A decrease of 0.1% in goods I would hardly call a plunge. The Fed is not going to pivot. Wishful thinking on the part of the markets.

> My auto insurance went up over 150%

Which company should we all avoid?

AAA in states that don’t start with M offers good value, otherwise Geico in my experience offers the lowest cost.

My homeowners ins went from $650/yr in 2010 to $1,475/yr today. No claims filed. I asked the dudes at USAA why the increase? They blamed inflation and the Maryland ins commission. Then they hinted at having to pay a lot of hotel bills for people’s homes destroyed in hurricanes and storm surges.

You need to call them and see all that they have changed for coverage you don’t need. Same thing happened to me last year. They increased their “standard coverage”. I ended up with what I wanted for the same old price. Corporate America is always trying and they just need attention sometimes….

Do what you have to do and say what you have to say,

I’m just going to get back to the San Fran Bay.

fever tree

Great review of the Services CPI problem. Were i at the Fed, i wouldn’t be happy about the CPI either.

The steep decline in energy prices in the US is largely attributed to Biden’s draining the SPR. There isn’t any more government oil sitting in the tank to give away, no more elections for awhile to try to buy. And except for last week, this winter has been very mild in North America and Europe, which has kept a lid on natural gas prices. Will that last?

I live in Asia, where one of the biggest macro stories is food prices here. India is urbanizing at probably an even faster pace than China did, which means hundreds of millions of farmers trying to become office and factory workers. In other words, less food being grown here, putting a call on LatAm and perhaps Africa to fill in the gaps, which are huge. And they’re not ready, yet.

These problems are structural and deep. 20 years from now we’ll have roughly the same population in the world, but with 600 million fewer farm workers than we have now. And with all the money sloshing around from the a generation of Fed and ECB and JCB mistakes, no way the developed world doesn’t see a long-term rise in food and energy costs.

If a recession arrives this year, will FED have any tool to start the recovery? They can’t slash interest rates because of inflation!

“Nearly two-thirds of consumer spending goes into services. ”

Interest rates on credit catds now at 20%. That’s “twenty”. It’s kind of 10*2.

There’s your “consumer spending”.

Interest rates for a lot of people were already 30% a year ago.

But now it’s twenty for all of the people.

Nonsense. It’s not. Mine is 14.9% (I just checked), and I don’t care because I use the card to pay for stuff, and I get 1.5% cash back, and I pay it off every month, and never ever pay any interest.

About $5 trillion get paid for with credit cards in the US every year, and nearly all of it gets paid off every month and never accrues interest — just like I’m doing. The amount in credit card balances that actually accrues interest is pretty small, for obvious reasons.

My Father in Law was paying 36% on his credit card. Used it to buy groceries and was completely broke. The credit card companies are like leaches. They suck off the people who can least afford it.

This is true about all the financial institution. They call it risk management, sub prime borrower etc etc

Let’s hope it isn’t running in the family.

Franz Beckenbauer

Don’t worry,

Ms Swamp & I are creatures of the old school. Save your money and buy when you’ve got the funds. Pay off your Mortgage early. Driving a 21 year old car, Still running great.

I forgot to add above, my Father in law even borrowed on his whole life ins policy. It became worthless. Luckily, the VA paid for his burial expenses, and Medicare paid all of his medical bills. I had to shell out $2,500 out of my own pocket to pay Lawyers to settle his estate. He even left a squatter in his house which we took 3 months to evict.

Will be interesting to see if this tick-up in import prices carries through next month as it could indicate more inflation pressure feeding through. Feels like a lot of people have jumped on the inflation is done and dusted train that it’s going to bite back.

Don’t the statisticians have to justify the reduction on health care expense? I know no one who thinks that’s happening!

They did. And it makes kind of sense. Their system of measuring inflation in health insurance doesn’t work very well. So they over-estimated health-insurance inflation in 2022, showing annual health insurance inflation of 28%, and so now they made a huge adjustment to correct for that, and they’re spreading the adjustment over the next 12 months. They make adjustments every year, in both directions, but this year it was just huge.

Click on the link in that paragraph in the article. It will take you to a deeper explanation. Or well, here it is:

https://wolfstreet.com/2022/11/10/services-inflation-spiked-to-second-highest-in-4-decades-would-have-hit-new-high-if-not-slowed-by-biggest-ever-adjustment-of-health-insurance-cpi/

I’m a recent discoverer of this site, and just wanted to say that the depth of knowledge and experience on here is quite something. I like to think I am a relatively intelligent guy, and my brain hurts after spending an hour here.

Thanks to all of you for sharing your wisdom.

My Bookie just raised their commission for running the football pool from 10% to 20%. That’s some serious service inflation, 100%!!