“The prospect of substantial home-price declines puts them at risk of losing money.”

By Wolf Richter for WOLF STREET.

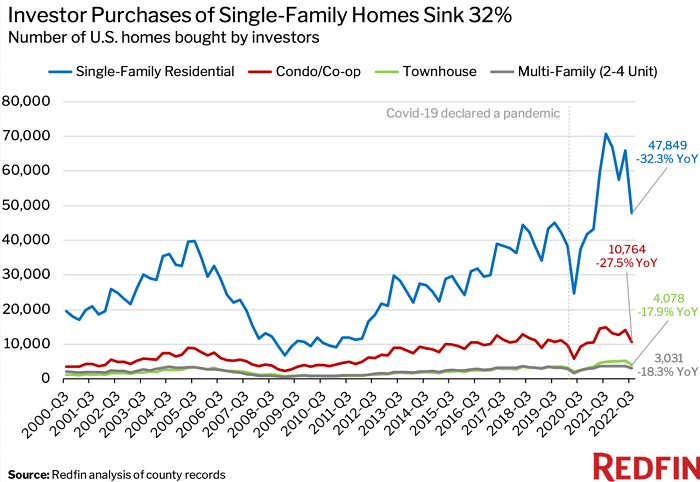

Investor purchases of single-family houses plunged by 32.3% in Q3 compared to the same period last year, according to Redfin, based on county records in the 40 most populous metropolitan areas. Beyond the lockdown Q2 2020, this was the steepest percentage plunge since the Housing Bust.

Investor purchases of condos and co-ops plunged by 27.5%; of townhouses by 17.9%, and of multifamily buildings with 2-4 units by 18.3%.

The chart shows the count of homes purchased by category of homes; and on the right, the year-over-year percentage plunge. These “investors” are defined as institutions or businesses that buy residential properties. (chart via Redfin):

The increase in investor purchases in recent years also shows the impact of a major shift: build to rent, where homebuilders build entire subdivisions specifically as rental houses, fill them with tenants, and then sell the whole development to a big fund manager. Build to rent was the hottest development in the housing market before the downturn.

“Real estate investors are retreating because the prospect of substantial home-price declines puts them at risk of losing money,” said Redfin in the report, echoing what the largest buyers of single-family houses – American Homes 4 Rent, Invitation Homes, and others – have said in their earnings calls.

For example, American Homes 4 Rent, which in recent years has focused on buying build-to-rent developments, said that it had cut its purchases by 80% year-over-year to “allow the market time to recalibrate and stabilize” because home prices have yet to come down enough. “We’re starting to see some price discovery happening. But we’re still early in that process.” It said that these homebuilders still want prices that “you would have seen in March.”

According to Redfin, “It’s unlikely that investors will return to the market in a big way anytime soon. Home prices would need to fall significantly for that to happen.”

“Investors Purchases Plummet in Pandemic Boomtowns”: Redfin.

Some of the metros that investors had piled into with particular devotion are now seeing the steepest plunge in investor purchases.

“Investors expanded in these areas during the pandemic to cash in on soaring rental prices and home values, and are now pulling back as these markets slow down relatively quickly”:

| Metros With Largest % Drops in Investor Purchases: Q3 2022 | |

| % YoY | |

| Phoenix, AZ | -49.4% |

| Portland, OR | -47.4% |

| Las Vegas, NV | -44.8% |

| Sacramento, CA | -43.2% |

| Atlanta, GA | -42.2% |

| Charlotte, NC | -41.7% |

| Miami, FL | -37.7% |

| Denver, CO | -36.4% |

| San Diego, CA | -34.5% |

| Riverside, CA | -33.8% |

Investor purchases increased year-over-year in only five of the 40 metros that Redfin analyzed: Philadelphia (+46%), New York (+11%), Baltimore (+8%), Cleveland (+5%), and Newark (less than 1%).

Investor share of total purchases in Q3.

In those 40 metros combined, investors purchased 65,000 homes of all types, accounting for a share of 17.5% of all home purchases, down from a share of 19.5% in Q2 and from 18.2% a year ago, as overall purchases have plunged, and investor purchases have plunged a faster than individual purchases.

This trend was also outlined by the National Association of Realtors through October, with nationwide existing home sales plunging 28% year-over-year, and the investors’ share of those plunging sales dropping further.

According to Redfin, investors had the highest market share in these markets:

- Jacksonville, FL (share of 29.6%);

- Miami (28.9%)

- Atlanta (27.6%)

- Las Vegas (26.9%)

- Orlando, FL (26%).

In terms of Jacksonville, despite the large share of investor purchases, overall purchases plunged, and investors purchases plunged with them, by 31.9% year-over-year! “Many investors are looking to offload properties,” according to a local Redfin agent, Heather Kruayai: “Almost all of my listings right now are people looking to sell investment properties or second homes. They want to get rid of them now while they still have some value because they’re scared there’s going to be another big crash.”

Investors had the lowest market share in these markets:

- Montgomery County, PA (7.1%)

- Providence, RI (7.3%)

- Warren, MI (7.7%)

- Washington, D.C. (8.6%)

- New Brunswick, NJ (9.7%).

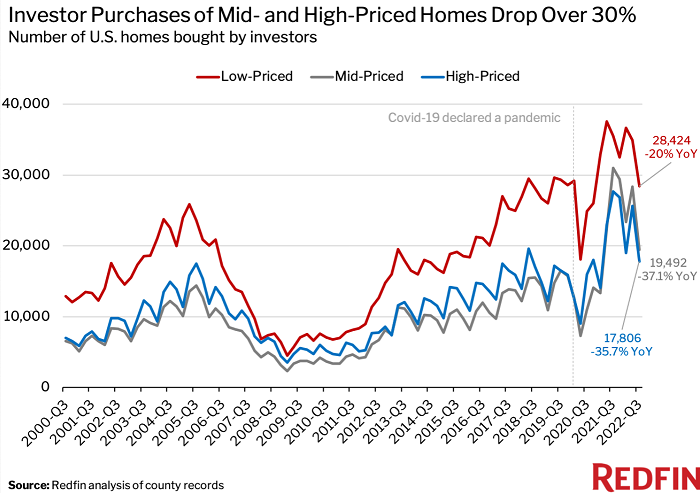

Investor purchases plunged across the price spectrum.

Year-over-year percentage decline of investor purchases by price category (chart via Redfin):

- High-priced homes (-35.7%)

- Mid-priced homes (-37.1%)

- Low-priced homes (-20.0%)

“Investors” in the housing market fall into different categories.

There are the big money managers, such as BlackRock and Blackstone and pension funds that buy entire built-to-rent developments from home builders or entire companies that are already huge landlords. The rental REITs, such as American Homes 4 Rent and Invitation Homes, also buy entire build-to-rent developments. These companies aren’t competing with individual home buyers; they’re buying established rental properties.

Then there are smaller investors buying homes as rental properties, and they’re competing with individual home buyers. But they’re facing high mortgage rates and declining home prices that make this a tough call.

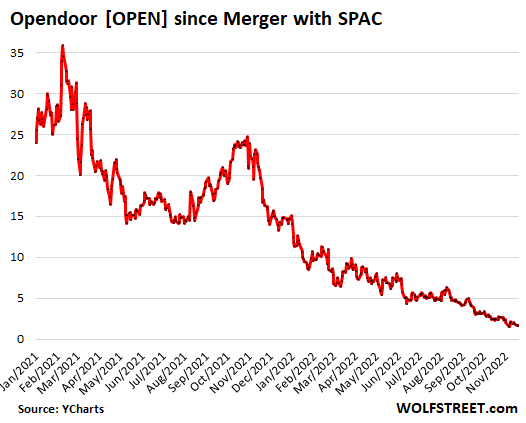

A relatively new development in the investor scenario is the i-buyer phenomenon where companies funded by investor money piled into the house flipping business. This phenomenon has already collapsed. Zillow abandoned it last year amid huge losses. Redfin threw in the towel this year. Opendoor, with nothing else to fall back on, has cut back its purchases. The company, which had gone public via merger with a SPAC in December 20202, lost $928 million in Q3, bringing its total loss since 2019 to $2.2 billion. And every house it bought it has to sell, and that turns out to be much harder than anticipated. Its shares, now at $1.64, have collapsed by 95% from their peak and are in my pantheon of Imploded Stocks:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“The company, which had gone public via merger with a SPAC in December 20202, lost $928 million in Q3, bringing its total loss since 2019 to $2.2 billion.”

SPAC has turned into a four-letter-word, like sh*t. Someone clever out there needs to come up with a snarky new definition.

Single purpose accelerated crushing

Articles on Mainstream media:

2 months back: Housing remains to be a good investment in Long term.

1 month back: Housing is still up year on year. This time is different than 2008 and while prices may not go higher, they should go sideways.

Today: 2023 hung markets look ugly but it will not be like 2008. There will be no forced selling and there is so much demand.

2 months in Future: While there were brutal corrections, housing has become affordable again and investors should come back increasing demand.

4 months in future: There was force selling due to uncertainty in job markets that took significant toll on Housing, but the bad news has passed, Fed is ready to Pivot. So the storm has passed and it will only get sunny from here.

6 months in Future: Job market has still not recovered and continuous lay offs have been hurting the housing. The good news is, the conditions are set for instant Fed Pivot.

Shyster Ponzi’s Always Crash

I’d be good with this. I hate the idea of investors buying up single-family homes in general so I’m fine with this sort of crash. Large multi-family units and big apartments for rentals, sure that’s fine, that’s one of the ways to increase housing supply after all. But there should be strict rules against even small investors (leave alone bigwigs like BlackRock, Blackstone or Zillow) buying up SFH’s that are already in short supply and driving up prices even further. That’s plain corruption, another price paid by the big majority of Americans for dumb QE and ZIRP policy over 40 years so that a few well placed rich speculators could get even richer. AFAIK a lot of countries in Europe (maybe even an EU regulation) have very strict rules against investors buying up single-family homes. Or at least sharp tax penalties for SFH as investment homes, they actually have less of a property tax burden over there for a primary home used to live in, or just tax at purchase and sale–doesn’t make sense to tax a primary home at high rates year after year when it’s not like rising home values actually give you the money to pay the increased tax rates for those values

The US has higher homeownership than Europe. Germany is only around 50%, France is around 64%, UK at 63%, and the US at 65% (which is near long-term averages, despite all the sky is falling rhetoric). Regulation tends to backfire, similar to rent controls.

Maybe you read a different article than I did, but Wolf never intimated a “crash”.

He only observed a substantial decline in the volume of transactions in the RE sector.

Reply to John below:

You’re right… as far as you went.

According to Wikipedia there are close to 50… that’s …five zero… countries with higher homeownership than US.

Sure some are poorer countries than US but not all are in difficult times.

Norway at 80%. Taiwan, Poland, Singapore, Croatia all nicely above 80%.

China and Russia come in just a whisker below 90%. Romania at 89%.

Ahhh but they are terrible homes ?

I wouldn’t assume that.

Most Chinese homes are newer than ours I might guess ?

Its a very assorted mix of countries that have much higher homeownership than the US.

And think of it this way:

One in seven Poles does not own a home. Over twice as many Americans do not own a home…35%.

Worse with China: three and half times as many Americans do not own a home as their Chinese counterparts.

I’m American… cant say I really trust our corporate and government leaders when it comes to good policy … especially for poorer folks.

@Dang

Not saying there is a crash, only that it wouldn’t hurt to have one when prices on even simple starter homes reach such nosebleed levels. And the definition is subjective anyway, large price declines can certainly feel like a crash to big investors who rely on prices constantly going up. It’s often the only way to pop outrageous asset bubbles when they get this large, and restore prices to closer in line to actual incomes

@John Stotes

It’s useful to be specific about what the homeownership percentages actually mean, 65 percent homeownership doesn’t mean that 65% of American adults individually hold a title to their own home and it certainly doesn’t mean that 65% of Americans in younger age groups (Millennials and Zoomers) or couples thinking of starting a family have that kind of homeownership rate in the US. It just means that when you survey home addresses, someone among the person or people in those homes holds a title instead of renting it. So it could mean that an individual (or a spouse in a married couple) indeed holds the title to a home. But it could also mean that the home has boomerang kids returning to their parent’s house because inflation and the housing bubble have made it too expensive to buy their own homes–and those numbers are close to the highest levels we’ve ever seen. It could also mean multi-generation households, 3 under one roof is common in Texas, sometimes also because housing prices and rents are too high. And again, homeownership for Millennials and GenZ is lagging badly. Too, even among the sub-set who are homeowners in the traditional sense (ex. single individual or married couple with dependent young kids), many if not most don’t own those homes free and clear yet, so until the mortgage is paid off, the bank remains a co-owner, and the home could be lost if the title-holder loses a job or ex. gets sick and has high medical bills.

I have no issues with individuals purchasing a second, third or, say even sixth home for the purpose of renting them out. If they want the headaches of being a landlord that’s their problem.

I know of ONE acquaintance whose ‘retirement job’ is taking care of the three homes he purchased for that.

I do FEEL, however, that large corporations should only be permitted to buy large, multi-family rental properties. And not whole subdivisions of single family homes.

That’s MY opinion … my feelz :-)

re: “strict rules”

Agreed.

QE affects asset prices.

” Or at least sharp tax penalties for SFH as investment homes…”

Most US places already have some kind of tax penalty against nonresident owners, in the form of a tax break for owner occupants. Property tax on my house would be about $800/year higher if I moved out and rented to a tenant. Many places the amount is much more.

I will start using it as a verb.

ie. Don’t SPAC your head against the wall, it will really hurt.

Or the large bug SPAC’d into my windshield.

Wrong context.

He just SPACd the bed.

I have to go take a SPAC.

You’re so full of SPAC.

If you SPAC in one hand and wish in the other, which one will fill up first?

I don’t give a SPAC.

Does a bear SPAC in the woods?

He beat the SPAC out of him.

What a SPAC-y ending to the movie.

This tastes like SPAC.

I just stepped in dog SPAC.

You’re SPAC-in me.

Holy SPAC !!!!!!

lol, i’m good with this list

I feel compelled to offer a moment of silence to the poor slobs that fit the criteria you have so ignobly cast them into.

Losing large sums of money on an investment is never pleasant. In this case, it is worse, as you gleefully point out.

I refuse to go so far as to suggest that they should be compensated for their unhappy experience stepping in the dog stuff.

Simply put— all crap

Squalid Ponzi Annihilates Cash

Some People Are Crazy.

With a SPAC-SPAC here

And a SPAC-SPAC there

Here a SPAC, there a SPAC

Everywhere a SPAC-SPAC

Old MacMarket had a con

Ee i ee i o

See People Acquire Crap

Which they most all will routinely do…..in this sick society, anyway.

Cyclists can you name the ride, SPAC.

Wonder if those Chinese and other foreign money still buying hand over fist in SoCal/NorCal market to park their money? Probably still happening in Irvine or Arcadia since asking price from sellers still reflect that sadly..

In the six big counties of Southern California, sales of single-family houses in October have collapsed year-over-year by (California Association of Realtors):

Los Angeles: -39.8%

Orange: -38.5%

Riverside: -41.5%

San Bernardino: -47.9%

San Diego: -40.7%

Ventura: -33.5%

So you do the math on foreign buyers. Investors from China don’t want to lose money either.

Good and good riddance honestly, we won’t miss their money here. Hopefully the next step is for these foreign buyers to start dumping. Now a man can dream if below can happen in SoCal soon enough too..

“Many investors are looking to offload properties,” according to a local Redfin agent, Heather Kruayai: “Almost all of my listings right now are people looking to sell investment properties or second homes. They want to get rid of them now while they still have some value because they’re scared there’s going to be another big crash.”

There is a possible/likely link between foreign buyers of American homes/real estate and the perpetual trade (and fiscal) deficits that DC has been oh-so-blase about for decades.

Put yourself in the shoes of a foreign exporter to the US for previous 20 years.

1) For decades, you’ve had little problem exporting larger and larger amounts to the apparently insatiable American consumer.

2) But

3) What do you do with the USD you get paid?

4) If you bring it back to China (to randomly pick a country, ahem) your own government forces you to convert it into Yuan, a currency *they* control the supply/etc of. At a foreign exchange rate the Chinese G sets.

5) If you take your USD export proceeds and put it into safe US Treasuries, you get paid a destroyed US interest rate that the American G sets. To near zero.

6) You can invest in the vastly over overvalued US equity markets, as your compatriots have already done…generating the overvaluation.

7) or

8) You can take your USD export proceeds and pour them into leveraged US real estate.

9) By doing so, you exploit the ZIRP that would otherwise abuse your savings.

10) and

11) You buy a lavish, safe (ish) escape pod from China’s ultimately authoritarian government.

This sequence of events may very well have been the unspoken history of the United States 2002-2020.

Reply to cas127.

Then, what happen if all, or at least many of, those foreigners start to cash out and move their money out of the USA and to other currencies than US dollars?

It could be combination of QT, high interest rates, falling asset values and a weaker US dollar. With the USA importing CPI infaltion as well.

Yeah that’s also been happening in Vancouver for a while too, ironically the locals in British Columbia practically cheered when Xi and the Chinese government started to impose tougher capital controls on “investors” (often embezzlers) trying to park their money into unoccupied homes in Vancouver that weren’t even being used much as rentals, just basically sitting there rotting and depriving Canadians of badly needed urban and suburban housing. The only people in tears were the corrupt sellouts in the Canadian federal and provincial governments in charge of the provincial housing and treasury authorities. Instead of actually making the hard decisions to raise revenue by taxing the excesses of the Everything Bubble (or taxing progressively at all), they were happy before that to shaft their own citizens and rob them of needed housing by taking the easy route of allowing foreign investors to swoop in and buy at inflated prices. It’s just outrageous for a country or state to allow for mass purchases of scarce housing by foreign investors esp with a housing shortages and housing bubble, and the Canadian, UK and Australian governments (and many US states) are notorious for this. Now with increasing rates there’s a long-delayed comeuppance.

I should say in general I’m not a fan of rising property taxes for home values on a primary home–this has been one of the worst consequences of the US housing bubble, with a lot of tech workers from the Bay Area moving into once sleepy small towns and pushing up home values so much that the locals are priced out and face an increasing property tax burden. It’s not like the rising home values actually give them more revenue to pay the extra residential taxes, basically the costs just to live there go way up while the “asset” (their home) isn’t liquid at all unless they sell. In a sense you really don’t ever truly own your home outright in the USA even if you’ve paid off the mortgage, when property taxes can go up arbitrarily like that due to a bunch of rich outsiders (or foreign investors) driving up local prices, and without actual income rising to pay those taxes–you’re just renting your home from the government, and it can put a lien on that property and seize it by force when those wealthy out of towners and investors move in and push the home prices way up. (Yet another failure of Fed QE and ZIRP policy for 4 decades causing the Everything Bubble in the first place) But it totally makes sense to tax the purchase and sale of homes (which after all does involve a liquid transaction) and to have especially high taxes on investment properties and especially on investors buying up single family homes, to discourage this sort of thing. That’s how a lot of Europe, Asia even South America does it.

What is Fox News, with all the anti-foreigner rhetoric? International purchases are only 2.8% of used home sales. And the top two countries are… Mexico and Canada, not China. And 92% of purchases are under $1m. 43% of these purchases were primary homes, i.e. they live and work in the U.S. (H1B, etc). These numbers are way too small to matter, and they are pretty consistent over the long term, so no trend change to explain the bubble. Let’s just accept that the bubble was caused by the Fed money printing machine and move on.

That 2.8% statistic is misleading. That’s a nationwide average. And it’s used homes.

1. Many foreign buyers buy in very concentrated locations, and there the percentage is multiple times higher, such as in big West Coast cities for buyers from China.

2. Then there is the issue of NEW home sales to foreign buyers. Entire condo towers are being marketed to investors in China with EB-5 visa promos, etc. Investors from China and other countries love to buy new homes, sight-unseen often.

The dollar peg is hurting China investors pretty well to boot

But do it hurt the US dollar?

With the Remimbri pegged to the US dollar, two of the worlds largest economies do in practice have the same currency.

Without the peg, the US dollar part of world economy can be said to decreases a lot.

The dems sure have made California unliveablei live in northern michigan on the west side its pretty rural. There is absolutely NO inventory i just inquired on a modest home on ten acres and by the time the realator looked into it there had already been 4 offers above the asking price.

I think people are fleeing these urban hell holes the dems have created for places like these that are more secluded and less dangerous

Clearly you enjoy living out in the boonies. Good for you. Thank god we all like to live somewhere different, or else we’d all be living in the same place. What sounds like paradise to you may sound like a Siberian penal colony to others. Everyone gets to choose.

Actually its a resort town loaded with some extemely wealthy people buddy.

A long cry from a siberian death camp.

Wealthy people enjoy things like skiing in the winter months and lounging on their yacht in the summer…

“resort town?” That (and your description) sounds like a hellhole to me. I’d rather LIVE in a vibrant real city LOL

The closest I’ve ever been to these places is when I watched Dragnet and The Brady Bunch a more than half century ago.

The Chinese only buy where prices rise not fall. They won’t buy into falling markets.

Wait! All the RE pumpers promised that home prices would not go down much because when interest rates got too high for average Joes to afford a mortgage all the investors and ” cash on the sidelines” would step in a scoop up all the homes for premium prices.

The home prices haven’t reached a premium low price yet to generate a rental yield better than a 1-2 year 4.6% Treasury Bond. Back when Treasury yields were below 1%, rental yields were acceptable.

Even a few large cap beaten down stocks are paying 5-7% dividends. For the moment.

I expect when home prices fall 20%-30% (2019-2020 levels) the sideline cash will start jumping in. We haven’t reached that premium price yet.

Wolf has such excellent charts. Look at the steep climb in 2011-2012 on the first chart where investors started jumping in. This also happens to be the point where CPI inflation intersected with house prices and the housing market price levels regained its correlation with historic inflation.

We aren’t there yet. Another 20% to fall and/or another 10-20% increase in inflation. It took 4 years (2008-2012) for the bottom to be reached last time. I think it will be faster this time.

I think psychology plays a big part also in the timing.

Back in 2008-2010 when houses were plummeting and people were losing their jobs, it is unlikely people were going to jump in with any cash they had left to catch a falling knife.

When prices began to bottom, people were employed again in 2011-2012, they all woke up en-masse and noticed that house prices were very cheap and could yield a good return compared to the plummeting Treasury yields of the time. If your neighbor bought an investment property, so should you.

If house prices plummet 20%, we may have the same psychological effect this time and investors will wait a year or two before jumping in.

Given the pandemic increases alone, I’d hardly call a 20% decline “plummeting”.

At near 7% mortgage rates, mortgage payment on a $400,000 property (about the national median) is about $2600. Add in taxes, insurance, maintenance or HOA, utilities, and possibly PMI and the “all in cost” is at least another $1000 per month.

The CNBC article I read claimed this is “affordable” for a household with an income of $107K (up from $73K a year ago) but it isn’t, not unless someone never plans to retire and has other typical living costs. It’s about 40% of gross income.

Prices, mortgage rates, or both will have to decline substantially to restore actual affordability.

Augustus,

I agree that a 20-30% drop is not a plummet since they were the prices in early 2020. Just 2 years ago.

It is a psychological effect.

MSM and just about everyone have declared that Bitcoin has plummeted down to $16K from $65K. However in early 2020, Bitcoin was at $8K. Is doubling in price in 2 years really a plummet? The same is true for many plummeting tech stocks.

I can see many who “lose” 20-30% of their home value to consider this a plummet. Especially if they refi’d or HELOC’d the equity out of it over the last 2 years.

I still think prices will stabilize at pre-pandemic early 2020 prices. It is a matter of opinion on whether this is a plummet.

Housing is a highly regulated market. As people are priced out of regulated markets they get forced into gray markets. More people converting sheds, garages, living in vans and campers to make ends meet.

Big story in Raleigh news that I think it was around $100 million of Pandemic funding to be used for affordable housing. Has to be spent by 2026. Never let a crisis go to waste.

It’s just a little ol itsy bitsy gully.

The funniest part is most of that “cash on the sidelines” was borrowed in too, part of the outrageous level of leverage that ZIRP, QE and the Everything Bubble made possible. All part of the “housing and stocks only go up” mania of this latest episode of bubble madness. Like one of our financial advisors said years ago, whenever asset prices soar way beyond actual incomes and savings of the people in general, it’s a bubble by definition.

Amazing how the business model devised on “free money” collapses when the interest rate must reflect market prices.

The Fed sets the interest rate, not the market.

It’s closer to a market price, not actually one.

An example is mortgage rates with government guarantees or funded with insured deposits. Due to both, not a “market interest rate” in a long time.

Exactly this, and it’s long overdue. The ZIRP and QE regime was a dumb idea from the beginning, but letting it go on for so many years long after the GFC troubles had been stabilized (and really for 40 years when we think about it, even since Paul Volcker actually fought inflation hard in the early 1980’s) was criminal. Pure idiocy that Ben Bernanke of all people got a Nobel Prize when he and Greenspan were at the center of this before JPow had even gotten his turn at the wheel, but the Nobels these days (even for sciences) are more and more about as realistic and reflective of the way things actually went down as some drunken Tweet or social media post. Even the MMTers had to admit that inflation posed the main bound on the money-printing regime, unfortunately it took a while for the Fed to get the message.

My horrible little town here on Vancouver Island is riddled with empty houses and ridiculous prices, and a whole lot of out-of-province interest. Mercifully, that seems to be waning/mostly-gone, and a lot of empty houses are hitting the MLS already, but I am disappointed (to say the least) that our various levels of government seem incapable of enacting simple policy to keep speculation and hoarding out of real estate. Blows my mind because it cannot be a hard problem to solve, with a little spine and some thick-ish skin.

Anyways, excellent article, as usual, and I am watching with great interest to see what happens with listings in the spring when, presumably, speculative excess will really get wrung out. Fingers crossed, at least. I’d like to own a home before I die and do so without having to delay retirement by 30 years while making some free-money-virus gambler rich.

TEMPLE

“our various levels of government seem incapable of enacting simple policy to keep speculation and hoarding out of real estate.”

Could it be that higher prices drive higher valuations which draw higher taxation rates?

It’s not that they can’t, they don’t want to. They collude with the REIC. All politicians are bought and paid for. They are doing the bidding of the corporate special interests. Your financial situation and well-being are immaterial to them.

Did anyone talk to JPMorgan about what’s going on? They are investing another half billion to buy homes.

“JPMorgan has formed a joint venture with Haven Realty Capital to purchase and develop entire communities of new homes. Their statement says they are seeding the venture with three Atlanta-area communities, and plan to deploy enough equity to acquire more than 2,500 single-family rentals.”

They’re NOT buying anything major now. They’re still trying to raise funds from investors. They’re trying to get investors excited about the fund so that they can raise more money so that eventually they can buy stuff. What you’re citing is a fund promo to raise funds. They’re PLANNING to buy “build to rent” developments. After prices have plunged enough, they may buy rental developments from desperate homebuilders and teetering mega-landlords at rock bottom prices? But they’ve got to set up the fund and raise the money first, and that takes time.

100% Rental neighborhoods end up being sketchy places to live, when there’s no pride of ownership involved. Council estates in the UK are often no go zones unless locals.

Daz,

That’s BS. There are riskier neighborhoods, and there are very safe neighborhoods with predominant rentals. Renting is a life-style choice. This idea that only poor people rent is also BS.

There are tons of higher-end rentals, single-family and apartment, for people with money and people who are mobile and don’t want to deal with the hassles and costs of homeownership. For institutional investors, that’s where the money is. In the US, nearly all big institutional landlords try to focus on that segment. The slumlords you’re talking about – they exist but are just a small portion of institutional landlords.

For example, about 2/3 of the housing stock in San Francisco is rentals, and the median two-bedroom rent = $4,000 a month. These are high-income people that rent in SF because they want to. They could buy a house in the boonies just fine, but they don’t want to. It’s a lifestyle choice.

Daz,

I have visited council estates such as you describe.

For non-UK readers an explanation of ‘council estate’ may be helpful: it’s a complex of housing built by local government expressly for rent to those in greatest need of shelter.

The landlord is the local government, rents are low and evictions are rare – even in cases where tenants behave badly.

According to a WSJ headline, the key to avoiding high mortgage rates is to pay cash for a home.

Dolts… all of them.

That’s why cash purchases are up. For people with cash, that’s a good option. Where else are you going to earn a risk-free essentially untaxed 7% return on your cash? But that’s the effect of paying cash instead of getting a 7% mortgage. Money saved = money made.

Sorry, I was just laughing at the headline.

I’m sure many WSJ subscribers have $1M in their savings accounts.

However, sadly, not me or my son.

What about the risk of the price decline? That’s a huge risk that cash buyers assume. Cash buyers can’t mail the keys back to a bank, as though the transaction never happened.

But why would they?

Yeah, this would seem to be a huge risk unless someone truly has cash to burn. Though given the dumb excesses of the Everything Bubble of last few years, that’s probably not that small a number.

Bobber,

There are only 12 states that have “non-recourse” mortgages, and in those states the homeowner can hand the home to the lender and walk away. It still ruins your credit rating, and a person wealthy enough to pay cash for the home isn’t going to readily do that over some loss on the home.

In the remaining 38 states and DC, homeowners are personally on the hook for any deficiency when the home is sold at a foreclosure auction and the proceeds aren’t sufficient to pay off the mortgage, interest, fees, and expenses. So if you have $1 million in assets that are not your home, you’re going to think twice before you walk away because they’re going to go after this money.

I should have voiced my main point, which is that mortgage rates have doubled in less than a year, after a ridiculous 10-year price boom, and prices haven’t had time to adjust yet. I believe its one of the worst times in history to pay cash for a house on the Coasts, which is where much of the investment goes. Getting 5% on a treasury is a much better bet at this point.

A lot can change in a couple years. Why not wait until the downward price trend ceases? It could save you 40% of your capital in many areas.

As an example, families in my neighborhood that purchased in the frenzy earlier this year in Seattle are already showing 25% losses in the $400k to 500k range. That’s a lot of cash to lose in a few months. Ouch.

“…are already showing 25% losses in the $400k to 500k range. That’s a lot of cash to lose in a few months. Ouch.”

Actually, they didn’t lose any “cash.” They should stop looking at Zillow every day, enjoy their home, make their mortgage payments, and come to grips with the fact that a home is an expense, not a leveraged high-risk bet on home prices.

Why didn’t I think of that?

House keys are also good stocking stuffers for many families.

Its all fun & games until the NRA commercials come on tv, with Larry Yun dressed up as Santa Claus imploring you to give a loved one a house for xmas, ho ho hope!

*NAR

Things can get a little confusing here in the heat of the battle.

The car commercials you start seeing this time of the year where a spouse buys the other a new luxury car for the holidays is equally cringe. I just saw my first one of the season a couple days ago.

What?….you don’t believe in true love?

If I purchased a new car without my wife approving, she’d immediately return it.

After 35 years, her decisions and tastes surprise me sometimes. Maybe that makes it work.

Look at those price cuts, even in popular American cities.

Meanwhile, the politicians and elites in Canada are planning to protect the housing bubble at all costs, at the expense of Canadians, healthcare and climate change.

Canada is a Pyramid Scheme. Bring in more Greater Fools to pay sky high prices for real estate

The people are voting for it. All people who own real estate want the high prices, no matter what it means for the young and the poor. “F**k ’em if they can’t take a joke” is their attitude. It’s a religion of greed.

I whole heartily echo your “Fxxk you” sentiment, may I also add flippers and RE investors to the mix as well?

Are Canada, America, Great Britain, Australia and New Zealand bringing back the landed gentry like in feudal England?

Seem to be moving in that direction. Feudalism 2020’s style, here we come..

Don’t take the easy way out and just blame the well to do.

The Middle Class is all too happy to have politicians support NIMBYism or whatever else that improves their home values. Less new housing construction, especially low end ? Great ! …you can hear the Middle Class homeowners exclaim.

Rich investors buying up homes everywhere creating bidding wars ?

Great ! …you can hear the Middle Class homeoeners exclaim.

Anything to make their home price increase they will likely applaud.

Politicians care more about the upper and middle class than they do the poor. Ditto the media. This includes so called liberal politicians.

I think your POV is disjointed from reality. First, the young and the poor aren’t trying to buy houses. As Wolf’s article convincingly indicated, the prices for commercial purchases of single family homes is declining.

The sheep can only be sheared when they have a full coat.

I live in Eastern Washington state.

About a year and a half ago I read that based on a survey (per some consulting firm from the west side of the state) one half of the renters in this county would like to buy a home… most haven’t because it’s not affordable to them.

Never could understand this attitude that rising home prices are just assumed a good thing, even for real estate owners. This just means costs of doing maintenance, property taxes, repairs, insuring anything go way up for the sake of a theoretical value assessment. It’s only concrete value is at the point of sale, but if a homeowner isn’t selling at the moment (big majority aren’t), seems like the higher home values just means more costs than benefits

Its interesting how this point gets overlooked:

” All people who own real estate want the high prices, no matter what it means for the young and the poor. ”

I have a dubious view of my fellow Americans even if they are often hard working and clever.

The middle and upper class dont give a hoot about the difficulties the poor face. Anything that would cost the typical middle class family money is bad news even if it benefits the poor.

Politicians talk race and gender, occasionally indirectly ethnic concerns. But class differences, huh ?

It surprised me how very little attention the liberal TV media and politicians had given to affordable housing up until the last year or two. And even now its mostly focused on the homeless. The homeless deserve concern for sure. But the more general issues of housing: poor people unable to buy a home, new construction too large or too tiny, unavailability of manufactured home subdivisions. etc… are not discussed by liberal politicians or the TV media. Not that I have seen.

Why is that ? I believe its because of what you wrote: they don’t want to offend homeowners by pushing for more affordable housing that might, after all, hurt or at least not help, the values of current homes.

Politicians. including liberal ones, don’t want to risk losing homeowner votes. The liberal television media doesn’t want to lose advertising dollars. Or they don’t want to lose viewership by putting off homeowners.

Australia is very similar, with money from mainland China being a substantial influence. We’ll see how it plays out with that country’s economy slowing, Covid lockdowns blocking traveling abroad and the clampdown on ostentatious spending and capital flight.

I watched some Milton Friedman clips in Freedom to choose.

Everything he argued with a Congressman, a former Fed head and a West German central banker are coming to light.

Printing money, lowering interest rates and government spending fuel inflation.

Then they try to tax or gain more revenues to fill the deficit at the expense of everyone else.

“Overdrawn? But I still have checks left!”

Works on paper.

The government increases taxes on the working class while giving more bailouts via inflated contracts. Works like a charm.

Why is the government and the central bank colluding beats me.

Where to begin. I guess your first mistake was admitting that you internalized the thinking of one of the worlds greatest economic crackpots of all time. An non-combatant aristocrat spewing guesses.

His insane ramblings, without a shred of proof, have been tolerated by the Ivy league out of fear of his ancestry.

And now add the layoffs to the mix. Tech workers are highly paid with lucrative RSUs. There is a lot of fear out there, therefore the downward pressure on home prices will be more pronounced going forward due to fear of job losses. Many H1-B workers who bought will have to sell and move back to their home countries as well.

Fed speaker George admitted that MBS buying led to housing inflation, and said he would stick with raising rates no matter what.

The stock market once again rallied today and showed the finger to the Fed.

The “free market” will certainly rise before “black Friday”.

A rally has a different meaning to different people, I’m sure. The choreography of today’s rally as an enticement to splurge on black Friday was, I admit, troubling.

It is the Fed’s finger that has been firmly secured up the arse of the “free market” for 15 years. Suddenly, we are supposed to believe that they are acting independently. You first.

A much awaited unwinding of malignant zero-interest-driven processes, and it can’t happen fast enough.

Yep, rode up on the gondola in Telluride with a guy and his family. He’s bragging about owning 5 homes in Aspen and looking to buy in Telluride because it’s so cheap. This was 7 yrs ago and I commented about how the housing market will go down and people who want to live in Mountain towns can’t afford it. His response was that I just need to make more money. I can’t help but hope that dude ends up homeless.

I have a house in Aspen. If this conversation was 7 years ago, today he stands at a great return.

Oh yeah. I was wrong but I hope my timing was just off. The hording of homes should be illegal and just making money and bragging just makes you a doushbag.

For every one of those liars there are two. I certainly don’t share your enthusiasm for homelessness as a remedy for ignorance, otherwise Wisconsin would become the disaster area that I believe it must be. Based on the unfortunate encounters I have had with residents of that state that were “enjoying” the west.

The Fed pay attention to interest rates, but not to money. Money move

the world around. Money disappear in a sucking sound.

M1, the real stock of money, is down from $7.3T to $6.7T since Jan 2022.

Where did the $600B go : we don’t know.

The want for money is growing. Money shortages are signs of recession.

not inflation.

Where could $600B have gone? Maybe Bankman-Fried could give us some ideas.

Oh the irony of that guy’s hyphenated name.

Bankrupt- Fraud

Can’t throw a dart at the map in Phx without hitting a house for sale at some ridiculous price by open door or offer pad etc.

I own several properties in one of these hot Southeastern markets.

I still receive 4-5 calls a day per property from various outfits asking if I want to sell.

In the meantime, although prices are down by only a little bit, sales volume is low, inventory is building by quite a bit, days on market has nearly doubled in the past several months and rents are down. The housing trend is down… Seems like a stupid time for investors to be trying to buy houses but they are certainly still trying, hard. These calls BTW, although they are auto-dialed, are always handled by a live person so there is definitely an expense associated with making them (unlike say recorded robocalls).

These are people on the hunt for forced sellers and they exist during every period. Obviously they’re not offering nearly enough money interest most, but I imagine real estate work is pretty slow right now.

These cold-calling ‘will you sell your property to me’ calls are a new phenomenon which started with the pandemic.

Even a forced seller would be wise to test the waters of the market before taking the first call they got out of the blue.

Real Estate is local and regional. The places were price doubled the past few years are seeing some big price declines.

I am in the midwest and I see what you are seeing.

– median prices have not rolled over. They dipped briefly in August but rebounded since and are at new highs.

– sales volume is way down

– inventory has increased from the bottom this past spring. Inventory is probably up 30 to 50 % from the bottom. But inventory is still about 40% lower than the historical average.

I keep waiting for prices to roll over but they have not yet.

There has been a disturbing trend of hoarding real estate. In 1970 a single family home was 1500 sq ft. In 2020 it was 2300 sq ft. Real estate is one of the most popular investments known. In 2006 home prices peaked in a number of markets. Five or six years later prices bottomed. There was a wave of foreclosures and bank failures. AIG insurance needed a government bailout.

The data seem to confirm my suspicion, that the housing thing might be a classic example of the extended definition of the basic “bezzle”. A term originally coined by JK Galbraith, that captures Minsky’s third, Ponzi, stage of his Financial Instability Hypothesis. Further extended by Charlie Munger,

“what should be recorded as a speculative rise in the price of an asset is recorded as an increase in operating earnings, which in turn increases the value-added component of the GDP calculation.”

as cited by Sal Syat via Yves Smith and the Naked Capitalism blog

From the Carnegie Endowment for International Peace cited in the NC article:

“But as Minsky explained, “over periods of prolonged prosperity, the economy transits from financial relations that make for a stable system to financial relations that make for an unstable system.” Because the bezzle is, by definition, temporary (though it may last for a few years or even a decade or two), at some point the bezzle will be eliminated, and its elimination will reverse the earlier boost to the economy. When that happens, what appeared to be a virtuous cycle becomes a vicious cycle.”

My cliff note understanding of what a “bezzle” is, I have invented a scenario in which two friends decide to go to the neighborhood tavern. One friend has a wallet with 300 bucks in it because he is paid well. The other friend has a wallet with 10 bucks in it because he is not paid nearly as well and he has a family that depends on his contributions into the family financial pool.

Rich friend asks his buddy to hold his wallet so that he doesn’t blow it all. The other friend, now endowed with a pocket full of cash, begins to be inebriated and starts spending the cash in his pocket, matching the spending of his rich friend that is confident that his 300 bucks is safely being monitored by his friend. Spending in the neighborhood tavern explodes because there are two rich guys paying.

The rich friend continues to spend thinking that his money is secure while his friend also spends the money doubling the intended spending.

On second thought, maybe my personal experience is not as straight forward an example of the bezzle as I originally thought.

Michael Pettis wrote the CEIP article and further states:

“The bezzle cannot be quantified, and it cannot even be proven to exist until after the fact. ………

…… when there is a significant (albeit temporary) divergence between the perceived value of assets in an economy and their future contribution to the production of real goods and services—whether this divergence is created by fraud, irrational exuberance, or malinvestment and other forms of nonproductive investment—this divergence will change economic behavior and activity in ways that are not sustainable.”

“divergence between the perceived value of assets in an economy and their future contribution” is a wiggle phrase, as if this troupe are likely to take exception. Will the selling price of an existing home decline by 35 pct ?

maybe. That is the current market clearing monthly payment that the best that American society has too offer, can afford.

Good to see people are reading Michael Pettis.

I highly recommend all his articles.

Barron’s announced today that “stocks have already bottomed”

Ha. that’s like me announcing today that real estate has already bottomed.

Wall Street never stops trying to lure in the suckers to offload their crap to, I mean spac.

I got an email from a realtor yesterday with his Q4 update. He assures me now is a good time to buy because prices are down 10% which is the average of the price reductions the last few downturns.

Also, and I wish I was making this up, one of the other reasons to buy now is that creative financing is back. There are now 7 year interest only loans at 5% that have the same monthly payment of a 30 year mortgage at 2.91% that you could have gotten a couple years ago. “If you want to pay 10% less than a few months ago with a similar monthly payment, now is the time to buy!”

Welly,

For the past 15 years, I have been the “sucker”, suffering through zero pct interest, sure that the bezzle in the asset market would resolve itself in a collapse, at any moment.

I am not, nor have I ever been an economic disaster ghoul, wishing for a collapse that would validate my conservatism.

What I may currently be, is an old guy who remembers too much bullshit

that

I wish I could forget, like hell.

I’m a survivor having been hit in head several thousand, plus times, during my sports audition, which spanned from the day I was born until I earned my degree in Engineering.

Heaven Forbid that I would dare to recommend a course of action that would, inevitably be misconstrued as doctrine.

About the coming economic down turn that, frankly, there is a cohort that yearns for it. I do not but am unsure of the future. Which reminds me of a day 45 years ago.

To prevent hoarding retailers like grocery stores put a limit on how many items can be purchased when supplies are limited. Why doesn’t the government apply that principle to housing?

We don’t need a limit, we need investment properties taxed at double owner-occupied properties.

Long ago, where I live, owner occupied properties were taxed at 6%, rental properties at 10%. Now all property is taxed at 10%. I think second homes were at the owner-occupied rate, but don’t remember for sure.

Also tax the income on AirB&Bs at hotel rates, because that is how they are rented.

Tax it high enough and there is less of that investment. Maybe a sliding scale. The more properties owned as rentals the higher the tax.

Apartments are considered one unit because we also need those rental units in a tight market.

In Florida that is essentially what happens since although the tax rates are the same (investment vs. OO) on paper, investment properties don’t benefit from the homestead exemption, other tax discounts and also aren’t subject to an annual appraisal increase cap. The result is that investment properties generally pay significantly more in taxes over time.

However, while this is an interesting concept in theory, it hasn’t done much of a dent in home price appreciation, with prices having almost doubled in the past two to three years, while investor purchases have skyrocketed nonetheless. Moreover, the higher taxes are normally just passed on to the tenants in the form of increased rents.

Yeah Florida’s had some of the worst rent increases esp around Tampa, a shame because like you say things like the difference in policies for the homestead exemption and cap should’ve put a lid on some of that investor speculation with property in the state and advantaged owner occupied SFH’s, but looks like some of the investors just decided to dump the costs on their already struggling renters and pose an even bigger burden on their incomes and savings

CONgress responsible.

IRS tax form treatment differences-

Schedule A or standard deduction for owner-occupied.

Schedule E for Ma & Pa landlords. Combination of E and A if owner-occupied 2/3/4 flat. Limited deductions. Big phase-outs once the owners make more than $100,000 from their real jobs. That amount has been set more than 20 years ago.

Schedule C for Corp landlord. All sorts of write-offs and deductions. Buy the Escalade to check on the properties.

Would never happen. RE investment is a massive industry.

The novice passive income types are starting to sweat, at least in my area. Rents are still absolutely crazy, but I dare say just starting to come down a bit. In the past few weeks I’m seeing Craigslist ads from small-time landlords that are down right hilarious with off-putting, sharp, extensive demands of their tenants’ lifestyle/character and read as if exhasperated new landlords finally encounted the reality of the business. No responsible tenant wants to rent from a bitter, fried and invasive newb.

After 20 years of responsible renting, this side of having a multimillion dollar investment business and excellent legal team on call, you couldn’t pay me to take out a 2nd mortgage to buy a short or long term rental unit. OPM is not worth the headache.

Well… New home sales for October yielded some unexpected numbers. According to MW, sales rose 7.5% from 588,000 to 632,000. And one might expect that maybe home builders are finally dropping prices to snag those buyers and strengthen volume, but nope… Median price made a massive jump from $455,700 for the prior month to a record $493,000. Nuts.

If investors have been pulling back, then I would think that these weird October numbers represent a larger share of independent private buyers. So I guess folks who can afford a half-million dollar home are still doing surprisingly well, even at these higher mortgage rates.

I’ve said before and I’m going to keep saying it… Continued interest rate hikes are the wrong tool. We simply printed way too much money. This insanity will not properly end until we either remove a sufficient amount of that money or inflate our way back to equilibrium like we did 40-50 years ago.

hahahaha… 7.5% uptick after 11% plunge:

https://wolfstreet.com/2022/11/23/massive-cancellations-make-mess-of-already-low-new-house-sales-inventory-glut-at-deep-housing-bust-1-level-buyer-traffic-plunges/

These sales are based on signed contracts between buyer and homebuilder, and they’re no indication of how many of those deals actually close. And those sales that actually close are far lower amid a huge wave of cancellations. Homebuilders have been lamenting those cancellation rates for months.

These new house sales based on signed contracts haven’t been reduced by these cancellations… reaching a 49% cancellation rate in the Southwest

Hot off the press just for you so you don’t have to be misinformed by reading headlines:

https://wolfstreet.com/2022/11/23/massive-cancellations-make-mess-of-already-low-new-house-sales-inventory-glut-at-deep-housing-bust-1-level-buyer-traffic-plunges/

“An important provision of the G.I. Bill was low interest, zero down payment home loans for servicemen, with more favorable terms for new construction compared to existing housing. This encouraged millions of American families to move out of urban apartments and into suburban homes.” – Wikipedia

Wolf really likes using the word “plunge.” Would that make a good drinking game?

QE bubbelized the heck out of every little or big thing, no matter the asset class. every thing in America is way over priced, especially homes. We bought our home right before Alan Greedspam began QE liftoff in the 1998 financial crisis. its really sad looking back over the past few decades how QE has hollowed out the core of our country. wages are the worst for the majority of job holders, and the few industries left that pay well are corrupt as can be. its pushed every mom and pop into a plethora of scams. ftx MERELY one of the latest.

the worst is yet to come though for many countries, especially those who dont produce their own energy or food. millions will starve or freeze over the coming winter across the globe.

germany will suffer bigly. its auto industry will be decimated without plastic, which needs natural gas feedstock, and russia has cut that off.

2023 will be known for a humanitarian crisis far worse than what occurred during the peak of the covid pandemic.

QE was indeed one of the greatest financial crimes in US history, and an indictment of incredibly corrupt Federal Reserve policy to benefit asset-holders, investors and plutocrats at the expense of hundreds of millions of US workers. We’re just beginning to tally the damage. That having said, not sure I follow the last part of your comment. We were just in Europe on a multi-country business trip and they’ve been surprisingly resilient, Germany esp has been a whole lot stronger than expected and they’ve been very careful to diversity their energy sources. Remember they get a lot of natural gas from Norway (and they do have their own North Sea sources) and are getting more piped in from ME sources, and from African suppliers as well. Also, although this isn’t said out loud too much, Germany still does get a lot of NG from Russia even if just through back-channels–it’s not like this is a one-way issue here, Germany has a diversified economy (and a lot of alternative energy sources to help fuel it), while Russia’s already teetering economy absolutely depends on those gas and oil exports, and they have very little else to stay afloat. Without exporting its gas (a lot of it to western Europe), Russia has basically nothing to even maintain a functioning economy, and it practically falls back to 19th century standards. And it doesn’t matter how much repression they try, if the economy collapses that hard, the Russian government gets overthrown if things fall even slightly further from where they are, and the people have little to lose. There’s also lot of increasing LNG shipments from US exporters and NG coming in from Iran, again sometimes from back channels (though Europe doesn’t have this hangup about Iranian exports like the US–that’s not their fight, we got ourselves into that mess with the Mossadekh coup in the 1950’s). We were in Germany around the time the Q3 numbers came out and all the experts were expecting a deep recession to be announced, instead Germany posted a lot stronger growth than expected. Source diversification is a big part of their policy.

Germany is a shell of what once was..

The long-term charts are really interesting to me… especially the first one which shows Investor Purchases of Single Family Homes. You can definitely make out a plunge in single family house sales in the mid-2000s which took place LONG before the supposed market implosion in 2007-2008. It kind of takes the wind out of the sails of the argument that “no one” saw the Great Recession coming.