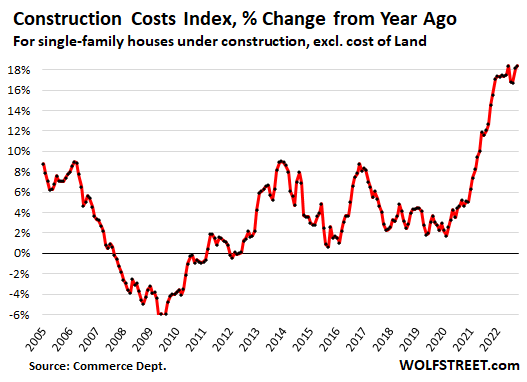

Another thing: inflation. Just when you thought the construction-cost spike was abating, it hit a new record.

By Wolf Richter for WOLF STREET.

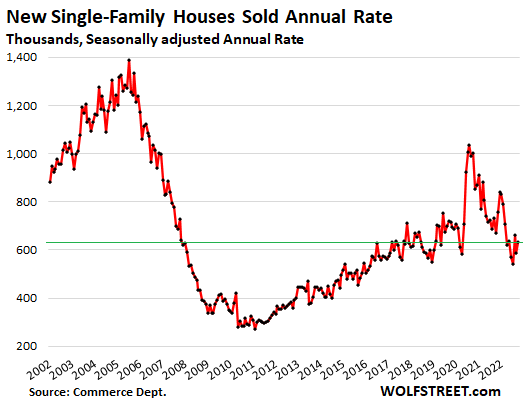

Sales of new single-family houses have been zigzagging along low levels for months. In October, they rose 7.5% from September, after having plunged 11% in September, according to the Census Bureau today. At a seasonally adjusted annual rate of 632,000 houses, they were down 5.8% from the already low levels a year ago, and down 37% from two years ago.

These sales are based on signed contracts between buyer and homebuilder, and they’re no indication of how many of those deals actually close. And those sales that actually close are far lower amid a huge wave of cancellations. Homebuilders have been lamenting those cancellation rates for months. But those cancellations are not reflected here. We’ll get to them in a moment.

A similar plunge occurred in sales of previously owned homes: -34% from peak in October 2020 and -28% from a year ago.

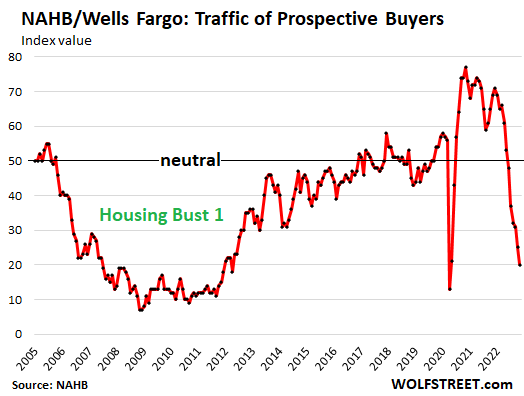

Homebuilders reported plunging traffic of prospective buyers of new single-family houses, according to the National Association of Home Builders last week. Its index of Traffic of Prospective Buyers has plunged for eight months in a row and in November fell below the May 2020 level.

Beyond the lockdown-low of April 2020, it was the lowest since 2012, during Housing Bust 1. But this time, the descent has been far faster than during Housing Bust 1

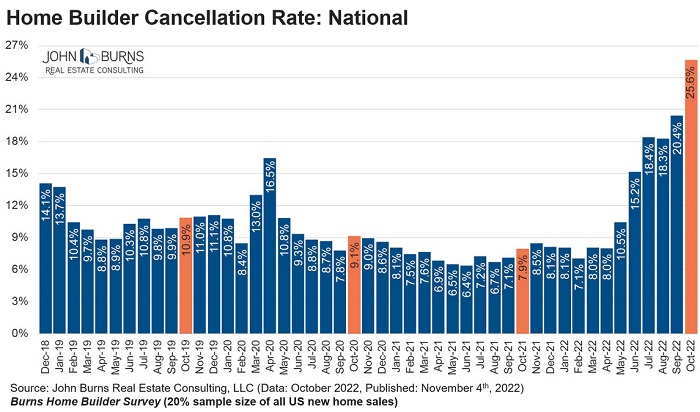

Cancellations Spike, worst in the Southwest.

And many of those folks that do show up to look at a house, and that then do sign a sales contract are massively getting second thoughts, followed by buyer’s remorse, followed by canceling those contracts – and those spiking numbers of cancellations are not included in the new-house sales data by the Census Bureau above, which just tracks signed contracts.

According to the homebuilder survey by John Burns Real Estate Consulting – with a sample size of roughly 20% of all new home sales – the cancellation rate spiked to 25.6% in October, up from a rate of 7.9% in October 2021 and from 10.9% in October 2019. Over a quarter of the signed contracts are cancelled! Chart via Rick Palacios Jr., Director of Research at John Burns (click to enlarge):

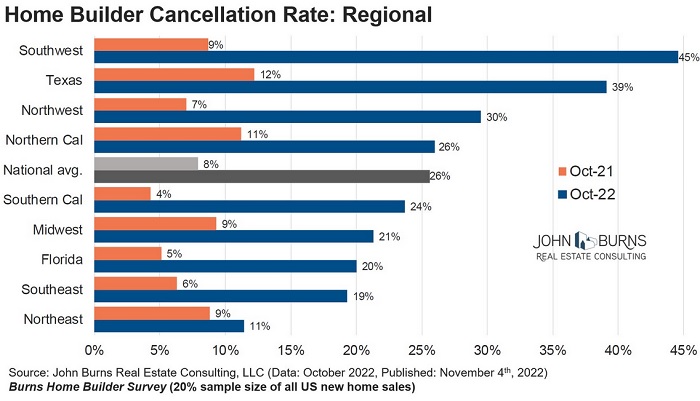

The cancellation rates vary substantially by region: In the Southwest, the cancellation rate spiked to 45%. Nearly half of all contracts signed are then cancelled! This was up from a cancellation rate of 9% a year ago. In Texas, the cancellation rate spiked to 39%, up from 12% a year ago.

This kind of huge spike in cancellation rates renders the sales-contract signings data a practically irrelevant figure because a cancelled contract is no longer an actual sale (chart via Rick Palacios Jr., John Burns, click to enlarge):

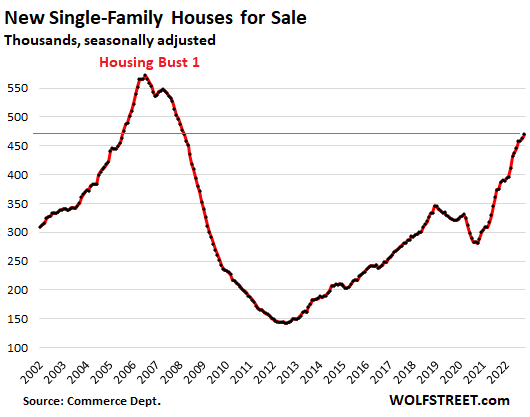

From shortage to glut: Inventories continue to spike.

Inventory for sale in all stages of construction jumped to 470,000 houses, up by 21%, from the high levels in October last year, the highest since March 2008. Compared to the early phases of Housing Bust 1, it was the highest since September 2005:

Supply of unsold new houses has been in the 8-10 months range since April, due to the combination of low sales and the surge in inventory. Supply in October was 8.9 months, Housing Bust 1 levels.

But supply is figured as how many months it would take to sell the current inventory at the current rate of sales – but the current rate of sales is based on contract signings, and those contracts are getting canceled at record rates, and the fact that sales keep falling through is fueling the relentless surge in inventory.

Another thing: inflation. Just when you thought…

Construction costs of single-family houses – excluding the cost of land and other non-construction costs – seemed like they’d peaked in June, and then the spike slowed or stalled, and on a year-over-year basis, the spike backed off from a historic record of 18.3% in June to 16.7% in August. But then it started spiking all over again and in October hit a new historic record of 18.4%. This inflation will continue to dish up surprises, just when you least expect it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I thought that the fall in lumber prices would have reversed a little of that inflation. I wonder how much of that inflation is labor costs versus materials.

The market continues to live off the pivot theme.

“The market continues to live off the pivot theme.”

Look at the one-year chart of the 10-year Treasury yield and see if you can spot anything unusual. No, everything is normal: a big surge in yield to new highs is followed by a smaller pullback, which is followed by a big surge to new highs, which is followed by a smaller pull-pack, which is followed by a big surge to new highs… that trend is perfectly intact. Don’t get distracted by the day-to-day movements.

Had this comment on Crypto article, but it fits better here. As per Mainstream media:

4 months back: Housing remains to be a good investment in Long term.

2 month back: Housing is still up year on year. This time is different than 2008 and while prices may not go higher, they should go sideways.

Yesterday: 2023 housing markets look ugly but it will not be like 2008. There will be no forced selling as there is no credit risk and there is so much demand.

2 months in Future: While there were brutal corrections, housing has become affordable again and investors should come back with increasing demand.

4 months in future: There was force selling due to layoffs and uncertainty in job markets that took significant toll on Housing. However, the bad news has passed, Fed is ready to Pivot and it will only get sunny from here.

6 months in Future: Job market has still not recovered and continuous lay offs have been hurting the housing. The good news is, the conditions are set for instant Fed Pivot.

……….

And so it keeps going on for people who don’t read wolfstreet.

Spot on.

all this says is that rental market will remain with 95-98% occupancy

hmm, wonder how I should react??

Leo – that is a very perceptive script you have crafted for “House Bust 2 – the Sequel”.

I particularly like how you weaved in the “this time is different” delusion.

It reminds me of the famous Italian film director and screenwriter, Bernardo Bertolucci, who once said the secret of a good film is to “delay the f**k”.

Using your script, there will be a lot of rent-seekers in 6 months from now who will be totally f**ked.

LOL

Haha

This seems brutally accurate for the Long Island area. Sellers still seem to be delusional with asking prices, and if anything it seems they creeped up even more.

My next door neighbors are retiring and moving back to Turkey. Selling the home they’ve had for 20 years and that he painstakingly upgraded/renovated himself, from the bathrooms to the immaculate paver driveway. Asking price? Redfin estimate at 1.06, his agent lists it for 1.09. Lady trying to eek out some 30k profit on top of the already crazy price of the home. Has had open houses the last 4 weekends, only 4 people came looking the first weekend, nothing the subsequent ones. No price drops.

If you had to pull a mortgage with 20% down, at 7% your payment was an astounding $8900 a month. For West Hempstead school district that is insanity.

Sounds about right.

Our backlog kept us from servicing machinery & hunting

in Nov.

In the past month my friends who own small manufacturing

are back to visiting clients.

Will it be like 08? I understood the labor force dynamics back then. This time around I do not.

Totally, well said. Captures the cluelessness of the mainstream media and financial media esp, they’re a one-trick pony in service of the investor and plutocrat class, have been at least since Greenspan started the whole QE mess. They’re junkies addicted to the next hit, fantasizing about a pivot to get them more of those hits they crave, and now as the painful reality dawns on them that they’re going to have wean off their habit, they’re screaming at the top of their lungs or finding all sorts of wishful thinking to convince themselves someone might re-inflate the housing bubble and other asset bubbles. Those bubbles are the source of this nation-ruining inflation in the first place, so it’s not happening. But they need to get high again, so they try to fantasize otherwise.

Miller,

Not picking on you, but I am SICK of MSM being written of as “clueless”. You sound like Palin, Trump, et al, who would prefer you seek out their chosen “alternate” news….(alternate “facts”)

Media corporations are HUGE, and getting bigger ALL the time. Comcast, for example is the largest American owned media conglomerate. 2nd biggest in the WORLD.

PLEASE PLEASE look them up and see who they own.

Here’s their Board of Directors,

Board of directors[edit]

As of May 17, 2020:[25]

Brian L. Roberts, chairman and CEO of Comcast

Kenneth J. Bacon, former Fannie Mae executive

Madeline S. Bell, president and CEO of Children’s Hospital of Philadelphia

Naomi M. Bergman, senior executive of Advance Publications

Edward D. Breen (lead independent director), executive chairman and CEO of DuPont

Gerald Hassell, former chairman and CEO of The Bank of New York Mellon

Jeffrey Honickman, CEO of Pepsi-Cola Bottling

Maritza Montiel, former deputy chairman and CEO of Deloitte

Asuka Nakahara, former CFO of Trammell Crow

David C. Novak, former chairman and CEO of YUM! Brands

You would call these people “CLUELESS”? Deloitte is a nice touch.

Compared to WHO? Compared to WHAT? Your selves? Your belief structure? That’s FN hilarious!

They have a better designed AGENDA than anyone here.

Wolf is “alternate media” but it’s the one I prefer…..few predictions, just a snapshot in time and some food for thought.

Basically what Adam Smith did, and any good social scientist does…..he didn’t write a prescription that holds true today, anymore than the “Founding Fathers” did.

And someone PLEASE get real about why they chose to ignore Tom Paine after his writing literally DROVE the Revolution FOR them…not Washington. I don’t care WHO you agree with, just explain the dynamics of that interaction…in you OWN head would be just fine.

Otherwise you are just talking your own econ-book and badmouthing people that are “stupider” than you are….which is all great fun as you all know well….but pointless.

Never stop learning….written word or experience (and NO you don’t have to PAY for it about everything you can….it’s a great way to lead one’s life….just personal notion, that’s all.

Back pain is really great for getting me pissed off at boring non-original commenters. But I had to wait until now to take them so I can be “agreeable” at Thanksgiving dinner. Sister is having 2 extra non relative guests besides my 100% and pretty damn far gone disabled Viet vet brother, which is gonna make this even more difficult.

Anyway, Happy Turkey!

All true, but I suppose we have to be careful about the definition of “pivot,” or at least keep in mind what the (gullible) investing hoards take this word to mean. Does it mean holding at the final rate–say 5%-ish– for a year or so? Does it mean reversing? Nobody knows, really. Which, of course, is only one reason why the talking heads, who don’t define what the “pivot” actually means, are talking nonsense.

In reply to NBay, there are only two alternatives.

Either the directors are clueless, as are their employees, or else they have a particularly evil agenda.

Take your pick.

Wolf, how do you know that 10-year yield will continue going up and stocks continue going down?

At some point this will reverse, but the question is how to know when this happens.

And what do you think about inflation going forward? Did you try to estimate it?

That reversal of the trend might be years out. We haven’t had this kind inflation in 40 years. This is something that will stay with us for years.

Yeah but — a relief rally happened today on Wall Street after publication of Fed minutes indicating a majority of members are scared of rate hike dislocations, and think we are closer to being on track toward 2% inflation. I thought the overall tone and language was equivocal, but boy, equity buyers disagreed. Even bitcoin perked up.

It would seem there are nothing but soft landings and sunny heights ahead!

VIXY (reflecting VIX) has reached new 52-week lows. I’m buying it, but nervously.

But how do you know inflation will stay for years? Did you try to estimate it?

Let’s say, what would you expect over the next 12 months and why?

The longer term is a bit of a different story.

Disinflation setting in. Oil dropping like a rock and bonds rising. China collapse will drag everything down.

The only inflation soon will be coming from the overpriced homes and rent. Healthcare premiums up 10-15% nationwide caus inflation. Feeds into service inflation, until layoffs start.

Fed is weak willed and talks out of both sides of its mouth. I’d like to think they’d stay the course but they won’t. They’re already waffling. Remember they created the inflation in the first place!

I am fascinated by the DC cage match.

In one corner politicians whose power is being able to spend borrowed money (they have spent a lot of it) and in the other corner Powell who is claiming he is going to smack them down with whatever it takes interest rates.

Powell raises rates, politicians keep finding wars and welfare to spend on.

It will not last for years. The treasury does have to sell more to non primary, so rates could stay high with lower inflation

@Yo

Again be careful about the “China collapse” talk in making investment decisions or giving investors advice, our first investment club years ago was a disaster because we bought into that meme and it cost us bigly. It took several business visits there to realize that Western financial media and esp US media doesn’t understand a thing about China in reality (most of our reporters don’t even speak much Mandarin there) and most of what we hear is inaccurate–the lockdowns are a minor and diminishing part of the Covid response even though the attention they get, it’s mostly about ventilation, air filtering, nasal vaccines, testing and tracking. And despite even tougher Covid policy before, China’s economy has grown more and done better (with comparatively little inflation) than the US or anywhere in the West. They may not grow as fast as before, but they’re very resilient–they’re the biggest trade partner for most of the world now and that’s each year growing even more–and if inflation is to be countered, it won’t come from that. And above all, do not count on that contributing at all to the similar fantasy of a Fed pivot, it is not happening. Inflation continues to be the biggest threat to the US economy, and the Fed absolutely is going to continue focusing on fighting it and keeping it down for years from now. This kind of ZIRP and QE will never likely never happen again, it’s delusional to pretend otherwise.

@cd

Indeed. This is very much a potential scenario.

Could the spike in construction cost be attributable to higher labor rates?

Most home sellers are also buyers. When you sell you have to buy something else right? With a majority of homeowners locked into sub 5% rates, buyer credit scores and incomes being healthier than ever, it’s tough to imagine a scenario of forced selling. For employed homeowners to sit the family down and say “housing market is crashing, we need to sell now and go rent a comparable house for more!!” Is tough to imagine. If rates stay high I think we will be in a mortgage rate lockdown scenario. The real crash is in transaction volume. Check on your realtor/mortgage broker friends, could be tough for a while.

Well forecasts are just that never perfect but grounded in data. I for one believe Wolf and his forward thinking and understanding of the Fed. I wish I were full of facts but have read that inflation to drop by the amount needed by the fed only has happened in history when Corp bonds are above 7 and stock PE gets to 12 being an spx of current earnings at 2800. In Addition the 36 months prior spx needs to be flat or negative because of the potential wealth effect from the rich. The stock owners of the world are still spending and their behavior will only stop after a meaningful drop in markets. They represent about 50 percent of consumption of goods and services . Much of services expense is fixed (medical mechanical and home repairs etc)

I’ve always said everything is rigged for the Black Friday sales and the Christmas buying season and I’ve been sport on but its no surprise when you already know what will happen. Of course once everyone buys their Christmas gifts and boxing day merchandise inflation will take a second leg up with oil and gasoline prices spiking again at the start of this January just like clockwork.

That’s just your own homemade BS. But if you want to believe in your own BS, fine with me. Don’t spread your BS here.

Wolf, would you say the same applies to the dollar? Seems like it will follow yields but is taking a breather right now.

In terms of currency pairs, the dollar gained against all the money printers, esp the EUR and YEN. The ECB has stopped money-printing and has started rate hikes, big ones, to not fall further behind the Fed, and that supports the EUR. The BOJ is propping up the yen by selling US assets and yen with the proceeds. It will likely start rate hikes next year after Kuroda leaves.

The countries that have raised their interest rates ahead of the Fed and higher than the Fed have kept their currencies from falling against the USD. For example, the Mexican peso is at about 19 to the USD, which is where it was before the Pandemic. The Brazilian real has strengthened against the USD since 2021, when the Bank of Brazil started its monster rate hikes.

It’s just that the idiots at the ECB and the BOJ were/are glued to their idiotic NIRP policies. If they had raised rates ahead of the Fed, their currencies would have been just fine. The Fed gave them many months of warnings.

In other words, monetary policies have an impact on exchange rates. And I expect that big enough rate hikes in Europe (not just the Eurozone) and in Japan will bring the currency relationships back into line.

All that did was pad builder’s profits. In July, the media new home sales price was $478K, then dipped to $441K but has now climbed back up to $493K in October. So much for a slowdown in new homes sales translating into a long-term trend of price declines. Labor costs are still way up anyways, offsetting lower lumber costs.

But, hey, builders are still awash in cash, so they’re pilling on all sorts of discounts to keep the sales prices high. It’s a very crazy time. The only question is how much longer all of these shenanigans can keep going on, and the second most important question is when will 30YFRM begin a long-term decline towards 5%.

IMHO, once they reach 5%, housing will stabilize and turn around, assuming we’re not in a full-fledged recession.

Jay,

Nah. What does the article say about plunging volume PLUS massive cancellations?

The median price was based on signed contracts, a quarter of which got cancelled. In addition, even before cancellations, sales volume plunged.

THIS MEANS that there is a huge shift in the mix, as to what gets cancelled (low end) and what sales don’t happen because of high mortgage rates (low end), and so the bottom is falling out at the low end after cancellations AND THESE SHIFTS SKEW THE MEDIAN PRICE UP.

Sales under $500k collapsed. Which shifted the mix, and pushed up the median price.

That’s why I didn’t discuss the median price because it’s worthless with these kinds of shifts. And I didn’t want to sort it out in the article the way I’m doing now because it’s not the point. The point is cancellations and plunging volume, not how the median price gets skewed by shifts in mix.

Here is my favorite example: First, the median price is the price in the middle. The 2 lower-end sales don’t happen because people don’t have money; nothing else changes, the middle moves up, median price jumps:

wow, made an account just to say thanks , this is fantastic analysis! I learn more from your website than the sensational headings in FT :)

As usual, your analysis is very good, Wolf! I have no real problems with it. But IMHO what is needed is for the entire range of prices to move down. The question is when and if ever this will actually take place.

All your data really show is that housing affordability continues to get worse. Basically, we’re both saying the same thing just from two different vantage points.

And, we both know that builders are not in the type of existential threat that existed 13 years ago, so this means, despite reduced sales & “the bottom falling out”, the big builders are nowhere near going under. Furthermore, builders are simply pivoting to multi-family.

Let’s see what housing looks like in the next 3 then 6 month checkup, especially if multi-family goes into a decline.

A lot of people got nosebleed rich due to the onslaught of pandemic money. There are so many people that are so incredibly wealthy now, that they will be pushing up the median price for a long, long time due to these “mix” issues. Also remember, that “money” that was dumped into the economy is still out there changing hands every day. It wasn’t “spent down” as the media says. That talk is nonsense. That’s why either an increased pace of QT or a very long time horizon are the only two ways to get inflation to settle down. The shrinking availability of labor with the increasing overall (older) population size is just exacerbating the inflation problem further.

lol no, such a laugh at how delusional the housing pumpers, home flippers and real estate speculators still are about things. All that matters is the fundamentals–inflation remains high (still ongoing on top of damage already done to US price stability) and is the great mortal threat to the US economy, social cohesion and national viability, and it’s the Fed’s overwhelming focus. And will be for years to come. The housing bubble has been one of the biggest contributors to this inflation mess, the only way to break inflation IS to have a huge and sustained plunge in home prices. This is a huge difference than 2008 and it indicates the eventual drop will probably be even deeper and more sustained than the housing crash with the GFC, after all back then, with low inflation, the Fed had more latitude to apply the ZIRP and QE that got us into this mess in the first place. A sharp housing price drop is the whole point and the very goal of the Fed in the first place. All this pivot talk is the same fantasizing we heard with the “the Fed will never stop QE” last year. Sorry, that’s ship’s long sailed.

The primary goal of the Fed right now is to push wage inflation down. The Fed has never had a problem with inflating asset prices, as they’ve done everything in their power since the mid 1980s to make that happen.

Housing will not drop until the renters disappear. They must be forced out by layoffs, because no one wants to move or can easily. All inflation is supported by hyper rent prices. When the renters collapse finally gets full steam, most inflation will lose strength. Housing will crash then by forced selling without their rents. This scene played out last housing bust, and should play out again. Imho it will be much worse with all the massive overbuilding, unprecedented debts defaulting, and global geopolitical black swans. This may take years as Wolf suggests, but it can be expedited by the Fed or global crisis like more pandemics or expanding wars etc. The rate of decline is the steepest on record in some metrics. The future is extremely uncertain going forward, tilting heavily to extreme risk as it looks now. All kinds of liquidity crisis are emerging and some on edge already.

A 2×4 stud was something like $1.18 not so long ago, but went up to some crazy price and now they’re down to $3.75 at my HD store.

So, lumber is still at very high prices (3 times what it was a while back).

Halibut, I don’t know when you saw a standard 2×4 for $1.15, but it isn’t in recent memory… Maybe briefly at the very bottom of the GFC-fallout? When I re-built the deck at my last house in 2015, an 8ft 2×4 was right around $3. Current lumber price is waaaay below the pandemic peak sitting remarkably close to its 1999 and 2005 peaks. It’s even cheaper than it was for part of 2018. So actually, lumber is not all that expensive now.

I was just at Home Depot 2 hours ago, and I’ve been kind of surprised… Comparing prices I saw with what I paid to spruce up my last house in the 2010-2015 range, I’m amazed that tile flooring, a nice kitchen range, washer/dryer, paint, lumber, etc. haven’t really moved in price at all. For example, I bought a low-back range in 2015 for about $1,100 and I see several that are frankly nicer for $950-$1,000 now that we’re well past the pandemic appliance & furniture buying mania. Plenty of floor tile options under $2/sqft. Nice Samsung front loader washer and dryer under $1200 for the pair. PCs and Laptops are downright cheap again. Consumer product prices have cooled way down. Services are where the heat is.

You forgot to account for the “quality” deflation. Price stays the same but quality gets slashed. See how long your Samsung washer and dryer last before they need to be fixed/replaced.

PNW Canada, is messed up of a different sort.

Construction materials’ cost and availability have improved vs covid years.

But construction labour rates are up maybe up 50%. So yet and still adding to housing cost.

The Central bank has the brakes locked on, and is adding quarterly to the cost of housing.

Meanwhile the federal and provincial governments are standing on the gas pedal. Adding turbo boosters even. (deficit spending, doubling down on new arrivals)

So affordable housing is a concept. Increasingly, the availability of housing (rent or buy), and the availability of public essential services, are diminishing.

A good PMW lifestyle, is available, but still depends on one’s wealth status, and or on prior-housing ownership or inter-generational-access.

SpeedQueen -Ripon WI lasts forever.

Whatever. My mom is going into hospice. She’s going to die. I’ll discuss the price of lumber later.

Halibut, Condolences. I’m sorry you’re going through that with your mom. Best wishes from an internet stranger.

In Canada they up the immigration quota for the next 5 years and bring in the FHSA (Tax-free First Home Savings Account) to try to push home prices even higher.

Lumber futures are hovering in the low 400’s nowadays.

Yes, prices have dropped significantly except for products like LVL lumber & trusses. I watch about 6 different lumber prices on Menards, and neither of these items have dropped $0.01 in the last six months. Lumber prices really don’t matter. The drop is simply padding builder’s profits at reduced sales volumes.

What matters is how much more residential housing drops through ’23. There needs to be a major, 30%, correction all around the country. Otherwise, 30YFRM will begin to fall next year and will intersect with a modest drop of ~10% and then housing will stabilize.

Houses in my neighborhood, 20-YO starter homes, are still going up. Ultimately what matters is does Uncle Same step in with rent & mortgage relief if housing drops more than 15%.

Price of ALL lumber depends, sometimes hugely on species and grade Hal.

While it has been a couple years since I bought much, 2x4s of SPF ( SprucePineFir) was going for $2.98 for a 92&5/8” length one of ”stud” grade then. 2x4s of SYP (SouthernYellowPine) in 96” was $3.75 for #2. 2x4x96” of Structural Select grade was $4.29…

Then ya have various kinds and levels of ”pressure treating” to add to those numbers, especially if you want the ”marine grade” PT, as opposed to that not rated to touch the dirt,,, etc., etc.

And then ya have the boom and bust cycle of construction as Wolf makes very clear in this article for recent times, but some of us elders have seen that cycle since the early 1950s, and heard about it from old folks back then who lived through it since the 1890s…

FRB has done very little to STOP these cycles, but in fact has distorted them hugely as we are seeing emphasized this time.

”Keep yer powder dry folks” opportunities lie ahead!,,, though exactly WHEN can only be known at the time, eh???

Well, see Vintage, there’s inflation right there. A stud for typical 8 ft ceiling has been 92 1/4″ since we climbed down out of the trees and now according to you 92 5/8″ …..no, wait, that’s Disinflation! More wood, same money

Thanks for the info on the complexities of the lumber mkt – details matter.

But one way to reduce the significance of costly complexities is to simply build *simpler* – smaller, simpler houses mean less lumber, which means less cost (almost regardless of lumber specifics).

Twenty years of ZIRP created a hallucinatory landscape where elementary, cost-saving tradeoffs got buried under a mountain of real estate agent, highest-end everything jibber jabber.

I only wish there were more “simple building” online tools and references that could aid a return to rationality.

The “small house” movement is likely driven by this impulse, but it tends to elevate novel-ness and “twee” impractacalities in its own way.

Where are the Levittowns of yore?

I bought some paver stones exactly 2 months ago at HD and took pictures of that section – it was $5.26 per stone back then. I went to the same store yesterday and stopped at those pavers in disbelief – $8.88 per stone, almost 70% increase in just 2 months, and if I am not mistaken, gas prices actually went down over the same period.

… And I was hoping for some construction materials to drop in cost sharply following the decline in new home construction. So far it looks like it’s a false hope.

Gotta be some good brick and stones free for the taking amongst the Detroit Ruins.

I’m partial to the old Bullseye Brick from Ohio myself.

2×4 studs are at USD$320/thousand board feet and begging for orders. That translates into $1.70/stud, fob mill.

Jpm just said buy builders

Inflation will devastate GMs

gametv,

Lumber is not as large a price factor as most suppose. Given a 2000 SqFt single level home with a conventionally framed roof, plus a 500 SqFt garage, all on a concrete slab, expect to pay around 12K. This would include floor and roof sheathing based on $900MBF.

Most contractors (so-called) can’t, or don’t, do their own take-offs and rely on the lumber supplier to give them a bid, thus generally paying at least 30% more.

Labor spikes are the last phase of money printing economic effects before the downturn. First money goes to banks then to assets then to wages then recession.

Was waiting for Wolf to dissect the Fed minutes. But just realized it is a non-event. Everything was already known, but the market still went up anyways. My volatility short bet is hurting but still hanging on. If I end up making profits, more donation for Wolf.

Mainstream media spin: Fed minutes point that there is no indication of slowdown in inflation, but Rate hikes will reduce “soon” => Fed no longer cares about Inflation => Only 50 basis point hikes => Pivon Starts => Massive QE and negative interest coming => big stock rally coming => all assets must rise (stocks, bonds, real estate) => screw shortsellers!

Well-said. But the market’s action is telling us the Fed should speed up the QT. We all know Powell is too coward to do it. They can see through his character. Maybe the banksters and the Fed are indeed in this game together.

“Maybe the banksters and the Fed are indeed in this game together.”

Maybe???? LOL

Maybe K???

How can there be any reasonable doubt left that the FRB is the servant of the banksters???

Certainly NOT serving the oldsters, savers, thrifty working folks, folks on fixed incomes, etc., etc.

kinda funny AA,,, elders singing the same song!!

And this time keeping in time and tone, eh

“Maybe the banksters and the Fed are indeed in this game together.”

Maybe ? Banksters are the only thing the Fed is interested in protecting. Powell’s lips moving in front of a microphone mean absolutely nothing as far as the average person is concerned.

Didn’t Neil Cash ‘N Carry ‘change sides’ from banker to Fed during the last go-round?

lol that’s a perfect description, the financial media is all in on the stupid pivot talk, gotta reel in enough dumb naive bagholders among the retail investors for the big boys to unload their junk to in coming weeks. The Fed minutes didn’t indicate any kind of dovishness or laying off of the rate hikes or esp QT, in actually reading it their tone was even tougher than before. They’d already been talking about lower rate hikes for December as a given, while they’re still undecided and weighing factors, the minutes show a 75 bp rate hike is actually much higher probability than thought before. We have to remember it’s not just the percentage of inflation now, it’s the fact that this percent price increase is layered on top of the high inflation from before, so even just a 3 percent inflation right now would impose a lot of pain on Americans coming on top of the inflation before. While a recession is a concern, it’s secondary to the inflation dangers, and in fact a recession–even a deep one–may be the only way to break this housing bubble and these asset bubbles that are the main cause of this inflation mess, esp if it happens in early or mid 2023 that may be best case scenario, and allow for a recovery in the months after even without rate cuts, just like the recovery from the 1983 recession took place.

Yeah, soft landing is coming.

Entrenched inflation remember they’re all bankers. They all are invested in one form or another, remember debt is how the rich oay no taxes. That scenario is spot on. Wolf, telling you buddy soft landing is coming, unless something pops big enough to call margins. Or raise required margins to the devaluation of asset

Spoiler: there was no mention of selling MBS.

Correct. I was looking for that too. I know they’re talking about it because they have said that they’re talking about it. So maybe we’ll have to wait for official confirmation that they’re talking about until 2023.

There was nothing new and interesting in these minutes. Rates still headed to “sufficiently restrictive,” “ultimate level” of FFR still “somewhat higher than they had previously expected” (5%+); getting inflation to 2% still priority #1; QT still running as planned, no deviations.

Well there was something fun — the hawkish pivoters want 75 in December:

“A few other participants noted that, before slowing the pace of policy rate increases, it could be advantageous to wait until the stance of policy was more clearly in restrictive territory and there were more concrete signs that inflation pressures were receding significantly.”

= 75 still on the table in December.

Thoughts of 75 could heat up again next week with non farm payrolls and PCE.

Gotta have a little mini rally into Thanksgiving!

You just know that when the hike is only 50 basis points that the market will take it though QE had started again and interest rates were dropping. Optimism abounds.

LOL Yes, there’s a chance.

Or if they hike 75, then the market rallies because the pivot to 50 is surely coming next year.

This stuff can be really funny.

Brian,

When the dot plot has dots over 5% and Powell is hawkish AF they won’t have a choice but to raise terminal rate expectations.

It’ll almost certainly be 50bips tho. Like wolf said, big picture, things are going exactly as they should and the Fed said it was going to be 75 then 50 a couple months ago

“Or if they hike 75, then the market rallies because the pivot to 50 is surely coming next year.”

It all just proves the same thing – that there’s too much liquidity sloshing around and the FED is derelict in their duties and not taking it seriously. Only when they’ve done their job will you not have ridiculous rallies based upon bogus narratives, all a result of cheap money.

The fact that inflation hasn’t even budged and they’re now talking about dialing back the rate hikes just proved they were never serious about inflation in the first place. That’s why Jerome Powell should have been fired long ago. There are zero ramifications for being an inept central banker. Fail and enjoy endless job security.

I KNOW it’s only an index of 30 stocks, but the DJI now stands at 34,195…it’s ATH is 36,800…..

Believe it or not but as things stand today, the DJI is only 7.6% below it’s all-time high…….

On Oct 13 after the CPI report came in hot and everything crashed before turning into a historic intraday pivot, the DJI hit 28,660… in the 30 trading days since, the DJI has risen 19.3%

Something to chew on, other than your Thanksgiving meal…

Happy Thanksgiving all… Wolf, one of the many things I’m grateful for is this site AND your interactions with us… Much love to all!

Rosarito Dave,

ACTUALLY look at the DOW. Apple, by far the largest stock in the US by market cap, is way down on the list and weighs only 2.9% in the Dow, which is ridiculous. United Health dominates the DOW at 10%, which is ridiculous. If you cite the DOW as representation of the market, you do not know what you’re talking about.

Here are the 30 DOW components in order of their weight in the DOW, and their percent weight in the DOW:

10.2% UnitedHealth Group Incorporated

7.4% Goldman Sachs

6.2% Home Depot Inc.

5.5% Amgen Inc.

5.3% McDonald’s Corp

4.8% Microsoft

4.6% Caterpillar Inc.

4.2% Honeywell International Inc.

4.1% Visa Inc. Class A

3.6% Travelers

3.6% Chevron

3.4% Johnson & Johnson

3.4% Boeing Company

3.0% American Express

2.9% Walmart Inc.

2.9% Salesforce Inc.

2.9% Apple Inc.

2.9% IBM

2.8% Procter & Gamble

2.6% JPMorgan Chase

2.5% 3M Company

2.1% Merck & Co. Inc.

2.1% NIKE Inc. Class B

1.9% Walt Disney

1.2% Coca-Cola

1.0% Dow Inc.

0.9% Cisco Systems Inc.

0.8% Walgreens Boots

0.8% Verizon

Wolf, I wasn’t particularly saying anything about the DJI’s representative nature of the market, rather, any way you look at it… It’s STILL a HUGE move up in the index in such a short time… The DJI is watched by most folks (to some degree or other), but particularly with your average to non-informed investor. A 5,500+ move in 30 tradings is an average of 180 points/day….

I remember when stocks would seem to fall fast and rise more slowly…

Still waiting to check that scenario out when they start falling again (hopefully sooner rather than later for my purposed.. lol

They ‘suggested’ it, unless that meant simply just letting the existing holdings expire.

“In addition, members agreed that they would continue reducing the Federal Reserve’s holdings of Treasury securities, agency debt, and agency MBS, as described in the Plans for Reducing the Size of the Federal Reserve’s Balance Sheet that were issued in May.”

Fine with me.

Little reason if any to sell MBS at a loss IOT manufacture a QT milestone.

This financial system is getting rickety. Think about it. Lowest interest rates forever, followed by the largest increase in M2 followed by M2 growth cratering to zero while interest rates explode off zero bound. It’s over management by central planners.

You want to reduce liquidity, tax it away. The inflation is stubborn because of more than 40 years of tax cuts, not to mention income hiding, all of which is inflationary. Forty years! Fighting this flood or liquidity is going to take a while.

Increasing taxes in the right places would be helpful (e.g. phase out the ability to claim depreciation on single family residence real estate), but it won’t solve the overall inflation problem.

California has been fighting those tax cuts every step of the way, but can’t do it alone. It’s time for other states to step up and do their part. ;-)

Volatility is in cantango out 4-5 months

The daily gap was closed, just dipping into oversold

Probably good place to start scaling in but a notorious bullish seasonality

Great news to see just right before Thanksgiving. Give me something to be thankful for as long as this momentum continues. Hopefully by Christmas we can see existing home inventory spike to these new home month of supply too, that would make for a good Christmas present.

Sales of real estate will go down because, as in 2008, RE prices have now reached levels at which most buyers who would wish to buy cannot afford to do so. All of these effects are symptoms: the majority of the population in the US (and most developed countries) is under greater and greater financial stress (which decreases sales) each year. The latest inflation spikes have only increased such stress dramatically. However, inflation is not the sole problem but only a tool of banksters and a symptom.

Through engineered inflation, the banksters have slowly sucked out of the wealth of most Americans using their bankster cartel, called the “Federal” Reserve, (and other secretly-private banks in foreign countries, e.g., the Bank of England.) Thus, Americans who could have afforded a large family in a big house on one salary in the 1920s need two salaries to have a reasonable living standard now and may not even be able to afford a house in the more popular, US areas.

Working hours have been cunningly increased through the mechanism of creating financial desperation through money printing and consequential inflation. Many Americans now work jobs requiring longer hours or even two jobs to meet their increasing expenses.

This kind of thing happened also in other countries, albeit in places like communist China it was the CCP cadres with their Ponzi-real estate companies that did the financial blood-sucking of the savings of most, Chinese victims, not their buddies and fellow parasites, the US banksters. However, the effect is that all these populations are in worse and worse financial circumstances and the value of their earnings has decreased in relation to their needs. (Albeit Chinese wages dramatically increased for years, the CCP has printed many more Yuan per year than the Fed did dollars, so the value of the Chinese Yuan has decreased through resulting inflation.)

That financial stress is the key reason why the populations in developed countries are crashing, albeit there was a recent, temporary spike in childbirths in the US after people had paused starting a family during a pandemic. Most Americans (and citizens of other, developed nations) will not have children when they only survive day to day (in financial terms) and only by never retiring or getting seriously ill.

I predict that the upper end of the real estate market will keep getting worse, as to sales, albeit foreign investors might temporarily get spooked by some event (e.g., a CCP invasion of a certain island) and flee into US real estate in the future. As in 2008, in many areas, the purchasing limits of Americans have been reached, because inflation is effectively decreasing their wages (which are mostly not increased enough to keep up with inflation) while their expenses are increased with inflation.

As expectations decrease, however, I predict that low-priced and mid-priced real estate in good areas will retain more of its value: however the new homes discussed will be priced with a premium for being new, so new home sales will not be able to compete with existing, lower-priced, comparable real estate.

RH- outstanding. Demographically, the globe has shrunk to a point that more are now able see some trees for the forest (still begging the old question, ‘…What is to be done?…’.

may we all find a better day.

This inflation has created such stress among the workforce that some have resorted to cheating to take in some extra bucks. I’m not talking about WFH dudes that don’t do any work and are essentially out of sight and out of mind. We know all about that. I’m talking about my WFH insurance claims adjuster who was just fired. Reason: Was WFH for another company at the same time. My claim was sitting in a queue for a whole month with no action taken on the claim.

The post pandemic volume of new home sales is still dwarfed by the pre-GFC mania despite that fact that the population has grown since then and a newer larger generation of thirty somethings are in the family-formation stage of their lives. It has fallen back to sort of a “normal” pre-pandemic sales rate and, at least for the time being, it amazingly seems to be settling at that normal rate. No doubt that when we look at cancellations, lower buyer traffic, and higher construction costs, it’s reasonable to assume that builders will be buttoning up the projects that are in-process, and hitting the brakes on any new projects. Supply of new houses will start dropping again.

It’s clear as day that the market is continuing to slow, but look how much bigger that mountain of sales was in the early 2000s. Anybody who thinks we’re going to be seeing massive GFC-style price drops across the board should probably look at that graph again. Post pandemic sales volume never got anywhere near pre-CFG levels. Then pay attention to a Fed that talks a big game, but tiptoes through their actions using interest rate hikes as a distraction from the real cause of inflation (way too much cash sloshing around). They’re not going to remove enough of that cash at a sufficient rate, so the dollar will continue to lose value over the next several years until price and value reach equilibrium in real terms just like they did 40 years ago. Interest rates don’t affect cash-holders very much, and cash holders don’t want to sit on their evaporating cash… Over the long haul of the inflationary period we’ve entered, many of the dollars that the Fed refuses to remove quickly enough are going to continue finding their way into assets.

The most likely reason for a difference with GFC is a probable second mortgage moratorium.

But first, rates will need to “blow out” which probably won’t happen until the second leg up of the new interest rate cycle.

Second, higher unemployment but first the pink slips need to start flying and that’s substantially contingent upon the stock mania being. The connection is already evident now in techland.

Housing is way overpriced to most potential buyers (especially with shrinking equity) and unless the interest rate cycle didn’t really turn in 2020, only a partial retracement is in store. There is no wage boom either, though it’s been happening selectively.

There is a wage boom happening in the lower spectrum of wages.

I know lot of companies who used to pay $14/hr are now paying $18/hr. This is not the case in the higher spectrum of wages.

But the problem is: Low wage people even with wage boom can’t really afford these homes.

They never could

Jon,

“Low wage people even with wage boom can’t really afford these homes.”

They bought them back in 2005/2006. They will try to do that again.

My experience here in the “high end” of skilled labor/hourly engineering and manufacturing labor in Silicon Valley:

2-3 years ago, you could find employers willing to pay well into the low 6 figures for talented technicians/weldors/junior engineers. Now. . .I see a TON of openings at the $75-$90k range. Often requiring a 4 year degree and a minimum of two years experience. In the land of $120k/year poverty level, these employers are 15 years behind the wage curve. I get lots and lots of young recruiters reaching out to me from all over the country, trying to snag an applicant for a job 1-3 hours away from me, that pays 40-50% what I could get in 2018-2019. The market appears to be awash with these jobs. It’s always funny when I tell them that regardless of how it looks on a map, San Jose to the North end of Berkeley, or Sausalito to Mountain View is NOT a tenable bay area commute. And will not be happening for $35/hr, when the income required to buy a home in San Jose for a single earner is $379,000/yr.

Hey Galt, you still remember how to make that car motor that runs off ambient static electricity? We could sure as hell use it now, and you’d also be back in the BIG bucks where you belong, for sure!

Nbay- Good one! Vague reference, but I still laughed 🙂

Re “ many of the dollars that the Fed refuses to remove quickly enough are going to continue finding their way into assets.”

If you really believe that, please point me to a situation where you manage to “put your money into assets” without someone else simultaneously “cashing out”!

Building a new house.

Also:

Creating almost anything from scratch.

Rebuilding an old house or car.

Hey, I did that. Off grid. Took 16 years (only a bit over 4 years full time) and still wasn’t finished (especially inside) when I sold it, but the experience was priceless. Had to spend all my IRA, though…..a third on roads and pads…..Not a lot (maybe $120K) as I just stayed in a sure thing non-marketable bond fund.

Didn’t trust Corps, still don’t…..in fact make that, hate them.

If there’s enough historical data, it could be really, really informative to make a graph where the “New House Contracts Signed”* data are corrected for the approximately-measured cancellations. At a 25% cancellation rate, the rate of actual house sales is not 632,000/year but 474,000. The October cancellation surge undoes much of the apparent rise in sales from September too. Going back a little further, it also looks like the whole “sales plunge is pausing” meme from the last 5 months will be undone.

*Now that we know they aren’t final sales, can’t call it New Houses Sold anymore.

P.S. Somewhere there’s an enterprising bankster running a sweatshop where employees frantically robo-sign new home purchase contracts, and then a day later frantically robosign cancellations of said contracts. Contract churn would be worth a lot to the homebuilder industry right now – prop up the “New Houses Sold” number to keep the industry afloat in the eyes of Wall Street, while the soaring cancellation rate goes ignored… Then in a few quarters, after all the C-suites have unloaded their shares, they’ll have a “Kitchen Sink” earnings confession quarter and load back up on the shares as Wall Street goes into panic.

Thanks, Wolf, for these articles. reading all this information anxiously in anticipation of some normalcy. Our government defrauded us of our savings.

About to head out to look at houses on Friday. Perhaps, I can get positive thoughts and a little luck from the WS team. Maybe drink one from the cool glass gifted to donors. I will report my local findings when I return.

Don’t be afraid to offer what YOU think a home is worth. I’ve been looking at sales lately (albeit delayed data) and some homes are closing for far less than asking, just not enough of them yet. Good luck.

The new home price calculations are not just caused by cold feet but by cold hard finances. Back in the late spring of 2021 my son signed a sales contract for a new Lennar home, and put down a very small deposit ( $1000). Then by September he had to show he could get pre-approved for the mortgage ( but no interest rate lock). And then in December he had to get the actual mortgage with an actual interest rate. from there the house had to finish and have occupancy within 3 months for that mortgage and rate to be good. Even then, the final appraisal ( when the house was complete) had to come in high enough to justify the mortgage. During that time the appraisal went up from the time he signed a contract and the mortgage rates stayed steady. But if you signed a sales contract 6 months ago todays mortgage rates and lower appraisals would leave most people dead in the water with no way to finance the house and the sale would be dead.

The housing bubble flipped to cancellations. It might be affected by higher mortgage rates, layoffs, creepto and fears of recession. It might be temp or systemic. In the long run home prices are bound to fall in real terms, clipped by inflation.

Small changes are hard to observe. After few years or decades they accumulate. Price/Rent will get better. When there will be no more hope for home owners ==> it’s time to buy.

1) TY is rising. TY rise isn’t good enough. Rising 10y note prices means lower 10y rates. If the Fed increase by 0.75, the 2y/10y inversion might exceed minus (-)1%.

2) Both in US and in Germany all rates are under 1y. The 1y is the peak, but US 1y is higher than the German 1y.

3) If the Fed stay the course the highest rate on the chart might be 3M or 6M.

4) Gradually, both in US and Germany, the long duration will rise, before exceeding the 3M & the 6M.

5) The yield curve will be flat at higher plateau, before tilting up on the

right hand side, at the long duration ==> all rate will be normalized.

6) At that point the yield curve no longer will be defective.

1) In normal environment banks will lend and make money. The banks will

gradually keep their mortgages, instead of dumping then to Funny.

2) Their assets will grow and the Real M1 slump will recover. The Real M1

might exceed $10T, before moving higher.

3) The gov will shift lending back to the private sector. The banks will be in

charge, take control make money.

4) The shadow banks and the regional banks borrow in the o/n market, providing US bills/ notes as a good collateral. The good collateral is moving hand to hand, for a small profit, several times/per night every night, in

the o/n market.

5) Many small businesses producing REAL GOODS can use 90 days promissory notes that expire within 90 days, to finance themselves, to pay workers, to pay suppliers, to make money, without banks

borrowing. Money make them run. Without liquidity they will shut down.

That’s what have happened after WWI.

Hello Wolf, that last chart creates more questions than answers for me. How is the construction cost index formulated? Is it possible that the Fallout in the bottom end of housing has caused an artificial increase in the construction cost index percentage rise? Just curious.

It’s possible. The index does not include “substitution” to account for a shift in buying behavior, and a large shift like that could impact the index.

Just putting this out for everyones thoughts. What about aging population and shrinking first time house buying population percentage?

Politicians will do their best to mitigate aging demographics, by continuing to permit a flood of immigration. It’s not targeted specifically toward the housing market but a side consequence.

This of course won’t make housing more affordable to more first time buyers, but to the extent the government can distort the housing market further through more subsidies, I anticipate they will try.

1. “aging population,” like all demographics, doesn’t happen from month to month or year to year. Their impact is measured in decades.

2. millennials are the largest generation, and they’re entering their peak earnings and buying years.

3. the median age in the US has increased by only 1 year since 2011, to 37.2 years. So the millennials are the median.

4. demographic stuff is completely irrelevant for month-to-month and year-to-year economic data. Just doesn’t happen quickly enough.

The real impact of demographics is the culture of the different generations. We have gone from a very frugal WW2 generation, to a live at the very top of your ability to borrow millennial generation.

Yep, let’s blame millennials for ZIRP causing changes to their savings and borrowing habits. It’s all their fault that savings earned nothing for the past twenty years.

Hi Wolf, Yes, I use the Scripps network in the States (primarily as my ex is a nurse there and I went through some severe health issues in the mid-2010’s so I have a good relationship w/ many of the facilities.), but once again, the facilities are less than an hour away.

In case of emergencies, the Red Cross has a facility here as well as a few local hospitals that if something needs deeper care will provide an ambulance (cheap) to the States.

On the OTHER hand, Baja Cali is KNOWN for quality dental work with a large choice of providers. The prices are (NOW after being a good deal cheaper 3-5 years ago), still about 25-30% of what work costs in the states. For example, I had 2 root canals and 3 crowns that cost a total of about $850 shortly after moving here. EVERYONE has their own favorite dentist here.

Also it’s known for cosmetic (plastic) surgery… LOTS of Americans come down here for both services… also LOTS of Americans are moving here as well…

I could also talk about the effect of this migration in terms of the cost of housing… it’s following the money, which isn’t Mexican stimulus money, rather Americans coming in w/ cash fleeing in the hopes of cheaper living and a better lifestyle.

For example, I called my realtor today and asked him what my place might be worth. He did some research, came back at about $185G (I paid $125G almost exactly 5 years ago). It’s a very interesting dynamic going on down here now. Products, services and food are rising similar to the States % wise, but they started at a much lower base. This are still cheap here.

It’s a good life here and I’m a blessed man.

Many retirees are planning to live outside of the US because housing and healthcare are out of control here. I’m seriously considering it too.

Petunia… I’m one of those! 5 years ago, I moved down to Rosarito Beach, MX. NICE 9th floor condo on the beach cost me 125G.

Only 30 minutes to San Diego. Gas is $1.60/gal cheaper as is pretty much everything else. I do use my Medicare Advantage plan and have the SAME PCP for the last 20 years…

I’m very grateful I made the move, life is good!

Do you have to go to the US to use your Advantage plan?

Hi Wolf, Yes, I use the Scripps network in the States (primarily as my ex is a nurse there and I went through some severe health issues in the mid-2010’s so I have a good relationship w/ many of the facilities.), but once again, the facilities are less than an hour away.

In case of emergencies, the Red Cross has a facility here as well as a few local hospitals that if something needs deeper care will provide an ambulance (cheap) to the States.

On the OTHER hand, Baja Cali is KNOWN for quality dental work with a large choice of providers. The prices are (NOW after being a good deal cheaper 3-5 years ago), still about 25-30% of what work costs in the states. For example, I had 2 root canals and 3 crowns that cost a total of about $850 shortly after moving here. EVERYONE has their own favorite dentist here.

Also it’s known for cosmetic (plastic) surgery… LOTS of Americans come down here for both services… also LOTS of Americans are moving here as well…

I could also talk about the effect of this migration in terms of the cost of housing… it’s following the money, which isn’t Mexican stimulus money, rather Americans coming in w/ cash fleeing in the hopes of cheaper living and a better lifestyle.

For example, I called my realtor today and asked him what my place might be worth. He did some research, came back at about $185G (I paid $125G almost exactly 5 years ago). It’s a very interesting dynamic going on down here now. Products, services and food are rising similar to the States % wise, but they started at a much lower base. This are still cheap here.

It’s a good life here and I’m a blessed man.

Wages will increase but I don’t see Millennials ever working two jobs at the same time like boomers did.

It’s called the hustle.. everyone has a side hustle.

Anyone seeing the news within the news? Does not matter if the number is 1200K, 800K, 600K, or 450K. 450 new homes is the equivalent of building an entire new town…and they are creating 1000 of these every year, year-after-year. The whole damn thing is inefficient and lousy towns become lousy cities. This is not what these people are going to need handed to them in the future…it will be a mess that will conflagrate into a worldwide nightmare and that will lead to international conflict as resources become overburdened. This shitshow should stop now. It has gone on far too long and is the worst kind of planning for accomodating a population which is going to increase one way or another. What was, is over. What will be, is coming hard and fast. Rant over.

Micro economics lesson?

At Home Depot yesterday, looking at bathroom fans, simple one with a light in it.

Choked on the prices, from $112 up to $350! For a simple bathroom fan! Other stuff is notoriously up, way up even since mid summer. Went home with a pack of AAA batteries.

Yes, I cancelled my “contract” to get a replacement fan, the old will just have to carry on!

What in the world are you talking about CreditGB? A quick HD website search shows bath fans in stock at my local HD for $22 or $44 fan only, $55 or $80 with light. $180 gets you a programmable LED panel light and 110cfm fan combo with a humidity sensor for automatic operation (fancy). Hell $120 gets you a light and fan with a 1300 watt heater to keep you nice and toasty. These prices aren’t out of line with pre-pandemic prices. I find it remarkable how little inflation seems to have hit this particular retailer.

I get that we’re experiencing inflation, but the fact is that consumer products aren’t bad at this point… A lot of these products are well past the mania and shelves are full again. It’s services that are still wacky. Saying that you can’t find a basic fart fan under $112 at HD is more than a simple exaggeration to make a point. It’s clearly and verifyably not true.

Misunderstandings are fine. Incomplete or flawed analysis is understandable, we’re all human and I do it too. But I don’t understand why people feel that they need to make stuff up to push a narrative that doesn’t fit reality.

The Dow is down 7% from the top. The blue zone dump stocks. They will use JP as an excuse to send the market down, whatever he says, to buy

stocks at lower prices, for fun and entertainment.

We don’t know how far it will go.

Looks like new housing starts, not seasonally adjusted, are on their way down. Not unusual for this statistic to fluctuate up and down month to month when viewed over time. However, this time, the 2022 peak occurred in April with the warmer “building season” seeing month to month drops that continue through October. Additionally, there are new and heavy weights around the necks of those who might consider building a new home.

1. Their inflation ravaged incomes are being reallocated toward living necessities, leaving little if anything for expanded housing considerations.

2. Savings, which might be intended for a down payment, are dropping fast, perhaps to support necessities that are realistically 30% or more than year ago.

3. Mortgage rates effectively reduce the affordability of the prospective new build.

4. Builders are paying 2 times the costs for so many construction components now that what margins they may have are evaporating by the week.

Friends, I think that these headwinds may be just too much for the potential homeowner to overcome in the near term. And as the war on fossil fuel, the foundation of any economy rages on, those costs will continue to percolate up through the input costs of literally everything, since at minimum, everything is transported on a diesel powered train or truck including your diesel, gasoline, coal, and LP fuel. Even the wind and solar farms are constructed and erected by diesel powered machines. The all electric future Green dream is a dead one, and a nightmare just now forming.

Barely related question:

According to the Port of LA statistics, it looks like container stats, both import and export, through the port of LA July to October 2022 have dropped off significantly since July. Off by 27.4% Last 3 year’s data doesn’t reflect this July to October drop. A media writer might actually refer to it as a “crashing number”….?

What does this mean for the post holiday shelves, once the gift buying orgies have subsided credit cards are maxed out, and inflation continues to eat away at the dollar?

Any significance here or just ignore it, it’ll go away.

Warehouses are filling up. Even the long term contracts are getting

renegotiated.

Imports down, Exports ( fossil fuels ) up = GDP up?

I run a couple small businesses. I can confirm major slow down in retail sales starting around July 22. My businesses both received big booms and record sales since the pandemic. Things have quieted down to near normal 2019 sales numbers this year. Coming off back to back record years I am not complaining. During the craziness of Covid and importing from China a normal container from China was running around $5,000. At the peak, I think containers were commanding an insane 25 to 30k per container.

The companies I sell for ran out of product in 2020. Ordered boatloads of more product, like every other company, at higher container prices, etc. Now they are sitting on massive amounts of inventory as shoppers stopped spending once the free stimulus checked stopped printing.

These manufacturers are going to be cutting their price to move these massive amounts of product sitting in warehouses.

Needless to say, the next year or two will be interesting.

Better solutions too.

The first shoe to drop is housing sales, the second is construction jobs. Once construction jobs go, the rest of the job market follows.

– The ongoing drought in western parts of the US also won’t help lowering construction costs. (think: forest fires leading to less supply of lumber).

With all the 50+ folks out of the workforce now -either taking retirement or just taking time off and living off reserves- I am of the mind set that there aren’t many individuals in the workforce that have any true experience with a real downturn. Went out with some folks from work the other night when one of the upcomers – bench for management -said he graduated in 2006 – I knew there was no real experience in the queue to handle what’s coming. Well, what’s already here. There are too many homeless camps (figurative for suxkles off the system) for the fed, imf, wef, bankers, business, or anyone else to resolve this impending crisis. It will be worldwide. It will stem from crypto, business loans, Ukraine loans (look up FCPA and oil for food to make the connection) and even the PPT wont be able to save the spike down. Wolf sounds and looks like a seasoned veteran of the last three or four cycles. In my opinion – interest rates needs to go to 12% or 18% just like it did in the 80s to resolve this. Funny enough, Volker, and Biden were part of the FCPA root (I think). Hold on and prepare for the worst in a few generations.

Take care.

I hope the PPT is on vacation tomorrow I’m playing the volatility index long a day trade tomorrow bought yesterday at the close.

Brazil, klinsmann gol.

Heard there’s a Big VIX Can’Tango, ME…..gol.

I see a lot of cheating going on around here on homes that have illegal rental units and accessory units which do not have the proper occupancy permits. If there ever was a fire in one of these illegal units all hell would break loose. I would say upwards of 50% of the properties we have looked at in the last few months have had some sort of violation. The Real Estate agents are so eager to make a commission that they look the other way or claim ignorance. The lenders are the last line of defense. I wonder how many properties are slipping through with all of these code violations.

Not attempting to pick a fight with all the doom and gloomers here, but we may be near the bottom of the real estate correction. If/when mortgages ease next year, and if Powell backs off, there might not be that big drop in home prices next year. Then everyone will be left behind chasing the next wave up.

If Powell “backs off”, there will be “Inflation Hell”. Sitting Presidents don’t like inflation hell.

Not sure what you are looking at but there is nothing in the data out there that suggests we are anywhere near a turn around. In fact, just the opposite. The average American household has lost between a quarter, and a third of their net worth. They are up to their eyelids in debt, and the jobs market is getting ready to implode beginning with the construction industry, and spreading to everything else.

There are no “sides” in this, just the recognition of reality, or the failure to do so…. Or as a very smart man once said..

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so. “ – Mark Twain

The Fed is not going to pivot. What you are hearing is propaganda and wishful thinking on the part of Wallstreet. Wake up!

“lso remember, that “money” that was dumped into the economy is still out there changing hands every day. It wasn’t “spent down” as the media says. That talk is nonsense. That’s why either an increased pace of QT or a very long time horizon are the only two ways to get inflation to settle down. The shrinking availability of labor with the increasing overall (older) population size is just exacerbating the inflation problem further.”

Absolutely.

How long before the housing units currently under construction hit the selling market, egg in a python style?

Or will they?

So once everything is ” Fixed ”

then they will cut rates and start all over again !

Create Inflation so a few can make Millions as everyone else suffers again that’s the American way All Fuc*** up