Investors are also pulling back.

By Wolf Richter for WOLF STREET.

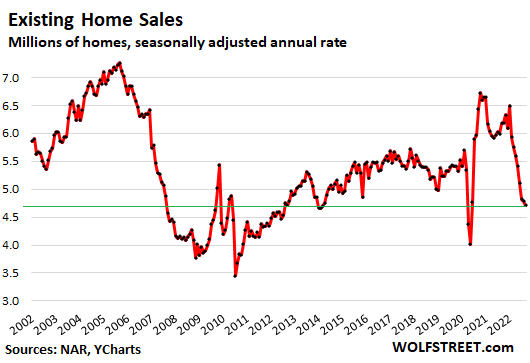

Sales of all types of previously owned homes – houses, condos, and co-ops – fell for the eighth month in a row, by 1.5% in September from August, to a seasonally adjusted annual rate of sales of 4.71 million homes, according to the National Association of Realtors. Compared to the peak in October 2020, sales were down 30%.

Beyond the two lockdown months of April and May 2020, this was the lowest rate of sales since March 2014, and since the summer of 2012, indicating to what extent the housing market is frozen. Potential buyers refused to even look at prices that sellers want. Sellers refused to cut their aspirational prices to where the buyers might be – though there is a lot more price cutting going now than a year ago. And other potential sellers waited for a Fed pivot that would lead to lower mortgage rates and higher prices before they put their homes on the market – though the opposite is now happening (historic data via YCharts):

These are sales across the US that closed in September, based on deals that were made earlier. So they just about entirely predated Hurricane Ian which made landfall in Florida on September 28.

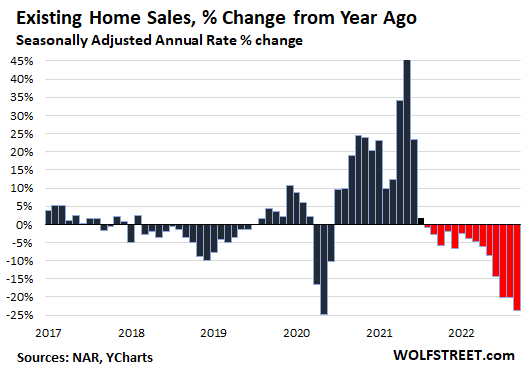

Compared to a year ago, the seasonally adjusted annual rate of sales was down 23.8%, the fourteenth month in a row of year-over-year declines (historic data via YCharts):

Sales of single-family houses dropped by 0.9% in September from August, and by 23% year-over-year, to a seasonally adjusted annual rate of 4.22 million houses.

Sales of condos and co-ops fell 5.8% in September from August, to 490,000 seasonally adjusted annual rate, down 30% year-over-year.

Sales by region: On a year-over-year basis (yoy), sales plunged in all regions. On a month-over-month (mom) basis, only the West showed no declines in sales from the desperately low levels in August:

- Northeast: -1.6% mom; -18.7% yoy.

- Midwest: -1.7% mom; -19.7% yoy.

- South: -1.9% mom; -23.8% yoy.

- West: 0% mom; -31.3% yoy.

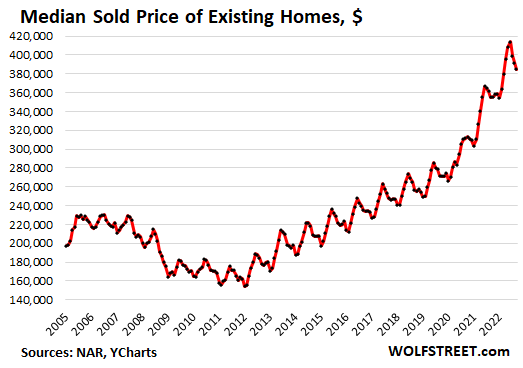

The median price of all types of homes whose sales closed in September dropped for the third month in a row, and is now down 7% from the peak in June.

In terms of seasonality, the 7% decline was the largest for this period since the end of Housing Bust 1, and more than double the 3.2% decline during this period in 2021. The average decline during this period over the prior 10 years was 4.2%. In 2020, prices jumped during this period. In 2019, prices fell 4.9% during that period. And in 2018, prices fell 6.2% during this period, but the housing market was weakening as mortgage rates were heading to 5% amid QT, rate hikes, and swooning stocks.

This monthly decline in prices whittled down the year-over-year price increase to 8.4%, down from the 20% to 25% increases at peak frenzy last year (historic data via YCharts):

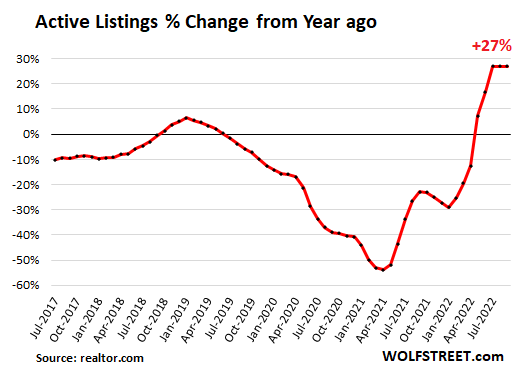

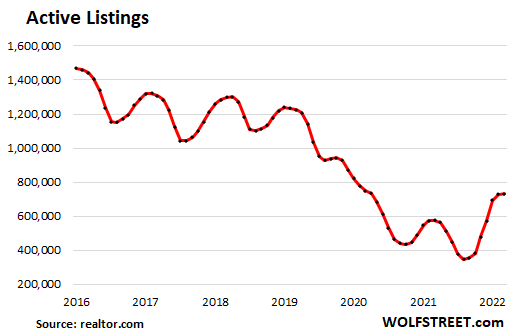

Active listings – meaning, total inventory for sale minus the properties with pending sales – rose to 732,000 homes in September, the highest since October 2020, up by 27% year-over-year for the third month in a row, according to data from realtor.com.

Compared to pre-pandemic years, active listings remain low, in a sign that the housing market is sort of frozen, with sellers not interested in selling at prices where the buyers might be; and buyers not interested in buying at prices where the sellers are, and so there is this standoff that shows up in the plunge in sales.

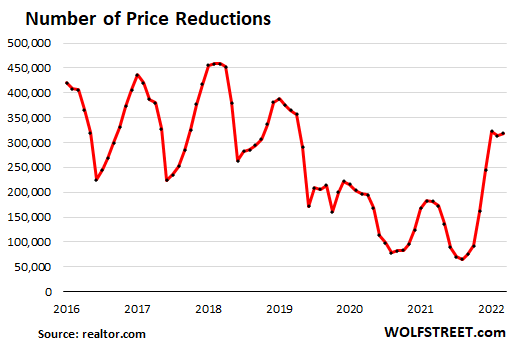

Price reductions have jumped from historic lows, a sign that some sellers are backing off from their aspirational prices and are cutting prices to where the buyers might be.

The number of price reductions jumped by 75% year-over-year from the mania-lows of the pandemic and is back in the range where it was before the pandemic:

Investors or second home buyers purchased 15% of the homes in September, down from a share of 16% in August, and down from the 17%-22% range in the spring and winter, according to NAR data.

“All-cash” buyers, which include many investors and second home buyers, declined to a share of 22% of total sales, down from a share of 24% in August, and down from a share of 25% to 26% earlier this year.

This declining share of sales to investors, amid plunging overall sales, shows that investors are losing interest in this market at these prices.

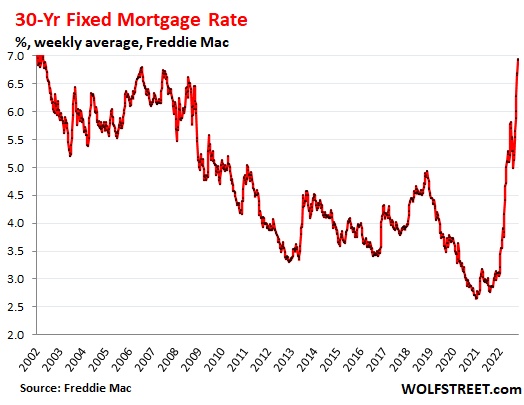

Holy-moly mortgage rates. After the fantasy-Fed-pivot-drop from 6% in mid-June to 5% by mid-August, mortgage rates are now at around 7%.

The daily measure of the average 30-year-fixed mortgage rate jumped to 7.37% today, according to Mortgage News Daily.

Freddie Mac’s weekly measure of the average 30-year fixed mortgage rate, released today, based on mortgage rates early this week, rose to 6.94%, over twice the rate a year ago.

But a 7% mortgage rate, as huge as it may be when applied to today’s crazy home prices, is still low, given that CPI inflation is over 8%. But it’s catching up:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Canada is a different Twilight zone.

There are bidding wars for apartments at Jane & Finch which were listed for C$1900 a month.

A decade ago, Jane & Finch was a low income community.

Every low income community in Toronto is being replaced with downtown rental rates. It’s dire.

Wolf, how about a home affordability chart? One that shows Median House Prices and calculates EMI based on Average Mortgage rate for a 30 year mortgage with 0% down.

That one should be going to the moon? Is anyone paying attention to it?

The solution to the affordability crisis is lower home prices.

A national affordability chart is useless. You need local median household income and local home prices, along with mortgage rates, and then it might makes sense. But I really don’t care about affordability charts because there are so many variables involved (home prices, mortgage rates, household income, property taxes, insurance).

“Investors or second home buyers purchased 15% of the homes in September, down from a share of 16% in August, and down from the 17%-22% range in the spring and winter, according to NAR data.”

What’s the all time high % of purchases made by investors?

Wondering when/whether they will begin to unload properties

The all time high isn’t as important as it’s been pretty darn high for many years. It’s accumulative to some extent. 26% is massive if it’s SFHs. Even a 3 – 4 % decline makes a lot of difference.

The smarter investors are starting to get rid of their dogs now. I’m seeing more ruined houses come on the market- they were abandoned for too long or used as pot grow houses- lots of mold and rot. Structural issues. Also seeing ones in better shape (relatively) for more but overpriced and they are not selling.

I just saw one that the price has now gone down 50% from last year- of course it was (and still is) overpriced – no water source and off the grid, bad long eroding dirt rd etc. It’s a funny house- very small with new paint, granite countertops and new flooring placed over a steaming pile of grow shack. I think it’s going to just sit there for quite a while.

Today, as many homes went on the market in the past 24 hours as went on the market in all of the past week before that. All overpriced still.

Great analysis as always. I would like to add:

Lawrence Yun is again babbling about the fact that there is a shortage of housing and that should keep prices high (25% of homes had a bidding war according to him). I believe this is the last effort to mislead the delusional sellers which will worsen the situation.

With 75% of homes bought with a mortgage, people either qualify or don’t, and right now most don’t quality with high home prices and high interest rates.

So if they don’t qualify the bank won’t given them more money because a “housing shortage” will increase home values and change the bank’s appraisal.

I heard a marketplace item on NPR the other day, (I know, I know, save the invective — their dulcet murmurs & French horn interludes sometimes ease my nerves on short drives through long traffic), where the featured analyst was rounding off the burrs on the current state of inflation and the near-future of the housing market, citing “historically low inventory” as one the key drivers which would prevent a real fall in prices.

Not only nonsense, but it’s not what’s happening. Prices are falling. Duh.

Watch out after election,things could change quite dramatically.Free giveaways from current administration might slam the door on spr,student loan relief . We’re in bad shape can’t even ship on Mississippi River,WOW

Historically low inventory is a myth.

I hear the same thing in 2006-2007 as well where people would cite that prices cant fall as we have extreme shortage of housing.

Let the price fall little bit more, the sellers esp investors/second home would come out in droves to sell.

In the face of obvious evidence to the contrary, people make this claim because falling prices are contrary to their personal preference.

A few commenters here consistently do the same thing and it’s easy to infer it’s for the same reason.

Wolf has a graph for inventory that totally destroys the “inventory shortage” meme. It deserves its own article TBH.

There was a shortage a year ago.

There’s no shortage now.

The inventory surge is nicely duplicating the 2006-2008 surge.

For new homes only. But when you have new and existing homes competing, the lack of existing home inventory keeps prices of all homes high. That’s all that matters, at the end of the day. Prices are way too high, and those prices will come down slowly unless/until there is a panic selling increase in inventory. Most people are afraid to sell because they can’t afford the new mortgage rates at current elevatic prices. At some point (hopefully), there will be panic selling that will snowball price declines.

If even 4% of existing homes in some areas are owned by investors or are “second homes” or paid with cash (very low estimate in some places) then that won’t really matter much JeffD.

Using the GFC as a reference point, my daughter tried to buy a house during that period of time. She had a 10%+ down payment, stellar credit (800+), no debt, was pre-qualified, made over $100K, had stable employment (7 years), made offers at list or higher (but around the 3% gross/4% net income standard I use) , and NEVER was selected. Why? No one wants a get-me-done sale, especially in distress with 60-90 day closes. They just laughed at her 10%. The mortgage company stips were usually enough to kill the deal.

She was finally successful because my wife and I partnered with her which allowed her to pay cash for the house, with a 15 day close – only contingencies were inspections. No appraisals. No repairs. The offer was submitted with a proof of funds to eliminate any uncertainty. They bumped her $5K over her slightly above listing offer and we grabbed it. There were 20 other offers – most were higher – but they picked hers because cash, quick close, and no claims for repairs. If the inspections sucked, we’d just have walked. What little crap that we did find, the home warranty that I beat out of her agent covered the repair.

Some of the comments from folks that think their 5% down will “win” the day when prices drop allowing you to take your wrath out on the seller due to your being previously priced out of the market. If the bank owns the house, you have next to zero chance unless you are a cash buyer or your uncle is the bank president. Private seller? If they’re at risk, they’ll take less money on a deal that they are certain will close if there’s any chance of seeing daylight. But at 5-20% down and 90 day close? You’re dreaming. In a falling market, the bank can say it doesn’t appraise and refuse to fund. And, no, you can’t time the bottom. Don’t even try. You might get lucky, but you could also win the PowerBall or get hit by a meteorite.

Correct, there can be demand for housing, but without people being to able to purchase the homes, it is not a housing shortage, but the demand is pseudo-demand and the shortage is a pseudo-shortage. Moreover, the costs of insuring and maintaining the home seem to be headed higher.

Agree the sellers won’t be able to sell at current prices and those who are able, won’t sell, and places may just stay on the market as inflation lowers the inflation adjusted selling price.

Mortgage Backed Securities, MBS, is in effect a real estate backing of the dollar much like the dollar once was gold backed. Finance may not like to see the value of the backing destroyed.

How to get the real estate market running?

Make the mortgages follow the house. When those that bought expensive, but at low rates are to sell, the new owner step in and take over the mortgage.

The housing value remain and the new owner get the low mortgage rate. The seller get the high price, the buyer get the low interest rate and the MBS holders see the backing of the securities stable. And the show do go on.

“Make the mortgages follow the house.”

The loan is firstly based upon the creditworthiness of the borrower. This isn’t possible with guaranteed assumable loans.

You’re describing another welfare program for the housing industry, lenders, realtors, mortgage brokers, and homebuying debt slaves. All of it at taxpayer risk.

A house is supposed to a roof over your head. Financializing housing (on steroids) is the root cause of the problem.

I’m old. I remember assumable mortgages, but was never involved with one. Of course when the interest rates were on a 40 year downward slope the previous higher interest assumable mortgages were a moot point to a prospective buyer.

If I recall correctly the Robert Allen – No Money Down book ~ 1980 had quite a bit of content about seller financing. It had to be more of a high-trust society in those days for something like that to be mutually beneficial to both parties.

Shiloh1, it’s actually a solid investment IF the house is priced to a downward market and the buyer has a very big down payment. Like 50% or more. There have been a lot of deals like that where I am- not with the seller, but with private investors.

Maybe (?) unlike other areas, the agent I know who did private money financing required a very big down. Rates were quite a bit higher than market. People generally refinanced after the sale. These were houses that would not pass a bank inspection. I don’t think higher than market rates will fly much now, but I’d be surprised if we didn’t see more partial seller finances.

NEED TO RAISE WAIGES

LET GO TIGHT PURSE 👛 STRINGS

BUILD FOR THE 75% HARD AF WORKING CLASS

Great idea! Add to inflationary pressures by raising wages to fuel additional spending! That’ll fix ‘er.

Plus, the other 30% of people with cash would be insane to buy a house at these levels. NOBODY with a brain is buying.

With month to month 0% decline in the West…that tells you how many braindead we have here..

California is special alright…

I’ve been sitting on the sidelines for > 10 years. Do I have a brain? I feel pain but am resolute I’m not going to blow my wealth on a house until I can easily afford it. This means either wait until I’m much richer, or houses are much cheaper. 1990s prices.

Easily afford it to me means can pay cash with no stress, that the maintenance and taxes on the house would never be a burden or headache, and I’d have plenty of money to pay others to care for the property, including remodeling or refreshing every 20 years as needed.

No rush.

As a Broker for 47 years, Lawrence Yun could not predict his way out of a paper bag. Totally missed 2008-2012. And it looks like he is just a cheerleader for NAR this time even though it’s going to be worse than 2008+ and hundreds of experts are calling for a major recession.

“… he is just a cheerleader for NAR”

Awe give Larry a break He looks great in that pleated skirt ….

I just find it odd that CARs has given up and already fully admitting 8.8% decline in prices in 2023. Somehow this news has not travelled up to NARs.

Lots of red here….likely a LOT more on the way.

Here in southern CA we are in a Mexican standoff. Sellers vs Buyers. Prices are still stupid high (40% over 2019 prices) and some morons are still buying and closing. This is further inflating the sellers confidence that prices will stay high. I really hope we do get a correction soon.

That’d be called a blow-off top in the stock market. As demand wanes, prices float upward on declining sales volume for a little while. Then when the last

idiotsbuyers have been milked of their money, the crash happens.A person I know in LA has a landlord that bought within the last two years. Due to a medical emergency they have asked to pay rent a month late, but the landlord has said he doesn’t have the funds to float a month of rent. Unreal.

Wasn’t there a scene in The Big Short where the renters (paying rent) did not know that the owner-landlord was not making the mortgage payment.

BP,

It sound like the landlord is circumspectly telling his tenant that he is not a charity. He has bills also.

I think this depends on circumstances.

If the tenant was a long-term good tenant that has always paid on time, I’d float the rent once or twice and work with them to pay it.

I would value a good tenant and allow for temporary hardships.

If the tenant has never paid on time, and has destroyed the rental, I’d have the eviction papers ready.

They are not happy with the rental and cannot afford the rental.

Being a landlord is a business and not a charity. Your credit card company won’t allow you to float payments without a 30% penalty. A kindly landlord can do this for free as long as they are not being taken advantage of.

It really depends on the relationship between the tenant and the landlord.

Bob,

Landlord blah blah blah

Landlords of course also believe they are so smart that a tenant can’t tell they are really panicking because they really just made a speculative, parasitic investment. The guy has no money.

And think, we’re not even in a recession yet and there’s still lots of money out there.

Ha ha. Exactly what I tell people, this moment in time feels a lot like 1979/1980. Bought my first home at 12% interest. We have inflation, just wait for STAGflation.

Since there is now no official definition for a recession, at least one the common serf could see, we will never be in a recession until there is politically advantage to call for one…

The National Bureau of Economic Research gets to determine recessions.

I think the big issue is that unemployment keeps going home.

“Recession” was basically a new word contrived by the real estate industry ……

Designed to not have to use the word “depression” in describing the gift that the Fed is so historically generous in giving to us.

I feel very badly for the folks who bought their primary residence at the top of this market I’m not talking about giant hedge funds like BlackRock, I’m talking every day Americans. I truly fear many of them will get wiped out by this.

And yet, the fact is this: housing is insanely over priced, and it has to come to down, or there will be millions of folks who will NEVER be able to buy. My own all too modest home, tucked away in an unfashionable district deep inside the Bible belt, has more than doubled in just 8 years. And that’s here, in a quiet little side stream in the Deep South. Don’t get me wrong, I’d 1000% much rather this, than be underwater. But I’ve never seen my house as an ATM; its my home after all. If I could have my wish, some appreciation in value, sure, but not so much its cutting off the oxygen to some other family. That will never end well.

I sold my home 1.5 years ago. Way too high a Price so I feel a little bad for the couple, but not that bad. Stashed the $ in the bank (I know not making much) where it is very secure. Moved into an apt. for the 1st time in my life. You never realize how much a home costs you til you sell. No lawn service, no garbage pick-up, no watering, no repairs, not heating/cooling 3,000 sq ft of home, etc… Oh yeah, insane real estate taxes.

Next stop AZ when prices return closer to normal.

But they don’t have water in Arizona. Not sure that’s a solid long-term plan.

Greater Phoenix, AZ is going to have dirt cheap rental apartments coming out the wazoo. That’s probably going to be the most inexpensive way to live as this bust plays out. They’ll be offering “free 1st, last and deposit!” The place is so overbuilt it’s mind-blowing.

During HB1, there were condos with marble countertops selling in Phoenix in the 20Ks. It was unreal. These weren’t horrible neighborhoods, either. If you looked out in Apache Junction, you saw SFH selling in the 40s in liveable condition (cosmetically underachieving, but not falling down). I’m not certain any of these were available to the general buying public, as opposed to corporate investors, but they DID show up in the MLS.

I don’t know about Arizona, but they pulled a fast one in California during the GFC. All foreclosures had to be bought with full cash. The banks that owned them would not even loan with 80% down. And it is almost impossible to get a mortgage in California for $25K. Almost all banks will not loan less than $100K and many will not loan less than $200K.

So, all those homes went to cash investors- mostly large investment companies at a big discount.

Lynn….

My daughter was the beneficiary of that “fast one”. We bought her house for cash… and the offer was just like an investors – no contingencies other than inspections (roof, sewer, structural, termite/wood eating organism). Termites they’d have to fix by CA law (there were none). 15 day close. Prior to that, she was throwing offers around like wallpaper and every one was passed on.

El Katz, yes, I read your comment above as well. I’m researching alternatives for that $25K so as to be ready. One person suggested paying with CCs and refinancing, but I think I can get a personal loan. Hopefully not at 10-11%. The less the loan the higher the interest and shorter the loan term.. I understand why, but it seems so backwards. Maybe if rates go up near 8.5% in general I won’t need it.

El Katz, and thanks, that amounts to very good advice..

Actually, people who have bought their primary home in last 2 years with fixed 30 year rate of 3% or so are absolutely fine.

Why ? ==> because they have bought it for shelter, not for investment and if value goes down, should not matter as long as they are able to pay mortgages.

Investors who bought in last 2 years, second homes etc are the ones would fell the pinch and would be more than eager to exit the market.

It is very interesting to even think that you have buyers out there :-).

Few of my friends are buying their second/third home in San Diego in coming weeks.

Your first paragraph completely ignores the unfortunate fact that unexpected circumstances that can force a person to sell. For that reason and perhaps some others it is most definitely not “absolutely fine” to have purchased in the last two years.

Yeah, those 0.01% of homebuyers are sure in trouble.

Harrold, housing turnover is about 10%/year and about half of that is forced.

The best case scenario would be someone who buys at age 25 and sits in the same house for 50 years and then dies. That’s a 2% turnover rate as an absolute bare minimum.

The real kicker will be job losses when the Fed finally figures out how to actually stop inflation. (Hint: It’s the QT, not the rates. Higher rates just redistribute existing money via interest payments, from borrowers to lenders. They don’t reduce overall income. Higher rates are arguably even inflationary when the .gov is the biggest debtor, since the expanding interest payments drive additional government borrow-and-spending beyond the “baseline” budget. At least until the bond vigilantes force austerity measures.

Higher rates will make a lot actually uneconomic activity come to an end.

“At least until the bond vigilantes force austerity measures.”

Never happened in the USA and never will.

You people in the USA are in a heap of trouble with the economy and social order on a one way trip into hell.

Too bad you are going to take much of the rest of the world with you.

According to Nouriel Roubini, the dollar is going to lose its status as reserve currency. If that happens the US is done.

There are a ton of reasons people turn forced sellers and negative equity can hurt. Anything from death, divorce, job losses, illness and medical expenses can turn that negative equity into a realized loss. It took 6 or 7 years for houses to regain their “value” last turn. If we go the way of Japan they may never regain their peak.

“If we go the way of Japan they may never regain their peak.”

You had better so some research.

Some places in Japan have exceeded their bubble peak.

Average prices of new condos in Tokyo are at or near their peak too.

Other areas have not regained their bubble peak and never will. For most of Japan it was not more than an illusion.

What has happened in Japan is greatly misunderstood by most people outside of Japan.

Real estate turnover in Japan is minuscule compared to other countries.

During the real estate bubble supposedly the price of real estate went through the roof. Well, the truth is that there were a few sales of properties that had prices go through the roof.

Then everybody assigned that increased value to every piece of real estate in that particular area.

For example, in one resort area real estate is so illiquid that you had maybe one or two transactions a year during that time.

The other 99.99999999% of owners never sold and had no intention of selling. The increased price was meaningless and had no impact on them whatsoever except for increased property taxes.

And if they tried to sell at those prices, I doubt that there would have been a buyer for 99.999999999999% of the properties either.

Furthermore, one of the big reasons that the bubble was so bad in Japan was exactly because of the lack of liquidity in the market. One cause of this was tax. Taxes on gains were extremely high given the low cost of many properties.

Transaction costs were also very high including various government transaction taxes and levies.

So rather than sell the property, some people and companies took out loans based on those inflated values.

Sell and you’d end up with a whole lot less money than the sales price. Borrow at the “inflated” value and you could extract more money. Use the borrowed money for other things such as overseas investment.

You could buy a nice house in the USA for the equivalent fees and taxes incurred in selling a property in Japan. Borrow against the property and you still have the property and only the interest and low fees to pay on the loan.

But when it came to “pay the piper”……………oops the property wasn’t worth the loan value. Not even close. No buyers at those fake, inflated prices.

And that’s why the bubble burst.

Large pension funds like the Ontario Teachers Pension fund buy up entire towns in the USA for profit.

Quite amazing, given that Canada lauds itself as a socialist country with Liberal values.

Canada “socialist”???

The folks who purchased, in the last few years, at the top, with some mortgages 8x income and foolishly jumped on the greater fool property ladder insanity ZIRP cheap/easy money 3% down use my Uber job to boost my income statement bidding war no inspection bandwagon deserve everything coming to them…

Stupid should hurt. Fools will learn no other way…

I’m expecting mortgage forbearance and foreclosure moratoriums in the near future, again.

Agree.

2B, you have to take governmental stupidity into account. That brand of stupid tends to hurt responsible folks while rewarding those who made bad decisions. How will our central bank respond to the next housing collapse? How will our politicians respond to the next collapse? American voters screaming for handouts are much louder than they used to be and politicians are much more accommodating to them.

Nobody really knows what monetary policy is going to look like a year or more down the road. Maybe the Fed will stay tight or maybe they’ll loosen for a variety of reasons, but it at least looks like a pause is highly likely. If we run into a really dire GFC-like situation, they have a now well-established history of loosening too fast and for too long in a panic. Paper tigers don’t change their stripes. Our politicians have also set a strong precedent for things like debt forgiveness, payment moratoriums, and the like. The next collapse is not going to look like the last one. We should expect government intervention on a whole new level next time.

Unfortunately NS, I have to agree with you.

WE, in this case the thrifty and prudent savers, etc., have been and will be paying for this GUV MINT irresponsibility for ever…

And, as has been the case always, our money will continue to degrade until it’s even more worthless than it has become over the last 100 years + since the rich folks came up with the FRB to steal legally our savings and the value of our labor.

Might as well get used to it, eh?

Realtors in my market are still experiencing bidding wars on *some* properties that are appropriately priced and in good locations. Obviously things are much cooler relative to last year where any property, regardless of the location, was swamped with buyers. Also, 22% of buyers remain all-cash, meaning just over 1 in 5 buyers have no exposure to interest rates. Unless the remarkably resilient jobs market takes a swift, violent swan dive, many homeowners will avoid selling and stay put as their existing mortgages are likely at rock-bottom rates. The housing market may be correcting on a regional basis, but until large quantities of homeowners are forced to sell, I’m hard pressed to see a major correction in prices in the near term. I’d also wager we see a modest correction in the 10-year yield/30-year fixed rates by the end of the year which might take some pressure off of rates. If not, more and more buyers will go with ARMs in lieu of conventional.

” I’d also wager we see a modest correction in the 10-year yield/30-year fixed rates by the end of the year which might take some pressure off of rates. If not, more and more buyers will go with ARMs in lieu of conventional.”

Not with job losses accelerating and inflation raging in other areas (see Wolf’s articles on services inflation) which are reducing purchasing power.

Many big companies are laying off big, and the stock options are crashing (look at Facebook). This will be similar to 2010 when despite aggressive rate cuts and QE home prices continued to plummet due to job losses and uncertainty over employment, except this time the Fed’s hands are tied (Exhibit A is what just happened in England).

Are job losses accelerating right now? I try to keep up with wolf’s articles but the last one showed still strong employment numbers. I know tech companies are “downsizing” but a lot of those people are still finding other jobs.

Genuinely curious, because here in Canada it seems a lot of senior workers left for good and despite tightening conditions a lot of companies still struggle to fill positions.

Unemployment numbers remain near historic lows. Some high-flying “growth-oriented” tech companies are laying off in small numbers, but not enough to have a tangible impact on the job market. I work for a tech company that employs 300k people and so far, no mention of layoffs in the near future (knocking on wood).

In the past, ex-employees of the tech companies have spawned lots of startups.

They’re not, people on here try to wish doom into existence.

sc7, I also work for a tech company and I can tell you that almost everyone in the industry is worried for their job. Some companies like Amazon may not do layoffs but are rumored to be aggressively letting people go for performance reasons. There was just an article about Stripe implementing something similar. Then of course other companies have done real layoffs. Elon supposedly wants to fire 75% of Twitter. Of course tech is just one relatively small industry but these formerly well paid people will stop buying and be forced to sell houses, etc. More traditional companies like Ford have done layoffs. It’s not at the level of 2008 yet and I am not “wishing doom into existing” but I am certainly quite worried.

Job losses are not accelerating, at least not yet. The best real-time proxy for this is the number of unemployment insurance claims which is still skidding near historically lows levels.

Obviously anecdotal, but I have never ever at any point in my career received SO MANY messages from recruiters as I did over the last 2-3 months. I basically stopped checking my LinkedIn inbox.

And no, I am not any kind of a unicorn guru – I’m just a regular IT person with a pretty narrow skillset and stack of technologies I work with and I have not really updated my LinkedIn profile since my last job search in 2020.

I sometimes looked at those messages with some bitterness as my first thought normally is “Where the heck you’ve all been in 2020 when I really WANTED and NEEDED a new job and I would have considered any of those positions in a heartbeat???”

On another related note – we just had another team member leaving our company for another position (apparently higher paying) last month after only working with us for less than a year, and we are now interviewing other candidates and two of them updated us very shortly after the interview that they were not available anymore as they were accepting other offers.

I sure understand things can change very quickly, but so far it looks like our organization is struggling a lot to hire and retain people, at least for mid-level IT positions.

Agree with you on both fronts, sc7.

Job losses are not accelerating yet despite the wishful thinking of many posters here, who wish doom into existence. This MO seems to make up for the majority of Wolf’s audience despite Wolf’s always insightful and sometimes actionable posts, which is unfortunate because replies could be a source of further insight instead of what they typically are.

My local grocery stores in flyover have elderly working registers,customer service and younger staff picking groceries for delivery/pickup also bringing carts back to store. Most older people seem happy at these jobs

In my area, the elderly are bringing in those grocery carts just as much as the younger workers. These are seniors in their mid-to-late 60s from the looks of them, men and women. Not every Baby Boomer is living large.

As for Facebook, it seem Sandburg was heart and soul of company.

Realtors still peddling the ‘bidding wars’ nonsense? People may not want to sell due to low mortgage rates, but their houses won’t ‘worth’ what they paid for. Dilemma dilemma

These realtors are family members actively involved in the housing market. If it was purely anecdotal evidence, I’d toss it.

LOL you just gave the textbook definition of “anecdotal” evidence.

“I’d also wager we see a modest correction in the 10-year yield/30-year fixed rates by the end of the year which might take some pressure off of rates.”

With QT and no reason for the Fed to stop raising rates, I’ll take the other side of this wager. In fact I am taking the other side as I sit in mostly short-term t-bills, but would like to go longer-term if rates were closer to or a little over inflation. I think rates are still correcting, but to the upside. I agree with you the jobs market has been remarkably resilient, but that works against your belief rates will correct downward and is one of the reasons I think rates will continue to climb. I’m open to changing my mind as circumstances change and admit anything can happen over a couple months. I guess that’s what makes a market.

many home owners would not put their homes for sale but home prices are defined on the margins. So few home sold for less in a neighborhood bring the comps of all homes.

Josh, valuations are based on transactions, not the pipe dreams of people who think that not being “forced to sell” can somehow prevent transactions from occurring at lower prices, which is precisely what’s happening. This silly argument is very common right now. I guess this is a part of the denial phase.

JoshWx,

So if I think I can get $2 million for my home, hopefully, and I put it on the market at $500k to stir up a bidding war, then there’s going to be a bidding war, and I might sell it to the winner for $1.5 million, with “1 Million Over Asking after a Massive Bidding War,” in the headlines all over the news… Sounds funny? This is done a lot. RE is kind of funny.

Well if there comes a time where forced sales are much more common and sellers have no other choice than to take a massive loss, maybe a psychological coping strategy will be to list way below actual value, get an offer well over asking (Still at a huge loss) and just revel in the fact that closing was well over asking. “Hey I lost 200k on my house, but guess what, we got 100k over asking!”

But I do get your point – it’s all relative…

He just said that.

So there’s one thing that I am not sure I understand on a conceptual level.

Let’s say I bought a house in 2015 for $300k.

Some time in 2021 I may have refi’ed at 2.5%.

My neighbor sold his next door house in May 2022 (let’s assume it was 100% identical to mine) for $700k.

Let’s say I decide to sell in March 2023.

I can put a $720k sticker on my house, though probably nobody will bite.

Let say I finally sell the house in May 2023 for $630k.

This selling price would reflect:

~ minus 10% to the hypothetical price of my house that I may or may not have gotten a year prior

~ plus 110% to the price I paid for the house 8 years prior

Now here’s the thing I don’t get – everyone will call this 10% drop “housing market crashed!”. And this is where I get totally lost –

a) market drops – doom&gloom, “we will all die”, “market is crashing”!

b) market rises (!) – doom&gloom, “people are priced out of the market”, “housing is unaffordable!”

Now if I decide NOT to sell, I’m probably in an even better position having a mortgage of ~30-40% of my house current value at 2.5% rate for the next 10-15 years – doesn’t sound bad at all if you ask me!

I sure understand that market drop will be somewhat painful for my new neighbor who bought a similar house for 700k a year ago _if_ he decides to sell now, but I don’t see how the situation can be too bad for anyone who basically bought a house pre-covid? They are not really “losing” anything, unless we consider a housing just an asset that can be instantly sold and bought at will trying to time the market (which obviously it is not). So why such a panic lately and what market behavior would be optimal if either price hikes or price drops don’t seem to make people happy?

Sorry if that question sounds naïve or if I miss some fundamentals, but sometimes judging by MSM it feels like wherever the market goes, it’s bad, period, full stop.

I doubt many institutional buyers are actually paying cash. They are borrowing commercially. The appeal of real estate is substantially driven by leverage.

I don’t know whether these buyers are exposed to rising rates.

No business uses there own money ,always borrowed. Never put your capital at risk .Biggest problem is everything is leveraged ,got to have some skin in investments or it’s all fake. Return to 20% down on a house it will change market quickly

22% do lump sum cash purchase??? Yikes. Is that Canada?

I wouldn’t say that all-cash buyers have no exposure to interest rates. Institutional or private investors are likely enough to already have or take up new debt and interest rates will still affect their loans. Think of corporate debt issuance (bonds). If some of them are servicing variable rate debt, or making losses on stocks as bond yields continue to climb, then downcycles could push more investment properties into the mix.

This data gives me some hope, but, here, in a second-tier New England city that has absorbed many WFH folks fleeing expensive first-tier cities, I’m seeing price drops here and there, but nothing significant. Houses still move at significantly higher prices than they did last year, especially at the sub $300,000 range. I think it will take job losses for this to change.

I didn’t buy last year when rates were low, thinking I didn’t want to be trapped and underwater. Plus, all the houses in my price range seemed awful. But now it seems like prices won’t ever be as low as they were even last year, plus interest rates have gone up. So now I fear I’ll forever be trapped as a renter, even though I make a decent salary and have a decent down payment. I’m guessing this is a paradigm shift, the final squeezing of the middle class.

Or perhaps I’m being too internet-brained, expecting things to change in months and not years… Only time will tell.

Are there any second tier New England cities, price wise, other then a few small ones in northern Maine? Bangor was a very sleepy market until the pandemic hit and I would have put that at the most affordable 30,000+ city in New England. Sub 300k homes that aren’t dumps are just starting to show up again.

I reckoned he was talking about Worcester, MA. Sutton and the like used to be more affordable and solidly middle class, now not so much. Boston exiles to be sure, but 84/90/290 always drew NY/CT super commuters. Not hard to believe many more flocked in the past few years. No doubt some exodus will happen with return to office, its a smooth drive except for in the thick of Hartford but as a routine its not for the weak of heart especially regularly after a few months and with these gas prices.

“I make a decent salary and have a decent down payment.”

?????????

If you make a “decent salary” and have a “decent down payment” and can’t afford afford a sub $300,0000 home, I think there is something wrong somewhere!!!

Take a look at the available East Coast houses under $300k and you’ll have your answer. Be sure to bring Lysol.

I live in NH. The massive influx of out-of-state buyers has driven prices up statewide. We’re actually at a point now where a lot of northern NH towns have higher median list prices than southern NH thanks to all the prolific second, third, fourth home purchases (a lot of Boston $$). Prices are holding well across the southern portion of the state but if you don’t mind living up north, a big correction is inevitable north of the Lakes Region. Dilapidated crapboxes in North Conway area are selling for 450K+.

Anything on a lake up there is taxed to oblivion. A family member had to sell a very well used second home that had been in the family since the 1930s because of taxes. It’s now an AirBnB. Anything not right on a lake will be a great deal if you don’t mind living up there. Very pretty countryside. Not much in the way of healthcare.

Yes, this is the idiocy of New Hampshire governance, proudly boasting about having no sales tax and no income tax. Instead they have sky-high business taxes, hence why all of southern NH commutes to Mass. businesses, and also ridiculous property taxes where lakeside shacks get taxed like $5,000,000 oceanfront mansions. If it weren’t for Mass. businesses and very low fuel costs for so long, NH would have the same podunk economy as some don’t need to be named southern states do. They have never seemed to understand that you can shift taxes all around to play whatever game you want to play, but in the end you still have to pay the piper.

I am getting personal flyers from Berkshire Hathaway realtors now. I have lived here for 18 years and this has never happened before. I’m wondering if this a sign that sale properties are thin on the ground now.

I’m also getting a lot more Realtor ads than usual.

It’s not so much that there are fewer properties for sale, as it is that actual sales are down and their cash flow is receding. They’re trying to find more business.

The housing market being described as frozen mirrors my local market.

Listings exploded; nearly doubled in quantity a few months back, now essentially nothing new is being listed, nothing is selling, and prices are stuck at nosebleed levels.

Sounds like a denial phase.

Watch out during the acceptance phase……

Yeah, we’re only in the 3rd inning of this game.

During HB1, my friend took 2.5 years to sell his home. Original listing price was 800K, sold it finally for 475K.

He had numerous offers but he rather decided to chase the down market.

I’m watching one flip near me with particular interest. Purchased in February at $517K, back on the market in May for $685K (plus a renovation). It’s now been on the market for 152 days and the seller has cut the price 11 times, all the way down to $520K. The seller’s already accepted a loss and every reduction from here on just worsens the pain.

I love these kinds of stories. They warm my heart.

I’m still in the anger phase.

Why are you angry? It has been profoundly obvious that prices are insane for several years at least.

This is fascinating to watch play out. It’s like the Manhattan commercial market where landlords will hold empty spaces for far longer than seems sane because they will not lower the rent. I hate to say it, but it almost always the right decision.

Commercial rent is a completely different ballgame

Arya Stark,

Wait a minute…. Commercial landlords often CANNOT lower the asking rent beyond a certain point because of the requirements of the loan. Asking rents have to be high enough in theory to service the loan, pay for maintenance, etc., even if the landlord cannot find a tenant willing to accept the rent, and no one is in the unit/office. And when the LLC that holds the property (collateral for the loan) runs out of money, and the landlord doesn’t want to throw more money at it, the landlord hands the office tower to the lenders and says, hey, this is your baby now, and washes his hands off it:

https://wolfstreet.com/2022/03/22/another-office-tower-goes-bust-blackstone-walks-from-manhattan-tower-it-bought-for-605-million-cmbs-holders-to-eat-remaining-losses/

And the lenders then sell the office tower in a foreclosure sale at a HUGE loss:

https://wolfstreet.com/2022/02/17/whats-a-vacant-office-tower-worth-foreclosure-sales-show-how-values-of-1980s-office-towers-in-houston-have-collapsed-dishing-out-huge-losses-for-cmbs/

Yes but I was referring more to retail commercial space, i.e., store fronts in Manhattan. Although they may be under the same constraints.

That’s so obviously inefficient that there’s probably a lucrative business opportunity in there, for someone willing to take an entirely different approach to the game.

Someone who owned the property outright, or at least with far less debt, could afford to be extremely flexible on rents. They’d be able to keep their property fully occupied and destroy all competition during a deep recession.

I just saw an article about NYC landlords “hoarding” rent-controlled units (about 95,000) vacated during covid, by death or other reasons. One said because the units had long tenancies they needed a lot of work, and he did not want to refurbish for such a low rent. Apparently they are pressuring to have rent control lifted citing the housing shortage before they will rent them.

The “shortage” of homes in the US is all fantasy. Lack of inventory is due to (unoccupied) hoarding by the wealthy (since homes are investment assets now) and short term rental properties (e.g. AirBnB). The economica blog’s most current article describes this.

typo: meant Econimica blog

NYC is infamous as an offshore money laundering environment. Some of those buildings and condo units are worth more empty as they are traded like chips on a gambling table. Losses are not as important to billionaires laundering money. Chinese and Russian mafias, African government embezzlement, Latin American government embezzlement and cartels.

Same in Miami. When FiNCEN had a pilot program requiring the beneficial owner of the buyer’s financial companies to be exposed and monies accounted for, the all cash sales in Miami decreased by 70 or 75% almost overnight.

The pilot program was successful enough that some of the aspects of the program, including exposure to the government of true beneficial ownership of offshore LLCs will now be extended across the entire country. It will definitely have some effect, even if they find some loopholes.

Inflation is at eight percent, but the Treasury yields are approaching five percent and the Landlord class is panicking, especially in Canada where they charge a few grand a month to rent a makeshift furnace room with bizarre stipulations.

Everyone and their mother became a rent-seeker thanks to the FED’s easy money policies and the largest credit bubble in the history of mankind. There is a large number of people who have no business being landlords, not having anywhere near the resources needed to weather any sort of financial storm. Their financial clocks are about to get cleaned.

There can be no real asset devaluation without job losses. Why would the percentage of the market renting out their “illegal hotels until big tech disrupted the market”, i mean homestay rentals, purchased with all cash, want to put them on the market at a loss if high flying upper income earners are still renting them? When 6 figure jobs with no real benefit to society dissapear and there are no longer any CNA job openings, and when the rest of people’s retirement income, tied to a super inflated market collapses, then the affordable sales will happen.

If there cant be real estate devaluation with job losses then what explains this price decrease and low volumes ? The job market is still pretty hot, unemployment rate all time low.

The way I see it is : It is a question of affordability. A town may be selling homes for $500K, where the employment rate is say 100%, but people are earning measly $40K/year. Despite this 100% employment rate, the homes won’t be sold for $500K because people, although employed, are not able to afford.

The same is happening right now. Prices too high, mortgage rates too high.. making homes un affordable.

Agreed that this is what we’re seeing now, which is why i used the qualifier “real.” By real, I mean drops to prices even below late 2019 highs, which were already inflated without the turbo charger running. Otherwise there will be no reckoning of affordability for the great unwashed masses.

High rates and crashing stonk mkt sure isn’t going to make it easy for all the money-losing zombies to float more shares and/or debt to keep those unwashed masses employed, so we’ll see those price drops below 2019 highs soon enough.

The houses weren’t affordable for most in 2019, either.

A lot of jobs depend on home sales. Not just mortgage brokers, appraisers, RE agents. Also furniture and appliance businesses, painters, movers, carpets, all those things that often get changed when a home changes hands. And of course the MBS finance industry. Many of these people will be unemployed or earning less.

There’s also going to be a big downturn in construction, with the same kinds of income loss issues.

Lots of people will be forced to sell.

I am still patiently waiting for construction materials like hardwood floors to come down with sales&discounts as I didn’t want to pay what my builder was charging for premium options, but I am yet to see any meaningful sales on those.

Digger says: “There can be no real asset devaluation without job losses.” As opposed to job gains? The labor market has held up well considering the deflation going on in the financial markets. Inflation is a supply side problem. So fix the supply issues. Keep the jobs. A national job guarantee would also mitigate inflation.

People are still dying. The first forced sales are the kids unable to do anything with moms house.

Probate leads the market lower.

Off Topic but I had to toss it in: SNAP just went “crackle” and “pop”.

Investors who add milk to their shares and might at least end up with a bowl of cereal…

Check out META taken down by SNAP again, it seems.

Yeah the whole sector is getting haircuts after hours.

SNAP is off 26.88% as I type. That’s a lot of pain.

Cnbc said to buy,laughed so hard ,brought tears to my eyes

No real surprises in the home sales data given the recent rapid rise in the interest rates over the past 6 months and delusional sellers still clinging to artificially high home prices.

What home sellers don’t understand is the rapid rise in home prices from let’s say mid to late 2020 through mid to late 2021 was nothing more than a classic capital market “blow off top”. In the stock market, the blow off top occurs very quickly, first accelerating higher at a dizzying speed and then drops just as fast.

In the housing market, the final blow off top (of rapid price increases) took about 12 to 18 months, most likely ending maybe in early 2022. The drop in prices will come and have already started but the problem is, home sellers don’t want to accept that the last 20% increase in their home prices was all make believe (or maybe they simply don’t understand basic math). Just made up, out of thin air, courtesy of yours truly, The FED.

Any smart home seller will look to aggressively price their home and exit as they abide by the old saying “those that sell first, sell best”. For the others holding onto a pipe dream, once the real impact of interest rates roll through combined with job stagnation or losses, and then layering in “comps” from recent sales that will begin to push valuations lower, well all’s I can say is good luck.

Wasn’t there a scene in The Big Short where the renters (paying rent) did not know that the owner-landlord was not making the mortgage payment.

Got a “cold call” pamphlet in my mailbox yesterday for a brand new housing complex with extra fancy modernist luxury condos out in a modestly distant exurb from my current city. I am not sure how these developers are hoping to sell those especially given how the housing market is going as outlined in this Wolfstreet article. Its kind of hard to sell “All the cost of being downtown while in a distant hard to commute from exurb with no attractions. Plus, ‘all’ the zero-lot condo space with no greenery of downtown in an area that people only move out to for the purposes of having large houses with significant acreage (and often even horses.) Yes, we are the worst of all worlds!”

While it may have been clueless for them to build this space to begin with, there is a sign they are aware they are now in trouble. Namely: I am not on the market for buying anything and am showing no signs of being so, and yet these developers sent me a gigantic glossy magazine-sized and magazine-thick promotional pamphlet filled with large full colored pictures all on expensive thick and glossy stock. They seem to need someone, anyone, to start taking these off their hands ASAP and don’t care that they are cold calling with what might be $5 or even $10+ promotional pamphlets that were probably once reserved exclusively for people giving strong signs of interest specifically in their development.

Lets see how many more of these I get from other developers over the next year.

The Federal Reserve is still hiking rates and have no reason to stop, but the true believers still come out on every real estate article preaching how prices won’t go down and the Fed must pivot. They will have to continue hiking rates until those people go away, but the Fed has no credibility and it will take a long time to convince.

I see this incompetent administration over reacting to the spike in mortgage rates and signing an executive order freezing interest rates on new mortgages. They are probably already working on it. They will cite price gauging by mortgage companies just like they have done with the energy industry. Once mortgages hit 8% its game over for the real estate industry. The credit markets will freeze up and there will be no sales or listings. Those sales that are forced to occur will be 20% to 30% below current levels.

The problem is not interest rates, it’s prices. If prices drop, then housing becomes affordable for more people.

22% of sales are to cash buyers, so nothing will freeze.

I think some of the tax deduction laws, those especially aimed at the Real Estate market, should be eliminated. That would help tame inflation.

Eliminating just depreciation for single family residences would be a game changer, and would mostly affect rentier investors.

Wolf’s charts are so much more interesting than any drama on Netflix.

The articles and comments keep me up late reading and get me out of bed early waiting for the next plot twist. Thank you!

In summary:

1) House prices have dropped 7% from June 2022 levels but are still up 35% (They have to fall 26%) from Jan 2020 pre-pandemic prices.

2) Active listings are up 133% compared to the pandemic lows in 2021 but still 22% lower than Jan 2020 levels.

3) Mortgage rates are up from pandemic lows of 2.5% in 2021 to 7%. Mortgage rates are up from the Jan 2020 4% rates.

In order to restore the more stable 2020 pre-pandemic housing market, prices must drop, active listings must increase, and mortgage rates must fall.

I am staying tuned for the next exciting episode.

“In order to restore the more stable 2020 pre-pandemic housing market, prices must drop, active listings must increase, and mortgage rates must fall.”

Affordability is key. Unless lending standards just go completely out the window, prices will drop simply due to lack of affordability. Active listings don’t really matter yet, otherwise why would prices already be down now if active listings are still below normal levels?

Also, I think you meant to type “mortgage rates must rise” for prices to drop. That is correct, and a further rise from here will obviously worsen affordability. I see no way death-pledge rates stay under historical norms of 9% with the Fed lollygagging on rate raises and employment being so stubborn.

And just wait for higher rates to kill all the zombies. They’ll start laying off all those hopeful-buyers-in-waiting, just like the last crash. Then you’ll have both an influx of active listings AND nobody to sell them to.

“In order to restore the more stable 2020 pre-pandemic housing market, prices must drop, active listings must increase, and mortgage rates must fall.”

The 2020 housing market was still based upon a fake economy of QE and USG deficit spending. It wasn’t even close to normal.

If the 1981-2020 bond bull market is over which it almost certainly is now, mortgage rates aren’t going to return anywhere near pre-2020 levels.

I agree that the housing market was still crazy in 2019 and early 2020. I thought and commented that we were at a peak in 2019.

In 2020, the housing market went Batsh*t crazy.

Returning to just a crazy norm would be a drastic improvement.

I don’t think QE is gone forever. MBS purchases might be if the landing is soft. If there is a 30% crash, MBS’s will ride again and save us all.

You forget that we liven in the Outer Limits where the Fed controls the vertical, horizontal, and the clarity of our picture.

If there is a 30% crash in housing, there will be a recession and inflation will no longer be a problem to be solved.

“Despite weaker sales, multiple offers are still occurring with more than a quarter of homes selling above list price due to limited inventory,” Yun (NAR chief economist) said in a statement.

The lack of inventory is the problem that has to be rectified before the market can move downward in proper proportion to the higher home prices and interest rates. When there is a pre-pandemic level of inventory, we would see some movement. GFC levels of inventory, even better.

Yun’s statement is anecdotal, dressed up as average, and is therefore propaganda. If there were this kind of demand, prices would jump. But they fell. That’s what the numbers say.

Wolf – if you were to make an educated guess, how many months/years will it take for the housing market to find the bottom of this bubble?

Depends on the rich,they get nervous ,bad things happen they already pulled 25%.If retail investors keep buying dip it won’t end until retail is broke .By the way rich are also buying properties in foreign countries. Can’t stick around fort mayhem

Last time it took about five years to hit bottom. The Fed threw trillions of dollars at it starting in 2008, and then it bottomed out in 2011. Now we’ve got lots of inflation, and the Fed is doing the opposite.

‘Lack of inventory’ is indeed interesting. Instead of measuring in absolutes, months of supply may be more accurate. Regardless, I could argue that there is no escaping from the devaluation coming from high rates. Assume a scenario where rates are into double digits, record number of sellers exit the market, sales plunge and inventory is low. What happens? Someone on the block dies, their estate sells the house at market price and brings down the valuations for the entire neighborhood.

Housing always works on the margins. For most people the value of their house went up without ever listing it on the market. It goes down the same way. Even with low inventory, the reversion to mean doesn’t stop.

Agreed. The rate of decline doesn’t matter as much as the final destination.

As I’ve been saying from the beginning, people are still paying to live near SocalJim!!!!

The Freddie Mac rate of 6.94% that you refer to in the article includes 0.90 points to buy down the rate, which is the only reason it remains below 7.0%. Freddie Mac quotes rates that often include points – unlike the MBS rate quote of 7.37%.

Not that far away, a sale closed for about 90% of the initial listing price after being on the market for two months. This is close to the 7% decline in the median price of existing homes.

My next door neighbor’s house just went up for sale at a 7% discount from Zillow’s estimate. Coincidence or maybe they are aware of the statistic.

A few years down the line, may be time to buy real estate again… get ready now. I’ll be too old to play, most likely. But I’m going to prep my granddaughter. The housing shortage in America continues…

Probate Probate Probate.

The logjam will break every time a pair of siblings can’t pay the back taxes on mom’s house when she passes.

Probate always ends the impasse.

Not always. Here in So California, LOTS of millennials and even some gen-Xers live with their boomer parents in multi-generational households. The kids will happily assume the parent’s house that was purchased for much less a while ago. One sibling may not be able to afford a house, but maybe they could afford to buy out other siblings. I’ve seen this happen a couple times to gen-Xers I know in recent years. Paid-off houses can easily be put up as hands-off rentals handled by property management and the rental income gets split by the kids.

Sure, there will be houses that hit the market when the owners get too old or kick the bucket, but certainly not all of them. Houses can stay in the family too. Don’t forget, we millennials are a bigger generation than the boomers. We’re starved for places to nest and SFH construction has been really anemic for a solid 10 out of the last 12-14 years.

Yes and no. In the Bay, these homes of deceased parents no longer benefit from uber low tax rates. As I understand it, that law changed last year, and you would have had to make the transfer of ownership to kid(s) before the deadline change. Now, if your parents leave you a house, you’re on the hook for property tax at full market assessed value. For many millennials, this is barely affordable, or not at all. Property taxes are going to kill lots of real estate transfer in California once job losses mount. Think about an average price of well over a million dollars, coupled with a tax rate of 1.23%. Unsustainable? Yep.

Did they bypass the Prop 13 inheritance of property taxes in CA?

I think this only applies if you rent out your deceased parents home.

If you live there, you get to enjoy the $1.5K/year property taxes (2%/year max increase) on a house purchased in the 1970’s for 50K. Even though the house is now worth $2M house, thanks to Prop 13.

Your new neighbor who purchased for $2M will have to pay $22K/year in property taxes + Mello-Roos, bonds, etc.

Question: in what essentials, if any, is our real estate bubble unlike the Japanese debacle?

IE: is the optimism so widespread among realtors that we’re not heading to the same slaughterhouse warranted?

There is nothing similar between the Japanese real estate market and the USA real estate market other than the words “real estate”.

I live in Bellevue east of Seattle where real estate prices have been skyrocketing for years. New massive condo developments in construction all over the city. Today I looked at condos available for rent in downtown on Zillow and stopped counting at 575. Asking rents staying high. At some point the landlords will have to blink and then everyone will want a rent reduction.

A 7% reduction in prices when the normal seasonal reduction is about 5% is statistical noise. The real estate crash so many are anticipating might be coming… but it’s still not here yet.

I agree and share the sentiment. The directionality of data looks down. Not sure if the prices would actually go down in any meaningful way. When I say meaningful I want 30-40% or more to go back to 2019 levels which was quite high anyway to begin with.

We don’t need high unemployment for the prices to go down. We just need mortgage rates to keep climbing higher .

All the government and federal reserve needs to do is ensure mass layoffs never happen, then people will always be able to pay their mortgages and the price of they paid for the house won’t matter.

Wannabe oligarchs attempt to use lobbying and other means to influence politicians in Washington D.C. and the Federal Reserve officials in order to enrich themselves. For example, triggering housing crises and buying foreclosures in bulk for discounted prices. Fortunately, the USA middle class has a long track record of effectively overcoming the interests of oligarchs and preventing mass layoffs and housing crises.

Therefore everything is fine, nothing to worry about. Just get mortgages and buy as much house as you can qualify for.

We are simply working our way back to a normal market again. Inventory, prices, time to sell, reductions etc are all still out of whack.

These wall street & fed induced straight line booms and busts benefit no one. Slow moving, boring housing markets are always the healthiest ones.

Mortgage apps off around 60% yoy. Sales off about 25% yoy. Cash buyers about 22%. Those numbers do not seem to jive. Does the 22% represent a large increase from a year ago?

Jdog,

The mortgage app figure you cite is total mortgage applications, which equal the sum of: purchase mortgage applications (to buy a home) + refinance applications (to refinance an existing mortgage).

Purchase mortgage applications have been down between 23% and 37% yoy over the past six weeks. But this reflects what homes sales will look like in October and November. Mortgage apps in August, which would relate to closed sales in September (which this article discusses) were -18% to -24% weekly, right in the range of September closed sales. What current mortgage apps are showing is that October and November home sales are going to be extra shitty.

Refinance mortgage applications have collapsed by about 90% yoy

This has the details and charts:

https://wolfstreet.com/2022/10/05/housing-bubble-woes-mortgage-demand-plunges-rates-near-7-spread-between-mortgage-rate-10-year-treasury-yield-blows-out-most-since-dec-2008-and-1986/

We just got our first appraisal case after being stiffed for 2 weeks. At this rate we may qualify for food stamps. Our income will not even cover our overhead. The market is dead. No one is buying, selling, refinancing. Listings are non-existent. Real estate agents and brokers are going to be SOL (Sh$t out of luck). Lawrence Yun is going to be pounding sand.