Health insurance up 28%. Housing costs spike. New vehicle CPI jumps. Food-away-from-home spikes most since 1981. But used vehicles fall, food-at-home backs off from worst since 1979. Inflation Whac-A-Mole.

By Wolf Richter for WOLF STREET.

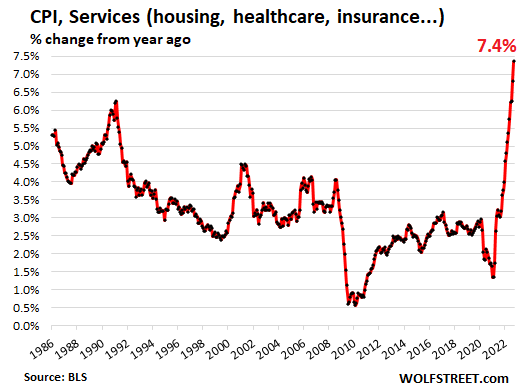

Nearly two-thirds of consumer spending goes to services. And they’re now the driver of inflation. The CPI for services spiked in September for the 13th month in a row, and by the most since 1982, and it accelerated month-to-month. Housing costs spiked, but also all kinds of other services, such as health insurance (+2.1% month-to-month and +28% year-over-year).

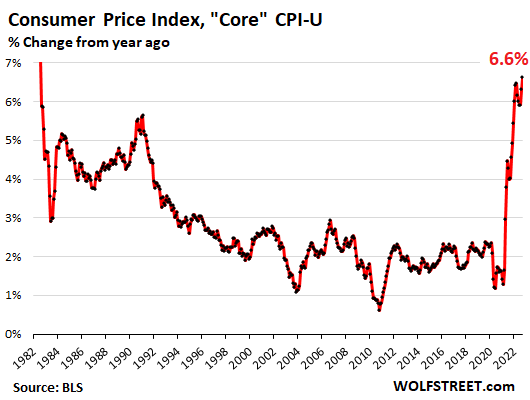

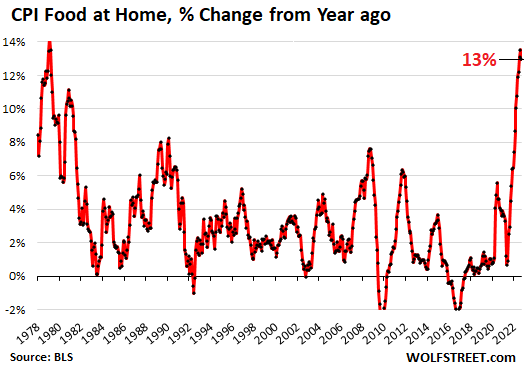

“Core CPI,” which excludes food and energy, was the worst since 1982. Food prices spiked again, but spiked slightly less than the prior month which had been the worst since 1979. But some relief came from a decline in prices of used vehicles and consumer electronics, and from gasoline, which plunged.

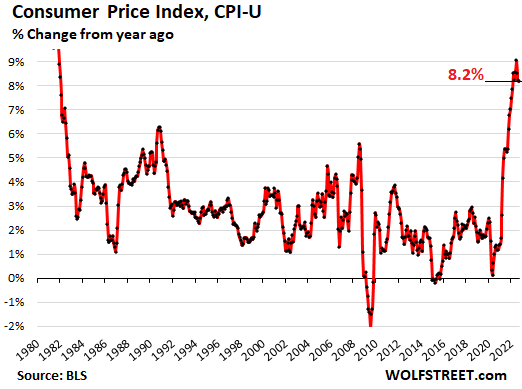

Overall inflation as measured by the year-over-year Consumer Price Index (CPI-U), released today by the Bureau of Labor Statistics, jumped by 0.4% in September from August, a sharp acceleration from the prior two months, and by 8.2% year-over-year. What held down overall CPI was the plunge in gasoline prices and the drop in used vehicle prices.

The Social Security COLA for 2023 was also determined with today’s inflation data. It is based on the average of the year-over-year increases in the Consumer Price Index for All Urban Wage Earners and Clerical Workers (CPI-W) in July, August, and September. For 2023, the COLA will be 8.7%, the highest since 1981, but in 2021 and 2022, the COLAs got crushed by raging inflation.

Services Inflation spiked for the 13th month.

The CPI for services spiked by 0.7% in September from August, a sharp acceleration from the prior two months; and by 7.4% year-over-year, the worst increase since August 1982. This is where nearly two-thirds of the money goes that consumer spend, and consumers are getting whacked.

I split services into two groups: categories where prices rose year-over-year and categories where prices fell year-over-year.

Service categories where CPI rose year-to-year.

In some categories, the CPI declined on a month-to-month basis but was still up year-over-year. Note the massive month-to-month increases in insurance, medical services, motor vehicle maintenance, and delivery services. More on the housing CPIs Rent and Owner’s Equivalent of rent in a moment:

| Services, where prices rose YoY | MoM | YoY |

| Health insurance | 2.1% | 28.2% |

| Rent of primary residence | 0.8% | 7.2% |

| Owner’s equivalent of rent | 0.8% | 6.7% |

| Motor vehicle insurance | 1.6% | 10.3% |

| Motor vehicle maintenance & repair | 1.9% | 11.1% |

| Medical care services | 1.0% | 6.5% |

| Delivery services | 2.9% | 16.4% |

| Pet services, including veterinary | 1.6% | 11.0% |

| Airline fares | 0.8% | 42.9% |

| Hotels & motels | -1.2% | 3.1% |

| Other personal services, such as dry-cleaning, haircuts, legal services | 0.3% | 5.9% |

| Admission to movies, theaters, concerts | -1.3% | 0.4% |

| Video and audio services, cable | -0.4% | 2.5% |

| Water, sewer, trash collection services | 0.7% | 4.9% |

Service categories where CPI fell year-over-year:

| Services where prices fell YoY | MoM | YoY |

| Telephone services | 0.0% | -0.3% |

| Car and truck rental | 2.5% | -1.4% |

| Admission to sporting events | -2.9% | -9.5% |

“Core” CPI.

“Core” CPI, which excludes the volatile commodities-dependent food and energy components, jumped by 0.6% in September from August, after having jumped by 0.6% in August, which had been a sharp acceleration from prior months. Year-over-year, core CPI jumped by 6.6%, the worst since August 1982.

Core CPI tracks inflation in the broader economy, beyond the commodities-based components food and energy, and it has been giving the fed the willies:

Food inflation still horrible.

The CPI for “food at home” – food bought in stores and at markets – spiked by 0.7% in September from August, same as in the prior month. Notably, some relief was to be had at the beef counter. Year-over-year, the CPI for food at home jumped by 13.0%, a tad less terrible than the 13.5% in August, which had been the worst since February 1979:

Food inflation is particularly insidious because it hits lower-income consumers the most because they spend a bigger part of their budget on food. A 13% spike in food prices wreak havoc on their efforts to put food on the table. And it’s not like they can downshift easily from expensive brands to lower priced foods, store brands, etc. because they’re already buying the lowest-priced foods they can find. The Fed is keenly aware of this and has pointed it out many times:

Beef prices started to drop a few months ago and are now down year-over-year, after the huge spike last year. But prices of pork and poultry spiked, as many consumers have shifted to them, from beef:

| Food inflation | MoM | YoY |

| Cereals and cereal products | 0.9% | 16.2% |

| Beef and veal | -0.1% | -1.1% |

| Pork | 1.8% | 6.7% |

| Poultry | 0.6% | 17.2% |

| Fish and seafood | 0.5% | 8.0% |

| Eggs | -3.5% | 30.5% |

| Dairy and related products | 0.3% | 15.9% |

| Fresh fruits | 0.7% | 8.2% |

| Fresh vegetables | 2.4% | 9.2% |

| Juices and nonalcoholic drinks | 1.2% | 12.7% |

| Coffee | 0.1% | 15.7% |

| Fats and oils | 1.9% | 21.5% |

| Baby food | 1.5% | 11.8% |

| Alcoholic beverages at home | -0.4% | 2.9% |

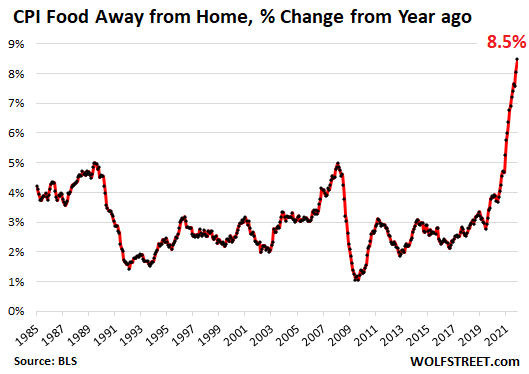

“Food away from home” CPI – at restaurants, vending machines, cafeterias, sandwich shops, etc. – jumped by 0.9% in September from August, and by 8.5% year-over-year, the worst since September 1981.

Food at employee sites and schools spiked by 44.9% in September from August and by 91.4% year-over-year, having nearly doubled!

Gasoline price plunge drives down energy inflation.

The Energy CPI dropped by 2.1% in September from August, on plunging gasoline prices. But natural gas prices spiked, and electricity prices rose.

| Energy | MoM | YoY |

| Overall Energy CPI | -2.1% | 19.8% |

| Gasoline | -4.9% | 18.2% |

| Utility natural gas to home | 2.9% | 33.1% |

| Electricity service | 0.4% | 15.5% |

| Heating oil, propane, kerosene, firewood | -2.8% | 39.9% |

Housing costs surge.

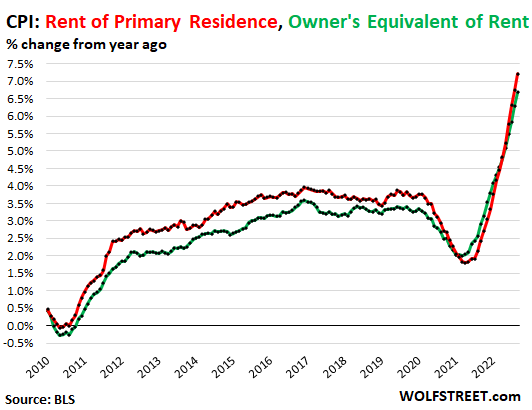

The CPI for “rent of shelter,” which accounts for 32.1% of total CPI, attempts to track housing costs as a service, not as an investment asset to be bought and sold. Its major components:

“Rent of primary residence” (accounts for 7.3% of total CPI) jumped by 0.8% in September from August, and by 7.2% year-over-year (red in the chart below). It tracks actual rents paid by a large panel of tenants, including in rent-controlled apartments.

“Owner’s equivalent rent of residences” (accounts for 23.8% of total CPI) jumped by 0.8% for the month and by 6.7% year-over-year (green line). It tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for.

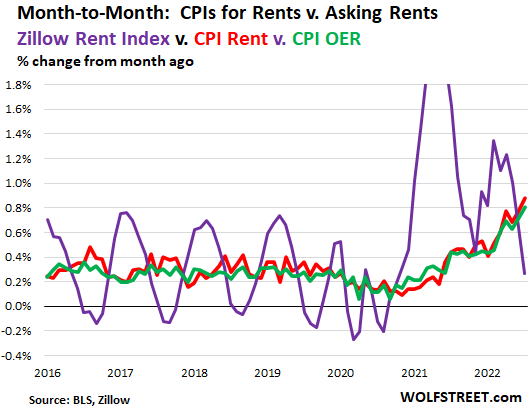

The “Zillow Observed Rent Index” (ZORI) tracks “asking rents”: advertised rents of apartments and houses listed for rent. Asking rents can jump when landlords feel confident, and if landlords cannot rent out their units, they will cut their asking rents. There has been a lot of volatility in asking rents as landlords tried to arbitrage the pandemic shifts, but not many people actually signed new leases at those asking rents because over a 12-month period, most tenants stay put.

In September, the ZORI rose by 0.3% from August to a record $2,084 per month. That increase of 0.3% was smaller than the increases in prior month. Year-over-year the index was up 10.8% from a year ago – which is still a huge increase.

But caution about the month-to-month changes: they’re very seasonal. Before the pandemic, the ZORI’s month-to-month changes turned negative every year in the fall. Every September, the month-to-month change in the ZORI was either 0% or -0.1%. The biggest negative readings occurred in November and December. By January, the month-to-month ZORI rose again.

This chart shows the month-to-month changes of ZORI asking rents (purple line), some of which will feed with a delay into “rents” that tenants actually pay and report (red line) and into “owner’s equivalent rent” as estimated by homeowners (green). I discussed this lag between asking rents and actual rents, and what it means for CPI in 2023, here.

The month-to-month increases of the CPI for rent and OER have been accelerating, as some of the asking rent increases have turned into actual rent increases for tenants.

With the ZORI, what we’re seeing is in part the seasonality. But September’s 0.3% increase contrasts with the normal 0% or -0.1% change in September. In other words, asking rents are still increasing substantially faster than they did before the pandemic. And come January, the month-to-month ZORI is going to bounce again:

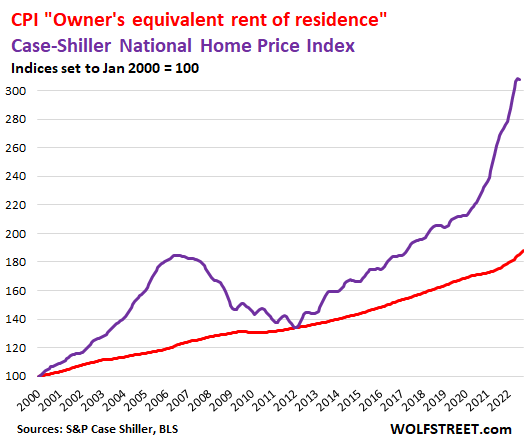

Home prices fell month-to-month for the first time in years, according to the most recent Case-Shiller Home Price Index. This reduced the year-over-year gain to 15.8% year-over-year (purple line below). The Case-Shiller index lags reality on the ground by several months, but already the steepest declines since Housing Bust 1 are cropping up in some markets, as depicted in The Most Splendid Housing Bubbles in America:

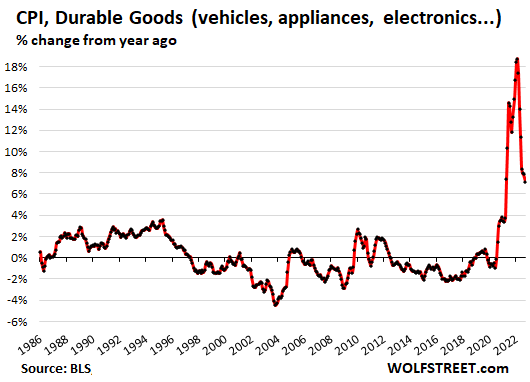

Durable goods CPI.

The CPI for durable goods finally dipped 0.1% in September. Sharp declines from the mega-spike last year have long been predicted, and we’ve seen some of that in used vehicles but not in new vehicles, the largest component in durable goods, where prices just kept surging.

For the actual dollar increases of the best-selling pickup truck and the best-selling car, have a look at the 32-year WOLF STREET Real-World New-Vehicle Price Index, F-150 XLT & Camry LE, 2023 Models, which shows a Ford truck price shocker (up 21% in two years), while Toyota barely raised the price of the Camry.

Durable goods include motor vehicles, appliances, furniture, sporting goods, consumer electronics, etc.

Consumer electronics – laptops, monitors, smartphones, WiFi systems, printers, smart speakers, etc. – almost always have a large negative CPI. This makes sense as manufacturing constantly gets more efficient, which pushes down the prices of the products. And importantly, CPI attempts to track the price changes of the same product, and if the product improved a lot, it’s no longer the same product. Consumer electronics have improved at a rapid pace, and the costs of those improvements are removed from CPI as part of the “hedonic quality adjustments.” Manufacturing efficiencies plus improvements of the products combine into a natural and sound form of “deflation” in consumer electronics.

| Durable goods | MoM | YoY |

| New vehicles | 0.7% | 9.4% |

| Used vehicles | -1.1% | 7.2% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.6% | 9.9% |

| Sporting goods (bicycles, equipment, etc.) | 3.0% | -1.1% |

| Information technology (computers, smartphones, etc.) | -0.6% | -10.0% |

Year-over-year, the CPI for durable goods increased by 7.4%, down from the 18% range last year and early this year, but still a huge increase.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Man, what a clown-show the stock market was this afternoon! Hilarious!!!!

Short squeeze. They can be dramatic.

Persistent high inflation means only one thing. Our politicians in both parties are incompetent and Powell can play both of them like a fiddle!

From Fed:

– Inflation is transitory!

– Our 4% rate will control an 8% Inflation!

– Our tiny QT will make housing affordable again and control inflation.

Are you saying the Inflation Reduction Act didn’t work?

Maybe if it was even bigger, that would do the trick?

Off topic somewhat, but something about today’s market action smells funny.

Don’t I remember some analysis of the latest Fed minutes stating that IF there were some extreme destabilizing market conditions of an unprecedented nature, THEN they would take steps to announce and implement a fed funds pivot? I seem to recall pondering that improbable exception to the strong anti-inflation policy commitment.

As evidence, I offer Wolf’s recent thoughts on the matter:

“But hedge fund gurus and bond kings and stock-fund apostles and other crybabies on Wall Street who don’t give a hoot about this raging consumer-price inflation because they’re rich and don’t mind having to pay a little extra for some stuff, but who’re losing their shirts because asset prices are skidding lower, and they do mind that, well, they’re on TV and on the internet and on Bloomberg and the Wall Street Journal bemoaning the consequences of the end of free money.”

Fast forward to today’s post inflation report market action… Who can move the markets 1300 points in unexpected gyrations? It’s the aforementioned hedge funds, and so forth. The average retail investor like you and me, are ants among the elephants.

It appears that someone or some organization was amplifying the swings in the averages in a shock campaign to convince the Federal Reserve to pivot back to the previous low interest jackpot.

Call me nutty. The inflation data was only incrementally awry. Not worth a 1300 point swing in the Dow. That was a convenient data point to exploit by the elephants, or “stock bakers”. Confined to orchestrating 30 stocks out of thousands. Courtesy of the Plunge Promotion Team.

If true, this goes beyond capitalism to brazen greed, and as we see in the world today, these no limits sociopaths have lost all fear of accountability and sense of shame.

Back-on-topic summary:

The service sector “bread” of inflation is rising rapidly from the oven of the stock bakers.

OTOH, cheap shoes and excess inventories of product are everywhere.

Above board – funny name for someone whose comments are below board:

“It appears that someone or some organization was amplifying the swings in the averages in a shock campaign to convince the Federal Reserve to pivot back to the previous low interest jackpot.” And,”If true, this goes beyond capitalism to brazen greed, and as we see in the world today, these no limits sociopaths have lost all fear of accountability and sense of shame.”

It would be nice to keep unfounded speculation and “BS Inflation” to a minimum on Wolf St.

When stock market is controlled by top 10% ,of course we peon,s are not in the gams = casino

This was likely the bottom for what will amount to (if the top is in) a large multi-month corrective bounce or (if the top is not in) new all time highs.

The market doesn’t work on fundamentals, at least you cannot predict or explain the market based on fundamentals because they are a lagging indicator.

The market doesn’t make rational decisions. Its emotional. People subconsciously begin feeling ready to stop feeling scared, ready to move on, whatever you want to call it. They become ready to take some risks again. One of the simplest ways to express this is to press the buy button.

There are obviously no guarantees and the market can do whatever it wants, but there is now a high probability we have a lot higher to go than lower, at least over the next few months.

For the first time in 15 years the market will need to compete with interest rates significantly above zero and moving higher. Rates that will correspondingly be a drag on earnings. It’ll be interesting to watch what happens as investors assess their options in a very different investing environment.

Rich are selling stocks ,buying treasuries or corporate bonds ,there’s a reason there RICH. Will us peons watch 401 k get decimated

“For the first time in 15 years the market will need to compete with interest rates significantly above zero”

This.

Essentially 20 yrs of ZIRP correlated basically all asset classes to the G’s rat-trap, money-printing, paint-huffing “Metaverse”

1) US Fed buys US Treasuries to abort natural increase in interest rates due to US G’s ever deepening debt,

2) US Fed does this using “money” backed by little more than “wisdom” and “integrity” of DC governing class,

3) US real productivity lags far, far, far behind rate of money printing in step 2.

4) Inflation.

But now that the resultant inflation is too gross to hide behind even China’s world-historic surge in product supplies, the Fed is forced to allow a tiny sliver of economic reality to be re-introduced to crack-addicted asset mkts.

Result – Chaos.

Interest rates have a huge physiological effect on behavior.

People are much more likely to spend money, especially on a big ticket item like a vehicle, if they cannot safely invest it at a reasonable return. Especially if they are able to get near 0% interest rates on a purchase as has been the case the past few years.

That all changes when interest rates reach current levels.

Example, someone who was contemplating buying a $60K RV can now invest that $60K and earn 3K a year to spend on vacations. That pays for a pretty nice vacation rental or hotel and some nice restaurant tabs, and you get to keep the $60K.

Bahahahahaha!!!!! A “bottom?”

The inflation data was not good today. The FED will stay the coarse with rate hikes. I’m thinking markets will be down tomorrow.

Look at the ramp in banks. Who reports tomorrow? Yeah, this was a scam rally to unload to the suckers. Love reading the bottom is in from the skulls full of mush, they never talk fundamentals because theyre horrible so they have to resort to sentiment, the pivot, years ending with 2 see a big rally in the fall, etc., etc. Waiting for them to cite planetary alignments and animal entrails as indicators the market is turning around

Yup, markets turned out about as I expected.

Yup. You sure did. Good call.

Back up today… let’s see how the other banks are fairing beyond BoA.

LOL. Do you realize how many zombie companies are out there that can’t rollover their debt and survive at 4-4.5% higher rates? Do you realize how much of the “profits” of even the good companies is dependent on the credit bubble and lending to poor quality consumers? The bottom, being S&P 3,500, was not “cheap” even based on the current earnings numbers. If those earnings drop, as I suspect they will, look our below.

Anybody know of a free access site tracking BB/CCC rated companies, along with their financial metrics?

It would useful to know which companies are going be pitched off the gang-plank first.

Disney,Tesla anything in aark .Very few sound companies but hell we just left the roaring 20s It’s a huge cliff

“The market doesn’t make rational decisions.”

Wrong. Outside of day-by-day spasms like today’s bath-salts mania, markets are very efficient. Those who do not abide reality get killed by it.

“Irrational” is more appropriate.

Lol! The market makes rational decisions outside of the times that it doesn’t?

The market being “efficient and rational” is totally subjective and just an easy way to reinforce your own biases. It’s rational when it moves in the direction you think it should, but irrational when it goes against it?

Was it rational that the market melted up over 100% during the middle of the worst economic shutdown in at least 100 years?

The creator of the EMH has even abandoned it.

Well yes, where else would $trillions on stealth bailouts, PPP, dark money go?

Dow 40K this December!!!

A David Hunter acolyte!

As I said in my post, this has nothing to do with fundamentals. You guys keep quoting fundamentals as if the market will follow them when it defies fundamentals ALL THE TIME. Like, hmm… TODAY!

Remember the Covid crash? We bottomed before any major shutdown. ALL the worst economic news was coming out as the market just looked the other way. At the time we bottomed everyone was calling for the market to go to 1500 or 1000. We bottomed within 7 points of the target that we had on our charts. One of the HARDEST things to do is to make objective decisions when the objective indicators and methods tell you a bottom is being struck but all the emotions are telling you that you’re crazy.

I’m not saying with certainty that this is certainly the bottom for the next few months, but the market never offers certainty. I’m telling you in probabilistic terms that we just entered a major support level at 3500-3550, with numerous indicators screaming that we are setup for a major rally.

This morning we were buying at the lows, with stops set in case we were wrong, and are now in excellent position to profit off a rally if it comes. If it doesn’t, our stops will be hit and we are will make a small profit. It was hard to do for all the reasons everyone mentions above. But that’s why we have objective rules that remove emotion.

IF we get a big rally from here, I hope some of you will realize that the market is controlled by sentiment and will not shrug it off as the market being manipulated or controlled by some omnipotent force. I sincerely hope you open your mind to look for ways to understand how to profit from that.

I’m not a perma bull nor a perma bear. I try to be perma profit, and I’m trying to help others see that as well.

Ok, Mr Perma-profit, thanks for the help. Post your trades in real time and come back often. A blind could see this bounce coming, especially comment on it post facto. This may continue for a while. Or not.

Winter Is Coming, and the humongous wall of money that protected the SPX 3500 border today won’t be enough to stop it.

The only way for the Fed to control inflation and make sure the dollar does not collapse, is to take back all the money it has given out, wag its finger at the markets and let it collapse……

The S&P 500 is about 8% the all time high set in February 2020 and right before the COVID pandemic.

Accounting for inflation which was about 16% from February 2020 to present day, the S&P 500 has a negative return since February 2020.

So the Fed already has erased all the COVID gains from the stock market. But markets over correct just like they over run, so 3500 may not be the bottom.

There may be downside support or enough risk for the S&P 500 to be 3000 if there is enough panic like there was in 2008.

At 3000, it would be +10% below the all time high set in February 2020. That would be enough of a bloodshed level for the Warren Buffet’s and whale value investors to drive up volume.

HIT: Benjamin Graham: “In the short run, the market is a voting machine; in the long run, it’s a weighing machine.”

We bottomed in March of 2020 simply because the Fed announced it would print trillions of dollars and Congress announced it would borrow and hand out trillions.

It wasn’t so much that the market was increasing in value, more that the dollar was decreasing in value and the large institutions got the assets first, through the Cantillon Effect.

Sentiment alone wouldn’t have been enough. It required massive printing which can not be repeated without destroying the currency.

AD,

The stock market was also in a mania at the February 19, 2020 pre-pandemic peak.

To the other post, there is no major support at S&P 3500+. That’s the recent June and September lows. It’s barely any support at all.

Look at a chart. There is no major support until the March 23, 2020 low at S&P 2300.

I believe about 20% of the funds invested in the market are held in 401K’s by people who really do not understand the first thing about investing or how markets, or business cycles work.

About all they do know is they are happy when they look at their statement and they have made money, and they are upset when they lose money.

Having watched this play out a few times, I have noticed that despite often regurgitating what they have been told about investing long term, they have a fairly low threshold for losses. Most by their third negative quarterly statement become frustrated and decide to stop the bleeding by moving at least some of their money out of the market. Especially if they have an alternative that is paying interest. This is usually when the real capitulation begins.

If the final top is not in, the subsequent crash will be even bigger.

Absolutley. The downturn that is coming will not just be a crash, it’ll be a prolonged bear market that lasts at least a decade if not two. We may have begun this already, and if so we will still bounce here, but it’ll be a choppy whipsaw bounce that will still be a few months long, but will eventually “crash” down to the mid to low 2000s. Even in bear markets sentiment is still in control of things.

People above seem to think I’m saying the market is now going to the moon. I’m simply saying we are likely at a bottoming region for a strong multi-month bounce. If the low is not in, it will not be much lower than where we bottomed yesterday.

So there might be another 100 points down, but probably 600 points up (or much more) over the next several months. Not forever!

Fundamentals always return to the markets even if emotional and psychological gyrations push it in one direction or another, it’s just a matter of how painful and extreme the correction is when reality hits. Granted, the Fed is able to distort markets like at no other time in history with QE and ZIRP, which is what’s happened more or less over last 40 years, but now the Fed is trapped by inflation which is by far the greatest threat to the US economy, the US dollar and the United States as a viable nation itself–inflation’s brought down more great powers than any way ever has–so the Fed has to stay aggressive now just as Paul Volcker did. So the Wall St. toddlers and crybabies won’t have Daddy Fed to bail them out anymore. The rising interest rates and withdrawal of liquidity with QT will take out hundreds of companies that are overleveraged, this alone is going to bring the markets way down. And consumers have far less to spend as they’re tapped out by inflation costs. It’s delusional to think otherwise.

I smell a trapped long high on hopium.

Lol, there is no logic behind market moves now, shows how much liquidity is out there.

Jeremy may be right: bunch of banks and funds joined hands to squeeze short sellers like Andy and Kunal :)

There is always logic in the markets.

Money was parked, waiting for the monthly CPI data release date (and recent downwind) to pass. The event itself, not just its output, guides market behaviour too.

The stock market wants to go on a run up again, subject to, as always, sudden events. It most likely will for a few weeks, even though it might be choppy for a while.

It’s neither a short squeeze nor a bull market.

Still a whole lot of Chips in the casino.

Must be that “tightening” thang.

It’s Trap.

Yancey, I’ve noticed that his “clown show” keeps repeating over and over on the market.

Here’s what I think is happening:

Some smart traders realize that after the stock market goes low, some mysterious force always seems to drive it rapidly up again for a short time. Is it Wall Street or the Fed trying to convince naive traders that a bottom has been reached? Or fools that no matter what, buy the dip? Then there are smart buyers who buy the dip–knowing that it will shortly jump up, then sell before it jumps down again. Maybe make 0.25- 0.5% on your money in a day, each time you do this. If you do it right, it would seem to be a really quick way to make a lot.

In order to understand whats happening you have to look at it on a much longer timeline.

The WW2 generation accumulated the greatest amount of “real wealth” in history. This money was primarily in real estate at reasonable valuations, and in cash.

The WW2 generation was very economically conservative, having been raised during the great depression, they lived well within their means and saved a decent percentage of their income in cash.

Their wealth was inherited by the Boomers who were not nearly as conservative as their parents and were eager to ratchet up their lifestyles using their inherited wealth.

Concurrent with the Boomers windfall wealth inheritance, came a new era of inflation, credit purchasing, and highly inflated asset valuations. Boomers were eager to make easy money in the booming stock and real estate markets that ensued. They used leverage to maximize their living standards and paper profits taking on massive amounts of debt.

Today, Boomer and Millennial wealth is dependent almost entirely on inflated asset values. Their wealth is measured in the difference between perceived value of their assets, and the debt they owe on those assets.

All that remains to do now, is to collapse the value of those assets by deflation, and the money changers will have stripped all the wealth earned by both the WW2 and the Boomers in one move…… They will own nothing, and they will not be happy….

Distribution phase on the weeklies has started.

No worries… social security to go up 8.7%

I just renewed my home and auto insurance policies. Up 25% from last year. No claims in decades and I shopped this insurance with several brokers. I even had to raise deductibles to get to only a 25% premium increase. This is Texas, not Florida or California.

Mine went up (auto) by more than 10%. I didn’t even bother calling around. The annoyance factor outweighed any potential savings which I anticipate wouldn’t even have materialized.

Mine wanted to raise mine by 35%. I ended up going to another for 10% less than I was paying before. Try it.

Who did you go with?

The current interest rates are not going to tame inflation much. We need a recession. You want house prices to drop? Then we need excess houses on the market. We need foreclosures….etc. I am still getting 3 or 4 people/companies a week still asking to buy my rental homes for cash.

Mid 6% mortgage rates are actually a good deal historically. It may take awhile but people will get used to the new normal mortgage rates. What they do not realize is rates can go even higher. Low or below 6% mortgages may not happen again for awhile. 1 year….5 years….maybe 10 years. My guess is we see 7% to 8% for the next few years unless the FED is very good at hammering at this liquidity bubble.

I know of a small company in Europe whose energy bill has gone from 500k a year to 1.5 million. This is a company that does 20 to 30 million in revenue a year. It will probably go over 2 million after this winter.

Grab the popcorn. This is going to be interesting. I remember my dad telling me that he bought a house in 1969 for $21k. He sold it in 1984 for $84k. That is a 300% rise in 15 years. This was in flyover land.

There is no guarantee housing is in a bubble if inflation is not tamed. My current house in the same state as my fathers took 22 years to double in price. Guess what, that is what it takes to double your money at 3% compounding interest rates. If inflation stays at 7% or 8% per year, my house price should double again within 10 years this time instead of taking 22 years.

FYI. It takes 9 years to double your money at an annual 8% interest rate.

Replying to Ru82..

Home prices have no where to go but down unless fed pivots.

I know people who owns rentals have difficulty seeing this.

With inflation running so high i can’t see any reason for fed to pivot.

Same for stocks as well

We may have bear market rally from time to time but the general direction is down only.

No, people aren’t going to get used to higher rates because affordability has nothing to do with that.

The slack isn’t going to be taken up by renter landlords either because they won’t be able to charge high enough rents to make up the difference indefinitely.

Replying to Ru82 below (?). This is just what I hear from others: in most western states urban areas the prices are just way out of wack with locals earning power. Many cite Moodys Analytics evaluations. Boise, Austin, Phoenix, Las Vegas, Seattle. San Jose, etc. Moodys predicting 10 to as much as 30% declines depending on location, recession (or not), etc.

Investors bought a huge amount of the housing stock in Southeastern state metro areas (Atlanta 33% in 2021, Charlotte, Jacksonville). More recently I saw a stat indicating investors bought just over 50% of homes in Tarrant County (Fort Worth), 42% in Dallas County… over the last year… I believe that was the timeframe.

Will they hold in to these rental homes

or not ?

Some question the ethics of this, I certainly do…. considering 35% of Americans do not own one home.

Mortgage rate 6% historically not bad.

Counter: mortgages now 60 to 70% higher for same priced home just 7 months ago. Many point this out, almost ad nauseum.

Home prices have only dropped significantly twice: 2008-2012, GD.

Not true. Other times, specific regions have had significant drops not reflected in nationwide stats. E.g., Texas in mid to late 80s: 20 to 30% drops. I owned a home there then, saw 25% drop over 3 years.

According to Reventure Consulting apartments are being built at the fastest clip since the 1970s. I hope they are accurate with that assertion.

He displayed a chart supporting it.

Less pressure on rents, less demand for SFHs.

I dont have much faith in our government… booms and busts benefit some but creates too much anxiety and distracts from more productive societal activities (scientific, engineering endevours).

Concernedguy, Progressive.

@Randy – Greate comments. Real Estate is certainly regional. There are certainly overheated areas that you mentioned and are out of whack.

IMHO Mortgages rates seem high, but historically they are not. The only lender in town the past 12 years has been the GSEs. If the FED is not going to buy MBS anymore….than get used to 6% or higher interest rates because no bank is going to want to lend at 3% to 5%. They did not the past 12 years so don’t expect them in the future. It is weird how people think mortgages will drop again. What is their target? If the FED starts buying mortgages again, then I will say sure, we will see lower mortgage rates again. But from what I can see…ZIRP has turned out to be a bad experiment….so will they try that again?

Apartments are being built all over my area. Why….people cannot afford a new home. Builders are only making 12% profit in my area, so they are not jacking up the prices. The builders cannot reduce the cost of a new home unless the input prices go down. What is the end solution? I guess they can build smaller homes.

@Jon – part of my point was to talk about inflation and its effect. Home prices “can” go up if inflation goes up. I think many people are discounting the inflation effect on asset prices. If inflation does not come down, neither will home prices (or not as much as people think) on the average. Look at Argentina. Home price are up 30% this year and are not dropping. Why? Inflation is 50%. Over the past 5 years in Argentina, housing is up 200%. Remember….inflation, interest rates, and housing all went up in the 1970s. I think Bank of America, or some other big bank just said they expect inflation to be at 5% for the next several years. Will they be correct? Who knows.

Let’s say it costs a builder $400k to build a home. At 5% inflation per year. In 5 years, the same home will cost $510k to build. It does not matter if there is easy money or tight money. It will still cost a builder $510k to build a house. Their profit margin can go up and down depending on easy money.

I was ready to sell my rental houses after the crazy run up in prices the past 3 years. I put that on hold and I am totally rethinking it if the FED cannot control inflation. If the 5% prediction BAC is spouting comes true, my rental houses will go up 30% during that time.

When the government says they have an inflation fighting bill that costs over 1 trillion. We are all being fooled that inflation is under control.

My whole mindset may change if the FED can actually control inflation. But I am not going to fight the trend.

There is a trivially easy way to fix the housing availability/affordability problem. Remove the dozens of laws added in the last 80 years that made homes attractive as investment assets. Before that, homes were seen as investment liabilities. If you do this, the Rumpelstiltskins out there will stop hoarding vacant homes, and also all those short term rentals like airbnb will return to the housing market.

Home prices in USA is tightly coupled with mortgage rates.

If inflation is not controlled, then FED has to hike much more aggressively, the rates go up, home prices go down.

People say real estate is all local, but this time cheap money was available globally and almost appreciation in most part of the world. You name a city and real estate price have gone up exponentially.

I see it opposite: More inflation means higher rates and thus less money for home//mortgage/rents etc thus lower home prices.

Texas has very expensive insurance. Check other states and you will find them much cheaper. A $500,000 house in San Antonio costs $5244 annually for house insurance. A $500,000 house in Quincy, Massachusetts costs $1704 annually for house insurance.

Then you look at the property taxes on those two houses: $5136 for the Massachusetts house $9684 for the Texas house. Texas has become a very expensive place to live with a very low quality of life. You tell me who’s to blame for this.

Must look at total taxation by each state, not just property taxes. Sales and income tax rates also vary widely.

Also a “$500,000 house” is not the same in different states. Age and construction quality vary, as do local claim rates for various hazards, and cost-of-repair for those claims.

Wikipedia has an excellent summary of each state’s taxation. Includes a graph which displays on a horizontal segment how much is income tax, properly tax, sales tax, and one or two others.

Worth a gander.

Wow,

I didn’t know you Americans paid so much for basic utilities (depending where you live), it just shows you how different countries have different costs.

Being in the UK, my health insurance is zero (like most of Europe) but house insurance is about £400 for a smallish £500,000 house, property tax starts at £1250 nationwide and goes to about a max of £3800 for those houses that cost a fortune (yes even if it is worth £50 million.) Oh and the pound and the dollar are not that far apart now.

At the moment my heating and electric bill is high,(because of those crazy Germans, in panic mode, outbiding everyone) it is approx £110 a month, so that compensates for cheaper insurance. Gasoline prices are much higher but as I always say, England is tiny, so we do far fewer miles than most Americans to do the same things.

I am exceptional here, borderline thrifty foolish. We have perhaps the cheapest electric rates in the country in Eastern Washington state (hydro a big help ?).

Average high, low January 34/21.

July, August now up to about 87/58.

(Last 5 years definitely hotter, surprisingly so… and now the smoke but I digress).

But I average $40/month. Not kidding.

About $0.08/kwh + $9 basic fee.

I do get a bit chilly in winter.

Wish I could say I love living here but that would not be true.

We have a lot of natural disasters in the U.S. Tornados, Hail Storms, Ice Storms, flooding, earthquakes, and worst of all Hurricanes. You need a lot of insurance for these events.

I have had my roof replaced twice in 20 years because of hail storms. 2008 it was $14k. In 2021 it cost $22k. That is $36k the insurance has had to pay out in 20 years. I think I have paid about $40k in premiums over this time so they have made some profit.

Our property insurance is $1,141 per year for dwelling coverage of $650K (not value, but structure replacement cost). That includes another $125K in “excess dwelling” coverage and $50K for code upgrades (this pile of bricks was built in 1980 with 3 subsequent remodels) and a whole bundle of money for contents – and some riders (supply line coverage, major systems coverage) and $300K in liability (we have an umbrella for additional liability coverage here in the land of undocumented workers).

I guess that’s the benefit of not having tornadoes, hurricanes, earthquakes, and the like.

“Texas has become a very expensive place to live with a very low quality of life.”

What about all the free pork? Love watching all those feral pig hunting/trapping videos on YouTube. Seems like a meat lover’s paradise.

Germany is now introducing “real-estate tax laws,” depending on the state, between now and 2025 which looks to incentivize big Karl-Marx type high-rise apartment building owners with tax savings, and dis-incentivize individual family howeowners (with property tax sticker shock).

Though its true that presently many Germans live in apartments, with the “property tax reform,” it still looks to me like part of the UN Agenda 2030 — own nuthin and be happy, ‘Besitz nichts und sei froh’ pogrom.

I see lots of parallels with US and Germany, like the government pressure to influence people buy EVs, esp. with current administration in trying to turn USA into a social welfare nanny State. Bring some popcorn and stand by for more fun …. resist where you can.

Ours in FL, the highest cost auto insurance in USA according to AAA, went up just a couple % this year, and was level after I got the phone rep to reduce the mileage on my two vehicles to 1,000 miles per year total.

Self insured otherwise on the ”tearer downer” ( next step below fixer upper.

At this point the z site says the dirt is worth 3 times what we paid for the whole package 7 years ago, and I am TOTALLY ready to get out of the heat and humidity and humanity and back into flyoverstan and the woods ASAP, where the whole package is less than half the dirt here.

Yeah have seen this too, Texas is not in any way a low-cost or low-tax state, that’s been one of the great myths peddled by some of the businesses there. And insurance and property taxes there are some of the worst in the country, healthcare costs are through the roof.

Depends. For high income people, the income tax savings of a state with no income tax outweighs any extra they have to pay in sales or property taxes.

Texas also has very high electricity rates.

I pay $0.12/ kwh and I am in Houston, Texas. Try Ca, Az, Ct, Hi, and others for comparison.

My last bill this summer (August) was $92 for a 2,000 sq. ft. home and it’s not shaded. Plus, we are running an oxygen concentrator 100% of the time (13 W).

And constantly running two full size refrigerators.

Texas is highest in auto insurance and property taxes. I have researched extensively in comparison Texas is brutal when it comes to property taxes which is why Elon Musk does not have a big home in Texas.

Elon is here for the BBQ, case closed.

You need to broadcast these FACTS more so the California crowd will stay in their low cost state or just move to Washington state. LOL

Excellent article, thanks. I’ve already seen people saying inflation has peaked after this CPI report. Perhaps it has, but it’s not going anywhere fast. You’ve nailed the dynamics of the inflation problem for a long time, including your prescient podcast last Sunday on the breakdown of price stability.

They’ve been saying “inflation has peaked” since before the FED even started raising. 7 months later, it’s “still peaking.” It’s like a never ending acid trip, I guess.

It is rather surreal. Wolf provides a corresponding dose of reality.

Well, a guess: CPI, Consumer Price Index, do peak when it catch up with (monetary) inflation.

Now, what do the chart of monertary expansion then tell us?

Inflation, once reaching feedback level, cannot peak until recession forces it to peak. Because so much of the economy is predicated on “future” purchases, once inflation gets to a certain point it has to be figured into business costs far in advance. Any company which is taking orders which are say a year out, must assume the inflation rate at current levels to minimize loses. This turns inflation into a perpetual motion machine which creates itself. The only thing that can stop it at that point is severe demand destruction.

All is good, Biden insists inflation ‘averaged 2%’ — even after data shows 8.2% annual jump.

Presidents live in perception-distortion fields which allow their local reality to be whatever they (or their handlers) wish, regardless of the world the rest of us live in.

It’d be hilarious if it weren’t so tragic!

To be fair, inflation was less than 1% between Monday and Friday.

I retired early 12 years ago (now 60) after investing in an off-grid home surrounded by national forest, using solar for power, local well (also on a river), with propane for winter heating (also have wood stove, but I’m lazy-ish). No debt, minimal expenses (LPG & taxes). Also moved my elderly mother in with me a few years ago when she needed more assistance to help her get the most out of her “golden” years. Thought I was insulated from most of the circus going on in the wider world (political, financial, and social arenas)…

Then I went in to my local hardware store yesterday to buy a couple extra bags of dog food as a precaution for the winter. Low and behold the price per bag went from $26 two weeks ago to $35 today. Thats a 35 percent increase in 2 weeks! Was told all feed supplies were jumping like that. Thankfully I’ve been expecting this for a while. All I can say it this is going to end badly for everyone. Such insanity.

And finally, thank you Wolf and all the great commenters. I have really benefited by the wisdom on this site. Cheers All!

Don’t forget that bag is 5-15 pounds lighter. All dog food in my area went from 50 pound bags to around 45 to 35 pounds bags and raised prices. Thankfully they kept the “bonus 5 extra pounds” on the bag. I feel so lucky they didn’t want to lazy and cheap to do a new graphic design.

I think millions of consumers have their personal hamster treadmills set on “fast” and are still strenuously job-hopping, demanding more pay, and blowing it away on ephemeral frivolities. I await their fatigue, a.k.a, the waning of the inflation regime. They may find the rug pulled quickly.

Some years ago I started, call it my own QT. I allowed some things to expire and did not renew them. They were consumer self-indulgences in my view, just fluff, just vanity, self-indulgent habits. Yes,I’m eccentric (poor people are “crazy”). I jettisoned:

Pets (looking at vets, etc.)

Drinks that are not water

Meat of large land animals

Name brand clothing

Long ago: alcohol, tobacco, etc.

A shrink

I did keep some things such as:

A pretty nice (if not new) car

A roomy and comfortable home in a walkable place

Good sturdy personal values

Sounds like a prescription we all could use. Or use CRSPR to edit the “status seeking” gene from our DNA.

We recently dumped cable internet. The criminals hit $90 a month “plus taxes and fees” for their mid-tier service. Replaced it with comparable 5G service for $40 a month – taxes and fees included with a rate lock for 2 years.

Going to dump the DVR next as we watch very few stations on our “free” cable provided via our HOA. That’s another $23 that will disappear. We tried streaming of two services (one’s $44 a year and the other is $7 a month) that have no commercials to replace the DVR as we can get the shows we want on demand.

The most significant utilities savings we have was from the installation of a solar hot water system (60 gallon tank, pumps and solar collector). Saved us about 40% on our electric consumption. We added a circulation pump on a WIFI switch to move the water through the house to avoid wasting water while waiting for the hot water to arrive. The 220 to the water tank is also on a timer as to not waste electricity on the heating element when it isn’t required (only runs in the evening when the sun goes down).

When I mentioned to my wife we should dump cable and not have the ability to record her 10+ favorite reality shows, and also not get the Astros games (without a subscription – she’s a big Astros fan), she asked me if I like sleeping on the couch with the dog.

I traipsed down this slippery road a few years ago when I subscribed to Netfix and Hulu and showed her how to use the three remotes, one for the cable/internet connection (Comcast), one for the TV to switch inputs (LG), and one for the Roku box to find Netflix and Hulu. She was less than impressed.

The $125.00/month I pay for Comcast cable/Internet is worth the price of admission to not sleep on the couch. LOL

If it was just me and the dog, it would be internet only. I can watch ball games at the local pub.

That and lot’s and lot’s more debt. The media keeps getting on this bandwagon about Americans job hopping like crazy and some of that is happening, but I’m very skeptical it’s anywhere as easy or straightforward like the media makes it, HR departments and contract clauses really don’t make it easy. Even in IT with our job openings and shortages, it’s just in practice very hard to move from one skilled job to another, and even in best case scenarios can often take 3-6 months to finalize. Non-competes are a huge headache and slow the process down, and health insurance for job switches is often a lot harder procure than first seems. There’s major age discrimination esp for SWE and IT, but even for young’uns right of college it’s not unusual to run into a wall of difficulty getting a new position, even if someone’s in that sweet spot of being a few years out of college with decent skills.

Those dumb bots and filters a lot of human resources depts. use, screen out a lot of good resumes and applications for the dumbest of reasons–I and a few other hiring managers a few years ago demanded that HR forward on all the resumes that the bots had screened out, and many of our best hires came from that pile! Then there’s also the specific challenges of moving for jobs that aren’t WFH. (And even telework can be tricky, it’s not guaranteed if you can stay that way–often things move to a one day a week or so in the office schedule–so even in IT, most still try to stay generally in the same area as HQ) There’s all the uncertainty about moving to a new job even with higher pay at first glance, and then on top, actual relocation is a huge cost in time and money, in a massive housing bubble (and many prior homeowners are now seeing massive decreases in their home re-sale value while buying into expensive markets). Job-hopping happens, but I doubt it happens all that often and I’m certainly skeptical of the way the media and squawkers make it seem like people can just hop several times every couple years for higher pay, that’s really difficult to do in the real world in practice.

Golly this is the answer folks. No wife and children either? Being a hermit is not a solution for most people. What is the point of this response? Do as I do?

He’s bragging.

All the “crazy people” in the world like you are a dying breed. That’s why the world is falling apart. The “sane” people now have an average 145% debt-to-income ratio.

That worked for us too WB, but only until I became too disabled to do the word NEEDED to maintain the 50+ acres, AND mom needed more or less full time care in her late 80s.

So be prepared for those eventualities that WILL happen no matter what.

I find these charts and tables somewhat depressing. :(

Cheer up, buddy. Ticket prices for sporting events went down. We can watch grown man chase ball for an hour for under $500 again.

I splurged at paid 450 bucks to see the 70’s rock band the Eagles earlier this year. I won’t be doing that again for a long time.

Anyone with their eyes open can see things are out of control. Wolf is one of the few guys out there talking about service inflation. From vet bills to insurance to pest control everything has gone up. I already started raising the rent for my tenants at 150 per month. I pay pest control for one tenant. She paid off my rental house and do it for her every other month. Used to be 50 bucks, went to 70 and today got the bill for 87 bucks.

I don’t see things getting better with the government recklessly printing money for their yearly budgets and debt hitting 31 trillion recently which the Republicans don’t even mention any longer. Things are not going to get better with this crappy leadership from both parties and poor fiscal control.

You can check out any time you want

But you can never leave.

The Eagles on “quiet quitting”

Well at least you picked a great band to splurge on!

The Eagles will be going extinct in the not too distant future.

JK, Congress hasn’t voted on an annual budget since 2012, let alone an actual balanced budget…yet the few that warned that this wanton spending spree with zero fiscal restraints by both parties in Congress over the last decade was a bad thing, were mostly ignored and kicked to the curb by the powers that be on both sides of the aisle in Washington, DC. Let the good times roll has been their MO.

CB: good points. a lot of folks don’t realize how ineffective Congress has become.

:) you wish, the shriveled stadium hotdogs are probably up to $20. I had to use quotes from A Bronx Tale to get my kid to understand the stupidity of glorifying professional athletes. Used to follow the Warriors but never cared for the Suns as much. Needless to say we don’t go to basketball games any more, nor pay exorbitant charges to watch it on the idiot box.

It amuses me to watch grown men yell and curse at a television set displaying people who can’t hear them over a game that was recorded while calling them “idiots” (while the “idiots” on TV are getting paid millions to play a sand lot game). I have never personally paid for a ticket to any sports game. Ever. Never will.

Last concert we went to was Paul Simon and Sting. The tickets were $300 each…. and not stage front and center either. Paul Simon just went through the motions and refused to return for an encore. His singing was flat and tortured. Sting carried the concert. That was the last concert (2010) other than subsequently supporting musicians at small, local venues for mebbe $50 a clip at MIM.

El Katz,

Those “grown men” screaming at a football game on TV?

They’re gambling addicts who have way too much riding on the outcome.

Few people are so infantile as to get emotionally distraught about the “home team”.

But a whole lot more are sufficiently infantile so as to become perpetual gambling addicts.

I grew up in Las Vegas – I spent those years witnessing the psychosis.

It really isn’t terribly different from the day trader mentality.

On the health insurance topic. Many companies subsidize this and contribute x amount per year that (as of a few years ago) covered most expenses.

A 30% increase in that context can look like a 10x increase or more. I just went from paying $50/mo to $550/mo for the same policy.

I’m as disgusted as ever by the FED and all the political cronies. They caused this. I have a hard time believing they didn’t see it coming. It smacks of intentional.

While everybody and their mother was watching inflation roar, Jay Powell was “not even thinking about thinking about raising rates.” Why wasn’t he FIRED? Now he’s in charge of fixing it? Yeah, I always have Jeffrey Dahmer head up the serial killer task force…

It seems to me this QT is way too little, too late. Why aren’t they speeding this up? A paltry $200 billion or whatever over 6 or 7 months when they were doing over $120 billion PER MONTH of QE? I’m sure we’re soon to hear “we should have implemented QT more quickly.” The FED is ALWAYS telling us, in hindsight, that they should have done this or that differently. Why are the same failures never fired?

Depth Charge, I’ve been thinking the same thing about the Fed and also wondering exactly why they did nothing all last year even though they surely saw it coming. What was in it for them?

I like your Jeffrey Dahmer analogy. It’s the best laugh I’ve had all week.

Powell is as good as it gets. There is no reason to believe any replacement would be any better. Bank heads tend to get more hawkish in their second terms anyway.

The Fed is at fault, but they’re not the only ones at fault. Tariffs on China and other countries, curtailment of fossil fuel exploitation, wild spending, and a pandemic that merited at least some of the draconian response all did their own damage and put central banks in a bad place.

If you want to chew out CBs, chew them out for their pre-pandemic easy money policies.

Good points.

But what of this: aside from external forces causing inflation … in a very small country such as Singapore or Iceland is it so naive to think the government and business leaders could enact a voluntary curb on price increases. Or monitor industries and fine or otherwise punish those companies raising prices more than their peers … with reasonable exceptions ?

Is this silly ? But not in a big country like the US with so much divisiveness ?

It’s because they are un-elected. Were they elected it would be much much worse. Just look at our representatives.

“Why are the same failures never fired?”

Because they’re doing an excellent job. And it’s their only job…..

To protect the rich.

I hear Bernanke is being considered for the Nobel Prize in Economics.

Depth Charge, will you write a recommendation for him?

What I find interesting is that vehicle rental CPI fell, while vehicle insurance rose 10%.

Maybe it’s because labor costs rose for the insurance co’s, but auto rental is also a labor-intensive business – lot of admin interactions with customers.

Auto ins has to cover replacement costs for damaged vehicles, but the auto / truck rental business also has to cover essentially the same behaviors and outcomes.

Why the big difference in annual CPI (-1.4% for vehicle rental, +10.3% for vehicle insurance)?

More generally, can anyone explain why some services CPI increased so much more than others?

Airline fares…well that may be mostly fuel cost increases. What about veterinary services?

And how about health services rising by 6%, while health insurance rose 28%? Isn’t most of health insurance going to cover health services, exclusive of the cost of drugs? Why the disparity?

Good questions, my guess is price gouging, companies are trying the most they can get away with.

People have to get insurance, rent etc and can’t get around it. It is very though for peasants, but what do others care…. as long as they got theirs.

Agree with Depth C, too little to late with qt and everything. Imagine inflation running high/near high for next 2 years and most peasants will get crushed.

I know I know some will say the rich those who hold assets will get crushed too, but here is the difference their getting crushed means less wealth, peasants getting crushed means unable to afford the basics.

All of this is a sick joke.

The day the peasants are disarmed, eggs will be $100/dozen.

Bloomberg “Odd Lots” had an interview about CPI a week or two ago. There are some timing issues regarding the cost of medical services, because during the ‘demic folks postponed care, and now there’s some catch-up, and because most medical services aren’t directly paid. This, if my recollection is correct, results in reduced CPI medical costs now, with the increase showing up later. There seems to be a link to the interview at

Car insurance increases are the result of the increased complexity of newer cars. All the active cruise control, parking sensors, etc. can take a small accident and launch costs into the stratosphere. There’s hundreds of dollars of “calibration” fees associated with aligning cameras and sensors that weren’t previously incurred. Same costs are incurred when you have to replace a windshield (camera alignment in rear view mirror base).

Spare parts costs have gone up as well. Will even rise more so when the reality of increased energy costs hit aluminum components (and the ban on Russian aluminum won’t help). Wiring harnesses for many European products are made in Ukraine.

Our recent repair took 8 weeks to fix a fender, headlight, and bumper cover. The holdup was a $58 wiring harness and a $35 bracket. I sourced the wiring harness for the repair shop because the local dealers couldn’t find one – and paid through the nose for it as even the manufacturer didn’t have one for “emergency release”. They had zero in stock nationally and no shipments scheduled from the supplier for “a month” (the guy I talked to at the parts depot said they say “a month” but they truly had no idea). The bracket was snagged out of an “emergency supply” that was invisible to the dealers.

The rental car costs increased as our vehicle was out of service for 8 weeks. We survived for a few weeks with the garage queen but when the monsoons hit, we figured it’d make a lousy submarine and got a rental. Enterprise provided us with a one year old RAV-4 that had 50K on it and appeared to have been stored in the bottom of a lake and subsequently washed with a bag of gravel. Worst rental ever – and I’ve had some pretty bad ones. Their lower costs might reflect the reduction in depreciation on the aged inventory.

Wiring harnesses are mostly made in Ukraine.

New windshield for my 2021 Hyundai was $879.00 installed (covered by insurance 100%). Tech said 1/2 the cost was installing and aligning the cameras in the camera module in front of the rear view mirror. Insurance won’t release the car or pay if the alignment data is not correct.

The lesson of history is that inflation will never be brought under control unless rates are significantly above inflation rates.

We will get there but the damage will be enormous as the reckoning is delayed.

Otherwise, expect the stock market to spike as they lose confidence in Fed getting inflation under control and start pricing hyperinflation scenarios.

A market move like today if followed in the coming days could signal such struggle to price hyperinflationary risks.

A determined Fed would call an extraordinary meeting and hike immediately 100bp and signal more hikes.

There will be pain but that is the only way at this juncture if we arent to suffer complete societal collapse.

Complete societal collapse? It’s already happening. When I moved to Texas in 1991 you rarely saw a homeless person on the street. Now there are homeless everywhere. Crime is out of control as a result. I-35 is one huge traffic jam from Laredo to Dallas. The electrical grid is dysfunctional. Taxes and insurance have doubled and tripled. Who do you think is to blame for this? The only people who are better off here are the wealthy who pay almost nothing in taxes. Texas is an expensive Third World country just the way some people want it.

Just like the old computing maxim ‘garbage in, garbage out’, leaders propagating garbage ideologies eventually create their garbage worlds.

Counterpoint:

It’s not that bad.

Many big Texas cities are filing up with illegals and “folks from prosperous states”. Both events will not improve conditions.

But in my home state and city (in Connecticut), crime is really getting bad. Last night, two uniformed police were gunned down responding to a call for help. A real setup according to the local news there.

The U.S. is slowly turning into a third world nation before our eyes. I’m actually glad I don’t have any grandchildren to leave this mess to.

Don’t let facts interfere with your rants:

“FBI data released Monday suggests that the violent crime rate in the U.S. remains on a decades-long downward trend, falling by 3.9 percent in 2018. Overall, the violent crime rate has plunged by more than 50 percent since the highwater mark of the early 1990s.”

Key word “violent crime”. Now look at the same data on property crime and retail theft. Then factor in that most petty thievery (like any theft under $1,000 in CA) isn’t prosecuted and, therefore, often not reported as the police don’t bother to show up.

Who cares about retail theft?

I order all my stuff from the internet.

As my wife likes to say, the Supernova has already happened, done deal. We are just waiting for the 8.3333 minutes it takes for that information to arrive.

“The lesson of history is that inflation will never be brought under control unless rates are significantly above inflation rates.”

Agree. The current interest rate relationship to inflation leads to wealth destruction…..a very slow moving train wreck.

Looking at the M2 chart from the St Louis Fed, the trend line of money growth is about $4 Trillion dollars below current levels amped up by COVID relief, etc. Removing that $4 Trillion will likely never happen as the Fed has handcuffed themselves. Perhaps they like the handcuffs and it serves their ultimate purpose, monetizing debt.

Absent from any Fed pronouncements is the mention of price “rollbacks” . If the Fed truly believed that 2% inflation is appropriate, then getting prices DOWN to the trend line would be warranted. Never hear that from the Fed…just MORE inflation but at lesser rates. The citizenry can not handle that scenario, IMO.

No, high interest rates do not bring inflation under control. High interest rates add more money to the system and keep inflation going.

Remember, inflation is adding more money to the system. CPI is and index, that may or may not measure inflation.

To get inflation under control, use modern technology and make every dollar in all account have their own uniqe serial number like on dollar notes. Then stop issuing new serial numbers and continue QT. That is deflate the amount of money.

Then, prices may stick or wind down. With some indended and unintended side effects.

What high interest rates actually do is force the economy into recession for various reasons. It is the recession in turn, that ends inflation.

Inflation is the result of too much money chasing too few goods and services.

Recession causes both lower asset price revaluation and debt default. Lower asset valuation, and debt default cause money destruction which drains money from the economy ending inflation.

So what is it, persistent inflation, Fed hikes and QT, housing values tipping into a dive down, stock market lurching up and down (until capitulation), job market softening, wage hike stall, layoffs, fear, consumer refusal to stop spending until the personal balance sheet combusts, continuous massively premature calls for a “pivot” LOL, gamesmanship and brinksmanship on a global scale, and the pain of middle/lower class metastisizing upward inevitably, the smug’o’meter needle pegging in the red for the smarter than thou 40 somethings who know not the pain of hard times but will eventually be served a heaping slice of humble pie, slice after slice they will have to choke down involuntarily.

2023 brings harder times not better times, 2023 provides no relief.

Valuable charts as always.

“….a large panel of homeowners report their home would rent for.”

I am astounded by this metric. What panel? Who compiles the results? 23.8% of the CPI? Slippage and tweaking would be caught by whom? And Case Shiller has hard current data and it is not used in inflation calculations?

The market will be tough to be short going into the election, IMO. That could have been the low, and a retest would be a buying opportunity. The Fed will hike then declare a pause. IMO.

There is no reason for the fed to pause, nor any reason to believe they will.

You can check the methodology. A “panel” means that the same 10s of thousands of homeowners get asked on a rotating basis twice a year what their house would rent for.

Seems archaic with lots of room for slippage….for such an important input number for the CPI. IMO

Spoke with a real estate broker in a southern coastal state….

He said still lots of buyers, few sellers.

Pure wisdom dispensed daily.

Wolf predicted this rally.

If you think there is a better website to get your financial information, you are wrong.

The maverick of Wall Street is very well versed in economics and especially the ” Stock Market”.

I am a home owner and have no idea what my home would rent for.

I am quote educated financially.

Fed should bank on hard data instead of this bs survey

“Rent” is hard data. “OER” is an opinion.

I don’t know the details of owners equivalent rent, but my first questions are – how do they pick the responders, and how much time and thought do the responders put into it?

Also, has the GAO or other accountability office ever reviewed the historical accuracy of the result?

I’m a little baffled why food inflation has kept so high, I always thought these were highly competitive markets. I know that poultry and eggs are being impacted by some type of flu that is killing herds. Ukraine is impacting global stocks of wheat. But the inflation seems to be hitting many categories. Just greedy companies stoking inflation.

The lack of affordable purchase prices on real estate increases the rental prices, as people cant buy a home. This is going to take some type to get unstuck, as home prices need to plunge by at least 25-40%.

Healthcare is a just a horrible industry that needs to be gutted. Americans receive horrible quality of care for ridiculous prices.

What a mess!

Come on. Health care is a hugely profitable business in the US. We spend ten times as much per capita on health care as Mexico but our life expectancy is a year greater. In this as in so much else, there is a reason for why this is so. You figure it out.

I recall Blue Cross Blue Shield operates on a 6% profit margin. This came up during the “affordable” health care bill deliberation.

Do you recall that Blue Cross Blue Shied was started by doctors to make sure they got paid?

Houses peaked when the 30 year mortgage rate bottomed around 3%.

To get them down to early 2020 levels, the 30 year rate should level off around 6%.

That would lead to a 30% drop based on a 10% drop for every 1% increase in the 30 year mortgage rate.

On average home prices went up about 30% to 40% from 2020 to early 2022.

Our townhome in Florida panhandle (2 miles from beach) was around $240,000 back in early 2020. Same style home in our HOA was selling for $320,000 in March 2022, and one just sold for $300,000 this month. HO-3 property insurance is what is killing us as it went up from $600 in 2017 to $1500 in 2022.

A 30% drop would wipe out a 42% gain in price.

AD

.

Might wipe out the “gain”, but likely won’t change the property insurance premium. Insurers don’t insure property value as the land and foundation rarely gets destroyed. The insure the structure and the replacement cost (based on current material, labor costs, costs of alternative housing if the damage is severe enough) won’t drop just because of a loss of value.

History does not prove your theory.

House flippers in 2004-2008 had mortgage rates in the 6% range. 6% still caused a housing bubble.

1) Housing prices were lower in 2004-2008 so monthly payments were less. All that matters is the payment, not the interest rate or the price, but if one goes up, the other has to go down to accommodate the payment.

2) Lenders were making LSD loans so that anyone could buy anything. That is not the case today. People prior to 2008 were buying on speculation, and it caused the worst housing crash since the great depression.

Agree, the US healthcare industry and healthcare system in general is predatory and a complete disaster. The USA has by far the highest healthcare costs in the world with some of the worst quality–the worst life expectancy in the developed world (we’re also now below Cuba, China and Costa Rica), lousy infant mortality and high medical error rate. It makes a mockery of the US self-image as a capitalist champion–who the heck runs a business by charging high prices for consistently terrible and worsening service? But, that’s US health care for you.

The system is opaque, hard to get a sense of prices, both hospitals and health insurers find all kinds of lame ways to overcharge–openly fraudulent billing–while weaseling out of payment obligations even after they’re happy to take your money in premiums and other charges. (One of our neighbor’s premiums went up 40 percent in just the past two years at his company–and he’s a super-fit, 20-something non-smoker and varsity athlete in college) And it is indeed driving inflation. Healthcare in the United States is the very worst of rentier and crony capitalist mixed with the very worst of socialism and state coercion–I used to think those comparisons of the US to 3rd world countries was hyperbole but we certainly are 3rd world in the way so much of our healthcare system works and totally shafts over hundreds of millions of Americans. Worse than 3rd world actually–at least in an actual 3rd world country, healthcare is usually cheap (and often higher quality than here too, from those commonwealth-fund rankings).

The last private practice doctor I had told me he was being driven out of business by all the reporting requirements that required him to go from one nurse and receptionist to one nurse, one receptionist and two billing/paperwork processors.

He went “concierge” and I paid $1,800 a year to see him (even if I never saw him). But he did make house calls and I had 24/7 access via his cell phone.

Yep being hearing that from our doctors too, they’re busy enough as it is and now those dumb EHR’s and documentation requirements keep piling up more and more every year. The big investor and venture firm-owned practices keep dumping even more admin requirements onto the laps of doctors and nurses but it’s not like they have any extra hours in the day to complete them, while in effect reducing the actual salary per hour for doctors. So the docs take the docs home into the wee hours, can’t see their families, medical errors go up, less time with patients and then docs and nurses burn out all over. It’s a bizarre case of a healthcare system that’s terrible for both patients and the practitioners, but great for at least a few high placed middlemen who then have enough money to buy a Congressman or two. It’s only that corruption that still sustains this unsustainable system, otherwise everything from market forces, to consumer demands and just the weight of terrible outcome data would have reformed it long ago in a very different direction. We’ve also being looking at concierge options lately with a couple of our docs who left their practices.

If Western countries go ahead and implement that whole insane oil price cap thing on Russia, gasoline will shoot up again.

Winter is Coming.

My diesel went up 22% in the last week. Back over $5/gal.

With the idiots we have in charge of fuel & energy policy,

not sure what rate increases will change.

I saw an amusing headline somewhere in the past couple days, which went something like: “The FED’s moves are having no impact on inflation whatsoever.” This made me laugh out loud. These clowns printed waaaaaaay too much, and now they can’t put the genie back in the bottle. Their credibility is permanently shot.

Inflation has made Jerome Powell its bitch, and is having its way with him. In his infinite arrogance he thought he could do a little soft landy-poo sort of thing, like he just magically controls things, but there will be none of that. Even the market today laughed in his face with bad breath. Now it’s back to the drawing board. Maybe somebody can tape his balance sheet to his thick skull? Do something for once, clown boy.

> In his infinite arrogance he thought he could do a little soft landy-poo

LOL! I see Powell in his kindergarten softy mentality, steering his little kiddie tricycle into the heavy traffic of the world at this moment, like out onto the tarmac at LAX, looking for that soft landing. And tens of millions of children are being tucked in with bedtime stories of this wonderful antic hero.

Not unlike a UK with absurd personages steering the clown car into ruin. It’s all fun and games until the bond vigilante adults pull the rug.

2020 Bottom to 2021 top was trillions of free money to the markets. 2016 was also fake. QE. Buybacks and corporate tax cuts. I fully expect the SPX to return to 2016 levels. SPX went up some 700 percent from the 2009 low. It will pay for all the moral hazard as Will retail investors, pension funds and 401k Buckle up

Great article. Lots of juicy detail.

US retail inflation is still a bit toppy. Although, the 0.4% MoM total increase for Sep 2022 points to a YoY runrate now dipping to under 5%.

Would be great also to see some deep detail on the leading indicators of US “wholesale” inflation. Prices of things like shipping containers, wheat, etc. have tumbled up to -70% from their peak in recent weeks.

Producer Price inflation was reported the day before consumer price inflation. It’s still running hot.

The consumer price numbers are being gamed for the election. The strategic petroleum reserve can’t be drained much longer, and gas prices that were low last month are already much higher. Food inflation is partly a matter of scarce fertilizer and poor weather depressing crop yields. Food also requires labor.

Both labor and energy cost inputs will continue to rise and pretty much everything requires one or both!

It’s under appreciated, but I also suspect the ginormous Tonga volcanic eruption is having indirect effects similar to those from Krakatoa – couple years of bad crops.