The Fed is getting nervous about inflation. “Temporary” doesn’t cut it anymore. And the bond market is getting a whiff of it.

By Wolf Richter for WOLF STREET.

The 10-year Treasury yield jumped 11 basis points today to 1.43% at the moment, the highest since early July, and the biggest jump since February. Apparently, it sank in today what the Fed had said yesterday afternoon. It placed the beginning of the Big Taper into November to be done with by mid-2022, which would then pave the way for rate hikes. Fed officials keep moving the first rate hike closer and closer. And they expressed their nervousness about the red-hot “temporary” inflation lasting a disturbingly long time.

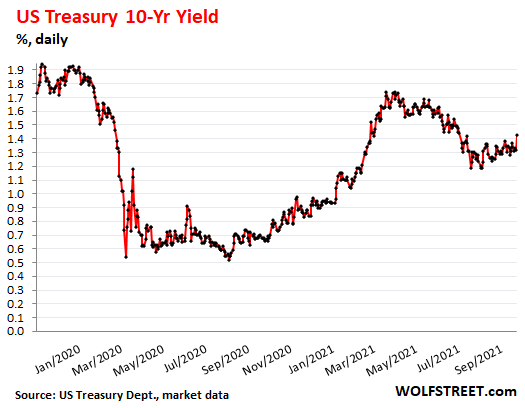

Tapering the asset purchases and ending them in mid-2022 would remove the single biggest and most relentless buyer of Treasury securities, mortgage-backed securities, and Treasury Inflation Protected Securities (TIPS) from the bond market. QE was designed to push down long-term yields; and it did so with marvelous success. The end of QE is going to take that massive force off the market.

Bond yields rise as bond prices fall, so for holders of long-dated Treasuries, this was not a good day.

The short end of the Treasury spectrum – from the one-month yield to the two-year yield – was roughly unchanged, which is the area where the Fed effectively controls markets with its policy rates and trading activities, including the target range for the federal funds rate of 0% to 0.25%, its repo rate of 0.25%, its reverse repo rate of 0.05%, and its Interest On Excess Reserves (IOER) of 0.15%.

Over the past 12 months, the Fed officials’ median projections of inflation at the end of 2022, as measured by the lowest lowball index that the US has, core PCE, has steadily increased from 1.8% a year ago to yesterday’s median projection of 2.3%, the highest inflation projection since 2007. Core PCE inflation is currently 3.6%.

Fed officials have been saying that the “temporary” factors would recede by late this year and early next year, but these projections are for the end of 2022, long after the “temporary” elements have faded.

And there is a message in these projections: “Temporary” isn’t going to cut it anymore. There is durable inflation being figured into the equation now.

It’s clear that this Fed is getting nervous about inflation that has been spreading far up the supply chains, with companies paying higher prices and being able to pass on those higher prices to the next entity in line, and finally to consumers, for all to see.

The US has the highest consumer price inflation among major developed economies, with CPI-W for urban and clerical workers at 5.8% and CPI-U for all urban consumers at 5.3%. Producer price inflation is much hotter, indicating what is coming down the pipeline, with PPI Final Demand at 8.3%, and PPI Intermediate Demand in the double digits.

This inflation is occurring even as the Fed is still stomping with its iron boot on the insane accelerator, doing $120 billion a month in QE and repressing short-term interest rates to near 0%, with real yields now being negative for nearly everything except the riskiest junk bonds.

This is truly a crazy situation, and even the Fed is getting nervous about it.

Other central banks – including the Bank of Japan, the Bank of Canada, the Bank of England, the Reserve Bank of New Zealand, and the Reserve Bank of Australia – have already either ended or throttled back their large-scale QE operations. The ECB has announced that it would “recalibrate” its QE. The process of ending massive money printing has started.

And the first rate hikes have started trickling in among developed economies: The Bank of Norway today raised its policy rate by 25 basis points to 0.25% and put another rate hike on the table for December. The Bank of Iceland hiked its policy rate twice already this year, by 25 basis points each, to 1.25%. The Czech National Bank has also hiked its policy rate twice this year, to 0.75%. The Bank of Korea hiked its policy rate in August, by 25 basis points to 0.75%.

They’re all worried about inflation getting out of hand, but none of these countries faces the type of red-hot inflation that the US is now afflicted with.

But the Fed is ever so reluctantly getting the memo that “temporary” doesn’t cut it anymore, that the enormous amounts of monetary and fiscal stimulus have created the most overstimulated economy ever, that has outrun supply, and that even if the Fed ends the stimulus now, the stimulus already washing through the system, including the ridiculously deeply negative real interest rates, will continue to push up inflation. And the bond market might have gotten just a whiff of it today.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And another tidbit, from Mortgage News Daily: average 30-year fixed rate mortgage jumped to 3.10% today.

Next week the stock market goes down 3% and the 10 year yield will drop to 1.15% , why bother. The game is rigged.

The most insidious effect of inflation is that people get demoralized and withdraw from society. Read Thomas Mann how societal relations broke down in post inflation Germany.

Why sweat it for a couple thousand dollars when people in government are printing trillions of them out of thin air.

People not returning to work is just one of the symptoms of the break down of society. Thank you Jay.

I would think having someone stay home with the kids would be a benefit to society.

But who can afford said home.

Yes, the same garbage from FED over and over again

Eastern…

The inflation is crippling to many Americans and the Fed people in the bubble just look at the markets.

How is it that these monetary dictators can decide to PUNISH those who attempt to SAVE by promoting inflation, and allowing an inflation that is running over their “illegal” target?

It looks as if the “upper class” (there, I said it) is pulling the ladder up on the rest of society. Loaded to the gills with stock and real estate, they cattle drive everyone else to buy what they already own.

How is it that they would know the Fed would not “promote stable prices” but instead promote inflation? And once achieved, not lift a finger to fight it?

Govt programs funded by the Fed’s “cheap money debt creation machine” placate the masses with child care and child credits, etc..

One for you, ten for me.

If only the Fed was held to its mandates, and their ever expanding powers contained…(can one person really decide to expand the money supply (M2) of the United States of America by 27% in less than a year?) There is no way this is intended, no way so much power concentrated into the Fed and their “dictators” could have been the idea behind the Federal Reserve Act.

Reports re Chinese real estate developers and HSBC mean HSBC RIP? I do not know. Search Kyle Bass and HSBC. No doubt banksters “Federal” Reserve would bail them out if they get in trouble. It will always bail out banksters around the world, again.

Homelessness is another symptom of “why even try”. My wife and I make “high middle class” income and we can’t afford anything. If we were low income we’d be in the same spot with govt subsidies paying our rent, school, healthcare… so much BS I don’t even want to play the game anymore.

“I don’t even want to play the game anymore.”

You are not alone!

Watch oil re: inflation. WTI just hit 74, highest in 3 years. Average 2020 about 35.

(PS: I’m not sue how or if the 2020 number includes that weird week where oil went negative, but still highest in 3 years)

Oil isn’t just a feedstock or input to everything, it is also a way of valuing the US$, other than by other currencies, which have also depreciated against oil.

8 years ago a 3.1% rate was unheard of for a 30-year. Now it’s considered “too high”.

Meanwhile, the 10-year Treasury is so far below the historical (much less current!) rate of inflation that it ought to be renamed. Any so-called “security” ought to offer actual security of principal (purchasing power)…

Today’s Treasuries are more like “Certificates of Confiscation”…. but that nickname is sooo 1970s. I propose…

Truth-in-Advertising Renaming of Treasury Debt Instruments

Treasury “Bills” (short term) –> “Portfolio Haircuts”

Treasury “Notes” (medium term) –> “Portfolio Blood-Donations”

Treasury “Bonds” (long-term) –> “Portfolio Amputations”

Treasury “Inflation Protected Securities (TIPS)” –> “Portfolio Strippers”

Note that todays TIPS have negative yields (-2.5% after inflation!), plus the “inflation adjustment” is taxed (as well as being under-counted). In short, TIPS provide neither inflation protection nor security.

A 30-year Treasury, meanwhile, offers only 1.95% while the Federal Reserve targets inflation > 2% (and backs it up with QE as needed), and the average inflation over the past 30 years is well over 3%. The good news is that compounding works backwards in this case – I think a 1% annual loss of purchasing power only results in a 27% Portfolio Amputation over 30 years!

Brilliant. I concur.

“Treasury “Notes” (medium term) –> ‘Portfolio Blood-Donations'”

I was just thinking, while reading the article, how a few years ago I could probably have more easily and profitably sold my blood compared to the chump change I got from purchasing a Treasury.

I had registered at the government Treasury auction website, and bought a 6-month or something like that. The final yield seemed trivial, not worth the hassle. And general feeling the government website seemed to impart was that it was doing me some great favor.

Wisdom…

For 7 decades and until 2009, Fed Funds equaled or exceeded inflation. This can only be taken as “normal” given the history of this rate relationship.

Who decided and when that this was no longer the “norm”? To have the “inside” on this decision is everything …. for where would the markets be now if Fed Funds were 5% to meet the current inflation rate?

In 2006 and 1999, when inflation was in this neighborhood, 30yr mortgages were 6%, now 3%. Why? How? Why would a Fed buy MBSs well below the inflation rate?

The Fed seems to have mandates of making water run uphill, spinning plates, and holding beach balls under water.

“We the people” decided, collectively, by tolerating policymaking that led us to where we are.

“Every step and every movement of the multitude, even in what are termed enlightened ages, are made with equal blindness to the future; and nations stumble upon establishments, which are indeed the result of human action, but not the execution of any human design.” – Adam Ferguson, Scottish Philosopher, in the 1700s.

I love it

In October of 2013, the 30 year averaged 3.56%… how was 3.1 “unheard of”?

Fair point – but I meant for the index, not for individual borrowers.

2013, 8 years ago, was the pre-covid low for mortgage rates, and the 30 year fixed rate mortgage national average (the number Wolf referred to) was never below 3.3%. So in the sense I intended, 3.1% was unheard-of.

But that is a national average, there’s local variation, and a few borrowers willing to pay points could buy the rate down below the average too. So at the individual level 3.1 wasn’t unheard of.

But it’s still true that “generational low” from 8 years ago is now “unaffordably high”!

Love the choice of the word amputation.

Wow, I think that was a huge move, cause I recently saw something like 2.86% as the Average 30-year Indentured Servitude Loan. Folks, we got trouble right here in River City! Yelled the carnival barker at the Fed.

Yup, was going to refi today and the credit of 750 became a cost of 5K in 12 hours. No way, am borrowing under 70% of loan to value….

Can’t wait to see where it’s at once the FED fully ends QE. Granted, I’m not going to hold my breath it will happen, but if it does, say hello to 5%+ mortgage rates again and a 20% drop in real estate.

Andrew Ruhland is saying that the US bond market is the real warning sign out there. It is going to be hit with a high interest rate shock, falling and US consumers will be hit hard with declining pensions and real estate values. He is saying the real risk is in the US bond market.

Is he right, who knows but things are getting really bad in the debt pumping up machine in the US and worldwide with endless money printing, much higher long term inflation, real estate values unsustainable, a US government that looks more socialist everyday and spending on social programs and creating unsustainable deficits, debt etc.

I meant in my comment, falling real wages more than inflation not seen in decades and higher and higher payouts to bailout big corporations like Evergrande in real estate.

Does anyone know how much hedge funds, private equity etc, have borrowed at near zero cost of capital? Better yet how do those loans stimulate economy? Those kind of investors don’t bring value to business. They instead take out all possible equity then start marketing it for a public offering.

There is no yield. Private equity has gone haywire. Pensions have nowhere to go.

The roll ups I have seen are preposterous.

I find it comical that since 2009 the Fed and their enablers swear that they haven’t done money printing. Maybe comical isn’t the right word.

This kind of reminds me of what happens when you first see a dead skunk in the middle of the road. There is a time delay before the smell circulates through the vehicle’s air ventilation system.

You’re a quarter mile pass the dead skunk, before someone in the car says “Phew! What is that awful smell?”

Clearly the Fed is driving with the outside air vent closed! They don’t want to smell what they are seeing!

These people are going to destroy this country. And I for the life of me cannot figure out why they think they’re going to come out smelling like roses. I really can’t.

The 0.01% will be just fine. They might not rehire for the one maid that quits.

No they won’t. Do you think they’ll want to live like the rich do in third world countries, where you have to live in a gated compound and can’t leave without security?

@RightNYer For a long time now the rich in the US have lived behind various types of walls and had protection since the regular police forces overwhelmingly patrol and enforce ‘peace’ in wealthy areas. They own the politics system on both sides of the aisle.

Andrew, having a police force patrol a nice suburban town is a much different story than the way the wealthy in Caracas have to live.

WES

If the 20 and 30 year olds knew the debt load, the lousy financial environment being created for them by this Fed and the massive debt subsidizing machine that is being enjoyed by the federal govt leviathan, they might be outraged.

Someone said …”It is incumbent on every generation to pay their debts.”

Whoever said that was not a Fed person nor a Congressman.

SPY from low point on May 12 until now is up 9.3%

TLT from low point on May 12 until now (after the drop today) is up 9.4%

Wish I could figure that out.

Thank you Wolf, great explainer for the biggest treasury move in a while.

Slowly…we might return to a positive real yield world again, which would be healthy.

11 basis points isn’t a jump. Its more like leaning into a wind that most assuredly will blow it back!

I think the FedEx report yesterday spooked a lot of inflation deniers and caused a selloff in the bond market. This isn’t transitory anymore.

Markets also don’t like the fact we have supply side inflation for both Labor and product inputs, as this is not something the Fed can fix by via QE or low rates or jaw-boning the populace. This time really is different as the supply side issues are going to bounce around for a very long time, in ways which will make it impossible to predict when this inflation will end. Thus why the Fed chose the word “transitory”, as it has no relativity to absolute time. The “Word Wizards” at the Fed must be IQ 200 as they do come up with some special quirky terms that seem to satiate the masses. For example, Quantitative means measured by the quantity of something rather than its quality. Yes Jay, you got that one right, good boy…LOL

Also markets will not like the raising 10 year yields, as the dividend yield on the S&P 500 is 1.33% today (per Bloomberg). Who wants to be 100% long in equities at the highest levels on every level EVER when the 10 year yields 1.75% to 2.10%? And how about 3-3.5%, which is where 5 year CD rates had been just 3 short years ago…

Supply side inflation means, you need an industrial policy that favors USA manufacturing and supply chain and you need to break up the oligopolies that have built up that have created a very low cost but highly profitable outsourced supply chain and with the dials set at maximum profit extraction. Fixing theses is an anathema to Free Market types.

Labor side inflation means you are going to have to let in all the immigrants that show up at the border to lower wages. Allowing this is political suicide to any politician.

Nothing will get even thought about fixing until the boomers are gone from government and corporate power. They are morally incapable of doing the right thing. Look at Grassley from Iowa (not a boomer) but running again for senate at 88, he needs a big stroke now.

Beware….food prices are about to shoot up. The nat gas price increase is causing the price of fertilizer to go up. Fertilizer is 20% of the cost of growing corn.

Nat Gas is 5 in the U.S. but is between 15 to 20 in Europe. I read that one Europe fertilizer company is going to stop production because of the nat gas prices. That can only mean fertilizer prices will go higher.

Does anyone believe Nat Gas will drop?

@r8

It was a US co in UK which closed 2 plants. Co2 nearly ran out for food chain and nuclear also needed Co2, didn’t know that.

The US Ceo was hauled over to UK Govt and got a price increase from £200/tn to £1000/tn plus cash in hand (unknown) to keep the show on the road,

Desperation!

Farming, food processing and logistics are all energy intensive. All this global warming nonsense and costly regulations making energy more expensive results in higher food prices. On the other hand, politicians like Gore, Pelosi, Obama become multi millionaires from this shake down.

Would you believe anthropogenic climate change was real if I told you that Bill Gates and George Soros were causing it with 5G nanoparticles?

@PS

Climate change has always been real because the climate has never been static at any point in history and never will be. There are as many opinions about the changes as there are changes.

A majority opinion is not necessarily a correct opinion and a case can be made that majority opinions are more often wrong than right historically.

Just sayin’

Food prices are already up 20 to 25% with certain products. Get with the times.

When it makes it to 2% that will be it….

CNBC had a article:

Housing prices in the U.S. increased 48.55% over the past 10 years, according to RenoFi. When doing the projections, RenoFi assumed housing prices would again increase by the same amount over the next decade. Here’s what else RenoFi shared in its report:

New York City will have an average home value of $964,101 by 2030.

The average home value in Nashville will reach $539,292. Currently, the average home value is $387,000.

Houston will see an average home value of $309,806 by 2030. The average home value as of August 2021 is $231,326.

FYI….I may sound like a housing bull. I am just trying to be realistic.

I was a huge housing bear in 2007. I was telling everyone I could that a housing crash was coming. I actually got out of the stock market early 2008 when all the mortgage brokers started to file bankruptcies as I new about 4 trillion in loans would not be paid by subprime borrowers.

Housing keep and I am looking for a catalyst for it to go down but I really do not see one at this point.

It really depends on the FEDs low interest rates and the GSEs funding Mortgages at low rates.

Who knows….if we have a recession, the GSE will just implement forbearances in the future to prevent any foreclosures. I would not put it past them. They would sign up a Blackrock to become their property manger and just rent back the foreclosed homes? Nothing would surprise me in an attempt to prevent future foreclosures.

Coming Jan 1, the conventional loan limits will again be increased. The rumour is that the new conforming loan limit will be $625k and in “high balance” counties (I.E. LA county) it will go up to $925k.

This will open the market to even more higher and stimulate demand for those properties that were previously “jumbo” which will now become conventional.

If fed prints more money it’s possible

Compare the FRED M2 Money supply chart to housing. The correlation is very close. The more they print the higher house prices go up.

RenoFi predictions could actually be low based on the M2 growth curve.

M2 money supply 8 years ago was 10 trillion. It is now 21 trillion.

M2 will most likely be 26 to 30 trillion by 2030. If so I suspect housing prices could easily increase by 30% by 2030.

Are those percentages are raw? US inflation over 10 years is about 20.7% so real price rises are less spectacular @ around 27.8% over 10 years or 2.485% per annum when compounded.

Minus maintenance, insurance and taxes.

Can anyone explain to me how the housing market will continue to fly up and double again in another 12 years, when just looking at property taxes, it now taxes 20 TIMES more cash in a safe CD today to pay a $10,000 property tax than it did 12 years ago when the property tax was half as much at $5,000/year:

$1,000,000 five year CD at 5% rate 12 years ago =$5000/year safe return

$20,000,000 five CD at 0.5% today = $10,000/year safe return

So in another 12 years, we have our $10,000 property tax move up to $20,000 when the house value doubles again?

If CD rates are still at 0.5%, then it only takes $40,000,000 CD to pay a $20,000 property tax (more if you include taxes).

So instead maybe our genius Fed can then give out negative 5% mortgages, so we can all borrow $4,000,000 and get paid $20,000/year (via negative interest rate FeD MaGiC) to pay our $20,000 property tax. Silly, I know…that is EXACTLY the point…how silly a game we are playing right now…

So what is the point of no return???

5% on one million is 50K, not 5K.

Math is hard….

$50 US for a quarter-pounder, no fries, no drink.

My dinky 1300 SF home in Woodstock GA, according to Zillow, has appreciated $105K or 64% in 3 years, $165K to $270K. The most recent house sold for $260K and needed some work and was ~ 100SF SF. The housing market is well past zonkers and its real cost is vastly understated in the Owners Equivalent Rent used in calculated CPI. Hell, my property taxes are up 10% over the two years I’ve owned my home, and my hazard insurance is up 10% in one year due to the inflation associated with the cost to rebuild skyrocketing. And none of these three things will be “transitory”. The only thing that will cause them to decline is a recession, at which point the FED will lower interest rates back to zero.

What happens every time the Fed attempts to taper?

Well, I can tell you what’ll happen before hand. Members in the Fed (not the governors necessarily) will go out and buy puts, and that will be followed by members of congress. Then the Fed tapers. It tanks the market, the buyers in question switch bias, sell puts, and buy calls. The bosses cite weaker economy, and stabilize taper or slightly increase it, and then in turn, the bull market occurs.

Rinse and Repeat.

Printing money allows politicians to get re-elected by deceiving people that bad policy has no consequences. Think about how many able bodied deadbeats didn’t pay rent while 5% of Grandma’s savings were stolen. Think about how billionaires got 30% more wealth from the money printing. That’s an immoral policy.

Old…

Exactly.

The Fed pretends to “help main street”.

What they have done is provide cheap money to the federal govt to then be doled out to encourage others to be idle.

This depresses employment numbers, then the Fed points to those numbers as reason to keep rates low….round and round we go.

Meanwhile, workers, earners, savers are punished at a 5% clip….

So the net is…

The Fed assists those who choose to remain idle

The Fed HARMS those who report for work each day.

Oh for some honest questioning of Powell before committee.

The Fed inflation projections aren’t consistent with this analysis. They project CPI at 2.8 by 2022. Only half the Fed wants a rate hike next year. So how do they get from here (5.8%) to there with half a rate hike? The Fed must be working on the assumption that QE works, they can moderate economic growth, (avoid the boom and bust) and the markets responded today. We know by fed history that taper promises are made to be broken. Rates will normalize on their own, if they should the Treasury will simply loan bonds to the Fed at a hefty discount and monetize social safety net spending, they have some cover.

The rate hike narratives are ridiculous.

What is being discussed….1/4 pt? Meaningless, ineffective in combating or countering a damaging inflation.

In the late 70s and early 80s, rates would bounce around 1/4 to 1/2 each week! The increments discussed today are a distraction. Where is Volcker when you need him?

He’s dead

His ideas are as well

His ideas launched a 20 yr period of responsible financial behavior

H

I realize you are obsessed with your version of history.

However…..in the present day

Volcker’s ideas are just as dead as he.

Histo: Volcker is revered inside the Fed. Many don’t like it becoming a puppet of the WH. There is a reason it’s a 7 year appt.

I fail to see how debt can have value when nearly every government on Earth has to print money to finance constant crises. With climate being number 1. Why would private money go into returnless ideas like direct carbon capture or unreliable wind or solar when they are worse in every regard than what they replace for average people?

I really wish somebody could answer this question. There is simply no way traditional capitalism works, which is what BoJo finally admitted yesterday at the UN. People are shunning further fossil fuel investment without anything to replace it while simultaneously STILL supporting unregulated manufacturing in China and India dumping pollution directly into the air and water.

Bottom line: enjoy reliable electricity while you have it. The hypocrisy of the entire “climate crisis” has now surpassed any real practical attempts at solutions or even attempts at solutions.

I just read some place recently that 70% of the electricity is produced burning natural gas. Natural gas will be used as the main source of electricity production for a long time. Big joules bang for the buck with a lot less pollution than oil. Methane capture and reuse will be a big game.

Not everywhere. In Canada most electricity is hydro. East coast, Quebec, Manitoba, BC. There is untapped hydro potential in Sask, as well as further possibilities in northern BC.

a few facts:

67% of Canada’s electricity comes from renewable sources and 82% from non-GHG emitting sources

Canada is the world’s third largest producer of hydroelectricity

Canada exports about 8% of the electricity it generates to the United States. There are 34 active major international transmission lines connecting Canada to the U.S.

With site C coming online there is a huge potential for exports to the US west coast from BC. Of course California reneging on paying their bill during the Enron fiasco might be a dampener on future sales.

And despite the attacks on oil and gas, it is great to live in a country that produces 2.5X its domestic requirements.

Hydro is not green. It involves terraforming that only works out of sight and mind. See Oregon and northern CA salmon spawns. Canada has a lot of out of sight and mind because it’s largely empty.

There is no answer that will satisfy the targets. Affordable cars are already out the window. So is affordable gas. This inflation is just the tip of the iceberg to pure centralization of a ration-based economy that will emerge. Because what else can emerge?

Currencies have literally evolved into a meme worse than dogecoin. Hypocrisy needs to go away and this smiling slimeball rhetoric based governance should be putting people in jail, not further enriching them. We could very well be on the precipice of an ecological cliff. But the words and the actions are downright opposite of each other. And let’s sprinkle in whatever inequality (racial, wealth, etc.) We can as well and pay that lipservice too.

It’s disgusting.

I mean there is literally no answer. This is a giant mess woven by the hypocrisy of 2 sides of the same coin.

Roger: ‘the perfect is the enemy of the good’

‘Green’ in this context means not polluting the atmosphere with gases from combustion.

Terrraforming?? Never heard of it, but at first attempt at an English- to- English translation it sounds like altering the landscape. So does that include a farmer ploughing a field? Excavating a building site?

Yes there will be costs to building a dam. The first ones predate electricity by thousands of years, they conserve water that otherwise runs into salt water. The hydro power is a byproduct.

There are also benefits that are purely ‘hedonic’ Many of the lakes people visit to experience ‘nature’ are actually reservoirs

The available shore is multiplied by orders of magnitude.

‘See Oregon and northern CA salmon spawns. Canada has a lot of out of sight and mind because it’s largely empty.’

It just so happens I’ve been on a gillnetter fishing for salmon on the Fraser in downtown Vancouver. It was an odd one and a while back but there have no dams built on the Fraser mainstream since or BEFORE. The Columbia has many, which is why the Fraser has a healthier salmon run than the Columbia. This is common knowledge to anyone on either side of the border interested in salmon.

But to return to the main error, simply labeling power sources ‘green’ or ‘not green’ and calling hydro ‘not green’ lumps it with coal plants.

From what I have read if you believe in clean energy, you believe in mining because it takes multiples of mined materials to build any green energy project as it does to build a gas powered plant. I just don’t believe society will accept the scarring of the land with mining, square miles of solar and wind farms when they get a feel for how much land it’s going to take to do what a gas plant can do.

We have a large solar farm close by. They are pretty unattractive, especially if installed on rolling hillside

Until fusion is real there is no truly green energy in my opinion.

The antihuman sentiment of the green movement needs to go away though. The U.S. needs more domestic material extraction and manufacturing with real oversight. The big conglomerates need anti-trust suits and the private sector needs to change the heirarchy to be client>employee>shareholder. The farce that is the S&P should be at 1600 or so and currency needs rebased. The ancaps are going to gain in number unless major changes happen to the paradigm of what capitalism actually should be in the 21st century instead of outrage over rhetoric.

The charade will go on as long as possible because it allows the rich to get a lot more and the poor to get a tiny bit. To make a change wealth must be redistributed, no one above the middle want that. Not only within countries, but also between countries. With that redistribution a lot of “freedom” will go too, like the freedom to travel far fast. Not that things will be any law against it, it will just be to expensive.

People would have to do with less stuff of all sorts, but may get more time. Time to sit down, read a book or do nothing. Want to travel, just go for a walk or ride the bicycle.

… and you can row yourself to Europe in about four months if you are in good shape,.

Roger

“There is simply no way traditional capitalism works, ”

What we have seen for the last 12 years is NOT traditional capitalism.

It is a fairy tale land created by central bankers stealing from the future to fluff the present.

True capitalism needs free markets to act properly. The Fed and other central bankers have inverted reality….the lender is slave to the borrower…

and who is the largest borrower in the world?

and who empowers the Fed?

Same answer.

While you make some good points on hypocrisy and the situation is just flat out complicated with many gray areas people don’t account for …. the biggest impediment we have on switching to carbon free energy is this false attitude like this that we can’t do it. We could bankrupt our enemies, create millions of jobs that might be the midwest’s only hope, and get rich selling and installing it to the rest of the world … not to mention stop the world from burning….. if only people would stop encouraging this propaganda from the fossil fuel industry and their politicians who are the only ones who benefit while you get hurt in every way.

It’s just completely absurd you approach this like we have a choice and your opinion is that it won’t be a “big deal”. It’s coming for us or is already here and we’re all in real trouble if we don’t do something but people won’t seem to entertain any solution that might cost them a little more or inconvenience them in some way and the inescapable truth is that whatever your opinion it’s going to cost us all much more ignoring it and now there isn’t even an economic argument for maintaining fossil fuels. We can never do anything unless it goes completely catastrophic … just like monetary policy… and you do seem to understand that … in this case you’re the Fed driving us to the brink with these policies we can all see will eventually fail.

America is already the “can’t do, won’t do” country.

Literally everything that everyone else are doing now (on smaller budgets) are somehow impossible and against the laws of nature!!

Most theory agrees that Venus was once an earthlike planet. Now its atmosphere prevents sunlight being reflected and the surface is far above boiling. (600F?)

We may be at or near the point where the earth’s warming becomes self- sustaining as the reaction effect of higher CO2 ‘runs away’

An example is the albedo effect: snow and ice pack melts to reveal rock or ground. This does not reflect sunlight, it absorbs it, warms the air, which melts more snow.

For an observer, the ‘beauty’ of being at the inflexion point is that things that took thousands of years are now taking place within decades, or zero in normal earth- science time. Thus the Ice Man emerges from a glacier in Austria as it melts. He has copper tools, which makes him old, right? In the usual time scale for atmosphere science he died yesterday.

The first ship to navigate the North West passage was the RCMP St.Roche in the 1930s. This took months as it had to grope its way thru countless false leads in the ice. Now you can take a cruise through there.

It just rained on Greenland’s highest point for the first time.

The explosion in the use of fossil fuels is so recent it makes the Ice Man look old. Large- scale coal burning only began shortly before 1800. It needed Watt’s steam pump to keep water out of the pit. Coal, at first only used for warmth, then fueled the industrial Revolution with vastly improved stream engines. Oil burning began a century later but at first this was for oil lamps. It became large scale only after WW1. In traditional atmospheric science, none of these intervals would be measurable, as 4004 years is zero in geology.

Since this virtually instantaneous change in the atmosphere coincides with the virtually instantaneous use of fossil fuels, isn’t it likely they are related?

We may be cooked but given the stakes it’s worth a try. There are some costs. although most people would put the pain of looking at ugly windmills towards the lower end.

Hasn’t the past shown that rates fall once they stop QE? Not taper but actually stop

After the great recession, QE ended in Oct 2014. A little more than a year later the FED started to raise its funds rate from .25% up to 2.5%. Over the same period, the 10-year treasury moved from ~ 1.9% to just over 3%.

And the thing that no one really talks about is the FED’s balance sheet, which will peak at more than $10T sometime next year once IF the tapering actually happens. That’s more than twice the amount when it peaked in 2015 @ $4.5T. The whole reason why banks are parking $1.3T in overnight reverse repos is because the FED has bought up so many assets.

When the FED sold off assets in late 2017 through Sept 2018, the reverse repo market freaked out, causing the FED to pump at least that same $600B back into the core banking system.

I’d love to see Wolf speculate how that effort will go for the FED this time around. Think about it. Within 12 months, the FED will have enough assets on its balance sheet to pay off 1/3 of the US National Debt. Yikes!

The FED’s balance sheet is the reason for the homeless crisis. I’m not kidding.

You can’t have inflation without wage increases.

Well, here we are. They will have to open borders

in order to control inflation. It has worked for

the last 40 years.

Got a couple burgers at the local In-N-Out today; it had a large ‘help wanted’ sign in the window advertising $17/hr to start, potential to $25/hr. The minimum wage in California is $15/hr, and we’re in the (relatively) low-cost Central Valley (decent houses available for under $400K).

A friend just drove up from FL to the midwest.

He said many fast food outlets closed….no workers.

Meanwhile the Fed pegs rates at zero to encourage employment while the federal govt takes that cheap money and pays people to be idle.

This arrangement seems absurd, at first. But it might be design. It allows a false argument to keep rates at zero and keep fluffing stocks and housing which apparently is their FOURTH mandate.

You cant even get a decent house in Idaho for under $400k anymore

And pretty soon you won’t be able to even afford to live in an RV, or even a car. Then, after that’s unattainable, the swinemen will corner the market on tents. They want everything you own, then want you dead.

Alright. Here is a game for all us. The rules are based on honor system. If we fail in our prediction we have to buy a mug from Wolfstreet media empire. Agree?

1. Fed will be forced to raise rates (higher than inflation) and bring the chaos in everything bubble under control before 2023.

2. Fed will reduce the rates. The effective rates will be negative, that is lesser than inflation before 2023.

My choice is 2. Wolf can get a screen shot of this. If I see Fed rising rates before 2023 Jan 01, I will send a cheque for the mug. What is your choice?

Long time lurker, first comment. Have not bought a mug but would love to be wrong here:

2

Cheezin

3. Don’t care if they raise or lower rates.

I would vote for #3 since the interest rates are irrelevant to me and many others. My credit card rates are very high and my credit is still bad from the GFC.

When the moratoriums end I will have even more company than I do now. There will be millions whose credit is also shot and don’t care what the interest rates are as well. Who are all those landlords going to rent to then?

“Who are all those landlords going to rent to then?”

Answer: The people that can’t afford to buy a house.

But do the purchase power of ther renters meet the rent expectations of the landlords?

And can renters purchase power sustain the landlords expenses?

A A,

You obviously haven’t been in the market for a rental in a long time. They want your income to be 3X the rent minimum, for upscale rentals, 5X the rent. They also want a pristine credit rating. For a $2K rental you would need a $6K income and a credit score in the 700’s. No evictions, ever. And now they will probably screen for rent moratorium participants. How many people do you think will walk out of this economic mess with those numbers? Not many.

Once poor credit scores reach critical mass, credit scores themselves don’t matter anymore. We saw that after the last meltdown, which is why people were allowed to buy houses only a few years after going into foreclosure. Wash, rinse, repeat.

Cobalt Programmer is another Swamp Creature. Don’t believe anything he says or any deal he promises.

1. They’ll be forced to raise rates, but it wont bring everything under control.

I will buy a mug if I’m wrong.

I just read some place recently that 70% of the electricity is produced burning natural gas. Natural gas will be used as the main source of electricity production for a long time. More Bang

for the buck with a lot less pollution than oil. Methane capture and reuse will be a big game.

WTF!!!!

B

AND…………….It is a mongolian clusterfuck!!!

b

PS.

FUBAR!!!

B

If inflation takes off……nominal earnings will increase at just about the same rate……so SPY is reflecting the higher earnings expected in nominal terms. …..adjusting for the higher P/E called for because rates are negative (after taxes and inflation) means an explosive market…..until the end.

Companies will attempt to absorb some of the additional costs but eventually they will raise prices. The consumer will buy at any price because they don’t save anymore (no point to it) so with their funny money governmental transfers and pay raises coming in left and right its just spend spend spend. Social security going up about 6% in January will fuel more spending. Government pensions going up. The tariffs have been in place about 2 years, economists tell us it takes roughly that long for price adjustments to filter thru the economy in reaction to the tariffs. Its all coming home to roost.

‘SPY is reflecting the higher earnings expected’… WTF? 🤣😂😅 Wow, that was a good one!

The wealth of the 400 wealthiest Americans soared from 2% of GDP in 1980 to almost 20% in 2021, fueled by zero% interest rates and huge asset purchases by the FED .

We are at a Marie Antoinette moment , where the FED is basically telling everyone but the wealthiest to “ go eat cake instead of bread”. This is going to end one of two ways . Either the Fed reverses policies and allows rates to normalize with the resulting collapse in bonds, stocks and real estate or else it continues its current policies and the wealthiest garner an even higher share of GDP.The latter inevitably will result in a violent response. Remember Americans own over 400 million guns .

The upper class has pulled the ladder up on the rest of us….

You are forced to buy what they already own…stocks and housing…

And you are PUNISHED for attempting to SAVE. The later is UNAMERICAN!

Saving and watching your spending was a reliable way to get on your financial feet…..no more. “THEY” have decided that is not going to work anymore…..you will be punished.

Remarkable there is no more blow back on this.

I guess the game is to get people from “two paychecks away from broke” down to “one paycheck away from broke.”

Direct deposit of your income, automatic payment of your bills. When hyperinflation hits it will all be automatic. We’ll send you a text – “You’re insolvent (i.e. broke). Move out of your home immediately. Oh, and return the car.”

I think the people in the capital riot got confused and forced their way into the wrong building.

It WILL not happen.

Another excuse for delay will come up by December. They don’t like Inflation but they will happily live with it, in fact they need it for the debt and asset bubbles they have created

it will be “persistent transitory inflation”.

Orwell spinning in his grave.

Marco…

perhaps…

It is unlikely that the arsonist will reach for the fire hose.

I can now see the Three Horsemen of the Bond Market Collapse riding over the horizon, peering through the smoke and mirrors of rate suppression applied ad nauseum by the Wizards of ZIRP at the Fed. They are, in no particular order: the Specter of Credit Risk (hoping you’ll get your principal back, forget the miniscule interest payments), the Specter of Inflation Risk (praying you won’t lose Purchasing Power due to those miniscule interest payments), and the Specter of Currency Risk (for unenlightened foreign buyers when they covert bond sale proceeds and/or minute interest payments to their domestic currencies to get out of Dodge). These ghosts of bond market discipline of ages past never really went away, they have just been on vacation with a grossly manipulated American debt market.

Eventually, the reality of these Three Horsemen rears its ugly head and we begin to have true price discovery in the American debt markets. Since we have record levels of this very shaky paper across the land, ub virtually all categories, the impact of even a 0.10 percentage change in the cost of paper has huge absolute impacts upon the burdened issuers’ abilities to service and retire same. Big changes coming our way.

David W Young

You didn’t include the 4th Horseman which is the biggest risk of all. Capitol loss due to declining Bond market values as interest rates rise.

Debt markets in decline can wipe off wealth faster than a stock market decline. The fall becomes geometric

Yes, Swamp Creature, had a senior moment on that one, the Specter of Interest Rate Risk, that is still somewhat behind the horizon because American investors are so Pavlov Dog trained to expect yields to only go down, and bond prices to go up. It is truly the Four Horsemen of the Bond Market Collapse. But the 4th Specter is riding very hard and fast to catch up with the other Specters. We live in interesting times, so say the Chinese who will probably give birth to this Son of Lehman Brothers moment.

Hello,

I thought I’d be a little more on the contrarian of things and simply say, “don’t fight the fed” as the ole saying.

Going over everyone’s doom and gloom comments…I’ll bet that what you think is going to happen definitely won’t happen. Everyone knows that if there is even a rate hike that new bonds will get issued anyway enticing savers to get good interest for once. As Wolf simply put, “yields fall as bond prices rise” They are inversely correlated. You also clearly saw a similar inverse correlation during the Covid crash in Feb 2020..simply put…as the stock market crashes…investors seek out long term t-bonds. There’s an inverse correlation there as well.

The way to protect yourself against rate hikes currently would be to seek out short term/intermediate t-bonds in my opinion. I highly doubt we’ll see a Volcker era inflation or if you’re scared of inflation…you could seek out treasury inflation protected securities (TIPS)

I know logistics/shipping prices have been inflated recently, but i mean….the consumer has been paying for “free shipping” for the past 20 years.

If wages don’t follow inflation closely, folks will quickly run out of money by paying all the higher prices. If supply of goods then restores when nobody has money to buy them, you could get a surprisingly quick recession.

It all depends on how many well paid jobs appear and how quickly supply and demand get back to normal.

It could still go either way.

If QE is ended, it means rate supression is ended but it could take years to get back to normal.

IMO

The Fed has always followed the market, not led it. Give them time and they’ll raise rates substantially to catch up with the market, which is already off to the races. There’s a good chance this will result in a real recession – not a one month Covid blip – which in turn will likely lead back to lower interest rates. A real market correction is coming and overdue and probably arriving sooner than most expect.

CCCB

“The Fed has always followed the market, not led it.”

That once was true…..but not since 2009 and QE.

They slashed rates in 2020….1.5 to zero in a hurry.

The “new” Fed lends money to the mortgage industry 3% below inflation…

and 120 billion a month to the federal govt up to 5% below inflation.

The Fed has become the market.

If only they would get out of the way and “follow the market” as before, we could find out what things are really worth.

As I posted before, the real estate market will be the first casualty of this “everything bubble”. Rising 10 year bond rates will be the trigger. Mortgage rates which are tied to the10 year bond will go up and housing will become even more unaffordable than it already is. The shadow inventory will appear out of nowhere and suddenly we’ll have a glut of homes for sale and no buyers.

What about when the real estate market tanks along with the economy and everybody that has vacation rentals wants out?

We didn’t have that X factor in the 2007 crash…

SC:

What do you foretell those “sitting on the sidelines” and “poor millennials” that are currently priced out of the real estate market will do?

Some on here have claimed that the price appreciation has outrun their ability to save the down payment required.. but if they already have saved a down payment and the prices drop, why wouldn’t they wade in to achieve their “dream” of home ownership?

I know of several people that are sitting this one out (at the moment) waiting for the inevitable adjustment. I’ve always said that it’s the price you pay for the item, not the payment, that matters. You can always refi at a lower rate in the event that rates drop or pay down the mortgage at a faster clip. Sure the percentage rate eats into what you can afford on a monthly, but it’s far easier to pay off $100K loan than a $200K loan. You can impact that greatly by making periodic principal only payments (if your loan is written that way). Been there, done that.

El Katz

I was in that situation a while back. Wound up buying an estate sale house that was totally inadequate which I thought I would be in a few years and then trade up. Wound up staying there 21 years. Fixed it up and sold it for a good price and moved into my current home. RE is a long term investment and a roof over your head. Any other use is just speculation. A lot of people are going to lose their shirts when this bubble collapses. I hope they don’t come whining to me because I am not interested in hearing their problem.

See this idea assumes that once they raise they keep raising meaningfully. If rates went to 5% yes, that would happen … but they won’t. They will pretend to raise, maybe raise once or twice but then stocks fall off a cliff and they stop raising and start QE and other bailouts.

My opinion now is that they will continue to do the worst thing they can do so they will just seesaw back and forth at low rates but with the increasingly higher amounts of QE or whatever is needed to keep the gas on the fire. Meanwhile inflation keeps going. Mainly it’s not going to be binary with high rates or low rates and all that entails. They will never just do the right thing and allow market rates, we know this. So they will continue doing things like they already have and make us go boom bust over and over, just probably quicker and quicker now.

Probably a much better guide to what the FED is going to do would be a running tab on everything the individual FED members are investing in. In close to real time. With a few analysts on the side. I wonder if some private whales haven’t invested in such a program.

Treasury Sec. Janet Yellen warned of an “economic catastrophe” if the debt limit isn’t raised.

Yellen said, if the debt limit is not raised the banks would not have any more money after a few days.

Bluff or no bluff is however a statement not to be taken lightly about the current situation of the banks in my opinion, we are close to breaking point ?

The bump in treasury interest rates coincides with the lack of a debt ceiling increase agreement. The budget proposal asks for more spending and higher taxes.

Brazil raised its overnight funds rate a full percentage point this week.

Mojer,

The debt ceiling will be raised or suspended, as it always has been before.

But if for some idiotic reason it is not, then yes, it would entail a financial meltdown moment of historic proportions.

The issue is that Treasury securities might go into default, or technical default, and this would impact everything, including the banks, because Treasuries are being used as collateral and suddenly the collateral goes into default. That’s a bad, bad deal. You would see a financial meltdown of historic proportions, globally. And all the Congress folks, from Pelosi on down, would lose half or more than half of their magnificent wealth overnight. And that is precisely why the debt ceiling will be raised or suspended.

They will do a suspended ceiling. It is the cheapest way to hide all the sloppy unfinished work below the joists.

I got some beans that will grow money if you plant them.

The debt ceiling is solely in the hands of one party.

If it isn’t raised or suspended then it would be the work of the Squad. And tantamount to political suicide for them since they want endless social nets to begin with.

There are 551 members of congress to blame, if one is objective.

“the banks would not have any more money after a few days.”

Wait. I thought they were awash in liquidity? What bank is Janet talking about…..Jamie Dimon’s?

How about the Federal Got borrow at least at the rate of inflation…say 5.5%? That might halt the creation of irresponsible debt for a while.

How about some comic relief from Chief Market Strategist JJ Kinahan in an Ameritrade “Ticker Tape” article titled:

“Thanks, Fed: Rally Continues After Relatively Rosy Economic Forecast, More Clarity on Taper”

“…(Thursday Market Open) Wall Street got some clarification from the Fed yesterday after a long wait, which helps explain why major indices are painted green this morning. The Fed basically said the economy is doing better, and that’s good to hear.”

Even during the ’00s bubble years, when famous economists were writing that it wasn’t a bubble because all that mattered was the monthly payment, and those were low because mortgage rates were low, rates averaged above 5%.

https://fred.stlouisfed.org/series/MORTGAGE30US

Now they’re 2.88%.

At 2.88%, the monthly on per $100k is $415, at 5% it’s $537, so if rates ever rise back to 5%, price has drop to $77.4k to keep payment at $415. 20% down payment t equity gone (esp. After closing costs). 10% down payment equity lonnngggggg gone. At April 2000 rate of 8.14%, $55.8k. Oooooooohhhhh.

Pricing homes according to monthly payment is like trading bonds.

I’ve really never been able to understand the concept that it’s a great idea into pricing houses like bonds and trading with 5:1 or even 10:1 or greater leverage. No one would let the average person trade bonds with such leverage.

jm,

“Now they’re 2.88%.”

That is like so last week. Now they’re 3.1% as of today. You might have to redo your calculations.

2.75 at a local credit union for 30 year fixed as of this morning.

Sure. That 3.1% was the average. Now 3.13%. The range is 2.75% to 3.45%.

Everything in America is now about monthly payment. Now you can buy shoes using monthly payment. A lot of companies providing monthly payment service like AFFRM are doing quite well and people are buying little things using monthly payment

Why did God create economists?

To give the weathermen someone to laugh at.

Touché

Congress is printing the trillions. The fed is just their outsourced factory. Tell us what congress should cut so we can have a balanced budget.

Should they cut welfare and have 100 million inner city poor people starving and rioting? Should they cut social security and medicare and have their most reliable voters throw them out of office? Should they have not done pandemic relief and not compensated all the businesses that were harmed by lockdowns?

This charade has been going on since the 60s.

mark,

Cut out the wars, and cut the Dept. of Defense, the Intelligence Community, and all the other mastodons of corruption. Let the CEOs of the military intelligence industrial complex go hungry and riot in the streets.

I like your style, but cutting defense to zero still doesn’t balance the budget. Not even close. Even before this year’s pandemic spending.

The fed will be printing forever. If they ever let interest rates rise to reasonable levels, markets will crash. State/local budgets will be busted. Housing will do what it did in 2009, killing the banks. And they will be forced to print again. And again…

It’s fun to dream, though :)

That is called a military coup. 😉

Or if it is the “intelligence” comunity that take the driver seat a “regime change”.

Joking aside, there are countries where this have happened. Following cuts in military spending by the gouvernment there have been military coups.

There won’t ever be a military coups in America. After three decades in uniform I can promise you that. It is just not in the DNA of the US military.

But you are not wrong about that being a trigger in other countries. I worked for the Navy in West Africa for the final seven years of my career and it was almost a rule there… when the government stops paying the people with guns… the people with guns will install a new government.

Wolf, you make perfect sense with that comment. Printing money like a drunken sailor, the US has forgotten the axiom that a society must choose between “guns or butter.”

When you subsidize something, you get more of it…

and the Fed has been subsidizing debt for 12 years…..with unrealistic rates…

Unrealized is the amount of debt and stock that has been created in the private sector……which is enormous.

Agree 1000%

Cutting some of the fat in these agencies would be a good start. I was there from 1983 – 2010. At least 90% of the hardware/software projects were total failures. Contractor fraud was the norm, not the exception. You get about 10 cents on the dollar with the military industrial complex.

Just because they fronted me money for phase 1 of my obviously impossible proposal doesn’t mean that it’s fraud per say.

I don’t trust the fed. Why should I? I remember Greenspan telling congress he made a mistake. Bernanke said subprime wasn’t a problem. Janet Yellin said we won’t have another financial crisis in our lifetimes. Do you remember Jay Powel having to drop rates to 0 when they hit 2.5%? The repo market? The reverse repo market?Transitory my a**! Irrational exuberance? Bernanke telling Ron Paul the fed holds gold only because of tradition? $4 trillion wasted in the middle east for 20 years of nothing. Wake up people! We are being lied to, we were lied to and we’re going to be lied to in perpetuity. In 1971 our president told us he would remove gold from backing the dollar. That was 50 years ago and it’s still not backed by gold. That’s not temporary! Now the BIS are starting to push central bank digital currency so they can control when we spend and how much we spend… just for starters. Inflation is here to stay and the only truth I trust is that barbarous yellow shiny metal. I am so sick and tired of this crap

Believe a lie once. No shame. Believe a lie times infinity. Shame on you.

Wake up and let your politicians know you’re mad as hell and you’re not going to take it anymore!

Humans are too expensive. We’re selfish, bloated, greedy, and unsustainable.

I wonder how coordinated any of this is. For instance… is there any reasonable explanation for having the smaller nations’ central banks tighter first (before the Big Bad Fed does)? It just seems odd that the Fed is so slow to pull the trigger.

Then again, perhaps the Fed in a holding pattern until they see how big the Reconciliation bill is going to be?

Spencer..

The smaller nations have more agility……and much smaller issues/problems than the ECB or Fed…

One click for them has little impact…..one click for the Fed..???

Yeah… that is exactly what I am getting at.

So far the Bank of Canada has reduced the assets on its Balance Sheet by 17% this year! I find that fascinating… but logical. As I have said before on here… for THEM that is an easy solution… as long as the Big Bad Colossus to the South continues to expand both fiscal spending and QE (and their own country has a plan for reducing its own deficit spending by 50% in three years)… then why shouldn’t they take advantage of this moment? It is the smart thing to do… for THEM.

My real question is “Why is the Fed expanding this MOMENT?” I mean does it want the other Central Banks to take advantage and get a head start? Does it coordinate these things with them?

Or is the Fed just in a holding fire until the Reconciliation bill is passed and they can see how much federal deficit spending will be for each for the next ten years? That is pretty important information to a Central Bank whose main responsibility is to balance Unemployment against Inflation by managing the nation’s money supply.

I just don’t know.

TWO CORRECTIONS>>>

then why shouldn’t they take advantage of this moment? Ending QE is unlikely to hurt CANADA’s economy since the U.S. is their biggest market. It is the smart thing to do… for THEM.

Or is the Fed just holding fire until…

Hike rates all you want and it won’t help supply chains (the root cause of consumer price inflation), but it will screw up lots of other things.

Loose policy won’t help unless it is intended to address supply chain problems. Good luck with that.

Juggling chainsaws.

look out below in the dollar denominated foreign bond markets, think Evergreen on steroids as the yield rises on US bonds and thus the dollar rises in price due to increased demand, another another emerging market sovereign debt crisis anyone?

DXY hasn’t really changed much. It jumped around July or so but that was before Evergrande. At first I thought vaporizing billions of dollars by defaulting it could create a demand for dollars but considering how many dollars are out there it’s a drop in the bucket.

There are a lot of other factors that affect UST yields, like the debt ceiling and the Fed Paradox of sopping up dollars via reverse repo while still maintaining their bond and MBS purchase program.

Rube Goldberg couldn’t have come up with a better contraption.

I am absolutely amazed at how long this process has gone on. My greatest fear is that the longer you push the pendulum one way the farther it swings the other way. IMHO they have been pushing the pendulum one way for 10 years.

Isn’t it more like a high speed wobble on a Vincent Black Shadow when doing 147 mph?

Had that happen on a Triumph Trident at about 125. Nerves of steel put on full throttle and lightened the front. Never, ever, rode with a backed off fork damper again.

The sober reality is, once you have accumulated that much debt, once you have discovered the “miracle” of money printing, the situation cannot be fixed in a democracy. Nobody is willing to endure the needed pain and no politician would survive in the job long enough to make a difference. Volker was an aberration from long ago time. Inflation is the only way out.

An autocratic regime such as the PRC might be able to reign in the excesses. See the three red lines instituted for real estate companies that tripped up Evergrande. But the jury is still out if the PRC can pull it off without causing mass riots.

Regarding Evergrande, nothing big would happen. The Foreign investors would eat their losses and domestic retails investors would be protected.

I am sure PRC would manage this without causing any mayhem.

My 2c.

Agreed. Even politicians who run on a “reduce spending” platform lose interest in it over time, as there is always someone willing to outbid them and take their spot by promising more borrowed/printed money.

Sounds about right. There will always be a cause in need of government spending and stimulus to justify the need for the debt limit to be increased. Another war, disaster, unseen circumstance, being leap frogged by a foreign government in any sector deemed in our defense of national security, infrastructure, disease/famine…etc…

We can always borrow more to help the children now.

Why would anyone buy a 30 year US bond 2.00% yield or a 30 year bond 1.92% yield when i can buy a 5 year guaranteed investment certificate or GIC for 2.30% to 2.4% CDIC deposit insured or a 3 year GIC for 2.5% or a 4 year GIC for 2.6% provincially Ontario deposit insured. It boggles my mind.

A 30 year Canada bond 1.92% yield is what I meant to say. Heck, there are 18 month GIC rates at 1.60%. Why buy a 2.00% 30 year or 1.92% 30 year bond in US or Canada. I don’t get it.

– The FED is merely jawboning. But the FED won’t raise rates anytime soon.

– The US 10 year & 30 year yield rising is VERY DEFLATIONARY. And no, this isn’t the result of “rising inflation” or “rising inflation expectations”. No, it’s simply a matter of good old fashioned “Demand & Supply”.

– If one uses one’s braincells a little bit more then it will be clear that we’re talking about “deflation” when yields rise.

– When a stock is rising in value then this is called “asset inflation”. The mechanism for bonds is a bit different. When the yield on a US T-bond (e.g. the 10 year yield) falls then the PRICE of the bond rises (= “asset inflation”). But the reverse can also happen. When the yield rises for a US T-bond then the PRICE /Value of that bond drops. And that is called “asset deflation”.

– The yield curve seems to suggest that we have left a 40 year period of falling rates and have entered an era (5, 10, 20, 30 years) of rising interest rates.

– There is another danger for the US economy. The Trade Deficit has shrunk or remained flat but the budget deficit has gone through the roof. For those who understand the Balance of Payments and the implications of the 2 things mentioned above know what I am talking about.

Rates are up again, US 10 year 1.52%, 20 year 2.00%, 30 year 2.06%. It like a losing proposition buying US bonds when interest rates, yields are rising.

There could be 10% to 15% loses by year end in mid to longer term US bonds.