ECB is second giant to taper. Bank of Japan already ended QE. Bank of Canada shed 15% of its assets. Bank of England & Reserve Bank of Australia are tapering. Reserve Bank of New Zealand quit QE cold turkey. Riksbank will end QE this year. What’s taking the Fed so long?

By Wolf Richter for WOLF STREET.

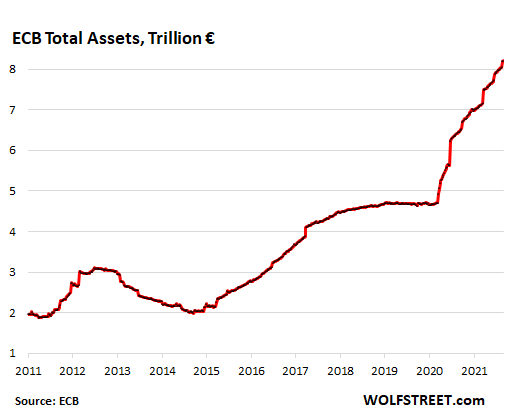

The ECB has increased the assets on its balance sheet by a monstrous €154 billion ($181 billion) per month so far this year via an alphabet soup of programs, blowing by even the crazed money-printers at the Fed with their average rate of $123 billion a month. While there appears to be consensus at the Fed that “tapering” its asset purchases will begin this year and will be completed in the first half next year, with assets then remaining level, the ECB announced today that it will start tapering its asset purchases now.

And thereby it is way behind the Bank of Japan, the Bank of Canada, the Bank of England, the Reserve Bank of New Zealand, and the Reserve Bank of Australia. But ahead of the Fed.

Following in the footsteps of the Bank of England, which had denied in May that its tapering was tapering, and in the footsteps of the Bank of Canada, which had denied last October that its tapering was tapering – though it has since then cut QE to nearly nothing and shed 15% of its assets – ECB President Christine Lagarde also denied at the press conference today that tapering was tapering, and stressed that tapering was instead a “recalibration” of QE.

Markets eagerly swallow these taper denials hook, line, and sinker. Anything but tapering.

In the press release, the ECB said that the pace of net asset purchases under the Pandemic Emergency Purchase Program (PEPP) would be “moderately lower.” PEPP is the biggie in the alphabet soup of programs, running at about €80 billion ($95 billion) per month recently.

The ECB didn’t specify by how much it would reduce its purchases under PEPP, but said that it would “purchase flexibly according to market conditions.”

The asset purchases under PEPP will continue in diminished form “at least” until March 2022. After that, the balance would be level “at least” until the end of 2023, before the “roll-off” of those bonds might begin. The roll-off means that bonds mature and roll off the balance sheet when they’re redeemed and would not be replaced with new purchases. This has the effect of reducing the bond portfolio over time as bonds mature.

The other programs would go on as before.

The Targeted Longer-Term Refinancing Operations (TLTRO III) will continue. These are loans to Eurozone banks, now with a balance of €2.2 trillion.

The Asset Purchase Program (APP), the now relatively small classic QE program that existed before the pandemic and includes sovereign bonds, corporate bonds, covered bonds, and asset-backed securities, would continue at a monthly rate of €20 billion and would “end shortly before” the ECB starts raising its interest rates.

This is in line with the consensus among central banks, confirmed by the Fed, that QE needs to end before interest rates can be hiked, on the rationale that QE pushes down long-term rates, while raising policy rates pushes up short-term rates, which would wreak havoc on the yield curve.

As of this week, total assets on the ECB’s balance sheet rose to €8.2 trillion ($9.7 trillion), about $1.4 trillion more monstrous than the Fed’s monstrous holdings. The four largest groups of assets on the ECB’s balance sheet are:

- €4.6 trillion in bonds (mostly sovereign bonds, but also corporate bonds, covered bonds, and asset backed securities).

- €2.2 trillion in loans to banks under TLTRO III

- €515 billion in gold and gold receivables

- €477 billion in foreign currency assets

Shrinking its balance sheet is not new for the ECB. It has reduced its assets by one-third over a two-year period, cutting them from €3.1 trillion in late 2012 to €2.0 trillion in late 2014.

In early 2015, it kicked off a massive QE program that ended in late 2018. From then until March 2020, assets remained flat.

Starting in March 2020, the ECB went hog-wild. And now the ECB is trying to figure out how to get out of this without blowing up the Eurozone:

Lagarde said that the decision to taper – oops, I mean, to recalibrate – the asset purchases was unanimous.

Timidly following in the footsteps of:

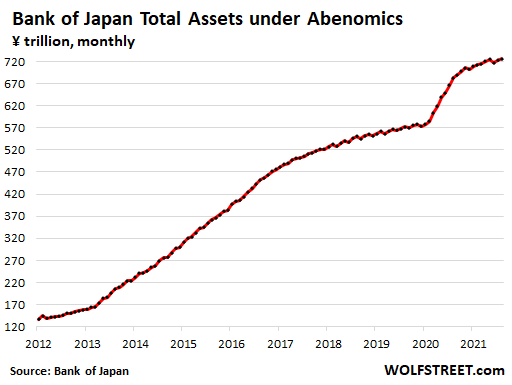

The Bank of Japan cut its asset purchase to near-zero, without any hoopla, thereby not only ending the pandemic QE binge but also the third leg of the economic religion of Abenomics – namely massive money printing. The current rate of asset purchases is minuscule and the lowest since before Abenomics in 2012:

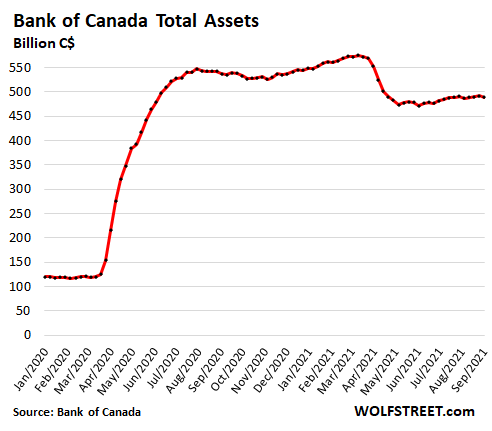

The Bank of Canada started tapering its purchases of Government of Canada bonds last October, ended its purchases of mortgage-backed securities, and shed its repos and Canada Treasury bills, with the effect of cutting is total assets by 15% since the peak in March:

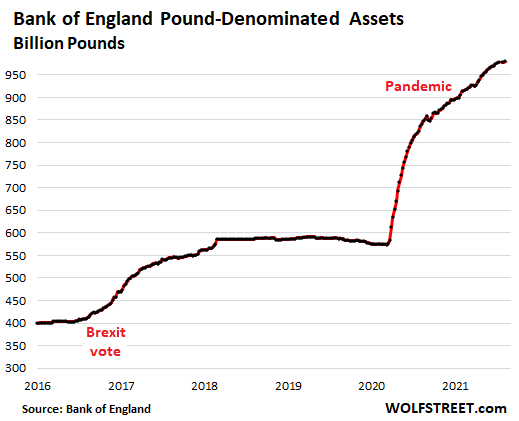

The Bank of England announced its decision to taper its asset purchases in May, and has since cut its weekly bond purchases, on net, from about £4 billion a week to close to £2 billion a week through the summer:

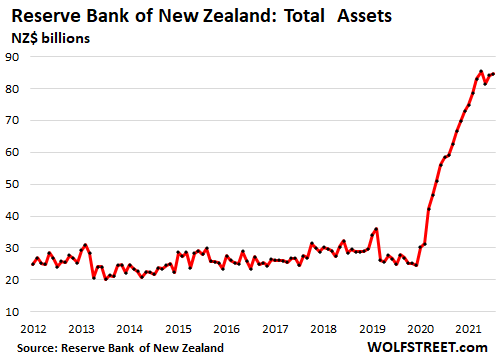

Reserve Bank of New Zealand ended its asset purchases cold turkey in May without tapering to pull the plug on the #1 housing bubble in the world:

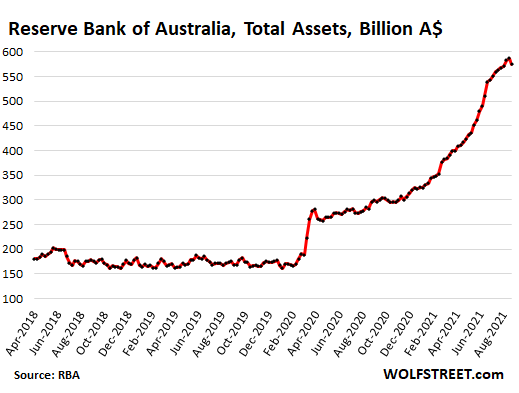

The Reserve Bank of Australia announced in July that it would start tapering its asset purchases from A$5 billion a week to A$4 billion a week. Total assets on its balance sheet declined last week for the first time all year:

The Riksbank of Sweden confirmed that it is going to end QE entirely by late 2021.

And what is taking the Fed so long? No one knows. Amid the most monstrously overstimulated economy and markets ever, the Fed is still printing $120 billion a month, though there appears to a consensus to not fall much further behind the curve than it already is and start tapering its asset purchases this year.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Maxine Waters says that JPow better not taper if he wants to keep his gig.

Not her decision.

Wolf, just like the last time, they’re just reloading the printers. Watch out for the next $15 Trillion when the market is down 20%.

😜

👛\💰💵💶💴

🎶money makes the world go around .. a mark a yen a buck or a pound .. money makes the world go around .. money money money .. money📯

Exactly this. I used to think that these people know what they are doing and will do the right thing. I now think that these arseholes are never going to stop.

Can you imagine interest rates at the long term average of ~8%? Exactly.

Yep. I would say if the market drops 10% they would start printing.

Do you think Powell is gonna be kept on the J team? I think he will be out. The elected one needs a scape goat.

I think Biden wants him to stay. But there is some pressure to get JPow out. I’m not speculating on what will happen. I’ll just wait till it happens.

Ms Brainard will replace Powell. Look for the announcement in the next month or so.

Powell will probably stay if the SHTF because no economist will know what to do about the fiascos that will be uncovered by a downturn. That’s when you need a wall street lawyer who knows how to wrestle with the pigs.

It may be true that Pres. Biden (and others) may want Powell to go but do you really think there will be anyone who will take a very different turn on FED (Congress) monetary policy?

We’ve gone too far down the road to be able to safely navigate any turns in the road to fiscal sanity.

Just hang on and hope you don’t break your nose at the bottom!

I don’t think the House members get to vote on Confirmation. But I agree that it will be interesting to watch who aligns with whom in the upcoming battle.

He will not taper and will lose his job anyway. Biden needs someone to blame for his failed economic policies. J Powell is toast.

The price of a home in Germany doubled in ten years.

Better than five in the US

The median price of a U.S. home in 2005 was $232,000.

In 2021 the median price of a home is close to $375,000.

There was a bubble burst in between.

It’s really not so bad except in HCOL areas. They’ve practically gone exponential and are now so far out of line from the medium household income and that it’s a sad, sad problem.

My home in a Texas burb took 14 years to double from 2007 and is still $120K below the national average while wages are 20% above the national average.

The former LCOL (now medium cost) ‘burbs in many big Southern and Midwest metros are the shiznit, especially in Texas. I’ve decided to never move back to SoCal. Why suffer?

Depends on what area. Some areas have doubled in 5 years.. Much of that increase in the past year and a half.

There was an interesting article in The Telegraph today “Why Germany has lost patience with QE”.

Germany has now also started paying rentiers more than wealth creators.

“Germany has now also started paying rentiers more than wealth creators.” This is how a state expresses debauchery: by the pursuit of a perfidious path that hastens its demise.

Since you are obsessed over the word rentier, perhaps you would give us a clear definition of what you mean by it.

Rentiers do not produce, they typically claim a monopoly upon something then demand money despite failing to create value.

It’s a very common econ term. Rent seeking is another phrase.

examples:

* profit from the unimproved value of land that rose due to societal development

* intellectual property claims to retain a monopoly, eg obvious software like Amazon “one click ordering”.

I would also add profits from shares into that given the wider context. The government is constantly adding immigrants to ensure labour supply is always far, far greater than demand, to suppress wages. In that climate it’s very, very easy for companies to pay workers far less than the value they add. The artificial labour climate and the suppression of wages are not natural, and shareholders reap the unearned gains.

OS,

Mostly rents, interest, dividends, and inflation created asset appreciation. I would also include the theft of labor by suppressing wages, but that is just my addition.

Georgist,

“Rentiers do not produce, they typically claim a monopoly upon something then demand money despite failing to create value.”

You mean like a politician or a gvt bureaucrat?

(Monopolies of legal force, money printing, etc.).

Georgist,

That’s what I thought you meant. What do you expect to do when you are 70 and can’t work?

You must have income from your investments be that loans, rental income or equity investments.

If you have a job when you are middle aged it’s more than likely because some grandma or grandpa needs income and so invest in loans, real estate or shares

Savings or income from productive investments are not rentier activity.

As I said I’d argue that stocks are no rentier thanks to the govt manipulation of the labour market, but that could be reversed and leave the reward for productive activity without the extra gains from exploiting labour.

To the other guy who just has to write about govt stuff because he’s american “liberal” – yes it can include that, but it depends. If you are a school, that’s not rentier activity.

It really is more complex than the American attempt where you just show up, label stuff “free market” or “communist”, but not that much more complex.

@Old-School “What do you expect to do when you are 70 and can’t work? You must have income from your investments be that loans, rental income or equity investments.”

There’s an error in this thinking. You don’t need any income at all to retire, if you save enough in, say, gold or silver. At age 70 your odds of living another 50 years are zero, so you could just spend out the principal 2% at a time.

The reality is that there isn’t enough genuine non-rentier “investment” income to fund mass retirement for such a large share of the population. Even “Social Security”, funded originally by gold-standard dollars pre-paid by workers, has today become a rentier system where the elderly harvest taxes extracted from younger workers. There’s a good reason to do it that way but it’s still a rentier system.

Wisdom seeker,

I do agree with you on the gold in theory as that is true savings, but the government makes it tough with capital gains taxes, plus the premium on buying and selling.

In a nonfinancialized economy good capital investment by good management benefited society by widely distributing new inventions such as railroads, electricity, automobiles, telecommunicationas, personal computers. The 100 year average return on capital is about 6% above inflation which is certainly not an astronomical return considering the risk taken.

In the modern world good paying jobs require capital. For most corporations it takes about $1 million dollars of capital to support one high paying factory job. An employee without capital is nearly always going to be nearly worthless in the marketplace.

Even Michael Jordan wouldn’t have been worth anything playing in a high school gym. It took the multimillion dollar arena and marketing but mainly the investment in television and cable infrastructure to make him worth millions each year.

Michael Hudson, “Finance Capitalism versus Industrial Capitalism: The Rentier Resurgence and Takeover,” Michael Hudson (website), July 6, 2021,

Abstract. Marx and many of his less radical contemporary reformers saw the historical role of industrial capitalism as being to clear away the legacy of feudalism—the landlords, bankers, and monopolists extracting economic rent without producing real value. However, that reform movement failed. Today, the finance, insurance, and real estate (FIRE) sector has regained control of government, creating neo-rentier economies. The aim of this postindustrial finance capitalism is the opposite of industrial capitalism as known to nineteenth-century economists: it seeks wealth primarily through the extraction of economic rent, not industrial capital formation. Tax favoritism for real estate, privatization of oil and mineral extraction, and banking and infrastructure monopolies add to the cost of living and doing business. Labor is increasingly exploited by bank debt, student debt, and credit card debt while housing and other prices are inflated on credit, leaving less income to spend on goods and services as economies suffer debt deflation. Today’s new Cold War is a fight to internationalize this rentier capitalism by globally privatizing and financializing transportation, education, health care, prisons and policing, the post office and communications, and other sectors that formerly were kept in the public domain. In Western economies, such privatizations have reversed the drive of industrial capitalism. In addition to monopoly prices for privatized services, financial managers are cannibalizing industry by leveraging debt and high dividend payouts to increase stock prices.

For Germany, the events of 1914 – 1945 spanned a hyperinflation bookended by 2 lost wars. The economic repercussions were sufficient to keep Germany on a path of financial rectitude for another 70 or so years; this included a housing market that was not a “get rich quick” scheme. Sadly, that financial rectitude appears to be coming to an end.

“perfidious” “rectitude” …

Dammit , R, will you quit trying to make me smarter… I only have so much capacity…

Yeah, it’s not like the degenerates know what those words mean.

This for Pet:

Feeling almost totally degenerating(ed) on all sides these days,,, but I DO know what rectitude is,,, or at least what it was a few decades ago!

Not that I ever attempted such at altitude, in spite of attempts on the part of parents and mentors and womentors to inculcate same for many years…

@r

Germans I speak to are still as anti-inflation as they have always been but they sold their conscience to the EU and the bandits at the ECB. They haven’t had much inflation to contend with due to all the usual statistical shenanigens but now it’s coming home to roost at 3.9% last count so watch the winter of their discontent turn into a glorious summer or the other way round given we’re in September.

Will it become GERXIT??? Heard FREXIT mentioned for the first time today. Halleluah!

Just askin’

‘GERXIT’

Sir, enough of that rough language, this is a family blog.

Germany did very well with the Euro.

It made Germany more competitive in business being lower than a German Mark would have been.

@cb

Exactly, BMW, Mercedes, VW/Audi absolutely loved selling their German built models to all the other members who were building up DB loans to buy them. Not so good for DB although Merkel has their back.

Oh! but she’s gone next month.

Mine doubled in 20 years. In reality, adjusted for inflation and dollar devaluation I didn’t make a dime.

Mine doubled in 20 years too from 180k to 360k. I looked back and added up the all the maintenance and it has easily eaten up 50% of the appreciation. Stuff like new roofs, painting, yard work, new furnace, water heater, windows, water leaks, new carpet, etc.

Well, at least you can do the math!

So will foreign central banks be able to force the Feds hand?

I would imagine that volatility among politicians in DC makes USD less attractive while foreign yields rise

@PG

IMO what’s different about USA is that you have the most viciously ‘on narrative’ MSM in the World and your politicians and officials would never dare to face a grilling by the likes of that horrendous Haddow person.

Elsewhere the MSM eventually are forced to confront reality and change their tack.

Tapering! Hmmph!!! Ending QE!!! Haaahh!!! Turning off the printers? Wussies!

Well we’re not equal enough yet. Need many more crumbs.

There is no such thing as equality check communism Putin one of richest people in world dictators control military steal everything in sight that’s why we’re called peons

Ron is another one that believes Putin is stinking rich with loads of assets.

The same propoganda the Americans used against Gaddafi who didn’t even own his own house.

Has anyone seen Putin living it up on a super yaught, going to his mansions or using a fleet of executive jets.

Putin doesn’t need to because the state supplies him with everything he is using and hasn’t the time for leisure it would appear with his busy schedules.

I am not Russian but do get the impression that the west is actually becoming envious of Russia and the way Putin has transformed it after the Russian oligarphs were behaving like the American elites.

Cashboy,

Putin and his propaganda machine certainly want you to believe what you believe. It’s almost copy and paste. They did a great job.

In terms of other reports, they’re all over the internet. Just google it a little.

Yep, we all know that. The State Department has promised us to reveal how rich Putin is decades ago. Still waiting…

As to the “reports”, it is very lamentable that a financial analyst like Wolf would believe the product of “infowars”. But since he claims that these reports are credible, maybe he should write an article on how rich Putin is, in his view. Do a small valuation exercise.

DV,

The absolute last person on earth that I’m going to believe talking about himself is Putin. His propaganda machine is #1 in the world. Or maybe #2 behind China. You’ve been my comments buddy in Russia for years, so yes, you would say that.

Sorry J!

You’re soon Fired!

By Camilla BJ Harris 😎😎

I will get another term and print FOREVER!!!!!!!!!

Wolf..

in previous posts, I believe you said Blackrock only advised the Fed regarding commercial MBSs.

But is this true..?

:The date that Powell signed his latest financial disclosure, May 15, is noteworthy. It means that more than 45 days after the New York Fed had hired BlackRock to manage its commercial mortgage-backed securities program and its $750 billion primary and secondary purchases of corporate bonds and ETFs in no-bid contracts, Fed Chairman Powell saw no reason to avoid the conflict of interest of allowing BlackRock to continue managing upwards of $25 million of his own personal money.

According to a statement released by the New York Fed, BlackRock was retained on March 24 to manage the $750 billion corporate bond buying programs for the Fed. The commercial mortgage-backed securities contract was entered into with BlackRock on March 25. ”

from wallstreetonparade.com.

historicus,

Seems you’re hung up on Blackrock. And I keep having to say the same thing. The corporate bond program topped out at $13 billion, bonds and ETFs combined, not $750 billion, and was cancelled last year. It was run through big bond fund managers, a whole bunch of them, including State Street and many others, which applied for these contracts. I’m on the Fed’s email list, and I got these forms and notices that went out at the time. Blackrock was one of the bond fund managers, the first one because it’s the biggest bond fund manager.

It’s like the Fed’s primary dealers. The Fed works with large financial institutions to do its stuff with Wall Street.

Blackrock is a PD, up to their eyes in China, Soros called them out. What’s it all mean? Don’t tell me one Blackrock is not the other.

PD?

PD = primary dealer

This is a good time to point out, again, the fed is an insular organization. They only work with their own.

Soros and Kyle Bass are now both pointing out that investing in China, as they reportedly push, is dangerous. I urge all of you who believe to put all your money where your mouth is and invest it now in China, which desperately needs your money now, particularly if its US-dollar denominated debts become harder to service if US dollars cease being printed willy-nilly by the “Fed.” Read about its recent sales of its metals and oil reserves.

No doubt, having investments in China during its Cultural Revolution V. 2.0 will work out beautifully for you! LOL

At least, you will be contributing to the CCP members’ “common prosperity.”

Are you on the email list of the St. Louis Federal Reserve?

No, but the NY Fed, the SF Fed, the Atlanta Fed and the Federal Reserve Board of Governors. I think that’s all.

If it happens it’s hard to imagine all the falling dominoes.

Higher interest rates hitting stock and bond prices is baked into the cake.

Higher yields makes dollar stronger thereby making foreign debt denominated in dollars harder to pay off.

Businesses who borrowed short will be rolling over loans at higher rates.

Counterparty risk a la 2008, with a “Post-Lehman” system lockup and then in cones the Fed cavalry with TARP-like programs that will not help the little guy but actuallyhurt him. Who will know who’s holding bad paper, or rehypothecated good paper as collateral on something else that went south?

They should have pulled back on the reins a decade ago.

The songle optimistic sign I see is that just about every major bank seems to be predicting a crash now. I’ve been reading about investment firms bailing out for years predicting imminent crashes. I think Mish called a top 3 or so years ago.

I started following Mish mid 2007. Met him in person at local Chicago conferences a few times back then. When his economic analysis turned into a dud he reinvented himself as a social-political commentator, complete with clickbait topics and moat of toxic commenters.

Mish !!!

LOL

Isn’t this the wedding photographer who fancied himself an investment expert ?

THAT Mish ?

what Mish says is pure MUSH ..LOL

“When his economic analysis turned into a dud”

Just like every other analyst who disagreed with “Buy the dip no matter what. The Fed has your back” on the grounds that that made “markets” a joke because true price discovery is then impossible.

The successful “analysts” simply agreed with that mantra.

I am TRULY amazed at how long the central banks have been able to kick the inevitable crash can down the road. Like a vast spring compressed for decades, the stored potential energy for destruction is HUGE.

“kick the inevitable crash can down the road”

“There is a lot of ruin in a nation”…and the CBs are fully committed to finding out exactly how much.

Bingo.

is deflationary outlook never happened. The FED won.

So….

“reinvented himself as a social-political commentator, complete with clickbait topics and moat of toxic commenters.”

There are some toxic commentators on that board that are narrow minded. Not worth the effort .

Right. Robert Prechter and Harry Dent come to mind – they also had to revise their crash survival books :)

The Chicken Littles of finance along with Marc Faber.

And Jim Rogers has been very quiet about China for years.

Don’t forget your Sovereign Man Plan B or Doug Casey’s Galt’s Gulch in Argentina.

I don’t consider most of them crackpots. Fed policy has been a dud since 2008. No empirical evidence it helped the real economy as economic growth was anemic.

Let’s take the stock market at 3.5 price to sales when price to sales of 1.0 is the mean value. The crackpot is a crackpot til things unwind to the mean value or until government imposes capital controls that don’t let things unwind.

Yes, since broken clock is right twice a day, the value of prognostication of big change (a “how”) falls off quickly with the absence of an accurate “when” (as with all things financial). Of course our world will end; “when” makes almost all the difference. The Internet is full of people grifting off this portentious prophecy baloney. If it is useful, it helps limber up the mind.

Phleep,

The when can’t be known.

Only lessens from history and valuation estimates based on future cash flows can be determined. Everything else is guesswork.

@ Old School –

Newsflash – even “valuation estimates based on future cash flows” is guesswork. That’s obvious for stocks – economists and analysts demonstrably fail to predict both the future of the economy and the future cash flows of specific companies. But it’s also true for bonds, where the cash-flow part is fixed but the “value” part depends on whether the issuer stays solvent and how much money-printing/inflation takes place over the duration.

Wisdom seeker,

You are absolutely correct with two exceptions:

1. You can estimate fairly accurately a minority of stocks that have mature stable businesses. A lot of these would fall into the category of paying increasing dividends for a long period.

2. You can estimate fairly accurately the future earnings of the entire stock market.

For example the dividends paid by the SP500 can be estimated fairly accurately for the next 30 years. Sure it’s going to fluctuate a bit, but basically the dividend most likely will grow somewhere around the nominal growth rate of the economy over the long term.

If your long term estimate exceeds the return on a 10 year Treasury by enough say 5% then it’s a risk probably worth taking.

@MG

Did you just spell out all the reasons why it’s never going to be allowed to happen?

Nah, it’s easier to print money and get the MSM to scam the inflation stats!

This is the sequel to the 2008 debacle, and similar to what has been going on since ~1995- in various “strengths and flavors”.

In the early ’80’s, the powers that be (i.e. Fed, Govt and even private financiers?) decided it was time to squash the inflation problem. They did it with the famous deep/double dip recession. It was actually similar in depth to the 2008 recession (many are too young to remember).

Will they do it again – to get rid of the financialization/globalization bubble(s)?

If they just stand by while the markets tank ~50% again, I guess we’ll know the answer.

Keep in mind the classic trading rule that when everyone in a market expects something – something ELSE will happen.

When every bank is predicting a crash you should expect the opposite to happen. Ask yourself: Why would banks be generous enough to tell YOU to sell stock?

Psychological cues are often a major part of starting crashes. Your point on reverse psych isn’t wrong, however starting a major cascade of selling pressure requires getting the small and mid size guy to start selling. That way it becomes a feedback loop. The big institutional holders start buying at a determined point on the way down and hand back ever increasingly worth cash to the bagholders. At the end, the institutions own everything and can start the process all over again. They need the small and mid size guys to participate in the selling to create a feedback loop and legitimize that the bubble has indeed popped. It’s psych tactics to start a crash. “OMG .com is overvalued, everybody start selling! OMG real estate bonds are tanking, everybody start selling!” Etc. Hard to explain but hope that makes sense.

*worthless cash

Since the GFC in 2008. The players who saved the monopoly board have been saving the board with heroic lifeguard abilities. This convenient pandemic (forever perpetual seasonal flu) and zero interest rates has continued the Board game. And turned everything else into a turd.

The Public had nothing to fear in 2008 or 2020, Except for the “players”.

Hyper inflated equity valuations.

Over valuation list:

Apple 70%

Microsoft 50%

Amazon 60%

Google 65%

Tesla 95% (bankrupt within 4years)

Nvidia 90%

Moderna 95%

Real estate – propped up by federal program. MBS are worth zero.

This is Gary Yary opinion, not investment advice. Always think for yourself.

Thanks always for your dialogue platform and research Wolf!

Thanks you Wolf Street regulars for the back and play of ideas!

GY

I agree with you Gary

But I am invested in all of the above assets stocks because I know Fed has got my back and Fed has to cater to rich people

I am not rich though

Even the Fed members are deep into stock

Powell is worth $100 million or so mainly in stocks

Would would fed do anything that may screw their assets

You are still assuming that they can actually prevent a collapse. If that were true, why would we even work, create anything of value or pay taxes?

A decade ago nobody would have thought the current situation would be possible because it makes no sense whatsoever. But not (yet) collapsing has created this recency bias with an entire generation growing up with the idea that you can simply invent stuff out of nothing and there are no consequences for anything you do, because the central banks can and will backstop everything.

But this new religion, believe in omnipotent central banks, is exactly what will make the coming collapse so bad. And the trigger is not going to be “tapering” or anything like that. It is likely to be something that nobody is watching right now.

We are dealing with a complex system with many interactions. Nobody understands how it works. Chaos Theory teaches us that even tiny changes can sometimes bring a complex system suddenly into a completely different state. And this is what we see happening in the world (and nature) all the time.

As usual, hubris will bring us down.

@Y

Don’t get depressed you’re young, us oldies have seen and lived through worse before.

Focus on the real world which can be massively positive. Today Sergei Lavrov was pleased ‘common sense’ had prevailed as Russia and Germany, working together, welded in the final 200858th pipe to complete Nordstream 2 which will secure Germany’s continued status as an independent manufacturing superpower. Takes away Ukraine as a flashpoint for war and keeps Russia’s interest in co-operating with Europe (not the EU which is not Europe). Guess what! All these engineers will now be available to get on with their next project, which is probably to pipe gas to Eurasia, then watch that boom.

Financiers play with money, engineers build worlds unless they work for the military.

Don’t know how old you may be A, but at 77 I have NOT lived through ”worse” than what is becoming ever more likely to be coming soon IMHO.

MIL is 91, so did live through the ”great” or greatest depression so far in her childhood, and is set for the remainder of her life with three kids doing their best to take care of her diligently, keep her in the home she has lived in since early 1950s, etc., etc.

WE, the family WE, are OK so far, and likely to continue OK until and unless the us guv mint fails, which IMO is also becoming more and more likely with all the crazy, irrational, and irresponsible actions SO FAR.

WE, WE the Peons, (thanks Unamused) are very likely to be very very badly worse off both sooner and later IF the vast and really unknown ”financial instruments/assets” continue to grow versus ”real” assets, and continue to be used as weapons against the vast majority of We Peons everywhere.

If I were younger, even in my 50s, I would be looking to establish a ”homestead” type of situation, taking first consideration of my neighbors and only then access to water and the fertility of the land.

@VV

I won’t disclose my age because it could hurt my employment prospects, it does beat yours though.

I’m sorry if I was insensitive to your current anxiety, we Brits always think of Americans as prosperous and well-fed(very).

I don’t want to parody the classic Monty Python sketch of the old guys trying to outdo each other on ‘hard times’. All I’ll say is that, as a child, I was allocated a cardboard box with a gas mask which I used to scare my mates at school. I still hate the sound of prop planes at night.

In my reply to Yushan I had the UK 70’s disaster in mind, I could write a book, but how about over 15% inflation, no rubbish collections, no burials, petrol bomb street riots, etc. For me personally the worst thing was a long term savings account which dropped from around 175p to something like 34p in 1974. I was paying in around £100 a month and it was the one thing I determined never to give up. I discovered the magic of pound cost averaging and compound interest working together which served me well for the rest of my life.

My £100 a month was buying 5 or 6 times more shares. Dividends actually held up well, so they bought more re-invested shares as well, it showed as a big boost to the total number of shares owned. It took big sacrifices to keep up the payments but saving is the only way a working man can stand up to events outwith his control, and ownership of real physical share assets is also crucial IMO.

I would still say USA has a very, very, long way to go before your Treasury Secretary gets hauled off an aeroplane to negotiate an emergency loan with the IMF to prop up your currency.

Just sayin’ Cheers

I like what Peter Schiff said that original concept of central banker was to do triage in a crises.

1. Financial institutions that don’t need help- do nothing.

2. Financial institutions that are solvent but illiquid- loan at penalty rate.

3. Insolvent institutions- let them go bankrupt.

Throwing savers money at everybody is not the Fed’s job.

Yes, this was the normal state of things before 2008.

The days of Lombard Street are long past.

Once you give power to an institution, the original function tends to get lost but the power is preserved at all costs.

In Monopoly it is always good to hold the utility companies and have a get out of jail card.

They can’t taper or they would’ve already started. Does anything seriously think with their army of economic PHDs they don’t see the real inflation rate is 10 or 20% right now? They’re lying and trying to set policy and talk markets along the tight rope as long as possible, because once the taper actually starts, the stock and housing bubbles will unwind, bringing the pretend economy to a screeching halt. It’ll be too late to fight inflation or reverse what’s happening at that point.

The greatest depressionary collapse of all time awaits. Anyone thinking it’s normal to have imaginary pictures of rocks on the internet sell for millions of dollars doesn’t understand the psychological component of bubbles or how euphoria changes from one ridiculous thing to the next like spacs to crypto to NFTs. Buckle up, it’s about to hit the fan. And god forbid they actually raise interest rates with $30+ trillion in public debt. They won’t even get to 1% before doing a $25 trillion QE ramp into the heavens.

Every single NFT is either money laundering or one person with two accounts and a need for publicity.

G,

Do you mean to tell me that an “unknown investor” can buy a digital picture of himself, from himself , using illicit funds thereby cleaning the funds on the back side?

Damn that’s good… wish I’d thought of it…

As you get into a bubble fewer and fewer assets are priced off projected cash flows starting with the current earnings power and more and more things are priced on an optimistic view of the new future (EV, crypto, SPAC, IPO, green economy, NFT). All are speculations until they demonstrate they give a decent return on capital).

There is nothing wrong with speculating, but you shouldn’t count on it to provide your future needs.

The depression that’s going to hit will catch most of us by surprise.

“What !!”

“Turn of the tap.”

“Have you gone mad !!”

“Yesterday we were beggars & look at us today, we want for nothing.”

“No, no, no, no, no.”

“You always were a bit strange, now you are insane.”

M,

My rule is that sometimes you gotta show a little crazy…

Keeps everyone around you more honest…

That rule didn’t work in my family , though… they were already whacked…

COWG:

“….sometimes you gotta show a little crazy…”

Nixon tried it! (Hear his dialogues with that other “crazy” Kissinger)

“Does anything seriously think with their army of economic PHDs they don’t see the real inflation rate is 10 or 20% right now?”

They don’t just see it, they LOVE IT. They are trying to inflate away the debts and permanently distort asset prices. The problem with that plan is they continue to encourage new, bigger debts, so their plan can’t work and will blow up spectacularly. These guys are focked and they know it.

Janet Yellen didn’t see the housing bubble while a Fed governor with her big staff Phds. Took some street smarts to see it. Fed is outmatched in the real world financial markets.

Feature, not bug.

Nah. They see it just fine. They just lie about it and say “nobodycouldaseenitcoming.”

Old School- yes, Yellen, Bernanke, Greenspan- you can do an internet search and find all of them on video saying things were not risky. You can also look at some of their personal history of buying and selling their personal residences. They bought into bubbles (as did Treasure secretaries).

I don’t mind people being wrong except when they assure us that they and their PhD army understand and have everything under control. If they would take action more as if they didn’t know everything, the markets and economy would do better.

Perhaps the Fed hasn’t tapered because they want stocks and RE to rise another 100% before the crash. Current price levels are then more likely to be a floor in the event of a crash. It’s not much of a strategy to cling to, but the Fed is desperate at this point.

That is an interesting idea Bobber.

Forgive me all but I do sense there is no immediate short term danger to a crash. Remind me if I’m wrong soon! : ) I don’t even think it would be in China’s interest to spark something now… Still going up… To infinity and beyond (did I get it right?!)

Top floor please.

Hey you up there in heaven, here we come.

Bobber

I would agree. Assets have been “overvalued” since 2009. All the QE from 7-11 years ago had not run its course before we doubled down (or more) in 2019 to today (and continuing).

It could take decades for assets to normalize.

Schiller earnings yield is 4.2%. Ten year Treasury at 1.3%. delta of 2.9%. Textbooks say equity risk premium about 3% so relative valuations not that far off, but future returns in USA look horrible.

I’m seeing more like 2.5%. 100/40. Where are you getting 4.3 from?

Yep. You are right. The 4.2% is just current earnings yield.

Wolf,

You forgot the most important player and signal of all. The Fed is signaling the end of QE via media… see latest from Kaplan and Rosengren decision to sell all of their individual stocks ahead of September 30th. A sure sign that the taper is coming. The rest of the people in the Fed have surely gotten the memo by now. The taper will start sooner than expected.

They pledged not to trade stocks while they remain Fed presidents and will only put proceeds in passive investments, do you think that applies to shorting the market via puts on ETFs like SPY and QQQ? Technically, that’s not trading a stock, it’s a derivative…. Alternatively, short ETFs like SQQQ are technically passive….

:) There are loopholes for everything

Yeah that’s what I thought too when I saw those Fed monkeys selling their stock. But I’d be more confident if Madam Speaker were to do the same thing.

You will find out three months after the man has made his money through his insider knowledge.

Oops sorry, didn’t mean to imply our unimpeachable speaker would do anything bad like that. Not like that jerk off Ryan…. AKA SPAC boy that’s not as buff as Chamath.

Y’all got the memo, right? I told my homies to sell!!!!!!!!!! Even that super dove Kaplan! Throw your hands up in the air baby!!! This rollercoaster is on the way down!!!!!!

Throw ya hands in the air

An’ wave ‘em like ya jus’ don’ care

My name J-Pow and I rock the Dow

Everybody say “oh yeah!!!”

They may sell individual stocks but they d buy etf or keep etfs.

Etfs are nothing but comprised of stocks

So its a wash

I see the popularity of index ETFs as a systemic risk. If some components crash and therefore negatively affect the price of the ETF, many people will (try to) sell their ETF which then leads to indiscriminate selling of ALL components. And some of these components can be illiquid too, amplifying the move.

What if retired boomers suddenly realise the game is up and want to sell their ETFs before it is too late, after a 6.7x price increase since 2009? That seems like a pretty easy decision if you have only 10-20 years left to live. Why keep risking it at these levels? And who is going to buy their stocks then? Zoomers and Millennials who still live in their mom’s basement because they cannot afford a home? Besides, they rather buy Bitcoin.

Narrow focused ETFs are a problem in my opinion as you can get problems if there is heavy selling.

Corruption plain and simple

But, but, but .. I heard that AI capacity computers run the .. never allowed to fail system .. will AI even let the system hiccup .. let alone fail ??

Turning The Free Money Tap Off.

The RBA of Australia are tapering ..

Are You Sure ??

Australia’s PM has not done spending yet .. this is after the several trillions of FREE dollars he has already thrown in to the wind.

In Australia .. the media is being utilised to get the COVID message across .. main stream media time is not cheap nor is it FREE .. it costs big money & none of it was for free to the PM & his pandemic collaborators .. who shamelessly paraded their prowess .. day in day out.

Then there is the corporate world .. who have been supported like the lazy .. drop in guest brother in law who has an aversion to work.

Then we have the W.A. Premier .. Mark McGowan who delivered a $5.6 billion budget surplus .. tucked in the premiers back pocket.

With respect Mr. Richter .. I do believe that someone has told you a lie.

I suspect many .. I’m not saying who .. fear the prospect of some real jail time .. down here in the banana republic.

Maybe central bankers know the risk of asset values increasing another 50% is destabilizing and as long as they keep rates below inflation they have given fiscal policy the free money to keep deficit spending.

I don’t think they will taper due to Covid being out of control in the US. Even with today’s vaccine announcements there is at least a 2 month delay in improving infection numbers.

Then there is the debt ceiling machinations, the proposed 3.5 trillion package, and the divisiveness about everything, even basic facts. I don’t see things improving at all. The Fed is in a corner and screwed no matter what they do. They left it 6 months too late, maybe 3-4 years too late. They were bullied into inaction and the price will be paid in economic disarray.

They left it 10 years too late. The ECB got it right initially and started to raise rates in 2011. But they reversed course because less “growth” and went full retard since 2015.

The Bank of Canada had to taper or everyone will be priced out of the rental market meaning no new immigrants coming to Canada due to the sky-high cost of living.

Rent is set by wages. House prices are set by available credit.

Rent is set by income, and often by government payment, neither of which in many cases has anything to do with wages.

Yes unemployment benefit and other “help” is a direct subsidy to landlords, that the regular economy cannot meet. It artificially lifts rents, allowing freeloading bankers and landlords to leech.

I would have assumed the addition of demand and location in there as well…

Hose prices might be set by available credit as long as they are going up, but once they start declining available credit doesn’t matter much until a bottom is put in. Who is going to leverage up a declining asset?

The decline will begin *because* available credit falls.

“Hose prices”: love it, Everything Inflation, added to my classics on WOLF STREET.

Was it a taper or just a slight nip & tuck ??

We could add a new definition to ‘botch-a-lism’! A monetary reaction caused by weakness, blurred vision, and trouble speaking! I never thought of comparing the FED to a disease before, but they’re both certainly toxic!

In the UK, the immigrants come foor the free housing and benefits the government gives them.

So the UK is always desirable for them.

I wuld think Canada was the same.

The Fed and bankers are currently preparing an end strategy for themselves. For the past 25 years, they have brilliantly stacked the deck to profit themselves, if the middle class raked in a few peanuts, it was ok.

We see now the pandemic was and is a blessing for the rich to make money because they could change the rules as needed, spend the country’s cash as needed for a fast return to themselves. If a crash happens, it’s not so much about making money, but control, and someone will come out on top. When all the debt defaults, Fed-backed banks will be everyone’s new landlord.

Time for a deck of cards like in Iraq

This is basically why I disagree with those who say “the Fed can’t raise rates”. They can and they will.

And it will hurt the markets (most of which are vastly overvalued to begin with) but that is ok because everyone “in the know” will be positioned short so they made bank with the market/assets going up and they will do fine with the market/assets going down.

The “retail investor” will take it in the shorts as in 2000 and 2008. Nothing new here. You’d think more people would opt out of the game.

Fed is betting the $ being the reserve currency will compensate.

Mark my words, this is a small slowdown before the next vertical acceleration , remains to be seen what the trigger will be, a 5% stock market plunge or another variant of the virus.

More great charts from WolfStreet. Tapering has started in most countries and the Fed will have to taper soon. The likelihood of any of the charts turning down significantly and the size of central banks’ balance sheets returning to pre-pandemic levels is very low. The debt monetisation is permanent.

I agree….the risk of high inflation is greater than any deflation…or should I say less inflation?

Too much debt in the world to let any type of deflation take hold. Deflation would be a really bad event.

This will only become meaningful when:

1. they totally stop QE

2. they allow interest rates to rise

3. when rates do rise housing prices *will* tank

4. when housing prices do tank they continue to let rates rise

Until I see that, I don’t believe it.

You know why I don’t believe it? Because of everything that’s happened since 2000.

The Fed hiked interest rates and reduced its balance sheet until Trump trampled on Powell publicly and repeatedly. Biden isn’t going to do that.

If FED is independent then why did Powell give 2 hours to what Trump was saying?

Why do you think Biden wont do that? How about Pelosi and gang, will they do it? Why or why not?

Only Trump could pull that off with such consistent panache after having called for higher rates during the campaign (the fake interest rates, fake markets). He bullied Powell, day-in, day-out, bullied him in the worst way. And the media ate it up. No one else comes even close to this kind of talent.

Your sycophancy disgusts me. Excuse me while I go vomit.

Obama+Biden had 8 years of zero interest rates from 2008-2016. Yet you utter not a single word about it.

Trump got hit by the psycho fed that did a 180 degrees so fast heads started spinning.

Rates went from 0.25 to 2.5.

Balance sheet went from 4.5T to 3.75T.

Yet you turn a blind eye.

Nacho Bigly Libre,

This whole discussion was about whether or not Biden will be able to do what Trump did with the Fed. I have no idea what you’re reacting to.

“whether or not Biden will be able to do what Trump did with the Fed”

Biden is not put in that position at all. Where are the rates today?

Trump improved the economy, Fed responded by increasing the rates and reversing QE. Biden printed trillions and still enjoying near zero rates and QE.

Clear?

Nope. But OK.

Ok, let me try one more time.

All politicians love low rates. Obama/Biden were never put in a position where they had to deal with high rates. When Fed is not getting in the way of him spending trillions of dollars why would Biden complain?

Aren’t you the one saying Biden will beg the Fed to raise rates? Ever wonder why that hasn’t happened?

Until then please save your “Biden isn’t going to do that.’

Why would the Fed cave in to Trump? Wasnt the reason for reversing the taper that the markets started to fall apart?

I think the economists at the Fed are seeing they have backed themselves into a corner and dont know how to get out of it. They were unwilling to admit that we cant use monetary policy to get out of this, we need a new economic policy.

Everyone keeps saying that the Fed will hold down interest rates, but how can they keep long term rates down if they cant increase asset purchases, but need to raise a ton of money with the sale of bonds once the debt ceiling is raised?

I see economic chaos coming after that debt ceiling raise. And if they dont raise the debt ceiling but go into default that creates another whole mess.

Maybe the FED caved in to make it look that Trump had hair on his chest.

“…they have backed themselves into a corner and dont know how to get out of it.”

Traders understand that getting in and then getting OUT must be considered BEFORE one puts a trade on.

These academics in the central banker arena only know how to “get it”……

Bernanke in a WSJ article in July of 2009 outlined how the end of QE would occur…..roll offs, etc. Sounded wonderful and level headed at the time. The opposite occurred.

@gtv

“they cant increase asset purchases,”

Why not?

They’ve got about a trillion of asset sales coiled up in RR’s so tapering is just a PR game for the MSM pundits.

Technically you could argue that building up those RR’s was much more aggressive tightening than it would be by just gradually winding down asset purchases. These RR’s are there ready to fund future treasuries whenever Congress drops the flag. The treasuries can be funded by running down the RR’s while, at the same time, the Fed can taper QE. They might even have enough ‘juice’ to sell some assets. IMO

just sayin’

Yeah I seem to recall a “taper tantrum” on Wall Street.

Lol. Good one, Wolf. Am I reading The Onion.

Won’t believe it until I see it. Clinton. Bush. Obama. Trump.

Every leader has been useless, for two decades.

If Trump was bullying Powell, he could/should have quit.

Volker reportedly quit in ’87 because the administration (and others) insisted he keep the party rolling. Volker wanted to slow down the train. He didn’t and we got the ’87 crash (the last real crash).

Neither political party responsibly discharges their duties when it comes to the economy. However, I think one is a little better (or could be) than the other. A large fraction of one party literally believes that money can be printed forever without consequence. The other party believes money can be printed for a long time without consequences. Forever is worse than a long time.

If you knock out a 4 trillion dollar hole in a stock market crash you will quit hearing the BS that cash is trash. The margin call will flood the market with homes that were speculated on using a primary residence as seed money. The panic covering will be entertaining to watch. Massive Deflation will follow with a left hook on anything leaverged. This bitch of a market can only go straight up and it has to go fast to Dow 80K and 1 million dollar median homes and $200k F150 trucks. It can not dither in stasis. Geometric progressions is the bitch that even the Fed can not step in front of and Wall Street can’t front run. This is how fiat debt notes die. It is coming and no one knows when. Wrap yourself up,in a cozy cognitive dissonance blanket while you hit the buy button if you think otherwise. If you lose 50% of what you own free and clear you will still have 50% left that is free and clear. I will take my debt free 50% and be thankful I have it.

DR DOOM

You state

“….This bitch of a market can only go straight up and it has to go fast to Dow 80K and 1 million dollar median homes and $200k F150 trucks…”

Yet you state having 50% value of something you own free/clear is better than ???

I gather you opine all the $$$ injected into our economy will somehow stop inflating assets or at least maintaining the status quo ? What exogenous event could make this happen ?

Beardawg. If you own your home out right and are sitting on 200k in cash and a you wake up one morning and your house lost 50% of its value on paper and your cash has been de-based by 50% you still have your home and 100k. So what? You woke up alive, debt free. As far as whether we have deflation or inflation or stagflation and to what degree I have no idea . The only thing that I have a shot at controlling is not going into debt.

DR DOOM

Thanks for the clarification. I am a debt-free’er myself and the lack of stress associated with that has value for sure.

I still do not see ANY exogenous event which could de-value any asset by 50%. Even if that did happen, as long as the debtors continue paying the debt with inflated fiat instead of relinquishing the asset(s), the debtors win. Unless someone must sell an asset (land, home, equities) for a medical emergency or something, there really is no downside to “borrow and invest” until all this QE gets through the belly of the snake. That looks like decades right now IMHO.

Beardog,

There is a principle in financial markets that most of the time the bigger the bubble the bigger the crash. Stock valuations are in the once in a hundred year valuation level so it could be that we go to the once in 100 year on the down side or around 85 – 90% loss.

Same for interest rates being at all time loss, they could spike to all time highs. What seems to be impossible in financial markets tends to occur.

LOL….it might be better if you only had 5% equity in your home and a big mortgage if home prices dropped 50%? In this country….you just walk away from bad debt?

But cash and a home will not drop at the same time. If cash gets devalued by 50%, your home will go up 100%?

You guys imo talk as if the world is ending. As if a big reset is happening soon yet the date or can is pushed down the road and never happens. Not disputing this but a 5 to 30 year future event means not much at all at the moment. What I never hear from you guys is a housing or stock prediction for 6 months or 1 or 2 years from now.

Red

I concur. It might take decades for all this QE (which has not stopped yet) to filter through and manifest in a leveling of asset prices.

I will take the Warren Buffett side of this. Anyone that says they know what the stock market is going to be in 6 months or a year is fooling themselves. You must have enough cash not to have sell at distressed prices.

Red. The world ain’t ending. To the contrary if you are debt free it could be a new beginning. I bought property with cash in 2010 that was driven up then collapsed in the house mania loan bubble. I sold it a few years later and made 20%. When you get Easy money Never get Greedy. The point is being debt free gives you the peace of mind to sit back without worry and pick out your next opportunity. No one knows what will happen when,where and how.

Just don’t make the mistake of the great depression when the market dropped by about half some bought and it went down another 65% or so for a total of 89%.

Yep, you had several opportunities to buy the dip all the way down. There were several rallies. As some wise sage (or maybe I read it on a beer mug) said, nothing goes to heck in a straight line.

I wouldn’t put five cents into the housing or stock market right now. Maybe by the midterm elections, next year, I will change my mind.

The question at hand is who wants a crash? And do they have more money and influence than those who don’t want one?

Petunia

The game is rigged for sure, but the rules are open for everyone to see. Choosing not to participate based upon ideology / pride could be perceived as foolish ? Sitting idle right now has one moving backwards on the tracks somewhere between 5-10% annually, depending on which stat lunch you choose to feast upon.

The market is as seductive as anything, especially with Fed being a tail wind. You can’t be like Isaac Newton and make mistake of selling out at a nice profit and then going back in and getting wiped out. The easy money was made from sp500 from 666 to about 2500 or even 3000. Any money made now is Cinderella having a good time, but risking everything by staying too late at the party.

“As long as the music is playing, you’ve got to get up and dance” — Chuck Prince, destroyer of Citibank

“Chuck Prince famously said we have to dance until the music stops. Actually the music had stopped already when he said that.” — George Soros

I really though there would be some hard times as we were approaching Housing Bubble 1. The FED nipped that disaster in the bud and we only had 2 or 3 quarters of deflation when Trillions of dollars of debt was suddenly determined worthless.

Now with covid, they can print money in a second. From 2009 until now we have seen so many new financial engineering ideas pop up I sort of believe they may have hundreds more?

ru82,

What we now have that we didn’t have back then is a massive bout of inflation that is threatening to spiral out of control as monetary and fiscal stimulus continues. And the Fed can see this too. So the Fed is going to try to deal with this inflation at some point, whatever stocks are doing.

So true on your inflation statement. The FED and all the CBs really opened the firehose this past 1 1/2 years.

It will be interesting to see what their plan will be to reduce inflation. Grab the popcorn!

Come to Australia & have a look around, you are all velcome .. in Australia everyone is a wirgin .. you don’t believe me (??) come & see for yourselves.

Inspired by the video Willkommen – Youtube .. from the brilliant musical Cabaret.

People I trust tell me Australia is one giant jail.

Eh, returning to their roots! :)

LOL!

I hear they’re considering a law where politicians go to jail as soon as they’re elected.

Even worse Pet, they now are arresting folks for having more than 6 beers per day,,, and/or ”confiscating” the brewskies!!!

Wonder what’s happening to those brews???

This would be an absolute deal breaker for many folks,,, and coming from a political entity who claims to want more immigrants certainly puts the doubts on that, eh

I just learned Japan stopped the sale of alcohol in restaurants back when they put in covid restrictions. Some restaurants closed over a year ago and haven’t reopened. I can’t imagine why this was considered necessary.

The ECB is quite a different animal from the rest of the bunch. The newest kid on the block where the monetary Dracula’s delivered their final creature after they went completely nuts, if you will.

Frankenstein, Godzilla and Nessie (that would be Mrs. Lagarde) combined.

The real “biggie” is not in the alphabet soup of crazy stuff, but in the TARGET 2 balances. There was a brilliant article by Alisdair McLeod on Zerohedge (just about the only person in the world that really has a clue, it seems) about that.

And that will go on until the EU implodes. Which has operationally already happened in the “pandemic”. It’s just that nobody yet noticed.

The ECB played that one brilliantly. Draghi made the cost of a breakup so expensive for the paymasters (Germany, Netherlands etc) and this way basically created the fiscal union that democratically elected governments would never sign up to.

This defacto fiscal transfer is explicitly forbidden by all relevant treaties and even goes against the German Grundgesetz (kind of constitution). The last word hasn’t been said on this yet, but the juridical process is so slow that there is no way back anyway because nobody would dare pull the plug now.

In my opinion, what the ECB did is nothing short of a coup d’etat, sidelining democracy. The central bank must be independent and cannot be criticised by politics. HOWEVER, it is exactly for that reason that the central bank’s mandate must be extremely limited. In case of the ECB, that means inflation only (as was defined at its creation). Keeping countries inside the eurozone is NOT the mandate of the ECB. Nor is financing government and corporate debt, “green policies”, etc. All that stuff must be under democratic control.

Ideally, we should simply have sound money, which doesn’t require any central bank. But that is another story.

Fed governors personally and the Swiss National Bank played the central banking policies very well….”almost” like cheating, having the answer book.

Maybe “almost” is the wrong word

“Brilliant” is not exactly the word that comes to mind.

“Completely insane” is more like it.

The key paragraph from the zerohedge article:

” all the national central banks will have to be bailed out on a TARGET2 failure, presumably by the ECB as guarantor of the system. But with only €7.66bn of subscribed capital the ECB’s balance sheet is miniscule compared with the losses involved, and its shareholders will themselves be seeking a bailout to bailout the ECB. A TARGET2 failure would appear to require the ECB to effectively expand its QE programmes to recapitalise itself and the whole eurozone central banking system”

If anybody is looking for complete modern monetary madness, this is it.

The costs are effectively shifted towards the taxpayers in northern countries. Their central banks will end up with a shortfall when this thing falls apart.

Tax payers are ultimately backstopping central banks, not the other way around, as most people seem to think!

Why? Because central banks cannot create anything of value, but governments have access to value by means of taxation. This ultimately dictates the limits to monetary policy.

Base money is created by the central bank by buying government bonds. So the money printed is backed by something that has value: government bonds. Why do these bonds have value? Because the government can extract real value from the economy by means of taxing real wealth and income – but only up to a point. When making good on the bonds by means of taxation is not credible anymore, then the money also loses its credibility.

At this moment people are fooling themselves thinking that bonds (and thus money) is still credible because the government can borrow at such low rates. This is a circular argument. The whole thing can therefore blow up literally overnight.

This for FB and YS:

Thank you both for your input on this very very important subject, the base of which illustrated and explained by Wolf to start with, as usual:

As a certifiable elder these days, who got OUT of the SM in the 1980s due to perceptions of crazy corruptions arising from ronny ray gun’s clear distortions/lying distorting all rational investing as I had been doing since the ’50s,,, I am currently only in cash and RE, with returns on the latter more than making up for losses in the former, for now…

Literally ”studying” on Wolfstreet.com to try to figure out IF to get back into SM,,, and, more importantly, WHEN…

Thanks again,,,

I was surprised to read that gold only makes up about 1/2% of people’s assets overall which is below trend. I just recently surpassed 1% if you include silver so I can understand that it’s not so convenient to do.

Anyway you would think with so much printing there would be more of a run to gold. It will be interesting if it ends like Mississippi bubble where people exchanged gold for worthless stock shares.

Well located single family homes are the gold.

Well located single family homes with ample nearby water sources are the gold, none of which are in SoCal.

Old School. My grandfather love to come up behind me while I did homework on his old glass top desk and toss a gold eagle on the glass and sing out ” that’s the sound of eating money son” and then expertly swipe it off the glass. He had 5 oz of coins for every one in his household ( including ol’ Sam the Blue Tick) . He said that’s what Mr Roosevelt said We could have . The 5 eagles per person still works today and is what gold is for to the every day man . Eating Money.

While the “citizens” may want to break up the euro zone, China and Russia are helping to keep it together. Both now need the euro as fx and their holdings are growing. The US may need to start a campaign to break it up to prop up the dollar.

Bullshit.

Russia and china combined and the rest of the shanghai cooperation leave “old europe” in the dust. Payday has come. Revenge is a dish best served cold.

The only reserves of russia and china that are growing are of the shiny yellow stuff. The real shiny yellow stuff.

Why have central banking at all?

From history it looks like central banks are needed to make sure if things go bad the government survives as long as possible and you are left with worthless paper. It was tougher when they had to come to your house a shake you down for your real money.

Franz Beckenbauer,

I started writing about the Target 2 balances in 2012. They were already huge back then. Now they’re huger.

On WOLF STREET in 2012:

Now, 9 years later, the Bundesbank’s receivable under Target 2 = €1.02 trillion. And still nothing has happened. Maybe someday…

That translates into 1 trillion of non-performing loans ( read: dog shit) stuffed onto the balance sheet of the completely under-capitalized ECB in an economy of 20 trillion with a highly leveraged, insolvent banking system.

Oops.

Got gold ?

“What’s taking the Fed so long?”

Have to laugh…

They catch a few Fed Governors that have “invested” with TREMENDOUS insight….so they are to “divest” themselves……at what could be the TOP!

What a penalty.

Central Bankers make sure ..

all charts move from low left to upper right.

So now the central bankers are going from “way too much” all the way down to “too much”

As long as chicken little doesn’t have to cross the road in order to get free money, everything will be ok.

The Fed is getting ready to go “Woke” big time with the appointment of Ms Brainard to replace Powell. The first think to look for is for the Fed to “nationalize” all the outstanding student loan debt and take it off the books of the major lenders. They will buy off the debt just like they are buying MBSs. This will essentially “BUY” the votes of all the millenials in the next election cycle. The banks will be happy too because most of these loans are in default and they won’t have to write them off.

So when that gets done, what happens to this millenial who:

– Has privately held student loans (refinanced pre-covid to get the interest rate down)

– Has been paying rent and loan payments this entire time?

Moral hazard is real and exciting.

(Also, just as a data point, I know of at least two people at my job who used the money they’ve saved from not having to make loan payments during covid to get a mortgage on a house.)

2 bold predictions. Student Loan Debt writeoff might happen, but I don’t think such a brash move is politically viable. Perhaps accelerated forgiveness tied to an employment component, but not straight up one fell swoop forgiveness.

Bear,

This is an example of extreme tone deafness. If millennials had jobs, never mind jobs that paid well, they would be paying their student loans. And not living at home.

Giving money to people with money is what they resent, because it is inherently unfair. You seem resentful of helping those that really need the help. Those for whom the economy is not working.

I have a millennial at home, and yes, he would sell his vote for loan forgiveness, and I would encourage it too. Why the hell not, it’s the free market, right?

Petunia,

Facebook, Google, Microsoft, Apple, Amazon’s tech divisions, Twitter, all kinds of moneyed startups, and just about all tech and social media companies are stuffed to the gills with millennials, including at executive levels, and some are run by millennials, and they are making a lot of money and have stock options, etc., and they could easily pay their student loans.

Petunia

I enjoy the discussion. I am in fact completely deaf in my right ear (Meniere’s Disease) – but as a musician and a lead vocalist, I need near perfect tone – and I have it – so you might be half right. ;-)

I have a Millennial myself. She availed herself of the UE bennies (rightfully so – she is a massage therapist). She lives on her own with my granddaughter. She pays all her bills, including rent, which was achievable with the UE bennies. She no longer has student debt, but if she did and it was offered to be forgiven, of course she would take that deal – so would I. If it were contingent upon her remaining employed but forgiveness was accelerated connected to employment, she (and pretty much everyone I would estimate) would see that as fair??

My comment RE the “political” ability to sell full-on forgiveness is NOT a statement about rich v poor (i.e. class status quo), is not about a dog I have in the fight. It is about what politicians can get away with. I don’t think any legislator (D, R or other) would curry favor with the majority via wholesale forgiveness of debt with no conditions. Even the bailed out banks have stress tests (now).

Wolf,

I think the universe you cite is tiny and doesn’t reflect the reality of the average millennial. I know millennials in tech and none are making big money. Some have two jobs and almost all share living spaces. And they are among the better off ones.

From my view the salaries are ok considering the alternative. None make anywhere near 100K, most make between 40-70K, and they are desperately trying to pay off their student debt. Bonuses and stock options are a promise, but no cigar.

Petunia,

Yes, of course. Totally agree. What I was saying is that blanket student-loan forgiveness or even blanket forbearance is nuts. Debt forgiveness should come when the debtor cannot pay. In credits other than student loans, this is handled in bankruptcy court.

We ought to create special student loan bankruptcy courts to let judges decide who cannot pay off a $50,000 student loan over 10 years. So if you can pay for a $60,000 new vehicle with a 7-year loan, you shouldn’t get student loan forgiveness. But if you’ve got an MA in history and are working at an Amazon warehouse because that’s all you could get, and you have $50,000 in student loans, I think a bankruptcy judge would be in a good position to rule how much you can pay per month, or what percentage per month, for 10 years. And the rest is forgiven in this special federal student loan bankruptcy court.

And then we need another law that allows the government to claw back tuition, room & board, fees, and textbook expenditures from universities and textbook publishers for every student whose student loan was dealt with in this special bankruptcy court. This way, the parties that generated the costs for the student loan have skin in the game.

Bear,

The student loan payoff benefit your daughter received was earned compensation. The company chose to pay her that way but she still earned it with her labor. I don’t consider that benefit loan forgiveness in any way. No benefit is given, it is earned.

Petunia

The deaf part of my being may have kicked in. I guess I am not following. My daughter earned compensation from working a job (after schooling ended) and paid off a separate contractual debt (student loan) with those earnings. She did not receive a “student loan payoff benefit” from the lender, unless you consider the lender making the $$$ available to her when she needed it a benefit – which I guess it was. OR – that the loan allowed her to gain skills which allowed her to earn at a higher rate?

Yes -that is also a benefit. The lender did NOT forgive the debt, she paid it off in full.

Back to my original point. If in the near future she hypothetically still had student loan debt and it could be completely forgiven if and when she is employed under some new accelerated student debt forgiveness program – that sounds like a good deal for everyone. My daughter is productive (society benefits) and debt is forgiven (which benefits her personally).

Wolf,

Seriously, what pct. of the “millennial population” works at these companies? I would guess less than 10%

Bear,

I misread your comment and thought your daughter received student loan payments as a benefit at work. That is actually a thing these days, the employer making payments towards student loan debt. Those payments are compensation earned by the employee even though the company is paying on the loan.

Hope this clears up the confusion.

I may be old school, but I saved money for my kids college education in a 529 fund. When it came time for them to go to college I used the funds in the 529 which was in their name to pay the tuition and room & board. I had to kick in additional funds to cover the shortfall. Since they were dependents they were on my tax return as a deduction.

I’m surprised at the number of comments and excuses for parents and the millenials not paying school loans, and asking someone else to pay the kids bills. What a disgrace.

Petunia- you are right about the macro view of the millennials. It’s not really a “generational cause”, in my view, however. Everybody in ~ the lower 50% (maybe 35%?), is paid too low because of globalization of labor markets. Millennials land in that group because they have less experience. If nothing changes, the millennial income distribution stats will look like every other generations in this dysfunctional employment market.

There is a fundamental misunderstanding of the details of the lower skilled job market. It is much more dynamic/fluid. People can go from one skill to another because it takes a shorter period to gain the skills and credentials to do these jobs. If a job in another skill/field is impacted such that pay is lowered, most all other low/semi-skilled jobs will also be impacted.

See the Hay Point system. They benchmark jobs in widely varying skills to come up with a pay guide. If plumber salaries start to fall, so will auto mechanics, etc. Many (most?) large corporations follow this type of salary bench marking.

It will happen in some form.

I have seen too many twenty somethings posting student loan forgiveness on social media. The politicians will read this and go after those votes.

I told my kids it’s ok to not go to college until they figure out what to do so they don’t go into debt for a useless degree

What do the numbers tell you? How many students at what ages have forgivable federal loans? How much would it cost to buy those votes versus another strategy?

That’s all it comes down to. I think the numbers are not yet in favor of student loan forgiveness (yet), but who’s to say that strategy won’t work in 2024? Or 2028?

Right now it appears to not be viable but perhaps in a few years it might.

My vote is for sale for any politician that can can nationalize healthcare. I just got the breakdown for having a kid at the ER for 3 hours due to food poisoning. Over $12,000 total. First saline IV charge for 1 liter was $1,077.50. I had a family who works as the hospital pull the actual hospital price for purchasing the 1 liter saline IV…it was $3.30. The antibiotic single pill charge was $787….hospital paid the drug company $1.34 for that same pill. The anti-nausea pill cost us $82…hospital paid $0.24.