The housing insanity “softens.”

By Wolf Richter for WOLF STREET.

There are now all kinds of reports that the Canadian housing market – the #2 housing bubble in the world behind New Zealand’s – is “softening” or “decelerating.” Today, Statistics Canada added to that notion when it reported that new house prices increased by only 0.4% in July from June, the slowest price growth all year, with prices in Toronto up only 0.2% and in Vancouver up 0.3%. This is what the current notion of softening means: Prices are still rising but at a slightly less crazy rate as demand has backed off and sales volume has dropped. Sales of existing homes in July had dropped for the fourth month in a row.

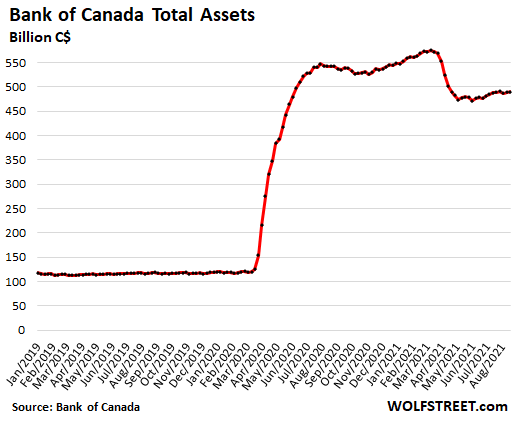

In recent months, the Bank of Canada repeatedly cited the craziness in the Canadian housing market which formed a historic spike as a result of the Bank of Canada’s no-holds-barred asset purchases and interest rate repression.

So the BoC started tapering its asset purchases last October. It stopped buying mortgage-backed securities. It stopped buying provincial bonds. It shed most of its holdings of repos and Canada Treasury bills so far this year. And in three announced taperings, it reduced the amount of its weekly purchases of Government of Canada bonds, from C$5 billion per week last year to C$2 billion per week currently. The overall effect is that the assets on its balance sheet dropped from C$575 billion in March to C$490 billion currently as of today’s balance sheet.

And there may be some signs that this tapering by the BoC has started to remove some fuel from the housing market – that “softening” that folks have been reporting.

In July, the Teranet-National Bank House Price Index rose 2.0% from June. That’s still a massive jump – 24% annualized! – but it was down from the jumps of 2.7% in June, 2.3% in May, and 2.4% jump in April. And year-over-year the index was still up by 17.8%, the most on record.

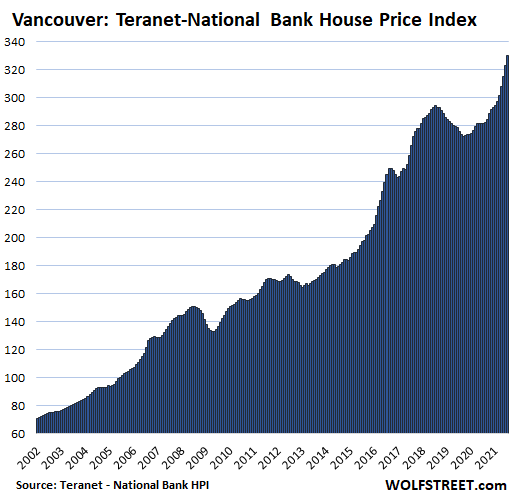

In Greater Vancouver, house prices jumped by 2.1% in July, a “softening” from the jumps of 2.7% in June, and 2.3% in May, for a year-over-year spike of 17.1%. The BoC’s no-holds-barred monetary policies starting in March 2020 flawlessly turned around Vancouver’s housing downturn that had started in August 2018:

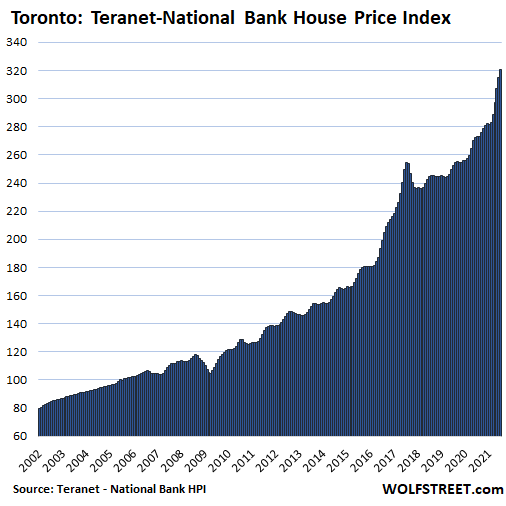

In the Greater Toronto Area, the price spike “softened” to 1.6% in July from June, the smallest jump since February, after the spikes of 2.7%, 3.4%, and 3.0% in the prior three months. Year-over-year, the index jumped by 17.4%. Toronto too had experienced a decline in house prices in 2017 followed by not much action until the BoC went hog-wild:

The Teranet-National Bank House Price Index uses the “sales pairs” method, similar to the Case-Shiller Home Price Index in the US, comparing the price of a house that sold in the current month to the price of the same house when it sold previously. It tracks how many more Canadian dollars it takes to buy the same house over time, and it now takes a heck of a lot more Canadian dollars than a year ago, just house price inflation, which is what the BoC has fueled with its radical policies.

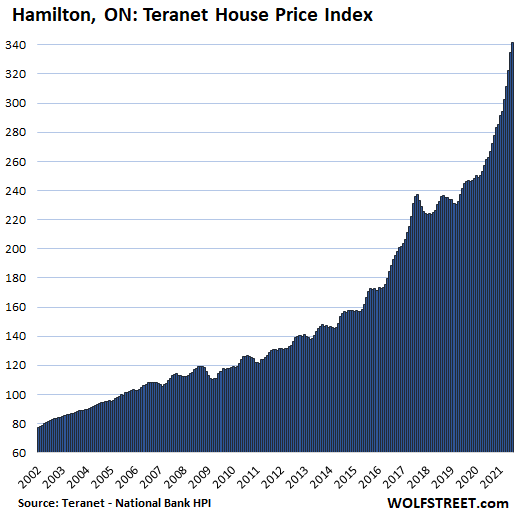

In Hamilton, Ontario, house prices spiked by 2.1% in July from June, but that was the smallest jump since February, having peaked in June with a 3.8% jump. The “softening” has set in. But year-over-year, the index spiked by a mind-boggling 30.1%.

All charts here are on the same scale as the chart for Hamilton. As we go down the list, house price increases were smaller than in Hamilton over the past two decades, resulting in larger white spaces above the curve.

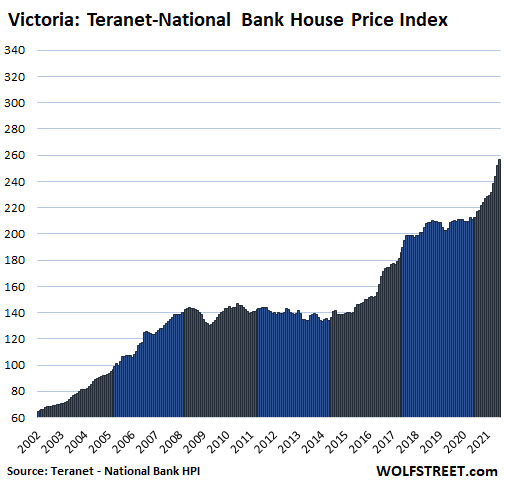

In Victoria, house prices jumped by 2.1%, “decelerating” from the jumps in the prior three months that topped out at 3.6% in June. Year-over-year, the index soared 21%. The housing market had flattened from 2018 until the BoC went nuts in March last year.

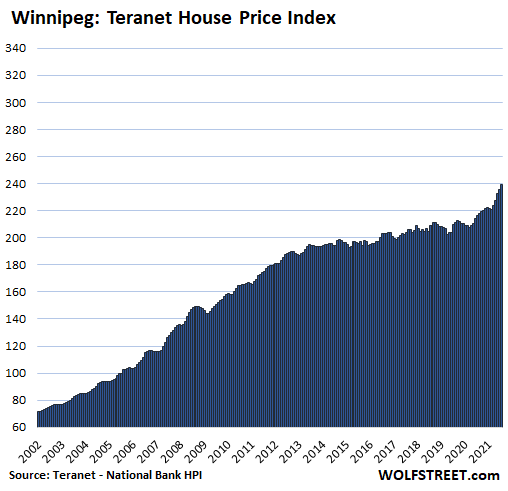

In Winnipeg, house prices jumped 1.6% for the month, and 10.5% year-over-year. House prices had flattened from 2013 on, until the BoC decided to fix that untenable situation in March last year:

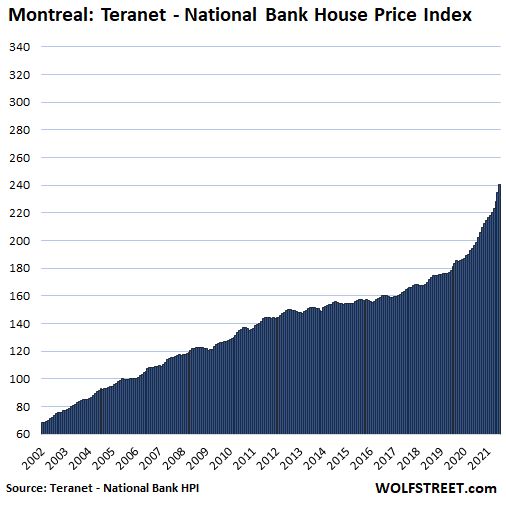

In Montreal, house prices jumped 2.5% in July, softening from the 2.8% jump in June. The index was up by 21.4% year-over-year:

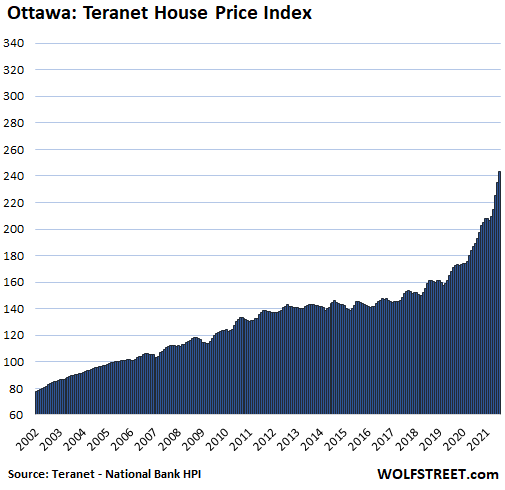

In Ottawa, house prices spiked by 3.7% for the month, but that was softer than the 4.0% and 4.9% jumps in the prior two months. Year-over-year, the index spiked by 28.9%:

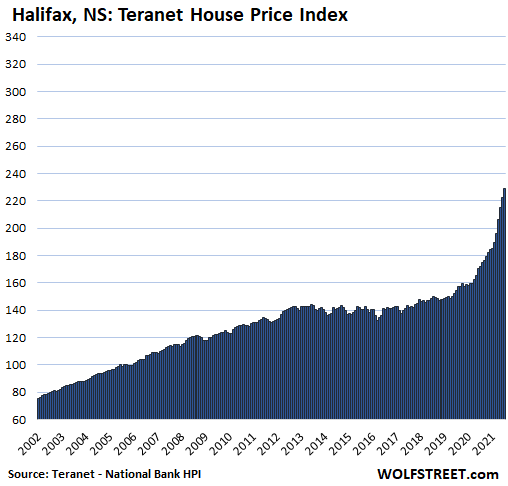

In Halifax, the Teranet index spiked 3.0% for the month. As crazy as that might seem, that was a brutal deceleration, so to speak, from the jumps of 3.5%, 4.3%, and 5.4% in the prior three months. Year-over-year, prices spiked by a breathless 33.4%:

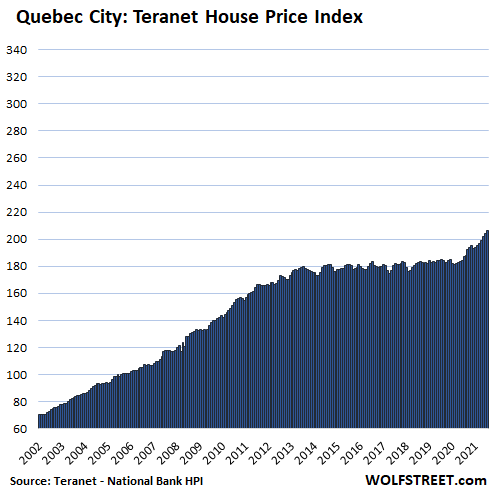

In Quebec City, house prices rose 1.0% in July, softening from the 1.3% jump in June. Year-over-year, the index was up 10.3%:

In Calgary and Edmonton, the oil-bust towns and remaining two cities in the Teranet-National Bank House Price Index, house prices were driven in the past by big spikes in the price of oil and hopes in Canada’s oil patch for instant riches. But that hasn’t been the case since 2007, which was when the last oil-powered housing bubble peaked and then imploded.

In both cities, prices have recently been rising. In Calgary, the index is up 7.5% year-over-year, having squeaked by the oil-bubble peak in 2007. And in Edmonton, the index is up 6.5% year-over-year, but remains below its oil-bubble peak of 2007. And so these cities, with house prices that might actually make some sense, don’t qualify for inclusion in this crazy list of the most splendid housing bubbles in Canada.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Actually, home prices are increasing almost all over the world. this is the testament to the fact that nearly all CBs are doing money printing like crazy thus devaluating currency.

Unless the rates go up bigly in USA, I don’t see home prices going down. I don’t think FED would increase the rates though they have been talking a lot but never done this, may be 25 basis point

You might be right, the way the Fed talking & behaving I don’t see how rates go over 1% before 2025 unless hot inflation continues for another couple of years and even then housing prices might not drop significantly. In mid term I think there is more chance of stuck market correction.

If foreign nations start offering 9% 10 yr gvt bonds and the US goes into yet another decade offering less than 3% 10 yrs, who the hell – including US citizens – would want to hold DC paper?

At 9%, your money doubles every 8 years.

At 3%, your money doubles every…24 years. (By which time, your foreign gvt invt has gone up…8 times vs 2x in USD).

USD dumping is as predictable as DC sh*tt*ness and Afghan defeat.

Cas

Foreign bonds are much riskier than US and Europe bonds pay even less then U.S. So yes some will end up buying them but will keep plenty of U.S bonds too. Plus the Feds could continue buying them and keep the 10 years interest rates low artificially just like they are doing right now….. It doesn’t seem FED has any imminent exit plan despite tapering talks.

Cas127,

The issue is that for those foreign governments, their debts grow at that same rate. Few foreign governments have currencies that are used as reserve currencies. Only America has what is essentially the global dollar. Countries with reserve currency status might be dumb with their currencies, but they are far less likely to go off the rails like in a way that, for instance Venezuela would. Countries without reserve status have less to lose by defaulting on their debts; they also are more likely, because of this, to have trouble raising new cash to cover old bonds; this pushes them towards defaulting. There also is the issue with foreign bonds, on whether the underlying currency will maintain any value.

Everybody has to stick their savings somewhere, and so far America has never defaulted.

After the everything bubble crashes, all us and euro bonds, could go negative. Foreign governments could be much higher paying even a few percent, but would the exchange rate, make this a good offer? Usually not.

America and the EU are being the smartest dumb guys in the room. Because they started in the best position, when the dumbness started, they can also make more mistakes and still stay ahead.

The question like always, is where exactly, are you gonna stick your money?

The USD will lose spending power domestically but strong internationally because meme bonds like Turkey will offer higher rates but if you trust Erdogan I got some beans to sell ya too.

The “stable” currencies offer no yield on debt, destroying the middle class. That’s what is happening. Nowhere to get yield on savings without risk which is garbage policy unless you can afford to wait out downturns.

Even a HINT of Fed taper will collapse the stock market because everybody has been forced to be risk on or debt dependent for over a decade. The people that get hammered are those who can’t afford a downturn. Problem is that real yield on stocks is now garbage too. The reality is setting in that the market has decoupled from corporate earnings and relies almost entirely on fed debt. Which is crap, not capitalism. The people who win are the banks because they are the Fed’s conduit. Jamie Dimon may be the biggest piece of crap on Earth tbh. He is like the poster boy of this garbage.

Latest thing I have been seeing and reading makes me think rates want to go lower over the next 18 months or so, but Fed has through reverse repo ensured front in of curve can’t go negative and through regular repo are going to encourage banks to buy long term treasuries driving long term rates lower.

Maybe even lower mortgage rates in USA. Maybe more refinances to take equity out. What a mess.

Old School

(Fixed auto correct) sorry

Rare want to go lower case the Fed keep buying more bonds then prevent it from going negative via the reverse repos. What I’m saying the whole reason it needs to prevent rats from going negative is buying more bonds by the Fed itself. But I agree it doesn’t seem that we are going to see meaningful increase in mortgage rats any time soon. I have more hope for a stock market correction at this point, like you u have plenty of cash waiting to see best course of action.

They’re never going to taper or raise rates unless a currency crisis forces their hand. Even Kaplan, who was the most reasonable of the bunch, came out today saying delta was making him reconsider his tapering proposal.

These people are full of crap. Economic growth is going to slow, not because of “delta” (which no one outside the media talking heads care about), but because the “base effect” includes trillions of “stimulus” which will not and cannot be repeated.

So, they print trillions of dollars and allow it to be handed out, which creates GDP “growth” and massive inflation. They then use the fact that the growth will slow (or even go negative) because of a reduction in future printing as a reason to keep printing.

These perverts are NEVER GOING TO STOP until they’ve destroyed the country.

“…. delta was making him reconsider his tapering proposal.”

That’s not what he said. He said that if delta hits the economy, then he might reconsider his GDP growth forecast and maybe the taper. But there are no signs yet, he said, that delta was hitting the economy in a significant way.

Okay, fair, but what if the just slows for the reasons I stated, that the “base” now includes the effects of trillions of unlikely to be repeated stimulus? These guys will then claim that a quarter of negative GDP growth is because of delta, and put off their “tapering.”

Powell said, that the economy is never going to return to where it was before the pandemic. In fact it has. We have the same (tight) labor problems, and the same weaker GDP, after the same overly stimulative Fed policy (recall the six month emergency REPO window), and they were slow to close that. The fact that Delta correlates with slower GDP is not causation but only a non-pervert bureaucrat would bother to parse that distinction and then on the face of it they would be wrong. GDP is higher now than before the pandemic. Is that the result of stimulus or increased demand for (medical/funeral services? What Powell means is GDP won’t be that low again for a long time and if it drops, (remember the recession storm warnings before the pandemic?) they will have to employ “emergency” measures, like more QE, which is how they justified the pre-pandemic market pump. Potus wanted lower interest rates, so Powell cooked up the China kerfuffle, which in the current context is Delta variant.

I agree with RightNYer,

Fed and partners are just experimenting things. So far, they let economy running by printing money. However, the country is already destroyed, and that’s why they have to give hand outs. I am thinking what would be the next “Abracadabra” ?

As you can see now, the effects are very bad. Look at the sky rocketing inflection, and housing prices. Believe it or not the crisis is brewing even more. How? Soon, when the crisis hit again, expect them to start to talking about cash handouts again along with negative rates, too.

At that time country is broke, can they print more paper?

“These perverts are NEVER GOING TO STOP until they’ve destroyed the country.”

Exactly. Just look at the tent cities everywhere across the land. These central bankers should have been arrested for economic terrorism long ago. They are displacing human beings from shelter in the name of avaricious greed.

Each CB has a complicating factor in that they’re locked in a multipolar world where other CBs are working at the same time as they are. It really is a form of 4-D chess. CB head #1 says what will CB head #3 and #4 do if I do “Move A” or “Move B”? There’s some attempts at coordination but these are halting and slow.

And avaricious greed is what drives the market. It’s called the profit motive in more sane times.

As Gunlach saida central bank can add a zero to stock prices. They can turn 3000 to 30,000 given enough time. Same is true for housing. It certainly happened in my life time as my first house was $48,000.

Vancouver looks scary as 20 year rate looks like it’s around 9% annual gain.

How to raise the rate substantially when the printer ballooning the national debt to $29T? Minor rate hikes of 25 ~ 50 BP just for show and overtime the FED will lower it towards close to 0. In the 70th, national debt is <$1 T. If the rate is 5%, how much the interest the country will pay for the debt? Instantly, the country would become insolvent. So, rate hike is a no go land but the market will keep debate on this topics fueling by mainstream financials channels.

Tapering is also another show as long as the world still believe in the G7 financial strengths. They are the group of countries that printing $ during this crisis, creating something from nothing. I do see the same parallel of IMPERIALISM now, using PRINTED MONEY. Back in past few centuries, they use GUN & CANNON.

When the developing world are demanding something has REAL VALUE for goods exchange instead of PRINTER MONEY. Then, the magic show would end!

bubbles keep going until they are unsustainable. there are always momentum buyers who are buying because they are afraid of missing out on future home price appreciation.

once the market starts to see home price declines, noone will want to buy at the high prices. the current crop of buyers are all momentum (fomo) buyers at the end of a very long trend.

I live in an emerging economy; home prices for prime real estate went up 15-20% this year. I don’t think Canadian prices are out of whack. It’s a global phenomenon.

Did local incomes go up 20%?

No need for incomes to go up 20% as The drop in interest rates makes up for more than the 20% increase. That’s what goosed the market higher. This jump in pricing puts a lot of homeowners who are stretched thin making mort. payments at today’s rates. Every 1% higher will severely damage the housing market and the economy. Central Bankers know this and have no choice to let inflation run hot! or cause a deep recession like 08!

Credit availability isn’t the same in emerging economies as it is in the US.

Prices aren’t necessarily low either, especially for the incomes, and interest rates are presumably noticeably higher. I doubt 30 fixed rate is available either.

Canada like the rest of the West is structurally broken, de facto banko and all the politicos have left is printing trillions in fake fiat currency. Since that is all they have left to address their banko countries, like a banana republic, will print until the currency breaks! Western economies are already creaking and cracking under the weight of trillions in fake fiat currencies, uncompetitive industries and banko gvts! Canada will be ravaged with hyper inflation and then rip-the-economy-apart deflation. Then you will not just see a correction in pricing but a collapse! All you will hear from the Central bankers and politicos for the next several years and until the final collapse we must do these extra ordinary monetary actions due to the Wuhan flu!

Oh it makes up for 20% increase? wow realy?

“No need for incomes to go up 20% as The drop in interest rates makes up for more than the 20% increase.”

Pure, unfettered bull excrement.

Obviously, some here are mortgage-interest rate ignorant. Before interest rates dropped in 2020 a million$ mortgage at 4.5% was $5,700 a month and now the same million$ at 2.5% is $4500 per month.

Payments for the same million$ mortgage are over 20% lower. Interest rates goose and deflate housing markets!

Obviously, some here are mortgage-interest rate ignorant. Before interest rates dropped in 2020 a million$ mortgage at 4.5% was $5,700 a month and now the same million$ at 2.5% is $4500 per month.

Payments for the same million$ mortgage are over 20% lower. Interest rates goose and deflate housing markets!

There are so many bond funds and lenders chasing yield that in some cases interest rates offered and compared to before 2020 lockdown will save a borrower upwards of 30% on their monthly payments. Ontario, Canada has lender offering 3 years at 1.4%. Remember yields are negative the EU and Japan and Canada and the US have ZIRP policies, or very close to it! 400 billion of excess reserve sitting on the Bank of Canada balance sheet collecting 25 basis points. while Fed Reserve offers 10 basis points. Remember too over a trillion in reverse repos as banks have too much excess reserves deposits (liabilities no where to lend it) and not enough assets(loans and treasuries)

Canada ran a 8 billion trade surplus with the US in June.

US rates are set to explode higher. they are forming resistance right now. there is one simple reason they have not exploded higher – the debt ceiling. the market is simply being starved of debt by the Treasury as they use up all the money in the reserve account, instead of issuing more debt to cover the deficit.

once the debt ceiling is lifted, the Treasury will need to sell half a trillion of debt in the following month and that oversupply of debt will lead to much higher interest rates. the problem is that once rates start to rise, investors will stop buying Treasuries for the price appreciation of the bond and will require much higher interest rates to be willing to invest in bonds. and the core problem is that the Fed will be prevented from massive intervention due to inflation.

go back and find Wolf’s article showing who is buying US debt. it is coming from large ETFs and pension plans and the Fed. there is no increase in Treasury buying from foreign central banks. the US banks are also buying alot of Treasuries.

once interest rates start to move much higher, the US banks will have large priniciple losses, but since they dont need to mark these to market, the problem will just sit there on their balance sheets and get worse and worse. another bank crisis is coming in the years ahead.

the rise in interest rates will also cause many large domestic investors to pile out of Treasuries, which will put more upward pressure on interest rates.

the Fed cant come out and tell everyone about this pickle, or it would create instability. so it feeds us a false narrative.

the people who say the Fed will always keep interest rates lower dont understand that only happens when inflation is under control. when inflation rages, the Fed is limited, it cant simply buy more debt because that sparks inflationary pressures.

right now, the Fed is talking about higher rates and will assure investors that the higher rates that occur after the debt ceiling is raised were intentional. but that isnt the case. it will be due to a reset in the supply-demand equation for debt.

some of this interest rate increase might be slowed by using short-dated notes and bills to finance the deficit, the so-called interest curve management, but that creates more instability as it causes interest payments to become more sensitive to future interest rate increases.

the hole that has been dug by politicians is insanely huge at this point. president biden has badly bungled the Afghanistan situation and will do the same with the economy. he is far too old and inflexible to be able to grasp and handle this situation.

LoL, what income increase? They are in the fear of losing their jobs.

Specially the middle class that now see the minimum wage jobs are paying almost same as their jobs. They feel that all the hard work and education and student loans was for nothing.

Underreported story behind China’s drive to complete the BRI and digital yuan is all the money-printing during the Great Financial Crisis. The developed world prints trillions like it’s nothing, but it’s the people in the developing economies that really suffer, since food and commodities are priced globally, but labor is not. Domestic food security is ancillary project in BRI countries.

From personal experience, food is NOT priced globally, at least not anywhere I have been in Asia, Caribbean, Europe, Central America, so far. For example, the last 3 star 5 course meal I had at the Peninsula Hotel in HK was less than 1/4 what the same meal would have been at the same level of quality in SF or LA!

Friends tell me the same re food in their travels many many other locations, though they do say some, such as Australia, NZ are priced similar to USA…And we can figure that ”tourist foods” may be an exception,,, AKA ”suckers,” eh

Please let us know locations, facts and figures if you think otherwise.

Thanks,

In American businesses have to pay taxes s s insurance rent of course it costs more

Yeah, almost everywhere in Thailand, even in the Bangkok megapolis, there are local open markets, as well as mom/pop food stands peppered on streets, where locals can get very cheap ingredients to make a meal, or a traditionally prepared hot meal. Also a great variety of delicious tropical fruits for very cheap.

A poor person can get a decently nutritious prepared meal for around $1.50, and much cheaper of they buy ingredients and cook. I avoid some of the dishes, like green chicken curry which usually has half-inch or so size cubes of cooked blood (or I take the cubes out).

Of course you can also go to a Pizza Hut and get a pizza for about the cost of six basic traditional meals. There are plenty of those (McDonalds, etc.) in the tourist areas.

Restaurant food is priced locally. The ingredients are the third overhead in the cost: the first two being either the literal overhead (roof) or labor. The street vendor usually has no premise rent, unless it’s baksheesh and is working for a low wage. Thus the cheap meal by developed world standards.

The main stays of the ingredients, like rice flour, lentils (huge in India) etc. ARE priced globally, are up, and is one of the reasons the UN etc. is predicting more than usual food shortages in poorer countries.

The people threatened by hunger don’t eat out very often even at street vendors.

Rowen,

The main goal of the digital yuan is to establish absolute control over the Chinese civilians. With the digital yuan, the CCP can track every single transaction in the country and if you do anything they don’t like. They can shut off your ability to have and use money. You would be literally penniless, without the ability to ever get more money, for as long as they say. If anyone, buys stuff for you, they can also be punished. The CCP is putting it’s cameras inside all the stores and restaurants.

Usually, if you anger the CCP, they will at the minimum harass you and possibly people associated with you, the money shut off will likely occur, when you are about to be arrested; but, the CCP does weird things to civilians and they will probably sometimes, just punish people by shutting off, taking, or restricting their money. Civilians in China, will not benefit from the digital yuan.

Nearly everyone, including China, has been issuing debt like crazy.

The CCP-19 pandemic has cost every country involved in the BRI far more than the CCP has ever invested in them. Global trade hasn’t been improved by the BRI and most of the projects have disasters, which only benefit the CCP. The CCP also uses these projects, to buy off corrupt leaders/rulers.

The global economy is merely a tool for manipulation for the CCP. They dont care about currency values. To them it’s a minor annoyance that currencies exist at all.

My experience from 7 years in Qingdao, China is that an American dollar goes 5X as far as it does in the States. House prices went way up, but the market is much different. Most people pay cash. The family of the groom buys the house for the young couple, who get married about age 30. They have 30 years to save up for this, and they do. The grandparents, who often live in the same home, can chip in, and the young couple, who have been saving for a decade, can also try to close the gap to make a cash purchase.

I bought 3 weeks ago in Europe, landlord wanted to sell, didn’t buy the rental I was in. Paid 1.9 times my salary or 1x my household income. House was about the same price as a Tesla. Market falls 10percent every year. I will be lucky to sell for what I paid but at least I have somewhere to live. If it wasn’t for social housing in Scandinavia I think the market would rock and roll but having house’s sell for build cost minus depreciation is actually pretty senseful.

New Zealand just went into total lockdown because of a single case.

And has basically closed its borders too.

Hard to see how that bubble lasts with just that alone.

“the #2 housing bubble in the world behind New Zealand’s”

The NZ bubble is fueled by the 0.1% who don’t care if the rest of NZ is forced to stay inside their homes (except to cook and clean for them).

They’re busy selling houses to each other at ever higher prices, like cryptos ;-]

I can’t even get 1/2% per YEAR on my savings account, yet these “crypto” scams have returned over 100% in the past month. F*** these blankin’ central banker blankety blank blanks.

World may look very different next year at this time. My mental model is late 1700’s France. The Fed and Congress will eventually be forced to make a tough decision as money printing wealth illusion evaporates. Then we will get the big recession.

Old School

I believe that the negative rate are coming, they experimented it in Japan and Europe, now they will try to implement it here in US. Any thoughts?

3 houses on my street sold in the past 2 weeks (very unusual, this is a quiet street where people stay for decades). Two of them have signs out front that claim “record breaking sale”. This is just north of Toronto.

I don’t see how this can last. There’s not that many families around who can carry a mortgage that size, even at the currently low rates.

Even with a substantial down payment, the buyers are likely looking at $4-5000 Canadian per month in mortgage. There aren’t that many people making a quarter million a year in Toronto…

I thought the same : “how long can it last” and this was 5 year back :-)

This insanity can last much longer than we can think.

“This insanity can last much longer than we can think.”

Until reality intrudes (see 2008).

DC isn’t filled with magical unicorns that can poop diamonds…just political pathological liars allied with media pathological liars.

One aspect that rarely goes commented on – the long distilled *rage* of savers expropriated since 2002, in the name of furthering DC’s habitual failures.

Yes, I know…domestic terrorists.

I’d like to see some income numbers for recent first-time buyers in HCOL areas. Either people are insane or it’s not first-time home buyers and typical families purchasing. There’s just no way “regular” folks can swing payments that high and be comfortable. It has to be very affluent people and existing owner/selling that are buying as of late.

I sold a home in Rockland County, NY back in March and 90% of offers were putting 5% down. It seemed most buyers were stretched and using the near historic low rates to max out their budgets.

Those property taxes are scary!

Not many families in Canada that can service that mortgage, but probably several in China.

These are definitely locals. We know the people on our street.

The $2.5mil houses a couple of blocks away are sitting on the market and not selling. I don’t think it’s affluent people buying on our street.

Maybe it is people with existing equity, moving upmarket. Maybe.

My guess is people are using non-bank lenders, and possibly fudging numbers.

Wealthy Chinese citizens invested in Canada in exchange for permanent resident visas. Chinese investors bought real estate in Canada and the U.S. for years.

Correct DH, and not just Chinese/Asian folks, but folks from all over the world and all over the USA, buying RE in Canada and USA…

Last time we were bidding multi family and commercial RE construction, both new and remodel in SoCal,,, ALL of the major new construction was for owners from outside USA, even though they all had ”agents” in SoCal doing the owners project management works.

Similarly for FL, for eva to my certain knowledge!!

There are Canadians in Florida. There is a Bank of Montreal near me. Snowbirds own houses here. Mainly US snowbirds. Their universal healthcare does not cover out of country medical bills. The Canadian dollar fell and the out of country medical insurance prices rose. Canadians have been selling out.

U.S looking to retire in Costa Rica will not be covered by Medicare unless they fly back to the U.S. for operations.

Canadians bought a lot of real estate in Florida after the crash in 2008. They seem to be the only ones with money for the first couple of years.

I think they can buy medical coverage for out of the country travels.

BTW, did you miss the zillion branches of TD bank in FL? It stands for Toronto Dominion.

Yes, when you go to a house visit in Montreal it’s full of Chinese who do not speak English or French.

Our political class have quite literally sold us out.

Land value tax would stop rentiers farming us as the owner would only reap the value they add. But apparently we can’t have that.

Money still needs to be laundered.

With govt crackdowns on big biz in China – more asset purchases of all kinds are likely to ramp up again here in the US and Canada. Asset prices are not flattening soon, especially when oil bust city real estate is going up 6% or more – likely a lot more Chinese continued buying, regardless of interest rates.

Why do we even allow it? I mean, allow it but slap some meaningful tax on it that benefits people who actually live here and don’t want to live in an “adorable bungalow” draped in utility lines, across the street from an auto shop.

Actually, Americans and Canadians have made real estate unaffordable for many people in many part of the world e.g. Mexico Beach Cities.

But I agree that foreigners should not be allowed to hold real estate/land in our country ie USA.

People should not be allowed to own properties outside their home countries full stop.

Monkey,

But we say that about city people buying here. There is one estate down the road from me where the owner only visits 2 weeks per year. She lives in Montreal but she might as well be Martian. Foreign owners are foreign owners…full stop.

I think foreign real estate investing should be reciprocal around the globe. If your citizens can’t buy there, they can’t buy here.

Good news article. One problem with the market where I live (Vancouver Island) is the pressure from flee buyers out of Vancouver, Victoria, and other higher priced markets. Plus, with the interior fires this summer tourists are coming in droves and many will choose to relocate.

This is what it is like. Yesterday a guy drove in and talked to my tenant and asked if I would be willing to sell him some of my property so he wouldn’t have an immediate neighbour. (he lives down the street from me). We get lookie loos driving down our road to see if they can access the river. (They can’t). The local campgrounds are full.

I wouldn’t say prices are dropping, rather they seem to have plateaued with the greedy not being able to sell, but decent places gone within a week. In the last month houses sold here with above asking bids if they had any charm, or property, whatsoever.

I live one hour drive west of Campbell River, which is about the cut off for decent west coast weather. Yesterday I spent some time in C River where I had previously lived for 20+ years. I hardly recognise the place it has grown so much in the 17 years I have been away. Even around here, we used to know almost everyone driving by. Now? All strangers.

The Island is changing so much we seldom even go anywhere because once beautiful sites are now developed. I’ve lived here for 55 of my 66 years, and almost all of the rapid changes occurred from 1980 on. The last 20 years have been frenetic. Luckily almost all vacant land where I live is in the ag land reserve or is designated forestry. As such there can be almost no development.

God help anyone moving to a Gulf Island. It seems charming, until you wait several sailings to get off by ferry. Then it’s a nightmare. Locals stay home as much as possible until after Labour Day and the kids go back to school.

Not any thing really new for anyone born in FL 70+ years ago and now having to live here again P:

FL in the 1940s and up until the early 1970s was a kid’s paradise, with the pompano biting on a piece of white cloth when they ran by the millions every year,,, shrimp by the dozens for a couple of kids pulling a 2’x6′ net through the abundant sea grasses in the bays,,, stone crab claws by the gunny sack in an hour, fish filled vibrantly colored coral reefs to match any in the world,, etc., etc… not to mention the deer and turkey in the interior,, ahem, , , ( in season of course…)

That world is gone, far shore,,, never to come back,,, as I suspect your area of the island will go sooner and later as well…

Enjoy it while you can!

Went to Salt spring island for a few days in October 2019. No big crowds then. That being said next time I visit the gulf islands it will be by boat Gorgeous territory

I absolutely loved Salt Spring Island when I went there 20 years ago.

Over here in coastal regional Australia it’s a frenzy. Every small town is surrounded by new estates. Even the shitty towns

What is happening in Canada is insanity on a stick.

Imagine you are under 35, so unlikely to yet own a home, and you watch your wages drop by 20% in one year relative to housing. At the same time your shopping bill is going up!

So – the primary cost of a house in an urban area is the land. That’s a fact.

Canada has, as Wolf would say, land out the wazoo. It’s everywhere. You drive out from an urban area for 10 minutes and it’s all one storey housing with gaps between and empty lots regularly placed.

So the primary cost is the land. And there is no shortage of land. I’m not talking about land in the middle of Northern Quebec here. I’m talking about very, very near to the centre.

How can this continue? Are the government going to stop people from building as they pile on immigrants to keep pressure on housing stock? Are wages going to be absurdly below housing?

Are we going to have lawyers and doctors who don’t own washing the cars of semi-literate landlords on the weekend to make their rent money?

No, this cannot hold. Supply will be met, and in the meantime skilled immigration will fall. Any skilled immigrant will do the analysis. Wages. Take nearly 50% off in taxes. 20% sales tax. Huge mortgage to live in a small apartment.

> I’ve put the immigration form in the bin dear, we’re not going

In addition you will have brain drain into the USA.

Trudeau would be working at Tim Horton’s as a late shift manager if he were from an ordinary family.

Immigration of skilled applicants to Canada is far far from declining. In fact it is the opposite reality.

The land restrictions you reference exist for two reasons, and cost appreciation for the rich is not on the list. Trust me, developers live to develop property and make a buck. We have a finite and scarce supply of good arable farm land, so it is protected from development to ensure food security. Otherwise, the farm land would have been broken up and developed decades ago. In BC the Ag reform laws began by 1975, well before price appreciation. Forestry land is protected for the same reason. A logging job pays between $100K and $175K per year, depending on the skill set. These are good union jobs requiring highly trained operators and specialists. If you get housing developments in harvesting areas, protests and moratoriums quickly follow. It’s like subdivisions near an airport. Pretty soon people complain about those damn planes.

My son owned his first home by age 26. He bought his second 3 weeks before he turned 37…this January. He rents out his first house to a friend of mine, and I caretake it for him. His 2nd home has the upstairs rented to two 50ish ladies with a teen, and he lives in the basement suite when he is home on days off. (2 weeks on and 2 off). It is part of his retirement plan. My daughter has owned a home since age 28. She teaches music.

It is absolute BS that people cannot afford to buy a home in Canada. Obviously, a home in one of the most expensive cities in the entire World is unattainable…(Vancouver and ilk). So what? Starting out you don’t live there or expect to ever live there. Lots and lots of options. I have a nephew learning a trade in Victoria. He knows full well he will be moving if he ever wants to own a home and plans to do so right after he earns his ticket.

What isn’t an option is embarking on life with no or few skills. One needs a career….not just a job. By career I mean a trade or a specific degree that is focused….like engineering, nursing, etc. Any apprentice in any trade can obtain a job in Canada if one is prepared to go where the work is. It has always been that way. You move where the work is and hopefully choose a place that is affordable. With the internet for research there is absolutely no reason to screw this up.

As for brain drain to the US it has been the other way around for the last few years and it doesn’t take a scientist to figure out why. Mind you, the upper echelon of any profession can work anywhere in the World. A good friend of mine was a shipwright. He designed a submarine and marketed them all over the World. He lives down the road from me having retired at 55. Lots of Canadians have worked for Boeing and NASA. Like I said, you go where the work is in your chosen field.

regards

I agree on many points. I would add the amount of empty land in Canada is deceptive as a LOT of it isn’t going to sustain large populations. The vast majority of that land certainly isn’t usable for agriculture. The vast majority of the land is Canadian shield, the Rocky Mountains and similar. There are practical/logistic reasons that most of it isn’t heavily populated. To be quite frank, if someone thinks that it can be successfully used for agri or for heavy populations, there is a lot of people that have lots of unicorns to sell them.

I would disagree on a couple of points. His kids purchased prior to the largest run ups and in an inexpensive area. The income to price ratio has changed dramatically in that time. Additionally, I would add that while you can always move to less expensive areas, the major centres with the high prices are still where the vast majority of the jobs are. So leaving those major centres could be a significant challenge. To leave, unless you are lucky in your preferred profession being one in the area, forces you to take the available work in that area regardless of your interests, skills or talents. That’s not a match for most folks. Additionally, even being as far out as Campbell River never mind, Port Hardy isn’t for most folks. Most folks would consider these areas in the middle of nowhere with associated lack of resources, service et al and would hate the weather. In aggregate, that makes it a really tough sell and why we aren’t seeing more people make that choice.

> My son owned his first home by age 26. He bought his second 3 weeks before he turned 37…this January

Please stop replying to me. I’ve stopped reading here as I have more interesting things to do. Anecdotes are intellectually *weak*.

Hope you’ll continue to comment. I enjoy reading your perspective. I’m sure we’re apart on much, but definitely enjoy expanding my views, and your comments do just that.

Just skip over comments by possibly demented individuals like I’ve been doing :]

Georgist,

My daughter and her husband never owned a home til 40. They saved for 20 years and plunked down the whole cash amount on a 3000 sq. ft forever home. Just ordinary people getting up and going to work and saving and investing. It can be done, even today.

Again, anecdotes are not the entire trend, and therefore pointless.

Anecdotes are actually an attempt to impart learning and experience… one might be wise to listen to those that have been there, done that and are generous enough to share them with this forum… it may or may not be applicable to you but some of are so “intellectually weak”, (not you obviously) that a small nugget of wisdom may help us see something we didn’t before… Anecdotally speaking, I wasn’t’ sure I believed in the Kruger- Dunning effect, until now…

Nope, it’s absolutely not useful.

We may as well have a guy who was born with one arm in Iraq who somehow made it big, who tells us “it’s fine to be born under Sadam Hussain, look at me”.

I think this is a higher education thing. It’s just not acceptable to respond to macro points with “my uncle….”.

Actually, what is hilarious about the personal replies is my education, which G assumes I have none. I won’t get into it here. It isn’t appropriate. I am most proud of being a carpenter because it is both practical, physical, and creative. It has also allowed me to build everything we own. Building is my passion, but only one of my 3 careers.

The smartest man I have met had a grade 8 education. I worked for him. Anyone can go to school if they want to borrow some cash, but not everyone can build and operate their own business for 40 years. I did my edumacation :-) by correspondence in the early ’80s, and later online when computers made that possible. It was pretty inexpensive, actually. I worked from an office out in my shop, every morning before I went to my job. I built the office for that specific function, truth be told.

Actually, my father in law who just passed away was brilliant. He managed to obtain grade 7 in Manchester until that pesky WW2 happened and his family was bombed out. He ended up working as a printer and graphic artist, built a sailboat and lived in the south seas in the early 60s with his family (my wife), could read hieroglyphics, learned basic Japanese, was an accomplished artist and Netsuke collector, and even taught himself to play the piano at age 75. In his late eighties he would still update and trouble shoot his Apple. Like I said, school is just school and doesn’t have much to do with other recognised intelligence categories.

Anecdotes = stories. The information on WS is about people and their lives, what they can afford, where they will work, live, and if they can afford to buy a home one day. The data is about people when you look beyond the numbers.

I highly respect most of the contributors to this blog. What a wonderful source of information. Thank you.

regards

“Canada has, as Wolf would say, land out the wazoo. It’s everywhere. You drive out from an urban area for 10 minutes and it’s all one storey housing with gaps between and empty lots regularly placed.

So the primary cost is the land. And there is no shortage of land. I’m not talking about land in the middle of Northern Quebec here. I’m talking about very, very near to the centre.”

Your above comment is as pointless as any anecdote. It’s an observation devoid of facts. What do you know of those one story homes on the lots evenly spaced within 10 minutes of an urban area? What is the zoning? What is the quality of the soil (stability)? Is it in a floodplain? Is there suitable storm sewer infrastructure to handle the runoff from the additional density (rooftops and concrete do not absorb water)? Are they on septic requiring ample space for effluent leaching fields? Are they on a well or is there city water? If there is city water, what is the cost to connect to the main to develop the additional lots? Is there sufficient infrastructure to support higher density (city water allotment, sanitary sewer treatment capacity, storm sewer management)?

The flaw in your argument is that the primary cost is not the land in and of itself. It’s the cost to develop and improve the land. Someone has to absorb the cost of streets, street lights, sewer, water, electricity, etc., as well as meet all government mandates – which can include upgrades to existing streets surrounding the property (additional lanes for traffic, turning lanes, etc.). The city government does not develop the land… that takes private money.

I’ve read your posts and I’m curious as to what your advice is for those who are no longer of an age or physical condition where they can be gainfully employed. Since they own assets, should they not be allowed to leverage them in order to provide for them in their old age? Or should they give them away (sell on the cheap) and hope that someone (family or government) provides for them? Not to put words in your mouth, but it appears that your position is that “all rentiers are evil” – so what is your solution?

In New Zealand our housing bubble is still going gang-busters. The central bank was supposed to lift interest rated, but we have gone into a lockdown so they’ve left the cheap money tap on.

New Zealand and parts of Canada both have similar dynamics in that they are the “bolt hole” for the wealthy.

Vancouver is the failover site for China.

New Zealand is the failover site for rich Westerners.

In both countries politicians make a political choice not to help the majority and safeguard the future.

True. We do get a lot of wealthy bolt holers here…also have a central bank and government very supportive of property…now every man and his dog is into property, as enormous returns for little effort

Real Estate bubbles are much more dangerous than stock bubbles because of the immense leverage involved and the problems it can cause the banking system.

No offense there, G…. But why do you care what happens anywhere else… I don’t think any of it is applicable to you… as a general observation in a discussion, sure, but applicability is moot… me thinks you may have been a victim of the YOLO then the FOMO crowd think… now that you’re entering the YAMO (You Already Missed Out) phase, try not to let that color how you live in the future… sometimes you have to go backwards to learn the things you didn’t first time around … darn it, there one of those intellectually weak anecdotes again…

> But why do you care what happens anywhere else…

Because I’m not American and I will never, ever give up on people because I’m totally selfish. If I ever become so disgusting as to lack empathy I hope my life ends soon after, I don’t want to be an animal.

Georgist,

Depends on how you look at it. The person that participates in the system and goes into a factory and produces toilet paper, laundry detergent, soap, plumbing products or drives a truck or stocks a shelf for wages is acting in his own self interest but is providing just as much or maybe more value than the compassionate person handing out food at the food bank.

Democracy with market based system brought more people out of poverty than everything that came before it. Of course big government spans high levels of waste, fraud and abuse and we have plenty of that in USA.

That woman is a disgrace! To run on a platform of reducing house prices, and not raise rates now, after her 3 years of doing nothing about housing being out of control. Just like Obama, wolf in sheep’s clothes

Bank of Canada Governor Tiff Macklem took to the pages of a major newspaper to defend a three-month run of excessive consumer price gains. The central banker’s opinion piece, published Thursday on the front page of the Financial Post, comes a day after Statistics Canada reported inflation rose 3.1% in June.Jul. 29, 2021

This AM while surfing I ran across a bit about a BIg Six Bank disagreeing with the gov of the BoC but I can’t find it. All I’ve found is above. But the piece I can’t find has a senior economist pretty much telling the gov he’s wrong. The gov cites the ‘base effect’ for the inflation #s. There was a covid contraction and so with the recovery there is an brief inflation, soon to end. The economist with the bank (not the BoC) says this is a big mistake and inflation is about to take off. He also said the BoC’s new way of calculating inflation understates it.

It is very unusual for one of the big banks to publicly disagree so abruptly with the BoC.

Blind Freddy can see this policy error!

Smart people and institutions are finally calling out this insanity…. just 10 years to late

Canada, along with most other western countries are opening up to vaccinated Americans.

Unvaccinated Americans are unwelcome around the world for the foreseeable future. Wonderful from my point of view…less stupid Americans abroad.

Again, and I will keep saying it, an utter failure of the American education system.

Never, and I’m an old crusty guy, have I seen so many Americans unable to leave their country.

*fewer* stupid Americans, not “less stupid Americans”.

The irony!

I’ll leave my opinion of you to myself.

????

I’ll bit my tongue too!

Vaccination is a poor second to limiting your exposure to other people. Of course not everyone is able to do that. In a way it’s a math problem of how many people you are going to come in contact with.

Ticket takers, bartenders, healthcare workers, etc., are on the front line. Best wishes to them…

The Liberals want out before the Trudeau bubble bursts

So what does Trudeau think when he sees these graphs? Basic human needs are food, clothing, and shelter. One of them is getting out of reach.

Yes, but there has been a change in a lot of people’s behavior over the years. Now for a lot of people:

1. Food means the convenience of semi-prepared meals from grocer, take out and eating out.

2. Clothing means got to pay up for the fad logo and replace when out of style, not when worn out.

3. Shelter means living in something that’s less than 20 years old or has been updated within 20 years to latest trend in countertops, appliances, cabinets and flooring with two car garage.

There is nothing wrong with any of the above if you can truly afford it.

In Seattle, 3x average gross family salary will buy you a moss infested mobile home on 1000 sq feet of land. I’d say housing is getting out of reach in Canada and the US, at least near coastal cities, where many people grew up and have roots. If I didn’t have the money to stay in my home territory, I’d be pretty upset.

Bobber – I don’t think he does think, see, know, appreciate or truly care. The silver spoon is wedged too deeply. We’re talking about a guy that proclaimed and has run a country on the argument that “budgets balance themselves”. If he truly believes that (which appears to be the case) why would he understand or care about these graphs. Furthermore, I would argue that increasingly it’s not just housing but also food that is getting out of reach. That or you have to chose between the two if you don’t grow a garden.

As perspective, I don’t follow a particular party or leader so this isn’t a Conservative, Liberal, NDP or Green bias. I’m just anti-dysfunctional and anti-bad leadership.

I think people are realizing a house is a protected asset. In a crisis, the government can let stocks and bonds fall, which impacts the wealthy, but they will fight like crazy to avoid a housing price fall, which would impact 60% of the population. In this world of overpriced assets, housing seems the most protected. Also, if you put 20% or less down, your loss is capped, unlike stocks and bonds.

I wouldn’t call that capped – you are leveraged … if housing does “adjust” like 15y ago, you lose all your 20% and are on the hook for a long time

People walk from the mortgages and turn in the keys. In 5 years, the banks are again begging you to take out a government guaranteed mortgage. 20%, or even 3.5%, is the downside for somebody who is willng to walk. Plus, there is unlimited upside if the governments keep printing money.

> People walk from the mortgages and turn in the keys.

We don’t have that rule in Canada.

@georgist, You said:

“We don’t have that rule in Canada.”

It’s really not a rule, it’s an action. When you go BK, or lose your source of income, and are underwater on your mortgage and ca;t pay it, you can just mail the keys to the bank and walk away. What’s the bank going to do? Put you in jail?

Anthony A – Recourse mortgages are the norm in most provinces,and therefore, the bank comes after you for the difference and costs. You now have to file a proposal (basically restructure) or bankruptcy. The bank is probably 1st up to be paid out. Quite frankly, it would be less costly all the way around to step up and you will have to do it anyway’s.

We have all been influenced by life since Bretton-Woods and now 40 year run of declining rates. We almost have no good frame of reference for a different monetary situation which probably is coming.

Shelter is a necessity and we all have to determine how we are going to get it. The US government subsidizes 15 and 30 year mortgages so it’s probably a good idea to lock in a fixed rate if one can still be disciplined about the price of the home.

One thing not mentioned too much is a home can be a liability. It’s a target in a lawsuit. When you sell does it have asbestos or lead and probably the list will get longer? When it’s at the end of its life the home may need to be disposed of for the land to sell.

It’s complicated decision that so few of us make more than a few times. There used to be a saying, don’t be house poor which is still good advice.

At one time I read a home had 2.5 man years of labor in it plus the raw material cost. If you make the same wage as people building the home that would be 2.5X your wages for the home plus land and material plus government take. Only way it’s going to be cheap is if you make several multiples of wages of people building the home and if land and government take isn’t too much.

We are supposed to start escrow on a house in Los Angeles and the very same day I get a report how we are in a worse housing bubble than 2005-9 – from an investment research firm that it is very good – basically we are 40% above “inflation adjusted” housing prices…I don’t know what to do … Fed will only raise rates if inflation becomes “real” and if inflation becomes a true problem, real estate is a good place to be in – catch 22 …. but I do think there will be serious drop in housing next 4-5y

Feel your pain. Remember buying a house in 2010 thinking the moment I sign this document the market is going to fall out. In time the value shrunk but in the end I walked away with a healthy profit and a place to live for several years to boot. Home ownership is much more than a prize or asset as it becomes the place you spend a majority of your time at.

Congratulations!!!

Buy the house, make it a home.

That’s why we should buy these things.

Welcome to the world controlled by the money printers. Your future house value will to a large part be determined by them.

I don’t have a house and I have a lot of cash. They control my destiny as well.

I went backwards in the last bust. Couldn’t get out. Trapped.

I was fortunate during the last bust as I had gotten totally out of debt and quit my job a year or two before crisis hit. I had about 15% not in the stock market and threw that in as well when things got very cheap. It was a tough year or so as things got even cheaper.

I hunkered down and spent nearly nothing for 5 years and cashed out way too early around late 2015.

Anyway it set me up for a decent retirement, but I am too old and don’t have to go all in now if we crash again.

An old mentor once stated that banks make the same profit on a RE transaction regardless of interest rate. They will allow RE to increase in value to make the difference. Banks are greedy but transparent. The only problem is when small banks lose their business on bad RE transactions. The big banks can mitigate that risk. The investors lose the most. I was just a child during the late 70’s. What did the RE look like during the Carter years?

Related to the economy and everything else: a hell of a piece on CNN just published, ‘The South West’s Most Important River is Drying Up’

The above is not some quickie, looks like it was a ton of work, lots of video and charts that scroll as you read.

The first cuts to states below the Hoover Dam on the Colorado will start in October. There is a very complicated sked on who and where gets cut first, second etc. but some farmers are already not planting.

If trend persists by 2025 the Dam will only be 50 feet above point to make electricity and 150 feet above ‘dead pool’ where water no longer flows past dam and would have to be pumped over it.

In the worst case scenario, a lot of problems now deeded huge, are going to either shrink by comparison or be made much worse. What is real estate without water? One town (not in this piece, saw it on TV) has been allowed 50 gal per hse per day.

In the ME, there have been times where a tanker of oil has traded one- for- one for a tanker of water.

Correction: ‘150 ft above dead pool, should be 105 ft’

I’ve been sitting on the sidelines of an outrageous housing market here in Bend Oregon, where we’re having some of the same issues. I wonder how long the story of wildfires and water shortages can go before it has any impact on the thousands of people moving here each year. I’m 6 years established here with friends, neighbors and my kids have their friends here. I don’t think I’d consider Bend a very great place to move to right now, and if I had no roots I’d likely move somewhere with a little more rain. We’re rounding a corner where in a short amount of time I feel like it might be a good thing I don’t own here.

I review a lot of full time RVing sites. I know it would be pleasant, but people that boon dock can get their water use down to about 3 gallons per day per person. So 50 gallons would seem to be a unpleasant, but manageable amount

As I have said before, the key to real estate success is seeing the big trends before everyone else does, or at least getting in early. Best bet going FORWARD:

Facts:

1) lack of water, drought, fires in the West

2) Hot temperatures, global warming everywhere

3) Sea levels rising

Results:

4) Water availability is critical

5) Northern, increasingly temperate climate

is sought after, especially during brutal summer heat

6) Lakefront more sought after than Oceanfront (due to to rising sea levels, hurricanes, and events insurance premiums)

Conclusion: Lakefront, in the North, where water is plentiful. Great Lakes. Bingo. Places like Traverse City and even Duluth are the future boomtowns.

NZ wouldn’t do it. Canada? USA? Who’s going to test the waters of higher rates?

BoC has *zero* control over rates.

If the Fed raise Canada have to raise. Who is going to save in CAD when every Canadian can easily save in $$ and get a better rate? Nobody.

Canada could push land values down and crush rentiers, by taxing the unimproved value of land. They could also use the income from land value tax to cut the high labour tax, that punishes people who add value.

But they won’t do any of this because Trudeau is a joke, and so are the people who dig their own kids into a hole, who vote for him.

Almost too easy…. G, your hypocrite side is showing… pull your skirt down… you rail on the selfish Americans but want to save in US currency… when the CAD was $1.35 to $1.00 US, how did you miss out on the FLA real estate investment? Weren’t paying attention? You live in a country, as do I, where the collective rules… get over it or start an expat trend yourself… UGANDA maybe, but you would have to brush up on your Mandarin… the point is, there are always opportunities, if you bother to look for them… and that’s what people here are telling you…if you didn’t see what was coming, you weren’t paying attention or were just looking for the world to give you what you think you deserve… listen to some of your “ uncles and aunts” here… As your Uncle Paolo would say, “ quit complaining about the way it is, look for the opportunities to be successful and make it work for your own personal situation… most of the folks here have a far greater education than you with a diploma from the school of hard knocks…

This again is poor quality stuff.

I’m not talking about what I will do, I’m talking about the BoC and the situation in Canada. Then I get some absurd post calling me a hypocrite because I will save in USD instead of CAD.

Please, let’s not make this like a children’s playground. I’m talking about the macro situation of the BoC. Why bring your imaginary idea of what I will or will not do into it?

The rest of the post is even lower quality. It’s stuff you’d find on some youtube channel about buying gold because the government is going for a big reset. Please, if you can’t stick to actual macro comments that address my post, do not reply.

This immediate low quality forum “well I’ve got you now!” stuff is a total waste of bytes.

So what does a square foot of Canadian housing cost? They have plenty of trees.

Lumber in Can costs market, which is the North American price minus shipping to where ever, that’s why the price here in logging BC went up 200 to 300 % like everywhere. I don’t know what the US tariff is right now. The US Home Builders Association was complaining about it, but don’t know if it had any effect.

Materials are not the main cost for the majority, who live in urban areas.

Land is the main component.

You’re grasping, G… nice attempt to backtrack, but not buying it…you got it handed to you by 65 yo man who barely finished high school… it stings and I understand that probably in your world, it doesn’t happen… that being said, all the snark aside, the point you refuse to grasp is that, while I am sure you are superior with your “ higher education” thought processes, you are a poor inferior soul with aptitude… intelligence may let you see opportunity, lack of aptitude prevents you from taking advantage of it… many very successful people are intelligent but lacking aptitude, so they hire it… without aptitude, intelligence fails…looking forward to your thoughts ( without the personal attacks please)….

This is entirely in your head, I’ve zero idea which post you are referring to, plus this is a different thread so stick on topic. Macro.

That’s very sad. I am not used to land value being but 10 – 30% of cost of dwelling.

Framing lumber is the least expensive part of building a home.

Labour and building services #1

Finishing and setup materials would be number 2…appliances, flooring, drywall, bathroom kitchen, etc.

Land is next

Site prep and concrete next.

Framing and roof system about the same.

Permits are also expensive.

It all depends on where you are building and what you build.

I have built many many homes and apartments over the years plus some commercial work. Also, many renos.

Land is # 1 in an expensive city, not so much across the country.

Right now a person could buy a decent serviced lot where I live for well under 100K, about the price of a new truck. Down the street from me a couple just bought a cottage on one acre for 85K, but the sellers were Germans and the guy had an inside track.

I always chuckle at people I know who buy or build a small sawmill and spend 1-2 years milling up their own lumber. By the time they start building and deal with rising prices they have a net loss.

I just built a large 400 sq foot post and beam covered deck. The T&G pine for the ceiling was $3400 alone. Posts and beams were $900 direct from my buddy’s sawmill. Add on roofing, decking, etc he total material cost was $10K and I get a hefty contractor discount. No labour obviously. If I had to pay for someone to do the build it would have been between $40-50K.

Its really too soon to see if the Housing Mania has peaked in Canada. Interest rates are rock bottom and a lot people buy now because they think housing prices will keep going up or just more expensive later on, so best to buy now. I’m in Calgary, and we have not been as crazy as a lot of the country, but houses still well pretty quick here. This latest boom is different because it has been outside of the traditional markets boom markets in Canada. Not just big cities but small towns within a few hours of big cities. However, if mortgage rates went up a percent or two, or start to normalize (I believe the 100 year average for mortgage rates is around 6%?) I think it would all crash.

Here in Western Europe prices have been going up for 20 years. Why?

Interest rates. They’re negative. Deeper and deeper so.

There will be no taper ever. They cannot and will not do it. Even in the face of inflation. Talk is cheap, money is cheaper.

The result of all this? the rich who own 1,2,3 houses and more are getting ever richer.

The renters are moving forever farther from owning.

That’s what central banks do: socialism for the rich and free money for the uber rich.

I tend to agree it will continue until there’s an uprising. People will not tolerate being permanent serfs. At least in the West.

Sorry Guy’s it is not about supply and demand or the economy or the interest rates but it is all about the availability of Land. Canada has lots of land but the government does not make it available to build / change from farming and others to Housing. Just drive 2 miles out side the major cities in Ontario, there is land all over but not available for housing.

Is it the government, investors, landlords or who else?

It is all about keeping the supply of land low and make money.

Alfredo (Fred) De Gasperis owned all the land in Ontario and was unofficially the richest Canadian by lightyears well before his death in 2013. Most of his money was always parked outside of Canada. My father knew him from elementary school. They were in the same class.

So is there a chart showing the number of, and amounts of, mortgages that are about to go “underwater” if the prices stop rising or demand softens?

This is all vaguely familiar.

I heard it was DIFFERENT this time!

The Chinese are always there to backstop the market from falling so it virtually never falls.

Detached home prices in Edmonton, Alberta fell about $25,000 the last month putting them on par with pre-Covid-19 prices. The last of the suckers bought right before the new stress test kicked in. Resale apartments and resale townhouses are still 50 percent below their 2007 peaks. Many resale apartments in downtown Edmonton are selling for what they sold for way back in 2001. Lots of foreclosures. An apartment can still be bought for under $50,000 and a townhouse for under $100,000. The same townhouses that cost $100,000 in Edmonton would fetch about 1.5 million 30 miles away from Toronto, Ontario.

Proof for Edmonton, Alberta home prices. Not endorsing the real estate company.

https://www.livrealestate.ca/blog/2021/08/weekly-market-update-aug-27-21.html

See comment $30,000 drop in the last two months.