First effect of MBS taper-talk from the Fed: Mortgage rates flat since late April even as long-term Treasury yields dropped.

By Wolf Richter for WOLF STREET.

The evidence has been piling up for months in bits and pieces: While investors still have the hots for this housing market, potential buyers that need a mortgage and those who want to live in the home they’re thinking of buying are getting second thoughts, as evidenced by sharply dropping sales of existing homes and new houses even as inventories for sale have now risen for the third months in a row and new listings are coming out of the woodwork.

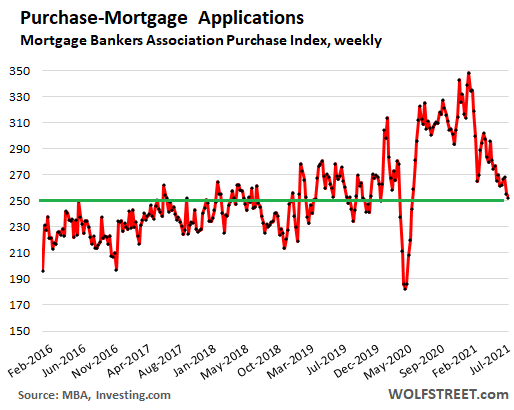

So here’s the latest piece of evidence: Demand from buyers who need a mortgage to fund the purchase of a home has been declining for months and in the week ended July 2 fell further and is now down 14% from the same week in 2020 and down 8% from the same week in 2019, according to the Mortgage Bankers Association this morning. Mortgage applications are now at the low end of the range in 2019. The entire Pandemic boom has now been worked off, plus some (data via Investing.com):

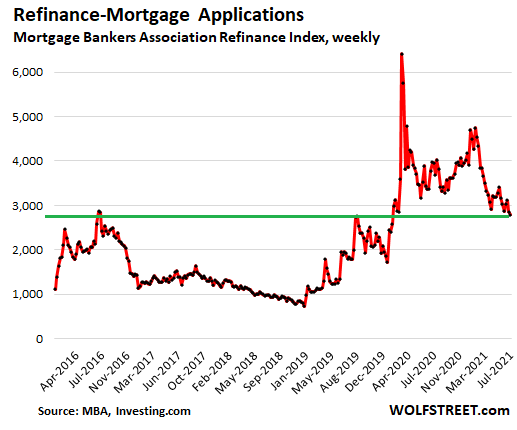

Mortgage applications to refinance mortgages in the week through July 2 fell to the lowest level since February 2020, having now also worked off the entire Pandemic spike, despite mortgage rates that are much lower than they were a year ago.

Refi mortgages go through boom-and-bust cycles based on mortgage interest rates, with lower-than-before mortgage rates triggering a refi boom, and with higher-than-before mortgage rates putting a damper on refis.

So refi applications in the week through July 2 remained 55% higher than the same week in 2019, when mortgage rates were a full percentage point higher than today; and refi applications were over twice the very low levels of 2018 when mortgage rates were grinding their way to 5%:

Can you imagine what this immensely overpriced housing market would look like with mortgage rates at 5% — meaning barely at the rate of CPI inflation? Me neither.

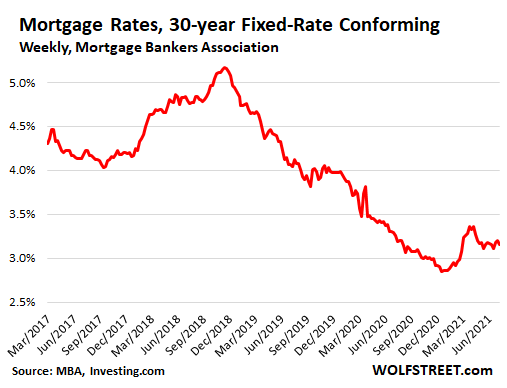

The average interest rate on 30-year fixed rate mortgages with conforming balances and a 20%-down-payment was 3.15% in the week ended July 2, according to the MBA today. The rate is down about 20 basis points since the recent high in late March and has remained in the same narrow range since late April:

It is interesting that mortgage rates have dropped 20 basis points from their recent high in late March, while the 10-year Treasury yield has dropped 40 basis points over the same period, widening the spread between them.

There is now consistent taper-talk coming from the Fed, including ideas about tapering its purchases of MBS sooner or faster than tapering its purchases of Treasury securities. Several Fed governors have now publicly expressed concern over the housing bubble, over investors’ involvement in the housing bubble, and over the Fed’s providing fuel for the housing bubble.

The first effects of this Fed talk concerning tapering purchases of MBS may already be showing up in the widening spread between the 10-year yield and mortgage rates – that’s maybe what we’re looking at here.

Price discovery over rents in uncertain times. Read… Is this the Reversal of Exodus-Triggered Plunges & Spikes of Rents? Mmmm-maybe

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Buyer, Seller or Holder – where do you want to be when the music stops?

I would rather be holding cash when the music stops

Not if there’s hyperinflation!!!

In general (and short of a wheelbarrow hyperinflation), I think it is safer to be in cash (and therefore capable of easily recalibrating goods and asset purchases) rather than trying to pick one low liquidity asset/asset class in a hugely asset price inflated environment.

I get the argument that the house-in-place value is supposed to increase faster than the vanishing value of the dollar (because the house has utility) but that sort of presumes the house wasn’t two or three times overvalued to begin with.

Maybe in the modern hyperinflation, the smart money will exit the USD entirely for Yuan/Altcoin/Whatever rather than push homes to 4 or 5 times overvalued.

Homes are overvalued when the rents that they can command are so out of proportion (on the low side) to the sale price of the house. Using the income approach to appraisal value is one of the best ways to get the real value of a house. If you can’t make back enough in rent to cover your mortgage payment and expenses then the house is overvalued. That may go on for a long time especially in this low interest rate environment but eventually when interest rates normalize, the true value of the house will materialize and it will be a lot lower than it is now.

Reply to swamp:

Value should be equal to rent chargeable. Sure, in a vacuum. But a lot of markets have huge amounts of outside money that screw everything up.

Example-Think about how much Hawai’i costs, every house is an Air BNB or a fifth home to Oprah.

Locals living on wages & paying rent do not set the market.

You’d be better off having converted some of that cash into the non-perishable and useful things that you will be having to buy for the next twenty years, as the prices will continually inflate for them and the supply of them may be non-existent.

We did that last November and have saved upwards of 20-20% on the building material and 5-10% other things we will need, like dishwasher powder, detergents, garbage bags etc. Plus we got 2% points on CCs.

Shrinkflation’s happening, as well as far as package sizes, “same price” or “modest increase”.

I agree with you. Unfortunately I am not in a position to do this now due to space constraints where I live. Also do not know if I will move far away from where I live now which might make it impractical.

I would like to buy as much as possible that will store for the indefinite future. Did some searches on the internet to get an idea of what can be stored long term and what cannot be.

Zactly.

Silver.

Amen but cash is only good for a short time due to the hyperinflation risk. I just sold most of my stocks at nice profits in my retirement account. I think that the fight to raise the spending limit that begins soon and will continue through October 2021 will be catastrophic, even if the mainland Chinese Ponzi schemes, which the CCP’s allies the Wall Streeters and the banksters laughably call “stocks,” do not crash first and trigger an avalanche of sales due to the outrageous overleverage of all Americans, e.g., by the historic overuse of margin in the purchases of stocks.

Now, the issue is where can I park the money before hyperinflation (which may yet also come, because the US is getting so many of its products from other countries and they may lose faith in the US dollar and want to divest themselves of US investments) takes most of it away?

0.5% at Ally is the best I can find for cash without locking it up basically “forever”. I’m not close enough to retirement to think of selling anything I have in the stock market but I do old some cash from a windfall that I like having around in case California real estate takes a big dive. That seems more likely to me than inflation eating away too much of my dry powder.

Home builders have a backlog of orders for new homes.

Mortgage rates have dropped a little over the past 30 days (mortgage news daily website).

A neighborhood where there were once 20 homes listed for sale, not pending or contingent, now there are none.

Los Angeles sees the flood comming, listing numbers increased lately with rare but some price drops. We passed the peak, ( maybe, I hope).

At least, for sure it is not war of 2020

In San Diego inventory is showing up and I’m starting to see numerous price drops

Funny, I saw a price drop in SoCal the other day too. It was kind of shocking because it wasn’t a bad house and the price didn’t seem any more out of line than others.

Like, nobody AT ALL wants your glorious overpriced home? That’s a first for 2021. I’m sure we’ll be seeing more of that at some point. A lot more. Wish I knew when “at some point” is.

This is not what the data shows regarding back log. Also it’s in their best interest just like real estate agents to claim the music is never going to stop.

Also real estate is local, you may live in a hot area but overall the trends are showing less purchases and larger stock piles of homes.

In Boston metro I see houses that sold last year coming to the market almost for the same price, I don’t know maybe they end up selling for more, But it seems that there is more inventory…. Also a house in Cambridge just sold for 1 million over asking, so there is that too.

My neighborhood in San Diego near the beach added over 70 SFH just in the last 5 days.. already listed homes (600+ in San Diego city) are now roasting on the market for 30+ days, and are now showing price drops. This whole narrative of a severe shortage of inventory is a lie. These homes will transition back into rentals when they don’t sell

I hope so. San Diego has blown up more than any place I’m familiar with. A correction is in order, if you ask me. But I’m not sure “they” would permit it. Heaven forbid a crap shack in National City become “affordable” at $400K for some working class family. It cannot be allowed!

When the music stops I’d like to be flyfishing in New Zeeland.

The only reason why the Fed had not yet acted is because JPow is up for re-election and he is obviously using the expected rate hikes for his own purposes. I’m sure politicians are lining up to put in bids on when to raise rates and wreck the markets.

Biden’s choice on fed chair will be coming soon hopefully by the end of summer.

What will JPow do if unelected in the last few months of his remaining term?

Worse yet what happens if he gets re-elected?

This site is like zerohedge. Always wrong. Supply is down. Simple as that. Where i live prices are insane and no supply. Everything sold in a few days. Maybe high rises are not selling? Come on.

“This site is always wrong >:(“

Makes claim, doesn’t back it up with facts.

Also down from when?

2006?

1986?

Last week?

I can tell you that supply from Sept. ‘20 to May ‘21 supply has only increased according to the FRED by about 1.5M homes.

Your primary residence must be in a large city…. Goodluck with that. And short term charts mean nothing.

Then why read it? Perhaps the more likely explanation is that you are wrong. You came here looking for evidence of your preconceived notions and didn’t find it. So instead of thinking “What possible reason would Wolf Richter have for lying to his readers?”, and accepting Wolf’s information at face value (a widely accepted face value cos you are in a definite minority here), you just defame him by saying he’s wrong. So all those other data agglomeration sources where Wolf gets his information from are wrong and you are right based solely on your own anecdotal evidence? And you seriously want me to believe you on that basis? Grow up, manchild.

He came here to suffer the inaccuracies of Wolf Richter obviously. He wants to be punished by what he perceives to be the UNTRUTH. Well, to each their own, I guess.

Pilot,

“Supply is down. Simple as that” — for the US, that’s just a lie, see charts below.

“Where I live….” — OK, maybe where you live, which is not in the US, which you forgot to tell our readers here.

In the US overall, supply of new houses is UP and fairly high:

And in terms of existing homes, supply is UP for the third month in a row. Inventory rose 7% in May to 1.23 million homes, the third month in a row of INCREASES. It’s the highest level since last November. Supply rose to 2.5 months, highest since October last year. More supply coming on the market even as we speak.

Seems to me that the upper chart shows new SFH supply has finally returned to the level 20 years ago. Has the number of people stayed the same for 20 years? IMHO this is still a loss.

Second chart. Supply hasn’t even returned to pre-covid and definitely not to 2003. Again, more people now than 2003?

Thats what I am also seeing in Cook County,IL.

Wolf makes charts with actual data. He doesn’t seem to be much if a guess the future fellow. Maybe a little sometimes. Sure, we commenters make some predictions. But my goodness, compare the comments here to Zero Hedge. The IQ gap must be 50 points.

Maybe more buyers are paying cash as they made a killing in the stock market?

SuzeB”,

From the article, first paragraph (make sure you click on the links and check out the data)

“The evidence has been piling up for months in bits and pieces: While investors still have the hots for this housing market, potential buyers that need a mortgage and those who want to live in the home they’re thinking of buying are getting second thoughts, as evidenced by sharply dropping sales of existing homes and new houses even as inventories for sale have now risen for the third months in a row and new listings are coming out of the woodwork.

OK, well here is the data of declining home sales: 1. chart total existing home sales; 2nd chart new single-family house sales:

Rolling bubbles? What’s next? Sometimes it looks like the FRB will do anything to accommodate a market…

I keep hearing this as a theory, but I don’t buy it. Here’s why.

If any significant number of people sold stocks to “take profits,” prices would plummet. The entire overvalued market is based on very little selling pressure. So the valuation depends on very few people actually realizing that value.

Now, there is a thing to the “wealth effect.” But the wealth effect isn’t based on people selling their stocks to buy things. It’s based on people feeling emboldened to spend their cash on things BECAUSE of their “gains” in the stock market (leaving aside people borrowing against their portfolios, which).

In other words, the thought process is more like “Eh, who cares if I drain my entire checking account to buy a new Porsche? I can always sell some stock if I need the cash later.”

The problem with this, of course, is obvious. If asset values collapse, the “wealth” is now gone, and the cash is already spent.

That’s why the idea of the “wealth effect” is nonsense. All it’s based on is spending based on money you don’t yet have. And when it disappears, consumption drops, in many cases, enough to counteract all of the increased consumption from the “wealth effect” period.

Wealth effect psychology is real but probably has minimal impact on spending habits of ordinary people with assets in stock market (because their ‘wealth is unrealized until they sell their stocks– so disposable income is otherwise unaffected).

On the other hand, a wealth effect from rapidly rising home values (as in current ‘raging mania’ per Wolf) likely stimulates more consumer spending behavior because the average Joe feels richer when his house ‘asset’ is rising in value without any effort on his part.

More importantly, homeowners can actually extract those paper housing gains through refi’s and home equity loans for immediate use.

“because the average Joe feels richer when his house ‘asset’ is rising in value without any effort on his part.”

Maybe, but even average Joe knows it is a lot harder to sell a house than a stock…so he likely discounts some Zillowfied home price estimate more.

I will admit the refi cashouts are a different beast because they snowmobile-buying-cash-on-hand.

But it would be nice to think the banks making the cash out refis could not possibly be this stupid…twice…within fifteen years.

Cas127, LOL. Maybe if they were keeping the loans on their own books, they wouldn’t be so stupid. But they’re not, so no sweat off their back if and when it goes south (again).

The “average Joe” is actually poorer when his house raises in value unless he sells and take the gain. Otherwise he’s paying ever increasing taxes and expenses just to keep over his family’s head. “Average Joe’s” earnings have not (by any measure) kept up with the rate of inflation, let alone the property tax rates (which went up 18% this year in my neighborhood).

Compounding Joe’s problem, not only is his house less liquid than a stock, but to realize any gains from it he has to not just sell the house, but sell it and then move out of state.

KGC

Even when the seller cashes in a takes the gain they have to buy another place to live, where the prices have usually risen by the same amount or more.

@RightNYer, But he still has the Porsche (the purchased asset) which can be sold for cash.

Heinz, I agree it doesn’t impact the spending habits of ordinary people, but the upper middle class, it definitely does. I know of people who have bought “toys” like fancy cars, boats, and so forth because their $10 million stock portfolio is now worth $20 million.

Anthony, yes, but at a huge discount. That’s why during recessions you see a lot of used luxury goods going on the market. I suspect we’ll see a lot of RVs in the next few years.

RNY, I have to agree on the discounting. But hopefully he was one of the buyers who bought his Porsche before the prices went ballistic in the last year or so.

I’m an old “gearhead” and follow the classic/sports car markets pretty well. I’m still waiting for the bomb to vaporize the markets so I can pick up another (my last one) old Vette since I am still limber enough to get in and out without help (LOL). I know, I am nuts, but that’s my only vice (remaining).

The Porsche has some utility for someone who bought “high” as it still can be driven but is not a vehicle to live in if one loses almost everything. Kind of tight quarters and expensive to feed (premium fuel, of course!).

Anthony,

Sure…but at 35% off – the second the luxury sports car drove off the lot.

90% of goods depreciate (and a lot more homes should too…but DC has fostered a huge debt industry around housing that badly biases home prices upward).

A rich guy like me thinks ok my homes have doubled in price.. so have all other houses. It is a wash. Im no further ahead. I want a principle, summer city, and cottage. I will not do with less.

“But the wealth effect isn’t based on people selling their stocks to buy things.”

That’s too broad of a statement. We don’t know the number of people who sold stock to invest in the housing market. It’s the increased money supply combined with the ultra-low rates that is creating the buying pressure in all asset markets. And for every buyer in the stock market, there is a seller. And billions of shares get traded every day.

The last 5 or 6 properties i have bought in cash. Prices for homes are going up not down. Sorry if you missed the chance. Travel to other countries and they will tell you how they missed the boat many years ago. You will rent and get ubi and be happy! The rest of us will work and have lots of toys.

“they will tell you how they missed the boat many years ago”

Because the technology of how to build a new house (ever) has been lost?

In the end, a house is a manufactured product (with the exception of the land component, which is very theoretically finite) and almost every manufactured product around becomes *cheaper* with time as production technologies improve.

It isn’t hard to imagine that someday this dynamic may extend to housing (we’ve already seen one massive crash from ZIRP inflated heights).

DC has fostered a huge debt ecosystem around housing that biases prices upward…but that isn’t the same thing as saying that 90% of housing has true, eternal scarcity value.

And I’ll buy the dollar depreciation argument…but you’ll note that tvs, computers, etc. have all become significantly *cheaper* despite depreciating dollars.

You are lost. Im sorry i cant help you. Try to find qualified carpenters who are good at what they do. many years in the future drones and robots may be able to tape and finish drywall and lay ceramic and wood flooring…. We wont be around when that happens. So many small minds on these investment websites. Wow. No I wonder i am rich. Thank you

You are wrong. Trust me.

Pilot,

“So many small minds on these investment websites. Wow. No I wonder i am rich. ”

You sound less like a wealthy man than a 14 yr old troll.

Step through why you think it is impossible for the supply of higher end housing to outstrip the demand for it…then explain what happened in 2008.

Mkts respond to price signals…huge overvaluations in housing will shift labor and ultimately increased supply into those mkts (maybe way too much supply…see 2008).

Trolling?

Trolling.

Did some asshat really say “No wonder I am rich.”?!?

Hahahahaha…..

Thanks for letting us know!!! I pity the poor people that must suffer this buffoon.

Definitely.

Don’t feed the troll :)

Pilot,

Money is buying you economic insulation right now. But you are discounting the political risk that is mounting everywhere. You see it at very bottom and think that will never touch you, wait until it spreads up the chain. Last GFC, people still trusted the govt, now not so much.

I live in one of these large cities in a particularly desirable neighborhood with raging home prices, and for the past year each time a house would go up for sale there would immediately be people SWARMING it. Half of them would start an extensive remodel within days, at least it seemed. Total frenzy.

The last two have gone up with little fan fare and have been sitting for over a month with signs still up. Another house I drive by regularly has been sitting with it’s sign up for well over a month now as well.

Just some anecdotal insights to chew on.

I wonder, if like me, many people suspected the covid restrictions to persist much longer that they have. Now that even liberal, restriction-loving, maskerbating places like California have opened up that the frenzied moving is coming to an end, replaced with frenzied car-buying, travelling and other recreation.

If Texas had CA mask rules in place, 30,000 fewer people would have died. I’ll stick with CA, thanks.

Everything is bigger in Texas including Covid deaths and ignorance.

And the number of asshats we’re absorbing from blue states.

Please tell your friends that coming here would be a terrible mistake.

How many people have had their livelihoods destroyed? How many children will have mental and academic problems because they needlessly missed a year of school? My own state, CO, had a substantially lower death rate with far less economic destruction and school disruption than CA, and our Democratic governor has rescinded his emergency health order. I don’t think CA is a model to be emulated at all. I’m not a Texan and don’t think they did everything right but if I were a school age kid or a business owner or working class person, TX has it better.

Please and thank you. You’re not needed or wanted.

Az never really shut down. Masks weren’t worn by most.

We had the highest per capita infection rate – In The World. Twice.

Hospitals full of covid. Too many died.

I’m my area SFH’s went from 450k to 650k with 30yr mortgage rates under 3% in the last couple years. CA prop taxes add another 2k/yr. Heaven help these folks who bought into FOMO hysteria. The 130k down payment might be losing value in the savings account but might look a pretty good if SFH home values fall.

Personally I am now completely out of RE. Rental property is off the books as is former primary home. I am roughly 50/50 cash/index ETFs. Waiting and watching. Patience.

You just might make a killing when/if it hits the fan. Certainly some people did last time around. Problem is when and if but I think it’s clear things cannot continue as they are. Godspeed.

Perhaps buyers are waiting for the government policies to kick in. Hard to see how any affordable housing initiative is going to help this market, while the cost per sq ft starts at $200. This is where seeing the changes in the comparative markets, high tier to low tier would be helpful. Then maybe buyers have heard the whispers, wait for lower rates? The great inflation panic is wearing off.?

In our area demand is still running high. Big builders have stopped taking contracts for new builds and are only building spec homes, as they have to change materials and finishes according to availability. Any pre-build contracts have escalation clauses. There is a big shortage of homes for sale, so that could explain lower mortgage applications, at least here in the southeast.

It will s because people can afford Southeast – come and check the Southwest, LOL

“Several Fed governors have now publicly expressed concern over the housing bubble, over investors’ involvement in the housing bubble, and over the Fed’s providing fuel for the housing bubble.”

Maybe there is some type of bureaucratic obstacle preventing the Fed from tapering. It’s like the Fed is saying we want to stop buying MBS and we should stop buying MBS but by golly we just can’t get Bob in accounting to sign the paperwork so we can actually stop buying MBS.

If my recollection of the facts is correct, in 2007/8 the crash happened because of stupid real estate valuation and the ridiculous ability of anyone to get 3 mortgages. Am I right? Now, real estate valuation is stupid (by a standard inflationary model) but it’s hard to get a mortgage unless you have a lot to put down. Add to that, in 2007/8, I’m going to bold and say this, I think the 1% were not making the kind of loot that they’re making now. What does this all mean to me, three years away from a lifestyle predicated on retirement (part time work)? Nothing. As long as the rich are getting richer, as long as lobbyists are doing their bidding, as long as politicians are doing what they’ve learned to do since Reagan (get paid), the economy will continue to do exactly what it’s doing.

“but it’s hard to get a mortgage unless you have a lot to put down.”

In many cases, borrowers need only provide a 3% down payment to get into the game. To sweeten the pot, borrowers who qualify under certain government sponsored agencies can even get additional down payment and closing cost assistance.

Check out the extremely lenient mortgage loan requirements for FHA, Fannie Mae loans.

Subprime is still around today, only we don’t call it that anymore.

Heinz, didn’t 2007 feature no income verification loans with no money down for sub prime? Conventional loans are now much more difficult; very regulated. Why? Next time around, when the fed sells the MBS’s they own, they’ll be able to squeeze a bit more money out of investors gobbling up the wealth of the country. Save me from my cynicism and tell me that I’m wrong.

I watched a real estate vblog. The guy said yes, houses seem to be overbought. A crash…probably not like last time.

Just as you said, most people but some money down and a lot paid cash. Many have equity of 20% to 30%. They will not jingle mail like HB1 when most of the subprime had zero equity. Remember there were zero percent down and interest only loans back then. Jingle mail caused a domino effect.

Maybe I am wrong, but I do not see the domino effect. Sure we could get a correction of some type but what would cause a drop of over 10% or 20%.

Back in the housing bubble ca. 2005-2007 they jokingly referred to risky housing loans as NINJA loans– No Income, No Job, or Assets.

I would argue that especially with agency-sponsored mortgages (e.g. FHA) we have subprime alive and well in many respects.

FHA mortgages have no minimum salary requirement (according to their website).

Yes, qualifying for a mortgage is NOT difficult if you have a job. I went to an online mortgage broker and requested a mortgage financing commitment to go house hunting. Got approved in a matter of hours with an upper middle-class income flow. The mortgage loan commitment amount was about 4x gross income.

I am not a buyer. I was just checking out the riskiness of loan approvals for investing purpose. They did ask for W-2s.

“The mortgage loan commitment amount was about 4x gross income.”

That has happened to me as well. Then, the realtor only wants to show you homes priced at the top of your approval. No thanks. I learned the hard way not to work with someone who only works in their best interest.

With this push for more assistance to first-time home buyers, I hope they aren’t taken advantage of. At the very least, the gov should hold off until home prices drop.

I have a younger friend who is a mortgage broker here in south Texas. I saw him last night at dinner at the local watering hole. He said both refi’s and new mortgage applications have trickled to a standstill from the frenzy of last year and earlier this year. He made a ton of money on this madness though (he said).

He also sold his own house (he’s single) and is renting an apartment. He said he is going into a waiting period for the “fallout” up the road before he buys another house.

This kind of reminds me of the 2010 time frame when we bought a nice newer 2,000 square foot home out of foreclosure for 1/2 the original build/sell price.

All those people in forbearance that couldn’t pay, will still be unable to pay when it ends. They will have to re-qualify for a modification and may not meet the requirements unless they still have the equity and income. If the income is down over the period, they can kiss their house goodbye. This is not going to end well for many.

My divorced step daughter-in-law who has been unemployed for 15 months is facing that, but she just landed a fairly good accounting job. That’s a blessing for her and her young son. Through all of this she lost a car and owes everybody, including us who just paid $3000+ to have her house A/C repaired. Oh well…..that’s what family is for, I keep telling myself.

I recently told her she should sell the house and get an apartment, but that fell on deaf ears.

“If” the CDC let forbearance ends .

Seems like despite the fact that there are vacinated people and economy is getting back into its shape, the CDC will extend it without even an excuse.

Educated,

Absolutely! Although they could easily come up with some excuse. Up tick in COVID cases. That “transitory” inflation:-) OR, school starts soon. What an even better reason to extend, right? In the south, we start back early August!

From Corelogic for what it is worth.

In the first quarter of 2021, the total number of mortgaged residential properties with negative equity decreased by 7% from the fourth quarter of 2020 to 1.4 million homes, or 2.6% of all mortgaged properties, the lowest in over 10 years. On a year-over-year basis, negative equity fell by 24% from 1.8 million homes, or 3.4% of all mortgaged properties, in the first quarter of 2020.

In the first quarter of 2021, the average homeowner gained approximately $33,400 in equity during the past year. In 2020 it was $26k.

Many who have hoarded some $ will just walk away and move in with family,buy a rv,or rent cheap apt. Paying +6 months in advance.Maybe but a boat and live there?!

” Up the Road ”

No shortage of $$$ waiting for this up the road.

Starting to see more walkaways in my work area.

Nothing like 08…..yet.

I think rising home prices hit the brick wall of what home buyers requiring mortgages can qualify for. Rising rates makes the problem worse. I would also guess that as many work from homers get converted from real employees to 1099 subs the mortgage wall will fall even further as they learn getting a mortgage with 1099 income is more difficult.

Small data point.

I am in a very popular suburb. Was going gangbusters with most houses selling even before going on the market and going way over asking. And the infamous “bids accepted on this date” manipulation scheme most popular.

About a month ago….just hit a wall.

Houses are just sitting now.

Similar thing in my Denver suburb, listing are up 50% since May, things no longer selling in a few hours, I think we peaked in June.

IMHO, the Fed is buying MBS so that when the bulk of the asset side of their balance sheet turns to dust, they will at least hold title to some residential real estate. They will taper and eventually stop buying when they feel they have enough for that purpose. To be buying gold instead is a non-starter for multiple, obvious reasons.

IIRC, the Rentenmark (which replaced the worthless Reichsmark in 1923) was backed by farm land and commercial real estate.

History beginning to rhyme…

Home affordability, along with Income Inequality, may be at one of its poorest levels in American history; U.S. FEDERAL RESERVE TAKE ANOTHER BOW. When some very average construction homes on my street recently went for amounts that were $80,000 and $100,000 over 2020 County appraisals, at market value here in Virginia, I knew that the top was probably in for the local housing “mania” market.

No appraisal and no inspection sales are just plain crazy for a top-of-the-market buyer, but they were part and parcel to recent sales. Top that idiocy with contracted bids that were as high as $35,000 over listed asking price, and Dickens will have to make room for more characters in Debtors’ Prison in the years ahead. A foolish person and his or her money are soon parted.

Now Monkey See, Monkey Do sellers are rushing to put their still overpriced adobes on the market in order not to miss out on a mania and quick & dirty money. Kind of comical, except that the sums of moola involved are at least 6 times what the average homebuyer earns in a year, so recovered from Big Financial Mistakes take a very long time, if ever (Uber will have a key delivery service to mortgage lenders in the years ahead!! Maybe they can make money on that!!!).

So we have Rising Supply coincident with Falling Demand ( Mr. Economy with no Government Handouts the size of previous largess will also assist in being a Demand Buzz Kill!) leads to one very simple conclusion: Sagging Home Sales and Home Prices as reality rears its very ugly head once again in Hootersville. All rockets eventually come back down to Earth.

Mortgage rates will move up faster in the months ahead, faster than the 10-year Treasury will, as the Uber Key Delivery Service kicks into high gear. It’s going to be a very cold winter ahead of us.

I can sort of understand waiving the appraisal contingency, as if you want the house at that price, what it appraises for doesn’t really matter (assuming you don’t need a mortgage). But waiving the inspection contingency is just plain INSANITY.

I wouldn’t buy a used car without having a mechanic look it over. The idea of buying a house without having anyone look for structural problems, termites, black mold, leaking underground oil tanks, or the like is just unfathomable to me.

Well you still have a right to get that inspection, you just can’t go back to the seller for negotiation for any issues the inspection uncovers. But you at least know more about the house you’re about to buy.

For valuable property in Manhattan you must waive financing and inspection contingencies.

Or you can’t even bid.

I’m talking here about great real estate, not the average garbage.

I read this article about this guy from California who bought an oceanfront house with no inspection. Now the cliff face has eroded and it is getting ready to fall down 20 feet to the beach. He has learned Oregon has strict laws against reinforcing on the beachfront so his house is toast. Once it falls down on the beach he will face a hefty charge for cleanup. I guess he should have done more due diligence.

Sounds like an easier walk to the beach, eh?

The sales and mortgage applications are just down from the “WTF” high.

The next “WTF” high won’t ever be as good as your first one.

Yes, well said Seneca’s Cliff!

I lived for 20 yrs in the premier Oceanfront gated community in OR mid coast….and I just sold my home (Bayside, not ocean front) to a buyer with a VA loan guarantee.

I can tell you a thing or 2 about Pacific Ocean erosion, the reasons, mostly not natural but induced by man.

I’ve noticed a number of CA buyers buying ocean front nomes for around 1 million or more…which of course is cheap compared to CA oceanfront….

but WHY they bought what they bought just blows me away. What are these fools thinking?

Any buyer with eyes just has to take a FEW MINUTES & LOOK AT THE EROSION ALONG THE SHORE & the breakdown of 50 year old rip rap & they should have run the other way as fast as possible.

This is not to mention the totally incompetent & crooked (missing, unaudited $ 68,000 that is “unaccounted” for by the finance committee with no resolution!

Who wants to contribute to crooks running the gated community?

Not me….and I used to manage another oceanfront gated community in Or. I know what I’m talking about!

“Can you imagine what this immensely overpriced housing market would look like with mortgage rates at 5%?”

A GLORIFIED TRAIN WRECK

That’s why they are moving Heaven and Earth trying to keep a lid on this giant mess.

Wolf,

Some anecdotal evidence. A few months ago my wife and I put in an offer on a house in Solano county. I commented on here that the house was mediocre and needed a good amount of repair but it’s in a desirable neighborhood. The house sold for $80k or so over asking and had ton of offers with all contingencies waived. We paused our home search because it was crazy. We decided to come back in a week or so ago after seeing more inventory and longer times on the market. (And even some price drops!) We found a home we put an offer on. This time the house was in better condition, newer, same area and had a recent home inspection with no major issues. We offered $25K over asking. We found out a couple of days ago we didn’t get it. We don’t know what the winning offer was but our realtor told us there were only 3 offers on this one and it’s contingent on the winning offer selling their home.

Things are changing.

Jay, I hope you stay patient as level-headed home buyers like you invariably find a great deal (and generally make the world a better place).

That being said, anectodal evidence is often confirmation bias in disguise.

Thanks Artem. We’re being prudent with our purchase so we are not in a rush. When we find a home we like, we offer what makes financial sense and one that we can live with for the next decade even if one of us loses our job. I know that’s contrary to the current sentiment but we know it will work out in the long run.

As far as anecdotal evidence, you bring up a good point. I’ve never heard it phrased that way before but I agree with it. But that’s why seeing data such as the ones Wolf has been pointing over the past year is essential. What he’s pointing to from a macro level echos what I’m seeing.

I don’t know about the rest of the country but in our small section of the Bay Area home inventory has gone up steadily over the past few months. The frenzy has gone down from a 10 to Id say an 8 or even 7.5. Where it goes from here is anyone’s guess. But for the time being it feels like the influx of cash rich, high wage folks is slowing down while the market continues to price out average buyers (the majority of us) which could spell trouble on the demand side.

“Criminal” is the only word I have to describe the Fed’s actions of continuing to buy MBSs in light of the insanely hot housing market (especially in terms of price rises and inventory).

The Fed is supposed to act in a counter-cyclical manner vis-a-vie the economy. What they are doing is the complete opposite of that. I am not surprised when politicians act this way, but for the Fed, who’s supposed to be manned by level-headed economists to act this way is simply negligence.

I have noticed in my area not only a boom in new housing construction, but also a seemingly bigger boom in storage unit construction. Existing developments are expanding and new storage unit developments are popping up everywhere.

Can someone explain this to me. Is this a form of middle-class hoarding?

Lots of businesses run out of storage units when they have to close the retail location or can’t afford retail rent in the first place. If the business is mostly online, or a service they provide at customer’s home, people don’t generally care about the retail location. They care more about the website, reviews, and lower prices.

Thanks, Petunia. Makes sense.

So not hoarding, but entrepreneurs!

Its the hoarders who say they are buying 20 yrs worth of stuff to defeat inflation.

Sounds like a LOT of fun!!

I don’t know the particulars but investment in storage facilities is a tax efficiency thing…people invest in them to offset/reduce capital gains.

I’ve got a good nose for real estate and investing, but I am not going to kid myself that I am as talented as Michael Burry who saw the red flags in financial instruments leading to the last housing bubble and burst. The data shown above looks like we had everyone locked up for a year and then we got a huge surge and recovery. Now we are settling in to a more normal market, and the Case Schiller data in coming months will show this. Also, in many parts of the country we get the summer doldrums. People are less frenzied to get in a broiling hot car and go stand in the broiling hot sun to see a property. Normal.

When you look at the Redfin data, it’s clear that in most metros, there has been a sudden surge higher in listing price, resulting in an abrupt downward trend in pending sales. When houses keep selling within days or hours of hitting the market, only to sell at even higher prices the next month, it must mean that the sellers are asking for too little. Now the sellers are finally wising up and asking for more so that true price discovery can begin.

There are a few dozen houses located right in the Red Rock area of Las Vegas, a popular tourist destination just a few miles outside of the main metro area. At the peak of the last housing bubble, houses there sold for around $1 million. Now there are two bold sellers asking for around $5 million. It doesn’t hurt to ask. You never know what someone might pay. Or maybe since the rich are getting richer faster than the rest of us, it’s only logical that their assets are going to appreciate at a faster rate. Maybe there’s an even greater shortage of high-end trophy properties.

Then why not ask for 50 million? Sure there are sellers that are in the market because they are going to move somewhere else, but no doubt there’s plenty who think they are getting out at the top of the market.

Which is which? Remember, it’s a zero sum game. When a seller sells, he/she forgoes future appreciation. If the rich thinks that houses will only appreciate, why sell? They are the smart money right?

Honestly, I am surprised there’s not a platform for housing swaps already.

“Now the sellers are finally wising up and asking for more so that true price discovery can begin.”

True price discovery is a double-edged sword. If this manic housing market with grossly-overinflated fantasy selling prices is true price discovery then consider the reverse.

When this manic surge stalls and retreats (it assuredly will) we can then get together again and talk about ‘true price discovery’. It won’t be to your liking.

In Canada the Chinese have driven residential rents so high that when Trudeau starts taking in immigrants again through Quebec after Covid-19 none of them will be able to afford rent. In fact rent is about the same as the average person earns in a year. Now there’s jobs but no applicants as none of these jobs will ever fill unless housing collapses in price.

1) Mortgage Applications : draw a line (w/ permanent pilot pen ultra fine no XYLENE, black/ nail polishing removal) between 2016 high and 2018

high. Take a parallel from 2016 low.

2) The 2020 high was a throwover.

3) After correction and a test, applications reached the bottom of the channel. Probably will bounce backup, osc in the channel.

4) RRP is tapering.

5) The victimized mortgage moratorium will enter the school of LI man who didn’t pay mortgage since 1998.

6) Victimization infected soccer. With Raheem England win.

These data points are great Wolf !! Frenzy seems to have abated, but not prices (yet).

I agree with one of the commenters above that RE is location / geographically driven. When the correction starts and finishes, high desire areas will hold their values or come back quickly.

Anecdotal but San Rafael CA was dipping in 2018/2019 and looked to be poised for a correction. My friend’s 900SF house she sold for $825K there in 2015 was $950K in 2017 and then went to $850K during this “dip” and is now at $1.1M. If a correction brings it to $900K. Meh.

Seems to me that the spiking prices are a natural outcome of the lower interest rates. But what buyers dont understand is that these interest rates are essentially as low as they can possibly go. The Fed does not want a negative rate environment and if Treasuries remain above zero, mortgage rates stay higher.

And the really big issue is that the Treasury has not been forced to finance the deficit for the past 4 months. They are basically starving the markets of Treasuries, buying $100 billion a month and using the Treasury general account excess to finance the deficit. That ends pretty soon. Why the Fed thinks it is a good idea to continue to buy Treasuries and MBS when they are not financing the deficit with new bond sales is beyond me. It simply sets up the interest rates to explode MUCH higher when they are forced to end the purchases and finance the deficit at the same time.

I talked to a real estate agent who recently bought two homes because she said inflation is going up. Well, if inflation is going much higher then interest rates will explode upward and housing prices will get stomped on. Investors who dont realize that higher inflation is bad for prices are making a big mistake.

Unfortunately, our politicians will continue to destroy the future of this country for the sake of propping up this mess.

Treasury yields will rebound soon and move up real fast and break through the recent highs as the Treasury works down its balance. That happens in no more than a month. Watch for the housing market to turn real fast in the coming six months.

Great post. Aligns to my POV. Lots of upward pressure on 10yr and mortgage rates from here:

Fed at zero lower bound.

TGA normalizing, 10yr issuance will be up, especially as Yellen shifts mix to longer duration “while rates are low.”

MBS taper guidance coming soon-ish, no way they can ignore next Case Schiller which is moving into red hot buying months.

I think that will take at least 10% of prices in H2. And that should bring more inventory to market, once everyone sees a top.

Unsure about income growth offsetting higher rates, but I think most income growth is on the low end of the spectrum.

Also, let’s see if the Fed allows even a 10% drop… if they protect current price levels, we are truly past the event horizon.

I am a lay person who has happened on Wolf Street in a voracious search to understand the bizarre housing market of the past year. I just haven’t believed much of what I have been reading on mainstream media. As an English major, I am critical in my assessment of information and its source/angle. And although some of these articles and comments are beyond my ken, I read with great interest and am learning a lot—thank you. I was ready to buy my first home around 2007 and contrary to all advice (“It’s always a good time to buy a house!”), I waited. I bought in 2012. Ready to buy up I have found myself in a version of 2007 and so have been waiting again. I am risk-averse and prudent with my finances. Maybe it’s confirmation bias, but articles like these convince waiting is right a second time around. BTW my home has appreciated about 15% since 2012. Some of the homes I had considered in the 2008-ish timeline would have left me with nearly zero gain today.

Look for Days on the market as an indicator that the RE boom is over. Happened in 2005/2006 and will happen again now.

Home building is the US economy.

The US builds homes and exports dollars.

Home building/refurbishing/remodeling is what allowed the US and the world to recover from both the 2000 .com and 2008 recession/depression nothing else.

The Fed is given credit for everything but whether they realize it or not it is home building alone that is the driver of the US economy. If the Fed cannot drive mortgage rates below current levels it all stops and reverses in a shuttering collapse.

It was not the Fed’s intention to see the 10 year yield climb above 1.60%.

The US service economy is BS and is entirely dependent on housing.

At what point will banks simply stop mortgage lending and simply buy treasuries? 2.0%, 2.5%?

Yes, it is that simple and yes we are that close.

I have seen houses in very low income neighborhoods that have been nicely remodeled with nice stuff I would move in them if I did not know better.

Yep, see that here too

It’s simple – you can’t buy a house if there are none on the market LOL

I’m one of those Buyer who backed out. I got a $550K Mortgage many months ago and I just pulled out. The Bank wasn’t at all happy with me !

Why I did this, This Admin scares me. I would rather live in an Apartment watching to see what’s happens. You look at the Last 6 months from where America was under Trump to where it’s now. It’s Daylight vs Dark. They say a Financial Crash is coming, much worse than 2008.

If it happens I want to be prepared to Move Overseas, with no Stings to worry about. That’s how I think since I’ve lived from Europe to Asia.

I’m in the office. Wife is on the phone with the IRS.

1.5HR WAIT. We filed on time for extension. Have the mail dates

and signed receipt of the IRS receiving it. They refuse to accept that

and insist on us paying the fine.

They are threatening to seize our property….of course we filed because

our home & business burned to the ground.

Let them have it. And I’m surrounded by people who believe our govt. knows best for us.

tom21,

“our home & business burned to the ground.”

Very sorry to hear that! Hope you all are physically OK. All the best!

We are doing great! I’ll take material losses any day over

loss of a loved one.

I just can’t convince the Mrs into tiny house & Amish lifestyle.