The market is broken. “Raging mania” rules.

By Wolf Richter for WOLF STREET.

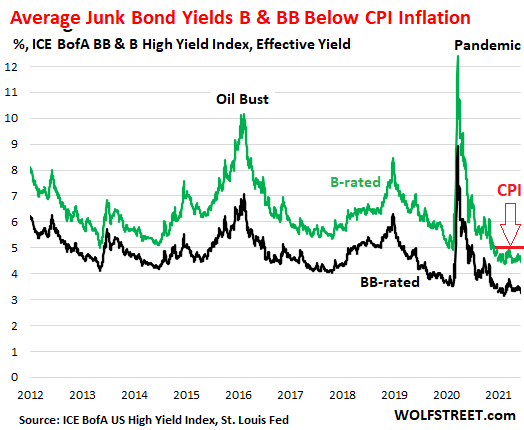

In these wondrous credit markets were everything is now completely out of whack, the first thing that happened, after the freak show of CPI inflation hitting 5.0%, was that junk-bond yields fell to new record lows. Even the average yield of B-rated junk bonds – considered “highly speculative,” per my cheat sheet of corporate bond credit ratings – dropped below the rate of CPI. When bond yields drop, bond prices rise, and a good time was had by all.

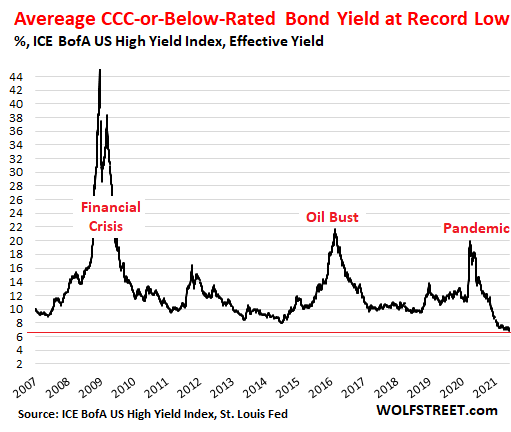

The average yield of CCC-and-below-rated bonds – ranging from “extremely speculative” to “default is imminent with little prospect for recovery” – dropped to a new record low of 6.83% as of the close yesterday, as investors apparently don’t mind exposing their capital to the massive credit risks offered up by CCC-and-below-rated junk bonds, for a “real yield” (adjusted for CPI inflation) of just 1.83%.

Those CCC-and-below-rated bonds are the only category in the US corporate bond spectrum whose average yield is above the rate of inflation.

Everything else has negative real yields, where the purchasing power of capital is being destroyed by inflation, while yields are too low to compensate for that loss of purchasing power. And there is nothing, zilch, nada in terms of compensation for the substantial risk of default and getting mostly wiped out during a debt restructuring.

The average yield of B-rated bonds – “highly speculative” – dropped to a record low of 4.46%, or to a negative real yield of -0.53%. And the average yield of BB-rated bonds – “non-investment grade speculative” – dropped to a record low of 3.27%, or a negative real yield of -1.73%.

Even if CPI inflation, after averaging maybe 5% this year, comes back down next year, as the Fed keeps promising, the purchasing power of the capital plowed into these bonds would be reduced by 5% for the year, and the yield from those bonds purchased at today’s prices would be below that, and the investor would be in the hole in real terms. And that doesn’t even consider the risks of default:

So, on average, these are very unappetizing substances, except perhaps for leveraged short-term speculators who bet on yields to drop even further, despite the surge in inflation, and who could then sell the bonds for more (when yields drop, bond prices rise) to the greater fool down the road.

But long-term investors – bond funds, pension funds, or insurance companies – buy bonds to hold them, usually to maturity. And those junk bonds at these yields today, given the credit risks of the companies that have issued them, are a shitty deal even if CPI inflation were at 2% for the remainder of their maturity.

But now inflation has been unleashed. The Fed is officially surprised by how fast it jumped, having totally underestimated this in their earlier pronouncements. And they’re still saying it’s just temporary, it’ll pass next year. And if it doesn’t pass next year, and if inflation doesn’t magically go back to 2%, then the Fed will act surprised again.

What is permanent is that the purchasing power of those bonds is getting chopped down by the current rate of inflation, and that purchasing power won’t ever bounce back. It’s just a question of how fast the purchasing power declines further next year, 5% or 3% or 2% or whatever.

The yield from interest payments is supposed to compensate investors for that loss of purchasing power, and also for the risk of default – where they could lose much or all of their capital. But investors aren’t getting compensated for hardly anything.

What it has come down to is this: In the Fed-engineered out-of-whack credit markets that are drowning in a sea of Fed-created cash that is now causing all kinds of issues in the banking system, the Fed is trying to control it with it via overnight reverse repos, while investors are trying to find a place to put this cash, and some accept zero yields or negative yields in the repo market, while others are vigorously chasing yield wherever they can find it regardless of the risks.

With so much excess cash floating around, what else are investors supposed to do with their cash – even as inflation is eating it up on a daily basis? That was a rhetorical question. Everyone is trying to find a place for it, but all assets are already overpriced, and yields are already repressed below the rate of inflation for most bonds, in markets that have aptly been described as “raging mania.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The WTFs keep comin

WTF is the new normal..better get used to it then fight it I guess.

So the Fed is complicit, via their cheap money policy, in the employment predicament and the record job openings, unfilled. If the federal govt had to borrow at real rates, the doling out would not happen to this degree, or at all. Nice job Fed.

And we have 5% inflation with zero Fed Funds rates. Never happened before, and all at the hand of the Fed who promotes inflation.

And we have near record lows in long rates, immoderately low.

So, lets review.

Mandate #1 The Fed is supposed to promote maximum employment yet what they do with rates has had the OPPOSITE EFFECT. Fail.

Mandate #2 The Fed is supposed to promote stable prices, yet they promote just the opposite, INFLATION. Fail

Mandate #3 The Fed is supposed to promote moderate (not extreme) long term rates, but we have near record lows, 30yrs almost 2% below inflation. Those rates are IMMODERATE and EXTREMELY low. Fail.

Arrest J Powell for breach of Fiduciary responsibility in his post as Fed Chairman, and let that be a warning shot to all the Fed governors.

SoundsGood!Arrest them all,let Them eat bread and We the people confiscate all their stuff so They own nothing and are happy,or is it dead????Cash should be going into gold and silver,some real estate before Lloyds and Blackrock gobble it all up.Heard Blackheart just gobbled up a whole ,newly built singlefamily Neihhborhood in Texas.Zillow moved into homebuying.Berkshirehathaway signs quietly and quickly popped up all over n.w. Cook County,IL after 08 shakedown evicted thousands of families.More of the same on steroids.Do Not sell a home to them,they jack rents up %30 adding stress to already stressed people.They are also jacking home inflation in some markets.

They advertise jobs paying below market wages or salaries, then complain they can not find workers.

The Fed cannot constrain the spending of the US Federal government, which is not currency constrained.

This has got to indicate some toxin like lead is in our water supplies or food. Given the Enron like shenanigans in even prominent, US companies, I would not get even investment grade bonds today.

It’s not just America, it’s everywhere. Collective global delusion. I wouldn’t buy a bond anywhere in the world, at present.

You buy a bond when rates are high, so that you receive high interest dividends for the term. Right now they are at historic lows.

Worst. Time. Evar.

Take your covid shot, go to the back of the bus, sit down & shut up. Big brother knows what’s best for you.

Nope, just a corrupt, rotten-to-the-core FED and .gov.

Yeah, but nothing that a genius businessman who understands absolutely everything going on couldn’t eliminate. But naturally the evil people he was out to eliminate, destroyed him first, but not completely, fortunately.

It took a famous corporal a while to rise to a position where he could eliminate all these “the enemies of the people”, too, but he and his followers didn’t give up until he had the banking and corporate organizations behind him, and of course the common man.

Not long now

My theory is that we are just a couple months away from a very difficult point for the Fed and the markets. The big problem will arise as the reserves at the Treasury are tapped out and instead of merely spending money that they had already borrowed, the Fed is forced to raise that capital in the markets.

Think of it this way. Over the past months, since February, the Fed has spent down from 1.8 billion to 670 billion and soon to be 500 billion, the reserves that were financed last year at very low rates due to the excessive fear in the markets. But now that the predominant theme in the markets is inflation eating away at capital, the Fed is going to need to raise capital in a market where 1) it must cut back on borrowing to stop the run-away inflation and 2) the dollar is under pressure, so foreign investors will have little reason to want to buy Treasuries when the dollar might drop more than the interest paid and 3) foreign central banks are cutting back on treasury purchases, including BOJ cutting back on purchases.

When you think about the totality of the recent stimulus it includes the Biden stimulus plan (unemployment plus PPP plus stimmies), the Fed buying bonds each month PLUS the amount of money that was spent down from the Treasury balances which did not need to be financed by markets.

Even if the Fed plans to hold down short term rates, how are they going to keep a lid on long term rates if there is little to no investor demand and they need to lower Fed purchases of these bonds to keep a lid on inflation.

I am feeling that the dollar is actually not going to fall further simply because interest rates will begin to rise very soon. It will likely happen after a Treasury auction where there is no demand. That will be the shock the market needs to sell off bonds. I am going to try to plot out that point in time and watch the Treasury auctions closely.

Anyone have an idea of the most efficient way to bet on higher interest rates? Would it be going long on banks, or an inverse ETF on bonds or is it some futures contract?

They cannot raise interest rates very much or the Government will get hit with increased interest payments….. in theory.

But high inflation will make paving old debt easier as it is worth less.

But you need wages to rise too with inflation otherwise people will vote you out.

You are absolutely right. Moreover, if the interest rates on rolled over treasuries increased enough to tame the rising inflation, as happened during Volker’s tenure, the government will not be able to meet its required interest payments and still pay its current military budget and entitlements. Something will have to get cut drastically.

With extremely low rates being paid now, due to the “Fed” manipulation to profit the banksters who pay their “Federal” Reserve 2.5% a year on sums that they borrow from it and charge you and I approximately 25% a year on credit cards, the interest payments are currently only 9% of federal revenues. See “How High Are Federal Interest Payments?” in crfb dot org. That amount paid is $303 billion a year.

If interest paid on treasury bills just doubled, then the payment would increase to $606 billion, which means that $303 billion would have to get cut from other programs. As the article cited puts it, “For example, if interest rates were one percent higher than projected for all of 2021, interest costs would total $530 billion — more than the cost of Medicaid. If rates were two percent higher, interest costs would total $750 billion, which is more than the federal governments spends on defense or Medicare. And at three percent higher, interest costs would total $975 billion — almost as much as is spent on Social Security benefits. On a per-household basis, a one percent increase in the interest rate would increase costs by $1,805, to $4,210.”

Thus, if the “Fed” were to raise interest rates now (after they have stealthily transferred TRILLIONS covertly to their bankster owners for decades) as some have implied can be done easily, the federal government’s interest expense would rise to catastrophic levels as far as the federal budget is concerned. There is a strong motive not to raise them: if they raised them, they would then face greater pressure to close the loopholes that have enabled the rich to evade/avoid paying taxes for decades. See “”The Secret IRS Files: Trove of Never-Before-Seen Records Reveal How the Wealthiest Avoid Income Tax” in propublica.

(I was astonished that some IRS official had the big brass ones that enabled him or her to risk their lives to release these records that will enrage the ultra rich. I hope that the whistleblower’s identity is never discovered for their sake.) See also “Britain’s Second Empire: The Spider’s Web.”

@K Thanks for the information you provided

Sell TLT, or buy TBT, or trade options thereon, or sell ZB or ZN or trade options thereon.

Working as planned. But one day the music (printing) will stop.

One day could be a decade away.

See my post above. I really think we are mere months away from a real inflection point in interest rates. Think of it as a simple supply and demand equation. The supply of Treasuries has been seriously limited due to the Fed using Treasury balances to finance the deficit over the past 4 months, plus the monthly purchases of bonds. That has propped up Treasuries and the whole chain of corporate and municipal bonds whose interest rates are priced in relationship to the US Treasury interest rates.

In just another month, the Fed will need to start floating lots of debt each month. At the same time, they will probably cut back on bond purchases to stem inflation. What happens? Much higher interest rates. I also wonder if some of the CCC rated bonds start to spike, as not only the whole interest rate pictures worsens, but the reality of an economy that will not get back to normal starts to set in and credit quality gets sucker punched on any over-leveraged company.

My guess is the Fed announces they will stop buying mortgage bonds as the first part of their efforts to get inflation under control.

The Fed loves inflating things. Why would they want to get inflation under control. Also as Wolf has REPEATEDLY pointed out, deflation has been rare in this country.

Treasuries are in demand to the tune of half a trillion dollars. It’s an everything bull market due to essentially unlimited liquidity. People are under the impression when the fed says inflation is transitory that prices will eventually come back down. There will be a long lag period before people grasp what is currently happening and come up with policy to change it. It’s a monetary policy solution to a biological crisis, fundamentally it can only fail spectacularly.

Haven’t you herd of the AMC/GME squeeze that’s about to happen? 500K floor? That’s where they will park all this printed money to divert inflation. That’s why they are saying HOLD.

We’ll all escape at once. Enormous wide door; the way to heaven is broad, no?

Oh, the door to Heaven is broad, but the guy at the door is a real brute.

Hell is more accessible

Well, they will wave you right through to Hell- they will even pay for your parking.

“Oh, the door to Heaven is broad, but the guy at the door is a real brute.”

For the demonic elites and plutocrats (demonic in sense of boundless greed and willingness to trample over the unwashed masses) running this crazy B-grade horror show, their mindset might as well be, as Milton wrote:

Better to reign in Hell (current conditions they have created on earth) than to serve in Heaven.

Heaven is a carboy, negative rates are the sugar component, and people .. both market participants and non , are the yeast!

Forgot to add that that yeasty respiration of CO2 is the inflation, turning Heaven into HELL!

Only the ‘bestest’ boyz n girlz survive to imbibe in the Squeeze.

No, that’s actually the road to destruction.

This is like the beginning of an all new big short. If anyone has the stomach for it. Although the premiums will be sky high.

The Bs are the new AAAs. And the AAAs is the new cash+++, putting + because I don’t know what to put.

When these come crashing down and all defaults, it will make the depression look like a minor correction.

That is true but I feel as if the Fed will buy up the bad bonds?

why wouldn’t they.?

So this is not a Bull market or a Dove market but a “Why are you even bothering?” market?

Inflation is not going to pass, nor is it going back to that (BS hedonic quality adjusted) 2% level next year. It’s like freshly poured concrete that’s currently setting up in the psyche of the consumer. Once it cures, it’s going to take some pretty heavy-duty jackhammers to bust it apart.

“….go back to 2%, then the Fed will act surprised again…”

And what will be missed is the simple math…

the 2% will be ADDED ON TOP OF the 5%….

never gets mentioned…ever…

At 5% per year the USD has a half life of 13 years.

These rates going higher is very likely. The FED is supposed to start outright selling bond ETFs pretty soon.

Jeff Bezos does not like inflation. That’s why he’s going to space ;)

11 minutes (unless he does a Major Tom) and when he returns Janet & Lizard have promised to give his loot to the proles. Democracy!

Too bad he’ll find that space inflates the most of all, what with Hubble’s law.

But perhaps… the Fed… knows something more about “dark energy”…

Dark matter, anyway

I for one approve of launching billionaires into space. I only hope they do global society a favor and burn up on re-entry.

They should name the rocket “Icarus”.

Billionaire s don’t pay taxes or give raises while government gives them money hand over fist our money as trump said musk owes us

“Fed Whacked Investors”….what a great term and so appropriate!!! More than ever, “pay no attention” to that man behind the curtain! That’s why it had to be Toto the dog to expose the “almighty” Wizard of Oz…we people, well, we’re just to smart, in fact so much so, that we fool ourselves. So, the question is: who will be “Toto” to expose the “Almighty” Wizard of FED???

Wolf: do you have any ideas?

Trinacria…

“Fed Whacked Investors”…..

How did the Fed expand their powers to minting and taxation.?

For to expand the M2 by 27%, on a whim from likely ONE UNELECTED UNACCOUNTABLE man is remarkable.

And for the Fed, who is obliged to “stable prices” to promote ANY INFLATION is at the least a violation.

5% inflation and 0% return on savings. That is a THEFT arrangement.

H

We heard you the first time.

Brace yourself. You’ll here it again.

“hear” it again.

Powell gets to repeat a promotion of inflation time after time… his self authored mandate….and not a word or mention of his “stable prices” instructions.

Such a weird set of circumstances.

You put money in a bank, inflation eats it.

You put money in bonds, the yields are lower than inflation.

You put money in cryptocurrency and you have lost half your gamble since Elon went on SNL.

You basically can only put money into the vastly overvalued stock market or real estate market and hope it doesn’t crash.

I don’t see how this ends. Either everyone just keeps funneling money into the only two places turning profits and defying inflation and the system ends up with housing and the stock market being non starters for the working class or it all busts and we have an economic disaster on our hands.

Honestly, I can’t really blame the fed for lying about inflation. I think they want to believe their lie because this is a bad situation that they’re in, and a lot of it is their fault but not all of it. They can’t fix the system by raising rates and turning off the money spigot due to politics because it’s already too far gone at this point. Anything other than free money at this point will crash the house of cards if you ask me. We’ve seen how easy the market is to spook.

Agree. They are trapped. I expect more of the same. Just my opinion. Of course it’ll all unwind someday. But isn’t the USD the cleanest dirty shirt? I think they have more runway. And when they run out of runway they’ll come up with a new currency or some other trick and life will go on.

The US budget deficit was ~ 18% for 2020 and is estimated to be about the same in 2021. The average budget deficit in 2020 for countries in the EU was 8.5%

After the end of this year the US debt/ gdp will be around 140% , double the 2008 number and is exceeded only by Italy, Greece and Japan among major industrialized countries .

In 2020 the US dollar was down over 5%

The US easily leads the world in the amount of trade deficits at north of 650 billion.

The US might have been considered the “cleanest shirt” in the past. That is no longer the case.It us now among the dirtiest of shirts

The Feds policies has created massive distortions in ALL markets. It along with the Federal government has resulted in the second highest GINI coefficient( a measure of income inequality) in US history , exceeded only by a short period in the 1920s . We are dependent on the government for 34% of income. By any standards the middle class which has distinguished the US from other countries in the past is at the lowest level in decades.

We have the highest % of low income and low wealth and the highest % of high income and high wealth groups in many decades.

Alot of countries fudge various numbers and metrics. The 2020 and 2021 budgets are ridiculous, but, don’t necessarily reflect future deficits. It also matters who owns the debt. In America, Americans and American corporations own the vast majority of debt.

Right now, there is only 2 major economies, America and the EU (Japan and China are large economies, but not major economies). The question of who will reign supreme, comes down to many things. The question of how integrated the EU will be in the future, is the biggest factor, if the EU cannot become more integrated successfully, it will probably lose by default. Right now, the EU is at an unsustainable level of integration, it will have to become more or less integrated. There are many factors in play and alot could happen at any time.

Sounds like Russia or China but never hear how much I is worth

An air conditioning repairman told me he gets $25/hour. It is not like he is a galley slave forced to row a Roman warship.

Those are the facts, the US is not “the cleanest dirty shirt”. At this point it is just a lie that has been repeated so often that the majority accept it to be true.

US politicians and bureaucrats decided to coast lazily along the path of currency dominance, but you can only coast for so long before you come to a stop.

Also, the US dollar is not “the” world’s reserve currency it is “a” reserve currency, it may have been the dominant currency but the Fed and politicians are ending that dominance.

I’m glad I got out of there. It may be seen as unpatriotic, but I think those who stayed, only to milk the last drop of easy money, are the ones who have betrayed the country and the people who worked and fought so hard to build and protect it.

MyLadyHumps,

And just who is “the cleanest dirty shirt”? Right now, debts are rising globally. All the major and large economies are stagnant at best. Only a handful of developing countries are actually still developing, even prior to pandemic. Those developing countries that are developing are only so, because factories leaving China, are going there, such as Vietnam. Just what is this fabled country with a benevolent government, at the moment?

Until the developed countries snap out of it, there’s not gonna be much growth anywhere.

“I don’t see how this ends. ”

Real estate and hard assets are likely not over-priced for the simple reason a great currency reset may very well be coming. Look to Modi in India who nullified much of the nations cash overnight.

As the US dollar becomes worthless there will eventually come a time when a reset is necessary and a new currency is born, probably valued against gold. All your old dollars will marked be down to their new gold adjusted price.

Or the US could just tax billionaires at a 90% tax rate like in the 1940s. I doubt though that our millionaire congress will allow such an event to take place. Much easier to destroy the currency since the rich are all flush with assets that don’t suffer from currency depreciation.

A sure recommendation for chaos .

Remember Americans own 450million guns and will use them if they perceive that they have little to lose. The Jan 6 situation in Wash. would be a nothing in comparison to what will happen with a currency reset.

Quite true.Also was going to suggest investing in guns and ammo as theyve become scarce or much more expensive.Chickens also would be useful.

Wealthy people control the supply of bullets. If threatened your precious bullet supply will come to an end. Your typical gun owner cannot make his own bullets.

Non-cooperation and non-participation are what the ruling class fear. Without you, none of their “assets” have any value.

If the game is rigged, stop playing the game.

“Real estate and hard assets are likely not over-priced for the simple reason a great currency reset may very well be coming.”

Real estate prices are denominated in dollars. When $ fiat currency reset occurs and everything in dollars is devalued accordingly, guess what happens to real estate?

it gets valued in whatever replaces the dollar?

Intrinsic value is intrinsic value. It doesn’t need a price to have value. Money is just a tool, mind-blowing, so use it or lose it I say.

“Honestly, I can’t really blame the fed for lying about inflation.”

Give me a frickin’ break, man. The FED is destroying the poor and middle class and you’re making excuses for them?

You could argue that from an objective, unbiased viewpoint, the Fed is destroying the poor and middle class, but at the same time the poor and middle class (the bottom 99%) are destroying themselves. It takes two to tango.

The viewpoint that the Fed is to blame is useful if it makes people angry enough to get back at the Fed and the system they are enabling. The system collapses as soon as some fraction of the population chooses to work less and consume less. Make GDP decline for more than a few quarters or years. The system is too dependent on growth to handle it.

I don’t have any good guesses as to how exactly this will happen, but I imagine that once the financial system resets, everyone will take a 99% haircut and the whole financial Ponzi game starts over from the beginning with 0% debt to GDP. We’ll just have to have a debt jubilee every 100-200 years until people get tired of it and make up a different economic system.

All this means is that all prices go up by 100 times. So gasoline now costs $349 a gallon instead of $3.49 a gallon. If you have cash, you lose 99%. If you have a house, maybe the value goes from $300,000 to $5 million. So it goes down 84% in value in real terms, but up 1667% in nominal terms. If you have a $250,000 mortgage, you still have that mortgage, but it’s only 5% of the value of the property, so it’s almost paid off. If your net worth was $1 million, maybe it becomes $75,000 in today’s dollars. Maybe Jeff Bezos and Elon Musk will be worth only a few billion dollars in today’s dollars. But they’ll be one of the few with the purchasing power to snatch up things at bargain basement prices.

If this happens, it must feel pretty stupid to have spent a lifetime toiling for your nest egg only to see it disappear. Actually, this happened to my grandfather who was a wealthy businessman in Japan. He sold most of his real estate prior to the war and bought government war bonds that would pay off big if Japan won the war. After 1945 he survived through subsistence farming.

“All this means is that all prices go up by 100 times. So gasoline now costs $349 a gallon instead of $3.49 a gallon. If you have cash, you lose 99%. If you have a house, maybe the value goes from $300,000 to $5 million.”

$5 million isn’t 100 times $300,000, nor is it a bargain basement price.

“Maybe Jeff Bezos and Elon Musk will be worth only a few billion dollars in today’s dollars. But they’ll be one of the few with the purchasing power to snatch up things at bargain basement prices.”

What bargain basement prices? That would imply deflation and strengthen the dollar. You said everything would go up in price 100x.

How about stocks? Up or down? Because up means Bezos and Musk will be 100x richer. Their wealth isn’t in cash. Do you think they have savings accounts holding billions of dollars?

The lesson that your grandfather taught is to stay diversified.

In a reset, you take the leverage out of the system. So if the current market is dependent on people paying 15% down and financing the rest, in a cash market, the price might go down 85% so that the 15% downpayment is enough to purchase a home. Indeed, $5 million is around 85% less than $30 million.

I think stocks are even more dependent on leverage as corporations keep borrowing more money and are valued increasingly for their intangible assets. When you look at what happened to big corporations of the past, such as Xerox or Exxon Mobil, it’s only to be expected that Bezos and Musk will lose 95% of their wealth.

The problem is that the Fed has been unwilling to say the truth. The american dream is dead because 1) we shipped all the jobs to china to make profits for the corporate fat cats and wall street 2) we have imported cheap labor from Mexico with illegal immigration to suppress wages, but then taken on the tax burden of providing these poor immigrants with free healthcare and education and other social services and 3) we have enabled a massive bubble in real estate and stocks to create a wealth effect that is a temporary mirage that keeps our numbers looking good.

The core problem is that both the democratic and republican party are 100% corrupt. if you are a partisan who believes your party is not the problem, you are a fool. wake up america. simply cross out every name on the ballot that has a D or R next to it and send washington DC a message.

100% correct.

Stock market crashes black rock buys everything 50% off rinse repeat been happening to long

Lookout below, falling timber…..

Yep, timber futures fell 5.6% last week due to increased supply and decreased demand. You want another WTF? WTF do you think happens when the price of a commodity soars? People smell opportunity.

But then there’s this from one of the timber companies’ spokesman:

“We’re at a new normal,” Reaves said in a phone interview. “We’re going to see this sustained level of housing demand and a new normal for a pricing floor in lumber.”

I’m trying to decide whether he’s Lawrence Yun’s timber equivalent or the reincarnation of Irving Fisher.

This is not a new normal. I live in production country and always have. In 2018 there was a downturn in the industry and ALL companies cut back logging and milling. It seemed reasonable until Covid hit and the insane RE market really climbed. Then, the planned harvest reductions were amplified by circumstances. Simultaneously, many mills shut or curtailed production due to infections and Worksafe restrictions, trucking and transportation was affected, and a shortage of truckers began to develop.

I have lived alongside and worked within this industry for most of my 65 years. It is a boom and bust industry, and always has been. It never stays the same. This summer wildfires might really make spot prices climb, yet it could also continue to drop. My construction supplies were down in price about 10% for May over April. Too bad this years work is done for me as I had to shell out at least 30% more in materials. :-)

In Canada there are new mortgage qualification requirements and a concerted effort to slow the RE surge. The US doubled lumber tarrifs under Biden. Read all the comments on WS and it is easy to see that home purchases, the biggest decision most individuals will ever make, could collapse in a matter of weeks, all dependent on interest rates and/or mortgage restrictions. The same is true of auto sales.

These times are anything but a new normal.

Meanwhile, our forest industry has thundered along and done very well this year. It has helped offset the hospitality and tourism sectors.

And a reply up above about dirty shirts, Canada’s deficit was 10.66% last year, a bit over 1/2 of the US deficit. Plus, our infrastructure has been in continual upgrade for as long as I can remember. If a bridge needs repair, it gets done. New ferries introduced the past 10 years. New icebreakers, a fighter jet decision, hasn’t missed a beat after stopping the F 35 purchase. Water system upgrades, etc…it is all budgeted in and undertaken with parliamentary cooperation, even with a minority govt. Communication and cooperation is the key takeaway.

The US consumer economy is so damn big that dysfunction in any aspect of the Country ripples throughout the World, especially with neighbours and allies; suppliers. I look at the deficits and dysfunction and simple increase my savings and preps. :-)

One more point about the “cleanest dirty shirt”, not only is Canada’s deficit much smaller than the US and more of the money spent on quality infrastructure (rather than targeted to transfer payments to lazy people for consumption) but Canadians also receive healthcare in the bargain – that is huge.

What really needs to happen in construction is an evolution away from building with timber. It is a really labor-intensive process and timber is at risk of water damage and is just a horrible way to build a home. There just isnt much innovation in the building industry. Too much risk in building with techniques like aerocrete that are common in Europe. Once again, our problem is a horrible government.

As a passionate participant in the construction industry for over 60 years, I could not AGREE MORE with your comment gtv!

Time and enough for our industry to get its head out of the sand/mud/ a***,, and get to work with all the modern and much more efficient AND long lasting techniques/materials such as 3D printing of solid concrete for where the earthquakes do not permit ”blocks” AKA Adobe,,, etc…

OTOH,,, some of the ancient techniques, Adobe for one,, work well for ”home made” houses,,, and many other similarly home made techniques, though usually labor intensive, continue to work well, EXCEPT for red tape not allowing them…

Friend bought an Adobe, reputed to be over 100 years old,,, completely burnt out of any and every wood component, but all the Adobe ”bricks”,,, 14 inches thick,, were still perfectly OK,,, they, ( he and his significant other, ) added floor, roof, windows, doors, and interior walls, plumbing and electrical, and had a very nice house for about $20/SF…

My home is bricks and concrete; it will last 1000 years. :)

” what else are investors supposed to do with their cash….but all assets are already overpriced, and yields are already repressed below the rate of inflation”

MPLX

If you People dont buy Silver/Gold your going to be Scroomed

#GOTSILVER?

Read upon Basel 3 not a good investment either

Then you don’t understand Basel 3.

It kicks the legs out from under the paper exchanges, diminishing price manipulation and allowing a true market.

Supports my thesis that corporate bonds are bulletproof. Fed sold theirs and etfs are surging. Meanwhile the treasury YC is coming down a bit harder at the short end. That is probably also positive. Interesting that Qa and QE are almost the same thing, conspiracy theories with mainstream credence and support.

The only logical explanation to investor acceptance of zero or slightly negative yielding bonds is that they believe there is a crash coming soon??

ThePeanutGallery,

If you expect a crash of any kind, the last thing you’d buy at the top are junk bonds. They will take a huge beating (look at the yields during the financial crisis) because many of them will default.

If you expect a crash, you wait (with your money in Treasury bills) until the crash has played out, and THEN you pick through the rubble and buy junk bonds when they yield 30% or 40% and hope that the companies survive.

These low yields show that no one is expecting a crash (which is of course one of the required conditions for a crash; you don’t get a crash when everyone is expecting one).

Excellent comment. Revealing. It points out the duplicity.

Wolf,

Thank you for yet another fantastic analysis. I am one of those who, sadly for society, expects a painful crash. I am heavy on cash. I stand ready to pick through the post-crash rubble for properly priced assets (“there are no bad assets, just bad prices”). I am sure that assets in all classes are overvalued. But I have no idea *when* the crash will occur. What chain of events might trigger the mass selloff that can reign in the current market mania across asset classes? I think many of the regular readers of this forum have exactly this question on their minds. If you have any insights on triggers and/or timing of a correction, I would love to hear them. Thanks again!

Basel 3

Looks like Fall is a good candidate for the crash. When much of the stimulus has run out and the drought caused food shortages show up. Inflation will have taken its toll on corporate profits. Lots of signs point to Fall.. So it won’t happen in the Fall..

I’m not trying to be a wise guy, but I was listening to Harley Bassman on a podcast the other week and he claimed that up until 1998 stocks and bonds moved in unison. It was only after the creation of the Feds new policies at the time, that bonds became a hedge to stocks (that is they moved up in price when stocks moved down). Hence we saw birth of the all weather portfoli by Dalio that rely on this principle as a hedge.

So maybe we’ll see at some point stocks and bonds go down together? Many funds will have zero hedge!

Just a thought.

That’s because Clinton removed all of the post depression era rules like the Glass–Steagall Act, sherman anti trust act ..etc that prevented these types of fed manipulations

No, if they believed this, they would get out. A real crash will result in most debtors defaulting.

The best explanation for this behavior with pension funds, bond funds and insurance companies is that those directly making portfolio decisions aren’t putting their own money at risk. It’s someone else’s. Same goes to a substantial extent for all institutional money.

This explains a lot of the behavior in this manic environment.

As for the buyers of the bond funds and insurance products, I’d guess most of them don’t have a clue what they actually bought or own. Those that do presumably are relying on the FRB put.

Or doing it due to TINA or FOMO (though not for bonds).

Mike Green talks about flow of funds into passive index funds being an important feature of today’s markets, without historical precedent. According to him, something like 90% of new money going into the stock market is going through passive index vehicles, so with a diminishing share of active managers (50% of assets), you have an increasingly illiquid market that operates on simple flow-of-funds via automatic IRA contributions, pensions, etc. That is great on the upside, but not on the downside, and would explain some of the manic action in markets.

I assume you say it’s bad on the downside because the “good” companies get dragged down with the bad?

RightNYer – when I say “good on the upside / not on the downside”, I just mean for whoever is invested at that time. It’s not a social or economic critique on what a desirable outcome would be.

and flow of funds only continues because the monetary supply is debased constantly by both our Fed and other central banks.

Maybe they just shorted the hell out of them, like some did in 2008, but it didn’t go as expected and now we have got a good short squeeze going?

Core inflation is at its highest rate in nearly 30 years. People warned about the dangers of deflation. Have not seen it in awhile.

Once they get this computer chip shortage solved, they might output more new vehicles.

People working from home may not need two cars.

More states will be ending extended unemployment benefits this month.

Eviction moratoriums are also scheduled to end. A landlord put the tenants’ furniture by the curb and changed the locks. They were evicted.

“Once they get this computer chip shortage solved”

Due to pent up demand from the now known to have been pointless shutting the world down for a year combined with the HUGE lead time and COST for more integrated circuit production facilities (“foundries”) and a reluctance to greatly ramp up capacity due to that lead time and great cost only to have expensive excess capacity sitting idle after the crunch is over, the shortage is going to last a long time. One industry expert claims at least into 2022.

What is the “pent up demand” in electronic? In travel, restaurants, theater, yes, but I haven’t heard one cogent argument in support of this meme. If anything, demand for electronics was pulled forward.

Nearly everything has “electronics” in it. Refrigerators, washing machines, HVAC, cars, boats, planes, even your doorbell and your kid’s toys.

The “pent up demand” is from manufacturers who need components to continue production. From customers who need a new fridge.

There is no “pent up demand” for experience (restaurants, theater, travel). Those meals / plays / trips will never occur because you can’t recover the time that has passed. There may be “demand” but, with the cost of necessities skyrocketing, there may be the will, but not the economic means.

It’s amazing junk bonds are trading at less than a 5% yield. Pension funds can’t buy them so who is buying all these? Is it Hedge Funds?

How the bond market shrugs off inflation risk is unbelievable.

This economy will be a case study in the future.

Stocks are wildly overpriced. Gold doesn’t provide any income. Vaporcoin is gambling. So pension/insurance hold their noses and go in the Fed’s outhouse.

The Fed is making water run uphill…

by creating, now….$120 Billion A MONTH!

The Fed is the biggest enemy of free market economics and forces.

They print and print….

They promote inflation when the understandings and mandates for their existence is to FIGHT INFLATION (Stable prices).

They STEAL the value of past labors (savings) and steal the value of present earnings and wages.

Where is the the outrage?

There’s no outrage because the majority of the population is financially illiterate. It’s difficult to be pissed about something that you don’t care enough to understand.

You’re absolutely correct. It would take Fox news or OAN to break everything down into more digestible sound bites to get the masses riled up over it. I got to hand it to the right side of the political spectrum, they have messaging figured out.

Anyway…more to the point, the masses are far more interested in baseball than the economy.

I do not know that the so called lack of outrage is attributable to ignorance.Firstly,I have gone to many other sites where there Definitely IS Outrage.People are trying to contain themselves and take individual survival action.They are encouraging and helping others.Secondly,someare outraged but do not know how to turn that into useful action.Should they visit their corrupt madon congressperson or the blackmailed puppet Senator?Should they vent very angry,hate-filled comments/emails and get arrested with the kids taken?

One way to address it longer term is to start teaching the basics of personal finance to students from kindergarten on up through grade 12. How far do you think a proposal like that would get in the face of the financial planner industry lobby?

The average citizen is willfully ignorant about the economy and finances. Period.

The savvy ‘literate’ ones may make up only a small percentage of population– but even most of them are all-in on current market manias now– so they are willfully and obligingly participating with full risk-on during the craziest economic environment imaginable.

But one thing social upheaval phenomena like the Arab Spring teach us is that complacent masses do have a breaking point. When they can’t fill their belly or afford decent shelter in large numbers you will see a seismic shift in popular opinion and action.

People who have nothing to lose are likely to ‘lose it’ and vex their ruling regime.

There’s really little to be done with any situation where the leadership is either failing or pillaging until it gets so bad that a critical mass of people willing to support insurrection or violence to fight it.

If you don’t have enough people on your side, whatever you do will be considered terrorism and you’ll be crushed. You have to have enough people first. And right now, people are generally comfortable, so there isn’t.

historicus; Spot on. The fed needs to pick a winner and a loser at this critical juncture and the american people have been deemed the losers under their current policies. BY the people for the people of the people thank god for this representative republic /s

Gordian….

Thanks and absolutely!!

Congress is complicit as they hold the reins on the Fed.

But free money is FUN!

AMC sold 800m in stock last week. It can use this money partly to buy back bonds. As long as companies can sell stock at silly prices , there is no need to finance via the bond markets. Those companies whose stock prices are selling at the silliest prices often are the same companies with the most junk bonds. At this rate there will no longer be junk bonds

“Who is buying them?”

Most likely it is the ETFs..

and

The Bond Funds

Spread out the risk and get a return. No Personal involvement..

And So Far there has been no huge blow up.. So there is No perceived risk.

The bond market? What bond market? There is no bond market, there are only those who are forced buy bonds and those who are not.

The Fed is buying treasuries, with money they create, at a rate of $80,000,000,000/month.

There is no market in bonds. Bonds exist only as a conduit for the Fed to monetize government spending – that does not constitute a market.

This economic stew is turning my stomach. I thought the Carter administration’s economy was the worst in US history but now I feel this is worse. There is nowhere to run and nowhere to hide. Whatever you do you are a loser. So said Rich Edelman on his financial talk show to people who play it too safe. He advocated getting into the casino because there is no other choice to preserve capitol.

I’m getting so fed up I’m going to protest by cleaning out my bank account and holding cash. Yes, green US dollar bills. I will only keep enough to cover monthly expenses. Why leave anything in there when they are giving you negative interest.

Thanks Wolf for your great coverage of what’s going on!

SC,

Read this and immediately thought if you. We’ve been here before.

“Deustche Bank’s chief credit strategist Jim Reid correctly points out that “the data isn’t going to change anyone’s mind of whether inflation is transitory or not.”

Still, as an aside for those who still care about fundamentals, he notes that the current gap between 10yr US yields (c.1.5%) and US CPI (5.0%) is a whopping 3.5%, the highest since 1980. In fact, the gap has only been more negative for 10 months in the last 70 years, all of which were in 1974, 1975 or 1980.”?

This is why you own Tips, for the spread. The Fed will always be behind the curve. Nominal inflation is not the issue. The Fed will have no choice but to implement YCC, keeping yields within reason. Now corporate bond yields are dropping, that’s more incentive to repress the surge in Treasuries. By the end of summer, inflation, supply chain problems, and unemployment numbers will have corrected, and the recovery will not look so red hot. That will be a scary moment, and they reissue the 30yr TIP in July.

You forgot to include the drought induced food chain shortages and disruption. We might have to add in some social/political disruptions too.

I just don’t see how any of your list will have corrected by Fall. These things take time. Low rates and disruptions/shortages will mean higher input costs and that either means higher prices or lower profits. Or Both!

I don’t think that things will look very Rosy in the Fall.

Then again, I have been wrong much more than right so Maybe!

RE;Econ. You know this, inflation expectations are tied to growth, and when they comeback that will not be a rosy moment. The yield in July will probably be higher yet than it was at issue, however inflation expectations will have come down to earth. Should the dollar collapse, hard, you could double your principle, which you may be able to invest at a discount. Nothing gets by the smart guys, you just have to wait and see.

Max out $10k a year at Treasury Direct ibonds yielding 3.5%, which are basically inflation adjusted. As a US bond no risk of default

https://www.treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_ibuy.htm#what

Sorry, this 10K is chump change. Its not protecting the rest of my nest egg from inflation.

Since my total holdings outside of tax advantaged accounts are still rather meager, I’ve been considering these I-bonds. However, with official inflation figures moderately understated, I’d still be losing purchasing power.

In this regard, stocks look more attractive. But we also know the equity markets are eventually going to reset and return to the mean. So, perhaps for the next year or two, I-Bonds might make sense. When the dust settles for the equity markets then naturally I would want to revert to stocks once again.

If they are paying interest based on the CPI, then they are paying you below the real rate of inflation. The website states that they pay a fixed rate and an inflation-based rate, but that fixed rate is set at 0.00%. They are thus paying interest based on the government numbers for inflation, which are widely believed to be intentionally set low.

They are paying 3.54% right now but the CPI just hit 5.0%, so it’s really paying interest based on the lagging CPI numbers from the last full half of a year.

This is indeed better than nothing, and actually beats the interest on most bank accounts, but it’s still not a good long-term investment in a time of accelerating inflation. If you want to park $10k because you intend to buy something big such as a car or house in a year or longer, then it would be a sensible alternative to a checking or savings account. You can’t redeem the bond for a year, so it’s not suitable as an emergency fund.

If somebody wanted to build up $10k a year for a down payment on a house, and they don’t intend to buy for a year from now, then this might be a good spot to park the money every year.

“There is nowhere to run and nowhere to hide”

Yep…

and not a condition created by free market economics, but by decision making by people who have power, power based on assumptions of conduct as outlined in their mandates, who IGNORE THOSE MANDATES!

“Stable Prices”? “Moderate long term rates?”

The Fed promotes INFLATION which is a TAX…

they are suppose to FIGHT INFLATION and they have no power to TAX.

Actually Carter put Volcker in charge at the Fed and told him to do whatever it took to stop inflation.

Carter is blamed for a necessary policy of austerity made necessary by the poor policies and decisions of his predecessors.

Carter took his lumps unfairly but he can be proud of who he sees in the mirror – something Powell must be incapable of.

Gold is not over-valued

I understand. But the people that sold Gold today thought so or they wouldn’t have sold :-]

Great Site Wolf, Thank you. In reply, I am not worried about daily moves or even short-term changes , just the preservation of my hard earned money.

Not much physical gold being sold only the paper stuff

Doesn’t matter. When you go to sell physical, the first thing they do is look at the paper price.

Who “sold” gold today? Were there big lines at the local coin shops? Did people empty their safes?

No, it was gold contracts and the vast majority of buyers will not stand for delivery. Theyll settle in cash. Comex is bullshit.

The US Mint announced months ago that they would not be producing certain silver coins due to the fact that they couldn’t get enough physical silver. Why isn’t silver at $100 if the US Mint can’t find enough? That’s definitely a broken and manipulated market.

BTW spreads between spot and physical have been increasing for quite a while. You can’t buy physical anywhere near the spot quote.

Spreads tend to widen during times of uncertainty. In 2008 physical gold cost 25% more than spot. So if spot was $800, physical was $1,000.

At the beginning of this month spot was about $1900 while a 1 oz gold coin went for about $2100. 10% premium.

THAT IS ALL ABOUT TO CHANGE (maybe. I hope)

Basel 3 is going to destroy the fake gold market. Before Basel 3 banks could hold reserves in either physical or paper form. Perversely, unallocated paper gold (contracts) could be valued at 100% for calculating reserves. Physical gold (allocated) was valued at 50% for reserves. Hey, we found another WTF!

Basel 3 moves physical gold from Tier-3 to Tier-1, allowing it to be valued at 100% for reserves. Up until Basel 3 there was obviously a disincentive for banks to own physical.

Paper gold going forward will be valued at 85% for assessing the banks assets, but the bank will need the equivalent value in reserves to offset those assets. Unallocated gold would no longer be considered reserves; it would be an asset requiring matching reserves.

Starting to look unappealing? These rules go into effect at the end of the month. It will either kill or badly cripple paper gold. Then there will be little or no spread between physical and paper.

There will also be no monthly slams of the price as expirations approach.

ATTENTION FED HATERS: another reason to hate the Fed (and its fellow travelers the US government, BIS, and other central banks)

The paper market enables these entities to manipulate the silver and gold prices through . . . . . wait for it . . . . fractional reserve trading.

By selling large amounts of unallocated metal without having to deliver it in physical form the US government and the NY Fed can make it appear that there is a lot more metal than there is, thus suppressing prices.

Precious metal prices are a reflection of perception of the stability of the economy. If PM prices rise, currency values will likely fall and interest rates go up. You might have seen discussions about how bonds went this way while gold went that way. That’s what’s behind it. There are some who say the Comex was formed in the 70s precisely to enable fractional reserve trades.

It’s estimated that the ratio of paper gold to physical is about 100:1. That’s why I have said repeatedly that if only 5% of Comex traders stood for delivery it would destroy the Comex. There wouldn’t be enough physical gold for delivery.

Paper gold is down but not beaten. There are very powerful forces with huge stakes here: The US government, the Fed, BIS, Comex, LBMA, and banks in general.

There are a lot of pigs feeding at this trough. We have about 3 weeks til lift-off and I wouldn’t be surprised to see the implementation date moved back to allow more arm twisting or back room deals.

Anything to deny us free markets.

Michael Gorback,

Just to this one point:

Try this: buy some gold at a dealer and take this gold with you and then two hours later sell it to another dealer. There will be a spread, a big one. That’s how dealers make their money. They will SELL to you above the spot price, for sure for sure, and they will BUY from you below the spot price. That’s their business model. How big the spread is depends on the dealer.

The US Mint has a shortage of physical coin blanks.

One reason there is a perceived shortage of physical silver is due to the insane buy-sell spreads. Physical silver has terrible liquidity right now, unless you can find another retail buyer and avoid a coin shop or bullion dealer. Buy physical silver since last March and you are immediately in the hole 20% to 25%. Add the unfavorable tax treatment, storage and insurance costs, and zero yield – it’s not exactly compelling, except for buyers who think it’s going to the moon.

Based my recollection of it’s current and historical relative price, it’s not relatively overpriced but not that cheap either.

I don’t pretend to know a lot about PM markets but I know this: the opposite of ‘spot’ is not ‘coin’. No one buying PMs for other than numismatic value buys coin. Even if the coiner is not a govt and wants a profit for its currency creation privilege, a private mint will want one.

I’ve bought the Canadian one oz silver Maple Leaf coins over the years and always knew I was paying extra, or as the dealer put it: ‘it’s too much for an oz of silver. But they are prettier than the wafer. And of course, you are no more likely to get a great price buying an oz of sugar than an oz of a PM.

PS: clarification: ‘spot’ does not equal ‘coin’. Coin is a special category of spot and will always be higher priced. You would pay a higher spread over spot aluminum if you commissioned medallions in aluminum.

Yes Wolf I understand the cost of a round trip in physical. I’ve been in the game for years.

Buy an ounce of gold at spot for $2,000. Pay 10% premium of $200.

Turn around and sell at $2,000 spot and get a bid of $1900.

Right now I’m on Kitco looking at a 1 oz Canadian Mint gold bar for $1946, while spot is $1878.

Bid from Kitco for the same bar is $1863.

I’ve never seen a way around it no matter what the vehiclev- bullion bank, funds backed by physical, etc. For example bullionvault let’s you trade physical atvspot in real time, but then there are the trade commissions, storage fees, etc.

Wolf This statement is not true ” they will BUY from you below the spot price ” they are buying above spot price. Here is an example

look at the buy back price compared to spot

https://www.providentmetals.com/1-oz-canadian-gold-maple-leaf-dates-our-choice.html

That’s a coin. You cannot compare the price of a coin to the spot price. You pay a premium for coins.

This same coin 6 months ago was going significantly below spot price for the buy back. That’s what I was getting at.

If you are really interested in buying and selling PM you need to start hanging around the coin shops and visiting coin shows. Getting to know people who are involved full time, not just dealers, but also collectors. It does take some involvement to know how to buy and sell at the right prices.

I say that to say this. There are quite a few people out there with wads of cash money. Lately, they are looking to buy PM, about anything they can get at decent prices. Hang around the coin guys and coin shows, you will know who they are.

Wolf…

The Fed is partnered up with Blackrock, are they not?

And the Fed is buying mortgage backed securities at rates below the current inflation rate…well below. This seems to be idiocy.

But Blackrock is a GIANT player in residential real estate..

Seems a massive conflict of interest to me…

Your thoughts

historicus,

The Fed partnered with a number of large bond funds, including Blackrock, when it set up its corporate bond and ETF buying SPV. But it only bought about $13 billion in bonds and ETFs, which is minuscule. It stopped buying last year, and it is now selling those bonds and ETFs. That “Blackrock partnered with the Fed” theme has been obviated by events.

PE firms, pension funds, etc., have long bought single-family houses to rent out. This is not new. In recent years, they formed REITs of single-family rentals and sold them to the public in IPOs, such as Invitation Homes.

I agree, there is a surge of investor buying in the housing market right now, but it’s a lot of investors that are doing that, small and large.

The gold market is a rigged market. The value of physical gold traded on the shanghai exchange is around 100 times smaller than the gold derivatives which are traded. That practically could mean that even in times of high inflation the gold price will decrease. Of course everything is legally correct but if you create a lot of paper stuff around the real thing, it is manipulated by those which move the paper.

We read again and again that the derivative totals are much higher than the physical amount on hand. True. And true for ANY commodity traded or not on Comex. The supply of copper in warehouses is a small fraction of the positions. So is copper manipulated? Daily, no doubt, but if short it’s best to take a profit, because there is lots of copper.

It costs money to have an idle ‘float’ available for actual delivery. Since most traders don’t plan on ever taking delivery, it would be wildly uneconomic to have enough on hand to deliver if per chance they stood for delivery.

There are vast amounts of silver that are not available to trading houses for spot delivery.

Factoid about silver. Don’t know it was true last year or two, but not long ago Franklin Mint was the largest US user of silver AND the largest US buyer of silver, including scrap. A lot of the silver it bought was Franklin ‘collectables’, eventually sold for melt.

Neither is silver.

So is gold and silver going up or down my guess down

Gold is reacting rationally at the moment. The dollar went below 90 briefly and bounced back above that number. Yields are dropping. On any day these things and PMs move in tandem. The last term you can associate with gold at this juncture is panic. Silver tends to reflect monetary issues, and has a better chart than gold. Some of the speculative energy came out of the markets last week. Palladium and Platinum consolidating their gains. Oil prices are the inflation wildcard. No economic reason for $70 crude, and on the way to $100?? OPEC+ (Russia) content to squeeze the Imperialists? Potus going to lay down the law to Putin. Saudis lose a friend in Netanyahu. And so the dollar bounced.

The price of gold is up 50 times the value of the dollar since 1970.

Nixon took us off the gold standard. I used to hear about the devaluation of the dollar on the evening news. That was when there was no such thing as ZIRP. Savings accounts paid interest. There were phone booths.

1) UST10Y = 1.5%. // German 10Y = (-)0.27%. // US inflation rate spike = 5%.

2) If US real rates will be minus 1%-2%, in the next 10Y, on $30T

debt, the gov will collect : 10Y x $30T x 0.02NR = $6T. For 1% = $3T.

3) US pension & health promises are down, because 500K elderly perished

during the pandemic.

4) US gov can sustain an average deficit of 5% – 7%, for 10Y, to stabilize the economy, including few deficit spikes. It cannot be done under

the gold standard.

This was in 2020, the last full year for which they have collected statistics, deaths this year are not counted yet as the year is not yet over. I’m using this study to compare annual mortality rates. Those went up by 15.9% last year, which is significant, but not enough to affect future demographics by a huge amount in a population of 330 million. 375,000 / 330,000,000 = 0.1136%.

I am so old, that when I began paying into Social Security, a dollar was actually worth a dollar. Today Social Security is repaying me in dollars that are worth less than nickels.

So think about that if you are a younger worker… If that trend continues by the time you retire your benefits will be worth about 1/4 of one cent per dollar….. But at least you can look forward to 1.5% increases as inflation goes up 8%…

Premeditated THEFT by the Fed that exists with the understanding they will promote “stable prices’.

We have been made love to right up the digestive canal.

You sure are drilling this FED is not doing their mandated job message into our heads!

I remember actually hearing Kashkari smirking over the radio in 2017 when he said “… and the Fed defines stable prices as two percent inflation”

Well, that’s stable inflation, not stable prices.

As as equally aged ‘investor’ as you AA, I can only reply that it’s about damn time that everyone knows what the FRB has done to us working and now formerly working folks.

I was ranting about the Fed back in the 1980s when I decided to get out of the SM after 30 years of so, because it was obvious then,,, just like now,,, that the Fed was absolutely conniving to distort that market and the RE market.

Been on Wolfstreet trying to figure out anything ”safe” and worth investing idle cash, just trying, so far without success.

This was precisely the dynamic that created the populist push by William Jennings Bryan in the 1890s. Farmers took out debt but then the ‘gold standard’ some readers here are fond of took over and farmers didn’t get the prices they anticipated. So they ended up paying with expensive dollars that which were borrowed in cheap dollars. They couldn’t pay. Good old gold. Screwing the working stiff while the rich laughed all the way to the gold bank.

My take on all of this financial repression is that governments are slowly but surely closing all of the escape routes out of fiat currencies.

An example of this is the new Badel III gold regulations. The net result of making it more expensive to operate in the gold market, whether paper or physical gold, is to reduce the number/and or size of market makers involved. This reduces the overall size of the gold market. This then reduces the number of market options available for investors to invest in gold.

So if investors suddenly decide they want to buy gold with their fiat currency, the door maybe too narrow to squeeze through or even be closed during a crisis.

While physical gold supposedly pays no interest, holding some over long periods of time, pays a higher rate of return than fiat currencies do. One can also sleep better for whatever little that is worth.

Basel III should not prevent buying physical gold. It only makes life harder for paper) unallocated gold.

It appears that it will cause problems to the bullion banks. Doesn’t make sense why the BIS would do this.

There’s gotta be a catch, I just don’t know what it is yet.

Like after Roosevelt had most gold forcibly redeemed by Americans and then voila,magically it went up Drastically in value!!Ancestors got screwed.Hide your metals in various hideyholes,Not security boxes,especially at a stripmall.

The easiest way to discourage buying the physical metal is to make it subject to sales tax or VAT and increase income taxes on it.

There may be capital gains taxes due on metals, coins or other collectibles.

The USA the leader and protector of the Democratic free world BULL SHIT .Your FED and congress are so corrupt and have been robbing you and the rest of the world blind You sleepy stupid Americans are allowing it to happen. A disgrace to your forbearers.The mistake they made the fed should have been elected by the people not appointed by government where is the independents. How bad does it have to get before you stupid Americans wake up to being lied to and screwed where is the protests at the Fed and congress what a big FAT DISGRACE not only to your country but to the rest of the world

World keeps buying U.S. Treasuries and investing in U.S. for most stable safe yields.

Which means the world are greedy insecure amoral enablers.

Given your rant I am going to assume that you would do no better. It’s easy to be an internet keyboard warrior. Perhaps you should be protesting outside your own government demanding that they take action. If your government is letting these stupid Americans “rob you blind” then maybe you should be complaining to them.

What country are you from, Bruce?

The Fed should be held to their mandates…

Mandate #1 The Fed is supposed to promote maximum employment yet what they do with rates has had the OPPOSITE EFFECT. Fail.

Mandate #2 The Fed is supposed to promote stable prices, yet they promote just the opposite, INFLATION. Fail

Mandate #3 The Fed is supposed to promote moderate (not extreme) long term rates, but we have near record lows, 30yrs almost 2% below inflation. Those rates are IMMODERATE and EXTREMELY low. Fail.

Arrest J Powell for breach of Fiduciary responsibility in his post as Fed Chairman, and let that be a warning shot to all the Fed governors.

“You sleepy stupid Americans are allowing it to happen”

Please get a clue. The following is most likely the case for your country, too:

Study: Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens [Princeton University, 2014]

Excerpts:

A great deal of empirical research speaks to the policy influence of one or another set of actors, but until recently it has not been possible to test these contrasting theoretical predictions against each other within a single statistical model. We report on an effort to do so, using a unique data set that includes measures of the key variables for 1,779 policy issues.

Multivariate analysis indicates that economic elites and organized groups representing business interests have substantial independent impacts on U.S. government policy, while average citizens and mass-based interest groups have little or no independent influence. The results provide substantial support for theories of Economic-Elite Domination and for theories of Biased Pluralism, but not for theories of Majoritarian Electoral Democracy or Majoritarian Pluralism.

In the United States, our findings indicate, the majority does not rule—at least not in the causal sense of actually determining policy outcomes.

When a majority of citizens disagrees with economic elites or with organized interests, they generally lose. Moreover, because of the strong status quo bias built into the U.S. political system [that describes the overwhelming influence of the administrative state and lobbyists – W], even when fairly large majorities of Americans favor policy change, they generally do not get it.

To be sure, this does not mean that ordinary citizens always lose out; they fairly often get the policies they favor, but only because those policies happen also to be preferred by the economically-elite citizens who wield the actual influence.

Elite dominance is a major problem but not the inability of the electorate to get what they want. The solution to this problem (if it were possible) is decentralization and cutting the size of government drastically.

The majority of the voting electorate can barely manage their own life properly and has no business making decisions for anyone else.

Obviously you have to get in to meme stonks , AMC and GME to the moon.

Pretty much all a meme these days !!!

as long as there’s beer and ball games it’s all good! ( sarc) You know either the fed is buying everything forcing rates down or there is an incredible deflationary collapse coming out there somewhere and that’s being reflected in these low rates.

If money has little to no time value(interest) it is essentially worthless. Read a real estate story out of Austin, TX where a woman was going to sell her home for $400K, based on comps. In the month it took to prepare the house for sale her agent upped the listing to $450K. The house went for over $700K. I saw a picture of the house and thought it was worth $250K on a good day.

While some see this example as exploding value in the real estate market. I see worthless money and disaster around the corner. And I have seen this before, in 2008 in Florida. And to a lesser extent saw it in NYC in 1987, after a bad day in the market.

Blackrock,Lloyds,and others are sucking up huge numbers of singlefamily homes,sometimes whole neighborhoods.They are becoming huge landlords.Heard on other site this week that Blackheart did this and summarily raised rents %30!!!!These assets can then becomefoundations for margin in markets,no?ETFs and other ways to squeexemore$$$?Must be nice to get free money and buy Actual,useful assets which you then get even more money for all because you are well-connected to cabal.

Waiting for Wolf’s posts to bust past WTF and into Dogs-On-Fire “This Is Fine” messaging.

Can the crash come so Wolf doesn’t get whiplash whenever he checks market data?

Jerome Powell…

“Let them eat inflation” June, 2021

A major War with nuclear weapons delivered from a variety of platforms. If that happens all major cities will be obliterated , all major military sites will be extinguished and the earth will be polluted by radiation for decades.

The chances of a major war are as close to zero as you can have imagine, while the chance of nuclear explosions by accident is not

Chasing yields is fine if you have no debts of any kind and all your living expenses for the next 10 years is salted away and you don’t need that money for even a whim.Inflation on $700 a month for food for two at home and at restaurants at 10% a year ain’t going to bother you and in fact the masses will revolt way before you collapse. The Fed, which is Congress’s bitch, cannot inflate its way out of its box without destroying the country. The Oligarch’s are not part of the country and they will be made whole,always are. Not you or me. There has never been a nation that has inflated or taxed itself to claim the sound money it de-based. It’s a bullshit wet dream that people repeat and never think about it. If you are chasing yields while carrying debt you may get screwed when this bizzaro economy flushes out , and it will. It is not different this time and you ain’t going to know when it will happen. Price of junk silver is $35 an ounce which is a 20% fear premium over the “market price” of silver at $28 an ounce. When you see fear premiums of 20% on a tangible there is no rational market. If you ain’t an oligarch you better start thinking like the peasant you are in the neo-feudal system that we have allowed to happen.

Great comment!

Believe it or not, the US did tax itself back onto the gold standard after it issued greenbacks – paper money – during the Civil War. During the Civil War, the ratio of gold money (coinage) to greenbacks was an effective barometer of the level of success that the North had on the battlefield. Read “Battle Cry of Freedom” – a great history book – for more detail. After the war, the government very slowly retired the greenbacks and went back on a true gold standard.

It CAN be done.

Then the Fed was born in 1913 and that then led to the de facto end of the gold standard in 1933, when all the gold was confiscated and the government just bullied everybody into accepting a dollar that couldn’t be converted into gold by the average citizen, because it was illegal for anybody to own gold.

We just have absolutely nobody, except maybe 1% of the most fanatical true capitalists, who wants to go back to the gold standard. Hell, we can’t even balance the budget for a single year during the best of economic times. Imagine demanding a $1 trillion annual surplus for 28 years to pay off the national debt – nobody would elect a party that ran on that platform.

Today there is so much fiat money and government debt that we’d need to value gold at something like $50,000 an ounce to have any chance of reinstituting a gold-backed currency. Otherwise, everybody would immediately redeem all the paper fiat for gold.

The music may have stopped playing for condos in the Swamp.

Just did one today in a good location and it had sat on the market for almost 90 days. They had to drop the price 5K to make the deal. The sellers had already bought another townhouse and were trading up, so they owned 2 homes for 90 days or more. If this is indicative of a trend then look out below. This is what happened in 2005/2006 when time houses sat on the market increased dramatically.

Condos have been wobbly in other cities too.

This condo softening is something new here, but I’m not sure its due to people trading up to townhouses, shadow inventory appearing on the market, or just people moving out of urban areas to the suburbs. Will have to get more data.

Seeing price reductions on condos, land and a few SFHs here in SD.

I hope you’re right.

Now all eyes turn towards Fed.gov to see what stimmie plan they’ve concocted next to prevent the dreaded fall in housing prices or rent.

And the injection of free money into the economy is a surefire way to cause a huge amount of inflation.

Good write up re Comex and Basel3.

TFMR and especially TF would be proud of you.

AG and AU to the moon ??

1) CCC Labor Force Participation 16Y – 19Y old : at nadir since mid 2010 < 35%. It's not about $15 min wage.

Solutions :

2) Send them to protest in the streets, to BLM, or the gangs.

3) Mommy will take care of them.

4) Send them to colleges to pileup $2T student loans debt.

5) A mandatory army service to get them some discipline, train and give them tech skills and pledge loyalty to the country.

6) The Labor Force Participation was rising between 1965 and 1978,

during the inflation period, peaking @60%.

7) The baby boomers were either in colleges, or the army, in the labor force, or hippies in NYC streets.

8) A hot summer of love is coming to Portland. De-fund the police will

send a former black cop to Gracie mansion. Chicago might form paramilitary units to patrol the streets with the police.

You can’t put them in the military. A lot of them don’t meet the physical requirements. As in too fat and and soft.

1) Fat and soft. Skinny ironmen within three months.

2) A change of character.

3) The cause : 70% of them are unemployed

4) The reasons : reasons don’t matter. Any reason can be a spark and ignite. The reasons are the symptoms. Treat the cause of the disease : 70% unemployment.