A massive source of liquidity is approaching peter-out moment.

By Wolf Richter for WOLF STREET.

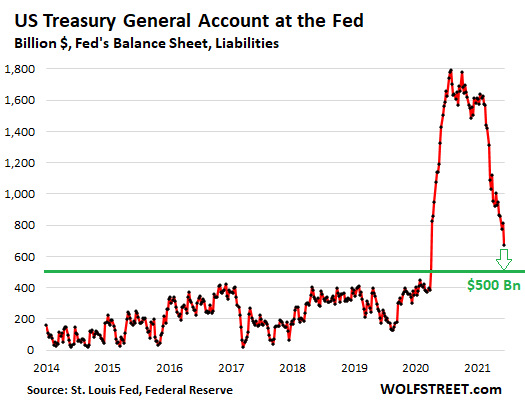

The excess balances in the federal government’s checking account – the “Treasury General Account” (TGA) at the Federal Reserve Bank of New York – that had ballooned to $1.8 trillion by July 2020 plunged to $674 billion as of Wednesday, according to the Fed’s balance sheet, released today, the lowest since April 2, 2020, having now unwound most of the monetized-but-unspent debt-binge spike from spring last year.

The Mnuchin Treasury started reducing the balance in the TGA in baby steps by borrowing less than they were spending. The Yellen Treasury announced in February that it would draw down the account to $500 billion by the end of June. $174 billion more to go:

Last spring, the government sold a gigantic amount of debt, piling an additional $3 trillion on top of its mountain of debt in just a few months.

At the same time, the Fed bought $3 trillion in securities as part of its QE and wealth effect program, thereby monetizing nearly all of the $3 trillion in new debt that the government issued during that time.

But the government didn’t spend all of the $3 trillion in proceeds from the new debt, and the TGA – a liability on the Fed’s balance sheet – soared from around $400 billion in February 2020 to $1.8 trillion in July. This $1.4 trillion addition that the government had borrowed and that the Fed had then monetized didn’t go into the economy and the markets but sat in the government’s checking account.

But now, during the drawdown of the TGA, that money has been going into the economy and the markets. The drawdown so far is money that the government has spent since February but didn’t have to collect in taxes or borrow from investors since it already borrowed it over a year ago, with the Fed having monetized the new debt.

Since February, this money has started circulating in the economy, markets, and banking system, as the government spent it, and is in part responsible for the flood of cash that suddenly started to show up in the banking system that was already up to the gills in cash, and poured out from there.

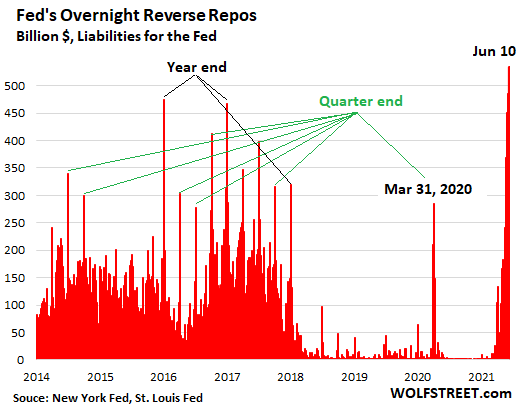

And this liquidity was starting to go haywire, pushing several interest rates to or below zero, even as inflation has started to spike at a pace not seen in decades.

So the Fed stepped in with its reverse repos (RRP) to mop up this liquidity and keep those interest rates above zero. This has the opposite effect of QE.

This morning, the Fed sold a record $535 billion in Treasury securities via overnight RRPs, to 54 counterparties. These overnight RRPs will mature and unwind Friday morning, and will be replaced by a new batch of RRPs. Wednesday’s $503 billion in overnight reverse repos matured and unwound this morning and were replaced with this new pile.

The amount of liquidity that the Fed has mopped up on any given day is the RRP balance on that day, currently $534 billion, having thus undone 4.5 months of QE of $120 billion a month.

When the TGA is finally drawn down to $500 billion, that source of liquidity will have dried up. At the same time, the Fed is getting closer to tapering its asset purchases. And it is under pressure to do so sooner rather than later because they’re another source of this flood of liquidity in a system already creaking under the crazy amount of liquidity.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So, who now owns this bucket of ‘toxic’ liquidity? And don’t tell me it’s someone I know!

If excess liquidity is a problem, negative interest rates solves that. It is not a quick fix, but over time negative interest rates is deflationary and reduce the amount of money. The side effects might be unpleasant to some.

Let’s hope financial repression isn’t with us for too long as it makes it nearly impossible for a person to accumulate enough real wealth to retire at a reasonable age.

Like the Bernanke used to say, there are too many savings (didn’t mention the Fed flooding the system with “savings”), so that’s why you aren’t allowed to get interest income. Go buy the nasdaq, it only goes up. Retail traders everywhere know this to be 100% fact.

There’s never been a better time to jump in at the top.

There is this popular idea that the Fed is to blame for wealth inequality and financial repression, but they are just doing what the common person wants: the guy on the street wants to keep his job so he can pay his bills. The Fed needs to prevent a systemic collapse to accomplish this. They’re doing it through financial repression. The average Joe is the one choosing how much to work and how much to consume. He can go on a buyer’s strike. He can go on a worker’s strike. Either one would stop the trend toward greater wealth inequality. But Joe loves his job so much and loves to spend his money so much, that he is willing to accept smaller and smaller retirement savings just to be able to continue working and spending at the same pace. I don’t see any indications that Joe is changing his attitude in a fundamental way.

“…But Joe loves his job so much and loves to spend his money so much, that he is willing to accept smaller and smaller retirement savings just to be able to continue working and spending at the same pace. …”

That drivel sounds like it came right out of the Fed’s playbook and is approved for public consumption.

Bingo: Everyone is invested in the system and wants it to go on. No one wants a Great Depression 2. The fed is doing what it has to save the system. You can complain about it, revolt, or figure it out and play along. Personally, we have a huge rainy day fund, but we have borrowed since the pandemic, and extra savings are put into assets not savings bc the fed is committed to making asset prices go up and the dollar go down.

Fool. Speak for yourself. Don’t imagine what others think.

Abolish the Fed and let markets work. The money created by the Fed that is slouching around is not under the control of “average joe” but the banks and large corporations.

“Everyone is invested in the system and wants it to go on.”

Speak for yourself and not others. Otherwise, you look the fool.

The Fed is just another instrument with which the rapacious oligarchy executes its domination over the lower classes. Sure, the people could rise up against them, but who’s going to volunteer to go first? Not me. I’ve got a family to feed.

This is the biggest load of nonsense I’ve ever seen. No, the Fed is not preventing a systemic collapse. It’s delaying it. And I would rather have it happen now than when I’m too old to do anything about it, or worse, to leave it to my sons.

Tough crowd. I don’t think a system collapse would be fun.

The concept of “retirement” is a relatively recent invention. Before the era of industrialization and financialization the concept of getting an income from a stash of money didn’t really exist. Though it was less of an issue due to shorter lifespans the basic theory before the time of “getting your money to work for you” was to actually own a farm or business that you could pass on to your children in exchange for them taking care of you, or just treating them well so they would take care of you in old age. I am afraid that the Fed is ushering us in to a return to those days when a “financial retirement” is no longer possible for anyone but the 1%.

“I am afraid that the Fed is ushering us in to a return to those days when a “financial retirement” is no longer possible for anyone but the 1%.”

The idea of pensions and old age retirement (e.g. Otto Bismarck) have been around for well over a century, maybe much longer (certainly before SS).

Modern idea of ordinary people retiring at 65 or younger and living off proceeds of saving and investments is however somewhat novel, so I agree with your premise.

Those tempting dreams promoted by the financial industry (401ks and whatnot) of retiring in a bit of luxury (villa by tropical shores, traveling around the world) are a pipe dream for your average American, and always will be.

The main thing is to arrange your affairs prudently so that, whatever the markets and economy do, you can indeed retire with some dignity and comfort well before you are too old and decrepit to enjoy it.

Living in dire squalor or poverty in old age (and fear of outliving your money) is no way for anyone to exit life.

@Sam,

FALSE: “negative interest rates is deflationary”.

Wow, you could not possibly be more wrong. Low interest rates are inflationary. Negative interest rates are hyperinflationary.

Sure?

Interest is a math function working on the amount of money. Negative interest rates reduses the amount of money. A declining amount of money is the definition on deflation as an increasing amount of money is the definition on inflation.

Price indexes may, may not or may to some degree have something with inflation and the amount of money to do.

Yes… “Low interest rates are inflationary. Negative interest rates are hyperinflationary”

You are 100% right. Sometimes people write nonsense posts!

I have never seen a situation like that. I lived 11 years in Argentina (Hyperinflation) and when you get Hyper…going out is really really really difficult!!! (They still are in Hyperinflation!!)

Central bank economist has been good at confusing cause and effects and even basic knowledge of the monetary system.

As for Argentina, what was the “inflation”, rise in prices measured by price indexes caused by? Low monetary expansion due to low interest rates? Or high monetary expansion by other mechanisms?

Now if prices rise on imported goods in a country due to falling exchange rates, is that inflation in that country? Or is it just an effect of debasing of the currency?

Read how the consumer price index, CPI, is put together and ask yourself one question: What do this really measure?

I love your terminology, “unpleasant” indeed. Does anyone else get the feeling that the billionaire banksters, who control their “Federal” Reserve and by giving funds to politicians, our economy, have no idea what to do?

Now, they just react to upheavals like a driver of a train with its brakes mostly out as it hurdles down a mountain. Hyperinflation here we come!

who knew this is what ‘drain the swamp’ meant?!?!

Is this then effectively the same as if I go to the bank today, withdraw $500 dollars and then my wife takes $495 of that $500 gets a money order and then deposit the money order back to my bank account?

No. Not sure how you came up with that analogy, or what you mean with it.

Yeah its a check kiting scheme, (Bob Prechter). It takes advantage of the transfer period, usually a few days for bank funds, they can roll REPO indefinitely. In your case you temporarily raise your account level to $995. You use that cash on margin to play the stock market casino (which always wins) and return the cash (and keep the profits) before the accounts true up. You really need three accounts to do it correctly which is the number of legs in any Fed discount window operation. Banks are always buying and selling Treasuries. The market gets a bit one sided the Fed jumps in and extends the holding period.

I believe all these RRP are tri-party transactions, the fed, the customer, and the clearing house(BNY Mellon).

Wow – $503B yesterday and $535B today. $1T running Repo balance may come before year end.

As for drawing TGA down to $500B, then:

“…that source of liquidity will have dried up…” ??

Sounds like there will still be $500B left for the Treasury to spend – no ?

The best thing about a gold standard was the discipline it imposed. Discipline in financial matters is a joke today. It’s going to be interesting to see if DC crowd is going to let the current party run out in September as is currently scheduled. I say they are going to be irresponsible til something breaks.

It’s pretty clear from history you get addicted to money printing and you pay a big price when the party is over.

A gold standard helps, but a “gold backed” national currency can also be debased. As we have seen in history, the amount of gold that backs the currency can simply be lowered or suspended.

So the solution is direct ownership of the metal. This can be either metal in your own hands, or in the form of asset backed digital currency (ABDC) that registers your direct title to the metal. But the point is that you MUST have title to the metal itself and not some form of IOU.

I wrote it before: I think the battleground is going to be between Central Bank Digital Currency (CBDC) and private ABDC. People will adopt private ABDC by themselves when they don’t trust the CBDC / fiat money anymore.

So true. If not 100% backed by gold, the percentage backing is a slippery slope until the percentage drops to zero. (woohoo to Nixon for hitting that in his term).

There were competing currencies which were all backed by and redeemable in gold. Perhaps YuShan can tell us more about those.

Couple of years ago, a rare thing happened – someone who believes in gold standard (Judy Shelton) was nominated for the Fed. Unprecedented opposition to that nomination ensued and finally withdrawn. Sad!

I’ve read that the US is the major buyer (importer) of silver this year, someone is catching a clue.

“asset backed digital currency (ABDC) that registers your direct title to the metal”

Hmmm.

1) If crappy, corrupt gvts (and their men with guns) are the ones administering the title system, it becomes as untrustworthy as the gvt.

2) Ignoring 1, if you can rely upon dematerialized title in something/anything…why not make it something with direct demand/utility value…like energy/oil. Or a diversified basket of such utility goods.

YuShan, please keep posting. I think your explorations in this area are valuable.

Having the title to the asset (gold) is not much different than “some form of IOU”. They are both just pieces of paper. If you give me a minute, I can whip up the title to the Brooklyn Bridge.

@Cas127,

“If crappy, corrupt gvts (and their men with guns) are the ones administering the title system, it becomes as untrustworthy as the gvt.”

Title is registered on a distributed ledger. It it is decentralised and nobody can single handedly change it. Also, the gold is not located in one vault in one country but in many vaults in many countries and can be moved when governments start behaving strange.

“if you can rely upon dematerialized title in something/anything…why not make it something with direct demand/utility value…like energy/oil. Or a diversified basket of such utility goods.”

Definitely possible. However, for backing of currency the practical options are limited. You need an asset that is fungible, has deep enough markets, universally recognised as valuable, doesn’t spoil and is easy to store. Gold is then the obvious choice. At current price, $1 billion worth of gold fits into just 1 cubic metre.

@roddy6667,

No that is very different. An IOU has counterparty risk. Direct ownership has not.

Also government issued “gold backed” currency is basically a kind of IOU with counterparty risk, as history has proven.

That doesn’t mean that assets that you own outright can’t be stolen or confiscated, but it can’t happen in a simple default or “revaluation” and assets being offshore also complicates this. A jurisdiction like Liechtenstein has protection against government confiscation written in their constitution.

Well, then we just need to insert the percentage backing into the blockchain, and we’ll be good right!!!

The Blockchain will save us all!!! If it’s written in the blockchain, it’s LAW!!!

A law that no one has ever been able to sufficiently explain to me.

The gold standard makes zero sense in the age of globalization.

Nicko2:

Exactly!

Could we have “globalization” with a “limited” supply of gold?

Makes no sense to even contemplate a “gold standard” with the “modern” economy.

With a limited amount of gold as a backup, you can only have a “limited” expansion of the economy. Then you end up in a “box canyon”.

On the other hand an economy based on fiat money leaves vast areas of potential fraud to occur to facilitate an “expansionary atmosphere”.

We have seen that in all the rotten financial paper that has been given birth to especially since the 1980’s.

All markets need some form of discipline. “Discipline” is not the best facet of human behaviour.

Gold is not the answer.

Wolf made an estimation of when he thought it would top $1T recently. It seems like a scared swimmer who puts his toe in first, then his leg, then up to waist and finally goes all in and goes underwater. Gently at first then all in

1) Diversion : SPX made a new all time high. // Since Mar US30Y is down from 2.52% to 2.1%.

2) In Yesterday 30Y bond auction foreigners were the largest buyers group.

3) US economy is strong. SPX made a new all time high. The trend is our friend. Yet foreigners are buying US bonds.

5) Diversion : the rise of the CPI is a small fraction of the rise in the commodity prices, Y/Y.

6) Last year BCD was $20. // This year it’s $30, a 50% rise in commodities prices.

7) Mfg payed more, but we don’t care !!

8) US gov budget deficit is the highest since WWII. The RRP cluster started in Apr. JP sucked liquidity out of the system. // US gov saving account in the Fed was drained again. US gov cont to spend.

9) UST10 is down since Apr from 1.74% to 1.45%.

10) Stock traders cont to be optimistic : UST10Y June low is a spring.

Again, the U.S. economy is not strong. As long as government spending is a component of GDP, GDP means nothing in terms of actual strength.

NYer : 7) Mfg paying more, but we don’t care :

we cannot afford the higher prices, because the economy is : Weak !!

Exactly. When government spending is sourced from DEBT instead of tax receipts based on production in such significant amounts as it has been. GDP dropping? Just pay for $TRILLIONS in pork barrel, central planning projects on the taxpayer’s credit card. What? $523 BILLION interest on that card last year. No matter…

Right, Mr. NY. Also, financials. An “investment” company like a mutual or hedge fund or a financial advisor only transfers real money from one pocket to another. It takes a slice for profit during this process, but does not make or do anything productive. There are more mutual funds than companies to invest in. There are more “financial advisors” than cockroaches. Their nefarious activities are included in GDP.

Yes. Our entire economy is largely unproductive financial products and time wasters like Facebook and Instagram. It works because the rest of the world provides us with the stuff we actually need.

The actual US economic fundamentals are very poor, and have been since at least 2008.

Most recent “growth” in GDP is government spending. If the annual increase in the outstanding debt as a % of the GDP was the same as 2007 and prior, economic “growth” since 2008 would be close to zero or negative most or every year.

Paying more for something than anyone else does also creates “growth”, like medical care or wasting resources on 70% of the world’s lawyers.

Then there is the increase in the FRB’s balance sheet since 2008. Another component of this fake economy.

GDP mostly measures the financial value of economic transactions. It’s a misleading indicator of how most people in an economy are actually prospering, or not. It doesn’t measure quality of life either, such as from congestion in the city I live where the population has increased around 5X since I first moved here in 1975.

Agreed, it only appears strong the same way someone high on drugs or adrenaline is, particularly if they keep chasing the dragon.

Once the stimmies wear off….

Exactly!!The FED/Govt.=much or most of the economy.How many 16-70 year olds are not working or barely working?College enrollments up or down vompared to 2019?They are down.Apprenticeship openings?Down or unfilled.How many nonmicro biz openings from june 2020-today compared to a year previous?How many more or less manufacturing jobs have we seen available in Merica compared to ladt June or June2019?How many restaurant,retail,services,charity jobs have evaporated and the jobs that Those jobs help fund?Here,in IL.,the numbers of permanently closed biz are not good.

Not sure what all this means?? Could it cause a correction the Stock Market or is it business as usual????

Is that a trick question?

It’s business as usual fed-style. Paint yourself into a corner from which there’s no escape, then contort yourself into a pathetic cartoon character desperately trying to pick up a turd by the clean end.

Kicking the can doesn’t work. It just makes the inevitable outcome worse. Like putting bandaids on a brain tumor.

Reverse repos are a sign of last ditch desperation.

There’s no graceful way out of a credit bubble and they not only allowed it but encouraged it. Unfortunately the First National Billionaire Bank won’t allow the Fed to let the air out.

Somebody or something eventually will, and it will be beyond anyone’s ability to control it.

No possibility of predicting any supposed “trigger” event in advance. Whatever it actually turns out to be, it will at root be a change in psychology. When enough people get angry or pessimistic enough, no financial engineering will be able to keep this ship from sinking.

There is a lot of “blowback” waiting to be unleashed in the future.

I’d say whatever the trigger event turns out to be is hidden in the “fat tails”.

It’s like Monty Pythons Spanish Inquisition – nobody expects it. We live in a nonlinear economic system where small 0erturbatiins can have massive effects.

Think of a snowpack on a mountain. It’s ready to avalanche at any time but it hasn’t. One day a squirrel drops an acorn on the snow pack from an over hanging tree and triggers the avalanche. That’s a fat tail event with an alinear response.

Gold buggery still exists. Keynes told the story that the Treasury should bury the amount of gilts it needed in abandoned mines then fill the mines in and ‘award’ private contractors to go dig up the gilts. Tying a currency value to how much gold was discovered is absurd. Resources and their use are what determines the true value of a currency in national economies.

Yeah…..I never understood the logic that miners would determine the value of the currency.

Let’s base our economy on random geology.

I’ll pass on that.

The concept of a gold standard s that although there is some gold mining that increases supply, a gold standard is immune to central bank buggery because you can’t print gold.

The government can still change the peg, which that a-hole FDR did, and alter the value if the currency. That’s what makes crypto so attractive in concept.

Incredibly there are some folks who think people, not the government, should own their currency.

Be happy in your serfdom.

Plenty of fake gold out there.

“And this liquidity was starting to go haywire, pushing several interest rates to or below zero…

So the Fed stepped in with its reverse repos (RRP) to mop up this liquidity and keep those interest rates above zero.”

1. I’m wondering what were the several interest rates that were hovering on or below zero. Or does that mean that the key interest rates will largely effect all interest rates.

2. How specifically it would profit the huge major dealers and financial institutions to be counterparties to the Fed’s RRPs? In other words, how do the dealers and institutions benefit by participating in the Fed’s RRP methodology for regulating the interest rates?

3. When the TGA dwindles to the 500 billion target balance, the RRP juggling act will end?

Re: 1 – Everything gets affected even USD and Gold, which spills into all other asset classes. Gold bottomed and dollar index topped around the same time this RRP facility began its ascent higher.

Re: 2 – The only entity using this facility in real size are government money market funds. They are benefitting because they are not forced to buy assets that yield less than 0. This facility by the fed pays 0. The banks benefit from this facility from a regulatory standpoint. They get to push off deposits that generate little to no yield to them. The banks will then use the capital/balance sheet relief to fund more lucrative endeavors.

Re: 3 – No the excess liquidity is still there until the TGA begins to rebuild itself after the debt ceiling. It is just the firehouse of liquidity from the unwinding of TGA is gone. This facility won’t unwind until the Fed stops QE and after the debt ceiling.

It’ll be fun to watch and trade when all this liquidity reverses and what it does to risk assets.

1) Nixon, who inherited LBJ 1960’s toxic junk, had no choice, but to divorce gold.

2) In 1929 the DOW slump and gold was running out of US gov vaults.

3) in 1931 when policy was tightened to protect the gold standard ==>

the rise of interest rates, – when the economy got badly hurt, – led to the depression.

4) The chart : Gold Futures (ZG) was rising until Mar 2008. Thereafter Gold

slumped until Oct 2008, building a backbone for the rise to 1,911, in

Sept 2011.

5) Since 2011, ZG backbone was never tested. Don’t fall into the gold

trap. Gold is more flexible and agile than u think.

By “toxic junk” do you mean the Vietnam War or the Great Society program, or both?

Michael,

As I commented recently, my Econ professor that I had as a freshman at the U of MN in spring trimester 1981, was Walter Heller.

Right after JFK was killed, Mr. Heller met with LBJ to propose that we enter into the “War on Poverty.” President Johnson engaged as Heller advised, but soon after, Johnson ramped up the Vietnam War. Heller told LBJ to raise taxes to pay for the war, and when the President refused to do so, Heller told him off and quit.

So to answer the question, I think it is both.

Walter Heller was also an architect of the Marshall Plan in 1947.

One of Heller’s TAs introduced himself my first day of college and said:

“There is only one thing you need to know about economics: The smartest man is not the man leaving a million dollars when he dies, but the smartest man is the one owing a million dollars when he dies.”

Words to live by.

Hahahahaha!!!!! You must be referring to the Grate Society!!!!! This is what LBJ created!!! A society where people only think of themselves and are so self-absorbed and shallow that they grate on others all the time!!!!!!! Hahahahahahaha!!!!

“Since February, this money has started circulating in the economy, markets, and banking system, as the government spent it…”

Strike anyone else as backwards in the most basic way?

We mere citizen folk PEOPLE exist to serve “the economy, markets, and banking system”. We serve them. They do not exist for our sake or benefit, we exist to for them. The market, banking system, economy can only be failed, they can never fail.

That’s one reason why we continuously see 10x more indignation in comments when the poors temporarily get $300/wk as we prepare to give billions to rich gigantic chip makes who use most/all of it to boost stock buybacks that benefit the subsidized and untaxed/inadequately taxed wealthy and parasitical financial industry.

Why, we even have folks telling us the wealthy more than their share of taxes vs the poors when one of the financial cos of govt is to protect property – which they have most of.

Guess we still have a lot of progress to make.

False equivalence fallacy.

Just because someone is against the extra $300/week doesn’t mean they are in favor of giveaways to anyone else, rich or not. I’m against both.

Wealth inequality is not in and of itself a problem, it’s how it happened. That’s the problem with it, use of political influence to get it.

In any society where the government has favors to sell which is every one, the rich are always going to be the high bidder and end up as lopsided winners. That’s a fact and there is no reason to believe any society will exist where this doesn’t happen.

The rich (especially the more affluent wage earning tax donkeys) already pay most of the taxes and the cost of government to protect their private property is vanishingly small compared to the amount they pay.

The rich don’t pay taxes, and if you do you’re failing. To pay taxes, one needs ‘income’, which is easy to obscure, indeed, most true wealth is held safely in tax shelters.

Depends what you mean by “rich.” If by “rich,” you mean a professional couple making $900k a year, they pay taxes, and a lot of them.

If you mean people who don’t really work a job, but make most of their income passively, then yes, you are right.

RE: “Since February, this money has started circulating in the economy, markets, and banking system, as the government spent it, and is in part responsible for the flood of cash that suddenly started to show up in the banking system that was already up to the gills in cash, and poured out from there.”

The coupons/play money/chits/worthless media, whatever you want to call the USD are essentially worthless. So what does that tell any one about inflation and deflation? Since the FED has started not revealing M2, and M3 data, does anyone question WHY?

The balance sheet link is great. Thanks. Comparison starting from that data with comparisons of REAL wages, and the fact that REAL wages, and REAL income have not increased are pretty significant little bits of data.

The REAL squeeze play based on what REAL income and REAL tax revenues to support any real growth in the financial survival of US citizens, to not be totally detrimental to the total US, is going. to reveal a little bit more than the baloney money games on the stock exchanges.

See how the price for bottled water really starts zooming. Who is making the real money are the people that are enjoying the REAL take-aways out of the US. Yeah, there’s a few still stuck in the US enjoying their gated privatized lifestyles, constraining and restraining the mass clamoring, just like this comment, everywhere, but not counting for beans!

The US is exporting their inflation to the rest of the world, it will have unintended consequences. US citizens, ie, Joe and Jane tax payer will be the last to get the memo.

It’s a stealth contractionary policy (expectation of slower growth). It’s a yield curve (time to maturity) flattener (compressing spreads between sectors).

Does anyone know if there is a skim or commission or fee or service charge on these vast sums sloshing back and forth all the time.

“When the TGA is finally drawn down to $500 billion, that source of liquidity will have dried up.”

I’m not entirely sure who the TGA account is a source of liquidity for. During the dot com mania the TGA account did not figure prominently in the rise of stocks.

I see the link to the primary dealers, and perhaps these dealers are making margin loans using treasuries on their books as collateral. The implication is that once the liquidity dries up, something must fall in value, but that all depends on what is being purchased.

It’s likely there are elaborate chains of loans that provide leverage to stocks, bonds and real estate. I see no crisis in confidence in the Fed. As long as inflation pushes asset prices higher, leveraged loans need not be reset.

Maybe all that TGA account money was going into crypto. It’s the only thing really falling!

Robert,

The TGA account is normally the most boring thing on earth. Just a checking account of a big government.

But what happened in the spring last year is that it became the repository of about $1.4 trillion in cash that had been borrowed and then right away monetized by the Fed (QE). So the Fed poured $1.4 trillion out there that didn’t go into the markets or the economy but went into storage at the TGA account. And the drawdown has been releasing that cash.

I don’t think this has ever happened before.

So what happens when TGA hits $500B target ?

Did they draw down the general account to finance Washington’s spending programs? Federal spending exceeds tax incomes.

Will reverse repo bring in more funds at the expense of losing the interest on the securities lent out?

Russia tightened by raising its interest rates today.

It would lend credence to much of those funds through the Economic Adjustment Committee down through Economic Adjustment Assistance trickling down through the CARES ACT programs and many other venues paying for everything along with Black Rock, Van Guard et. alia buying up single family homes and entire neighborhoods across the nation at 30-50% above asking price. So kneecap small business by paying people not to work, farm, or employment activities eliminating competition by destroying the middle class and Voila ! You have Nobles & Surfs again with permanent renters. You’ll own nothing and be happy….

Serfs have no opinions to voice. Censorship.

Serfs cannot travel. High car and gas prices.

Serfs cannot own property. Blackrock buying homes.

Serfs have no weapons. What is the point of 2A when you have nothing to protect of value?

Serfs have free medical care. As long as they are useful.

Serfs will be happy. They have no other choice.

Sounds like the Fed is getting its books in order and tapering will come after the excess reserve problem resolves itself. ER are lend able assets, so that goes a long ways to informing us about the recovery. The high yield bond ETFs (HYG,JNK) are up 1/2% since the 1st of June. Booyah.

I have heard rumors from different sources that the Federal Reserve has officially had it’s Charter revoked. Convincing the banks Monday this week to give up their liquidity for an over night Repo with a 25 to 1 return on Tuesday. Now if indeed the Fed is no longer Chartered would not that be an act of Fraud as well as having it’s bonds be instantly rejected through the rest of the week and in the near future ?

That’s hilarious. Thanks for the humor. Much needed.

Every time you see the word “liquidity”, substitute the word “reserves”, in the sense “reserve account balances at the Fed”. That’s what it is. Not “cash”. Not “liquidity”. Reserves.

Reserves and paper greenbacks are the only “real” USD-denominated money, money that can be used to settle interbank payments. Every other type of “money” (such as bank deposits) are just debt and the associated claims on the collateral against the debt (if any).

NARmageddon,

At least some of this is wrong.

1. Banks on their books call cash (an asset) “cash” or “Interest-earning deposits with banks,” or similar, which includes the cash they have on deposit at the Fed. They do not call it “reserves”

2. “Reserves” is a term the Fed uses; it describes a bank’s cash that it put on deposit at the Fed. “Reserves” are liability on the Fed’s balance sheet (money it owes the banks). It used to have a 10% “reserve requirement” (removed in 2020),

3. Banks on their books have not accounts that are called “reserves.”

Below are the asset accounts of Wells Fargo Bank, and the link to its 10-Q quarterly financial statement where the balance sheet begins on page 61. In the entire 10-Q, the word “reserves” shows up only once and in a different meaning:

Assets:

Cash and due from banks

Interest-earning deposits with banks

— Total cash, cash equivalents, and restricted cash

Federal funds sold and securities purchased under resale agreements

Debt securities

Loans held for sale

Loans

Allowance for loan losses

— Net loans

Mortgage servicing rights

Premises and equipment, net

Goodwill

Derivative assets

Equity securities

Other assets

— Total assets

https://www.sec.gov/Archives/edgar/data/72971/000007297121000221/wfc-20210331.htm#i379a784381c54b31ad371d993c457ae8_157

Nothing will happen, but those that got in on the right side of the asset line, before it was too late, will have to increasingly continue to be able to turn a blind eye to those that didn’t. Will be easy to ignore, now that wfh allows for not having to step over them in the streets.

1) US budget deficit is growing to stimulate the economy.

2) Europe & US will collect $10 Trillions in reparation from China.

3) Investors cashing in from the stock market will pay capital gains

taxes.

4) US gov will humble GOOGL & FB with new min taxes. The republican

salivate.

5) If the FED preempt, US saving rate will rise, to avoid risk assets.

6) Higher saving rate induce investment, along with a new infrastructure bill.

7) Taxes, capital gains reparation will stabilize the budget budget deficit, within a decade.

8) There is still hope !!

You have an odd way of looking at things.

First what and where are these reparations from China?

Second, where is this higher saving rate going to come from when we are looking at much higher taxes? Money paid in taxes cannot be saved.

The amount of tax increase necessary to service the ever growing debt is going to require massive tax hikes. Inflation is going to necessitate higher interest which in turn will mean higher debt service and more tax burden on every tax payer.

Hope for what? an extended period of lower living standards?

“a new infrastructure bill” I didn’t hear about this actually happening. The latest I am reading is DC liberals are steaming, while the Trump wing R’s (that is a lot of them) are pushing hard against any win that would be a success for this president. We will see. If the tactically centrist team Biden, trying to be bipartisan, can’t push this one out, I don’t think it will ever happen.

Engel…. US infrastructure bill is band-aid for crumbling highways and bridges…. meanwhile, China spends hundreds of billions building new Silk Road. No contest.

Malinvestment.

Gareth Bale plays today.

File Number 2 with: ‘and Mexico will pay for it’

In a parallel universe where China humbles itself before the world, releases political prisoners, allows free elections, the CCP apologizes for the Cultural Revolution, voluntarily disbands, but FIRST pays trillions to the West, this would extinguish China’s domestic credit impulse, a main driver of the world economy.

A process and result similar to the attempts to wring reparations from WWI Germany, now generally accepted as a cause of the Depression.

The better news: ain’t happenen.

What are the possibilities that the USD as reserve currency is challenged as the losing purchasing power triggers a global inflation?

Blockchain technology makes it easy to go back on a pure gold standard. Before the argument was its too heavy and there’s not enough of the stuff. Blockchain allows fractional ownership and transaction. Let’s throw in mobile phone voting too.

The Govt has nearly spent all the money it had in its ‘pooches’ (Scottish pockets). It’ll soon have to get some more to keep going just like us. The only thing it’s got to sell is Treasuries, so it will have to sell in the money market for more ‘dosh’. If they’re lucky they might get away with selling their ‘paper’ at full face value, if not they may have to offer a bit more in interest to get it away. If that gets too bad they might have to go back to their pals at the Fed to ask them to buy some junk off their rich buddies so there’s more money in the market. We’ll soon see.