New York Fed’s Williams prepares markets for “technical adjustments” to the Fed’s “administered interest rates” to get a handle on this phenomenon.

By Wolf Richter for WOLF STREET.

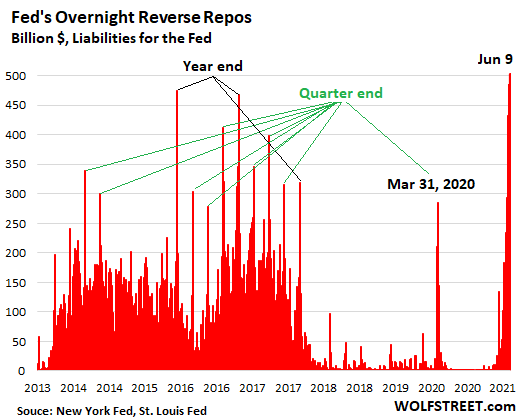

The Fed sold a record $503 billion in Treasury securities this morning via overnight “reverse repos” (RRP) to 59 counterparties, and thereby took in $503 billion in cash from the counterparties. These overnight RRPs will mature and unwind tomorrow. Yesterday’s record $497 billion in overnight RRPs matured this morning and were replaced by this new and even larger flood.

“Reverse repos” are the opposite of “repos.” They drain cash from the market and are liabilities on the Fed’s balance sheet – money the Fed owes the counterparties.

A similar phenomenon, but on a smaller scale, occurred starting in 2014 as the US financial system was awash in cash following years of QE. And at the end of the quarter, particularly at the end of the year, RRP balances spiked. The phenomenon declined as the Fed began shedding its assets from late 2017 to 2019. But this time overnight RRPs spiked beyond those levels during the middle of the quarter – with June 30 coming up:

By having drained $503 billion in cash from the market via these overnight reverse repos, the Fed has undone the liquidity effect of 4.2 months of QE, which continues at a rate of about $120 billion a month.

The coming “technical adjustments” to the Fed’s administered interest rates.

The Fed’s offering rate currently for overnight reverse repos is 0%, meaning that counterparties are handing their cash to the Fed, and get Treasuries as collateral, for 0% return. The offering rate is decided by the FOMC. The Fed offers these reverse repos to keep the reverse repo rates from falling into the negative as the tsunami of liquidity needs to find a place to go.

The Fed could get a handle on this liquidity phenomenon by tapering asset purchases and eventually reducing its balance sheet. That’s how the phenomenon was resolved last time.

This reverse repo offering rate is now getting lined up for what the Fed calls a “technical adjustment,” namely an increase of something like 10 basis points, either at the next FOMC meeting or at an in-between Zoom meeting before then.

The Interest on Excess Reserves (IOER) could also be subject to this type of “technical adjustment.” The Fed is currently paying the banks 0.1% interest on cash they put on deposit at the Fed. Those “reserves,” as that cash on deposit at the Fed is called, now stand at $3.8 trillion.

The FOMC may also hike the IOER by some basis points. This would help raise the floor of the effective federal funds rate to where it trades closer to the middle of the Fed’s target range, (0.00% to 0.25%). The effective federal funds rate has been around 0.06% when it should be around 0.12%.

So New York Fed President John Williams, whose outfit handles the Fed’s trading activities, prepared the markets for this type of “technical adjustment” to the Fed’s reverse repo offering rate and the IOER in an interview with Yahoo Finance last week.

He emphasized repeatedly that the reverse repo system “was working really well,” and “exactly as designed,” that there were “really, no concerns about that.” And he also shed light on where this tsunami of liquidity came from that the Fed took in: the “banking system.”

So he explained: “When we thought about and set this up [the reverse repo facility] a long time ago, we wanted to make sure, in a situation where we’re making asset purchases for our monetary policy goals, that the matching increase in liabilities would be distributed in the financial system efficiently and well. And a lot of it shows up in the banking system as reserves, but also some of it can show up through the overnight reverse repo facility.”

“And we have seen that get used quite a bit recently. We expected that to happen. It’s working exactly as designed. Really, no concerns about that. It’s a system that was put in place so that we didn’t have problems [INAUDIBLE], and we’re not having them,” he said.

“So to me, it’s working really well, and the fact that funds are flowing between the banking system and the overnight reverse repo, this is kind of what we would expect to happen in this kind of circumstance,” he said.

“And we actually, going back to earlier days, we’ve made adjustments, technical adjustments to these administered rates and these programs, specifically to make sure they’re working well. And for me, achieving the FOMC’s goal of having the federal funds rate trading well within the target range,” he said.

“So we have the ability to adjust parameters of our administered rates or other parts of our program so that they work really well and keep interest rates where we want. So we can do that if that’s called for,” he said

“We have the ability to tweak it, if you will, to make sure it’s achieving exactly what the FOMC is looking for in terms of short-term interest rates,” he said.

So these administered rates may be in for some “technical adjustments” upward at or before the next FOMC meeting. And this would be underlined by some taper talk. And meanwhile, the Fed is starting to sell its holdings of corporate bonds and corporate bond ETFs.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What impact will this have on longer term yields?

So Interesting are all these “technical adjustment” going to affect the “Fed Rate” then and if so how ? Almost nothing now Inflation on a daily rise Like Gas Prices / food Etc . Is the Plan to Go into Negative Rates or to raise the rate ? .

I assume since everything seems to be Backwards the Plane it to continue The downward Trend to increase Inflation and Prices .

I can only Guess since nothing seems to make sense that The strongest Doller Country shall take over the USA Assets over time now.

Inaudible part: no problems with our “temporary overnight hooker’.

Who are the 59 counterparties that bought a half a trillion dollars of this counterfeit debt at zero percent?

I’ve got some sh%t to trade for their gold.

We know who the approved counterparties are, but we don’t know which of them were among the 59.

The approved counterparties for reverse repos are the Primary Dealers (click on “current list”) plus these financial institutions (click on “current list”).

Those lists look pretty vague. Appears more like a magic show – appears/disappears.

There is nothing “vague” about those lists. These are huge well-known financial institutions that are the counterparties. They’re the biggest of the biggest. Zero, nada, zilch vague about it.

I guess when looking these reports over, I really expected to see specific parties. I may not be reading the reports correct but I expected more breakouts of individual groups and then found the following footnote in the report: “These reports are based on data voluntarily submitted by primary dealers to the Federal Reserve Bank of New York.” Forgive me with my uneasiness of it all when we are talking about such large quantities of money and reporting that is “voluntary and not audited” by the Fed. Again, this may be over my head but concerns me when I cant derive specifics and logic to what is going on here.

Lawefa,

What the heck are you looking at? This is just nonsense. I didn’t link “reports.” I linked the list of counterparties and primary dealers, and there is NOTHING about “voluntary” in them. The primary dealers and counterparties are publicly known. And I gave you list of their names.

“Forgive me with my uneasiness …”

No I won’t. You’re posting garbage.

Some of my Fidelity “cash” funds are on the list. Are these repo’s by design to protect the buck.. $1.00 NAV valuation? The SEC changed the rules to protect the treasury and not bail out banks as easily as the Financial crisis. Is the FED stepping in to protect banks by forcing them to take lending money off the table? I may not have this right Wolf. Thanks for your reply.

Sailorgirl,

Yes, there is some of that.

Again, maybe another ignorant question with this but with these reverse reps atbsich behemoth quantities, doesn’t this point to the fact that both parties are deeply in trouble and “scratching each others backs” for their mutual benefits?

Glancing through the details on that link, it looks like the Big Banks are forced to buy the Government’s crap. Thanks for showing us that Wolf.

REPO is an open window, and RRPO the seller reaches out the window and grabs the customers by the lapel. During REPO crisis rates spiked it was thought when banks were refusing the offer, didn’t want the cash, now they don’t want the paper. There could be a paper trail on this, a directive, but why? We have the telephone. The Fed says you need more collateral or you will fail your stress test. In 2008 the Feds authority to broker deals (or else) was established. However there are plenty of (taxpayer) carrots out there too.

The data on who is actually using this facility can be found on the NY fed site, but the data is very delayed. Even though the data is delayed, it still gives clues on who and why the counterparty is tapping this facility.

Search “Repo and Reverse Repo Operations” and under the additional data category there is a link called “reverse repo data by counterparty type” for an excel file. It gives a full breakdown by counterparty type on who is using the facility.

I asked myself the same question. Who are the buyers?

I’ll give the same answer as last time someone asked. Looks like a big player is in big trouble and they are covering it up by making everybody take part in the coverup.

It’s looks like LTCM all over again to me. They need all the big players involved to unwind the positions. It took them over a year to unwind LTCM, so settle in for the long haul.

In short, what John Williams, Ph.D. said: the system is fixed and is working.

Now I can sleep easy.

Yeah, okay. If that “sleep easy” is not hunkered-down, “RCR” – Red County Rural, your “wake-up call” may be more than jiz a little “alarming”, as in . . . “‘The Road’ nightmare”.

I’m glad it’s all good!

Remember…..soylent green IS people.

It’s fixed all right.

I am 100%… Too many distortions in the market…the longest WTF (debt-fueled) bull market in history… I am with Bill Gross. Better having cash than stocks Trash!

When this bubble bursts banks will go under.

The amount of derivatives and leverage is astounding.

Fed doing half a trillion repos now. This sucker is on its last breath.

Keep your cash under the fdic limit.

And even that is not sure as government can renege on their promises.

I respectfully disagree. The Fed and .gov will literally do everything in their power to protect the banks and Wall St.

Now Joe/Jane Citizen should not hold their breath as the Fed is not worried about us, unless of course we do not consume as consumers

So we are all set for this …

You are in cash and inflation is 4%….so you lose.

And what if the stock market just goes sideways or declines?

Everybody loses….except the largest borrower in the world.

-4% > -20%

“And what if the stock market just goes sideways or declines?”

I’d rather take the cash and run than ride out stock market roller coaster this late in a bull cycle.

So what if stonk market does not plateau or decline ever so gently? The Fed’s sport is a con game. Beneath Jay Jay’s padded superhero costume is a cowering 90 lb weakling.

Market’s serious correction is a possibility– nay, I’d say a probability at this point in late innings of this crazy game.

Don’t think the stock market goes sideways very much much. It’s either an escalator up or an elevator down. Very rarely a moving sidewalk

Stop

1) More ammunition to fight a downturn.

2) Back to 1865 to 1897, – not to the 1970’s/ 80’s – neither the 1929/ 33.

3) Annual deflation rates of 1% – 2% , with bouts of 3% – 5%, to cleanse toxic debt.

4) Car repos is deflation.

5) Mortgage default and vacancies is deflation.

6) Crashing small businesses is deflation.

7) Credit cards balance reductions, due to defaults or saving, is deflation.

8) Students loan jubilee, in stepping stones, is deflation.

9) Falling commodities, higher saving rate and a strong dollar, is deflation.

10) A climate change : a frog in a dbl door freezer.

Wink

Forgiving student loans is not deflationary…it’s just the opposite. The average monthly student loan payment amongst the 43 million individuals who collectively owe $1.7 trillion is $400. When the government forgives some major portion of that debt (there are several proposals being considered), it effectively puts upwards of $4,800 a year into the wallets of a majority of those who are in debt to spend on something other than paying off a student loan. Any company CEO worth their salt will figure out it’s time to get their company’s slice of that pie, in part, through price increases. That is inflationary, not deflationary.

Forgiveness means a bunch of people will take a loss no? What will the losers do? Increase spending?

More MMT BS here?

There’s no magic in this world with the exception of perhaps music.

No, they won’t take a loss. Uncle Sam will simply print another $1.7 trillion to add to the other trillions of national debt. It’s their go-to solution for everything…until it no longer works. Again, that’s why it will be inflationary. I wonder if the two-thirds of Americans who favor student loan forgiveness realize that.

By the way, perhaps it’s not clear…I am NOT a fan of inflation. For consumers, it’s tantamount to a regressive consumption tax, especially for those on relatively fixed incomes like many retirees.

Ok, then it makes sense. Of course, if there’s too much of that going on, it will be hyper inflationary.

Happy times are finally here again!!!

I suggest something that involves the following in some form..

Colleges with a certain size endowment must …..

cosign the student loan, or….

be lender themselves for the entire tuition or a lion’s share

and why not?

We have an arrangement now where the federal govt provides the credit for the purchase of a service from a “business”. (schools are big business, don’t kid yourself)

This in itself pushes tuition costs up.

If a person wants to buy a Ford, he deals with Ford credit. Not the federal car loan dept. What would the price of Fords be if federal credit was involved?

If you want to go ABC University, deal with ABC University Credit Dept.

If these steps, in some form, were implemented, two things would happen…

Tuition costs would cease their dramatic rise

Worthless degrees would disappear

Both, because the school would suddenly have an interest in repayment of loan.

one of the very first things Obama did on becoming President was to federalize the student loan program. Probably this being done to set up tuition increases AND forgiveness. All to the benefit of left wing faculties and their indoctrination centers.

Note how many times Obama spoke to college campus crowds.

Secondly,

The trajectory of college tuition has been in lockstep with the trajectory of the budget of the Dept of Education.

From zero in 1979 to $63 Billion a year!!!

For the simplicity of math, lets assume that each State received $1 Billion a year to spend on education in their State as they see fit. This would leave $13 Billion for a trimmed down dept in Washington.

This suggestion strips bare how the federal leviathan operates…they take and then give back after taking their cut. Maybe the money never should have left the State in the first place?

Student loans are high because the university system is grossly inefficent, with hordes of bureaucrats and ever-decreasing academic standards (I speak from experience here). Student loan forgiveness will simply exacerbate both problems. Taxpayers would be spending vast sums for overeducated baristas with philosophy degrees, and engineers who can no longer design things properly. In turn, this leads to increasing inefficiency in industry and commerce. This will not end well.

Spending money to educate your citizens makes more sense than:

1) Flushing the $$$ down the toilet in the form of bloody, expensive wars we don’t win (see Iraq, Afghanistan)

2) Tax cuts for the 1%

3) Corporate welfare

4) All the other various graft and corruption

Plus w/the wars we get LIED into and that we can’t win, the medical expenses of the 40K maimed and wounded soldiers w/missing eyes, burned faces, missing limbs, etc. really starts to add up over the decades after the “war”.

If you won’t stop the stupid, bloody, unwinnable wars for moral reasons (it’s wrong), do it for the $aving$s!!!

If forgiving student loans is deflationary depend on the bookkeeping. If it is done with stating a “loss” and reducing the amount of money it is deflationary. If, not it is neither as the inflation happened when the loan was paid out.

Now, how this affect the consumer price index and other price indexes are to be seen. The CPI adhere stronger to income/purchase power than inflation, so maybe.

Observe that CPI and other indexes is not a measure of monetary inflation and to what degree they follow the monetary inflation varies.

Let’s assume I’m a former student owing $50k of student loans, and that I’m a responsible individual who is dutifully paying $400/mo towards paying back my loan. Now let’s assume someone comes along and erases that debt for me, tax-free as has been proposed (which is ridiculous). Do I not now have $400/mo to increase demand of a myriad of goods and services in the economy? When upwards of 43 million individuals holding $1.7 trillion in student loans are in a position to do this, will this not increase demand versus supply and stoke the already hot inflationary environment we’re in post-pandemic? I believe it will, but we’ll have to wait and see. It’s just one reason I believe forgiving student loans is not fair to a large swath of the population, including those who sacrificed to find alternative means of earning a college education without resorting to student loans.

I’m waiting for a remake of “Repo Man” with Powell in the leading role.

Yes, one of the famous lines from that movie fits right in with the present scene.

“- Debbi to Duke, “let’s go do some crimes.”

Except in Wolf’s remake it will be Janet to Jay.

Wolf, picture Powell as Miller, not Bud. That would be a better fit IMO.

I am clearly most cut out to be Emilio!!! Look at me with my good looks!!!! I am cool babies!!!!! I am the repoman!!!! Hahahahahah!!!!! I am going to do it in the backseat!!!! And then I am going to steal the car and give it back to the bank!!!! Hahahahahaha!!!!!

Wolf-in aggregate, then, the Fed is J. Frank Parnell? (…and it’s beyond me how you can keep looking in the trunk without being vaporized…).

may we all find a better day.

“Students loan jubilee …”.

That is off the table, for now. And so is the student loan pause– students will have to start making payments Oct 1.

When you can print wealth accounting gets fuzzy. Students who want the loan forgiven maybe haven’t thought through that the loans are on government books as an asset. The moment they are forgiven they are just socialized as debt to general population with most of the burden to be carried by the young and not the old.

The Fed is about to become the overnight credit market. Then, if Treasury will agree to issue more bills and fewer bonds, the Fed can take control of BOTH liquidity and the shape of the yield curve. That’s real power and it will come as a shock to anyone who thinks the long end of the curve is determined by a “market.”

Until . . . what? Rampant inflation in the form of foreign-held FRN’s “coming home to roost” taking possession of REAL domestic ASSETs?

I’m currently betting on their power being somewhat less than you may expect, Joe. I’ll fall off my chair if the ongoing inflation doesn’t drive rates higher soon enough across durations.

Inflation is currently on the romp and has been for some time already (just look at PPIs from China yesterday coming in at over 2% on a monthly basis right in the face of a strengthening local currency!). That’ll likely move from there around the world as their goods dissipate across the globe with a lag. Their government is now even overtly expending political energy to try to hold down commodity prices.

And at the moment, in the US in particular, pressure on wage inflation is increasing due to the stuff we can read on this site, e.g. from an article just yesterday (https://wolfstreet.com/2021/06/08/wtf-spike-in-job-openings-in-an-unemployment-crisis-labor-shortages-while-15-million-people-claim-unemployment-benefits/). That sort of inflation does not tend to be a transitory blip, no matter what some central banker or another wants to tell us about base effects.

And if various countries shortly start embarking on their pie in the sky energy (and other) infrastructure dreams in order to sate various domestic demands for good jobs, wages and hope, then that’ll feed even more energy into any sort of inflation under the sun.

I suspect there is no way they under such circumstances can nail down short term rates – at least not without causing the creation of an unofficial rate alongside the official one…

Time will show, of course, but if they and their respective governments keep going full steam ahead on throwing new money into the economy (as I deem likely), then I reckon the probability of sustained higher inflation and rates across durations is pretty damned good, and I suspect it’s likely central bankers will go where they’re being led by their nose ring, whilst telling us it was their own plan all along.

Salt,

you don’t see any of this inflation as transitory? I know one of the amusement parks is now paying $20/ hour but this fall when a lot of the unemployment benefits run out people will be forced back to work and the labor supply will increase. Do you think by then companies will not be able to reduce wages?

Lumber – as i understand it, the raw log producers are not getting more for their product. Its the truckers and mills driving up prices due to labor shortages and this is expected to subside this fall.

I think if the Fed raises rates, housing and equity markets will respond pretty quickly. I am not sure the Fed has much wiggle room.

I’m sure that e.g. a number of commodities very well may move down a bit for a while, bart. But I expect there will be a rebound again pretty soon in most commodities. If not earlier, then by the time a number of different countries get started on rolling out their big spending plans at more or less the same time, by when they’ll all be fighting to obtain large quantities of a number of key commodities from a limited availability pool.

And wages tend to be sticky things, and I would furthermore suggest there is also an argument to be made that the political will to quickly return to only supporting asset prices and suppressing wages on an ongoing basis is fading, and that the massive new debts being monetised and put to work will, at least in part, need to be directed into the hands of the broader population, either through big employment schemes through infrastructure splurging or similar, and/or through the continuation of more direct means of income support.

CPI print at 5% this morning and long bond prices didn’t budge, yields down 15% in the last few months.

I’m not suggesting that rates necessarily have to react immediately. The ruling narrative is, after all, that it’s just a transitory blip. But if, as I expect, we see inflation for a longer period mostly hang about at a higher level than where it has been in recent decades, then rates will get dragged up too.

Of course, as and when the massive new debts and spending plans currently being imagined into life run out of steam again, then the story likely changes and rates reverse again, at least for a while, until central bankers and governments panic yet again on seeing markets tank, and double down and repeat the cycle until it’s finally some day glaringly obvious to everyone that real economic growth is no longer actually achievable…

Fed will own the bond market up and back. They will work to keep the debt slaves on the plantation as long as the dollar remains a currency. But only if the government takes control of labor, and creates one universal public employees union, with the power to negotiate how much you will make and how much in corporate profits is allowed. What the Fed is doing is arranging the party decorations. No populist donnybrook can stop this, esp when the opposition is the lower 50th decile in intelligence. The real stopper is crypto. What happens to all that debt they are playing with, when the value of crypto goes parabolic against the declining value of money and inflates the money supply umpteen times? The great debt collapse will end their dreams of monetary hegemony.

So the Fed is complicit, via their cheap money policy, in the employment predicament and the record job openings, unfilled. If the federal govt had to borrow at real rates, the doling out would not happen to this degree, or at all. Nice job Fed.

And we have 4% inflation with zero Fed Funds rates. Never happened before, and all at the hand of the Fed who promotes inflation.

And we have near record lows in long rates, immoderately low.

So, lets review.

Mandate #1 The Fed is supposed to promote maximum employment yet what they do with rates has had the OPPOSITE EFFECT. Fail.

Mandate #2 The Fed is supposed to promote stable prices, yet they promote just the opposite, INFLATION. Fail

Mandate #3 The Fed is supposed to promote moderate (not extreme) long term rates, but we have near record lows, 30yrs almost 2% below inflation. Those rates are IMMODERATE and EXTREMELY low. Fail.

Arrest J Powell for breach of Fiduciary responsibility in his post as Fed Chairman, and let that be a warning shot to all the Fed governors.

Come get me, babies!!!! You’ll never catch me!!!!! I am stealing from the poor and giving to the rich!!!! Hahahahahahahaha!!!!!!

There are not 50 deciles … how ironic.

Lmao

There are now. Thanks, Inflation!

Little bit of a scary comment by Druckenmiller to the affect that there isn’t a market response right now to inflation as Fed is not allowing price discovery. I thinks he thinks Fed is a monkey playing with dynamite.

I agree with that.

The purpose of adding liquidity is supposed to be to support increased activity in the economy. So with more money the banks should be loaning out all those excess reserves. But that isnt happening. Banks are not increasing loans and the velocity of money continues to move lower.

So they use this reverse repo facility to mop up some of that excess liquidity, while they still keep printing more money because they are afraid if they stop, the stock market will plummet. And that will stop the wealth effect, which is propping up consumer spending.

The problem is that they really do need to pull back the bond buying quickly, but if they do that too soon, they burst this bubble. That is a whole lot of risk and everything is not hunky dory as they want you to believe.

Interest rates have been trending down recently, as money moves out of risky stocks into less risky stocks and bonds. But this rotation could end violently, as money moves to the sidelines instead. One of the big problems here will be if the dollar breaks the existing support, then it will plunge to the next support level and that is a huge move.

I say that the Fed will move to stop purchases very rapidly, like possibly by July or August. The Fed has created a very dangerous set of circumstances.

Pushing on a string. The banking system is out of credit worthy borrowers so now they’re just sitting on tons of Fed injected zero yield cash (probably mostly business accounts, but then again plenty of individual accounts of anyone too scared of stocks and bonds). Hot potato money as Hussman calls it, but inevitably the majority of it still ends up in a bank account somewhere. So the banks no matter what get screwed with this 0% yielding asset if they can’t make a loan out of it for interest, but now interest rates are so low it doesn’t matter. Inflation is slowly killing the banks. It’s funny to me that rentier capitalism has tried to indebt the $#!7 out of everything until it threatened to collapse under it’s own weight unless the Fed artificially lowered interest rates. Now with zirp and nirp around the world they’re learning that there’s no free lunch as the rentier model starts to cannibalize itself. This happens when you can no longer get logical real returns anywhere (unless you’re willing to try to time a stock market bubble).

To “save the banking system” they may just as well start adding commercial banks to the government payroll. Heaven forbid the rentier capitalists lose their wealth in a grand reset. Instead we just keep inching towards a plutocratic centrally managed economy.

Everyone got PPPs and EIDLs. No borrowers left.

When we all look back to a time where a substantial portion of all savings were held by the savers, personally, in the form of stock issued by their local business community; everyone, saver and local business held substantial asset; against which their local bank lent working capital. Today, the majority of all savings are held by “Funds” . . . so the assets available for covering bank lending have accordingly diminished. Now we see that that flood of cash delivered to the “Funds” is constantly over flowing, back into the FED. The only viable road ahead is to return to where the savings were held by the saver, and to achieve that, we need a road map; such as; The Road Ahead from a Grass Roots Perspective.

So this is why I have been saying for some time now that we are moving towards a full reserve system with direct money printing by central banks. The commercial banks will be reduced to a user interface (which btw many fintechs are doing much better).

Central Bank Digital Currencies (CBCD) is another step in that direction. It doesn’t involve commercial banks anymore for money creation, it is direct money printing and passing it to government or population. This also fits into the Magic Money Tree playbook, where it is argued that the government shouldn’t borrow but just print money debt free.

Imo, the battleground will be between CBDC and private Asset Backed Digital Currency (ABDC), which lives completely outside the banking system and cannot be debased and are redeemable for the underlying asset (the obvious choice for underlying asset being gold).

Paying / transacting with an ABDC like Kinesis is essentially a trade in physical bullion, with your direct ownership registered on a distributed ledger (in this case a fork of Stellar), which is open source), is cheap and takes mere seconds. It marries useful technology that has emerged from the crypto hype with classic physical bullion trading that is as old as history itself.

The question of course is the extend to which vested interests will be successful in slowing down these initiatives. However, poorer countries are likely to embrace it first as they have suffered from exploitation by big banks, and of which large parts of the populations are still unbanked anyway. The 4th largest country in the world by population (Indonesia) is already embracing a gold-based parallel currency that runs on the Kinesis backend. It offers the government new revenue streams in gold, which they will use to top up their national gold reserves.

I here no mention of European bank’s collateral stifling interest in overnight lending. Any comment on that?

No, they won’t take a loss. Uncle Sam will simply print another $1.7 trillion to add to the other trillions of national debt. It’s their go-to solution for everything…until it no longer works. Again, that’s why it will be inflationary. I wonder if the two-thirds of Americans who favor student loan forgiveness realize that.

What a bunch of unmitigated clowns to think they have everything under control and interest rates across the spectrum of maturities are at their beck and call. When government autocrats start pounding their chests in self congratulatory hyperbole, it is time to head for the bomb shelters. No, this is not exactly what they expected, and no, they do not have everything under control. Wow. They sound like a bunch of professional wrestlers selling their own book.

Are the reverse repos a mechanism to avoid inflation without increasing the interest rate?

Why isn’t the market moved by these actions? Four months of QE have certainly moved the markets, but the overnight “undoing over 4 months of QE” doesn’t seem to have the reverse effect. This suggests that the term “undoing of QE” is probably not quite accurate?

They are only draining liquidity overnight. The swamp is still there. If we take what he says to heart, there is no end game in all this. BOJ used to routinely sweep cash out of MM accounts, and in the financial milieu of zombie banks no one blinked. The idea that CBs can inflate the stock market but not the dollar is arcane. Or that inflation isn’t really a devaluation of assets. Perhaps if we target 2% a year no one will notice? Beggar thy neighbor masks the coordinated devaluing of assets toward that socialist utopia. We’re not growing anything but BS artists and their Marx, or marks..

What is the great effect of “overnight reverse repos” when the Fed buys 120 billion a month with longer maturities?

What are you talking about?

The “swamp” was drained by that straight shooter, the billionaire who didn’t need any money, so he wouldn’t be corrupt! HAHAHAHA…….

Only in Murika can a slimy grifter geriatric silver spoon buffoon in a fancy suit land his gold plated plane in the middle of BFE, step out and put on a $1.99 (made in China) trucker hat and the local yocals guffaw and say “Uhhhmmmmm, look at dat….he’s one of US! Derp….meh…..”

“Marks”….yeah, to a lifelong conman, that’s all they ever were! Keep sending that money!!!! :)

I have to agree, the talent pool of president candidates has not been stellar for the last 30 years. One gets what they voted for, at least that’s the tag line.

Half a trillion dollars (and growing) that the banks cannot find good borrowers for. SMH

$500B in bonds are bought FROM The Fed for cash today, then the bonds are returned to the Fed the next day (overnight) and cash is returned to the Buyer.

Sounds like a zero-sum transaction and Fed’s balance sheet does not change. I don’t understand why this is getting attention.

Beardawg,

It would be a zero-sum game if they don’t buy ANYTHING tomorrow. But that’s not going to happen.

Tomorrow, they’re going to buy, for example, $510 billion, to replace the $503 billion that mature tomorrow.

On the Fed’s weekly balance sheet through Wednesday, which will be out tomorrow afternoon, the $503 billion of today will show up as a liability. Next week, it will be some other amount.

Thanks Wolf.

So there is kinda like a daily running balance of about $500B. I guess that is a fair percentage of the Fed balance sheet. If the running balance gets into the trillions, that would be interesting.

If the Fed doesn’t “tweak” its interest rates (RRP offering rate and IOER) or other things, my guess is that by June 30 (end of quarter), it could spike to $1 trillion.

I am bit confused. So with this process the money goes back to the buyer (which I guess is banks or financial institutions) at any given day no matter how much ($500 B or $1T) the amount. So this transaction is just to show liability on the Fed books but does not remove the liquidity from the market

Investor,

I’m the Fed. You’re the counterparty. You’ve got $100 that you don’t know what to do with, but you need a watch. And I have a watch I don’t need. So we make an overnight deal. You give me $100 and I give you my watch. The next morning, I give you the $100 back, and you give me my watch back. And then we take a breath and start over again, you give me $100 and I give you the watch for another day. Every Day. We can do this infinitely. This has the effect of permanence: I have your $100 and you have my watch which you can use however you see fit.

That’s how repos and reverse repos work. They’re very real, and it’s real money and real collateral and real balances. And it’s a huge gigantic market. And it can cause all kinds of problems if something goes awry in that market.

Thanks for the explanation Wolf. This makes better sense.

What’s the cause behind this? Clearly not cash, but lack of treasuries as a collateral, which the reverse repos are supplying.

But who is in need of treasuries?

Foreigners who borrow in dollars and traders who shorted treasuries.

And central bankers who need to control price/demand of treasuries due to some evil country dumping them.

@Petunia

Who would be so foolish to short treasuries, when the price of everything is controlled as these reverse repos prove.

Well, not everything, humdrum necessities of life like house prices are not, but those are things the overlords don’t give a chit.

The banks can roll those contracts indefinitely right? The fact the amount goes up or down a bit doesn’t alter the process. I am still unclear on how a Fed asset (paid for with an IOU) becomes a bank liability? or excess reserve. The Fed creates excess bank reserves buying Treasury assets (on the cuff), then using RRPO peddles that paper to the banks in exchange for those reserves, so the banks are directly monetizing the Treasury? Was there another instance of using QE and RRPO simultaneously??

So all those trillions are just bouncing back and forth between the Fed and the banks and not entering the economy as seed capital for new or increased businesses to borrow? Great.

And in a short while, a new clump of money ($1.7 trillion) will become available for “infrastructure” projects? How will those funds get into the economy?

Mostly with the purchase of private jets, and yachts, and estates, by Joe’s good friends who will take care of him on the flip side…..

Jdog – You mean they will change his feeding tube? Joe is going to be in an convalescent hospital before his term ends.

Why take a loan when you could get a government minted contract to build a bridge to nowhere?

So let me ask this in simple terms, if liquidity drove market prices up, won’t draining liquidity out of the market cause prices to go down?

1) Student loans written off gradually by the gov, without a major increase of the money supply, without Greenspan, Bernanski… the Cain’s family that resided in the Fed, since the 1930’s.

2) As result, for almost the same amount of dollars, young adults will have more dollars to spend, to get married and have a family.

3) The growth of supply of goods like houses, cars… will outpace the growth of supply of money.

4) Between 1880 to 1896, the wholesale price level fell by about 30%, or by

1.75% annually.

5) IBM 360 from the 70’s cost $5 millions, but an tiny AAPL cost $1K.

6) In China, a decades ago, or so, the GDP was rising about 7.5%

annually. The average retail prices declined between 1% to 3% a year, as result of the fall of production cost.

7) During this period, if the supply of labor was fix, than real wages were rising. That reflect the increase of the marginal productivity. The

purchasing power of every RMB, earned by employees, was rising as results of falling CPI.

8) There is nothing wrong with a “benign” deflation. The media is cancer.

9) Employees will buy more, or chose to hoard & hoard more ==> cash in the bank. A mild deflation will enhance economic prosperity.

If I hoard a thing of value, it may create a shortage. If it earns income it may be taxed.

Have you tracked the price of a home in China over the past decades? Why are the Chinese fascinated by gold, when they mine millions of new ounces of gold per year?

Are these reverse repos the reason the ten year treasury is falling?

US 3:2 Mexico

1) Example : one night a young worker lost his used car to the repo truck. Every day he walks/ jog…take a bus to work, coming back late at night. Every year he might save $20,000 – $30,000.

He can get married and feed a family. He can open a business…

Result : Less debt, more cars, more cash in the market. Moderate deflation is a good thing.

2) Example : a limited student loan jubilee for tech schools, for low

income family. Nurses, welders, aviation engineers, cyber…

Young people will be encouraged to go to tech schools, join the work

force within a short time and be productive.

Your example 1 is not logical. How many young workers spend $20,000 or $30,000 a year on loans for a used car? There may be a few male idiots who try to play ‘big spender’ and get a used Ferrari to impress even more foolish young women, but they aren’t the type of fools that typically get married and feed families. I also question why he would be more likely to open a business if he has to spend more type commuting by bus or walking to work. Extra time spent commuting is time that is not available to work on your business pursuits.

It’s also becoming more and more dangerous to be out alone late at night in most US cities that are large enough to have public transit.

Nope….still not doing anything, last I checked housing and stock market still wildly expensive and out of whack. Although bitcoin sure has dropped nicely but probably has nothing to do with tampering.

Not sure if these reverse repo is suppose to dampen the market mood but either a delay reaction or nothing can pull back this animal spirit now..

I don’t think this would have absolutely any material impact on any of the asset bubbles FEd has been propping for last few years

I guess the show would be on for few more years or decades

Anyone making sense of this insanity would is crazy

What exactly are the Fed’s current monetary policy objectives and what is their justification for them? With the PCE and CPI both running significantly above the Fed’s zero nominal interest rate (negative real rates), why haven’t they begun significantly reducing their $120 billion monthly purchases of Treasuries and MBS to allow interest rates to begin to rise? This Overnight Reverse Repo facility seems to me to be a component of a scheme to preserve QE-ZIRP and take nominal interest rates negative, even as the banks run up against regulatory capital constraints and the Fed uses Reverse Repos are used to dish out Treasuries to Money Market Funds. These Fed officials are not elected. Who gave them the authority to do this?

Way too little, way too late. There’s so much money sloshing around the economy that you can’t put that genie back into the bottle.

A few months ago I pointed out that RV dealers had almost no inventory, but then commenters showed up saying they were driving down the highway and saw tons of RVs on lots so that just couldn’t be true. Well it was, and IS.

“A major RV maker now has $14 billion in backlogged orders and is pretty much sold out for the next year.”

“RV maker Thor Industries has a $14.32 billion order backlog.”

Welcome to the clown economy, care of the FED and .gov, where a pandemic and the largest job loss since the Great Depression results in the most insatiable demand for durable goods in history. Because job loss = you get rich.

” The problem is a shortage of critical parts at manufacturing plants that makes finishing many RVs impossible or presents long delays. According to some sources, there are RVs sitting in fields waiting for just a few parts before they’re considered complete and shipped off to the dealers.”

I see this as an extremely fine tuning tool for controlling the liquidity in the market on a day by day basis.

QE would come in huge clumps on a weekly or monthly basis and could be disruptive, but this mechanism lets it be fine tuned, daily.

So far as interest rates are concerned I see direction as being the important factor, if successive ‘outs’ are bigger than successive ‘ins’, Interest rates are on the way up at the gentlest of paces. If these overnight removals get too large, they can sell a chunk of QE and take the RR’s back to zero and start building them up again. It’s like a shock absorber on the much coarser effect of minus QE. Extremely clever, in fact, in my opinion, and the Wonks must have access to some superb computer tech to be able to do this.

If it wasn’t for Wolf’s eye on the ball, only the insiders at the highest level would know this was even happening it’s so far off the radar.

Yes, maybe as a fine tuning tool to control short-term rates. The repo and reverse-repo transactions function more like loans with fixed terms than asset purchases in the open market. The QE asset purchases affect longer-term rates directly while reverse repo is being used (reportedly) to keep short-term rates from going negative (as Wolf suggests in this article).

Also, the very brief nature of the overnight “loans” means that the liquidity (dry powder) is still effectively there where it wouldn’t be in unwinding QE. That may be why the stock market is not reacting much to these repo operations as they don’t seem to affect liquidity or long-term rates.

Tonight, hypothecation take a break.

“Fed’s Reverse Repos Hit $503 Billion”

Isn’t it obvious?

The poors – who according to so many here are taking the mostest of govt spending – are using their $300/week to buy all these reverse repos and living the Viva Loca.

$300/week…is that Mrs Allen Greenspanes laundry tip money?

Just ask Javit Chip and Banana2.

If we just would cut taxes on taxes that corporations and the rich aren’t paying, the budget would be balanced already and this wouldn’t be happening.

Because corporations and the rich are paying too much taxes on the taxes they aren’t paying.

Maybe some can ask him to define normal?

“The Fed could get a handle on this liquidity phenomenon by tapering asset purchases and eventually reducing its balance sheet.”

Nope.

The system is working really well. We have everything under control. Ignore the iceberg.

Sincerely, your captain from the upper deck.

“The system is working really well. We have everything under control. Ignore the iceberg.

Sincerely, your captain from the upper deck.”

That brings to mind a picture of Powell as captain of Titanic.

On the bridge one frosty night, the lookouts spy a gigantic iceberg dead ahead. Capt. Powell does not blink one eye.

The other officers on bridge are astonished as he orders full speed directly ahead.

“But captain, what about the iceberg?”, cries the first officer.

“Not to worry”, replies Capt. Powell. “We expected that to happen. This ship is working exactly as designed. Really, no concerns about that. Get a grip, my friend.”

Not to over-indulge in a dire fantasy but I imagine something along the lines of the spider head from John Carpenter’s movie The Thing.

The flame thrower in that scene is a metaphor for higher interest rates.

1) Volatility comes in clusters.

2) RRP comes in clusters.

3) If the Fed will build a RRP cluster until the end of the quarter, there will be less hypo in the next 15 trading days, less money supply ==> JP taper.

What effect would the Fed raising the EFFR to fight inflation have on interest payments on the national debt?

The government would have to borrow a little more to make those additional interest payments. That’s it. Compared to the overall mega-deficit, it’s not the #1 problem.

Nobody wants cash. They want something that will be convertible to the next monetary replacement, whatever that may be….I have people knocking on my doors and calling me asking if I will sell them my properties, I have never seen anything like this. I only invest in land and productive manufacturing capabilities.

Last time this happened there were comments that some big players must be short of collateral to guarantee their loans overnight and the FED was backing them up.

I guess this is true again. But it must be some very big players.

European banks behind the curtain with toxic debt remaining from the Great Housing Crash. Without an EU TARP, the “federation” has no clothes.

The ECB is buying sovereign debt hand over fist.

The Martens (Wall Street On Parade) propose this idea:

” corporations are wary of parking their idle cash in money market funds holding securities other than U.S. government paper…”

“Since Treasury money market funds, that so many corporations and institutions are flocking to, typically cannot hold anything longer than a one-year instrument, there may be a surge in demand to get one’s hands on one-year Treasury bills.

Whatever is causing the rising fear on Wall Street, there is no question that the fear is spreading to more firms that do business with the New York Fed.”

Trailer Trash,

This is fiction and BS, like so much on that site, including their entire click-bait coverage on repos in 2019 — they had no clue how repos worked, none, zero, and kept posting total garbage. If you want to know how repos and reverse repos work, and you want to go to another site than here, go to Zero Hedge. They’re very good about this arcane financial stuff.

OK, thanks for the heads-up. It’s always interesting to see different opinions.

Is there anything to the idea that corporations are sitting on growing mountains of cash and are afraid of the money market funds? I recall that in 2008 (?) some of them “broke the buck” which resulted in a big commotion.

No, they’re not afraid of money markets. This whole concept you quoted of “rising fear” is nonsense. Big banks are flooded with corporate deposits, and they told their clients to take their money out of their bank and put it into smaller banks and into money market funds. And they did. So now, money market funds are overflowing with corporate funds and they’re chasing after things to buy with it, and they’re doing it in the reverse repo market, which has pushed yields to zero or below zero. Hence the Fed helping out by selling Treasuries to those funds. That’s part of the dynamic here.

Isn’t this a matter of banks not wanting to lend to each other?

No. The opposite. Banks have too much cash (from deposits). The whole system is flooded with cash. That’s what this reverse repo issue is about.

If banks were unwilling to lend to each other, the Fed would use repo transactions and not reverse repo transactions to alleviate the situation. We would also see rates being near upper bound rather than lower bound.

NY Fed breaks down how much each counter party type takes down on an aggregate basis. They won’t tell you who the exact counter party is, but will tell you the type and how much. The majority of the uptake is done by money market funds, and not banks, gse, or primary dealers.

Banks have more or less stopped using the reverse repo facility b/c they have IOER that pays more. Previously, pre-2018, the facility was used at quarter-end by non-US banks to create window dressing for their balance sheet.

I got it.

So too many reserve deposits (because … they’re not lending?)

Heaven forbid we should mention EU GSIB anyway, right?

We had a TARP.

D’ya think REPO could go to 10% again? No offense meant.

Just enough snark to wet my beak, is all.

1) The $6T budget was born to fail.

2) The infrastructure program, possibly, was born to fail.

3) An attempt to please the Bernie’s crowd, to fail Chuck D’Israeli and to blame the other side.

4) Two failed attempts to extrapolate debt, to Cain the economy might be enough for a change of character, to deflation.

5) There will be less 500,000 elderly to support. In the next decade gov support will deflate the boomers tsunami.

Comment moderation : 6) SPX made a new all time high, an UT, but UST10Y and the German 10Y don’t care.

7) SPX made a new all time high in deflating dollars.

Thanks, this is really valuable info & thoughts.

I thought the operation was supposed to be limited to $500B. E.g. here it seems to state an “aggregate operation limit”. https://www.newyorkfed.org/markets/domestic-market-operations/monetary-policy-implementation/repo-reverse-repo-agreements/repurchase-agreement-operational-details

Am I misreading that? Are you telling me there is in fact no limit?

Is there any publication where they announce in advance what they’re going to do with repos? (I mean other than Wolf Street — like from the Fed ;)

John,

“Am I misreading that? Are you telling me there is in fact no limit?”

You’re mixing up “repos,” which you linked, and “reverse repos,” which I discussed. “Reverse repos” are the opposite of “repos.” There are currently $0 “repos” outstanding.

Reverse repo.

I have $500 billion extra in my checking account. I give it to the Fed and they give me $500 billion in return and a new Timex watch tomorrow.

Why do I have to do this trade?

Why do I have $500 billion in excess?

What if the Fed is not available to offer me a watch “overnight”?

And, why does this escalating overnight reverse repo need to be done every night? Especially for a cheap ass watch for $500 BILLION. Analogy obviously – but for a fraction of a fraction of a percentage point.

Awesome work Wolf!

Wolf: “So now, money market funds are overflowing with corporate funds and they’re chasing after things to buy with it, and they’re doing it in the reverse repo market, which has pushed yields to zero or below zero. Hence the Fed helping out by selling Treasuries to those funds.”

Is this ‘Fed helping out’ referring to the Fed doing overnight reverse repos with the money market funds? How would this help the funds if it is overnight and no return?

It seemed like the article and some of the comments indicated that the Fed’s reverse repos were some kind of Rube Goldberg device that helped FOMC “regulate” federal funds rate trading / short term interest rates.

The Fed’s reverse repos help keep the yields in that market from turning negative. This allows money market funds and banks and whoever to get rid of cash without having to pay a price (negative rates).

Help-you don’t mean the endless, self-generated/self-serving, dead-ends that the poltroons running this so-called ‘audit’ in AZ keep attempting to drive through on the public dime, do you, ?

may we all find a better day.

Wolf, long time follower of your great blog, my first time to post a comment.

Can you (or someone else on here) please explain couple of things to me??

1) Banks have too much cash and all the reserves piling on their balance sheet affects their SLR (Supplementary Leverage Ratio), reserves are assets on banks books so they either raise capital against their increasing asset base or get rid of the reserves, this is, as I understand, the main reason the Reverse Repos are spiking so much.

The SLR exemption expired in March, my question is: Reverse Repos are an asset swap in the balance sheet of a bank (Reserves for Treasuries), so an asset is still there (the Treasuries) so this does not affect the SLR anyway??

2) Reserves are assets on bank balance sheet and liabilities on the Fed books, when a Reverse Repo is executed, the bank balance sheet replace Reserves for Treasuries but what happen to the Fed books?? The Treasuries swapped leave the Fed books but reserves are not assets for the Fed (the Fed creates them on the fly when they buy assets). Does the Fed book “shrink” with just a record somewhere in the Fed system of the transaction to be unwound?? I hope I explained myself sufficiently!!

Thanks

Dominic: “The SLR exemption expired in March, my question is: Reverse Repos are an asset swap in the balance sheet of a bank (Reserves for Treasuries), so an asset is still there (the Treasuries) so this does not affect the SLR anyway?”

I’m not sure why money market funds or banks would want to get rid of cash (as Wolf mentions above). Because cash seems like the most liquid Tier 1 capital (I think, anyway) and would be good for a bank’s SLR.

I’d be willing to hold the bank’s cash for as long as they wanted me to. And I wouldn’t charge them any repo fee when they wanted it back.

Not all deposits that sits on the banks balance are the same. Basel 3 introduced weightings on the deposits and how “sticky” they are. A retail deposit v non-operating deposits from corporations are weighted very differently.

Currently banks are telling some of their corporate clients to move their deposits or get hit with a fee. Corporate deposits only real option is to move it to a money market fund. The current 500b in the reverse repo facility is more or less showing, these mmf are unable to find assets that yield more than 0% in the current market. If they could find an asset > 0%, they would buy it.

Plumbing thank you for your reply, however some aspect are not clear to me. The banking system, as a whole, cannot get rid of reserves, they can just move from one bank to another within the Fed system or be Reverse Repoed at the Fed facility. Reserve can be removed only by the Central Bank. Are there Money Market funds existing as separate entities from banks and that have their own Reserve accounts at the Fed or are they just different divisions within banks or at least relying on an “underlying layer” of banks when it comes to reserves management??.

Thanks!

Dominic

Your welcome. The comment section is a great way to learn off one another.

You are right that reserves can only be destroyed by the central bank issuing it. It is just a game of hot potato at this point. The reserves/deposits essentially have to move away from anything affiliated with the bank for the bank to get balance sheet relief. I am going to point you towards someone who does a much better job describing the process of how a bank sheds the reserves than I could.

Search: American SICO – 4.1 A Band-Aid Known as Reverse Repo

Barton does a great job breaking down the entire RRP process and how a bank sheds the deposit they do not want.

Plumbing thank you!!

The FED has to keep that ponzi scheme going to keep the dollar from slipping off the cliff. Its hanging on for dear life now. More gimmicks to keep the ponzi scheme cranking. One gimmick after another. But no matter what they do all ponzi schemes eventually collapse. Whats the next gimmick there gonna come up with? It’s pure insanity whats happening in the world today. Crypto crap which everybody thinks bitcoin has a limited supply. Its unlimited. Each coin can be broken down to 100 million bits. If bitcoin was supposed to be a dollar and it went to $60,000 the supply increased by a factor of 60,000. Simple math can tell you it has a unlimited supply. People buying invisible statues and NFT art. I have grains of sand, grains of sand here, get your grains of sand only $1 each, grains of sand, get your grains of sand. At least sand is real. If fiatl is worth money, crypto is worth money, invisible art worth money then what the hell grains of sand are worth money too. Oh wait people dont know what money is. Read the constitution it specifically states only specie(Gold and Silver) is money. Anything else is just a illusion and illegal according to the constitution. IQ’s are steadily dropping in this country. We live in a world of morons where people believe the most ridiculous crap. Gods, fiat, crypto, NFT, pandemics lol. The real Gods are the super rich that done bought and paid for everything in the world including the corrupt ass government we live under. Wake up morons and smell the stench. Be a free thinker and quit having your thoughts told for you.