Investors in subprime auto-loan Asset Backed Securities should be genuflecting in front of US taxpayers to thank them for the backdoor bailout.

By Wolf Richter for WOLF STREET.

Subprime auto loans are risky but very profitable because they carry high interest rates, even in these times of crazy-low interest rates. Much of the risk is shuffled off to investors by securitizing these loans into subprime auto-loan Asset Backed Securities (ABS), that are cut into tranches, ranging from the highest credit rating that take the last loss but get the lowest yields, to the lowest-rated tranches that take the first losses, but get the highest yields. So there is something for everyone.

Repossessions of vehicles are generally easy and fast, and there are not a lot of hoops to jump through, and there is a very liquid auction market to dispose of the vehicles efficiently. Professional repo firms get the vehicle, clean it up, and take it to the auction. For subprime lenders this is all pretty slick.

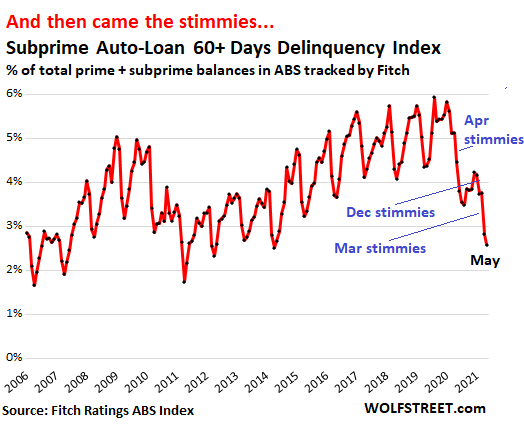

So subprime auto-loan delinquencies of 60 days and over that had been securitized into ABS and were rated by Fitch had been rising for years as lenders were taking ever more risks, amid a voracious appetite among institutional investors for subprime auto-loan ABS. By 2016, the 60-plus days delinquency rate blew past the highs during the Financial Crisis. In August 2019, it matched the spike of October 1996, the worst in the data. And in January and February 2020, the delinquency rate blew by the worst Januarys and Februarys ever. So this was going in the wrong direction. And then came the stimmies.

In May 2021, the 60-plus day delinquency rate of subprime auto-loan ABS dropped to 2.58% of total auto loans (“prime” and “subprime” combined), according to Fitch Ratings. This was the lowest rate since 2012, when delinquencies dropped because by then the delinquent loans from 2009 through 2011 had been written off and cleared out of the system, and lenders had become circumspect with new loans.

Fitch’s ABS delinquency index for “prime” auto loans, which had remained below 1% even during the financial crisis, dropped in May to a historic low of 0.14%.

Clearly, the stimmies had been used in part to catch up on past-due auto loans. And this didn’t particularly help the economy, or jobs, or whatever, but it bailed out the lenders and investors that might otherwise have seen big losses on their subprime loans and ABS.

So that pension fund in Texas, California, or Norway, and their beneficiaries, should be genuflecting in front of the stimmies, and in front of US taxpayers that paid for this backdoor bailout.

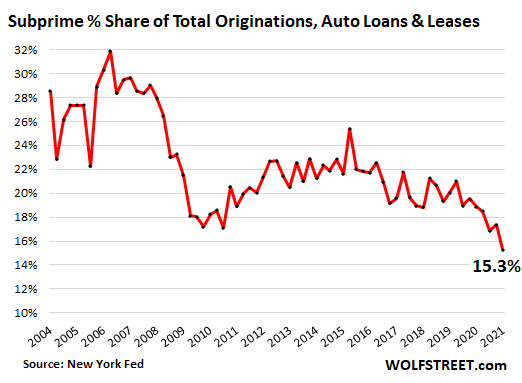

But at the same time, auto buyers with subprime credit scores – below 620 – have stayed away from buying a vehicle, perhaps deterred by the crazy new and used vehicle price increases, or perhaps because they still hadn’t gotten a job.

According to the New York Fed’s Household Debt and Credit Report, the share of subprime-rated loans and leases being originated in Q1 2020 dropped to 15.3% by loan amounts, the lowest level in the data going back to 2004, another confirmation of the K-shaped recovery:

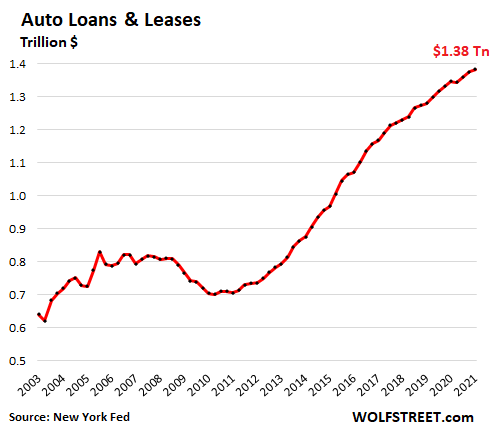

At the end of Q1, there were $1.38 trillion in auto loans and leases outstanding, up by 2.7% from a year earlier, the smallest year-over-year growth since 2011, despite massive price increases of new and used vehicles, which should have driven up loan amounts. This may be a further confirmation that more people paid cash, perhaps plowing their stock market gains into the economy; and that more subprime-rated potential customers are on buyers’ strike, either not wanting to or not able to buy at those prices.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, I look forward to each and every new post.

“securitizing these loans into subprime auto-loan Asset Backed Securities”

I can’t get my head around viewing debt obligations to high-risk (loser) borrowers as an “asset.”

A person’s debt is another person’s asset. It’s all a matter of perspective.

the perspective of one persons no debt and everyone’s stimulant.

I think we are getting closer to a new brand of coffee.

Love your comments RB, no matter what you are or are not!

Please continue to amuse and entertain and educate us wolverines,,, aka Wolfstreet.com regulars…

Thank you for your efforts…

And may the Great Spirits, ( to which all of we, who care, all of we hoping type folks,,, know / hope to achieve BTW )

And may the Great Spirits help us all to at least begin to understand ALL of what/who WE the People vote for…

Better not to mention the absolutely intentional confusion promulgated by the Fed and so many similar Federal ”guv mint” agencies in order to screw us working folks and retired folks…

Thank you…

When somebody has taken out a loan to buy a car/house/etc., they are obligated to make a stream of payments (long) into the future.

It is that stream of incoming loan payments (which include both partial repayment of principal and interest) that constitutes an asset.

Loan originators can sell off their rights to these repayment streams.

Such streams from many, many loans can then be bundled together (for risk diversification purposes).

Then there are aggregated, very large streams of loan repayments coming in.

For further segmentation of risk exposure, these bundled loans can be turned into publicly traded securities that have different priority rights to repayment (tranches – like tiers on a wedding cake).

The toxic tranches at the bottom of the securities “cake” are responsible for absorbing all losses before a higher rated tier/tranche has to suffer any (think compartmentalized flooding in a sinking ship).

A lot of these concepts are not bad ideas…they greatly help to diversify and segment sales of risky debt.

But…

1) Market players, etc. have abused these tools beyond their ability to help – making known god awful loans, only to dump the risks on the general market public.

2) The underlying physical US economy is dying faster than the tools can help. Systemic economic collapse in the US cannot be diversified away so long as investments are in US “assets”/dollars.

An outstanding film explaining all that: The Big Short. And a great quote from it relevant to so many important topics even to this day:

Mark Baum: “It’s time to call b******t.”

Vinnie Daniel: “B******t on what?”

Mark Baum: “Every f****g thing.”

– from the nonfiction film “The Big Short” (2015)

And, eventually, we’ll get to another great quote from that film:

Mark Baum: “Boom!”

Cas127

Excellent recap of layered debt tranches and securities offered in association thereto. I make my living as a 1st position lender for residential properties (cash flowing rentals purchased from me by other investors – I carry the loans).

All my loans are 10% interest only. The profit calcs are so easy to make with such loans (10% on the invested principal, every year to eternity or to the end of the loan term). I thought about “bundling” all my loans and selling them as a “fund” (which I could not do because I don’t have enough to create a fund). I see these Loan Fund ETFs paying out in excess of 15% annually – or at least that is what the purchaser of shares of the ETF is willing to pay.

When most of the loans in those ETF portfolios are 30 year term at 4% interest, maybe some of them slightly higher, I ask myself how in the hell an average profit of 5% (interest earned) in the fund creates a share price increase of 15% or more – EVERY YEAR ??!!

Beardawg,

Very interesting.

If I understand things correctly (and I may not).

1) You are more or less providing what looks like owner financing to putative investors who “buy” (in quotes bc no principal amortization apparently) rent flowing properties.

My guess is that said investors are putting little to nothing down because it looks like you are able to get 10% interest pmts in 3.5% mortgage world (wow!!).

So your risk is theoretically high (low to no down pmt from investor-“buyers”) but in practice you still more or less own the house (no amortization paid on your loan so no equity to them, and my guess is that you retain title…so any possible foreclosure would, in theory, be very speedy).

This is an interesting, albeit a bit convoluted, business model…and I’m curious as to the kind of investors willing to pay 10% (on a house they really don’t own, possibly).

And, my guess is that those investors are always on the hook for the initially agreed upon home sale price/loan principal from you…regardless of mkt movements.

Of course, they could always walk away…but you would get the houses back fast and have a (large) claim against the investors.

Perhaps I am mistaking some of the details.

2) My guess is that somebody, somewhere is buying up/bundling paper such as your own. If my interpretation is correct, that is paper drafted very favorably to you/any subsequent buyer. In the ZIRP world, I’ve gotta believe there are more than a few good size buyers of owner-financing notes. If not, perhaps a lack of standardization impedes the mkt.

3) As to the mystery of 15% ETFs in a 5% world, my guess is that is the yield on the trashiest of toxic 1st loss tranches, for mortgages doomed at the outset.

Then bundled into an equity ETF to try and muddy up what is really going on (being on the hook firstest and mostest for horribly underwritten mortgages).

The stated yield is huge because securitizations can direct cashflows first to any tranche/in any amount that designers want…but that almost always comes at the price of taking the first losses up to some horrible level.

(ie, getting 15% for two years before losing 90% of your principal due to mtg defaults)

Please keep posting…”creative financing” in the housing mkt isn’t discussed here too much…but it will have more and more of an impact as home prices exceed median incomes more and more.

And if enough “creative financing” is going on, it can gave unexpected impacts upon the macro stats.

MiTurn and Cas127 – Excellent question and summary!

But add this: the Vehicle (or other collateral) is also an asset. If the borrower stops paying, the lender at least recovers the value of the collateral too (less expenses).

These subprime loans are secured by collateral. If the borrower stops paying, the creditor may call for a tow truck operator to pick up the vehicle and bring it back.

And someday the defaulted cars may simply self-drive themselves back to the lender’s preferred dealer!

Amen. Also, keep in mind that the “Fed” will ultimately bail out those institutional lenders involved as their losses mount, because it is owned and controlled by the billionaires that own them, whose welfare the “Fed” protects at all costs. Bless ordinary Americans; they are tightening their belts and paying off their debts with their miniscule assets and income.

Sadly, it will not be enough. Hyperinflation is inevitable, because the economy needs stimulus and on top of that, the “Fed” is admitting to buying $40 BILLION a month right NOW in mortgage backed securities (“MBS”), aside from other things that it is doing to bail them out, including the #2 TRILLION that it created in 2019 and 2020 to purchase other MBS. That will ultimately drive inflation higher.

At a minimum, I predict that in the next two years, interest rates will rise significantly, including (as slowly as the “Fed” can manage it) interest paid on treasuries. That will raise American’s required, interest payments dramatically.

As I had stated before, if the interest rates on rolled over treasuries increased enough, the federal government will have to cut spending drastically. With extremely low rates being paid now, due to the “Fed” manipulation to profit the banksters who pay their “Federal” Reserve 2.5% a year on sums that they borrow from it and charge you and I approximately 25% a year on credit cards, the interest payments are currently only 9% of federal revenues. See “How High Are Federal Interest Payments?” in crfb dot org. That amount paid is $303 billion a year and will rise dramatically.

As the article cited puts it, “For example, if interest rates were one percent higher than projected for all of 2021, interest costs would total $530 billion — more than the cost of Medicaid. If rates were two percent higher, interest costs would total $750 billion, which is more than the federal governments spends on defense or Medicare. And at three percent higher, interest costs would total $975 billion — almost as much as is spent on Social Security benefits. On a per-household basis, a one percent increase in the interest rate would increase costs by $1,805, to $4,210.”

Thus, if the “Fed” were to raise interest rates now (after they have stealthily transferred TRILLIONS covertly to their bankster owners for decades) as some have implied can be done easily, the federal government’s interest expense would rise to catastrophic levels as far as the federal budget is concerned. They would then face greater pressure to close the loopholes that have enabled the rich to evade/avoid paying taxes for decades. See “”The Secret IRS Files: Trove of Never-Before-Seen Records Reveal How the Wealthiest Avoid Income Tax” in propublica. See also “Britain’s Second Empire: The Spider’s Web.”

It’s simple math actually. Subprime borrowers, if you look at the amortization of their loan, the first year of payments is simply applied to interest alone.

If they default within a year, maybe two, as Wolff stated, there’s little hassle in seizing the asset.

You polish it back up, place it back on the market, and use it to bait your next catch.

May seem like too much hassle, but most of those loans yields a 15-25% interest rate. Other than CC debt, what investment returns such a rate?

It’s pure GOLD!!

Repo guys are having a tough time eh, they will have their day in the sun again.

Another resounding success for MMT. Let’s do more. This is great . I love the sugggggggggaaaahhhh………. Reminds me of my days in San Fran sitting on a soon to be FPO mailing address ,courtesy of tricky dick. The Filmore West “house” band Quicksilver Messanger Service had a hit . Have another hit of Fresh Air. Whoa Nelly !! the grey matter is dredging up Captain Cody and the Lost Planet Airmen and Flash Cadillac and the Continental Kids. Single Malt is way F?fking better than Prevagen.

*NOT quite there yet

Thanks for the Great Idea :)

I can start loaning money then go in the repo Business and sell for more then they paid for the Cars ( as they went up ) :) I just have to make sure I don’t sell to Government Agencies as they well just print more money to avoid Repo

I was wondering when you where going to offer solutions and what they might be Humm .

Solutions to what???

So Wolf the risk has gone out of these high yielding securities? Where do I buy some, and is the lower number of subprime paper being created put a premium on this asset?

DB:

“Tote the Note” lots (buy here / pay here) have been doing that for years. They require a down payment for a car that’s more than they have in it (built in profit already), finance the balance of the sale, the guy pays for it for awhile (more profit), customer “goes bad”, the TTN lot repos the car, then resells it following the same format. Sometimes, they let them keep the roach because it’s more of a hassle to go get the car and they already saw daylight in the transaction.

Rinse. Repeat.

Close, but not how it really works anymore. After 10 years in this business I can tell you the industry average down payment is 800-900 for a used car. Lately our average cost of car is 2,000-$3000, and that’s before we fix issues. Average selling price is 6-7000. Not a massive profit unless it goes the distance of the note. Then there is the human factor, no maintenance is done and the car is driven until it stops moving. Customer then goes to next TTN lot. Or worse yet in our case last week went to repo a car and customer was living out of it. Hard way to make a living most days.

Buyer’s Strike for $500, Alex!

I’ll go for sub-prime going on an involuntary Buyer’s Strike due to a lack of money and jobs. The punch bowl is now empty! It is “inflated” hang over time!

I am not buying Coke, lumber, or a vechicle because I am blind! Tesla self driving coffins don’t interest me one bit!

Get a base Lightning. 40k -7500 standard deduction -2500 made in US -2500 made in a union shop … happy days!

“ Tesla self driving coffins don’t interest me one bit!”

Are you sure? Do you plan to be cremated instead? Don’t worry, the Tesla can be equipped with a flame thrower, also made by an Elon Musk company. They can service your end of life needs there either way.

?

No need to buy the flame-thrower add-on. Numerous news reports indicate that “Auto-Cremate” is an undocumented standard feature.

Yes, that is true, the advantage of a lithium based fire is that it’s just slightly more difficult to put out since it’s more of a chemical fire.

Thank you for the reminder about not needing to add on the flame thrower feature.

Save some ?

G-7 finance ministers, today, after years of discussions, have reached a historic decision to reform the global tax system, to make it fit for the global digital age – & crucially to make sure that it is fair so that the right companies pay the right tax in the right places.

If finalized, it would represent a significant development in global taxation.

ME: Change need to happen & it’s been a long time coming .. if it eventuates.

Can we have a comment please Mr. Richter.

This G7 drove is so smart they included the jurisdiction of second largest economy for that agreement. Wait, what’s that? China is not part of it?

Maybe they have not yet approached the Chinese on joining….LOL

China to G7… if you want you iPhones, your TVs, your appliance, shut up.

Speaking of the G7, I never noticed, when did they put in the EU flag in there? Kinda hard to be the G7 when there is 8 flags. So that means when it was G8, there was 9 flags?

Well the Big Ten now has 12 football teams.

What if they just made France, Germany, and Italy all one country and called it the EU, then we’d have the G5. Less people, more succinct.

1) Home equity loans might reduce c/c and car loans, along with the stimmies..

2) Home equity loans are falling since 2009 to $262B/Y. They are the cheapest.

3) Since RE prices are rising, home owners might finance consumption

with cheaper rates.

4) There is one thing they forget : inflation reduce the real value of their house.

5) SF & NYC RE nominal prices are down 30%. Due to inflation the are down 38% – 40% since the peak.

6) If suburbs RE go south, those who bought lately might lose their entire equity.

7) Example : if Palo Alto RE market will be down 20% in the next 4 years, in

the next 6 years, due to inflation, the real value will be down 30%.

8) If brand new 2021 car book value will be down 40% in 2025, the real value will be down 50%, due to inflation.

“3) Since RE prices are rising, home owners might finance consumption

with cheaper rates.”

Golly gee, that worked out swimmingly for homeowners who tapped out home equity loans just before subprime housing crash of 2008-09– NOT.

With all due respect Mr Engel, that is appalling advice to give near end of the housing bubble to end all housing bubbles…

“appalling advice to give near end of the housing bubble”

Engel is just following precedent set by earlier Fed chiefs (appalling advice).

That would explain his cryptic announcements…he is in line for Fed chief.

We have a 2019 Toyota Tacoma base model pickup we purchased new as an extra rig for projects and such. As it is a base model we only paid about $22,000 for it. After wolfs posts on crazy used car prices I looked it up on KBB and it appears it would fetch $10,000 more than we paid for it. So we cruised by the Toyota store to check out what we might want to replace it with if we traded it in. The lot was empty, very few new cars, zero pickups and a few scruffy used cars. This is a major metropolitan Toyota dealer and they had tumbleweeds in the lot. No wonder there are strange going ons with every aspect of the car business.

Add to that the proprietary software required for repairs of new cars. It forces buyers to return to the dealer for any work. My buddy told me years ago he could not do a simple brake job on his Jetta without their software. Brakes….a 30 minute job in days past.

I was wondering just today if new cars will last beyond the 7 year financing terms many buyers choose to utilize? Any repair seems to start at $1,000. On tv old rappers shill for auto repair insurance plans. It all seems unworkable.

“Add to that the proprietary software required for repairs of new cars. It forces buyers to return to the dealer for any work.”

Exactly right! And I know from experience that auto dealerships are shysters.

I fix my own cars. The choice between paying $150 in parts and doing my own labor or having the dealer charge me $1000 is a no brainer. I’m just glad that I have the skills necessary. I know that most people don’t.

“I fix my own cars. The choice between paying $150 in parts and doing my own labor or having the dealer charge me $1000 is a no brainer. I’m just glad that I have the skills necessary. I know that most people don’t.”

One simply has to assume that you are lucky and own older vehicles that don’t require dealership’s proprietary software and tools to service them. Good for you.

The “proprietary software” for brake jobs is typically to cycle the ABS pump when you bleed the brakes…. There’s devices you can get (for not a lot of money) to access those features through the OBD port (reset CEL for example as well as “read the codes”. The more sophisticated systems are obviously more expensive.

What you are describing is the current flap over “right to repair” legislation winding it’s way through the various state governments. It’s hit the farmer’s especially hard because they can’t fix their equipment themselves (all computerized) and the cost to transport a combine to the franchised dealer is prohibitive unless they own their own flatbed tractor trailer.

Car parts? You should try HVAC work! Local company wanted $500 to replace $30 worth of start/run and a run capacitors. Shot me a number approaching $2,000 to “maintain” my heat pumps. Did both for about $150 – including cleaning the coils (both condensing and evaporator). Two beers, some water, coil cleaner, and about an hour. Still had 10 beers left, enough coil cleaner to last a few years, and the part numbers to have the capacitors in reserve stock.

“Did both for about $150”

El Katz,

Where did you go (sources) to find out how to diagnose and fix the AC problem?

Knowing where to find the information necessary to “cookbook” a fix is 85% of the battle.

Look at Mikey Pipes on YouTube.

Paulo,

Having owned cars for over forty years, I have to agree that repairs ARE more expensive.

BUT they are far less frequent. My memories of car repairs, once the car were more than two years old, regularly occurred every two to three months.

Newer cars such as I now own have gone four or five years with no repairs AT ALL!

This is hard for an old codger to admit, I like things like this FAR better than overly rosy views of “the good ole days “

My 8-year old Toyota is now priced at what I paid for it 5 years ago. It’s not that Toyota here lacks any new cars though and I might take them up on it.

My sister was offered $38K for her 2015 Toyota 4Runner Limited from her local dealer when she had it in for service. She paid $44K for it -brand new- back in 2014.

In our local paper there was a indignant letter to the editor complaining about how the county appraisal office was ripping him off with the value of his car. It had gone UP since he bought it new, and he knew that was impossible….

Since I read this place, I was amused…Thanks Wolf for a smile.

A Debt Jubilee is just another form of theft from someone else, imho. It is the same as mortgage forbearance, rent moratoriums, student loan forgiveness, etc.

What ever happened to natural consequences? People borrowed money for a car they could not afford to buy. People then lose car. If people stop buying expensive cars, maybe manufacturers will produce a product that is affordable. Maybe a reconditioning of older cars will pull the rug out of the current crazy options out there.

“A Debt Jubilee is just another form of theft from someone else, imho.”

I completely understand where you’re coming from. I think, however, that in this case the jubilee will be freedom not from debt but rather from the phony money we have been forced to live with. I consider jubilee to be the day that honest assets are compared only to other honest assets, and the manipulating and distorting forces of our present politically-based currencies are eliminated for generations to come.

What kind of debts are we talking about here?

Please wait until I go load up on those first.

I am just astonished debt jubilee is seriously being discussed as a public policy.

Paulo

It’s true, the general idea of “debt jubilee” with no other qualification does seem overly simplistic,

But a question:

When the Fed creates $3T of money, and gives it to people with questionable bonds–so the people with those worthless bonds don’t panic, that essentially gives real money with real buying power in exchange with something otherwise nearly worthless. If that real money were taken away from the former bondholder, would that constitute theft from the person who formerly held that worthless bond?

Is it a “natural consequence” that those bonds should be made whole? Seems to me that constitutes theft from all the people who have earned their money through hard work.

If money can be given with some wealthy suffering no “natural consequence” at least it’s understandable to me why some people talk jubilee.

It’s hard to respond without knowing the details of this debt jubilee proposal. Are you saying all the debt held by the Federal reserve should be voided? Or are you suggesting student debt, auto loans, mortgages etc should all be forgiven?

In any case, one of the wrong assumptions you are making is that jubilee only affects the ‘rich’. A lot of times the counterparty is a pension fund or a ‘non rich’ retail investor.

That’s the part that is always overlooked. If the Fed can’t dump all of those bonds back on the market (which is the only way to remove that liquidity from circulation) at the same prices they paid, who takes the loss?

Obviously, when they bought trillions worth of bonds in March-May of 2020, they paid way above market prices.

Nah, -NO- debt jubilee!

We need a massive, worldwide deflationary crash via bankruptcies which EXTINGUISH debt, a crash that is too large for central banks to stupidly cover via the bailouts they’ve been using thus far, thereby FORCING the return of the absolutely essential Darwinian mechanism of capitalism, bankruptcy of the weakest, which would then result in actual price discovery again VIA that PROPER mechanism and NOT some blanket forgiveness of all debt even to those, as in the GFC, not deserving of it.

@RNYer

If you don’t know who is taking the loss, look in the mirror.

For better or worse, we are in a closed system, where someone is always impacted, whether you like it or not, you are at the poker table. The sucker is you (Metaphorically speaking, of course) and me because it’s Vegas rules, and we are just stuck for the ride.

The way I look at it, all this is doing is inflating the money supply with the consequence of destruction or devaluation of the value of our work, past, present, and future. Eventually, when the bonds comes due, the Fed might be left holding the bag, but it’s really us because the Fed prints more money and make the problem disappear one way or another.

MCH, I’m asking in terms of accounting though, not reality. If the Fed prints $4 trillion to buy bonds for $4 trillion, and the tapering results in those bonds being “sold” for $3.5 trillion, what happens to the $500 billion write down on the Fed’s balance sheet?

I understand/accept it is way more complicated than my shoot from the lip response about a Debt Jubilee, especially when debts are packaged up as investments.

I’m not looking beyond individual responsibility, and that does included investors in debt instruments. But take student loans for example. What about all those individuals who kept their borrowing down to a minimum, and those who paid off their loans one month at a time? Or those who bought a cheap car, did without until they could afford to buy one, or paid off their debts?

If there is a debt jubilee forgiveness plan for the loudest issue in the room, then taking that to a ludicrous conclusion those they did pay off their loans should be reimbursed.

Reparations for the responsible. :-)

I’m kidding here, but if society spends money willy nilly then there is not much left for those who really do need help. I believe we should help those less fortunate, but not those who are less careful or feel entitled.

“If money can be given with some wealthy suffering no “natural consequence” at least it’s understandable to me why some people talk jubilee.”

Supporters of a so-called ‘debt Jubilee’ style need to consider unintended consequences and who are the winners and losers of a jubilee (there are always winners and losers).

Ancient Hebrews did not consider a Jubilee as time of total forgiveness of debts, rather a time to redeem debts with payments in kind, often crops.

The jubilee idea as is tossed around loosely today is moral hazard to the nth degree and would reward reckless borrowers and big-time debtors, while stiffing good and hard responsible individuals who played by the rules and lived within their means.

In such a scenario the big winners are the wealthy and powerful elite who would manipulate the process to attain favored status in any outcome– not that they would permit a jubilee in first place.

The history of debt jubilees is old, from the time when money was gold. The need for debt jubilees then did come from failure to follow the Bible, that stated that interest should not be taken. Whatever religious motifs, with gold as money there is a pretty much a fixed amount of money. Now, interest increase the amount of money, and after some years the amount of money on the books got much larger than the amount of gold. This made the monetary system grind to a halt.

Today, with fiat money there is no problem with discrepancy between the amount of money on the books and circulating. The distortion today is the size of financial economy vs. the part of the economy that produces physical goods. The problem, there is a limit on with how much the real economy can be taxed with interest before it grinds to a halt.

As for natural consequences, why should any bank or finance company be too big to fail? The bail out of banks and finance is what really distort the system. If a small change was done to bankruptcy laws no bank would be too big to fail. Start to treat loans issued by a bank like shares issued by the bank in a bankruptcy and have the owner of the collateral keep the collateral if the bank goes bust. Then no bank is too big to fail.

Go back to buying houses with 20% down will show real value of housing

@Ron

As opposed to all cash buyer in the form of investment companies?

Make them take on debt?

?

Is it really theft if the debt jubilee is simply unwinding a giant ponzi scheme a la Madoff? I would argue it is not theft because that’s exactly what they did with the Madoff ponzi.

Wolf, clicked on Uber app today. Uber Premium, which is like black towncar, is $30. Regular Uber $46.

I saw a Twitter post last week from a guy in New York. He was quoted 200 plus for a ride from downtown Manhattan to JFK ;) He was going to fly to California. He said the ride cost him as much as his plane ticket.

I think both Uber and Lyft are hurting for drivers.

Because the Uber/Lyft models were never sustainable. They’re the type of businesses that only exist in an environment where yield-starved “investors” are willing to dump billions into dreams, hoping that some day they pay off.

The problem is that people aren’t willing to pay for the rides what Uber/Lyft actually need to charge to both be profitable for the companies and pay drivers well enough that they don’t quit after a few months. So instead, the companies subsidize rides with investor cash, and pay the drivers crap until they realize that they are making very little when you account for the wear and tear on the car and quit.

All along, Uber and Lyft claimed that they just needed to scale up. But this isn’t like an Amazon warehouse; there are no economies of scale. If the company loses money on a ride, providing 1 million rides loses money too.

Frankly, it’s amazing to me that these businesses have held on as long as they have.

When I ran a copper water tube manufacturing plant in Connecticut decades ago, we used to sell 3/4″ water tube at a slight loss. But we sold millions of pounds of it in high volumes since the sales guys could easily unload it. We couldn’t last as long as Uber will.

Oh, the vast majority of copper water tube (all diameters) is now made outside of the U.S.

Anthony, but what was your end game? Were you trying to sell other items, at a high margin, to customers already buying those water tubes?

Grocery stores are known for loss leaders, but that model actually works, as people do impulse purchase other things when they go in for milk or eggs.

RYN, yes we had higher value tubing products and several alloys of them (bronze, nickel, brass, etc). But the smaller quantities sold of those higher margin products did not “eventually” offset the loss leader water tube sales.

As soon as a downturn in the marketplace came for industry and construction, we died from the losses of the commercial grades of water tubing. The plant I ran eventually was closed as rising wages couldn’t be offset by raising prices, and so were the competitor copper tubing plants that had the same product mix and wage scales.

We didn’t have to export the technology of making water tube, it was easily copied and done on much more efficient machinery overseas.

My old company also “missed the boat” in the 1970’s on developing PVC tubing which eventually replaced copper on the drainage (non-pressurized) side. We also lost the copper penny contract with the U.S. mint when our senior management didn’t want to enter into the metal cladding market.

And then there was Harrison Radiator which used copper condenser tubing and copper fin stock they bought from us to use in the manufacture of millions of radiators for cars. Once Harrison and the industry switched to aluminum stock for radiators (made by competitors), we were history.

There are lots of stories like this in the U.S. One thing for sure, you can’t survive very long by selling a product you are losing money on by “trying to make it up on larger volume”. Maybe I’m wrong here with the NEW ECONOMY!

You are preaching to the choir, brother. Not just ride sharing. Food delivery is another scam. But hei we do live in the United Scams and Slaves of America.

One of my most vivid memories of being in the car business was when a dealer told me that I didn’t understand the automobile business because I questioned his “lose money on each one but make it up on volume” business strategy.

He claimed he’d make it up on the used cars (he over-allowed so… nope. Didn’t work there.) and service volume (customers drove 100 miles to his store in Wood River, IL to buy the car and had it serviced locally).

He was out of business in 18 months.

That’s where the old line came from:

How do you make a million dollars in the car business?

Start with $10M……

@Anthony:

I’m thinking that MMT is also a “sell product you’re losing money on and making it up on volume” scheme.

Whenever the government prints up extra money to paper over the media-hyped “crisis” of the moment, it looks like free money, BUT… there’s the deferred perpetual cost of servicing the new debt, as well as the hidden cost in devaluation of everyone’s purchasing power (except the recipients of the new money), and then the resulting destruction of value in fraying society between the solvent taxpayers and the MMT giftees.

MMT (and printed “fiat” money generally) is a hidden curse sold as a blessing. The greatest Trojan Horse in history wasn’t built by the ancient greeks, but by the modern fiat currency gurus…

Money seems so easy for some.

timbers,

We have bankruptcy laws that take care of debts that cannot be repaid. It works.

The whole idea of “debt jubilee” is being propagated by people who are brain-dead and ignorant and who don’t even know that one person’s debt is another person’s asset, such as deposits in the in the bank (such as your money in your bank account — asset for you, debt for the bank!). If you do a debt jubilee, forget about buying groceries. Your checking account would be jubileed into a vacuum. The economy as we know it ends. I’m getting really tired of reading this idiotic brain-dead debt jubilee BS here.

Wolf, I don’t quite get the part about “If you do a debt jubilee, forget about buying groceries”

Will all the farmers and food distributors in the country suddenly vaporize if a lot of wealthy people suddenly lose a lot of their money?

How does that work?

Exactly. Debt jubilee is about ridding humanity of funny money and returning to a condition where food is exchanged for work, or something equally valuable, that cannot be conjured out of thin air. It marks the end of financial gamesmanship, and the corruption of the monetary system engineered by the powerful and rich against the average Joe and Jane over many generations. I can imagine that debt jubilees of ancient days were the mark of a similar housecleaning, perhaps when complicated records and maths caught up with reality and simply could not be maintained any longer with even a hint of fairness.

I think we need to know the context first. Who has been advocating for a debt jubilee and what do they mean by it?

When I hear the term “debt jubilee”, I think of the way professor Steve Keen explained it. The way Keen defines a jubilee, it works exactly like the economic stimulus payment, except that if you have debts you are “required” to pay down your debt first, before spending the stimulus. If you don’t have any debts, you can do whatever you want with the stimulus.

It sounds to me like timbers, Paulo, and Wolf are talking about a different version of the debt jubilee.

Ortho,

And where will the money come from for that stimulus in the first place? Isn’t that borrowed? So the proposal is to create more debt to pay off existing debt?

Sorry, sounds like I am living in a bizarro world.

@OI

Being serious for a moment. Bankruptcy court is the way to go through this. Otherwise what is being described is just another form of giveaway with the entire idea of financial responsibility being tossed out the window.

Yes, well aware that there are various rules being bent and broken by the rich and such all the time. The government since 2000 has behaved irresponsibly and one could argue fostered a culture of such irresponsibility. Think about people who fomented and propagated the great financial crisis and whatever this is today, when they aren’t held accountable, it sends a message.

But there are reasons for rules, if we don’t, then all we get is anarchy. If financial responsibility is tossed out, what’s next? Look what happened when banking rules got lifted, now rules around pharma are getting loosened, and so on. A debt jubilee is just another way of promoting chaos and irresponsible behavior with a belief hey, that happened once, why can’t it happen again? (Think Reagan’s immigration amnesty that went without following up on real enforcement)

Ending the seriousness quotient, on the other hand, it’s no fun being the only one in the asylum who is sane.

?

Ralph Hiesey,

“Will all the farmers and food distributors in the country suddenly vaporize if a lot of wealthy people suddenly lose a lot of their money?”

There won’t be ANY transactions because there won’t be bank accounts (your asset is the bank’s debt and it will be wiped out in a debt jubilee). And there won’t be transportation because no one can pay for fuel because the payment system won’t work because all bank accounts have been vaporized by the jubilee. You can still barter, but the supply chains are not set up for bartering. Farmers will sit on their bushels of corn and soybean with no place to go.

We are undergoing a government mandated “debt jubilee” right now. If inflation is 8%, your debts devalue by 8% per year. In a decade or so, your debts are practically gone, if your wages and repayment ability increases with inflation.

If you by a long-term treasury, you can help fund that debt jubilee, for benefit of people who need iPhones and Teslas.

Nacho Libre and MCH,

Steve Keen’s idea is to reduce the private sector debt because that’s slowing down the economy. Think of how fast the economy would grow if we drastically reduced all the mortgages, student loans, credit card debts, etc. Steve Keen says don’t worry about the responsible people who didn’t borrow because they’ll get a cash payment instead. If I remember correctly, I don’t think the government debts is a big deal to Keen, because they can print money, so there is nothing to worry about there.

The thing about Steve Keen’s solution is that it gives people what they want. In essence, we are already doing it with the stimulus payments, except that people are voluntarily using it to pay down debt, while Keen defines a jubilee as a stimulus payment where you are forced to pay down any debts you have before buying more Chinese imports.

For those who advocate bankruptcy and other deflationary solutions, the best bet is to hope that CPI inflation is not transitory because that can be used as an argument not to do more stimulus packages with lots of handouts to everyone. But in only two weeks, the first wave of large states including Texas and Florida will stop the unemployment bonuses early.

I think there are eventually going to be more calls for stimulus. Steve Keen’s debt jubilee is actually a better form of stimulus compared to what we did over the last year, if you only you guys would open your minds.

There was a debt jubilee in Germany after WWII. No one had any money and the US issued everyone currency.

“The Deutsche Mark was officially introduced on Sunday, June 20, 1948 by Ludwig Erhard. The old Reichsmark and Rentenmark were exchanged for the new currency at a rate of DM 1 = RM 1 for the essential currency such as wages, payment of rents etc., and DM 1 = RM 10 for the remainder in private non-bank credit balances, with half frozen.[clarification needed] Large amounts were exchanged for RM 10 to 65 Pfennig. In addition, each person received a per capita allowance of DM 60 in two parts, the first being DM 40 and the second DM 20.” Wikipedia

Of course in those days, Germans did not hold mortgages.

This jubilation was done and no one starves. Still I would not recommend doing a complete debt reset. Fun is not the word for it.

You could pretty much claim the abode that you were living in and build a new home on any demolished property. Squatter’s rights.

NotMe,

That wasn’t a “debt jubilee.” That was the total destruction and total bankruptcy of a nation. You do not want that for the US — unless you’re the total enemy of the US. Making those comparisons is beyond brain-dead. People need to think before they post this kind of crap, sheesh!!

Wolf,

let’s not be too close minded to the idea. After all, we need to promote fairness and equity in our society. To support those who may have been… what’s the word… systematically oppressed.

So, may be let’s think about it. It’s not fair to call people brain dead and ignorant just because the idea is radical. Heck, sailing around the world was once a radical idea.

But first, let me go take out a few million in loans and buy some gold bars with it. Once that’s done. Debt jubilee away.

Remember, sometimes, when the world is going crazy, it’s no fun just to be a spectator, it’s time to join in.

Even paper money itself is a ‘Federal Reserve Note’, i.e. if we cancel all debts then that includes all Treasury bonds, T-bills, and all paper money, as they are all in theory a debt that the government or the Fed owes after by creating an instrument of debt.

This is basically a default on $28 trillion of national debt plus all US paper money, and much more. That would instantly kill the world economy.

The truly scary thing is that US hyperinflation would give more or less the same results as a default, except that it would happen a percentage point at a time. This continues until there are so many zeroes on the paper money that people start clogging the toilets when they use it as toilet paper.

This actually happened in Zimbabwe – the Republic of South Africa had to paint signs saying ‘No Zim Dollars’ on the public toilets near the border crossings. Plumbers are more expensive than paint.

That’s pretty much exactly what I said in my comment above which is “awaiting moderation” for some unknown reason.

Agree that bankruptcy works and should be used. The problem with student loans is the bankruptcy laws changed in 2005. The law made the debt nondischargeable. Look at pre-2005 and post 2005. The rate of change on this type of debt post 2005 is staggering.

Making the debt nondischargeable gave unscrupulous lenders and actors the ability to create “for profit” schools with no real use. Gave lenders the ability to indiscriminately lend without any sort of risk metrics behind the loans. They could just repackage the loan into a cdo. It pushed up the cost of colleges because when you flood an industry with too much money, it will inevitably increase the price of that good. This became a feedback mechanism that created more debt and more price increases.

A debt jubilee for student loans will just bail out those lenders that shouldn’t have made the loan in the first place. Just make the debt dischargable again. Watch how fast the price of colleges will drop and how fast the the student loan debt bubble will pop.

At least part of the trouble started when governments believed it when the banks said they were “too big too fail” and bailed them out. Instead of looking at the bankruptcy law and change what made the banks “too big to fail”.

Changing the law and treat loans issued by a bank like stock issued by a bank in a bankruptcy would be a start. With the collateral going to the lender. Then add regulations and mechanism to keep the settlement and money transfer part of the banks running in a transition period and no bank would be to big to fail.

Wolf,

I would argue that bankruptcy in this country doesn’t work because you need money to access the process. Someone broke and in a big financial hole has no access to that process because if they had the thousands it takes to go bankrupt, they would use it to survive.

The bankruptcy process in America is really a rich man’s game. They do it over and over again and get richer and richer each time. The broke guy stays broke and in debt because the bankruptcy process is a money pit to him.

My brother in law (ex BIL) declared bankruptcy in BC, Canada. He had started up a glass business and found he simply could not compete with the suppliers who also had installation companies. Plus, he was one of those guys who always thought he knew more than who he worked for. To make a long story short, he shafted his father in law for about 20K, walked away from tons of CC debt and a bank startup loan, but paid off a friend he had borrowed another 20K from. He did this by taking on a huge apartment paper route every morning before work. He made an extra $600 per month, and used it to pay off his buddy over 4 years. He walked away from everything else and had no credit for 7 years from what I understand. None.

He ended up getting together with an old flame who must have had some cash, because he is now a house owner in a very very expensive BC market. He also has a good blue collar job. For him, bankruptcy worked out just fine, but someone else picked up his losses. The father in law lost out, the banks lost out which would include deposit holders and shareholders, and he did not feel very good about the process or result. It wrecked his marriage, or at least hastened the collapse.

It did not cost him anything as he had nothing to lose. He was discharged from Bankruptcy in just a few years. Being a renter at the time his assets were pretty limited, but he regrouped and has rebuilt his life just fine.

I think there is also some responsibility for the creditors to limit his debt access. In hindsight he was going down for several years and yet he kept charging on his CC until it was too late.

Sub prime auto? Send a tow truck and Guido and then sell the car for the creditors. At least there is an asset to seize that the buyer does not really own.

In BC, they can bleed equity out of a house but don’t just toss you out and sell the place if you can make future mortgage payments. If you can’t make payments then normal foreclosure results I suppose.

I went to the biggest Toyota dealer in Seattle today and they couldn’t find a RAV4 for me!!!! And I am the head of the federal reserve of the United States of America!!!! This is outrageous!!!! I won’t stand for it!!! And why would they dream up the RAV4 Prime and not make any of them!! Hahahahahahahah!!!!!!

Ah, the Rahu4 was in Seattle, t’was a few years ago, and now Rahu4 is looking for his Ketu4 at the car dealership, but Ford eclipse raced circles around Nipigon, and Powell is left holding the steering wheel, until his driver Modi shows up to chauffeur him to the G20.

whew, long sentence

Fed chief – Order one from Japan. Easy!

Better yet, just print the d@mn car.

Lets summarize:

less cars are being repossessed ->

less cars to be sold at auctions ->

less inventory of used cars ->

rises in used car prizes.

Stimmies being payed (partly) by current used car buyers.(?)

I just looked this up on Kelly Blue Book:

My 2005 Mustang convertible (base, not GT):

Miles on it – 64,000

Condition – excellent (and it is)

Private party value (sell to anyone) – Average = $9,010

Last year it was valued at $6 K!

NUTS! This is a 17 year old car.

No car is in “excellent” condition if it’s been driven over the curb. Even if it were still in the original wrapper, a vehicle that’s 17 years old is “average” due to material deterioration (rubber components for example). Every car requires reconditioning. Brakes. Tires. Shocks. Worn seat bolsters. Heel pad wear. Rock chips. “DDS” (dents, dings and scratches). At 17 years old, your car likely needs suspension bushings… and probably engine mounts.

KBB is what was known as the “wish book” as in “I wish my car was worth this much”. Dealers use KBB to sell cars to customers (Wow! Such a deal!!! I’m giving this car away!!!! Hurry before I change my mind!!!!) and Black Book to evaluate trade-in values (or the more up to date Manheim online) because those represent the current market. (Manheim is updated daily and BlackBook weekly).

There are people who maintain their cars, do preventative maintenance, and keep up with things like you mention. Not everyone drives it until it stops and trades it in. I suspect Anthony is one of the former, and his car is very likely in Excellent condition.

Correct and thanks Mike. I am an engineer and perfectionist and have restored a classic Vette or two in my 77 years here. My second to last project was a 1971 VW Beetle and it took me two years to bring that back to very nice stock condition. This Mustang has been a year long project of mine and I have a list of work done on it as long as my arm. But El Katz has Superman’s eyes! LOL!!

I was only making a point as to how used car values have increased through my small world view.

@Anthony A:

“A vehicle is deemed in excellent condition by Kelley Blue Book®if it appears brand new, hasn’t had bodywork (including paint), lacks rust, is in perfect mechanical condition, and doesn’t require any repairs whatsoever. The interior is clean, as is the engine, which has no observable flaws or fluid leaks. The engine should also appear to be free of wear and tear. A car in excellent condition has an entire (provable) record of service and a clean title history. According to Kelley Blue Book, “less than 5 percent of all used vehicles fall into this category.”

Condition is subjective….

YuShan,

In general agreement…in some dark way, in these twisted times, every time the Fed is “brave” enough to allow a publicly traded corporation to go BK without hysterically printing up a new billion to bail them out (and necessarily steal more from every dollar saver) it is a “triumph”.

The “jubilee” hucksters/naive fundamentally misunderstand the enormous and enormously complicated interdependencies of debts and savings in the modern world.

You can’t erase one without erasing the other.

And if you try to on a sweeping/national basis, you will trigger the collapse of relationships that physical production relies upon…leading to chaos, famine, hyperinflation, etc.

It is like trying to cure an illness by destroying the patient’s medical records.

Yu shan:

I think university debt does not allow for bankruptcy. Economist Michel Hudson says debt that cannot be paid, will not be paid. Ancient jubilees, I believe, were made to create a ‘clean slate’ when a new ruling regime came to power. The debts forgiven were those to the regime. Commercial debt was not forgiven. Back then that meant small farms would be returned to original farmers who lost their farms due to indebtedness. “There may have been some fighting involved,” Hudson admits.

Yes, university debt is nondischargeable. Bankruptcy in its current form does not work for anyone other than the wealthy. Much like everything else in this nation. It’s insane that multiple commenters have pointed to bankruptcy as something that is a viable option. At this trajectory, future generations will be living in plywood shacks rented from Blackrock while they work for Amazon. All the while moaning about moral hazard and defending oligarchs. Oh well, the majority of this commentariat while be pushing up daisies by the time that happens so what do they care

1) In the last 5 years dealers expanded and opened new fancy franchises, finances by debt.

2) With less capital base , with less owners equity, they cannot afford to purchase 2021/ 22 pickup trucks, that generate higher margin profit. Small cars are garbage, crumbs.

3) Car dealers were forces to buy used cars from Manheim and the public.

4) The crowded momo trade lift used cars prices as well.

5) In mid 2021, dealers cannot afford both old and new, because it’s a new bubble.

6) Dealers consolidation is phase II. The public will say WTF ==> keep your F…junk pickup trucks and your F…bubble to yourself. The subprime virus will infect the rest, including the prime buyers. The car pandemic will deflate the bubble.

7) Prices will 30% in nominal terms, 40% in real terms.

Many of the facilities built with “debt” are loans from the finance arms of the manufacturers. Ford Credit finances dealerships as does TMCC (Toyota), AHFC (Honda) and other captives. Those are rolled up and sold.

The “Taj Mahal’s” were mandated by the manufacturers. Most dealers (even those who purchased existing enterprises) were contractually bound (as part of the letter of intent from the manufacturer / distributor) to bring the facility up to “minimum requirements” and meet their “image” design by a certain date.

Facility credit and floorplan credit (what pays for the new cars) is separate. The factory has a “blank check” from a floorplan institution (up to a credit limit that is part of the “minimum requirements”) to draft new car deliveries. If a dealer fails to maintain a floorplan – and shuts it down for 45 days – they can be terminated for breach of contract.

Dealers aren’t “forced” to buy cars from Manheim. The used car business is more lucrative (in most cases) than new. The margins on new cars have been declining for decades and replaced with “reimbursements” such as “holdback” and “floorplan assistance” and other alphabet soup below the line reimbursements. In other words, the car you bought at “invoice”, isn’t what the dealer ultimately pays for the vehicle. They pay less. Far less.

Dealerships don’t make a dime unless they sell something. So, with new car supplies reduced (no chips), they turn to used. More demand for used, price goes up. Not rocket science.

Many public company dealerships (Autonation, Lithia, etc., ) own most of their inventory outright. They also maintain floorplans for both new and used (new is required – used is a “pressure relief valve” to buffer cash flow).

Prime buyers will still buy. They have to as many of them lease (some non-luxury brands exceed 50% lease penetration) and the lease term dictates their re-entry into the market.

Dealerships are a lot more consolidated than you think. Lithia owns nearly 200 stores alone (@180). David Wilson Auto Group has multiple dealerships but they don’t smear his name all over the building – it just is marketed as if it were an independently owned store. Manufacturers have a “right of first refusal” built into their franchise agreements. If a dealership is going down, the manufacturer can (and will) step in and buy it (subject to state laws) if it is important enough to their sales volume/service network.

Mucho spot on synopsis.

Note: Ma&Pa (local) stores are selling out [to mega groups] while the ‘getting is good.

On the HD truck side, large equipment dealers are picking up truck dealerships

(ref Peterson).

Owner of twelve (diverse) stores conveyed that the real profit is realized on the second ‘flip’ of a trade-in.

“Owner of twelve (diverse) stores conveyed that the real profit is realized on the second ‘flip’ of a trade-in.”

In the olden days, that was called “wash out gross” where you followed the trail of profit generated from the sale of unit 1 on through all transactions associated with that first sale. Some dealers use the inventory stock number to track it (1234, 1234A, 1234B, etc.).

This is fascinating, thank you for sharing your insider knowledge!

I expect more of the same as what we’ve seen.

Just the mode of operation has changed.

UBI/helicopter money, rather than QE, brought into vogue by needing to support during the pandemic response.

Throw in a sprinkle of build back better/green/equality.

If everyone knew the impact of QE they’d have front run it.

Now everyone is trying to front run the new mode of operation, assuming inflation, and stocks booming in value again.

They may be right, but it could be a big hit to the markets first, then a short deflation, then the UBI will really kick in.

Of course the FED has great power now but once they have the digital accounts and bypass the banks for stimulus directly to the little people they basically will have absolute power. Time limit to spend stimulus to increase money velocity? Different stimulus for different favored groups? Not following the approved narrative? No stimulus for you. Absolute power corrupts.

I’m hoping it will not happen but I’m not so sure.

Oh I almost forgot: destroy the debt by paying it off during the economic recovery.

Easy to forget because it’s not gonna happen.

Housing bubble burst coming within a year, maybe 6 months.

“Housing bubble burst coming within a year, maybe 6 months.”

I hope so. Schadenfreude, I admit. Drive those out-of-staters back to where they came from, or at least keep more from coming. Worked during the ‘Great Recession.’ Fingers crossed…

I don’t want to take this thread off into housing, but I hope it comes up again soon in a new blog post.

Good article. Comments so so because most people don’t get it. As Winston said earlier in the chain watch or read “The Big Short. Most all questions would be answered. Last evening I attended a roll out meeting for a local candidate for CC in our community. The conversations covered a magnitude of topics but when came to most areas that involved knowledge of the state of financial discourse that we are now stuck in most are totally cluless ????

Wolf, why does the article header say 83 comments posted when I can only count 46?

Because one comment hijacked the entire comment section, and it got way out of hand, and so I deleted that one comment which took down all the comments in reply to it, four niches deep, including all my own comments in reply to it.

Wow! Thanks for the explanation.

I cannot answer, because 80% of my comment are deleted.

Micheal Engel,

I deleted the one comment that had hijacked the comment section, and that one comment when it went down, took with it all the comments in reply to it, four niches deep, including all my own comments in reply to it.

No offense, but your comments are the only ones on this site that I ignore routinely and without hesitation, because they are gibberish.

Wolf – You should do an article on rental car rates. They are through the roof right now.

I might cover that during my next inflation article. There are other services that are through the roof too.

The million dollar question is when will the Government and the Fed finally admit they are the cause of all this and reverse their policies.

It seems as if everyone already knows, so who do they think they are still fooling?

“when will the Government and the Fed finally admit they are the cause of all this and reverse their policies.”

Both had more than 100 years to admit and they never did, why would they do it now? In that duration the duo created multiple bubbles and busts – much longer and deeper than the time before the Fed was created.

They would never admit the mistake. You are also overestimating the number of people who are aware of their little game.

This is different.. First they make it so people cannot afford a roof over their head, now they cannot afford a used car. The cost of beef is up 30%. How low does the standard of living have to drop before people get off their lazy asses and threaten to hang their Congressman / Senator?

Most households have owned a house and car for a while, so they are FAVORABLY impacted by the recent price increases. The people without any assets are hurting, but they are a clear minority. They don’t have enough political power to do much about it.

Arguably, the economy would collapse if people had to buy major assets such as a home and car at today’s prices. Most people I talk to in Seattle say they couldn’t afford to buy the house they are living in. They bought their houses a long time ago at much lower prices.

It will be interesting to see who will buy homes going forward. In Seattle and suburbs, an average house goes for $600k to $800k, and not many people can afford that. That’s 10x gross income for most folks.

How is this different? Is it because you started noticing it now?

Increasing number of people have been priced out of assets for past few decades. Fed, with its policies has continuously blown asset bubbles and has devalued dollar.

Just because only now you are feeling the heat doesn’t mean the fire hasn’t been going on for a long time.

That house they own now has much higher property taxes and insurance because of re-assessed property value. That car now has much higher registration and use tax because of its higher value. Inflation gets everyone not just a few…

There is no accountability at the top of our government. If so, many in office would have been fired or even jailed over the years. Instead, one may even be praised or given a Noble Peace Prize. Those in charge will just enact a new law or policy and move away from the one that is giving them heartburn.

Washington DC is an ass clown circus. None of the people there have any practice experience in economics or anything else, with the exception of lying. They are expert liars nothing else.

They have screwed the American people and sold them out for bribes and their lavish lifestyles.

Every city in the country now is looking at establishing tent cities, something we have not seen since the depression of the 1930’s because the governments failed policies have made it impossible for the lower tiers of the working class to survive in most places. The politicians are criminals, and the American people need to wake the F up and realize that.

Tent cities have recently been outlawed in Texas. Police are now authorized to arrest all homeless people and put them in jail.

Ironically, when a homeless person gets out of jail, he is still homeless and can be immediately arrested again. It’s like the circle of life.

During the Depression in CA the right to arrest homeless at will were called “vagrancy laws” and usually up to the discretion of the local sheriff and large landowners. They’d let people camp out if there was fruit to be picked, then tell them to move on. Needless to say, under this situation, pay was not negotiable.

Steinbeck wrote a lot about it in his books and for his SF paper (the Examiner?)

Insofar as the bought and paid for federal government has waded into state and local governments by overstepping the constitution then yes, you can blame politicians. Consider that locally you get the government you vote for. I’d argue local policy has a larger impact on your day to day life than any federal yahoo. Thankfully, you can still choose where you want to live and how you want to vote, even if it’s in a tent down by the river.

If I can get another stemmie I will sign an affidavit that I will not go on buyers strike. As a patriot I must do my duty by consuming.

Interesting article and comments. A micro foundation dive that I found instructive. Yet the cure remains the same. Tax away wealth from the top, raise wages from below. “Build back better is more than a slogan,” IMO.

Reading the future is a waste of time.

5 years ago I was convinced these sub-prime auto loans would be the next big bust after sub-prime mortgages.

I thought they would get super creamed, but what the Hell, sleepy Joe comes along and sprinkles ‘fairy dust’ on them.

Does anything ever lose money in USA?