OK, it’s getting a little crazy: Massive shifts due to working from anywhere and the Pandemic. But some of those shifts started well before the Pandemic.

By Wolf Richter for WOLF STREET.

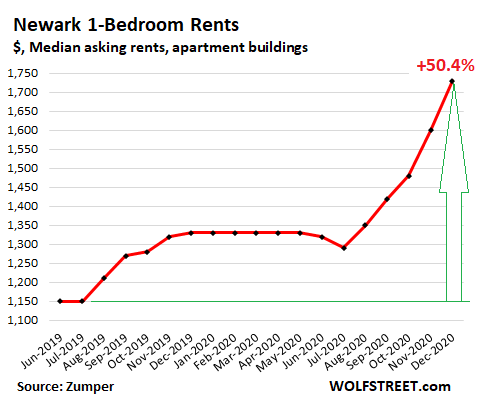

In the exodus cities, rents continued plunging in December. For example, in San Francisco, the median asking rent for one-bedroom apartments fell 1.5% from November and is now down 28% from June 2019; in New York City and in Seattle, rents fell about 2.5% for the month and are down 21% from July 2019. But in Newark, where some New York apartment dwellers that are working from anywhere have fled to, rents have skyrocketed by 50% since July 2019. Newark?!?

Yup, in Newark, the median asking rent for one-bedroom apartments in December jumped by 8.1% from November, and is up by 30% from a year ago, and by 50% from June 2019. This surge in rents has catapulted Newark into the rarefied air of the 9th most expensive major rental market in the US, up from 40th place in June 2019 (more in a moment on those expensive rental markets that are dominated by big double-digit decliners):

Rents are depicting the massive shifts playing out in the US housing market, brought about by the Pandemic and by working from anywhere and perhaps by a general urge to rethink things.

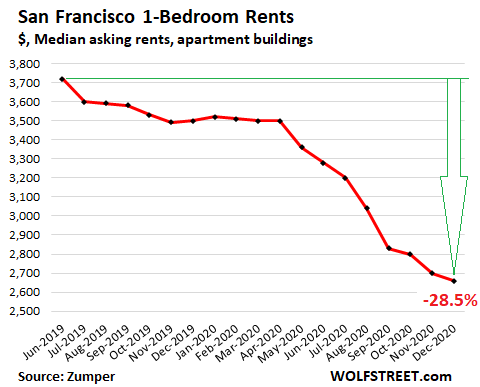

San Francisco rents in breath-taking downward spiral.

San Francisco remains the most expensive rental market in the US only because rents are also plunging in New York City. The median asking rent in December for 1-BR apartments dropped another 1.5% from November, and by 24% year-over-year, and by 28.5% from June 2019, to $2,660, according to data from Zumper’s Rent Report. In terms of dollars, the drop since June 2019 amounted to $1,060 a month.

This does not include the widely advertised incentives of “two months free,” or getting popular, “three months free,” which cut effective rents for the first year by an additional slice:

For 2-BR apartments in San Francisco, the median asking rent dropped by 2.0% in December from November, and by 22% year-over-year, to $3,500. Since June 2019, it has plunged by 27%, or by $1,300 a month, not including the incentives.

These are median asking rents in apartment buildings, including apartment towers. There are now reports of vacancy rates of 30% in luxury apartment towers in San Francisco, with landlords advertising “three months free.”

“Asking rent” is the advertised rent of a rental apartment, but does not include concessions, such as two months free. “Median” asking rent is the middle asking rent, with half of the asking rents higher and half lower.

Zumper collects this data from the Multiple Listings Service (MLS) and other listings, including its own listings, in the 100 largest markets of the US. These are rentals in apartment buildings, including new construction, but do not include single-family houses for rent and condos for rent.

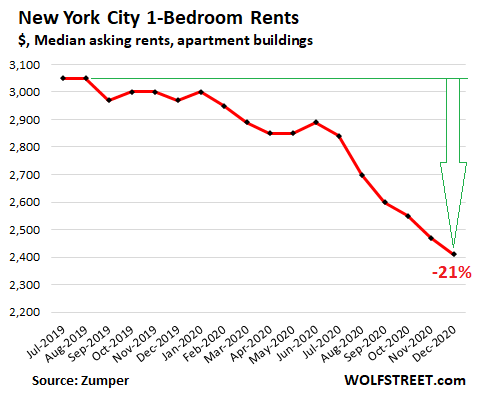

New York City rents plunged.

The median asking rent for 1-BR apartments in New York City in December fell by 2.4% from November, and by 19.7% year-over-year, to $2,410, according to Zumper data. Since July 2019, the median 1-BR rent has plunged by 21%:

New York City’s 2-BR rents plunged 6.1% in December from November, by 22.4% year-over-year, and by 25% since October 2019, to $2,630. There are now reports of soaring vacancy rates even at the very high end, in iconic apartment towers in the center of Manhattan, such as the “New York by Gehry” 76-story tower with nearly 900 apartments, where vacancy rates jumped to nearly 30%.

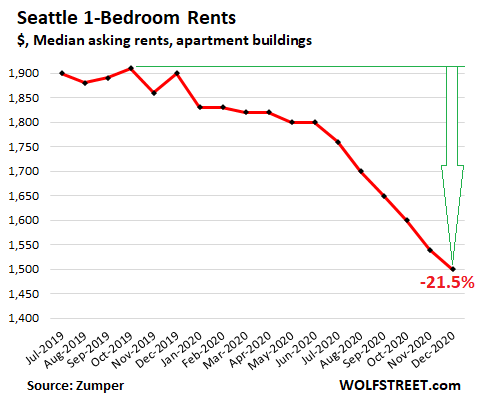

Seattle rents plunged.

In December, the median asking rent for 1-BR apartments in Seattle dropped by 2.6% from November, by 20.6% year-over-year, by 21.5% since October 2019, and by 25% since the peak in May 2018, to $1,500:

The charts above show that the trends in rents started in 2019, well before the Pandemic, but that the Pandemic lit a fire under those trends.

These are rents in apartment buildings, including apartment towers. They reflect the pressures on rents from two directions: The exodus from certain big cities with ridiculously high rents, which had started before the Pandemic, and the exodus from apartment towers given the virus transmission risks in potentially crowded environments, such as elevators. And that exodus has headed to apartments in cheaper areas, such as Newark, and to single-family houses, for sale and for rent, further afield, that no market was prepared for.

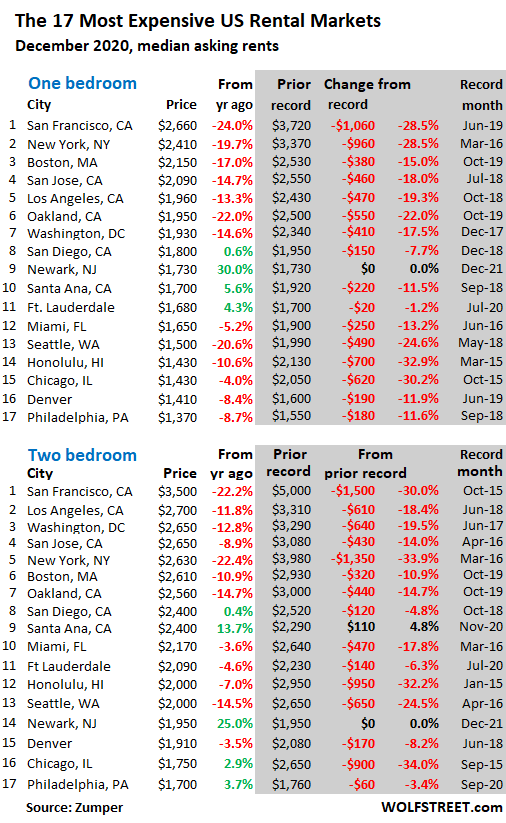

The 17 most expensive rental markets.

The new arrival in the table below of the most expensive major rental markets by median asking rents: Newark, NJ, with a year-over-year jump of 30% for 1-BR rents and a jump of 25% for 2-BR rents.

The shaded area shows peak rent and the changes from peak rent. The black entries in the shaded area indicate rent records set in December. Of the 17 markets, 14 booked double-digit drops in 1-BR rents from their respective peaks in prior years, with Honolulu topping out at -32.9%, followed by Chicago at -30.2%, and San Francisco at -28.5%!

The 24 cities with the Cheapest 1-BR rents:

These are the low-cost rental markets, where the median 1-BR asking rents range from $580 in Akron, OH, to $860 in Detroit. In some cities, rents are dropping, such as in Akron (-6.5% year-over-year). But in many cities at the cheap end, rents are rising, and in a few, rents are soaring, particularly in Tucson (+13.4%) and Detroit (+19.4%), whose downtown has been revitalizing for a decade:

| The 24 Cities with lowest 1-BR rents, $ & Y/Y% | |||

| 1 | Akron, OH | $580 | -6.5% |

| 2 | Wichita, KS | $640 | -4.5% |

| 3 | Lubbock, TX | $650 | 0.0% |

| 4 | Shreveport, LA | $660 | 1.5% |

| 5 | Tulsa, OK | $660 | 3.1% |

| 6 | Laredo, TX | $690 | -2.8% |

| 7 | El Paso, TX | $700 | 4.5% |

| 8 | Lexington, KY | $740 | 1.4% |

| 9 | Oklahoma City, OK | $760 | 0.0% |

| 10 | Tucson, AZ | $760 | 13.4% |

| 11 | Albuquerque, NM | $780 | 11.4% |

| 12 | Lincoln, NE | $780 | -3.7% |

| 13 | Augusta, GA | $800 | 6.7% |

| 14 | Baton Rouge, LA | $800 | 5.3% |

| 15 | Greensboro, NC | $800 | 11.1% |

| 16 | Tallahassee, FL | $800 | -3.6% |

| 17 | Bakersfield, CA | $810 | 0.0% |

| 18 | Omaha, NE | $810 | 1.3% |

| 19 | Winston Salem, NC | $810 | 1.3% |

| 20 | Memphis, TN | $830 | 7.8% |

| 21 | Syracuse, NY | $830 | 2.5% |

| 22 | Columbus, OH | $850 | 6.3% |

| 23 | Knoxville, TN | $850 | 4.9% |

| 24 | Detroit, MI | $860 | 19.4% |

The 26 Cities where 1-BR rents dropped.

In December, the median asking rent for 1-BR apartments fell year-over-year in 26 of the largest rental markets. In 19 of them, rents fell by 5% or more. In 11 of them, rents fell by the double digits, all but one of them the usual suspects on the list of the 17 Most Expensive Rental Markets. But rents also dropped in some of the cheapest rental markets, such as Akron, OH; Tallahassee, FL; Wichita, KS; and Laredo, TX:

| The 26 Cities where 1-BR rents dropped YoY | |||

| 1 | San Francisco, CA | $2,660 | -24.0% |

| 2 | Oakland, CA | $1,950 | -22.0% |

| 3 | Seattle, WA | $1,500 | -20.6% |

| 4 | New York, NY | $2,410 | -19.7% |

| 5 | Boston, MA | $2,150 | -17.0% |

| 6 | San Jose, CA | $2,090 | -14.7% |

| 7 | Washington, DC | $1,930 | -14.6% |

| 8 | Los Angeles, CA | $1,960 | -13.3% |

| 9 | Salt Lake City, UT | $1,000 | -13.0% |

| 10 | Pittsburgh, PA | $1,080 | -10.7% |

| 11 | Honolulu, HI | $1,430 | -10.6% |

| 12 | Nashville, TN | $1,250 | -9.4% |

| 13 | Buffalo, NY | $1,040 | -8.8% |

| 14 | Philadelphia, PA | $1,370 | -8.7% |

| 15 | Minneapolis, MN | $1,270 | -8.6% |

| 16 | Denver, CO | $1,410 | -8.4% |

| 17 | Akron, OH | $580 | -6.5% |

| 18 | Miami, FL | $1,650 | -5.2% |

| 19 | Madison, WI | $1,090 | -5.2% |

| 20 | Irving, TX | $1,040 | -4.6% |

| 21 | Wichita, KS | $640 | -4.5% |

| 22 | Chicago, IL | $1,430 | -4.0% |

| 23 | Lincoln, NE | $780 | -3.7% |

| 24 | Tallahassee, FL | $800 | -3.6% |

| 25 | Orlando, FL | $1,220 | -3.2% |

| 26 | Laredo, TX | $690 | -2.8% |

The 32 Cities where rents jumped between 6% and 30% YoY.

In December, the median 1-BR asking rent increased year-over-year in 68 of the 100 largest rental markets. In six markets, there was no change.

In 32 of these markets, rents jumped by 6% or more. In 19 of them, rents jumped between 10% and 30%, including five markets with year-over-year rent increases over 20%. Some of them, formerly among the cheapest markets, have been storming up the scale:

| The 32 Cities where 1-BR rents jumped 6%-30%, YoY | |||

| 1 | Newark, NJ | $1,730 | 30.1% |

| 2 | St Petersburg, FL | $1,270 | 25.7% |

| 3 | Cleveland, OH | $1,180 | 25.5% |

| 4 | Indianapolis, IN | $1,000 | 22.0% |

| 5 | St Louis, MO | $1,000 | 22.0% |

| 6 | Detroit, MI | $860 | 19.4% |

| 7 | Virginia Beach, VA | $1,190 | 19.0% |

| 8 | Fresno, CA | $1,160 | 17.2% |

| 9 | Spokane, WA | $890 | 17.1% |

| 10 | Richmond, VA | $1,300 | 16.1% |

| 11 | Chattanooga, TN | $1,030 | 14.4% |

| 12 | Providence, RI | $1,530 | 14.2% |

| 13 | Tucson, AZ | $760 | 13.4% |

| 14 | Boise, ID | $1,130 | 13.0% |

| 15 | Henderson, NV | $1,270 | 11.4% |

| 16 | Albuquerque, NM | $780 | 11.4% |

| 17 | Greensboro, NC | $800 | 11.1% |

| 18 | Sacramento, CA | $1,430 | 10.9% |

| 19 | Norfolk, VA | $1,020 | 10.9% |

| 20 | Rochester, NY | $1,020 | 9.7% |

| 21 | Chandler, AZ | $1,320 | 9.1% |

| 22 | Las Vegas, NV | $1,030 | 8.4% |

| 23 | Mesa, AZ | $970 | 7.8% |

| 24 | Memphis, TN | $830 | 7.8% |

| 25 | Gilbert, AZ | $1,330 | 7.3% |

| 26 | Corpus Christi, TX | $880 | 7.3% |

| 27 | Colorado Springs, CO | $1,070 | 7.0% |

| 28 | Durham, NC | $1,090 | 6.9% |

| 29 | Jacksonville, FL | $960 | 6.7% |

| 30 | Augusta, GA | $800 | 6.7% |

| 31 | Columbus, OH | $850 | 6.3% |

| 32 | Louisville, KY | $880 | 6.0% |

The Largest 100 rental markets.

Below are the top 100 rental markets, with 1-BR and 2-BR median asking rents in December, and year-over-year percent changes, in order of 1-BR rents. You can search the list via the search function in your browser. If your smartphone clips the 6-column table on the right, hold your device in landscape position:

| Rents, Top 100 Cities | 1-BR $ | Y/Y % | 2-BR $ | Y/Y % | |

| 1 | San Francisco, CA | $2,660 | -24.0% | $3,500 | -22.2% |

| 2 | New York, NY | $2,410 | -19.7% | $2,630 | -22.4% |

| 3 | Boston, MA | $2,150 | -17.0% | $2,610 | -10.9% |

| 4 | San Jose, CA | $2,090 | -14.7% | $2,650 | -8.9% |

| 5 | Los Angeles, CA | $1,960 | -13.3% | $2,700 | -11.8% |

| 6 | Oakland, CA | $1,950 | -22.0% | $2,560 | -14.7% |

| 7 | Washington, DC | $1,930 | -14.6% | $2,650 | -12.8% |

| 8 | San Diego, CA | $1,800 | 0.6% | $2,400 | 0.4% |

| 9 | Newark, NJ | $1,730 | 30.1% | $1,950 | 25.0% |

| 10 | Santa Ana, CA | $1,700 | 5.6% | $2,400 | 13.7% |

| 11 | Fort Lauderdale, FL | $1,680 | 4.3% | $2,090 | -4.6% |

| 12 | Anaheim, CA | $1,660 | 1.2% | $1,990 | -1.0% |

| 13 | Miami, FL | $1,650 | -5.2% | $2,170 | -3.6% |

| 14 | Long Beach, CA | $1,600 | 0.0% | $2,090 | 4.5% |

| 15 | Providence, RI | $1,530 | 14.2% | $1,880 | 17.5% |

| 16 | Scottsdale, AZ | $1,520 | 2.0% | $2,020 | -3.8% |

| 17 | Seattle, WA | $1,500 | -20.6% | $2,000 | -14.5% |

| 18 | New Orleans, LA | $1,460 | 3.5% | $1,690 | 3.7% |

| 19 | Atlanta, GA | $1,430 | 0.7% | $1,870 | 4.5% |

| 20 | Chicago, IL | $1,430 | -4.0% | $1,750 | 2.9% |

| 21 | Sacramento, CA | $1,430 | 10.9% | $1,730 | 18.5% |

| 22 | Honolulu, HI | $1,430 | -10.6% | $2,000 | -7.0% |

| 23 | Denver, CO | $1,410 | -8.4% | $1,910 | -3.5% |

| 24 | Portland, OR | $1,400 | 2.9% | $1,770 | 4.1% |

| 25 | Philadelphia, PA | $1,370 | -8.7% | $1,700 | 3.7% |

| 26 | Gilbert, AZ | $1,330 | 7.3% | $1,580 | 9.0% |

| 27 | Chandler, AZ | $1,320 | 9.1% | $1,530 | 7.0% |

| 28 | Richmond, VA | $1,300 | 16.1% | $1,450 | 6.6% |

| 29 | Henderson, NV | $1,270 | 11.4% | $1,430 | 5.9% |

| 30 | Minneapolis, MN | $1,270 | -8.6% | $1,690 | -6.1% |

| 31 | St Petersburg, FL | $1,270 | 25.7% | $1,720 | 25.5% |

| 32 | Nashville, TN | $1,250 | -9.4% | $1,450 | 3.6% |

| 33 | Austin, TX | $1,230 | 0.0% | $1,520 | 0.0% |

| 34 | Orlando, FL | $1,220 | -3.2% | $1,400 | -2.1% |

| 35 | Dallas, TX | $1,210 | 4.3% | $1,640 | 3.1% |

| 36 | Baltimore, MD | $1,200 | 1.7% | $1,450 | 2.8% |

| 37 | Plano, TX | $1,200 | 0.8% | $1,550 | -3.1% |

| 38 | Charlotte, NC | $1,190 | 2.6% | $1,420 | 10.9% |

| 39 | Virginia Beach, VA | $1,190 | 19.0% | $1,330 | 12.7% |

| 40 | Cleveland, OH | $1,180 | 25.5% | $1,300 | 30.0% |

| 41 | Tampa, FL | $1,180 | 4.4% | $1,410 | 6.0% |

| 42 | Fresno, CA | $1,160 | 17.2% | $1,380 | 15.0% |

| 43 | Milwaukee, WI | $1,140 | 1.8% | $1,320 | 12.8% |

| 44 | Boise, ID | $1,130 | 13.0% | $1,270 | 11.4% |

| 45 | Chesapeake, VA | $1,120 | 2.8% | $1,250 | 3.3% |

| 46 | Aurora, CO | $1,100 | 0.0% | $1,430 | 1.4% |

| 47 | Durham, NC | $1,090 | 6.9% | $1,250 | 10.6% |

| 48 | Madison, WI | $1,090 | -5.2% | $1,390 | 5.3% |

| 49 | Houston, TX | $1,080 | 4.9% | $1,340 | 6.3% |

| 50 | Pittsburgh, PA | $1,080 | -10.7% | $1,300 | -5.8% |

| 51 | Reno, NV | $1,080 | 3.8% | $1,390 | 10.3% |

| 52 | Colorado Springs, CO | $1,070 | 7.0% | $1,350 | 10.7% |

| 53 | Fort Worth, TX | $1,050 | 2.9% | $1,360 | 8.8% |

| 54 | Raleigh, NC | $1,050 | 5.0% | $1,250 | 4.2% |

| 55 | Buffalo, NY | $1,040 | -8.8% | $1,110 | -18.4% |

| 56 | Irving, TX | $1,040 | -4.6% | $1,370 | -3.5% |

| 57 | Chattanooga, TN | $1,030 | 14.4% | $1,180 | 14.6% |

| 58 | Las Vegas, NV | $1,030 | 8.4% | $1,210 | 4.3% |

| 59 | Norfolk, VA | $1,020 | 10.9% | $1,100 | 14.6% |

| 60 | Rochester, NY | $1,020 | 9.7% | $1,210 | 10.0% |

| 61 | Indianapolis, IN | $1,000 | 22.0% | $1,050 | 16.7% |

| 62 | Phoenix, AZ | $1,000 | 2.0% | $1,280 | 3.2% |

| 63 | Salt Lake City, UT | $1,000 | -13.0% | $1,300 | -6.5% |

| 64 | St Louis, MO | $1,000 | 22.0% | $1,260 | 9.6% |

| 65 | Kansas City, MO | $990 | 5.3% | $1,170 | 14.7% |

| 66 | Mesa, AZ | $970 | 7.8% | $1,210 | 9.0% |

| 67 | Jacksonville, FL | $960 | 6.7% | $1,140 | 11.8% |

| 68 | Anchorage, AK | $950 | 5.6% | $1,150 | 4.5% |

| 69 | Cincinnati, OH | $940 | 4.4% | $1,130 | -3.4% |

| 70 | Glendale, AZ | $940 | 1.1% | $1,170 | 10.4% |

| 71 | San Antonio, TX | $930 | 5.7% | $1,150 | 4.5% |

| 72 | Arlington, TX | $900 | 4.7% | $1,180 | 7.3% |

| 73 | Spokane, WA | $890 | 17.1% | $1,100 | 6.8% |

| 74 | Corpus Christi, TX | $880 | 7.3% | $1,130 | 8.7% |

| 75 | Des Moines, IA | $880 | 2.3% | $930 | 3.3% |

| 76 | Louisville, KY | $880 | 6.0% | $940 | 1.1% |

| 77 | Detroit, MI | $860 | 19.4% | $1,030 | 25.6% |

| 78 | Columbus, OH | $850 | 6.3% | $1,090 | 3.8% |

| 79 | Knoxville, TN | $850 | 4.9% | $1,000 | 6.4% |

| 80 | Memphis, TN | $830 | 7.8% | $880 | 8.6% |

| 81 | Syracuse, NY | $830 | 2.5% | $970 | -3.0% |

| 82 | Bakersfield, CA | $810 | 0.0% | $1,060 | 14.0% |

| 83 | Omaha, NE | $810 | 1.3% | $1,040 | 4.0% |

| 84 | Winston Salem, NC | $810 | 1.3% | $880 | 6.0% |

| 85 | Augusta, GA | $800 | 6.7% | $900 | 7.1% |

| 86 | Baton Rouge, LA | $800 | 5.3% | $920 | 4.5% |

| 87 | Greensboro, NC | $800 | 11.1% | $920 | 13.6% |

| 88 | Tallahassee, FL | $800 | -3.6% | $940 | 4.4% |

| 89 | Albuquerque, NM | $780 | 11.4% | $950 | 14.5% |

| 90 | Lincoln, NE | $780 | -3.7% | $920 | 0.0% |

| 91 | Oklahoma City, OK | $760 | 0.0% | $900 | 1.1% |

| 92 | Tucson, AZ | $760 | 13.4% | $1,000 | 14.9% |

| 93 | Lexington, KY | $740 | 1.4% | $920 | -3.2% |

| 94 | El Paso, TX | $700 | 4.5% | $850 | 6.3% |

| 95 | Laredo, TX | $690 | -2.8% | $950 | 0.0% |

| 96 | Shreveport, LA | $660 | 1.5% | $740 | 5.7% |

| 97 | Tulsa, OK | $660 | 3.1% | $830 | 0.0% |

| 98 | Lubbock, TX | $650 | 0.0% | $820 | 2.5% |

| 99 | Wichita, KS | $640 | -4.5% | $730 | 4.3% |

| 100 | Akron, OH | $580 | -6.5% | $730 | 4.3% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

Is there a way to figure out ,if in aggregate ,rents are going down in the USA as a whole? Or are we just seeing them bulge up in one area the same amount they are going down in another, like squeezing on a bag of Jello.

In aggregate, for the top 100 markets, asking rents are up a little YOY, with 1-BR rents up just over 2% and 2-BR rents up less than 1%. But this is not the data used for inflation. CPI uses a whole-market effective rent figure that includes rent control and other stuff.

Was wondering what’s the latest on all those expensive towers by the ballpark and especially the tilting one? Haven’t been down to SF for 3 years or and always take the Larkspur ferry, now. (or is that for another article?).

Sorry, guilty of not fully reading….but I’d still like to know if anything major changed on the tilting one.

The leaning tower of San Francisco is now leaning more than ever. And it got tangled up in complex multi-party lawsuits. I think they’re being, or have been, settled. There is a hugely expensive fix now being planned that won’t straighten the tower but hopefully stop it from leaning much further. The sidewalk around the building needs constant fixing because it keeps cracking. I haven’t been inside, but according to reports, the underground structures, including parking garage, shows the strains on the building, with big cracks in the cement, leaking and bursting pipes, etc. This is such a mess. It’s also so complicated, legally and otherwise, with everyone saying something different, that it gives me a headache just thinking about it. Thank god I don’t own one of those units.

Thanks.

Living in that building and looking in the toilet daily must be an even bigger headache.

Might (eventually) make one narly skateboard ramp .. or an epic movie set .. or maybe both!

Wouldn’t want to be ANYWHERE in the vicinity of IT’S footprint, should say … an 8+ shaker, come calling …

I just read an article on NOLA dot COM about people still not receiving their unemployment benefits. One person quoted said her landlord charges a $25 a day late fee. That’s the kind of predatory behavior which increases rent collections now and later leads to rent control.

Well, if they ain’t gonna pay rent, they ain’t gonna pay the late fee either.

What should the late fee be?

Jeff, I know this is going to shock you, but the late fee should be ZERO in the middle of a PANDEMIC. The fact that you need to be told this instead of figuring it out for yourself is what is destroying America.

It should be a regulated amount, not wholesale robbery.

It will be just another neoliberal (remember that word) monkey trap .. like virtually Every OTHER Big-Fin ferengi scheme, planned .. or in the works!

I’m sorry -annnnd it’s gone … All Gone …………

Rents are dropping fast while housing prices rising fast. This anomaly likely won’t last long.

Perhaps dropping rents are sending a message that housing prices are next.

Amen, albeit I predict that “crazy” is going to be 2021’s theme. This year will be a contest between reality and the “Federal” bankster Reserve’s ability to deceive and manipulate Americans, the world, and the economy to benefit Wall Streeters and banksters.

I love the politeness of so many who tiptoe about the irrational economic conditions that have been created by the “Federal” bankster Reserve’s decisions to covertly funnel the majority of US savers’ and investors’ funds to its banksters and Wall Streeters. It is responsible for the worst, financial abuses ever in real dollar terms but most are afraid to point this out.

For example, because he often reveals truths that the powerful would not like disclosed, I love to sometimes relax and listen at night to a commenter called the “Epic Economist” on Youtube. He has often cited articles from this website.

However, he does not cover the fact that the “Federal” bankster Reserve long ago abandoned its purported goals to focus on bailing out, gifting funds to, and protecting its little banksters and Wall Streeters, while using deception to deceive most Americans and foreign investors. For example, he quoted the “Federal” bankster Reserve’s current leaders as claiming that they have no concern about the real estate market, without much comment on their inconsistent conduct.

How could they have no concerns given their $2 TRILLION in recent bailouts? In 2019 to 2020, not only have they bailed out the banksters in their repo market, but the “Federal” bankster Reserve purchased $2 TRILLION in mortgage-backed securities (“MBS”) from the banksters, which means that they bailed out the banksters (purportedly) in advance from their stupid decisions by purchasing the nearly worthless paper that they were holding and clearly are STILL generating today. I say “nearly worthless paper” because those MBS did not have anywhere near the FMV prices that the “Federal” bankster Reserve paid for them.

It bought them at grossly inflated prices, way above their true FMV, essentially as gifts to the banksters and Wall Streeters who held them. If the banksters had suddenly wanted to sell a significant fraction of this massive amount of MBS paper in 2019 or 2020, since there is a continuing glut of real estate that is overpriced, the FMV sale prices of these MBS would have plunged.

The prices of most real estate would consequently have plunged and might still plunge if massive, covert inflation is not encouraged by the “Fed,” which I opine is the only card that the “Federal” bankster Reserve has left. (I grant that some income-producing real estate (“RE”) with an inherent value from its income production, like farmland or gold mines, might have retained its value, but that is a tiny portion of the total value of RE in the MBS.)

That was coming even before the pandemic because the banks’ real-dollar capital reserves were razor-thin for many years and probably still are now— if most are not already legally insolvent. Once the pandemic started and businesses had to close, the banksters’ “Federal” Reserve gave the banksters an additional $800 billion-plus this year for a total bailout of $2 TRILLION plus by the last part of 2020.

The “Federal” bankster Reserve is now effectively a gigantic “bad bank,” which the banksters have dreamed of and promoted in the EU and USA for decades to take away their bad investments and pay them inflated values for them. What will it do this year when there are so many landlords that will fail to keep or make their mortgages current, ever, because their tenants have defaulted on their rent or closed their businesses or been evicted?

How long will forbearance and extend and pretend work to keep this ticking, economic time bomb from exploding? I think that as the Epic Economist commenter implied, that economic time bomb will likely explode this year. We are seeing the first smoke puffs from what will likely be a gigantic fire.

I am surprised that the real estate prices in Florida’s low-lying cities have not plunged yet: read “Miami Will Be Underwater Soon. Its Drinking Water Could Go First” in Bloomberg.

I suspect most non-journalist types have stopped believing in rising seas climate catastrophes.

Burying one’s head in the sand in this case only means drowning before the surface water gets you; I think that between being overwhelmed by climate change including the impending demise of Miami, the incessant baloney of “nothing to see here, it’s all a plot/lie”, with bonus economic, political, and social unrest is making it hard to respond to impending doom.

TL;DR – The gigantic storm of fecal matter that has engulfed the United States makes it hard to react to anything.

Unfortunately, the Fed and the Federal government will fight that tooth and nail. If it happens widely, expect not just new programs to be spawned to allow houses to be bought regardless of creditworthiness. I think we will also see direct subsidies to the RE and CRE industries to keep them busy (even though CRE is overbuilt and housing units per capita is within 0.5% of its all time high).

None of this will help working Americans, of course, if the last 50 years is any indication.

It’s criminal. Since when was it government’s job to make peoples’ lives as expensive and miserable as possible?

Evern since some monkey bashed another monkey on the head with a stick and called himself King!

1976 I believe. Whenever the Fed received their dual mandate, softening the ground for Reaganomics.

Bobber,

Population is always rising, alot of people are nearing retirement, the rates of single people is rising, alot of people are moving right now. There’s so many factors that could push one to be more popular at any time, that it could swing all kinds of directions for any amount of time.

Right now, my guess is that because more and more people are deciding to stay single or only casually date, that apartments will win out (become more popular) for awhile. But, where people will want to live? I have no idea. The big coming factor is will most office jobs be automated away? Of course, there’s always obscure possibilities like that small pre-fab houses become very cheap and popular.

In CA here isn’t not really viable as a single person to rent an apartment by yourself when you could rent a house, get roommates, and pay less than half that of an apartment. Also, the population of CA is actually falling right now, so how are we still explaining the 10-15% increased in rent/prices as a shortage?

Housemates are about the worst thing in life. I did that for 2 years in my 20s and would never even consider it again.

Rip,

“Housemates are about the worst thing in life.”

Looking at the fact that 2bd apts almost always cost less than twice one bd apts (ie one bedrooms go for a premium), I would say that a mkt moving majority of humanity agrees.

Ground report from San Diego: San Diego is like a 3rd world country. People are crammed into small homes/apartments because the housing is so damn high.

Hope this remote work would over time ease things up.

I work from the rule of thumb here in Socal that rommates in a 2Br will pay appx 60% and maybe 65% of a 1Br rental rate. $2,000 2Br rental rate implies $1,670 1Br 1Bth rental rate ($1,000/.6. At low rent levels, the spread b/w 1Br and 2Br/1Bth is appx $250 to $300/Mo. $75 to $100 extra for a 2/2 vs 2/1.

So you pay $1,000 for 1/2 a 2Br or $1.650 to $1,700 for a 1Br. Plus with a roommate you split the utilities.

None of those demographics work to explain a 20% plus crash in one year. You could say they were part of a very slowly inflating bubble (delaying marriage in favor of dating) but C 19 is the pin that burst the bubble.

You have to wonder about the profile of the financing on these buildings. In the run up to this crash the typical RE guy mortgaged them to the hilt and buys/built something else. It worked for 10 years. Question is how many are in trouble and will have to sell or be foreclosed or be bailed out. The political climate for the latter may have taken a turn for the worse, but that is just a tea leaf reading.

Yeah, a real “black swan” for sure. Metal in that kicking can getting mighty thin. Maybe time for a new game?

nick kelly,

I’m talking about post pandemic. Pandemic and it’s effects are responsible for 2020. Going forward though, it’s not really possible to predict where the price of various housing is going. There are an enormous number of factors in play. It’s possible people could split (room mates) enough houses and apartments that the price of both crash. Or maybe not.

In a rent controlled apartment market, which SF has been since 1979, people tend to stay in their apartments longer. Why give up a $1,000 per month apartment when a comparable apartment is renting for over $2,600? A similar effect can be seen in the for sale market, where property taxes on homes of comparable value acquired in 2020 are much higher than those acquired in 1978 when California’s Proposition 13 passed. Then there is the large capital gains tax to consider on the sale of a home acquired in the Bay area in 1978.

Right and the AirBnB IPO is going to crash. In a article comparing the current stock market bubble to Dotcom, the writer said these companies are solid, and the chance of AirBnB going broke in the next five years is zero. Bottom line: this is a bubble you can buy.

Appraised value using the income approach would dictate a lower price. Market approach always lags the income and cost approach. Falling commercial values are also a negative indicator.

Slightly different markets. People don’t want apartment living now because of crowded elevator etc and need for space to WFH. Hence rents for apartment dropping and home prices rising.

Also some people can see the possibility of the pandemic winding down, so may be making a long term house bet that a landlord needing to fill a unit right now can’t make.

But I agree with you that if rents keep dropping it will bleed over to the housing price eventually.

Keep holding your breath for a housing crash. One day the doomers who missed out ten years ago may just have their moment.

Just shows what people really think of life in these cities. As soon as they have the chance to telecommute they get out as fast as they can.

The cause is actually that ‘life in these cities’ – cultural events, dining out, clubs, whatever turned you on – has been largely removed, destroyed, or altered beyond recognition. It’s no great epiphany, just a realization that there’s no point hanging around when there’s no there there anymore!

I really don’t think that people were paying three times the post tax rent ($25k+, pretax, every yr) because of live theater and better Indian food.

The “price plus” metros only massive appeal for most people were the higher paying jobs…which, if you penciled out the higher cost of living and taxes…might have been an illusion.

Another plus of non mega metros…they usually have much, much better access to buildable land (ie, not landlocked one way or another)…so that there is the promise of substantial future housing supply…and therefore a check on rising prices in the intermediate term.

Former SF resident, people live there for high quality food, ethnic diversity, weather, scenic beauty, many many reasons with high paying jobs much lower on the list for everyone outside of tech. There are a great many people who won’t look at life outside major metros for reasons of food and culture and ethnic diversity. I know many such people.

Not only that, but pure clean air right off the Pacific in SF….pretty important….although lately the fires trash it bad.

When I got my L1-L2 smog license (can run and maintain BAR Dyno smog equipment for diagnostics, but not certify..2012) I found out smog checks wouldn’t be needed in my area, except that the stuff is blown into the Central Valley and collects there.

But most everything post 2000 or 2002 (forget) is just done through the OBD-2 port, or so the tech told me in 2019.

From my observations, the only cultural events attended regularly by NYC residents are sporting events. Most high-end dining is business entertaining, while theater and museums are primarily visited by tourists. If you live and work in Manhattan, chances are you’re working a 60-hour week, and spending your free time outside the City (e.g., second home in LI, CT, or NJ). Also, lots of NY travel to New England. The locals hate them.

Migration out of the City of Seattle proper has been ably assisted by the city counsel, who would rather have homeless and drug ridden encampments than viable businesses. This too started before the pandemic and shows no sign of being reversed.

True. I was in downtown Seattle in October of 2019 and it was dreadful. Homeless junkies were everywhere. I saw a man walking around in a drugged out haze with no shirt on, and it was only like 50 degrees.

I was in Seattle in 1973 and stayed in a downtown hotel for two nights. The stairway was littered with bums who had passed out on the stairway. I had trouble making it up to my room. What sewer. I’ll never forget the sight.

Pretty much any major city downtown in the US in the early ’70s was a dump. Things have changed very drastically for the better, but have started to slide again the last 10 years.

Oh yea, it’s totally the same as it was before personal computers and the tech industry existed. Nothing has ever changed since 1973.

It’s one of the highest priced, affluent areas for no good reason at all.

Hard to see how a worker making $15 an hour

gets by after healthcare, payroll taxes, utilities,

food, clothing , etc… Something has got to give.

Property and rents are exploding all over Florida.

Very little inventory.

People realized that life is short and fragile, want to live in high quality of life, affordable, cities.

Oren,

Rents are NOT “exploding all over Florida.” Look at the data in the article.

Rents fell yoy in Miami, Orlando, and Tallahassee; flat-ish in Fort Lauderdale (1-BR up, 2-BR down); rose in Tampa and Jacksonville; and “exploded” in St. Petersburg.

Oren must be a REALTOR. He talks just like one.

Oren is quite correct if rent and property prices considered since 2014 in Saint Pete Wolf:

We started looking in early 2014 as we decided to move back to take care of elderly parents.

Houses in their hood were avg about $80K, with many below $50K. Average rent we saw was around $700/month for 2&1 house.

We were lucky by summer 2015, when our flyover farmstead finally sold, to find one for $80K that could close fast.

It’s now worth over $200K per zill O, while rents are at least $1800 for the same 2&1 — this a very mixed working class hood, with it’s share of retired, and many new houses replacing almost all selling the last few years. Other than some very overpriced ones, most houses here are selling in a few days.

Anecdotal, for sure, but having been in the biz for many years, I think it’s a fairly accurate picture of the last five years here. I also predict there will be a bust here for apts, as the builders continue to expand the downtown condos and apts, and the commercial is still growing greatly, with tech flooding in.

Saint Pete is no longer ”God’s Waiting Room,” as was so clearly the case for many many years!!

I certainly wish it were true that desirable places in Miami / Ft Lauderdale would drop but it ain’t happening. I don’t see it happening anytime soon. There are 2 million people in Broward. There are 2.75 million people in Dade. Population is growing by 10s of thousands quarterly.

I just looked at MLS for 3/2 all inventory condo and homes. Here’s what I find from Boca Raton to south Miami Homstead area (this area covers south Palm Beach county, Broward County, Dade County).

Under $400K There are less than 2000 units available. These are dumps in dumpy areas.

Same area homes from $401K-500K there are 900 available. Poor areas and needs lots of work.

Same area homes from $501K-600K there are 810 units. This is price range where maybe you’d want to live there. Still will need work and area maybe not great.

Same area home from $601K to $700K there are 700 units.

Same area home from $701K to $800K there are 500 units.

The fact is there is nothing affordable for families and there is nothing for sale. Anything that comes up goes in days. MLS is full of price increases.

Building we live in is full of new residents with NY, DC, Virginia, Pennsylvania license plates. This is new occurrence. They depart early off to go meet RE agents and they come home tired at end of day after seeing bunch of 500k+ “homes” that should be teardowns.

BTW, on another note Opa Locka and Boca Raton executive airports are now non-stop private jet traffic. I kid you not, it is non stop. Private jets coming and going like the commercial traffic at Miami International and Ft Lauderdale International used to be. Look up to the sky in south Florida today and you won’t find any commercial airliners. You will have no problem, however, finding the gorgeous chariots of modern day plutocrats filling the sky. It is incredible.

I Wish it Weren’t True,

We’re talking about RENTS in apartment buildings not purchase prices of condo and houses. They have disconnected in many markets.

Sounds like that Lawrence Yum who is a guest speaker on “Real Estate Today”. Always shilling for the “buy” side no matter what the market is.

What is $15/hour?

That is exactly why Google employees formed Worker’s Union.

The laborers cleaning Googlers’ houses should get paid more. Do you not agree?

Google workers make well into 6 figures. The union was formed to put more politically correct pressure on management

Google contractors — including bus drivers, cafeteria workers, janitorial people, security people, and lots people doing different jobs for Google, such as monitoring corners of the internet (I know one of those) — are low-paid workers. The Alphabet union is open to those contractors.

Wolf, please remember the Google creed from about 20 years ago. don’t be evil…

Honest, they aren’t evil… just follow the slogan.

?

And don’t forget Steve Job’s retort to that… which went something like this: don’t be evil, what a load of crock…

RE: Jobs’ comment

I remember when “personnel” went to “human resources”……what’s next, “carbon units” like on old Star Trek shows? Followed by a term for some part in a supply chain, full of “independent contractors” and “piece workers”?

I also remember when managers started using the term “backfill” for moving people around….that term came from pushing dirt back into a foundation hole.

We aren’t far from a new gilded age of some kind….but with no more land and fewer natural resources to colonize.

They better hope they can keep the Calvinism going.

In regards to hourly wages……

Easy math to convert a hourly forty hour wage into an annual total income…..

Here is the background math for conversion…… Fifty work weeks in a year multiplied by forty hours per week equals 2,000………so the hourly wage doubled and then add three zeroes is approximately annual income total.

Example 1)……..$10 an hour……..double hourly wage- add three zeroes….equals $20,000

Example 2)……$15 an hour….double hourly wage- add three zeroes…equals $30,000

……so…. just to emphasize…..the low to middle end hourly workers are struggling for monthly, food, living space, transportation, etc to maintain subsistence living. I think the hourly wage understates (camouflages) the financial struggle people face.

My son worked a $15 HR job. His salary was $31K, with a deduction of $3K for medical insurance with a high deductible and copay, roughly doubling the cost. For this job he need to supply his own car, computer, and cell phone. Even living at home he was barely making any money.

People live on a lot less than that. That’s about $2000/ month take home. Probably ought to be in the $800 per month rent area. Might mean finding a room mate. Cook your own food $200/ month. $50 phone and $45 smart phone pay as you go plan. Hiking or biking good healthy nearly free pass times. Read free on line. Throw out cable. Should be able to save $500/ month if you have incentive to delay gratification.

Hmm… close.

My math is someone “full time” at $15/hour is going to be held to 32 hours/wk or less. A lot of employers will want their people under 28 hours a week. This will be an on call job with hours for each day being decided sometimes 12 to 24 hours in advance. This is likely a job with no or very minimal benefits.

That means the gross is likely to be somewhere around $1920/mo. Likely much less. Out of that will come all taxes etc. So actual Net spend is going to be less.

Then factor in:

– Rent

– Commute cost. Transit likely means time tax. Car is less time, but more cash. Cheaper places are farther away.

– Food

– Don’t get sick; better not get COVID

– Utilities

– Emergency – Cheap car breaks down. Now what?

– Better have a computer or smart phone so you can log onto your employer web site to see if you are working tomorrow and what time you have to show up.

My son nets 1400 to 1700 a month. (First job out of high school.) He lives at home. We have done the numbers. He could move out to a house or apartment, but it would require 2 to 3 room mates and would take every dime he makes. Better to stay at home and save as much as possible.

People I have met, working unskilled labor, at that hourly rate are holding 2 or 3 jobs to make ends meet.

The reason I say what I do is I lived for five years on $15,000/ year, had a car, lived by myself, lived in safe neighborhood, gave my kids several hundred dollars each at Christmas. How did I do it. I lived a 1960’s kind of lifestyle. Americans have gotten used to a high discretionary income of $70 plus dollars per day. Thats $2100 per month. It’s not for everyone. But I was tired of working all the time so I lived on savings for five years. It was great.

Brian,

The Fed has hurt people like your son, while proclaiming to help the “People”.

And they have done so without essentially any course correction for 20 yrs.

“Don’t get sick; better not get Covid”

Yep! Don’t get sick, don’t get injured, don’t become disabled, and please, for the love of God…don’t get old.

Please, just don’t.

And enjoy Akron.

No offense, but 15$ an hour work is entry level work, adults in that range need to learn a marketable skill and earn more based on producing more. The minimum wage has never been sufficient for a home purchase.

The important thing is to pay as little as possible to live anywhere; it is necessary to keep the product of your Labor

Rents falling in multi-unit housing while they rise in adjacent single family homes. People are trying to distance themselves from their neighbors. I am a landlord, and I am very lucky that my rentals are all single families … I never thought this scenario would unfold. I know other landlords that own multi-unit buildings and they are fighting for their lives.

So when rents crater even more.. You, of course, will have sold all your rentals at the top.

Thanks for sharing.

Andy, where’s Costello? You’r not very funny. I appreciate SoalJim’s input whether I agree with it or not. That’s the purpose of this forum.

SocalJim

I am there with you. Had SFH rental investments from 2004 until this past year when I switched to exclusively private lending for SFH real estate. I carry the notes on most of the SFHs I remodeled in recent years which I sold to investors.

When CV-19 hit, I was mentally preparing to take some of those collateral assets back and reluctantly become a landlord again. Instead, my loan collateral is appreciating. It’s a wacky world.

This is what I’m seeing in the Boston area. Multi family is getting hammered right now.

However, SF is unique in that homeless people are placed in the hi-end hotels, for something like $8,000/month. On taxpayers dime of course. And drugs and booze purportedly delivered onsite. Rumors..

So $3K for 1-br does not seem too bad. Too much money here. They may even replace crumbling utility polls someday. Soon after they clean up all the glass from car break-ins.

Those hotels may be expensive, because all hotels are expensive in San Francisco, but they’re not “high end.” I know some of them, and they’re dumps.

Wolf, You don’t know what a dump is until you’ve stayed at the old Travel Lodge on Ellis. It had been converted to the Air Travel by the Chinese Commie Airline that had bought it. They saved money by recycling part of the sign. We ducked in there to avoid a New Year’s Eve DUI.

Blood red carpet soaked in urine and stained with trails of black grease that they used some kind of toxic cleaning chemical to try and clean, then that smell was supposedly covered up with cheap air freshener poured directly onto it. The smell sobered us up fast and we drove home. I think that even bums would reject that place.

Getting $2,500 for the rental of a two bedroom condo in a good neighborhood in DC. Close to the value in the table above. I’m starting to see homeless encampments in the close-in suburbs of DC. Also, a lot more panhandlers. No one doing anything to get rid of this eyesore. Its going to get worse before it gets better.

Given Joe’s age, he probably can take credit for developing the polio vaccine too (sarc)!

So refreshing to see droll political diatribes reposted in the comments of a financial blog. At least post something original.

Getting rid of the eyesore means getting rid of the people and where would they go next?

The reason for the increasing numbers of homeless people during the last forty years is the increasing gap between inflation especially in housing and the rise in income. Add the collapse of the economy because of COVID19…

Maybe if Congress had decided to help the majority of Americans suffering things would be different. However, the bottom 80% doesn’t have enough money for the political bribes needed to get that help, which is why most of the aid went to those who did not need it.

As for it getting worse, I expect 1960s levels of protests soon, followed by real unrest, then possibly violent suppression or civil war. Interesting times.

What a great, informative article.

I’m amused by the sky-rocketing rents in Newark. Things must be really really bad out there for Newark to be appealing. You wouldn’t move from Manhattan to Newark to escape covid. Since the article uses asking rents it could be some luxury complexes came on line and are offering ridiculous rents that never get filled.

The occupancy in Newark could be dropping as the ‘asking rents’ on average rise.

Newark is beautiful this time of year

Sure…but nothing like the Fall, when the lakes and air change color…

Or Spring…when the ground thaws and the bodies spring up…

Hi Wolf,

Any thoughts if the median asking rent numbers are being skewed by the fact that people at the lower end of the income spectrum are being disproportionately affected by the downturn?

I understand the eviction moratorium is artificially preventing some of the lower end apartments from coming on the market, but at least some people must be leaving voluntarily to double up.

Has there been a divergence in the mean/median asking price since the start of the crisis? If its truly the “white collar” folks leaving for cheaper living and the “blue collar” folks hunkering down while they are protected from eviction, then things are far worse than this data suggests.

In the big expensive cities named in this article, it’s the HIGH END, the Luxury stuff in big towers, that is getting hit the most, as I pointed out.

You could be onto something.

Since high end luxury big tower stuff in coastal cities rents at the same price as adjacent single family homes, those tenants can avoid COVID by moving to single family. So, the big tower luxury rents tradeoff bringing down the average apt rent while SFR rents rise. This matches what I see on the ground.

To me, your data seems to show apt rent drops only in cities that tend to have luxury tower rentals. That might be the answer.

“Why would you spend $5,000 a month for a two bedroom if you don’t have to?” That was the question a big landlord posed. And the answer is, you wouldn’t.

So if people can work from anywhere, and if elevators are scary suddenly, then well, they move… to anywhere. SFH rentals, as you noted, have been doing well, and even those in San Francisco have been hanging on.

CITI has a nice little(actually a really big, and it is FREE to boot application), to just step right in to save the day, MNE’s to invest in US, for all kinds of tax breaks. Do note not a mention that the US even consists of an organizational, geographic system based on property owners, living in STATES. Add to the non-mentioning of that little fact by CITI, as they advertise their great new software application, note that ALEC(a sort-of political group) has been pushing for eliminating having US elections of US Senators. Pushing along with other pushers the great idea that Senators should just be appointed. Not only are some well-linked international buddies outside of the US boundaries, but perhaps also inside the US boundaries seem to really be supportive of debt-slavery, and all kinds of real slavery globally. Check out the real money behind CITI. Where it really winds up outside of the US, even after all the well-paid top dogs fight over their deals.

https://www.citivelocity.com/citybuilder/eppublic/cb/us

There aren’t very many real projects with real financial backing either, when you deep-dive into the “US” projects either.

“A good boxer must also have fear. But he must master it.”— Henry Maske

Btw Absence of students maximus at local (OR state higher edu funded) university. Dozens of student housing facilities (units with 50-125 rooms each) are dark (night observation) & parking lots empty.

Insignificant quantitative aspects for rental housing calculus, though university budgeting is (probably) feeling the lack of cash flow from thousands of missing students.

Same thing’s happening here in Tucson. I don’t know how many students are missing from the University of Arizona, but, judging by the number of “for rent” signs I’m seeing, it’s a goodly number.

I’m thinking that the future of higher education is going to look a lot like an institution that already exists in the Grand Canyon State. I know a couple of people who went there, and they both spoke highly of their experience.

And that would be Northern Arizona University, which has operated an online division for a couple of decades.

I’m across Wolf’s swimming pool, over here in Berkeley, and things have gotten really weird here, starting with UC policies, which end up setting a bottom-line for the apt & rooming house market in this U-Town.

First, all the soriorities were closed, while the Frats were allowed to remain open, if with a lot fewer, “Bros,’ living in them (under a, “no parties” policy dictat), while all in-person classes were cancelled, as are next semester’s, at least to begin the semester.

Don’t ask me why or how UC Berkeley came up with this policy, all’s I know is the effect on my apt building (on Frat Row) was to be empied out of all the regular students, and subsequently refilled by at least 20 soriority sisters, who (as groups) moved into at least five of my surrounding apartments. I am literally surrounded on both sides by Sor Sisters. It’s nice…’cause only one set have high noses, while the other two are pretty good girls. But, it is weird…and there are not enough displaced Sor Sisters to offset a broad exodus of students.

I took a gander at Zillow for Berk, and rents are seriously softening, reflecting the all-online semester we’ve seen, as will be the next. But, there are offsetting factors.

The first is that science lab classes, and classes/majors requiring lab time are still being held. The second concerns wealth and class. The rich kids who can afford it are still pursuing the social aspects of college life, which includes leaving home and living at college, despite the pandemic and the class closures.

In other words, a significant number of those with the wealth, and therefore the flexibility to decide to still come and live in Berkeley, are still here.

But, that is only a fraction of the typical population seeking housing here during the school year, so the market is softening down to what I’d call interesting and informative levels of support… being supported by those few who can still afford to come, and those who have lab-work based classes.

I’ve observed that these residential trends roll downhill into commercial consequences for local retail properties, as the retail and food operations able to remain open, if only partially, only have a partial percentage of their normal resident student population to serve.

It’s a double-whammy: residential and commercial properties are spiraling-down together in the weirdest dance of economic destruction I’ve ever seen…

The weirdest economy ever is a product of a much deeper weirdness, being a product of the nature of the fundamental shape of our, “values,” or more precisely, the shape of the distortions in/of our, “values-system,” meaning that our social-political actions & responces (to the pandemic) are informative, as they are refecting the most fundamental nature and truths about our operative value-systems and our motivations. Something that cannot grow forever, will stop growing at some point in time. We hit that point in 2007… and kept growing by printing profits. Weakened by this long corruption, we now confront emergency conditions with depleated resources.

It’s our most fundamental greed and corruption that initially weakened us, our nation, prior to the impact of the pandemic, it’s our fundamental greed and corruption that’s conditioned our crazy self-destructive responses to the CFAF, while this same greed and corruption assures these already crazy econ distortions will continue to get even weirder and weirder (print to the moon…negative rates?) until it finally blows…

This is a layer-cake of weird…

We have added a lot of debt to an economy with a lot of problems. That means future is not going to be as bright for most everyone. Best thing to do is get your personal finances in good shape while you can choose to and not get caught having to make tough decisions in a financial panic. People who can pay will have to pay more maybe through financial repression, inflation or more taxes. Politicians will decide who and how. Congress has the power to tax and spend, but too much of that breaks the economic machine.

What do you make of San Diego? It’s flat, while LA/SF are down double digits.

San Diego seems to be the most sane Coastal CA large city and is probably an improvement in terms of quality of life compared to SF Bay Area or LA. Lots of things to do outdoors, the best weather of the major CA cities, bunch of freeways to get everywhere, homeless aren’t as visible as LA/SF, a lot of SFH housing, etc. Additionally, it is a huge discount compared to the SF bay area, and slightly cheaper than LA, while being IMHO a more desirable place to live.

The ‘problem’ with San Diego, and the thing that has kept prices relatively affordable in my estimation, is the lack of a lot of high paying jobs or a dominant industry that pushes up the local population’s wages. Now that SF/LA populations can work from anywhere, you can take your wages wherever, and San Diego offers all the benefits of Coastal CA living while being comparatively affordable and having seemingly less of the problems that are common to SF/LA (Traffic, homeless, crazy politics, etc.).

Source: Grew up in the bay area, still have family/friends in the area, lived in So AZ for 10+ years, and recently bought a home in SD. A new family moved in a few houses down from me a month ago. Apple employee with wife and 2 kids, moving out of an SF apartment to a San Diego suburban SFH…Still working from home for Apple.

@AZ to SD

“San Diego offers all the benefits of Coastal CA living while being comparatively affordable and having seemingly less of the problems that are common to SF/LA (Traffic, homeless, crazy politics, etc.).”

You sound like you’re describing the old San Diego from say ten or fifteen years ago. What you said was all true. Now, San Diego is crowded, expensive and there are homeless everywhere. And the building does not stop. They’re expanding the freeways and building building building.

San Diego in ten years will be a carbon copy of LA unless they restrict building. Sad really, and the city is killing its tourism biz.

“Slightly better than LA” should not be the city slogan.

“America’s Finest City” is the slogan, and most of what you say about building and expansion is wrong. One reason we no longer have an NFL franchise. Perhaps now that the county supervisors have a Democratic majority, they will open up the back country, but I doubt it. Project have to go to ballot proposition and voters are increasingly sensitive to affordability when they vote and few developers are willing to do them. The state has mandates for affordable which most cities can’t meet. Seems to portend more high density housing in more rural areas. The real action is outside the city limits, the city itself is quite large geographically and has a poor history of management in the fringe communities. More like SF that LA, there is a real political mix. much of it reactionary.

SD area overall much better than LA or SF for single family living. And less visible homeless problem by small margin. Sure, not like 10 years ago, but nowhere good is like it was 10 years ago. And SF and LA are much worse by comparison.

During the depression the cops just took them to the city (or maybe county) limits and dropped them off. Problem solved.

That’s how they do it now in Sedona.

Probably in a lot of other high end real estate places, also.

“Since the article uses asking rents it could be some luxury complexes came on line and are offering ridiculous rents that never get filled.”

I’m wondering the same thing.

When prices move this far, this fast, in a real asset (non financial) mkt, some reality check questions might be worth while.

1) Might it be possible that the apt mkt is more “financialized” than is commonly believed? By that, I mean is it possible that there is a broader “rent to sublet” mkt out there, where financial players were speculating on “rental flips” in the high $ metros…and are now dumping/repositioning those “rent to sublet” plays (might, maybe, explain Newark goofiness).

I’m not saying this was/is the case but financial players can make the mkts move faster and with more price volatility than you are likely to see with “real asset” users who just want a place to live.

2) How well do we understand Zumper’s methodology? Are we talking sampled surveys or complete price censuses in the selected metros. Again, Newark (more traditionally a place to catch a disease rather than escape one…) is an oddity that maybe Zumper could shed a light on.

Also, there are other rental surveys that could provide cross checks.

3) Construction is always going to lag price changes, but I don’t *think* apt starts in the “Escape from NY/SF” receiving metros have really tweaked upward yet.

Normally, your average developer is like a fly on…er…honey when the numbers pencil out for new starts. The banks might be slowing things down though, wanting to see how the rent in arrears wave plays out.

More broadly though, it is good to see housing costs across the country come at least somewhat closer to a rough (very rough) equality/equilibrium.

Doing a quick Google search, I discovered that Newark has a full blown rent control system in place complete with a staffed office, required registration and all sorts of other Orwellian niceties. May bear some further investigation to see what role, if any that is playing in the reported surge in rental rates.

Wonder if this is just the pattern. The housing bubbles start where economic activity starts to heat up (SF &NY). The wealth effect spreads from these centers to the outer burbs then smaller cities, towns and finally rural and the least desirable metro areas (Newark!).

Rents follow this wave. As the tide recedes its the pull from the wealth centers as first rents crater followed by housing prices (and with reduction of tax deductions being available this situation is exacerbated) that eventually pull down prices throughout the country.

I’ve read that for every high paying professional job, 6 service related jobs are created. At my company, the highest paid employees are being axed. Us remaining employees are recalibrating to pick up the slack. In doing this it becomes apparent that these highly compensated managers aren’t even needed. This is exactly the thing I saw back in the 2008-2011. Former controllers were taking jobs as senior accountants. I think we will see this trend continue as companies look to cut. The immediate effect will be the devastation of lots and lots of service jobs.

For those who think the Fed or the banks will not allow housing prices to collapse consider that there is a major counter weight – companies locked and loaded to make major purchases of bulk foreclosures and buy lease back to those strained to make house payments. Billions of dollars are available to invest in those schemes. Patience is required as the goal is to get as many in the pool as they possible can (the debt pool). And we’re close to that point.

In recourse states where property taxes can rise as fast as the legal jurisdiction they reside in need it, this buy-leaseback thing may look pretty good.

It would be interesting to have some data on how the housing collapse played out last time. Although it did seem a bit overnight.

“companies locked and loaded to make major purchases of bulk foreclosures and buy lease back to those strained to make house payments”

Coal company town, where you have to lease your home from your employer.

Would explain why Corps remained stubbornly ensconced in highest cost metros…they owned a chunk of local residential housing stock.

But probably not…would have showed up in their financials.

But…insiders and affiliates who controlled siting decisions…could have been big RRE owners locally…a nice off the books Bennie that would also explain the fondness for most costly locales…

MarkinSF, I don’t think this is a normal housing bubble. I wish it was.

This is a hard asset run for a number of reasons. A small hard asset run is OK, but this is too much. Home prices are moving up too fast and that invites instability. You have to worry what the future holds. This is a good time to make sure you have enough liquidity for an uncertain short term horizon. I am worried ….

This high-unemployment pandemic has started perhaps a rather brutal reevaluation of the usefulness of many positions in world of work today.

I think we will find, to actually no great surprise, that many jobs just aren’t that necessary, useful, or contribute meaningfully to organizations’ bottom line– not just in gubermint and academia but corporate space as well.

It is only when tide goes out that we find out who has been swimming in competition swim suits and who has been dawdling stark naked in shallow water.

“We must do away with the absolutely specious notion that everybody has to earn a living. It is a fact today that one in ten thousand of us can make a technological breakthrough capable of supporting all the rest. The youth of today are absolutely right in recognizing this nonsense of earning a living. We keep inventing jobs because of this false idea that everybody has to be employed at some kind of drudgery because, according to Malthusian Darwinian theory he must justify his right to exist. So we have inspectors of inspectors and people making instruments for inspectors to inspect inspectors. The true business of people should be to go back to school and think about whatever it was they were thinking about before somebody came along and told them they had to earn a living.”

– Buckminster Fuller

SuzeB,

And, yet, going by the fact that most metro rental rates have increased while incomes have stagnated (at best) for 20 years, a strong argument can be made that, for a while at least, the US has had an insufficient housing stock.

So, should we pay people a guaranteed income to do nothing…while homes remain unbuilt (and housing inflation worsens).

Or medical patients go under treated (even as the medical industry’s revenues soar).

Or college students are quoted tuition prices that are 10 times those of the 70’s.

Those are all predictable consequences of reducing the supply of labor that a guaranteed income might create.

The post-scarcity world that exists in academics’ heads exists only there and pay/price/cost/benefits are how resources get continually directed in the real world…outside of the ivory Tower, which too often exists in splendid idiot isolation…massively subsidized by the State (directly or through huge tax exemptions).

Ironically, for all the academic hippie-kum-bay-aaa, Lady Bountiful talk…academic institutions have some of the most abusively asymmetric work conditions/pay around.

Ask a teaching grad student or an adjunct.

Bucky’s thoughts on our education system;

“All the real talent is siphoned off into the Arts and Sciences, and that leaves the dregs to put it all together”

Some caveman probably said a similar thing shortly after invention of the wheel displaced all the rock carriers. Just as false now as it was then.

Not totally Happy, the learning curve is really flattening,

We are really bumping up against our limits now scientifically….the real small and the real big…..size limits. The physics equations in those edge areas are starting to resemble those of the social sciences…all approximations, probability, and statistical stuff…..maybe even best guesses.

Newton still covers most everyday stuff in science.

Not to mention getting enough power for this lifestyle of ours.

The authorities are now beginning to show just how desperate they are to keep the housing bubble aloft for as long as possible.

From NOLO:

“The Federal Housing Administration (FHA), part of the U.S. Department of Housing and Urban Development (HUD), announced that it is suspending foreclosures and foreclosure-related evictions through February 28, 2021.” … “HUD also said that homeowners will get until February 28, 2021, to request a COVID-19 forbearance from their mortgage servicer.”

Google Unions – the once generous perks are gone. Free meals, gyms, swimming pools, laundry are no longer with WFH. WFH ends up with India rolling out the red carpet.

How does rent control affect the SF rental market? New tenants with 25-30% lower rents are protected by rent control? The tide will reverse at some point. Not so good for the property owners revenue stream.

Rip, I agree with you 100%. I went on a motorcycle vacation to Yellowstone this summer. I’d rather rent a place around Jackson, WY and have a nice time walking in safety and not looking at blue tarp communties, druggies, and street thugs. The BLM/Antifa movement and senseless crime woke some folks up and they had enough.

I have a young guy that started working with us. Mid 30’s. He wants to rent a place at an apartment complex for 1800 a month in a good area. Do you know what he said? He doesn’t want to live in a lousy area with lousy people. It would put a strain some on his budget, but he wants this. Enough said.

Four of the top ten wealthiest counties in the U.S. are near Washington, D.C. Rents are higher there.

“Four of the top ten wealthiest counties in the U.S. are near Washington, D.C.”

Maryland has the most millionaires per capita in the US…and it ain’t because of the f@%#&/g crab cake industry.

Fear and panic expressed as the boy called ignorance and the girl called want. In the big picture, you can run but you can’t hide. The dash is no more rational than the system which indoctrinated everyone into believing this nonsense of the last 70 years could continue unabated by real consequences that would spread beyond all borders. Without a major change in the approach to sustaining so many souls, Doom is the end result. Admitting it for factious purposes, you make it worse. It will just export the same problem to new places until all are infected. Maybe the future will lie in bulldozer factories. All this tech and we’re still stuck in the 1840’s. The more things change…..

Escape from the frying pan to the fire. From one dem shole to another.

I know one couple that moved their business from NYC to NJ because rent and taxes were killing them. Took them 1 year to get permitted in NJ – then they had to close during the lockdown. We bought their inventory cause we are friends.

Look to Venezuela, Tibet, and Sri Lanka for the future.

The downside is you live in Newark, NJ.

Didn’t I read a day or so ago, on these pages, that Boston was the “go to” city for NYC residents bailing out of their city? Why are they among the highest losers in today’s data?

The highest mobility is among those who can afford it. Seems logical that high rent properties, and maybe businesses, feel the first and highest impact of an exodus. Will it spread and how far? Who knows.

I wonder if you’d get an honest answer from a group of moving folks as to exactly why they are leaving. I for one, fully understand why I’m looking to leave the inner suburban area. I grew up here since it was a rural area. It is looking and feeling like a liberally run city. Need an example? Look at any of Wolf’s top 10 list and see if you can figure it out. A clue: It certainly has nothing to do with working from home.

Lobotomized liberal governance has something to do with it, but the highest cost metros have been economically tap dancing on the razor’s edge for the longest and with the greatest intensity.

That probably has the most to do with it…with C19 pushing people to finally act.

Lower cost metros provide both companies and people with more of an economic cushion in case things turn bad…high cost metros force people to live on the edge.

Don’t disagree with any of your comment, good and to the point as usual; how some ever, IIRC at this point in the middle of my 8th decade, the ”razor’s edge” is where the fun and excitement and thrills mostly are, eh?

Walking around and across LA and SF and London many years ago, day and night, we were prepared and able to run really fast if need be,,, and racing through those same streets on bikes and in cars, ditto fast and it was fun while it lasted,,, sure, some of us lost our driving license, but mostly we didn’t stop, and we could still walk and hitch hike, etc., when we had to,,, and it was fun and challenging.

SO, my suggestion is, GO FOR IT now, cause ya can’t do ”stuff” when you’re old, or at least not as much stuff,, though it still is pretty easy to get into trouble,

Had a conversation with my millennial tenants. Boomers took the housing wealth, The next generation took the pension wealth,

What is left for them. A inheritance maybe. I havn’t thought it through

But maybe one of those apps that round up your purchases to the next

dollar and then invest it for you. Since so many make so little it

could be a start.

The wealthy stick this canard in their newspapers so no one will notice the massive redistribution of pre-tax income over the last 40 years.

Bankruptcy rates for those over 65 have doubled since 1991 mostly due to healthcare expenses and lost wages from those health issues between ages 55 and Medicare.

Most boomers don’t/won’t have the income stream in retirement that their parents had from traditional pensions. Boomers who hope to have anything more than Social Security, which they paid into, need to have saved up hefty 401ks.

And of course there’s all that boomer housing wealth that went “poof” in 08.

Young people do have too much debt, but the bigger issue is the horrible labor market they face.

My millennial kids are doing just fine. I think it depends on location and what careers they have chosen.

I distinctly remember telling them that “one” does not attend university to find oneself, or figure out what to do for a career while attending university. They both chose modest public schools and public post secondary offerings. They also worked their way through school with minimal help from Dad. Daughter ended up with $14K in student loans for a 5 year degree, son had no loans as he chose an electrical trade and now earns 200K per year in industry. My daughter should have had no loans, but one year she jumped on the borrowing band wagon and also went to Mexico. They both own homes and will be able to retire young should any economy remain functioning.

Yes, they will inherit my assets, but they don’t count on it or think about it from what I can see.

Re: “a little crazy”

That’s so 2020 and way behind the curve!

The new variant, SARS-CoV-2 VOC 202012/01, 501Y.V1 or B.1.1.7 will evolve the current WTF charts as we all drop our jaws.

Greater supply issues with homes, larger spike prices, lower dollar, lower gold, lower wages, higher unemployment, higher internet sales, shut down global economies, etc. Possible that Biden will have to shut down economy before end of January ….

I think one thing behind credit card weirdness is more poor people living together, combining resources, and perhaps that gets factored into weird new household formation and even combined families pooling everything together, as they consume less stuff.

What ever trend happened in 2020, look for batcrap crazy stuff for months ahead.

Exodus: Movement of Jah people! Oh-oh-oh, yea-eah!

…

Men and people will fight ya down (Tell me why!)

When ya see Jah light. (Ha-ha-ha-ha-ha-ha-ha!)

Let me tell you if you’re not wrong; (Then, why?)

Everything is all right.

So we gonna walk – all right! – through de roads of creation:

We the generation (Tell me why!)

(Trod through great tribulation) trod through great tribulation.Exodus, all right! Movement of Jah people!

Oh, yeah! O-oo, yeah! All right!

Exodus: Movement of Jah people! Oh, yeah!Yeah-yeah-yeah, well!

Uh! Open your eyes and look within:

Are you satisfied (with the life you’re living)? Uh!

We know where we’re going, uh!

We know where we’re from.

We’re leaving Babylon,

We’re going to our Father land.

“Boomers took the housing wealth, The next generation took the pension wealth”

Do you mean “the previous generation took the pension wealth?” Because, us Gen Xers didn’t take squat.

Speaking for your self rip?

This pre boomer has two of those Gen Xrs with at least twice the net worth of their parents, more likely 5 times.

Different strokes for different folks and the results that follow, eh?

Not even trying to keep up with the younger gens any more…

Brag much? And he said “took,” not “earned. Try to keep up.

Wolf, I would really caution using Zumper. It’s not a particularly well-known site, and I don’t really know where they are getting numbers from, but CoStar, a far more reputable source IMO (which pulls from Apartments.com, the largest apartment website in the country), has Newark rents down -0.5%. It’s pulling from an inventory of over 25K units it tracks, which is orders of magnitude more than Zumper’s inventory set of only 1,000 units currently listed in Newark. Providence, a 17% jump in Zumper data, is at only about 3% YoY in CoStar. Sacramento actually seemed larger around 6% in Costar, which makes more sense to me because of the SF exodus. Still a far cry from Zumper’s 18.5% figure.

The issue is that Zumper data is not methodologically sound. It is just taking the median of all apartments listed on Zumper, without respect to how it skews the historic mix. This is exasterbated by the small universe of properties that Zumper actually covers. This data issue is similar to the median home sales price being affected by the mix of homes sold, where larger more expensive homes are selling this year, and condos are not, pushing the median price higher (although yes, home prices are up overall – this is just an added effect on the median sales price). I believe you’ve written about that effect this year.

Looking at the Newark data set, its clear that the figures jumped in 2020 due to a luxury property in downtown Newark listing itself on Zumper. You can see on their website that rents shot up from $1,550 for a 2BR near the end of 2019 to $2,400 on January 4 – well before the pandemic. Many of those listings are still active on Zumper at that high price point, which would indicate that absorption of units has NOT taken place, which means that people are not moving en masse to Newark, exactly the opposite of what a cusory read shows. In fact, it shows rents in downtown newark dropping from that date – indicating that they are probably reducing asking rents to lure tenants.

On top of this, I doubt Zumper is using -effective- rents, which would be net of concessions (subtracted pro-rata over the life of the lease, IE a one month concession = 1/12 = ~8% off the monthly gross asking rent). A quick browse of Zumper shows that landlords are simply writing concessions in the body of the listing, so I doubt Zumper is picking this information up. Asking rents and effective rents have majorly diverged in almost all markets, as landlords hope to hold the line with asking rents and offer concessions, ideally removing concessions when the economic crisis is over – and then they will have maintained their asking rent levels.

I’d really encourage you to use a more reputable source like Apartment List https://www.apartmentlist.com/research/national-rent-data. They have actual economists parsing the data. Even still, Apartment List isn’t as robust as CoStar – but it’s much more in line with a believable figure.