And this is just for April, the very beginning of the Pandemic’s impact on housing.

By Wolf Richter for WOLF STREET.

OK, it’s actually worse. Mortgages that are in forbearance and have not missed a payment before going into forbearance don’t count as delinquent. They’re reported as “current.” And 8.2% of all mortgages in the US – or 4.1 million loans – are currently in forbearance, according to the Mortgage Bankers Association. But if they did not miss a payment before entering forbearance, they don’t count in the suddenly spiking delinquency data.

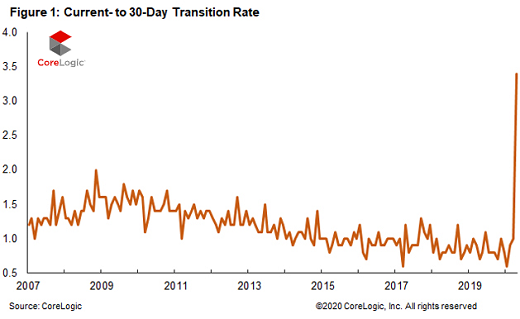

The onslaught of delinquencies came suddenly in April, according to CoreLogic, a property data and analytics company (owner of the Case-Shiller Home Price Index), which released its monthly Loan Performance Insights today. And it came after 27 months in a row of declining delinquency rates. These delinquency rates move in stages – and the early stages are now getting hit:

Transition from “Current” to 30-days past due: In April, the share of all mortgages that were past due, but less than 30 days, soared to 3.4% of all mortgages, the highest in the data going back to 1999. This was up from 0.7% in April last year. During the Housing Bust, this rate peaked in November 2008 at 2% (chart via CoreLogic):

From 30 to 59 days past due: The rate of these early delinquencies soared to 4.2% of all mortgages, the highest in the data going back to 1999. This was up from 1.7% in April last year.

From 60 to 89 days past due: As of April, this stage had not yet been impacted, with the rate remaining relatively low at 0.7% (up from 0.6% in April last year). This stage will jump in the report to be released a month from now when today’s 30-to-59-day delinquencies, that haven’t been cured by then, move into this stage.

Serious delinquencies, 90 days or more past due, including loans in foreclosure: As of April, this stage had not been impacted, and the rate ticked down to 1.2% (from 1.3% in April a year ago). We should see the rate rise in two months and further out.

Overall delinquency rate, 30-plus days, jumped to 6.1%, up from 3.6% in April last year. This was the highest overall delinquency rate since January 2016 (on the way down).

These delinquency rates are the first real impact seen on the housing market by the worst employment crisis in a lifetime, with over 32 million people claiming state or federal unemployment benefits. There is no way – despite rumors to the contrary – that a housing market sails unscathed through that kind of employment crisis.

Delinquency Hotspots:

The overall delinquency rate rose in every state. But there were some real hotspots, in terms of the percentage-point increase in the delinquency rate in April, compared to April a year ago:

- New York: +4.7 percentage points

- New Jersey: +4.6 percentage points

- Nevada: +4.5 percentage points

- Florida: +4.0 percentage points

- Hawaii: +3.7 percentage points.

The worst hit metros are tourism destinations and New York City where the most devastating and deadliest outbreak of the Pandemic in the US occurred. These are massive increases in the delinquency rates in April:

- Miami, FL: +6.7 percentage points

- Kahului, HI: +6.2 percentage points

- New York, NY: +5.5 percentage points

- Atlantic City, NJ: +5.4 percentage points

- Las Vegas, NV: +5.3 percentage points.

“With home prices expected to drop 6.6% by May 2021, thus depleting home equity buffers for borrowers, we can expect to see an increase in later-stage delinquency and foreclosure rates in the coming months,” CoreLogic said in the report.

With over 8% of the mortgages now being in forbearance, there is a lot of uncertainty about them as well – how many of them can exit forbearance or the extension and return to regular payments, and how many of them end up exiting forbearance and becoming delinquent.

CoreLogic expects to see “a rise in delinquencies in the next 12-18 months – especially as forbearance periods under the CARES Act come to a close,” the report said. To what extent the delinquencies deteriorate further depends largely on the labor market, and on unemployment, and that remains a horrible mess at the moment.

The time for deals on new vehicles has arrived. Read… Moving the Iron amid Sagging Demand: Tesla Cuts Price of Model Y, after Cutting Prices of Model 3, S & X, as Other Automakers Offer Record Incentives.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Is it any surprise? AirBnb now has a NEW feature where you can donate to your favorite hosts. It’s basically “help your hosts pay their mortgageS!!!”

Go to Twitter and see people skewering the idea. It’s truly hilarious.

funny – guy called me on my vacay property about turning it into airbnb

Wow. That’s amazing. “Please help your friendly neighborhood avaricious hosts pay off one of their 17 mortgages while they charge exorbitant overnight rates that are little better than traditional hotels, make you clean the property up before leaving, take out garbage, groom the house cat..”

Hotel rates are very good now. Why bother with BnB?

Hotels = sharing same air with many people.

Hilariously there is a SNL sketch about this that predates the apps for doing this.

Unfortunately I cannot find it.

Relatives came to my area and stayed in AirBnb, in a posh beach area of SoCa. The owners were in Europe and controlled the heat in the jacuzzi, only turning it on for one hour a day. Money is international now, China just ramped up new credit. Do the owners who are in the EU have access to liquidity they can use to satisfy American lenders? Will they cut their losses? In some ways it’s all a giant check kiting scheme, and the markets prefer to believe both parties are whole, not that any one party is insolvent.

Massive debt arbitrage fail.

In my experience, most charge market rates otherwise they will stay vacant. The platform shows comparable properties when you search for a property.

Banks will probably own most real estate in the end. Whatever it cost to get all of it will be how much is printed. When you are to big to fail and the government has your back you may as well get it all.

Italian banks got to own a lot of real estate after 2010, as the dust from the Great Financial Crisis (GFC) started to settle. They didn’t like this situation one tiny bit and they like it even less today. Banks are not REIT, much less so realtors or rental agencies.

Still these days, over a decade after the GFC and as the next crisis is starting to bite, one can find large-scale advertisement for this bank-owned real estate. Most of it is is half finished, in bad shape, in the middle of nowhere or just a combination of these three. All of it has been on the market for years with no takers.

In all fairness Italy’s largest banks have progressively shifted away from both real estate and construction and from overwhelmingly accepting real estate as collaterals. But the smaller local banks have stepped in with enthusiasm: these are the banks that will be hit like a ton of bricks. Again.

It will be interesting to see what will happen when the speculators these two-bit banks generously bankrolled will just hand them over the half-finished concrete horrors and move away, as the terms of their contracts and the law allow.

Banks like people paying mortgages better than them owning an asset that the owner (the bank if they foreclose) has to keep up, insure, and pay taxes on.

You’re so right. This is a capital grab.

Nope. Banks abhor REO as a giant cost sink. They just want to be bankers.

NYC will be hit very hard, I think 400 people migrate out every day, usually those are replace by incoming immigrants. That is now on hold. In Queens NY, the immigration capital of America, I do see a decline in demand for apartments already. If we do have Gov’t layoffs this will add fuel to the fire, as these people tend to migrate south. Major problem for RE ahead.

Nobody goes to New York any more, it’s too crowded.

I’d expect all very expensive cities to get slammed — tourist-heavy places like NYC and SFO in particular.

People are there for proximity to high-paying jobs or high income opportunities (running AirBnBs) that justify the excruciating cost and hassles of city living. At the same time, many of the lifestyle features, like restaurants and cultural events, are already dead because of Covid-19.

If their income drops, or the job can be done remotely, many people aren’t going to stick around paying through the nose for a tiny shoebox.

As a native New Yorker, Manhattanite, I will tell you that if you close the restaurants in NYC, you are closing down the food supply. NYC workers don’t cook, they eat out. There are very few supermarkets of any size, most NYers consider a deli with takeout a grocery store, but it is really a restaurant. When these places are forced to close, it is a LOUD message to get the hell out of the city.

As a NYer we’ve been overdue for a correction. Too much foreign-money real estate speculation, too much “hustler” AirBNB get rich quick schemes, too many aging millennials who need to start thinking more about living in a good school system instead of a good bar& resutraunt scene.

New York was going to contract anyway. What the pandemic is going to do is turn a gradual 5-year unwinding into a shock 1-year correction as everyone runs for the exits at the same time.

Funny how SoCal/NorCal is not on the list above, wonder what that market looks like in terms of delinquencies. Maybe these “invincible” markets are immune to it just like they are with everything else so far when it comes to demand, prices…etc

I don’t know about other states, but California gave everyone who qualified a 90 days forebearance, so things might get ugly soon.

I would guess about 20% that could have paid their mortgage didn’t, and just kept it invested, or earning interest, just because they could.

“Earning Interest?” Where?

They All bought Tesla stocks with the money and now they are good for 9 months more :).

Wells Fargo is losing money, their stock is down over 50%. Lending on real estate is a big big part of their business. Figure it out.

Also heard a comment from a suburban Atlanta, GA man that he had to go to 3 WF branches before he found one open. He also said BofA is closing branches there as well.

Interesting about Wells Fargo. They just closed down a branch that was located in the Vons market by my house. I’m in SoCal.

I wonder how that plays into this story: https://www.nbcnews.com/business/personal-finance/troy-harlow-has-always-made-sure-pay-his-mortgage-time-n1233635

Short version, Wells has been putting people into forebearance without their knowledge or request. Not clear how widespread it is, nor is it clear to me why they would want to do this, but that kind of behavior would mess with the numbers and it might be a sign of desperation.

Eh. Things are going to be fine. Inventory is down 44% with only 1.7 months of active inventory on the market in San Diego. Prices have risen 5-6% year over year. Simply put, there’s too much demand. If the shutdowns from Polio and Spanish Flu are any indication, things will be fine.

Yea, your right… I mean it is not like people need jobs to buy houses…. right? Record unemployment will have no effect whatsoever…..

San Diego is special and everyone wants to live in San Diego

I see median price in San Diego reaching a million dollar soon

This time is indeed different in San Diego

Sarc off

I lived in SD for 50 years and hated it the last 5. It is a crap place to live, and I feel sorry for anyone who has to live there. I lived in one of the nicest areas, but where I live now is 100 times better….

California May show up on these lists soon. I understand a new tax law will be up in Nov.3rd ballot for vote. Of course in language it is framed as something between the halves & halves not. And if you have it (property, home, etc), and think A family member should inherit, not without a little pain first for being so “lucky” here comes a new tax. I believe story said being cooked up In S.F.

Powder horn full and dry, have begun researching locations for retirement.

And looking at AirBnBs in desired areas

What’s a good area ?

I am in Socal and want to flee from here

BD how bout lexington or Allegheny highlands VA

Too late for the pebbles to vote. This trend will continue to accelerate as the current crisis is giving our so called leaders openings like never before to screw up the economy and sew up votes.

The requirements on no evictions mandated by all these states are going to have an impact on any small owner of rental property. I don’t mean those who leveraged up on Airbnb properties, that’s a problem of their own making. Nor do I care much about massive residential property owners who own a million condos, they can survive this.

Then, there is the inevitable increases in property taxes that are coming since all of the municipalities are starting to run out of money to pay their pension obligations. Illinois is just the first, wait until California and NY starts going. And of course, the ones who are going to get hit the most are the owner of single family homes and such. The businesses can handle this.

I wonder if one of the unintended consequence is to make the rich even richer, because they can leverage their capital to acquire even more assets and renters.

Lol, like property taxes matter in this case.

Buy gold. all else is moot. they have to

to print.

no wait, i think that deck chair would look a lot better a smidge to the left.

gold is at just over 100% over the 1980 price. $800 then > $1800 now.

think of all Of the massive economic growth in Russia, China, South America, United States, Europe, Africa etc. etc., couple that with the massive money printing, and how does all that relate to the change in the gold supply between 1980 and now?

Name one thing that has gone up just 100% in price in the last 40 years.

when gold rockets, it will mean the show is over. thanks for coming.

gold will be repriced to back everything. at the least, it will be a big part of it.

I agree, but keep in mind that when the shatner really hits the fan, everything is sold.

I’ll name a few –

televisions

Airfare

but generally – yes, inflation is huge, higher than reported

Implicit At first yes Gold could correct heavily if there is a big market crash HOWEVER it will most likely bounce hard and go to new all time highs once the FED and other CBs start more money printing(QE)

Try cigarettes, say 500% at least. Maybe hijacking a truckload would be easier than buying gold?

yeah, cigarettes apparently are a great money / currency. but silver is bulky enough, try storing / keeping cigarettes in the $1,000s for years… :)

house bought 2015 is currently TRIPLE RD,,, and nothing at all left for sale in hood, though one for rent for triple what it was 5 years back also,,,

land before that doubled b/t 99 and 14,,, etc., etc…

easy answer, eh?

Gold is great until the Govt decides they want to confiscate it.

Yes, it’s happened before here in the US in the 1930s.

Executive compensation, over 1000%.

“Name one thing that has gone up just 100% in price in the last 40 years.”

Real Estate…,certain blue chips…,

He did say in price… a can of coke or a gram of coke. take your pick.

@FluffyGato

if you think fear of govt confiscating ur gold is the reason not to buy it, you are definitely not thinking about this the right way.

1. Why do they want to confiscate it?

2. Will u be able to hide it from them?

3. What will be the price of gold after these shenanigans play out?

Gold must be ignored and verbally diminished until it must confiscated.

That’s the deal. If you are smart enough to get to this website, you should be smart enough to understand he reality of that truism.

Alberta Canada real estate outside of the core cities has gone up exactly 100 percent or doubled in price in the last 40 years.

Tell that two people who live in New Jersey

If I may borrow a sentiment from General Patton and apply it to the various bubbles in our economy:

No dumb bastard ever made a fortune by going out and risking his assets. He made it by making some other dumb bastard risk his assets.

Rephrase as you see fit.

“He made it by making some other dumb bastard risk his assets.”

This is basically the essence of all secured, collateralized lending.

So long as a lender advances no more than the likely post-downturn collateral value (say a 60% to 80% loan to current mkt value ratio), then even in a very bad downturn, the bank is shielded from loss by the 20% to 40% borrower down payment/equity buffer…the borrower loses everything before the lender is out any substantial amount.

It can be viewed as a sort of single asset CLO you can live in…

That is the true cost of leverage.

Doesn’t work as a principle when there are no buyers, whatever the sale price. Take a look at Spain and Italy, where there are banks still owning vast amounts of real estate from 2008/9 that sits empty still, and needs maintaining (or is effectively worthless if it was never finished), and costs property taxes.

Truckman…

My pt was to highlight the dynamics of secured lending (ie, borrower down pmt, etc, serve as cushion that must be burned through before lender takes loss, etc) not really say yea or nay to any given equity cushion level of adequacy.

I don’t think a lot of civilian borrowers really understand in depth how various legal loan terms work in practice to insulate lenders (and increase risk to borrowers).

Alternatively, there are plenty of Goofy lenders out there too who really don’t appreciate the dynamics of proper loan structuring…

MCH

Not sure if those property tax increases will come or if the Fed will instead go Brrrrrr and fund state / county tax shortfalls ?

If it gets put on the backs of property owners, then rental property owners have no choice but to increase rents to cover. At that point, politics will start boiling and supply of rental inventory will drop if rent control policies win the day.

That may not be such a bad thing, however, if apts get converted to condos and SFHs get sold at 3% loan interest rates to anyone with a pulse. At least the politicians will be able to say home ownership in the USA (or in their rent-controlled district) has gone up.

So will all those CA retirees in my state have to return home when the pension well runs dry?

:)

You can hope

MiTurn,

Nope, they couldn’t afford to return to CA, they will instead try to milk your state for benefits.

MCH,

California has Prop 13, property taxes are not going up.

More likely the public employee pension plan, CALPERS will go belly up when the stock market finally crashes

Gandalf,

Yep,

The only question is how, it will go bankrupt. Obviously, the stock market does have some real value, but, IF the stock market went down to 1/5 to 1/3 of current value, how would it get paid out?

According to pension precedent, even if the assets that back the pension plummet, the people currently collecting from the pension, will take the full original promised value until the pension is almost broke than the payout is reduced, until it goes bankrupt.

We have no idea when the stock market crashes, whether it will collapse to more or less than it should be worth. If it did temporarily crash hard, but, recovered to some extent later on, giving a full payout during this time would drain quite a lot.

The bigger problem is that after the stock market crashes, new and younger employees may not want to be a part of Calpers. All of this basically applies to most pensions.

The state may abandon calpers faster than people think (who knows), if it knows people forced into calpers would abandon the state. But realistically, we’re talking about California, they will do something ridiculous, that nobody could ever guess.

Gandalf,

Prop 13 is going to get taken apart in pieces, there is already a ballot I believe to try to repeal prop 13 for commercial properties in November. That will likely pass, because big business is evil, it’ll get vilified on how it is taking advantage of the state through an unfair law. And big companies should pay their fair share, and by the way the residential part of prop 13 won’t go away. Then, the easy part of prop 13 will be done.

The residential part is not so bad, because of turnover in the housing market. So, as the older generations die off, those pricing will get reset, and as houses are sold, then that’s done also. Some of that revenue will come in anyway.

As for CALPERs and the pensions going away, there is no way that the jackasses will let their base suffer like this. There are frequent requirements for bonds in various cities in CA to “support schools and teachers”, etc. The real reasons is always to sure up the teacher’s unions and get them money to prop up their pensions, jack up the administrator’s salaries, etc.

So, the day those things are allowed to die off without going through all the hoops to bail it out because of unsupportable promises made is the day that the Dumbos will gain total political power in California. In other words, it will NEVER happen.

The pendulum, ALL ”pendula (ums)”, swing(s) both ways M,,, in CA as everywhere, always have, always will.

There was a time, still in what’s left of my memory, when CA was a very conservative place, the birthplace of the Birchers if memory serves,,, and rural CA is still conservative in many place, some of which could be surprising…

Even good guv, Ed Brown, Jerry’s dad, was a conservative Dem, a breed now long gone, but formerly the majority in many states.

”The more things change, the more they stay the same.”

MCH:

“So, the day those things are allowed to die off without going through all the hoops to bail it out because of unsupportable promises made is the day that the Dumbos will gain total political power in California……”

Isn’t that what the gov did for the gangster banks in ’08-’09?

So, a bailout for your guys is ok….but not for the “other guys”??????

Why pick on the “…unions, pensioners, etc….”????

VV,

You left out Nixon and Reagan, who both started out in California politics.

Reagan today would be considered a moderate Democrat, Nixon a left of center Democrat.

Facts:

Reagan signed into law such Federal guvmint control horrors like a gun control law in 1986 that finally banned private ownership of full auto machine guns manufactured after 1985. And EMTLA, an unfunded Federal mandate that forced hospital ERs to treat indigent patients who showed up and refused to be transferred (before EMTLA, it was totally OK for a private hospital ER to just turf indigent patients to the city/county hospital regardless, like this guy who had been stabbed in the back at my medical school private hospital and got turfed to the city hospital with the knife still stuck in his back).

Nixon signed the landmark Clean Air and Clean Water Acts. He did Federal revenue sharing with cities and states. He proposed in a speech in 1974 a National Healthcare system which had EVERY MAJOR ELEMENT of what later became Obamacare. Google that speech and read it, I kid you not. So Obamacare should really be called Nixoncare.

2 of Nixon’s 3 Supreme Court appointees voted FOR legalized abortion in Roe v Wade

Neither Nixon or Reagan cared too much about balancing the budget. They were early adopters of MMT.

And of course, both were sooooo suspicious of Soviet subversion of American democracy and government, as was the rest of the GOP. That’s the part that is now incredibly weird how that’s flipped 180 degrees just cuz the Russkies managed to get their own man planted in the White House

So, to paraphrase Ronnie, who I voted for, Nixon and Reagan didn’t change, the country changed, and moved away from what they stood for in their time

Perhaps, but if you take a look at a place like Hawaii, there has been no real swings in 40 to 50 years. The state has gotten worse in many ways.

I for one would be happy to see more conservative jackasses and more liberal dumbos. I liked Jerry in many ways, he was a massive improvement over Arnold. It also helped that he had a crisis to work with. I am just not sure with Gavin, so far his crisis management hasn’t been too bad, he certainly didn’t preside over a disaster like NY. But let’s see what he does when this crisis ends. On the other hand, he had the good sense to kill off high speed rail.

At the end he’ll face the same structural problems as before, the question is how beholden will he be to his base.

@S7

Bailout of the banks was not ok. I understand the reason why they did it. But people should’ve gone to jail for the mass destruction they caused.

In CA, the problem I have is with the jackasses controlling pretty much the whole government, and that they fed their own little special interest to make them so bloated that it’s funny. And what do you hear every year from the people at the teacher’s union, the same damned thing: “more money, for the children.” And now, it’s about “racial equity… blah blah.” None of it is credible, if you read between the lines, it really is “more money for us, because the jackasses (and probably the dumbos before them) made promises that can’t be kept. But if you want to be in power, then you’re beholden to those interests. It’s why a state like Illinois is so deep underwater. Talk about taking from the future and funding the present, these bozos in the teacher’s unions and the public service unions are the worst.

By the way, this doesn’t mean I’m against unions, I think in certain places where corporate power has gone out of control, unions are a necessity. But you know the funny thing, I don’t see those same jackasses who go to bat for the teachers unions at every single turn eagerly demanding unionization in CA for Apple, Facebook, Google, and so forth.

I wonder why.

In case

If the whole work from trend becomes permanent, alot maybe most of the richer employees (of private companies) will be leaving California. If you make 100k, why struggle in California, when you can own a lake house or ocean house in another state with ease.

Another big problem is that, those tech companies aren’t going to make as much as they are making right now, forever, especially, once the yearly phone/tablet/laptop upgrade is too small for most to notice, this is only a few years away (arguably, most consumers won’t notice after the upgrades this year). The exorbitant fees for things like database software or other tech industries in California, won’t last either. These companies will also need less employees as possible improvements dwindles, and I don’t see any of them keeping their headquarters in California. Prop 13 repealed or not, big businesses arnt going to pay the taxes the politicians in California want them to. Even Musk, says he is considering leaving. It’s not just taxes.

Prop 13 is toast. I doubt if it will last the year. That money CALPERS owes…… the CA taxpayers are on the hook for it… The taxpayers have to pay for whatever shortfalls CALPERS incurs. CA is destined to be the next NJ or Illinois.

It’s a consequence of our “free market” system. Every disruption, every catastrophic event, every recession is an opportunity for the capital class to extort and steal from the poor and middle class. Events such as these only accelerate the inevitable outcome.

They have actually stolen less than people would think (it’s still very eviil), they mainly bid up the prices up assets that are easy to own (like stocks, if the stock market crashes, the dumber rich, will be alot less rich), because, they have no better place to park their piles of money. This effects economy, differently than most people think. The bigger issue is that they screw up the economy, in the process. If the economy wasn’t screwed up, they would be better off, as well. Some ways the rich get richer, though, are far more sinister.

All those REFIs and HELOCs for whatever reason now don’t look so great. Vacations, vehicle purchases, renos, debt pay downs, plus just buying over built and over priced housing are unfolding nightmares in this environment.

Sure, some folks were complicit, but many many were just living by what they thought were the fair and accepted rules of the game. This is a terrible time for many folks.

The winner is not in doubt when only one team is allowed to move their goalpost at will.

Thank you Paulo!!!!

Interesting data point: I live in Colorado, I went to dinner with a friend last night. He got laid off a couple months back, put his mortgage in forbearance, then decided to sell the house since he has a good amount of equity. Sweet deal for him: saved a couple months of mortgage and gets to cash out. Put it on the market on a Friday, by Monday he had 5 offers, he took the one that was $30K over asking price. This isn’t a starter home – Zillow shows his estimated value over $600K, that’s a serious mortgage payment. I’ve seen so many signs going up around here and then “Under Contract” shows up shortly after. I’m at a loss – some huge part of the US is in foreclosure, 10+% unemployment, and yet houses around me are selling like crazy.

Rock Hard,

Give it some time.

BTW, the two months mortgage payments weren’t free money. Your friend had to pay off the mortgage as part of the sale, and guess what, those two payments were still part of the mortgage that he owed, and that he paid off from the proceeds of the sale. Forbearance only provides a delay — in his case of only a couple of months.

Essentially a free Bridge Loan.

Your friend didn’t save a “couple months of mortgage.”

For the house to be sold, the mortgage has to be cleared.

Which means the mortgage will be paid in full, to include the forbearance amount with interest.

Yep, but mortgages in this forbearance did not have extra interest added to them; people had up to 3 months of typical payments.

Not just the forbearance; depending on where you live, for a fixed rate mortgage there are penalties for paying it off early unless it’s an open mortgage or a floating rate mortgage. If it’s a term mortgage/closed mortgage, (e.g. 5 years) and the interest today is less than when the mortgage was taken out (this is probably the case because recent interest rates are less) the penalty becomes the difference in the interest rate for the balance of the term.

As a hypothetical example, 2% lower interest rate today for a 300K mortgage paid out 3 years early would cost 18,000 dollars.

penalties for paying the mortgage early? no way. i have paid off two 30yr fixed rate mortgages and never had a penalty.

henri:

“unless it’s an open mortgage etc”.

There’s also IRD, Interest Rate Differential, if the rates go down.

I was hit with the 3-month penalty many years ago when very young, but none since. Understanding what you’re signing is important.

But people do get caught. There’s a recent example in Canada in the news where someone who is a lawyer and a real estate salesperson got hit with 30K IRD penalties despite their qualifications. Probably they had accepted the terms because they were getting a better rate at the time.

Open mortgages have a higher interest rate.

Not accurate for GSEs back mortgages, fha, va. Which covers majority of mortgages. Not sure about the rip off reverse mortgages.

Same thing in the local market here in NoVA. Coworker said his wife has sold more houses already this year than all of last year. On reddit r/realestate there are all kinds of stories about people going to open houses and the lines being around the block (socially distanced, of course.) Crazy number of offers, many bids. Reports of this in a number of states. Where I’m at if it’s under $800-900K and isn’t grossly overpriced it moves fast. The townhouses and apartments listed at the top end of the market not so much perhaps.

Trying to figure out where the money is coming from and I hear things like people living in apartments that want to move to SFH to get away from density, or people stuck at home due to COVID that want more room. But that doesn’t figure the money supply side. I am baffled.

Been on the sidelines so long, and the homeowners always get bailed out. If I had a place I would do 1 year forbearance and dump all that into principal if you can.

That’s not how forbearance works.

You still owe the money.

With interest.

“If I had a place I would do 1 year forbearance and dump all that into principal if you can.”

Nothing makes any sense in this market anymore. Not stock, not housing or anything with asset attached to it. Think like an insane person then perhaps this “trend” makes sense.

As Wolfe used the term “Extend & Pretend” maybe that’s what is going on now.

Alice in Wonderland: she was the only one sane in a world insane.

be Alice, because ‘they’ are throwing the book at us now.

“Think like an insane person then perhaps this “trend” makes sense.” Since none of this makes any sense to me, does it mean that I’m the sane one?

Nothing happening today is new, it is simply following the patterns of the past as these quotes from the great depression clearly show….

“Instead of judging the market price by established standards of value, the new era based its standards of value upon the market price. Hence, all upper limits disappeared, not only upon the price at which a stock could sell, but even upon the price at which it would deserve to sell.”

– Benjamin Graham & David Dodd, Security Analysis, 1934

“As in all periods of speculation, men sought not to be persuaded by the reality of things but to find excuses for escaping into the new world of fantasy.”

– John Kenneth Galbraith, The Great Crash 1929,

Every time I see individual anonymous anecdota like this, I click on my browser favorites list…

https://journal.firsttuesday.us/home-sales-volume-and-price-peaks/692/comment-page-1/

So, aggregate CA SFH sales data reporting a 40% year over year decline vs. your…”Dear Penthouse” bidding war story.

N. VA DC insulated Swamp bubble or not, I’m calling BS on your “Co worker”

He read it on Reddit… so it must be true. E

You are welcome to call BS on whatever you want, all I see in the market is low end (under $1mil) houses going fast. And yes coworker is truth. There are a lot of 1.5 to 10 million dollar homes that don’t seem to move as quick. Ive been on the sidelines for years, really missed out.

I also noticed 4 different friends on facebook just bought houses, they had been renters.

Bigest problem for realtors in rural VA is to few listings cause they sell every one.unfortunatley makes it tuff on us locals as what many see as a bargain is way overprised to us.when I travel to waynesboro area or even raphine near lexington via backroads Im mystified at the expensive holmes being built just how many of the 1% are there?

Where’s nova?

“Northern Virginia” – Washington D.C. area.

From that perspective the hot market makes sense.

Chinese ghost-city paradigm investments. Many of the homes stay empty for years and years. Also now Hong Kong investors. Also, I strongly suspect bailout money found it’s way to larger US RE investors, some of whom are owned in a large part by foreign interests.

If it continues the wealth gap will be unbearable and anger will grow… As it is a lot of our workers are homeless. Even those working full time.

The US should restrict foreign ownership of more than one or 2 homes, especially if those homes are not being lived in OR rented out. BC, Australia and others have begun restrictions to protect their housing stock.

How much of our housing stock is foreign owned and empty? No one knows. In some areas of NYC and LA people have said it’s obvious- large condo buildings with the condos all sold but very little occupancy. A small town near me on the west coast has so many empty buildings and houses that they can’t keep a volunteer fire dept going very well- all the younger people have had to move out because they can’t afford it. This isn’t just in the US- it’s a world wide problem in popular areas.

In regards to Hawai’i, I’m a little surprised that other areas in the state didn’t show up on the list especially on Oahu.

Tourism in Hawai’i is basically dead with tourism ‘reopening’ pushed back to 1 September:

“Ige said Monday that the state will wait until Sept. 1 to begin a program to allow passengers with approved negative COVID-19 tests taken within 72 hours of their trip to Hawaii to bypass the state’s mandatory 14-day self-quarantine for out-of-state passengers.

Ige said an uptick in coronavirus cases in Hawaii and huge increases in some mainland states led government officials to reassess the plan. Ige said he’s also preparing to extend the mandatory 14-day self-quarantine for out-of-state passengers to the end of August.Ige said Monday that the state will wait until Sept. 1 to begin a program to allow passengers with approved negative COVID-19 tests taken within 72 hours of their trip to Hawaii to bypass the state’s mandatory 14-day self-quarantine for out-of-state passengers.”

The state’s visitor industry, which supplies 17%, or the largest share, of the state’s GDP, began free-falling after Ige ordered a 14-day travel quarantine for out-of-state arrivals starting March 26.

Visitor arrivals fell nearly 99% in May amid COVID-19 fears and government lockdowns.”

Hawai’i has had 22 virus deaths to date.

Ige is the Govenor of Hawai’i.

Latest data shows mixed reults from the RE market with sales down and prices up for houses, but down for condos.

And with regards to rents in Hawai’i IIRC there are few what are termed ‘apartments’ for rent, but a huge number of condos which skews the rental price data.

Many of those vacation rental units in Hawai’i (usally termed condotels) currently have basically zero income and pay a huge amount of real estate tax compared to normal rentals.

(The rates are $13.90 / per $1K assessed value (as of 7.1.2019) for condotels, versus the residential tax rate at $3.50 / per $1K assessed.) value.

And finally while mortgage interest rates are low the acutal carrying cost of condos/condotels in Hawai’i is huge.

The Ilikai, a popular condotel, and the one that is shown in the original series with Steve McGarrett (Jack Lord) standing on the building has a HOA fee of about $700 per month, taxes of around $600 a month, and then the other associated costs of ownership for a one bedroom unit. And the Ilikai is acutally cheap in comparison to many others.

Just down the road from it is another building called ‘Discovery Bay’.

A one bedroom unit there will cost you about 1/4 the price of a unit in the Ilikai. (Ilikai units are freehold, but Discovery Bay is leasehold with respect to the land. You don’t own all of it, but lease it month to month.)

A recently listed Discovery Bay one bedroom unit will cost you $407 a month in lease rent, HOA fees of $755 a month, and property taxes of taxes of $159 a month (it is residential). So just those three items will cost you around $1300 a month before the mortgage………….

And for those that are interested a one bedroom unit in the Trump Tower Waikiki will set you back well over $1 million. One currently listed is priced at $1.48 million (twice the floor areas as the Ilikai and Discovery Bay at 1138 square feet).

The HOA fees on that unit are $1890 a month, taxes are $1835 a month. Tenure is feee simple.

So with the current state of the tourism market in Hawai’i I guess it is just a matter of time until numbers start to get worse for mortgages and prices…………..

The nice thing about Hawaii is that no matter what, you’ll always have your beaches. And if there aren’t tourists around, hey, the locals can enjoy the beaches without the overcrowding.

And if things get tough, don’t worry, the state government will always be there to bail out those who keep them in power. The jackasses in Hawaii know how the game is played, the dumbos don’t have a chance there, haven’t had it in forty years, (Lingle doesn’t count, she was a freak accident, but was soon put in her place), and won’t have it at least until the end of this century.

Ilikai, can’t believe that building is still there, but then most of the building along Ala Moana blvd has been there for a long time.

The Ilikai is one of the buildings in that has actually had good returns over the years.

Great location and name value.

The ‘one-bedroom’ units are IMO not really that nice, but the two bedroom ones are. Of course you are going to pay through the nose for those two bedroom units and the carrying costs are much bigger too.

The one-bedrooms are IMO more like a big studio type unit.

As you probably know in the ‘good ole days’ Hawai’i real estate used to have some really good price swings.

The condo we usually stayed in went from around $125,000 up to $300,000 and then back down and up again in a period of 15 years or so. The units now sell for around $400,000 – $450,000, but that now includes the fee simple land which you could have bought for IIRC somewhere in the $150,000 to $200,000 range which means that the actual price of the units hasn’t changed much in the past 30 years or so.

What has changed is the HOA fees inthat building have skyrocketed from around $100 a month to around $800 a month.

Another item that has also changed that has impacted owners is the myriad of changes to rules for renting out condos and units and the huge increase in taxes on rentals.

Hawai’i is too expensive, too little return, has had a government that has socked the crap out of real estate owners and in general totally incompetent at all levels.

Take a vacation to the islands in the Caribbean. They are better value, have better service, the people are nicer and they need the business more than the dolts in Hawai’i.

Real estate is better value, the taxes and carry costs are cheaper, and the beaches are nicer too.

My wife grew up on Maui and has been following all her old high school classmates on Facebook. Everyone of them is happy to be rid of the tourists. They don’t miss their mindless tourist jobs and are happily living off the land, enjoying the beach and turning in quarantine violators. They have recently begun to “reclaim” property owned by absent mainlanders. Some folks who think they own a house or property on Maui might be surprised when they finally return to a locals repo.

“are happily living off the land”

Are property taxes payable in coconuts in HI?

Who’s gonna collect em, the Maui county Sheriff who is in the same high school class?

Hilarious, glad to see property rights no longer “matter”. Wondering if the tune will change if the shoe was on the other foot for those enlightened folks.

When did they ever in the US. It is not like the indians sold the land

Property rights matter when you own the property.

But point Cas, it certainly didn’t matter when it came to the natives way back when.

Maui has always been different from Oahu.

It seems/seemed that lots of ‘new’ money went to Maui especially in the condos on the beach and the expensive homes up on the ‘hills’.

And as far as those locals being ‘Karens’ well, I guess that when push comes to shove they’ll have to ‘live off the land’ as they won’t be getting any imported food or fuel as they won’t be able to pay for it.

And as far as a tourist destination, even if I had the ability to leave Australia for a trip overseas (The Australian government has blocked Australian citizens and that includes dual nationals from leaving without a ‘valid’ reason such as medical, legal, or compassionate grounds and the process to get a ‘permit’ takes a long time. So we are just like people in the former Soviet Union here.) I wouldn’t be going to Hawai’i.

Barbados, BVI, and Grenada are better value and have a better environment.

They are also probably happily collecting unemployment.

I suspect the happiness is concentrated in the set if people who don’t directly profit from tourism.

A white collar worker or retiree might well be delighted.

However, even they may change their minds when the state moves to fill its gaping revenue hole. Tourism pays an outsized tax share, no surprise. Tourists don’t vote in local elections.

My neighbor – as in our yards share property line – just listed for sale at a healthy 33% above what I paid 4 yrs ago. The listing boast wonderful outdoor entertaining. I agree, seeing their yard and outdoor cooking facility and 3 season detached summer room. But it send oblivious to push that with Covid, plus I don’t think that’s a thing with millennials? Am I wrong?

It will probably sell in a day with 50 offers.

Dear Penthouse,

You are never going to believe this but during an open house to sell my SF pied-a-terre, two long legged Swedish exchange students with platinum tresses walked in and the taller one…after wetting her lips…quietly whispered, “We would like to double your asking price,” her breasts heaving.

“No, no!!,” the more petite Swedish speculator ejaculated, we must wait for Mamma!”

Just then, a stylish 40 something blonde in a strapless gown feverishly strode in to my open house, huskily breathing out, “I’ll triple the asking…”

lol! Well played.

33% higher than 4 years ago is a pretty weak return. That’s about 7% a year, nothing to write home about. In my village (as Wolf fondly refers to it) houses are selling for 30% higher than what people paid 2 years ago. 4 years ago pricing is 75% higher in the most sought after neighborhoods. It’s not millenials, per se, it’s refugees from big cities of all ages. I figure every night of rioting in Portland is a 1/2% increase in the value of my real estate holdings. I don’t want this craziness to ever end.

Right on Guy. I’m holding out for 20%/month. It’ll be sold before I list it.

Yeah, that’s hysterical!! All that rioting!!! Har!!!!

Next headline: “Airliner carrying urban escapees runs out of fuel and crashes into heavily mortgaged house taking out auto next door secured by subprime loan for unemployed tenant living on borrowed time! Tesla electric ambulance rushes to the rescue.”

“Tesla Electric Ambulance”

I was at their ’67 show at the Cow Palace.

Heavy, man, heavy.

Great news! I’ve been looking forward to affordable housing for a few years. It’s around the corner given that the extra $600 / month UE compensation is also ending.

That will bring consumption permanently lower, hitting business owners and white-collar employees harder. Wow, pandemics are such deflationary tsunamis.

I think that I would like a bit of deflation.

Yep, I’ll take a bit of deflation myself.

So will this lead to another 1000 points upside in the Dow? Whoops, made a decimal point error. I meant 10,000 more Dow points. All we need is the every other day goods news on vaccine progress. Right? Right?

Next vaccine I heard will be primarily made of Mercury. Really effective, stop the infected from long term suffering, also stop it from infecting others. Minor side effect might include instant death but 100% relieve for ICU capacity. Think of the demand it will create in the casket and funeral home industry as well. Better start buying up those stock now before market realize and rally hard on it..

Dear Phoenix_Ikki

Even better news, it is becoming clear that the antibodies that you get after having the virus don’t last very long (like all corona viruses) it means you can catch it again after three months (as some have)

The great news is we may need three or four vaccinations a year to “be safe”… Think of all the mercury you could sell…..and how many times a year you can die……smashing

Look at the bright side: Banks soon report earnings. The internets say they should be a disaster. That ought to send stock markets to explosive rallies. Then they can buy real estate and we all can become renters.

Meh. I bought stocks in the most corrupt bank around here who also happens to be “systematically important”: Danske Bank.

At 84 DKK on billions of Russian money laundering, this was well worth it.

Expect Governments to erode property rights even further. I always laugh when I hear about the U.S. having “strong property right”. Not true, not any more anyways.

Check out “AB-1703 Residential real property: sale of rental properties: right of first offer” – this will make it VERY difficult to sell your rental property in California. You may have to spend up to 12 months waiting for some “government approved entity” to accept (or not) your offer before you can sell your property. Already passed Assembly.

Then there is “AB-1436 Tenancy: rental payment default”, which will allow tenants to delay paying rent for 12 months for rent until April 2021. Already passed Assembly.

So if you are a small landlord, California government will force you “legally” to bleed money and go bankrupt while they take their sweet time to take (ahem, “purchase”) your property at a much lower price in a year. It’s a clear conspiracy against property rights from the People’s Republic of California, soon to spread across the nation. Don’t say you weren’t warned.

And there’s already AB1482 (it’s the law in CA), the rent control that caps rent increases to a hard 10%. So if (and when) inflation hits 20-30%, you are so out of luck, while still having to pay for mortgage, ever-rising property taxes, insurance, HOA, maintenance, repair, turnover and management fees (unless you manage yourself, which I don’t recommend unless you enjoy facing off angry jobless tenants), not to mention the Government revoking your right to evict non-paying tenant.

In short, if you are buying a rental property in California, you are an idiot.

Cry harder.

You’re just looking at buying rental property from the individual property owner’s perspective. That small business stuff is dead – today you have to think big like a hedge fund or like Wework.

What you do is get a corporation or a REIT going, raise lots of money from investors desperate for income, borrow all the money on it you can, and buy up rental assets. Make sure to pay yourself handsomely while it works. If you’re cash flow negative, just focus on sales growth to raise more capital. If the market crashes or the free money runs out, and you don’t get a bailout, then you just start a new fund, sell all your good assets to it, and BK the old one after the minimum timeframe shielding those asset sales from questions in the BK proceedings. Perhaps you can use your new firm to buy some of your old firms debt for pennies on the dollar to ensure that you take part in those proceedings.

That’s how our modern “capitalist” system works – you’re either big enough to access gobs of cheap money or you collapse from the next government-driven crisis.

Currently 60% of rental units in California are mom-and-pop small landlords. Converting that into institutional investor REIT of some sort will take ENORMOUS amount of money, and more than anything a MASSIVE crash in pricing.

If you look at rental prices in CA, and what it costs to buy the same rental, you’ll see that you’d need to get a spectacular discount on the price to even break even.

I guess that explains why there’s no massive rental buying in CA, by anyone really. I can attest that small landlords are itching to sell, but not yet. Maybe covid19, maybe fear, maybe just waiting for tenant to move out. And I don’t see BlackRock or some other company buying either.

Btw, current (and proposed) laws in CA are EXTREMELY landlord unfriendly, regardless of your size. The government is going after landlords with a socialist fervor never seen before in the U.S. (maybe except for NYC, but that’s crazy town). For big investors to get into CA, literally everything else must dry up, and I don’t see it happening.

Rental market in places like CA will remain near comatose for years to come, or at least until crazy-eyed policies are gone. Which may never happen.

I left CA years ago but still have a few rentals there. I’m only staying for now by inertia at this point, but if a good opportunity presents itself, then adios. I worked for a major buyer as a contract RE agent, and can tell you the appetite for rentals in CA is gone, and may never come back.

I too advise anybody thinking of buying in CA to look elsewhere, or just don’t do rentals, big or small…

As long as the vast majority is renting, and those rents are sky high compared to incomes – particularly in big cities with outsized political influence- you can expect policies to continue to be landlord unfriendly.

I think you’re right about exiting the rental space. Politics tend to amplify upward price trends through building restrictions and excess lending, and then amplify the downward trends as taxes and regulations skyrocket while public services get squeezed.

I advise you not to take offense from the lack of sympathy landlords will get from those who had their hopes of homeownership crushed. Just realize that the system itself is broken and we’re both pawns in someone else’s game.

Haha, this is so California. Thanks for bringing up these, never saw before. And I figure if they fail the first time, the jackasses will just keep trying.

The perils of one party rule, This is what happens when they are given the run of the place. It doesn’t matter if it’s dumbos or jackasses, they are all bad if they are given overwhelming power.

The perils of two-party rule as well… little real difference between Democrats and Republicans on the National level, although I will concede that Republican-led States seem to be run much better. This from a JFK Democrat, a species as dead as the Dodo.

Two party rule would actually work if we’re talking a reasonable purple state. When both parties have to actually fight to get their constituency to vote for them, that’s where things get interesting. I am looking at it from the state level.

I agree about the problems with the dumbos and the jackasses at the national level, they are literally in it for the power. No one can look at for example what happened to Garland and call it fair. Yet the same chubby who blocked him for years would happily ramrod through a nomination today if another opening occurred on the bench tomorrow.

Right now, the country is so split that it’s easy for any of the constituent group to be just taken for granted, because they are always going to vote in a bloc for one party. It’s just sad.

You just have to take a look at Biden’s comments on one of his key constituent blocs to know that he doesn’t care one bit about them, (it doesn’t matter what his mea culpa are) he thinks they’re locked solid in his corner, 90%+ will vote Jackass, so he panders to them a little, tossing in a few words here and there, but then when the chips are down, those 90% are just left behind, and they’ve been left behind for decades now.

The dumbos look at the same bloc and decide there isn’t a way to get at those votes, so why try. Who suffers? The ones that voted in lock step for the jackasses for the last thirty plus years. It’s a tragedy, and yet it keeps happening year after year. This is true of a whole lot of groups.

Until either a credible third party comes along, or there are leaders among those groups who realizes that they need to stop being pawns, the situation will persist.

Lara, put more simply: if you’re small, you’re screwed.

Tenants are in forbearance forcing landlords into forbearance. There is no forbearance for property taxes, insurance, HOA fees and necessary repairs.

With Tropical Storm Fay we had six named storms formed by the earliest date ever recorded. Property and auto insurance premiums are higher in my area. Storms tore off roofs, rains poured in and toxic mold formed. Cars were dented by flying debris.

But at least it’s tangible property, unlike cash in the bank.

“unlike cash in the bank”

Nice.

It may not be too many years before employees ask to be paid in Yuan, bitcoin, or gold…the DC dollar being as dead as the Confederate dollar.

And how could DC even laughably function then?

A large portion of the 8% of mortgages in forbearance might be the result of opportunistic behavior. When the government is providing giveaways, there’s a chance homeowners might get some mortgage relief in the form of outright forgiveness or interest rate reductions. Thus, why pay down your mortgage in that environment?

If I had a mortgage, I would have explored forbearance for this reason.

You need to submit paperwork to show that you have been impacted.

“You need to submit paperwork to show that you have been impacted.”

LOL. Come one man you’re not really this naive.

Dear Mortgage Company,

Covid really hurt me financially. Like really badly. Please give 120 days free mortgage.

Sincerely yours,

Joe Shmoe.

That’s the extent of the “paperwork” you need.

You are the one who is naive. Banks are not the cleverest, but they are not that stupid either. Will there be some frauds? Sure, just like the PPP, but most regular people will try to provide some real docs. I do have friends working in Wells Fargo, etc, after all.

And anyways, this is forbearance, not forgiveness.

You are 100%. Where are you getting this from?

May as well see, especially if one didn’t take out any student loans. If you’re not getting s bailout of some kind you’re not trying hard enough and being played for a sucker.

The rub is, the people who do that will probably spend part or all of that money on consumption. Depending on their agreement, they may be on the hook to repay that owed money rather than have it added on the back of the loan. I am sure few people read the fine print on the forbearance paperwork. The money changers have a long history of making desperation work in their favor……

Before covid hit there was a lot of money on the sidelines.

That money was not spent.Now with the reserve currency

depreciating it’s time to invest even if you don’t want to.

Of course people are running out to buy a house. Rates are super cheap. I am doing a refi, why? Dropping to a fifteen year, at 2.5 percent. 70 percent drop in interest paid per year.

And everyone is expecting inflation?

Inflation will only hit things with demand.

And everyone thinks asset inflation will continue…..

Yeah like bread and milk and sugar and coffee and gas and rent and utilities and fees for everything and…

Brainard at the Fed said today the Money Printer needs to go Brrrrrrr……weld the switch to full tilt on and buy hard assets. Everything the Fed said it would not do it has done except NIRP. And NIRP is next. Only a Paul Volker type has the grit to not cave when the crying and moaning and snot slinging starts when extend and pretend ends. Jerome ain’t no Paul Volker. Jerome will fold faster than Bernie. Americans will realize what this means when the Dollar hits 80 . Until then they will have blind faith in the magic of the Fed “printing” the economy.

DR DOOM,

What Brainard actually said:

“With the restoration of smooth market functioning and credit flows, our emergency facilities are appropriately moving into the background, providing confidence that they remain available as an insurance policy if storm clouds again move in.”

“With the policy rate constrained by the effective lower bound [no NIRP], forward guidance constitutes a vital way to provide the necessary accommodation. For instance, research suggests that refraining from liftoff until inflation reaches 2 percent could lead to some modest temporary overshooting, which would help offset the previous underperformance.”

Yield curve control but with fewer asset purchases:

“… there may come a time when it is helpful to reinforce the credibility of forward guidance and lessen the burden on the balance sheet with the addition of targets on the short-to-medium end of the yield curve.”

https://www.federalreserve.gov/newsevents/speech/brainard20200714a.htm

Wolf, I’m so glad you post in the comment section!

When we hit 10 Trillion or Negative Rates,I will jog your memory. In a polite manner of course.

I only corrected your interpretation of what Brainard said by quoting Brainard’s own words. That’s all I did. Those words I cited were Brainard’s, not mine. And I didn’t predict anything. I just corrected your interpretation of Brainard’s speech.

Brainard was being groomed for Fed chief in 2016. She is an extension of the role of Central Banker given to the Fed, the Yellen request for “authority to purchase a broader range of securities” which as events turned out, was unpresumptuous. Mere election year maneuvering, it did move the markets. IMO markets are on automatic here, and the incumbent, or challenger, could withdraw at this point and only cause a short bout of volatility.

Forbearance is a precursor to loan mods. Back around 2009 or so I began the process of having banks work with me on loan mods (several, and I got good at it). At first the banks didn’t know what they were supposed to legally do and how to go about it. Banks were failing left and right and loans were being sold here and there to whichever bank was appointed to take them, but part of the deal was that they had to modify a certain percentage. Regardless, they had to, by law, modify and work with folks. By 2010 and especially 2011 the banks knew what they had to do and I knew how to make it happen. We got mods on virtually everything we owned, sometimes at our behest, sometimes at theirs. Chase was the most interesting one in that they actually contacted us on their own offering 80k or so in removal of principal if we just signed on the dotted line in 5 days. I ran it by an attorney and we did just what they were asking for and it was the real deal. They had taken over WaMu’s stuff and knew there was no backing to anything they had so just wanted wet signatures they could sort of enforce should they have needed to. I think it was due to fear of the “show me the note” crowd. Another property removed (yes removed) 170k of principal of 550k owed and deferred 50k more to the end of the loan. 2% loan terms tiering up to 4.5 amortized across more than 30 years was the norm for those who could qualify and knew how to make it happen. Those were crazy times but these are crazier, way crazier. Back then you had every yahoo and his brother buying, but this time it’s mostly good paper so they know eventually they will get paid. The banks already know how to and have departments solely devoted to loan mods and they will be put back into use, whether by their good graces (HAH!) or by government intervention. Oh yes, good ol government intervention will save the day so invariably we are all doomed, but at least we can postpone it.

So my prediction is that you won’t see nearly the amount of foreclosure houses come to the market that people generally think will as many of them will be people who will fight and get their mod. Fringe areas and areas that simply don’t have anymore jobs will have really big housing issues, no doubt, as those folks will move or just up and leave the place for greener pastures. Nicer areas that tend to hold their value will see folks selling at market values and paying off loans and starting over elsewhere. The nicest of areas will probably do well as money is moving out of a lot of poorly run areas (think super blue cities with insane draconian laws) and typically, money wants to be in nice areas. That being said, all of my pontifications could be wrong and as Emily Litella used to say, “Never Mind”.

wonder how much % of market who saw price went down started the whole crisis last time around.

It’s said the current housing uptrend is helped by tight inventory and record high home equity. Wonder if that will buffer any downtrend this time.

Anybody here remember the prices the banks were selling foreclosed apartments and condos for in Texas in the mid-90’s during the big bust back then………………………..

(Probably most of you wren’t even born then.)

Give away prices.

Everyone can relax. We will soon have no flu, no Covid, 0.99% unemployment, greatest economy ever. For the internets are saying WH is taking over Covid infection reporting. Now we know for sure the flu will be cured and vanish. Just like when BLS reports unemployment by vanishing it, or just like when Jerome reports his 100% fraudulated propoganda inflation CPI, we will now have TRUTH reported to with Covid. IT’S ABOUT TIME!

I’m still hoping that the window is still open to sell my house in the mountains. After my deadbeat tenants trashed it, it still needs a bit of work. It should be ready by the end of the month.. they say the market is still good at this time, they say it’s because people are bugging out of the city. I’m selling as a fixer upper because of the damage. But the price is still good anyway. My feeling is, that it’s now or never. I’m of the opinion that time is running out, we’ll see.

Which ‘mountains?’

Hemmingway always comes to mind: “gradually, then suddenly”.

It’s what I’ve been saying forEVAH. finally the “experts” are catching on

PriceWaterhouseCoppers put out a report saying small cities is where it’s at when it comes to real estate. Big cities are dead. Kaput. Adios. Last one left turn out the lights. National numbers for real estate are meaningless.

There has been quite a bit of anecdotal confirmation of this. I have seen data on rents that also point that way and support that theory. It’s early, and we need to see confirmation, and we don’t know if this trend is just temporary (if it’s a trend at all), or if this persists. But if it persists, it would be a massive shift. Here are my observations about rents pointing at this shift:

https://wolfstreet.com/2020/07/01/rents-plunge-in-san-francisco-and-in-the-oil-patch-drop-in-other-expensive-cities-but-a-long-list-of-double-digit-gainers/

We’re managing to keep our units rented and are able to re-rent the vacated ones at asking price, however, there are, in my opinion, fewer prospects. I can’t speak for everyone, but my understanding is that most property managers have really risen their criteria to get accepted for fear of having to get stuck with someone who after three months says they can’t pay…it’s because of covid…mr landlord you’re screwed. San Diego isn’t a small city but it sure offers a lot so I think will do just fine. It appears we’re taking in a lot of folks fleeing from up north as well.

I live in Bend, Oregon, one of the smaller towns popular with fleeing residents of NorCal, Seattle, and Portland. Real Estate is hot right now across the price spectrum. Lots of Californians moving here, many paying cash. Prices are up slightly in June yoy. But with new listings down 20% yoy and inventory down 68%, what will happen to prices when new listings/inventory picks back up? As someone who is waiting on the sidelines to buy, I’m expecting (or maybe just hoping) that demand will fall accordingly with prices to follow.

San Gabriel mountains, Bob, someone earlier said that if you’re renting your house out in marxist California, that is foolish. I agree, so it’s take the money and run. I feel as though my property isn’t my own. They are trampling our property rights here.

My boss just bought a SFH in shorthill, NJ and he is moving from NYC. During his shopping period, he saw bidding war in every house he is bidding and the houses are selling fast.

So I don’t know how to make sense of it.

New Jersey is leading the country in COVID-19 fatalities per capita and has the highest property taxes in the US, along with Illinois. The state is number 44 on the U-Haul growth list. Illinois is dad last and California next to last. Not exactly enticing attributes.

Just wait. Fatalities are a trailing statistic. Florida, Texas, etc… are in the pipeline.

“Just wait. Fatalities are a trailing statistic. Florida, Texas, etc… are in the pipeline.”

I’ve been hearing this for months. And it isn’t happening. The new spike in cases is young people. Young people don’t die from it, in fact most young people barely know they have it. The death rate continues to fall while cases increase. This is the absolute best thing that could happen as herd immunity is finally starting to take shape.

Not that CNN will tell you any of this.

Just Some Random Guy,

Quit abusing my site to spread your INSIDIOUS LIES about Covid-19. Here are the spiking deaths in Texas and Florida and yes, they lag new cases by over three weeks, and as the number of new cases keeps surging, those deaths will continue to surge as well (click on image to enlarge):

Yes, let’s keep an eye on that. The age range of the newly infected will impact mortality data. Hopefully by now, states have in place policies to protect the most vulnerable, over 70 with pre-existing conditions, residents in assisted living and nursing homes. This past Sunday Face the Nation deer-in-the-headlights interview with the US Surgeon General did not establish much confidence in medical leadership at the federal level. Has Fauci issued guidance on protecting the vulnerable elderly population? Looks like cases in NJ may be heading up again.

“Hopefully by now, states have in place policies to protect the most vulnerable, over 70 with pre-existing conditions, residents in assisted living and nursing homes. ”

You are kidding right?

State and local governments have failed to protect those people in long term care.

North Dakota which has pretty good government at the state level, but some poor governments in the cities has had 72% of the deaths from the virus happen in LTC.

Other states’ stats are similar.

Mish had a nice travelogue on his blog a few days ago on his move to UT from IL. He had $15,000 property tax bill on $350,000 house, selling it for less than he paid several years ago. I think he lived in the far northwest exurb from Chicago. Denninger beat him out of IL by 20 years. He also was getting killed by property taxes back then, with house closer to the city.

“… less than he paid several years ago”

not exactly correct – I also browse his blog, and this one caught my eye, because it didn’t make sense – here’s a quote:

“We will sell the house for a lot less than we paid for it 20 years ago.”

This is what’s happening across the country. People are fleeing cities. Suburbs, small cities and towns are seeing real estate price surges. There is no mystery to it. There is also no real estate crash, to the chagrin of bears.

This people are fleeing the big city to bid up real estate in small cities canard does not hold water when you examine it logically. A very few may be in a position to do this but for most people to have the assets to buy a good place in an economically viable small city or suburb they have to sell the house in the big city first. Who is buying those big city houses at high enough prices to give the “movers” the equity cushion they need to buy a nice house. Then there are the renters in the big city. A few big city renters have the incomes and job mobility to move but very few of them have the liquid assets for a down payment on a house. I think most of the renters in the big city that leave town in the next few months as the eviction moratoriums come to an end will be heading for their parents basement in the heartland. Rents and home prices in the big city will drop but all that lost income and equity will be disappearing in to a financial black hole, not flowing in to magical small cities.

Stocks & Jocks podcast show based in Chicago area talked about this phenomenon locally past several shows. Tom Haugh, “The Chief”, has real estate broker connections who report many leaving the higher end areas of Chicago to move to the burbs past month or so. They all “want a nice yard”, but many have no children. I suppose that is a politically correct reason to state for making such a move; the property taxes are horrendous in either case, however.

very good thinking

Why would having or not having kids influence the need for a yard? I mean yeah if you have kids you definitely need a yard. But if you don’t have kids, it’s nice to have a yard as well.

For about 10 years we were told how millenials are changing everything!!! Nobody wants a home anymore. Everyone wants to live in a downtown condo with 172 restaurants, clubs and bars within walking distance. What these “experts” forgot was that 27 year old millenials in 2012 buying or renting these condos, would become 35 year olds in 2020. And at 35, your days of clubbing and bar hoping basically are over. And when that’s over living in a cramped apartment surrounded by homeless people and crime loses its appeal, fast. A home on a quiet, safe suburban street with a yard, maybe a pool…..pretty darn appealing. Kids or no kids.

2020 only accelerated what was already happening.

The effects of crashes do not hit the RE market prices for years. The effects of 2008 did not really cause prices to bottom until 2010-2012. Until the foreclosures begin, and begin to work their way through the system, there will not be any significant market impact.

If you are using a 3 mo. window as evidence of your position, you are sadly mistaken and will be proven so in due time.

RE is still a trailing indicator of the economy.

Please tell us if there’s a bidding war on his NYC house.

Most people can’t afford to maintain two places.

He sold his NYC apartment last year after big renovation. His household income can easily sustain more than 2 houses.

If one has half a mil in cash looking to buy a house out of the city, is it best to buy the house flat out or finance it fully or partially at low financing? Inflation has totaled about 17% since 2010, so where to put the cash safely? In the next ten years, inflation is certain and the dollar is a good bet to lose value on its own. Housing prices will inflate the same as the last twenty years?

If it were me I would put 20% down (100k) take 400k and invest in precious metals to hedge the inflation. Guaranteed to come out ahead. The Gold ETF inflows are nuts right now. It may seem like you are buying high but if your horizon is 20 years you will be happy you bought at $1800

It depends on your age and your kids age. If they don’t want the house when you die, there’s really no point in paying it off. Shield your assets from probate, and let the bank figure out what to do with it.

Ask yourself if you would pay $1.5 mil for that $.5 mil dollar house…. That is what you will pay for it if you finance it…..

Brant,

I have been mortgage free since my forties, and here is why I recommend it. One, my houses have always appreciated more than any other investment. Two, you never have to worry about losing your job. Three, you don’t have to do the politics required when an employer KNOWS you need to work. And most important….freedom. You want to switch careers? No problemo. While interest is low, debt is still a handcuff and always will be.

I paid off mortgage by saving and doubling up payments, and used sweat equity to improve my holdings. Plus, when it is all said and done not paying a mortgage every month is like getting a 2K per month pay raise. That extra cash could be used for investments as well. There is no better feeling than being independent and having some eff you cash in the bank, especially for a working guy.

I couldn’t agree more.

Not paying a mortgage is a truly liberating feeling!

One of our places will be paid off in 4 years and My wife and I are looking forward to it. We don’t plan on leveraging it again and are anticipating the cash cow it will become. I can see leaving some places leveraged and using them as the “sacrificial” ones to pay off the other ones, but eventually having everything paid will give us tremendous peace of mind.

“forbearance is a precursor to loan mods”. Maybe just maybe it’s a precursor to a jubilee . Crazy Nancy wants a 3 trillion stimulus bill. I was reading where all of the mortgage debt in the U.S. in around 3 trillion. Email your congress critter now!

I have a funny feeling this time around is going to make the Great Recession look like prep school. Jubilee is probably going to be an understatement for the money they’re going to be throwing at folks. There will be foreclosures a plenty but a lot of people will tap into the loan mod train and it’s a virtual guarantee that banks will have to comply. The mandate will start with all federally backed loans and go from there. Crazy Nancy is everyone’s Congress critter and third in line. If that doesn’t send shivers up your spine nothing will.

The suddenly part has already happened to commercial real estate where I am, I live in Europe’s largest marina on the south coast of England, 50 miles south of London. The marina is privately owned with about a thousand residential properties, all apartments.

The commercial properties were mainly eateries now all closed, Pizza Hut bankrupt, Cafe Rouge bankrupt, Zizis bankrupt, and six others all either closed or bankrupt, Rendevouz casino bankrupt, Cineworld closed, Bowlplex closed, loyd’s gym closed, I could list them all but you get the picture, its devastation, 90% of all commercial properties are now either closed, bankrupt or in bankruptcy proceedings.

There is one single place to eat left Weatherspoons pub, the marina used to attract several thousand visitors every weekend, last Saturday I counted 35 at peek time on the boardwalk, if the marina is a microcosm of the rest of the country we are all up sh#t creek without a paddle.

Appreciate your commentary and not faulting your investment choices. We’ve been there.