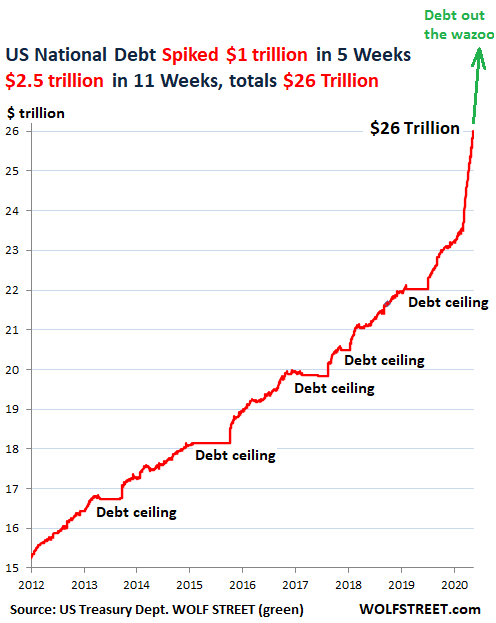

US National Debt Spiked by $1 trillion in 5 weeks to $26 trillion. Fed monetized 65%. Business debts spike to high heaven.

By Wolf Richter for WOLF STREET.

Trillions are now whooshing by at a breath-taking pace. The US gross national debt – the total of all Treasury securities outstanding – jumped by $1 trillion over the past five weeks, from May 4 through June 8, and by $2.5 trillion for the 11 weeks since March 23.

The total US national debt outstanding has reached $26 trillion, according to the Treasury Department. I’ve been fretting about this debt on my site since 2011. In recent years, I innocently added a green upward arrow with “Debt out the wazoo” to my gross-national-debt charts, unaware that this tongue-in-cheek label would turn into a factual, data-based technical term:

And think about this: The huge mountain of debt that took decades to grow to this gargantuan size has exploded by another 10% in just 11 weeks.

The curious flat spots in the chart are the periods when the national debt bounced into the Congress-imposed debt ceiling. During these periods, the government borrowed from federal pension funds and other internal sources – the “extraordinary measures” – to make ends meet, thereby continuing to borrow, and when the political charade was resolved and the debt ceiling was raised, bam, the debt jumped by hundreds of billions in weeks. Now the debt jumps by the trillions in weeks on a routine basis.

On February 19, when the debt had soared by $1.3 trillion in 12 months to $23.3 trillion, I mused: “But these are the good times. And we don’t even want to know what this will look like during the next economic downturn.”

Turns out, we didn’t get a regular economic downturn. We got the most epic and sudden economic downturn ever. And now we’re beginning to know what this looks like in terms of the US debt.

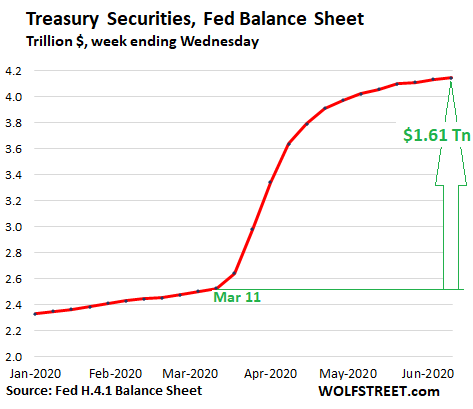

Fed monetizes 65% of the additional debt.

From early March through its balance sheet released yesterday, the Fed added $1.61 trillion in Treasury securities to its assets as part of its Everything Bubble bailout program. Over the same period, the US debt soared by an additional $2.5 trillion. The Fed has thereby indirectly – as is the rule in the US – monetized 65% of this additional debt.

But as you can see in the chart below, the Fed’s monetization of the US debt has slowed to a trickle in recent weeks, after the original shock-and-awe spree in March and April. In the week through Wednesday, the Fed has added merely $8.8 billion in Treasury securities, the small weekly total all year:

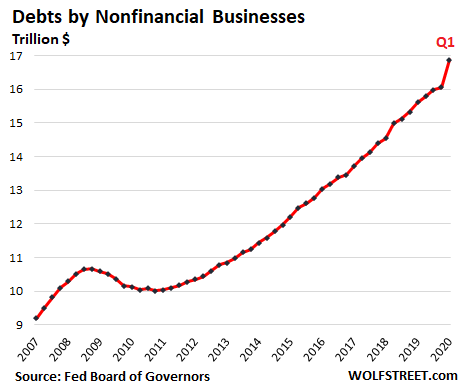

And then there is this: Business debts are skyrocketing.

Business debts already skyrocketed in the first quarter, according to data released yesterday by the Fed’s Board of Governors. In Q1, total “nonfinancial” business debts, which include corporations and other businesses but not financial intermediaries such as banks (that borrow to lend, and including them would result in double-counting a lot of debts), jumped to $16.86 trillion.

This was a 5% increase from the prior quarter, the largest such quarter-to-quarter increase in the data going back to the 1950s:

And for business debts, the second quarter is going to be a doozie. Businesses have sold enormous piles of investment-grade bonds and junk bonds in April and May. And this pace appears to be continuing in June. The Fed’s Board of Governors will report total business debts for Q2 in three months.

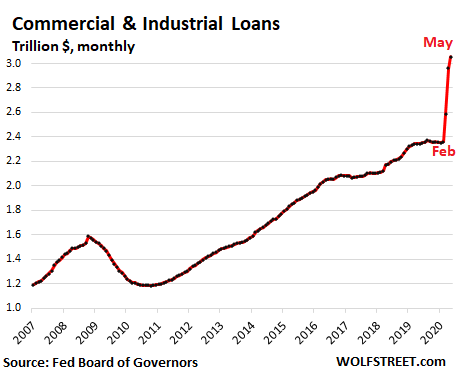

But we already know from the weekly banking report by the Fed Board of Governors that “commercial and industrial loans,” which are part of the nonfinancial business debts, have spiked by a stunning 29% in three months, by far the most ever, from $2.36 trillion at the end of February – and the end of the Good Times – to $3.05 trillion at the end of May (on a weekly basis, they have started to tick down since their weekly peak of $3.09 trillion in mid-May):

Households gorged less on debt. Municipal debt remains flat. But now everything has changed.

Household debts – mortgages, HELOCs, credit cards, auto loans, student loans, and other loans – rose to $16.3 trillion in Q1, another record, and up 12.4% from the peak at the early innings of the Financial Crisis in Q3 2008. Given population growth over the 12 years and inflation, in aggregate households were less vulnerable – until 30 million people lost their jobs over the past two months.

And with households, it’s not the “aggregate” debt that matters, but the debts of the most vulnerable 20% or 30%, which is where households are loaded up with debts, and this includes subprime auto loans and subprime credit card loans – and the mess has started to blow up even before the pandemic and before the 30 million job losses.

Debt by states and municipal governments, at $3.1 trillion in Q1, has remained relatively flat since the Financial Crisis, after having peaked at $3.2 trillion in Q4 2010. But states and cities now have a revenue problem of a stunning suddenness and depth.

$60 trillion in nonfinancial debts…

In Q1, total nonfinancial debt, including government debt at all levels, nonfinancial business debts, and household debts jumped to $55.9 trillion, according to the Fed Board of Governors.

And Q2 will likely add $3+ trillion in Treasury debt, plus the large amounts of business debts issued in April, May and June. All combined, total nonfinancial debts will approach $60 trillion by the end of June – having doubled in the 14 years since 2006. Debt out the wazoo.

No one was prepared for a collapse of the labor market like this. The data are all over the place. Two government agencies differ by 9 million unemployed. The jobs crisis bottomed in May. But “over 30 million” people remain without work. Making sense of the chaos. Read… A Word About the Chaos in the Unemployment Data: Week 12 of the U.S. Labor Market Collapse

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, which report and from what government agency is this data from?

For a while there, I thought we were looking at Chinese data ;)

It’d be really helpful to subtract off the portion monetized by the Federal Reserve (balance sheet).

Treasury doesn’t actually pay interest on the Fed’s portion, since they get the interest right back from the Fed (less expenses). That part is functionally the nation’s primary credit (today’s “money”) supply and not a national burden like the rest of the debt.

Only in that context, if one is trying to look/track at the total availability of HQLA available (and at what tenors) the subtracting out the 65% the primary dealers dumped on frbny, then ignoring that portion would be hindering that.

Irrelevant at this point, the Fed is an off balance sheet accounting gimmick for toxic securities, like Fannie and Freddie during GFC. They managed to save those agencies, and are now talking about privatizing them. After the banking industry collapses the government umbrella organization (FED) loses importance, like the secretary of Labor. We can close that one down too.

The balance is but a shoe box into which debt is stuffed and then pushed under the bed. Poof.

You should make Debt Straws for your beer mugs. You could write on the straws “US Debt.” Just like your chart, they’d pop out of the mugs in a straight line heading for Wazoo.

?

According to Modern Monetary Theory (aka Magic Monetary Theory) none of it matters anyway. And we must never confuse the debt of a state to the debt of a household because the state can invoke its sovereign privilege to create money and therefore can’t go broke.

One problem with the theory is that quite a few states do a pretty good imitation of a broke household.

Although most are in Africa, they haven’t all been.

Back in the 70’s New Zealand had a very far left govt, basically a hangover from the UK war time era. There was almost no area unregulated by the govt.

One day the Minister of Finance got a phone call informing him that the NZ central bank had stopped foreign exchange operations. He phoned the Bank and asked why? The answer: ‘Because we don’t have any foreign exchange’

NZ was based on agriculture but imported its machinery. But Cat, Deere, etc. wanted US$, which the Bank of NZ would usually provide in exchange for NZ currency.

NZ was so broke, it called its embassies around the world and told them to max their credit cards and wire the money home. Now. It then laid off half the employees of the state broadcaster in one day. It sure looked like a household going broke.

The end was a massive de-regulation of the economy and the introduction of the first VAT or Value Added Tax,

(this includes sales tax but is much broader)

In NZ it had and I believe has no exceptions: not food, not kids clothing, not funerals. The reasoning was that if they allowed any exceptions there would have to be a

govt agency to sort them and handle endless appeals.

There are some obvious questions re: MMT

1. If deficits don’t matter then why have any taxes?

2. If deficits don’t matter why don’t the Treasury just assume all underfunded pension plans of the states and cities

3. Who will want to own dollars?

4. Is there any limit on the amount of deficits that we can run?

If the answer is yes, then what is that number?

If the answer is no, then we are off to the races

5. If deficits don’t matter , then why gift everyone a billion dollars?

What interest?

TheBenBernank,

As I said in the text:

US debt from the US Treasury Dept: https://treasurydirect.gov/govt/reports/pd/pd_debttothepenny.htm

Fed balance sheet data from Fed’s balance sheet: https://www.federalreserve.gov/releases/h41/current/

The remaining data from two reports from the Fed’s Board of Governors, one released yesterday, the other released this afternoon, both linked in the text.

Mad, mad, mad world

Think the word trillions has lost its meaning. Not many can even comprehend how much money one trillion is, wonder how long it will take before we replace trillions with quadrillion, quintrillion, sextillion, septillion, octillion, nonillion, and decillion. I guess at least we won’t run out of unit of measure for a while…that’s cold comfort.

Since the money is only electronic digits anyway, we should use IT-type terms. So, we’ve gone from gigadollars to teradollars to petadollars.

And who in Congress doesn’t want to pet a dollar?

Given the scale of the silent transfer of wealth from savers to the G (via ZIRP) over the last 20 years, I would say that DC has been engaging in a lot of non-consensual heavy petting.

Let’s ball park it.

Let’s assume $10 trillion in all species of fixed income invts priced at a spread to Treasury rates ($10T is far too low, but it simplifies the math).

Now assume ZIRP had the impact of gutting the weighted median Treasury rate from 7% to 4%.

Apply that 3% differential to the $10 trillion in private fixed income investments…works out to $300 billion…for *each* of 15 to 20 years of ZIRP.

So, $4.5 to $6 trillion has been silently transferred from saver/creditors to borrowers/debtors (including the biggest debtor of them all…the G).

Without there ever having been a single vote, ever…just the whirring of the Fed’s printing press.

Now multiply those trillions times the true average size of the fixed income asset base over the last decades – let’s say $30 trillion.

So, $14 o $18 trillion appropriated by the G, sub rosa.

To accomplish…what?

The greatest mispricing of assets in human history?

And all these effects…all pre Covid.

“To accomplish what?”

Good question. Even if SOME policy actions are simply reactionary, it’s not ALL just random lever pulling. The logical conclusion is that massive asset inflation was either a goal or an accepted side-effect of the goal. Unless it’s all just a bunch of “HOLY $#!t WE’RE ON FIRE! PULL ALL THE LEVERS!” I guess I could believe that too. The only thing I don’t believe is that anyone has a plan to make things “normal” again.

Lol. Nice, I’m all for the IT terminology. We kind of already have the petradollar. ;)

Hi, Big Boy!

My name is dollar …

Based on the past, I would say we reach 1 quadrillion in US debt right around 2060.

The U in US is not guaranteed 2060 is optimistic

Based on the past 6 months, with annualized debt growth rate near 20%/year, US debt will reach 1 peta-dollar in just 22 years.

And I thought my wallet was bulging…

If you were to stack single 100 dollar bills in one column how high would 3.5 Trillion be?

$3.5T in $100 bills would be a little over 19,300 miles high. U.S. currency is about .0035″ thick.

https://www.answers.com/Q/How_high_is_a_stack_of_1_trillion_dollar_bills

My math says 1,933 miles. But your point is well taken.

Make them $1 bills, and make it $25 trillion per Wolf’s analysis… 4,832,500 miles.

That’s far beyond the orbit of the moon (240,000 miles) and well on the way to the Venus (25 million miles at closest approach) on its way to the sun (93,000,000 miles)!

One trillion dollars, in a stack of $100 bills, probably hits the space station… lol

“Not many can even comprehend how much money one trillion is,…”

It is the “small integer” game…

Nancy Pelosi’s Bill of 3.7 Trillion should be referred to as 3700 Billion, IMO.

One Billion seconds is about 32 years.

One Trillion seconds is about 32,000 years.

But “One” sounds small to the non thinkers…

Just imagine these numbers reported in Roman Numerals.

This is not our problem. It’s the problem of the sucker Nations that buy our debt and believe that we will pay them back with currency worth a crap.Besides “Modern” Monetary Theory Guru’s say it don’t matter. Just print baby and consume,consume.Dow 50k has to happen. .Money printer oiled and on Auto and it will keep going Brrrrrrrrrrrrr…… Get you a shot of this its gooooooooood…..

Did you actually read the article?

“Fed monetized 65%”.

WE bought most of the debt. Our right hand bought from our left hand or some such. And YOU own part of that 65%, so not sure which “Nation” you are talking about. 35% divided among a number of countries is A LOT SMALLER than the 65% that WE bought no matter how you look at it.

Federal Reserve monetizing 65% is not “WE”. That’s the bankers printing money to lend to the Treasury. And keeping their side as an asset, to earn some interest forever, even if minimal.

We can argue on the semantics on whether the Federal Reserve is “WE” or not, but the US Dollars they print is backed by the full faith of the government.

But putting that aside, DR DOOM’s point was that other Nation(s) would be the ones on the hook, but that’s not true. They’ll be on the hook for some, but not for most of the current issuance.

The FED is most certainly NOT “We” in any way, shape or form

Hey guys, it says right on by $20 bill “In God we trust.” RELAX!

I was under the impression that it says ‘Doing God’s Work, so Trust In Us’ ..

After all, Lloyd GoldenCajones said so!

The debt is ours because it’s our currency that’s being inflated, faster and faster. The toxic ‘assets’ on the balance sheet of the FRB will stay there forever, consider them written off. They were never able to unload any of that crap without a market tantrum.

35% of the debt that is owed to other Nations. That 35% was the point of the comment. That comes to 9.1 Trillion which is about $27000 per person that is owed to other Nations. The other 65% that “WE” owe ourselves comes to another $50000 per person. The only way to eat into the $27000 much less the other $50000 for a grand total of about $77000 per person is with inflation or increased productivity. Productivity at that level ain’t going to happen.That leaves inflating the debt away. The Keynesian wet dream of debt management.And yes I read the article . The Keynesian Money printer has to go Brrrrrrrrrrrrr. And Dow 50k will happen if the Fed continues its asset inflation.

We’ll Brrrrr until we rrrrrrB :)

Dow 50K? Too low. Let’s just shoot for Dow 500K.

Yep, we’ll pay it back, but with significantly devalued dollars.

@drDoom, sorry, still not correct. 65% was basically covered by printing more money, at the fed, which theoretically should cause inflation and debase the buying power of the dollar, although the fed promises to unwind the money-printing someday when wall street will allow it without crashing.

The other 35% was sold as treasuries. Of that 35%, only a portion of that is bought by foreigners, most is bought by US investors.

In the 30-year treasury auction last Thursday, Indirects (which basically means foreigners) bought 62.2%. So that’s 62.2% of 35%, under 22% of the total.

Eastwind,

also of that 22% how much of that was foreign-private vs. foreign-public doing the buying? thats one number i like to watch. i dont think that the foreign public sector is going to be propping US dollar up any longer! foreign nations stopped being “suckers” in 2014. if the private sector gets scared off fed will have to buy it all. the general feeling around here is that the shenanigans will go on for decades a la japan. im betting that it will happen all at once and sooner rather than later. “straight to heck” as it were.

It’s almost time for the great awareness to come back. It comes back every hundred years or so like some great clockwork clicking back to the starting point. I just don’t know if crypto will become part of or be adopted into that great awareness.

Crypto is a thing, because of what the G did to the dollar, in order to serve its short term, selfish interests.

Without the debased dollar (and the federal debt driving it) very, very few would have any reason to care about crypto.

But when your life savings are forcibly converted to Monopoly money, you start looking for the exit.

“Chancellor on brink of second bailout for banks”

It’s right there in block zero. The first block of the first blockchain.

Nations are not suckers forever.

Neither are savers.

Or citizens.

Epilogue: “The only way to sustain the budget is to slash Social Security, Medicare, Medicaid, and public education. Yes, we incurred the debt to subsidize Jamie Dimon, but that’s water under the bridge. It’s time for some difficult choices, America…”

Of course. Why do you suppose Jeronamo choose to do his Fed thingy speechifying at the Pete Peterson Institute? Because that’s exactly what Pete spent billions of his own money saying just what you wrote.

Can we get rid of the corporate welfare too?

Can the MIC do with less?

No, because MIC is free and doesn’t cause deficits. I read that here in comments. Same for Cory welfare, it pays for itself.

Thanks for making me laugh so hard I almost choked to death! :)

Hey Wolf, I want a “Wazoo” beer mug and maybe a themed shot glass. Beer alone may not ease the unfolding discomfort that lies ahead.

I would totally buy one too.

Me three!

Really like to have the ”whole set” if I can just live long enough…

Definitely some sort of ”debt wazoo” on one of the sizes — probably ought to be the largest size of mug; then another size with all the sides consisting of very very straight lines; the shot glass is also a great idea!! Especially for those of us from the old school when a lot of bars would give you any kind of beer you wanted, as long as you wanted the one, the only one, they had on tap, and same with the whiskey!!

Of course, the beer was a nickle, and the shot a quarter!!!

The price of wheat went from $2 a bushel in 1960 to almost $5 a bushel in 2020. They sold five loaves of bread for a dollar in 1960. White pan bread costs $1.38/lb in 2020. It is cheaper to eat at home than to dine out.

The price of a new car was $2,700. in 1960. It did not have window tinting. A new car costs $27,000. in 2020. It has a catalytic converter, antilock brakes, power steering, automatic transmission, five airbags, anticorrosion under coating, etc.

In the 1960’s a car lasted 100,000 miles. These days they last 200,000 miles.

A brick or concrete block house may last 100 years.

Now do microchips and cows (beef).

Used books and college tuition.

Medical costs and expected lifetime.

Microchips haven’t actually become much cheaper, per unit of area (square millimeter).

It’s the transistors that got exponentially cheaper. Because we can jam more of them into the same chip area.

We did, however, get some economy-of-scale cost benefits moving from 8-inch to 12-inch to 300mm wafers. But each of those moves took ~20 years. Silicon cost per unit area drops at a glacial pace, about the same rate as battery costs.

Sigh…okay, how about processing power costs (the thing people actually care about).

Grocery store where I worked as stocker/bag boy in 1961 sold 24 inch loafs of white bread for 10 cents every day…

MD used to come to the house to see us kids (all of whom he had birthed) for $10 per house call in the 1950s era…

Surprisingly enough life expectancies have gone down in USA due to fentanyl, etc.,,, but one ya reach 75, it is 11.2 years for europeans and blacks, 12.6 years for hispanics…

College ”tuition” was a couple hundred per quarter or sememster in 1960 era, including 1970, and apt across the street from CAL was $50 per month during that same time,,, and wages were $5 per hour for unskilled, more if you could prove your worth, (much less in other states,) ,,, books, new or used were my biggest college expense other than food/rent/utilities.

You’re a little high on cars at both ends, though it depends on models then and now. Cheap car today can be had for under $10K, but no upgrades at all included at that price, including no radio, and you forgot all the cars today have AC, non existent except in high end in 1970.

Hmmm. Looks like the dollar won’t be worth much soon. Luckily I’ve been saving my coins. The metal will be worth something while the paper will not. I believe a nickle is now worth over $0.07. I hesitate to think what a Fed created digital bit dollar will be worth.

And most other countries are doing the same thing… those countries also trust each others currencies and systems around exchanging those currency even less than they do the dollar

No entity knows more about just how full of sh*t a government can be…more than another government.

HA… continuing with this line of thought… perhaps CHAZ can create its on central bank and issue its own CBDC, CHAZcoin, that it can swap with FRBNY for liquidity… xD

Kyle Bass has been hoarding nickels by the palletload for a while now.

When he bought a million of them (yes, a million nickels) from the Federal Reserve, and they asked why he wanted so many, his reply was: “I like nickels.”

How much is the cost of the energy to melt down a pallet of nickels? Surely there is a better investment.

In 2013 the “melt value” of a US 5¢ coin was about 4.5¢, and it included both copper (75%) and nickel (25%), meaning a loss of about 10% at face value.

Since then highly refined (Grade A) copper has lost 29% of its value and nickel about 17%.

In short this Kyle Bass fellow has as much business giving investment advice as I have giving dating tips.

It would be worth it if he made a really epic Volta-column all with his nickels!

I find it amusing that the Fed is indirectly funding the $1 billion in new stock bankrupt Hertz is issuing.

I come from a world where $1 billion was once serious money.

The end is truly nigh.

No: “the beginning is nigh”.

When I’m bored, I stand on the street corner with a sandwich board that says that.

And a cowbell.

We always need more cowbell.

Heck, $1 is serious money. There are still people who would cut your throat to get it. Some even run corporations.

Regarding Branden’s previous article, so sad we’ve failed our Post Office in providing it the proper funding in deserves according to it’s Constitutional mission. Had we provided funding for the Post Office to bring the internet to all our nation including rural, the folks in San Fran could spread throughout our nation and spread the wealth and make us all stronger. A no brainier that would strengthen our infrastructure.

Timbers:

Well up here in Canada I am sure glad nobody gave Canada Post the money to bring internet service to the masses!

A recent letter from my brother in Detroit to me in here in Toronto took over a month to arrive!

I’d hate to find out what Canada Post’s internet speed would have been!

Yes, thanks called planned underfunding here the states. It’s a deliberate policy to enrich private firms. Another example is requiring the P.O. of pre fund it’s pension 75 yrs in advance, then bash it for being underfunded.

The Fed lending to corporations is illegal under Title 12 USC 24 (Seventh). So instead, the fed created shell companies, managed by BlackRock (a private asset management firm) to launder their purchases of these assets. I swear to God I’m not making this up I filed a whistblower complaint with the SEC and wrote a letter to the OCC. If this shit isn’t stopped right now the United States will collapse.

Not a joke the central bank is collapsing. In the 2008 crisis the private banks were poisoned by subprime derivatives, now the FED itself is purchasing junk bonds.

We couldn’t even make it 100 years without destroying our monetary system. Since the dollar is the world reserve currency this will likely destroy the economy of the entire world.

Why do you think Russia and China are buying up massive amounts of gold right now without even asking for the price

Richie, thanks for the post. It sounds like you know the law and care about your country. I wonder if the other countries of the world plan on keeping the US dollar as the world’s reserve currency, even at the risk of war.

Reserve currency is a tricky one. Not only does the country have to have enough float to supply the world trade but it also has to have a reasonable legal system because if you had to sue over something, you want a functioning legal system.. Neither China nor Russia nor anyone at this point can do what the US does.

That doesn’t mean we aren’t abusing our rights but the newly printed money really isn’t in circulation. The Velocity of Money isn’t climbing. And with the numbers of unemployed it isn’t likely to change any time soon. At some point, with the Zombie and Uncorn defaults on the horizon, much of the printed money that has recently been printed will just evaporate.

If we lose reserve status, that probably means world trade has just stopped.

Things are really weird right now with the virus, the economy and the politics.. The US has always gotten thru its hard times before and I sure hope that hasn’t changed.

Relax. All fiat has always ended up the same way, in hyperinflation. This time is no different. The $$ had a good run. Buy gold while they can still suppress it and enjoy the popcorn!

That isn’t debt monetization. That is a small slither of ownership. Being the reserved currency inflates demand for debt, especially during a pandemic.

We’re caught in a trap. There’s now way out.

As government debt balloons, it will become even *more* important to suppress interest rates. Which encourages more corporate borrowing.

All while GDP, incomes and revenues experience downward pressure. Which then requires more borrowing to “make up” the GDP, incomes and revenues.

We’re caught in a trap

I can’t walk out

Because I love you too much baby

Why can’t you see

What you’re doing to me

When you don’t believe a word I say?

We can’t go on together

With suspicious minds

And we can’t build our dreams

On suspicious minds

Golly, if only conservatives had screamed about this for the last 40 years…

Yeah they were totally screaming at these companies to stop going into debt. Tried to stop them from doing buybacks with debt. Tried to keep federal debt down between 2000-2008, between 2017 and 2018. Tried to stop a bunch of incredibly wasteful wars. Tried to stop banks from destroying themselves before they actually destroyed themselves. Heck Hank Paulson got down on one knee and begged Nancy Pelosi to help him destroy moral hazard. The party of responsibility right there.

If you’re talking about the voters, sure maybe, nominally they care, some of them? Who do they keep voting in though. The party is running a conspiracy against you. The sensible game theory strategy at this point is to vote for the party that benefits you personally the most as they both destroy the country. I’m not rich so I know who to vote for.

Ron Paul would have got us on the right path. “End the Fed and break up the big banks”, that is what my protest sign said back during the last crisis at a tea party rally even though I was not a big tea party fan; Just a place to protest.

The central bankers printing another trillion dollars is their way of taking another slice out of your hide.

DEBT spending is the panacea for all the financial problems both private and public, all over the World! How long this can go on, is any one’s guess.

There is no outrage or accountability either by the public or the lawmakers.

Every one is sleep-walking and hope for a miracle, I guess!?

$60 trillion in non-financial debts”

What are the FINANCIAL debts? under what category?

Public debt has been and can be taken care of by the ‘MMT’ being practiced by Fed in various forms. Fed is also back supporting the Corp Credit mkt openly!

Who is addressing the the private debt amidst the non-financial debt? Who is going to service those debts in the coming ‘severe’ Recession, especially after July? How many more trillions-bailout from the Congress?

sunny129,

In terms of non-financial debts, “financial debts” are those owed by finance companies, such as banks, that borrow money to lend money. They might borrow short-term to lend long-term, etc. That’s why banks are called “financial intermediaries.” Counting financial debt would duplicated part of the debt, since a bank borrows money to lend money, and so you would count this debt twice. That said, financial debt is about $17 trillion.

Thanks, Wolf,

Lenders(Banks) borrow to lend to borrowers- various parties in the economy. So there is a risk of double counting under stood!

What about shadow banking and their borrowers? where does it fit?

60T minus 17T = 43T involves the rest. Has the latter increased (by how much?0 since GFC.

Thanks again for your thoughtful insights on various issues.

Yes, shadow banks (nonbank lenders) are also considered financial companies, and their debts are excluded from nonfinancial debts.

So that math is this for Q1: $55.9 trillion nonfinancial debt, PLUS (not minus) $17 trillion in financial debt = $73 trillion in total debt (including some double-counting via financial debt).

Checkout this article.

No one else has pointed this fact on the US BANKING system. Every one repeats that Banks are well capitalized unlike during GFC. This article completely debunks that!

The article has a click-bait title and misses the most important factors in the US banking system.

Do banks need to borrow to lend? Can’t they digitize money to loan, based on the appraised value of the collateral they loan against?

Not overly concerned about the USG debt as we are in a deflationary environment in core CPI and a monetary sovereign spends money into existence. Private sector debt is an altogether different matter, though.

It is absolutely baffling to me why the Treasury is borrowing to build up its Treasury General Account balance at the FED. The cash balance sitting unused in that account is now up to $1.550 trillion from $395 billion on March 23rd. Why are they borrowing to build up such an enormous cash balance?

Is it to make Repo collateral available?

Its not a given that when dealers dump 65% of at club fed, that the rest left over are becoming more available to the rest of the market participants.

Thanks, GC. Setting aside underlying questions about true policy intent and the related efficacy of monetary policy, it seems to me the lack of collateral is a necessary byproduct of ZIRP.

Aren’t the Primary Dealers essentially the same group as those of James Carville’s dream of yore to be reincarnated in his next life as a “bond vigilante”? :)

Primary dealers have long cut back on traditional banking activities (see balance sheet growth [or there lack of] global banks since 2008-09), and thus rely more on exotic shenanigans for profit.

Some would say its ZIRP, some would say lack of new profitable opportunities worth the risk, and some would say you can only squeeze blood from stone so much before there’s not much left to squeeze.

I never understand why so many people say the US Dollar will become worthless.

Worthless against other currencies?

All the other Central Banks are doing the same printing in proportion so surely the US Dollar has no change in relation to them.

The US Dollar is still the reserve currency and what other currency could replace it over the next 10 years. It certainly will not be the Euro that is way over valued presently.

In Economic or Political turmoil, people and businesses change their local currency to US Dollars.

If there was such a concern, surely people would have changed their US Dollars to gold. Maybe not so because people don’t actually have savings like they used to. This has been quite evident in the way people have become so dependent on state benefits / handouts in recent times.

Some of us have done exactly that You can call me Goldboy , Goldberg, Goldstein but don’t you dare call me Cashboy

haha yes. cash will indeed be trash. but not before it carries a premium above credit.

why do you, cashboy write off the euro so quickly?

also, what makes you think a currency will be the reserve in the future?

as for gold, im surprised to have to scroll so far before seeing it mentioned.

americans have been lulled into believing long-term debt is a real form of savings. they’ll wake up the hard way.

“If there was such a concern, surely people would have changed their US Dollars to gold.”

That is precisely what China, and particularly Russia have been doing.

I never understand why so many people say the US Dollar will become worthless.

Because taxation is being replaced by borrowing at an exponentially increasing rate. What really creates the demand, or the value, for any currency is that one must collect it in order to pay tax.

When nobody pays tax, nobody needs the currency and the trade will move to something people does need!

Cashboy,

Put a space between “worth” and “less” — and you get “…dollar will become worth less,” which (though grammatically a little twisted) makes more sense and has been established as fact over the past 100 years :-]

The dollar will be worthless to you when the day comes that your pension will only buy 2 days groceries.

People who worry about the dollar becoming worthless because of Fed actions do not understand basic economics or how the system really works. They have this imaginary idea that the Fed is printing mass amounts of physical cash that is now included in supply and demand of goods and services. This is wrong.

What the Fed is actually doing is supplying debt and removing some assets from the market to inflate perceived value.

Debt is only money, so long as people service the debt. At the point where debt stops being serviced it becomes destroyed money. The amount of the money destroyed is equal to the amount borrowed.

When there is a financial crisis, as we are beginning to see, people begin to default on debt destroying money. Money not paid in rent, translates into money not being paid in mortgage, which translates into money not lent for new purchases, which translates into more unemployment, and the cycle repeats. The value of dollars increases because there is less and less money with every cycle. In order for the Fed to be able to generate inflation, they must have a mechanism to increase debt. That mechanism is debt. It is borrowing that causes inflation. During a financial crisis, borrowing declines, so the Fed is powerless to increase inflation.

Amen. Thanks for the reminder

@ Jdog –

I meant When the FED buys assets, it provides dollars

Jdog said: “What the Fed is actually doing is supplying debt and removing some assets from the market to inflate perceived value.

Debt is only money, so long as people service the debt. At the point where debt stops being serviced it becomes destroyed money.” ……

_______________________________

I would like to understand what you are saying, but can’t catch it –

When the debt buys assets, it provides dollars, either physical or more like, digital.

Would you please explain how defaulting on debt removes dollars from the system?

The debt(-derivative), which was an asset, now becomes worthless in a default (if it was unsecured, like nearly 85%-95% of corporate debt now) for the bank / shadow bank (non banks) / shadow shadow bank (OTC securities lending entities) that lent the money(-like) into existence to collect interest on, interest money (and par value) which they can no longer keep lending out (par value was already spent by lendees, insolvent lendees pay no interest), any assets that are reliant upon the need for money to be kept lending into existence (ie. repo / collateral lending use to buy assets) will go down in value since the supply of money is contracting.

Money that does not move (off bank / non bank / OTC securities lending entities balance sheets) can hardly be called money (M2 growth canceled out M2V contraction) as far as the economy is concerned.

Money not moving:

“All told, the SBA says it had approved $512.2 billion in PPP loans as of May 21. That’s nearly $150 billion less than the $660 billion allocated to the program, which was designed to keep Americans on company payrolls and off unemployment assistance. Many of Bank of the West’s PPP borrowers haven’t touched their PPP loan deposits, which total $87 million, Blankenship says, partly because they are confused about the terms. “I think it’s a mixture of uncertainty and anxiety and fear, and the uncontrollable factor about employment and rehiring.”

My personal favorite from a FQHC CEO recently of money not moving:

“I just got a $9 million dollar loan from the community bank in a 30 min conversation, where 20 minutes were spent on them asking me how we can work together to help build the economy in the local community”

The system treats debt as an asset, or money. When you buy something with debt, say on a credit card, the money for that purchase is created out of thin air right at the point of purchase.

The money in fact only exists because you commit to pay it back with interest at some point in the future. At the point you default on that commitment to pay that debt, the money simply disappears, although the item that was purchased by the debt still physically exists.

If you multiply that example by millions of transactions of all kinds you begin to see that the result is less overall money, and more overall goods. This has the effect of putting downward pressure on the price of goods and assets. It also has the effect of making credit decrease as risk increases, which tightens money supply.

Today the vast majority of the money in our system is debt. That money only exists if people pay their debts. This creates another problem because a debt based system creates debt trains. Our entire supply system is based on debt, and interruptions in debt payment effect other entities ability to pay their debt creating a chain reaction. The potential for money destruction due to debt default becomes exponential…

Good comment. I submit that the FED’s balance sheet is far less than what is advertised. They have enormous amounts of unauditable NPLs that can bear no scrutiny left over from buying the junk of FNM and FRE in the last round.

The FED was explicitly prohibited from buying that junk as was stated on the cover sheet of all of those CMOs. The cover sheet expressly states that the offerings are not guaranteed by the goomint or anything else. The FED inhaled the crap that was trading at 5%- 12% of par and put it on the books at par. Yeah it was at least rated A or higher, but Markit showed otherwise from actual sales.

Here we go again, and fuggetabout it if you want to see the books.

So many smart commenters on this blog post about exponential growth in debt at all levels.

Yet metal only mentioned once, and it was nickel.

Nickel, really?

Strange times indeed.

I used a small portion of my stimulus money to buy some silver and bronze earrings. They are pretty and affordable.

I know your intention is to push gold, but this disaster should be showing you that if it doesn’t have utility, it doesn’t have value. In the Caribbean they are lining up to use ATMs and to get into the banks for cash. What good is gold for people that need money to buy gas and groceries. When you sell your gold it will be for cash.

Such nonsense.

Gold is at or near all-time highs in most major currencies. Holders of gold, as opposed to cash, have benefitted IMMENSELY in recent years.

Setting aside the obvious and more extreme examples (e.g. Argentina), if one had exchanged Euros for gold during the ’08 crisis and held it until today, the value of the holdings would be nearly TRIPLE the current equivalent value of Euros.

Gold is up over 70% in Euros since 2014. Gold is Tier 1 bank capital. Gold is the first asset listed on the ECB balance sheet. Gold is hoarded by the very central banks that are largely petrified by what its sharp rise in value indicates.

What good is gold? It continues to prove itself as a preserver of wealth during times of economic stress that is arguably without peer.

Gold has little intrinsic value as a metal. It doesn’t rust and it has good conductivity but is too expensive to be used widely.

The banking system can back money with beanie babies as long as they control the supply. Metal is popular because it can be coined and carried, but paper is more portable. As far as your argument that gold is a store of value or a preserver of wealth, I would like to remind you that you live in the age of bitcoin and the trading of worthless stocks(Hertz). Both considered stores of value and wealth preservers.

More nonsense. You are comparing Bitcoin, which has been in existence for 11 years, with a metal that has proven its value over thousands of years? Please. No one seriously equates the two, and for obvious reasons.

Hertz stock? A store of value? What planet are you living on?

I have provided concrete, irrefutable examples of how gold has recently performed as a preserver of wealth during times of economic stress/crises. You, in stark contrast, have produced nothing of value to support a counter-argument.

Tinky,

You obviously don’t follow the financial news or you would know Hertz is selling more stock while in bankruptcy and its stock is the darling of young “investors.”

Tulips were a store of value once and more valuable than gold. So gold is popular again, ok, bitcoin is considered digital gold, ok, so what. A Chanel handbag is almost $7K, up ~25% this year, looks like a better investment than gold.

True that. Gold is finite and beautiful. Made with the unbelievable pressure and energy only found in the destruction and birth of suns and solar systems. Unlike diamonds, gold can not be made by living entities. This type of beauty and rarity has always been valuable over time.

ImplicitI: Actually, gold can be manufactured in a nuclear reactor as a breakdown product of either mercury or platinum.

Petunia,

You have again underlined that you do not understand the basic difference between investing and wealth preservation.

Until you are able to understand that distinction, you will continue to misunderstand gold, the economic role that it has played over the past several thousand years, and its current value.

Petunia, ive been reading you repeat this stuff for years and its as wrong today as it ever was. golds value is not derived from its industrial uses. just like a monet isnt valuable for its use as wallpaper. just like a classic car isnt valued for its gas mileage.

that is why gold is on a different level than silver, bronze or whatever. 80 oz of silver does not equal 1 oz of gold anymore than 1000 of my paintings equals one monet.

bungee,

Art is a very good example of utility adding value. The value of a painting isn’t the amount of paint on the canvas or the amount of bronze in a statue, it is the “productivity” added to the paint and bronze, which we call talent.

Gold is rare and durable, along with many other things, we value it based on historic norms and popularity only. We chose to call it valuable the way we decide steak is the most popular meat in our culture. You couldn’t give away steak in India, but they like gold.

In Japan and Asia, historically jade was the most precious stone, not gold. Jade is extremely rare and not as durable, but was valued more than gold. So, you see it is a societal choice that gives the value, not the thing.

Petunia,

Gold is rare and durable, along with many other things, we value it based on historic norms and popularity only

the “utility” and “talent” you write of is only worth so much. no one pays hundreds of millions of dollars for a cool painting in their living room. that is a popular misconception that us regular folk like to believe so we can pat ourselves on the back and say, “think of all the GOOD that could have been done with that money!” and we pretend that once we get that money we’ll be so much better with it. but really, those rich people are storing value in something that costs a lot in a tiny space. something they can pass down if needed and their kids can hock to some other rich kid. so yeah, these crazy things people buy for crazy money are ONLY because other crazy rich people value it as well. gold is the only one of these otherwise worthless items that us plebs can partake in. there is not 100 million dollars worth of “talent” in a warhol painting. but there is much more than 1700 dollars worth of value in an ounce of gold!

i think i’ve heard you mention expensive handbags before? is that right? if so, that is the perfect example of a brandname selling something for far more than it’s utility as a purse. those bags will likely hold their value. you could buy a well-made fake and it would serve the same utility as a social symbol and a place to keep your stuff, but that would be missing the point and in the long-run, money wasted.

the only problem with these expensive items is you’ve gotta buy the whole designer bag, the whole famous painting, the whole classic car.. &c.. i cant afford those things. but with gold it makes no sense to say that “it is too expensive” even if it has no utility other than storing value.

Ultra, thanks, you are correct, but it is not cost effective at all, I will read up on the other jewels and PMs and the rare earth metals. Interesting stuff.

Hey Petunia, I get a kick out of your comments and like the women’s perspective. The fashion comments are a must read.

Do you think that there is a market for Roman coins to make earrings? There is some nice bronze stuff around that is cheap so that a gal can have a link to 1800 years ago, you know, real antiques. The silver ones before they got alloyed below 60% are pricey and you would not want to drill them. Perhaps in a dainty bezel?

As for handbags of ladies.

My wife carries around some satchel with whatever she thinks that she needs to carry on the life. The weight of that would be considerably lightened if she carried enough gold to buy a Cadillac CTS-V.

What the heck, a single gold British pound coin is worth .2354x$1725 is 406 paper dollars that weighs more than the coin and is far bulkier.

Ooops, wrong – as I was typing Cashboy posted!

As I understand the only problem with printing money is inflation, since there is a limited amount of products to buy with said money. But US can produce & import a truly massive amount of goods + most of the printed money doesn’t go to consumers. So, how can things go wrong?

Most inflation is not caused by printing money. That is a misconception.

The only inflation that is caused by the Fed printing money to purchase assets is in the actual assets the Fed purchases.

The vast majority of inflation is caused by the interest paid on debt purchases. Whenever something is purchased using debt, the price for that item is inflated by the amount of interest paid on that purchase.

The price of an item costing $1000 purchase on a credit card at 20% interest and paid over a year is $1200.

If everyone began to pay cash for their purchases, or paid their debt in full every month, instead paying interest, inflation would stop.

Wolf, as the Fed slows its monetisation of treasury debt, how will the huge fiscal deficits be funded going forward?

So far, there is huge demand for US Treasuries — see the low yield (meaning high price). As long as the yield stays low, the Fed doesn’t need to do anything with regards to Treasuries. When demand evaporates, yields will rise sharply… and then suddenly, there is huge demand because yields are up and make these Treasuries a better deal.

If raising interest rates creates demand they would do doing it now. Yellen said there would never be another financial crisis and Powell says rates will never rise. I don’t expect any Fed to accept the link between higher risk and and higher interest rates. Ever…

Ambrose Bierce,

“Powell says rates will never rise.”

That’s not what Powell said at all. I don’t know where you got this BS from.

@ Wolf –

With the FED willing to monetize US Treasuries, and as you poited out, currently monetizing 65% of new issuance, how can there not be huge demand, and how can we make any assertions of demand based on price? The FED can digitize any amount of money to purchase as many Treasuries as it wantss and to set the yield it wants to set.

cb,

Look at the second chart in the text. It shows that the Fed has stopped monetizing this debt in recent weeks, and demand came from elsewhere.

Being that a single lowly trillion is a million $ a day for 2000+ years, I suspect there’s more than enough currency out there to create hyperinflation in short order, but we all know that it’s frozen up in assets held by the few, so not enough money velocity to end up on the right side of the inflation hockey stick.

So the question is, “What might lead to the unfreezing of that stored up asset inflation?” My guess is it’s gonna have to take the scenic route thru (already rising) consumer prices to start dragging up wage;s but they’re rising at a snails pace compared to what’s lurking in assets.

I think past hyperinflationary events thru history progressed much faster simply because there wasn’t the financialized assets around to mop up all the excess ‘liquidity’ so we’re in uncharted territory. Could be decades before that 2 taco combo at Rubios is $299.99 or it could be frighteningly only years away. And there’s where dread mixed with cognitive dissonance comes in.

Thomas,

Your comment was terrifyingly bang on. So many folks think, “This can’t happen here”, or “to us”, or “now”, etc. My question to them is, why not?

Maybe an even worse situation is if the printing goes on and on and nothing much happens as many people just remain unemployed and have no way to make money. In this scenario, increasing disparity of opportunities and wealth continues to increase as does anger and unrest. There is already a huge distrust of Govt and institutions.

This is no joke. As I said to my friend and neighbour yesterday, “We’re in the big leagues now. A pandemic and shaky economy is as big as anything can get short of all out war and mass dislocation”.

Our Provincial health officer always ends her daily news briefing with this, and her words and manner are a great comfort to BC. “This is a time to be kind, to stay calm, and be safe”. She also says, ” I know these restrictions are very hard for people, but it is just for now. It is not forever”.

I hope she is right.

Failed states suffer hyperinflation; for a current example look at what is going down in Lebanon. Their currency has depreciated 70% in a matter of days.

Nicko2, You mentioned Lebanese currency in the toilet.

They supposedly have a large amount of gold to back it…I laugh.

That is the old story from 1978 or so that showed that they had the best gold to currency ratio of anywhere and goldbugs should sell dollars and buy Lebanese pounds. That didn’t work out well at all but we still are shown official stats on their gold reserves. Lebanese pounds must be a good buy now?

There are no audits anymore on the claims of gold assets per currency units. Just try to get an audit on the USG claims of 8500 tonnes of gold. The last was about sixty years ago.

Hey Thomas — I think you’ve got it exactly right! Seems to me–all that has to happen is that inflation starts to rise at a rate somewhat higher than low bond interest rates in a $40T bond market. That will make bonds very uninteresting to most people who might happen to have one or two they’d be glad to sell. If they could. Then spend the cash fast.

Come to think of it, maybe the Fed would be glad to buy bonds to save bondholders if inflation zoomed up. Does “whatever it takes” means they would raise their balance sheet to go $40T higher to buy out the bond market?

I was walking this morning when a little boy came up to me from the opposite direction. He had a little puppy with him that he was walking on leash and it was heeling nicely.

I told him he had a wonderful dog. His reply? “He should be, mister! I paid $500,000 for him!”

Where did a little boy like you come up with $500,000 I asked?

“Easy”, he said. “I traded two $250,000 kittens for him.”

The little boy told me his name was Jerome, but that I could call him JP.

That one is just too good. It might be the basis for telling a kid just how screwed up the situation has devolved to. The last line is a killer. Monetise the dogs and cats and put them into a CDO and sell it to the FED.

CDO is wrong. Perhaps the valuable pets and strays could be incorporated in the Caymans and then get a small listing in HYG.

Thomas said: “I suspect there’s more than enough currency out there to create hyperinflation in short order, but we all know that it’s frozen up in assets held by the few”

___________________________________-

How many dollars (currency), physical and digital, are in existance, who owns them, and where are they?

A dollar (currency) is an asset. Other assets are not dollars. We may denominate their value in dollars, but that it subject to change, perhaps at a moments notice. If we think of dollars being frozen in assets, we may in for an unpleasant surprise when try to unfreeze those dollars. One might find their stocks or paintings might not provide but a small fraction of those dollars that they expected to receive upon “liquidation.”

I Think I’m correct in saying that the ballooning debt is a mirror image of the rate of collapse in spending, loan defaults and derivative implosions. I don’t think the Fed will be able to keep up.

@ Raymond –

i don’t think loan defaults balloon debt, but reduce debt.

Precisely, new debt creates growth which obsolesces old debt. Spending, other than sink holes like DOD, has been anemic. There was supposedly a trillion dollar bipartisan infrastructure spending bill, which never materialized. After which they cut revenue (corporate tax cuts). Drunkenmiller notes Fed monetized a trillion more than Treasury issued, which creates a problem when they need to monetize deficit spending. Fed will transition from the ridiculous to the sublime. No other choice

Inflation happens only when the money comes to the bottom tier men like me. Now, most of the money stay at the top like business and top 10% of stock holders and rich people. Unless the money reaches me, inflation will not happen. The newly printed money is in circulation only among the rich people, their business and assets like stocks or homes. A river in the mountains. Lets say, inflation increases housing costs. Now, rent is not rising. Quite the opposite, landlords are giving grace period and even cancelling the rent. With a huge inflation gasoline prices might rise. Now, there is decrease in gas prices in the pump. This money printing is selective about the pockets it reaches. Remember, there was only one stimulus check (other than unemployment income). Lot of people are out of work since April for three months. From pan into the fire, COVID led to peaceful protests all over the cities. The economic recovery will take longer than anticipated. Now, when the economy drops by the official metrics, there will be another round (or couple of more) money printing. I hope that money will reach the masses like trickle down economics

Cobalt- I think you DON’T want it to trickle down… that is when the s$!& hits the fan. I.E. I printed myself a billion dollars (or even got a fancy piece and put some big number on it) and keep it in my closet and smile… I’m rich! As long as keep it there – no harm no foul. When I go on a shopping spree – look out. When will all the funny money ‘need’ to be spent???

Since the official unemployment number of the U-3 should be about 14-16% because of a probably mid-answered survey question according to the Fed, which means not quite 25% for the U-6. The labor participation rate has been declining for decades and actually reached IIRC the 1973 low of 60.3. Keep in mind that the unemployment and inflation rates have been slowly jimmied to understand the true numbers each year leading to a true undercount although they do give a fair approximation especially month to month.

Add that the average American has had a declining for a few years and I am not sure where this idea of inflation zooming up any soon really comes from. Aside from real estate, luxury items like wine and watches, and of the stock market general denial of reality.

Also, two thousand dollars a month for six months for everyone who received that single paltry stimulus check of twelve hundred would have cost two trillion dollar and gone mostly to people who really needed it. Instead we have several times that amount going into the banks, investors, and other similar wealthy parasites who do not need the money to buy more stocks, real estate, wine, watches, and yachts. Not very stimulating or generally inflationary unless you are trying to find housing.

The concept of inflation as the excess growth of money supply does not seem to matter now. A more dynamic interpretation is to view inflation as the velocity of spending (of money/credit). The faster the transactions go around, the more quickly things and services are needed and used, the more valuable they become (and the larger the amount of money needed to purchase/sell). If the money just sits there as a yacht or mansion it doesnt go anywhere but go down the street to buy a few beers and you start it moving.

This all sound like the pea under (which?) thimble trick but heck even Powell cant figure why inflation hasnt happenned (Great Leader would never admit such ignorance).

ROD

Fascinating observation. As equities inflate in price, those who can buy them (demand) continue that inflation. For those who do not buy them, there is no (or little) inflation as we (the have nots) demand / consume only the necessities of life. Strangely reassuring.

Yes I have also thought about this in a similar way. As much as it sucks to have 90% of the wealth concentrated in the top 1%, can you imagine what it would look like to extract that wealth and spread it around? Those 1% can only buy so much and they are not directly competing with the other 99% for most goods. But if you took that wealth and spread it to the other 99%, suddenly all of that accumulated wealth would be in the hands of people competing for ‘regular’ consumer goods, and *that* would cause mass cost inflation.

We’re in a weird system where money printing does not cause inflation because most of the money goes to people who are just going to hoard it anyway, so it doesn’t get spent.

What it does do, however, is lengthen the amount of time that the 99% will be ‘slaves’ to the 1%. We may have already hit the point of ‘in perpetuity’ for that though.

“because most of the money goes to people who are just going to hoard it anyway, so it doesn’t get spent.”

You touch on the problem at the very end, but the key issue is this – asset inflation creates problems too.

Nobody trying to corner food supplies, so no famines (yet).

But consider housing, which is an asset too and a highly levered one at that.

Despite the stagnation in median incomes from 1998 to 2018 or so, housing prices essentially doubled (driven by ZIRP). Similar trends for apt rents.

So *at least* that category of asset inflation has serious impact outside the 1%.

Another kind of argument can be made for purely financial assets…if their prices pass out of reach for the 99%, how do the 99% accumulate wealth, ever?

ZIRP has created a huge, latent volatility in financial asset prices (because the Fed Put is wholly at odds with the real asset economy).

And that huge latent volatility/overvaluation/mispricing creates a sort of minimum buy-in to acquire financial assets…you have to be rich enough to endure the risk/volatility latent in those financial assets.

Not rich enough to outlast a 50% to 75% implosion in financial asset prices…then you have to stay out of the financial asset mkt and remain in the ZIRP ghetto.

That has long term consequences for the 99%.

People have become so used to debts and deficits going up with no apparent or immediate cost, it has become ho-hum. It’s when it breaks, when people figure out it can never be repaid, and they might be the one of those who do not get their money back (pensioners, bond holders, bank depositors, etc….). Are we close? I don’t know, but I expect there will be a major shock before the election (if it looks like Biden is to win-meaning he will start taxing) or immediatly after (if Trump wins, and free money taps are turned off)

What is created now is something other than “debt”.

Debt carries the assumption, the suggestion that repayment will occur.

Not in this instance. Rolled, but never repaid or retired.

Speaking of debt, savings, “assets”: so much of the “assets” that people have as savings (and in pensions, etc.) are actually someone else’s debt (MBS, corporate, etc.) that is now considered to be like money and a store of value. Used as collateral. What used to be a store of value? Actual dollars and gold and silver? What a quaint idea. There is a lot of risk lurking in our savings.

I think the idea is that the wealth of a nation is the ability to produce goods and services and that is a better foundation than gold. However, confidence in the dollar is a thing to be guarded as no one knows exactly where the Minsky line is that can not be crossed.

I expect many years of financial repression so that savers lose a 1% – 2% a year in purchasing power if all goes well. Seems like we are in for a rough decade as far as real paychecks and real investment incomes keeping up with inflation. An asset price is not income (unless sold for a profit.)

That is why the question must be answered –

How many dollars, physical and digital, are in existence, who owns them and where are they?

cb,

You keep asking the same question – and you get the same answer, only the quantity changes, but you appear not to like the answer, and so you keep asking the question over and over again. For the last time:

“Physical” dollars:

There are $1.9 trillion in “physical” dollars out there as of June 10. You can look it up on the Fed’s weekly balance sheet where they’re a liability called “Federal Reserve notes”: https://www.federalreserve.gov/releases/h41/current/

Yes, every financial instrument is an asset for one entity and a liability for the other entity, even physical dollars. For you, they’re an asset. For the Fed, they’re a liability.

It’s the US banking system’s job to always have enough “physical” dollars on hand to meet demand by bank customers.

Banks get those “Federal Reserve notes” from the Fed by posting collateral at the Fed, mostly Treasury securities, but also some small amounts in gold certificates and Special Drawing Rights. You can look that up too on the Fed’s balance sheet. No secrets here.

These Federal Reserve notes are held by everyone around the world, much of it in foreign countries. I have a wad of them in my pocket too.

“Electronic” dollars.

Electronic dollars only exist in form of assets and liabilities. Every single dollar out there is both an asset and a liability because every financial asset is some other entity’s liability. Even paper dollars, as explained above, work that way. This is a concept you need to understand.

An electronic dollar floating out there by itself doesn’t exist.

If you put $100 into a bank, it’s an asset to you. But it’s a liability and an asset for the bank: The liability for the bank is the $100 it owes you, and the asset is the $100 in cash that it can buy Treasuries with, or put on deposit at the Fed, or lend out, all of which are assets for the bank.

If you own a house free and clear, there are no dollars involved, other than as an accounting entity: You think your house is worth $1 million, which is an accounting entity in your mind or on the appraisal, not electronic dollars.

Then when you sell the house for $800,000, you get 800,000 electronic dollars (asset for you), that you put in the bank (liability for the bank because it owes them to you, and also an asset that the bank can buy Treasuries with, or put on deposit at the Fed, or lend out). And if the bank puts those $800,000 on deposit at the Fed, they remain an asset for the bank and become a liability for the Fed (required or excess “reserves”)…. etc. etc. forever.

BTW, same is true for things like stocks. They represent ownership of a company with an accounting value. Electronic dollars get involved only when you buy or sell them.

This is the first time I remember ever receiving an answer to this question. Thank you.

So the FED has an accounting entry for every single outstanding physical dollar, even those that heve been in my desk drawer for 30 years. How about electronic dollars? Do they also have an accounting entry for every single outstanding electronic dollar?

(and Thanks for your hard, diligent work)

“How about electronic dollars? Do they also have an accounting entry for every single outstanding electronic dollar?”

Re-read what I wrote and try to understand it.

folks a parabolic curve is what it is. no matter what market. And if you’ve been around markets for awhile then you know how they end. We are in the 9th inning 2 outs I think in government debt. Strike 3 by 2022!

As someone who holds Treasury paper, I am getting nervous. We are very close to a lame duck administration which has threatened all sorts of things. Usually big programs, like dollar resets, should be left to the incoming administration, which might be headed by a career politician. Some thought 2008 was scorched earth policy, the stakes are much higher here. Seems the market is betting on a replay, no reform or recrimination, paper over the problem.

“Seems the market is betting on a replay, no reform or recrimination, paper over the problem.”

that would be Uncle Joe. who do you think picked him as a candidate?

That would be all candidates of all parties. Who do you think picked all the candidates?

It would also be the US citizenry, which votes based on name-recognition and smart-sounding blabber.

The simple fact of the matter is that it is impossible to borrow your way out of debt. The Federal Government must service its debt. It must pay the interest payments. Those interest payments were about 20% of the Federal budget before this mass borrowing spree. At the same time they are taking on a massive amount of new debt, their tax revenue is shrinking substantially.. The last time the Federal Government was in this kind of trouble, they stole everyone’s gold. I wonder what they are planning to do this time….

Elastic fiat money has been good for the federal government and the ruling class. It has been good for the fire economy. Been a lot of people that have not benefited such as the prudent saver or the blue collar worker.

You might even say it is the crack that enabled politicians to create the pension problem as the system relies more and more on debt financing to pay the bills. As in a Ponzi scheme, the ones that get paid first are the winners and late comers will get surprised the wealth is gone.

They plan on keeping the interest rates low for many years so they can afford to make the interest payments. Same old same old

Richter’s concluding sentence: All combined, total nonfinancial debts will approach $60 trillion by the end of June – having doubled in the 14 years since 2006. Debt out the wazoo.

Reality: The domestic nonfinancial sector debt to Gross Domestic Product ratio was as flat as a pancake from the end of the Great Recession to the beginning of the Covid Recession.

https://fred.stlouisfed.org/graph/fredgraph.png?g=ry2K

marmico

You don’t seem to understand what you posted. This measure of debt to GDP that you posted hit a record during the Financial Crisis, which then triggered the implosion of the US financial system.

The chart shows that the much-needed deleveraging after the Financial Crisis was only timid and short-lived: while consumers deleveraged for a while, companies did the opposite and levered up. Federal government debt ballooned too. That’s what you’re seeing in your chart. You’re seeing the folly of low interest rates at work – which begat record corporate leverage.

In Q4 2019, before the pandemic, that debt-to-GDP ratio surpassed the Financial Crisis record. In other words, the record debt that helped trigger the Financial Crisis was surpassed in Q4 2019. As a reminder, the Financial Crisis wasn’t a state of calm that it would be soothing to return to, but it was when the US financial system began to collapse.

So in Q4 2019, and prior quarters, this was a scary level of debt (and debt-to-GDP) that even the Fed kept fretting about in its Financial Stability reports.

Then in Q1 2020, the ratio spiked way beyond that new record set in Q4 2019. That spike was caused by the reaction to the pandemic, including the decline in GDP in Q1.

In Q2 2020, the spike in the ratio will be huge: Nominal GDP in Q2 may be down to $20.5 trillion annualized, and total nonfinancial debt may be close to $60 trillion. Then the ratio you cited will be about 2.9 — up from 2.14 in 2006. It’ll be way off your chart.

You don’t seem to understand what you posted. You wrote: I’ve been fretting about this debt on my site since 2011. In recent years, I innocently added a green upward arrow with “Debt out the wazoo” to my gross-national-debt charts…

There was no debt out the wazoo during the 128 month expansion starting June 2009. The growth rates of the economy and nonfinancial debt were the same, i.e., no increase in the leverage ratio.

Of course, the Covid Recession changed that arithmetic.

marmico,

Now you’re lying. That line you quoted from the second paragraph and the chart that goes with it refer to US government debt only.

Over the 128-month expansion starting in Q2 2009 through Q4 2019, US government debt soared from 80% of GDP to 107% of GDP. That was during the Good Times. That’s debt out the wazoo. Got it?

From 2006 to Q2 2020, US government debt soared from 61% of GDP to 130% of GDP. Debt out the wazoo squared.

Our country is near the end if DeToqueville is correct, that the last stage of a democracy is raiding the Treasury. Now Alex didn’t see things like Modern Monetary Theory or Quantitative Easing…..but the concepts are the same, the theft is the same.

“A democracy cannot exist as a permanent form of government. It can only exist until the voters discover that they can vote themselves largesse from the public treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the public treasury with the result that a democracy always collapses over loose fiscal policy, always followed by a dictatorship. The average age of the world’s greatest civilizations has been 200 years.”

The voters are instead Central Bankers.

I suspect the duration of each great civilization seems to be shortening as the pace of change accelerates. Getting near time for the US to hand the reins over to its successor. The only thing preventing from happening is that no other country is ready to assume that mantle.

Only pure Americans think in terms of the world needing some leader country. Why can’t it be a multi polar world?

Some countries are fighting us not because they want to be the leader, rather they didn’t elect America to be the leader.

> Why can’t it be a multi polar world?

Nukes.

The great civilization we all belong to is Industrial Civilization, which began in NW Europe in the mid-18th century.

It is now at the point of greatest malignancy and corruption, tottering on a degraded and depleted resource-base.

There will most likely be no successor.

My big question,and maybe yours is this. Due to the Fed’s absolute control of the economy of winner and losers will the future be Deflation followed by Stagflation then a melt up Inflation then bust,straight out of the Austrian School of Economics “Hand book”.How about we go straight to Stagflation or conversely straight to Deflation? Or do we go straight into Inflation. If the masses can be polarized to a war footing do we go there as part or even all of the plan? Hell,I don’t know. The only thing I do know is I can control my debts. All the time I have spent reading and listening I end up in this same place . Am I an idiot and just keep missing the answer? Jury is still out on this.

The ultimate question for me when it comes to the Federal Reserve is: what will help the banks? Unless someone wakes up and allows the banks to go bankrupt, the most likely path is inflation and even hyperinflation.

Can we have deflation before that? Sure. In fact it may even be necessary to allow some deflation to happen to strengthen the hands of the inflationists.

Either way: the United States will soon enough be a banana republic.

My Black Swan thesis remains intact i.e. the US will go down first before other major countries.

A banana republic with gun ownership exceeding 400 m guns can he described as a combustible enviroment

There can be nothing but deflation or stagnation unless wages go up considerably.

Raise your hand if you still have a job and your wage went up considerably.

Bueller…Bueller…

Just look at M2 velocity. It has been heading down since the beginning of 2019.

Did you know they are monetizing debt right now to the tune of $2T per year or more? Velocity has a bottom to it, whereas money printing has no limit. Think about that for a minute.

Take a look around you, people are angry because they have no money and no work. In that scenario where is the inflation coming from? You need excess cash and income to sustain inflation and we don’t have that. Until people living on social security can buy whatever they need, we will won’t get inflation.

For an interesting short read enter: The Roman Financial Panic of 33 AD. Here is a snip from the end game, which began via political turmoil within the Senate, and with the Emperor.

‘When Publius Spencer, a wealthy noblemen, requested 30 million sesterces from his banker Balbus Ollius, the firm was unable to fulfill his request and closed its doors. Over the next few days, prominent banks in Corinth, Carthage, Lyons and Byzantium announced they had to “rearrange their accounts,” i.e. they had failed. This led to a banking panic and the closure of several banks along the Via Sacra in Rome.

As the crisis spread, banks began calling in their loans on everyone trying to raise capital. When debtors could not meet the demands of their creditors, they were forced to sell their homes and possessions, and with money unavailable even at the legal limit of 12% interest. The prices of real estate and other goods just completely collapsed in a downward spiral of DEFLATION. A full scale panic was sweeping the entire Empire.’

The caps of ‘deflation’ are in the source not mine.

I just finished reading “Bubble in the Sun” a new book about the collapse of the Florida real estate bubble in the 1920’s. The speculation was driven by income and credit and eventually killed off by a hurricane. Sound familiar.

BTW, I highly recommend the book, a good read on Florida history of the time and architecture as well.

Sure looks interesting to this old native son of FL Pet,

Thanks for bringing it to our attention; library has 14 copies and over 50 ‘holds’ so it may be a while til I read it.

One of my memories of ”olde” SRQ, (sarc) is of the old ‘ringling hotel’ on the south end of LBK that stood empty and half finished, a wonderful ”attractive nuisance” for kids to go to at night, and many fell down the empty elevator shaft(s?) to their early demise; just one of the ways the ”darwin awards” were given out ”back in the day” eh