With 30 Million Unemployed, Even Prime Loans Will Get Messy.

By Wolf Richter for WOLF STREET.

“Because consumer debt servicing statements are typically furnished to credit bureaus only once during every statement period, our snapshot of consumer credit reports as of March 31, 2020 is, in effect, largely a pre‑COVID‑19 view of the consumer balance sheet,” the New York Fed said today when it released its Report on Household Debt and Credit for Q1. So the credit-upheaval caused by the biggest and most sudden unemployment crisis in our lifetime is not yet included in the New York Fed’s delinquency data. But even in the pre-Virus Good Times, auto loans already exploded.

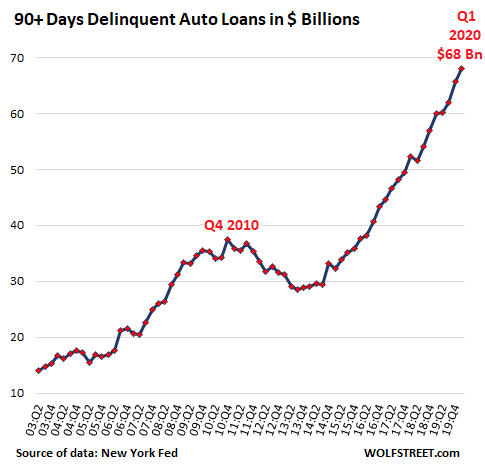

Serious delinquencies in auto loans and leases – those that are at least 90 days past due – surged by 13% in Q1 from a year ago to a historic high of $68 billion:

Delinquencies of auto loans to borrowers with prime credit ratings were near historic lows (0.27% in March), according to Fitch data. In the pre-Virus Good Times, it was the subprime loans – with credit scores below 620 – that were blowing up.

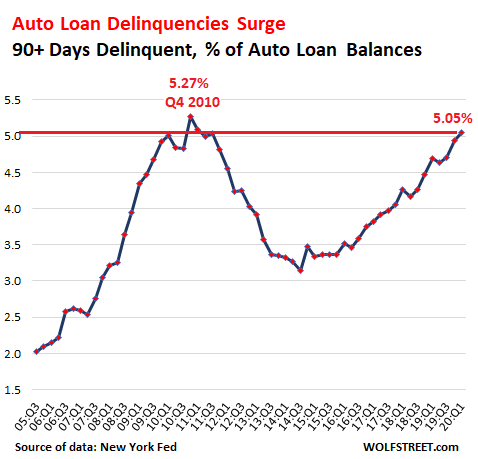

Seriously delinquent auto loans, at $68 billion, jumped to 5.05% of the $1.35 trillion in total auto loans and leases. This is only a notch below the peak of Financial Crisis 1 in Q4 of 2010 (when it was 5.27%), after General Motors and Chrysler had filed for bankruptcy as the industry was collapsing. But in Q1 2020, those were still the Good Times:

Delinquencies will now explode through the ceiling

In April, specialized subprime lenders started reporting surging delinquencies and plunging new business. Among the first was Credit Acceptance Corp [CACC] when it disclosed in an SEC filing on April 20 that it was getting hit due to the sudden job losses, as consumers were “delaying payments or re-allocating resources, leading to a significant decrease in our realized collections.”

It complained of a sudden drop in new business as consumer demand for vehicles fizzled. And this toxic mix of the surging delinquencies and dropping new business, it warned, “could cause a material adverse effect on our financial position, liquidity, and results of operations.”

Ally Financial [ALLY] disclosed on the same day in its Q1 earnings report that it had increased its provisions for loan losses by $504 million year-over-year “due to reserve build primarily driven by COVID-19 forecasted macroeconomic changes.”

During the analyst meeting, Ally CFO Jennifer LaClair said that about 25% of auto-loan borrowers had asked for a deferral of payment, and 18% had already enrolled in the program by the end of March 31. Ally allows auto-loan customers to defer payments for up to 120 days without late fee, but with finance charges accruing. This allows Ally to show the loans as current, rather than delinquent.

“We believe participation in this program will lower loss content,” LaClair told the analysts. “We will be able to track leading indicators of default and intervene early.”

Ally now also provides new auto loan borrowers who haven’t even made their first payment “the option to defer their first payment for 90 days without late fees being incurred but with finance charges accruing.”

These deferrals are not considered delinquencies. And it’s going to be tough to get a true sense as to who will still be making payments on their auto loans.

In mid-March, the world changed for subprime lenders. Delinquencies were already exploding in the Good Times, and now they’re in utter turmoil.

In addition, it is likely that prime loans are becoming delinquent as well, as many of these people too have lost their jobs – this includes dentists and other professionals with high incomes and big debts and lots of expenses and no savings, who’d suddenly had to close their operations, and their cash flow disappeared. If they fall behind on their debts, they’ll be subprime in a hurry.

In good times, subprime auto-loans are an immensely profitable business, with very high interest rates – often in the double digits – in a near-zero interest-rate environment.

The technologies for tracking the vehicles when it comes time to repossess them are effective; and a normally very liquid used-vehicle market via auctions around the country ensures that, normally, those repossessed vehicles are easy and quick to sell. There are losses and costs involved, but in good times, they’re more than compensated for by the big-fat interest rate margins the lenders make on all loans combined. And so the subprime lenders have gotten very aggressive since 2014. And for a while it worked.

Lenders have been able to securitize these loans and sell the asset-backed securities (ABS) into blistering demand from yield-chasing investors who have been bludgeoned by negative-interest-rate and low-interest-rate central-bank policies. Demand from those ABS investors fueled the subprime-auto-loan boom.

The Fed will try to force investors into a position where they feel they have to chase yield, and the Fed will try to create demand for these subprime auto loan ABS so that they don’t collapse.

But the normally liquid used-vehicle market isn’t that liquid anymore, as auction volume has plunged, and there is a flood of used-vehicle supply on the horizon from rental car companies trying to unload a big part of their now useless fleets, or creditors of rental-car companies taking possession of their collateral – the vehicles – and unloading them at the auctions, into very low demand.

This is a form of forced selling, and the whole industry is now afraid of it, and what it might do to wholesale prices. It will make it much harder for subprime auto lenders to dispose of their repos, and the losses will be greater, and there will be many more repos they’ll have to dispose of after all the deferrals run out and people cannot make their payments, and there won’t be enough new subprime lending business to cover up those losses.

No one has ever seen a mess like this before. Read… Used-Vehicle Wholesale Volume Collapsed, Prices Drop: Mega-Pain for Automakers, Leasing Companies, Rental-Car Companies, Banks, Bondholders, Stockholders

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I feel like it’s been mentioned somewhere before, but to get it right: 68 bn $ in auto loans means it’s about 3-4 million actual vehicles, that’s about correct?

Probably in the ballpark. If the average amount financed is $15k, it would amount to about 4.5 million vehicles. In a report last year, the NY Fed said about 7 million Americans were behind on their auto loans (I don’t remember if this was 60 days or 90+ days). So somewhere in that range.

Wolf Richter,

What is the reason that, especially during recessions, a lender doesn’t typically allow loan payments to be moved to the end of a loan, extending the loans length, but, preventing the loanee, from probably having to default?

Banks need cash flow too

contract law I assume also… A person signs a contract to repay and doesn’t, then it becomes a legal nightmare to allow some to extend and not others.. The money to fund also came from somewhere under a contract.. so the chains to undue are complex and probably in many cases intractable.

Thomas Roberts,

When payments aren’t made on time, and within the grace period, the loan is in default and is nonperforming.

So the bank may do a loan modification, to allow this (“extend and pretend”). But this is just a way of hiding or deferring loan losses. Regulators frown upon it too. That’s how banks, such as those in Italy, get loaded up to the gills with nonperforming loans from years ago that have never been written off, and that will never be collected. This leads to bank collapses.

Loan modifications are not uncommon – that is why the saying “extend and pretend” is a…saying.

The economy is in a fiscal induced high. Your key dates:

Mid June: Auto delinquencies due to shutdowns show up in servicer reports.

End of July: 3M extensions run out; Auto repos and dealer auctions re-start.

End of July: 600/week UI gravy train ends.

Sept: 6M of standard UI starts to run out for early layoff victims.

Sept: Home foreclosure moratorium ends.

Enjoy the summer.

FinePrintGuy:

Somewhat my own thoughts….

Beware the end of 3rd Quarter reports….might be downright “UGLY!”

On a lighter note construction in Santa Clara V. is reopening……medium to smaller sales/servicing firms are re-calling employees……many have received the “PPP” funds and are usefully putting those to good use.

Employees that have been home and receiving their supporting funds are still glad to be getting back to work.

Many weeks under the SIP protocol is leaving some indelible marks on the working pubic.

Enter ‘Mortimer’ a Twitter site on Vancouver BC Real Estate and there are some hard to believe ‘get me out of my lease’ offers. At least one is by an outfit ‘lease busters’ ( what does it tell you about leasing (like time shares) that there is a large industry devoted to reversing your decision)

Back to hard to believe, along with the mere 5K to take over a Land Rover lease, one guy is offering 30K to take over his lease. Give it a read. It can’t be true. Can it?

Sounds like a scam.

If you can’t make a lease payment, how can you come up with $30k?

Wow – I may be the first poster boy. All I can say is that I need a new (slightly used) car and I think it is about the perfect time to buy one !!

Wait a couple of months or more, the prices for unpopular models will go to the floor. They will have to get rid of their stock to accommodate pricier repossessed cars eventually.

You won’t even wait till they’re giving them away?

Thank you Wolf, as always.

“In mid-May, the world changed for subprime lenders. Delinquencies were already exploding in the Good Times, and now they’re in utter turmoil.”

Think this may be a typo. In ‘mid-March’ perhaps?

This issue has dogged me all my life :-]

Take Comfort Wolf! – this should be the worst “Issue” that you will need to deal with.. in the coming months and years :)

A car I was interested in was listed at $45K. I emailed the dealer and offered $40K. The dealer said, thanks but our price is $45K. I saw the car was sold today.

At Bring a Trailer, cars that sold for $50K 3 months ago are selling for $50K today. Zero effect whatsoever. If you don’t know that site, it’s a fun place if you’re into cars.

There may be 30M unemployed. But there are also still plenty of people buying cars.

You cannot sell 40 million vehicles a year (retail volume new and used combined in 2019) to 1 million well-to-do people. The math just doesn’t work out.

But you can sell 1 million expensive cars to 1 million well-to-do people. Then you only have to find customers for the other 39 million cars. Should be easy in this climate :-]

A lifelong hobby of mine is watching the used car market where I live. Good used cars priced fairly generally sell in 1-3 days (very quickly, strong economy here for many years). It’s now taking 2 weeks for good used cars to sell.

JSRG’s anecdotal references are just goofy, to put it mildly.

Wolf,

Given your experience in this market, when is a good time to start thinking about a used car? I assume right now there are still plenty of people holding out since we aren’t even 90 days into this yet.

Do you feel that the new car market will be hit as hard as the used one? Partly because of inventory of the 2020 model and assuming that the 2021 mode will be coming around in October time frame… will there even be a 2021 model year?

MCH,

I have never seen a market that is this screwed up. I can’t answer your question. Just keep looking.

If you can wait on used car purchase, then keep an eye on Hertz and the other rental car companies. They are looking to blow out their excess autos into the used market. But cannot so long as dealerships are closed and people are staying home. Also, a factor are banks and finance companies putting repo’ed cars into the secondary market. A wave of autos could start showing up in lots and online in August and Sept. Of course, you will be in competition…

MCH and Wolf, just wanted to add that in all my 60+ years of watching the SM, used car market, RE market, neither have I ever seen such a really messed up situation.

This from one who bought an old Rambler sedan for $50, and drove it for years with the only caveat, clearly and repeatedly mentioned by the seller, that it needed a quart of oil every 50 miles…

And SO many other $100 cars!!

My opinion, FWIW, is that at least in the short term, ”normal” ( not the antiques I bought for a hundred,, recently selling for $50-60K, sob sob) cars and SUVs that are way over abundant usually,,, (not trucks) will be going below all recent lows by a wide margin, 50% or so, and then will come back to par in about 18-30 months.

Yea, I am willing to bet I could walk on any lot and buy all the cars I want for 70 cents on the dollar. Sales are in the toilet, and dealerships have huge overhead. Manufactures are deep in debt and in big trouble and they are most likely giving huge incentives to dealers right now. It appears that it is not just the Fed who is trying to jawbone up prices. Good luck with that…

Actually. Jdog…from what I hear (where I live) new car sales are not in decline all that much. My son was recently dating a young lady who sells at a large local dealership and she has been doing just fine. She is 2nd generation at this facility and the family seems to be doing just fine. I drove through town, yesterday, following my recent hobby checking which businesses are open and working. The dealership service doors were all open (sunny day) and the hoods were up on the sales lot.

Yesterday, my daughter and son-in-law bought a used Honda CRV, low mileage and $1300 dollars worth of new rubber. They paid $7200 (cdn) and are tickled pink with it. The seller was asking 8k. Private sale for someone’s mother who could no longer drive. Life goes on for those with a few bucks, I guess.

“and she has been doing just fine”

With 20 to 25% of the employed population, well, um, unemployed, I would like to know the Wiccan incantations that manage to keep auto sales unchanged.

As Wolf points out, tens of millions of auto sales can’t be supported solely by the carriage trade.

“Life goes on for those with a few bucks, I guess.”

Yes, it does!

And some with a few bucks to spend, don’t.

They save it, in hard assets.

This for RD:

In spite of the very real, though slight possibility of default by the guv mint of USA,, my intention, if I ever do get a tax repayment, AKA whatever,,, from said mint,,, is to spend it on totally LIQUID assets.

Anything else in this market is sheer wishful thinking!

“Eat, Drink, and be Merry,,, for tomorrow WE DINE” Really and Truly MUST be the mantra for all patriotic persons of every nation and area of the world,,, at least for the next couple of years…

BTW,,, we went to the woods in 99, 45 acres of woods and some 10 of pastures, etc., did Great, almost all vegetables home grown and processed, only wood heat,,, etc., but, as age prevailed and much more elderly in laws needed help, there we went,,, just saying, don’t get too attached to any model,,, dare wines theories now being improved/understood as, ” the most adaptable succeed” ,,, not the former understanding(s), such as dominance, ”fittest” etc.

@VintageVNvet,

All your talk of wine got me to finally splurge and buy a bottle last week. Didn’t get such a good feeling as I thought I’d get (duh). Twice a year is fine I guess..

Good comment on expectations. My neighbor is approx. 95 years old. Looks 65. Strong and muscular. Rides a motorcycle. Drives and maintains many old luxury cars. Keeps his big place up. Just had a stroke. I thought he’d be out working on the place ’til he was 100+. Not sure how much he’ll recover, but won’t be the same after this.

1300 worth of tires on a CRV? those must be nice tires! in CA that jalopy can be VERY well shod for about $600

jdog,

You’re in dreamland. Car sales have been doing just fine. I’ve been shopping for a new truck for about 2 months. I held out for these mythical deals, but they simply do not exist. I finally closed on one last week. I got about as much of a discount off MSRP as I got 3 years ago, when I bought the last one. And I tried a lot of dealers, within about a 250 mile radius of me. Nobody was desperate to sell anything. The attitude was this is our price, take it or leave it.

New vehicle sales in April were down about 43% YOY. Not “doing just fine.”

JSRG, if you’re prefer to base all of your evaluations on personal experience instead of aggregate data, why do you even come to this site? One would think it would be to educate yourself about what the aggregate data says, but you always prefer to dismiss the data in preference for your own anecdotal data. Why bother even reading these articles?

States like MI, NJ, PA, NY and WA ordered car dealers in April closed and hence had 0 sales. I’d love to see some data of same store sales April 20 vs 19 for stores that were open the entire month. National numbers are meaningless when every state has a different set of rules for who can open.

Just Some Random Guy,

You should have waited longer. The heat will crank up on new car sales with 22 million people out of work. Also, the GM and owner at the dealership know their sales numbers on each brand/model/option package/color you target; they can see demand and logically know which ones will have a demand, even with this recession. The high demand cars would be more likely to hold their gross sales number, and therefore what they earn. If for example you wanted a Ram truck with no way cool option, they might blow it out and only make a minimum. BUT, if you want the way cool Ram loaded with all the goodies, a really nice black crew cab AWD, maybe Limited Edition Wild Ass Cowboy, then they aint gonna blow it out. They know their cowboy is still out there ready to fly in and rope it.

Hey big Z,,, the point of this wonderful site is that folks here are ready, willing, and able to ADD their personal anecdotal experience to the very clear data that Wolf presents to us in every post here, especially his very clear charts and graphs,,, (though I will add that his are better than the ones he brings in from time to time.)

If for no other reason,,, all of us are restricted by nature and so forth to anecdotal experience, as we cannot, certainly cannot, personally experience anywhere near the level of information that is now SO available for all of us these days.

According to many of the great teachers and sages and saints of many sacred traditions, we all live in the world of our own making! That some folks are able to get out of the limits that seems to posit,, to a world/cosmos/etc. not restricted by time or distance is presented as possible and so forth… please LMK if you know anyone who has done so.

Thank you.

This for RUK: EXACTLY!!

Bought my wife’s dream truck, a new 07, in early 08 for 30% off MSRP,,, bought my dream truck, a new 07, in 09 for over 50% off MSRP… Nuff said about ancient chevy her and history, eh?

Called my guy at the local RAM dealer couple of days ago, who I had told to call me, several months ago, when the 2021s came out so I could trade my 19 in,,, and, this call, told him to call me back as soon as the 2021s were available for approx 50% off MSRP,,, he laughed of course,,,

but I am quite sure that will happen sooner or later,,, OK, maybe this is the ”hard” asset that RD mentions??

Trucks aren’t cars. The pickups are moving (I hear) with 84 month zero-interest loans. Cars, on the other hand? Not so much.

Trucks are different…sedans are what will flood the market in 90 days.

What kind of car are you trying to buy? I doubt this will effect the enthusiast/ collector market as fast as regular commuter cars.

Could this be the end of ‘debt’ as we know it?

Not because the suckers were tapped, but because the loaners quit loaning, for fear of not getting back their principal.

Remember during great-depression, it was not ROI, it was ROM ( return of money );

Then & now, it ain’t what your earning, its what you can keep.

We just got a “just sign this check loan offer” yesterday. So no, they are still lending. The only difference is the interest rate actually dropped from the last time we received such an offer. Last time the interest was ~40% and now it is only 33%.

A high percentage of my junk email is from “friendly” lenders.

Maybe this is just a stupid question from a naive guy living in continental Europe, but here goes: on what planet does a company charge a preposterous interest rate of 40 % or does a client agree on paying such an insane rate?

It’s called subprime or predatory lending because they target people with bad credit ratings or in low income areas, the poor or the broke. The govt allows it because all usury laws were repealed under conservative administrations.

We lost everything in the GFC 1.0 and will never recover, so we are in their targeted demographic for predatory lending. We had a used car loan at 24% and were grateful to get it, because we needed the car to get to work. We also have a credit card with ~29% interest, which we keep for emergencies.

This is what they call the land of the free.

@Petunia

You have my sympathy for your predicament. But frankly, this is modern day financial enslavement. Is there no way to get out of such a debt trap? I get that most Americans tend to view countries in Europe as socialist enclaves (here we tend to frown upon that claim, mind you), but what you are describing is a capitalist system gone completely rogue. And disclaimer: I’m a firm believer of capitalism.

Petunia, if, as I suspect of you and most Wolferines, you are actually solvent and more,,, I also suspect we the wolfers will be getting tons of such solicitations going forward…

Good Luck and God Speed to all those folks reputed not to be able to withstand a $1K cash emergency,,,

As mentioned above, I plan to spend every nickle of any such tax rebate/stimulus and ASAP, to help out the folks who are most likely not getting anything out of any guv mint effort…

May even do again what I did in in the midst of ”ray guns recession,” and go downtown and give out $20s to anyone who looks hungry, without regard to age, race, color, gender preference, or any other of the factors the oligarchs use to divide us these days.

(Just to be clear,,, this is following many immigrant ancestors who volunteered in ”free clinics,” gave out cash,,, etc., etc., ALL of whom LOVED USA and were staunch and strict personal capitalists.)

Those offers stopped arriving in my mail 15 years ago when I put a freeze on my credit reports.

Lenders know asset deflation is a certainty now. That is why JP Morgan and Wells Fargo stopped making HELOC’s, they do not want to loan money on equity people really do not have. Used car prices are based on perception, not reality. A used car is only worth what someone is willing to pay. If no one is buying, that number usually decreases substantially with time.

I very rarely buy a car from a dealer, but when I do, I always make sure by the time I leave they are completely pissed off, and cussing like a sailor. If they aren’t, you did not get as good of deal as you could have.

“they are completely pissed off, and cussing like a sailor.”

And they still made money.

Sales and spiffs from add on revenue streams are how dealerships and salespeople survive.

Every second, of every day, when they are not actively working over a customer, they are thinking of better and better ways…to work over a customer.

Civilians tend to badly, badly underestimate the effort and expertise that goes into every aspect of the sales process…which the sales side is engaged in every hour of every day…not once every 4 or 5 years.

There is a (black) art and (mad) science to everything.

Where I live, dealers typically don’t make their money on the sales of new cars, but on servicing those cars afterwards. That’s when they start earning income.

That could be the end of Carefree Attitude.

I think it is a very first time since 1970s that western consumers were told that there are more important things than the Shopping.

That’s a mind blowing experience…

I also happy to read the word “paradigm” here. I very occassionally use in conversations only to hear “whaaaat is paradigm”?

Engin-i recall from the ’70’s: “…eventually, the Establishment absorbs and subverts the dominant paradigm…”.

May we all find a better day

So after 4 months of deferment people will just start paying again?

For a car that was free all this time?

I would like to see that.

Interest accrual will still happen, nothing is free.

Except for the ~30 million unemployed, who are likely to just. Drive for free and spend the UE benefits, and then be forced to declare BK since no jobs?

‘Round ‘ere, all car financing deals are ‘non-recourse loans’, meaning that they can repo the car and that clears the loan, including any outstanding interest.

In this environment, I suspect they intially will be quite large with the non-serviced loans because, just like 2008, they are probably stitting with a nice pile of debt on their books that they didn’t managed to get securitized and they will take losses on the repo’ed cars, if they can sell them.

Next move is that they will try to change the loan terms to convert them into recourse loans. So they at least can get your house also when they repo the car :).

When that fails, I think they will go to Zombie Mode: ‘You keep the loan + car and don’t tell anyone!’ and then just keep pretending that their assets are worth something and those loans are still performing.

Freee cars for deadbeats, basically!

Golly, it is almost like redlining industry sales by means of debt-fueled financing wholly predicated upon gvt interest rate destruction for two decades turned out to be a bad idea.

You know, as opposed to increasing productive efficiency and lowering the cost of cars, thereby expanding the sales base.

But “deflation”, something something, dark side, something something…

Thank heavens the housing market didn’t fall prey to the same politically inspired insanity…

Sam Zell says his tenants are still paying the rent.

Here is the problem with that post. What if you can’t increase efficiency and can’t lower the price to increase sales???? The U.S. has had a short termist issue since 2001, but it comes from a area of weakness.

BD,

Then you acknowledge the weakness and work to resolve it – you don’t literally paper over it by systemically debasing the currency (in practice confiscating post-taxed wealth) because it is politically easier.

Otherwise, you end up…here.

This isn’t some lightning bolt of unmerited malice, it is the predictable consequence of decades and decades of political and corporate cowardice and incompetence.

CAS 127,,, I would agree with you totally this time, but you leave out the really evil part,,, intentional criminal and corrupt behaviours that IMO are the worst part of the various and sundry and extensive continuing challenges for USA, and, as expressed on another post on WS re Europe situation, many other countries.

YES, we can do better,,, and YES we had better start doing better ASAP in USA,,, if for no other reason than that the pendulum that swings for all of us is getting ready to turn into a razor sharp device, possibly similar to the guillotine,,,TBD?? …

Wolf –

I am speachless. In the past few years, most everyone I see on the road in my town has bought a new car.

The good news is that as of today, in Wasington state, it is legal to shop for and potentially purchase a new car. Let’s see if there is any pent up demand…I doubt it.

Who in the heck is going to rush out in the near future and buy a new car? My biggest concern is that used car parts run short in supply.

I was born and raised in Detroit in the late 60’s and 70’s so I’ve been through this before. When I was a kid, some of those well-heeled folk who bought imports got there cars toarched, or flipped on end….the good old days.

It used to be that if you repo’ed a car, you detailed it and put it back on the lot to be sold again. Who is going to buy it in this market?

From the late 1960’s onwards I always bought my cars from a car auction. Most there in normal times were ex rental, but right at the tail end of the day came the part exchange deals, where a dealer was trying to get back at least the value given to make the sale of the new car. My advice would be to keep a close eye on auctions as they will make perhaps the best indicator of how values move during this new depression. Perhaps the bottom will be a long way away from where we are today.

Chris, is this auction information publicly available? I thought I heard that you need to be a dealer to be able to access car auction information (outside of eBay).

You don’t need to be a dealer, but most new car dealers have a subscription to Black Book which for a fee reports weekly values for used cars based on sales. How else would they know marketability on the trade in you just pulled up in? They check Black Book.

Not Canadian Black Book, a free publication, no idea how they work.

Chris/Karen: Keep an eye on Mannheim Auctions. It’s the Cox Automotive site and the info isn’t hard to get. Most recently, they were talking about auction volume being down 80-90% because dealers don’t want to buy used cars online.

Clete, Chris, and Kansas,

Here are a couple of articles on this topic of plunging auction volumes and prices:

https://wolfstreet.com/2020/04/24/used-vehicle-wholesale-volume-collapsed-prices-drop-mega-pain-for-automakers-leasing-companies-rental-car-companies-banks-bondholders-stockholders/

https://wolfstreet.com/2020/04/08/how-covid-19-lockdowns-impact-u-s-new-used-vehicle-sales-beyond-ugly/

Wolf, I think it will be even worse. On top of rental car fleets deflating, and repos of vehicles with delinquent loans, there’s a lot of other supply about to hit the used-vehicle market.

During the active times, many suburban families had 2 or more vehicles, to support two-job commuting, getting kids to/from school and activities, etc.

With extended shelter-in-place and the emerging trend of “work from home if at all possible”, there’s no need for 2 commuting vehicles.

School and childcare are largely offline for months, and with shelter-in-place the kids have nowhere to go, so someone’s going to be home with the kids at all times. Plus a high fraction of families now have one or more workers unemployed for some time…

Many folks are going to wake up to the fact that “new normal” isn’t going to be like “old normal”, and realize they don’t need that second vehicle for an extended time, and cut the expense if they can. With so much supply, it’ll be easy enough to get a cheap replacement car. The used, lease, and rental markets will all be desperate for customers.

Notice how the average individual has nothing left after room, board, transportation. Yes think about it, you work to provide a roof over your head, some food to eat, and a means to get to work. There is almost NO disposable income to enjoy life. How is that any different than being a slave who receives room and board? I guess its better not being beaten, but not much.

It was ever thus. All of this in an election year. Expect big change.

I think we abandoned slavery because all of the operating costs and risks of running slaves falls on their masters, which doesn’t scale … and for the same reasons, we won’t have any wide scale adoptation of robots!

Good observation.

But you see, it wasn’t Wall Street’s fault. About the Covid, that is.

Unfortunately, we can’t help the folks you refer to. All the money has already been spent giving free money to the Fed, Nancy, and Don’s rich friends, so they can issue more fraudulated junk bonds and stocks and the like so they can all get richer and richer. It’s called “The Credit “Market” which is our God and must be prioritized above all else including our lives.

We can’t help the 87% of Americans on public water/sewer, police, fire departments, public roads, public schools because “it’s their fault.” And while we fund every junkety junk bond and every over bought stock buy back failed corporation that ever existed, we must get rid of all those retirements the working folk have. Because it’s their fault.

And we must never ever provided people with universal free-at-the-point-care, healthcare.

87% of Americans on public water/sewer police force public schools.

Let’s sacrifice them to the Credit “Market” God. Our God will be happy then. Then all that remains is John Galt, with his own privately funded police/water/sewer/school/fire dept/train tracks.

Lol, you should create a global police force to stop tribal survival. Your “private wealth” is a scam, confiscated via the elite against tribe.

John Gault and a few peon “preppers”, who get along with private water, sewer, housing, power supply …

A much higher standard of living and more rights are the main differences between a slave and an average person in America. Though, the differences are diminishing over time.

As for the lack of disposable income, yes this is a major issue, the reasons why this happens is, because, of declining democracy, the lack of competition in America, and having a fiat currency. Basically, the top 1% have rigged the government, which allows them to rig the economy, which is partly enabled by a rigged currency “fiat”. Over time you get paid less “inflation adjusted”, while the prices are adjusted to continually charge more, to give you less. Competition and a hard currency, would make rigging prices harder.

To reverse the trend, the 99% would have to reestablish democracy, then bring back competition and switch back to a gold standard.

However, an enormous number of social issues, many of which are exacerbated by the 1% controlled media, make this nearly impossible to happen for the time being. Basically, too many middle aged and up are too comfortable with the current arrangement and will prevent any changes, until they become out numbered or their arrangement degrades. The only options are to either wait it out, jump ship “move out of America, my preferred option”, or force change with a minority “but still millions” of the population.

Gold Standard was a total copout and was anti-competition. It never worked. Science, with a joint ventures with the bourgeois state expanded market power. But the rate of innovation has slowed since 1900 and the science is already there. Hence, so much growth is almost now impossible except for population growth.

Too bad you think this way. But maybe you are right. Let’s bring back the gold standard con and a full scale liquidation. We can then liquidate the bourgeois state shortly after with its markets toast.

Thanks for fighting this round against the gold scam. If oil is worth nothing having infinite utility, gold is worth even less having low utility.

Saying gold (with a relatively fixed supply) is a scam, is not the same as saying that fiat (fixed only by the wisdom, foresight, and ethics of the political class…oh dear f*ing Christ) is not a vaster scam.

Your point about oil is well taken, the most reliable currency being one with actual utility (independent utility being a major backstop of value) and a fixed/predictable supply.

Oil succeeds on the first measure, but the ultimately unstable nature of OPEC (abetted by the increasingly unstable nature of the dollar) causes oil to fail on the second measure.

There is a reason why Bitcoin/its variants/Nvidia are a “thing”…it is because the tissue of faith in fiat is rent (after having been wrung out repeatedly, to save the incautious from their stupidities, at the cost of expropriating savers).

Stable supply block chain currencies do lack direct utility of course – perhaps the future lies in a hybrid of electronic/utility currencies.

Bobby Dents and Petunia,

LOL What!!!

You might be thinking of the Bretton Woods system, which is not the same thing.

There are different ways a gold standard can be implemented, and this does have huge implications.

The gold standard was never anti-competition, using gold/silver dates back thousands of years. Using precious metals worked with everything from ancient peaceful neighboring villages helping them trade and improve relations all the way to world empires. Using gold/silver kept prices and inflation from going crazy. This price stability is one part of preventing a rich class from totally owning and controlling a country. A hard currency is not a miracle cure, but, it’s one of the essential things needed.

Oil going negative is a completely different situation with nothing in common with gold standards. The reason gold standards work, is that you have a rare desirable easy to store commodity that can sit there forever, that backs your paper money. It’s not some arbitrary beaded necklace, it’s a natural element. The fact it isn’t needed for everyday life, like oil, is a plus, because, it won’t get used up. With Fiat money, all you have a piece of paper with a picture on it, the picture gives it value, and the price is easily manipulated. With a gold standard, you can issue paper money, with an exact weight in gold equivalent, no longer do you just have a piece of paper with a picture on it, you have a deed to a small stake in gold, that is easily traded with other people, or you could go to a designated bank and get that hard gold.

Gold/Silver/Platinum standards have their problems, but these problems add up to less issues than Fiat Money.

“the only money is gold, everything else is a credit”

Worth is defined what the price people are willing to pay. Governments still value gold as a type of non fiat back up currency, otherwise they would not buy it and

store it in large guarded facilities like Fort Knox.

Finite things like gold , silver, copper, rare earth metals steel oil, intellectual property etc.. are things that may be traded and bought without the inflation creating loan multiplier factor, and the destructive power to cause failures/bailouts through use of derivatives.

Currency should be tied to finite things of value that can be traded for other things or bought with currency linked to these things. It is not rocket science, it is honest money.

While we wait for the inevitable destruction of fiat created by fiat multiplier affected debt bombs, bring back Glass Segull as a start to prevent the creation of too many fiat debt bombs cubed from money created from nothing real.

Natural gas-one of the commodities that currency could be tied to; more bang for the buck.

Natural gas is the most undervalued commodity in the world. There is a lot of it. it has high joule efficiency/cost / productive output, and it is relatively clean compared to the best joule/ production commodity oil. If states demand going “green” too quick with their low joule/ production efficiency, this depression will last a long time.Natural gas should be the bridge.

The environmental destructive powers of gas are far less than oil’s i an oxygen rich environment with plenty of plant life. CH4 combines with oxygen and co2 is taken up by plants that produce O2

Often thought the “joule” would make an excellent accounting unit (and name!) for hard money backed by energy resources. Multiple energy sources can all be measured by that capacity for “work” – an inherent utility value to backstop the value of “money”.

Maybe better “Juul” … like, goes up in vape ?

Cas127:

Buckminster Fuller was on to this idea almost a century ago, and he expands on the idea in his 1980 masterpiece ‘Critical Path.’

“Common energy-value system for all humanity, costing (monetary ledger, i.e. money) will be expressed in kilowatt-hours, kilowatt-seconds, and watt-seconds of work.”

“These uniform energy valuations will replace all the world’s wildly-intervarying, opinion-gambled-upon,, top-power-manipulatable (the world’s central banks) monetary systems.” (page xxxiv of the introduction)

So yes, the Joule is a watt-second, and that would equal the smallest monetary unit of an energy based global currency.

Bucky was a smart mechanical engineer who was ahead of his time I reckon.

There is a new consciousness around gold. Just as the consciousness around this virus caused an unexpected reaction. Now governments want to reopen the economy and the public opposes the move. Gold has a place in this, and it involves bitcoin, which will never work as a store of value. If the bitcoin disappears after the transaction the user must park their money someplace.

I know a few people that are under 50 doing really well: two utility engineers, a civil engineer, a contract manager, owner of a garage door repair company, a boat mechanic for a large dealer, a human resources manager for a tech company. All working hard living the American dream.

Under 50, ain’t exactly young.

There are opportunities out there and some young people do very well, but, even though technology has advanced greatly, the large majority of young people are substantially less well off than their parents. Over time those opportunities get fewer and less good. Since I graduated high school about 10 years ago. The rental prices for a basic apartment and utilities in my city, have gone up at least 50 to 60%, food prices vary, but are on average, probably 2 to 3 times as much. College, healthcare, and much more continue to rise. Minimum wage rose, I think 75 cents an hour.

Alot of soon to be adults, especially in the expensive parts of the country, are going to be so poorly off their living situations will be comparable to the third world. Multiple teens to 1 studio apartment “in a sh*t area” in the country with the highest imprisonment rate in the world, no healthcare, junk food, can’t afford a car, or ever leave the city. And it continues to get worse.

Because of outsourcing and cheaper immigrants, it becomes very hard to know which career will lead to success. Those engineers may have their jobs outsourced, in the near future. Yes, I know utility engineers often have to travel to sites or possibly be the ones responsible for actually doing the work. But, cheaper immigrants can be used, or a combination of low skill low pay workers can do the work, while wearing something like Google glass, streaming what he sees to an engineer in a foreign country, who is giving him orders. They don’t have to replace everyone, just enough to, create excess supply of utility engineers to crash their pay.

Very big things are going to have to change in the future.

Hertz being on the edge of going belly up can’t help the market. You would think part of the reorg would be getting rid of some inventory to pay down debt.

Driving by the rental return lots at our airport last week, shows the spaces stuffed to the gills with autos. I mean you could not shoehorn another vehicle in there. I don’t think they can keep this up all summer. Reno, NV

From a limited number of sources, wholesale used car values have dropped over 10%. Retail used car prices have not dropped as much.

If people miss payments, their vehicles are repossessed and up for sale again. Last year repossessions were high too. That was with near record low unemployment. Now tens of millions lost their jobs.

Oil prices indicate miles driven per month is down. Demand to replace cars has decelerated. Who ever heard of negative oil futures? They bounced back a little. I do not know what is coming.

not directly related, but UK new car sales for April were a grand total of 4321 (appropriately, I guess), compared to 161,000 a year ago, and lowest total since 1946

it’s a new world out there alright

…and 90% of those are not ‘sales’ – they’re three-year leases.

Hence airfields and disused race circuits sitting full to the brim with three-year-old ‘handbacks’ for which there are no customers – why would you lease a used car when for a few pounds a month more you can have a new one?

Uber is laying off people in the thousands. How many from their car financing business? What is happening to those cars?

Maybe the Fed should just regulate credit to population growth. That would solve everything, but structurally raise unemployment. I just don’t see classical liberalism or Keynesian answers to this.

Look at Carvana’s stock. Crashed 70% at the start of the ‘Rona hysteria. Went from $110 to $30. Since that low, it’s up 250% to $85.

Everyone thought OMG OMG OMG nobody will buy a car anymore. And then everyone (well not everyone but mostly everyone) realized, wait a second, this is silly. Of course people will still buy cars once the ‘Rona silliness goes away.

There’s a key word so many people are not using. The word is temporary. This is all temporary. And we’re already on the tail end of this temporary event.

Just Some Random Guy

Driving up the price of a stock and actually selling 40 million cars a year is not the same thing. Why is this so hard to understand?

BTW, Carvana lost money every single quarter of its existence, revenue growth through Q4 stalled. It hasn’t reported Q1 yet, and Q2 will be a doozie.

But if you get your info about how the economy is doing from the price of a super-hyped money-losing stock, well, OK, that’s your thingy.

JSRG’s posts* need a disclaimer.

*FAKE NEWS!

I have a feeling we are just being trolled at this point.

I think we should stop feeding the troll.

VeryAmused,

Look, I think Just Some Random Guy is having fun with me. And I’m having fun with him. It’s like we’re playing ping-pong. As long as the game is interesting to watch, it’s good :-]

If you think that everything will be back to business after opening all the states, means you are really disconnected from reality.

It will take time for the dust to settle down.

Dudu,

You must live in NJ or MI or some other state with a power hungry governor. For most of the country everything is open again.

It will take some time to get back to 100%, sure. But that’s what he stimulus package was for. Provide time for things to ramp back up. Everyone on UE is getting $2500/mo from the feds on top of normal UE. Nobody has to pay mortgages for a year. That is a nice cushion to allow things to get back to normal.

Yesterday I was driving at 5:30pm and saw the first bumper to bumper traffic on the freeway in months. I was driving to look at houses for sale.

My world is back to normal. In a couple of weeks I’ll be able to go to a restaurant again, finally.

You should attempt to distinguish between speculation and reality.

I’ve been watching the new and used motorcycle market and I don’t see any significant price drops yet. Motorcycles are luxury discretionary items and usually the first thing sold in hard times.

While we don’t know when motorcycle dealerships will reopen here (if ever), on Monday several started re-listing their used stock to either drum up interest or secure a deposit from bargain hunters.

These are just two models I have been keeping an eye on (both collectibles and both are asking prices so subject to change).

BMW HP2 Sport: pre-crisis €25,000, now €16,000, down 36%

Moto Guzzi Daytona 1000IE: pre-crisis €20,000, now €12,000, down 40%

I expect the prices of both to go down even further at least until uncertainty starts waning.

We have already seen how Chinese authorities are performing veritable feats of acrobatics to convince people to go out and spend on big ticket items, be it a luxury handbag or a new Buick. Anything to get money rolling.

Here in the West it’s still too early for that, albeit promising that hard lockdowns won’t be re-imposed anymore and putting the doom-mongering on a diet would go a very long way towards calming frayed nerves while we move toward the post-emergency phase.

Instead of thinking about buying one or both those bikes as an alternative to worthless bonds and overpriced stocks I wake up sweating profusely at the thought the lockdown will be re-imposed. Subsisting on a steady diet of 3-4 hours sleep at night, most of it filled with nightmares, is not exactly helping me with discretionary spending.

MC01,

Yesterday I took my Aprilia Tuono in for the 1,000 km service/inspection. There were lots of new bikes on the showroom floor, more shoppers than I expected, and all four service bays had a bike and mechanic at work.

The top-end and mid-level 2019 bikes were discounted – but that’s not too surprising as the 2020 models are in stock too. No discounts were shown on the current year models though. Business looked brisk at the dealership and nothing seemed out of the ordinary to me.

Nice choice on looking for a BMW HP2 Sport! If you get the Guzzi, don’t ride it wearing shorts or your knees will cook behind the air cooled cylinders.

I picked up my first BMW Saturday with a 2016 M4 six speed manual. No sunroof; carbon-fibre lightweight top. A computer picks up the engine revs as the shifter moves towards a lower gear so you don’t have to tap the throttle while downshifting to match revs. A smart locking rear diff to boot. The thing really hooks up and takes off as you come out of a cloverleaf and into the highway!

What the hell, I’ve driven a few SC400 coupes for seventeen years now, so I decided not to wait any longer to step up to the next level.

If you’ve not had a chance to ride one, please try a Tuono just once if you can. You might decide it’s the way to go???

Good luck, and whatever you go with, enjoy & be safe!

The big problem with Aprilia’s is they do not keep their value well and have to fall a long way to find a buyer: around here they are extremely difficult to sell, not unlike the most recent Moto Guzzi models.

I have more bikes than I can ride already and this or these ones would just go straight to storage: as said they are an alternative to now yieldless bonds and massively overpriced stocks. I mean… AAPL over $300 in the present situation is not even funny anymore.

I know a person who has bought one of the ill-fated Norton V4’s as an alternative to bonds. In a decade that bike will be worth a fortune but from what we now know he’s made the right decision in sending it straight to storage.

Hertz filed for bankruptcy protection this week. They’re trying to work out a chapter 11 restructuring.

Hertz also lost over 3000 cars in the rental car fire in Ft Myers Florida in early April. That fire caused almost $50 million in damage – its still up in the air if insurance will cover this.

Initially, I wondered how you can lose 3500 cars in a fire without an Olympic class torchbearer named “Guido the Match”…but then I read that this army of unrentable vehicles was being stored in a grassy field…

2 to 1 the insurance companies ain’t paying, 14000 wheels among the wildflowers not exactly being proper, prudent storage.

Hehehe – the Pizza & Kebab places here do the same all the time!

Hertz now lobbying for federal “Kash for Kebabs” buyout program…

The mortgage market is seeing demand. From today’s weekly application report:

Mortgage applications to purchase a home rose for the third straight week, up 7% from a week earlier. Purchase volume was still 19% lower annually, but that annual loss is shrinking by the week. Just three weeks ago, purchase volume was down 35% annually. Demand last week was led by strong growth in Arizona, Texas and California.

Buyers are responding to incredibly low interest rates as well as to new technology and processes that allow them to house-hunt from afar.

Mortgage applications were still down 19% from the same week a year ago.

There is no demand. Have no clue what he is talking about.

Take out NY and NJ which are still on lockdown and those numbers are even better. The ‘Rona nonsense is over for the vast majority of the public. They’re back to buying houses, buying cars, and living their lives. I think the dis-believers are those who live in NYC and other places that are still on full lockdown. They refuse to believe the rest of the world has moved on, I guess.

The AEI flash housing indicators seem to support this. Huge differences between metro areas as to how much sales are down. Pittsburgh, Philadelphia, Detroit, Denver, Boston, Kansas City, Miami, San Francisco and Seattle are all down over 30% YoY (and last spring was tepid in many of these markets). Some of this can be directly tied to an equal lack of supply coming on the market in these areas.

Home Price Appreciation has seen a marked decline YoY nearly everywhere, though. Only negative in CA thus far.

Why donyou think cacc is holding up well despite no earnings visibility? Ally is down almost twice % wise?

I say another one of those useless bay area “sharing” companies are on their last breath. AirBnB. Stick a fork in it.

The silver lining in this COVID all the useless silicon valley companies are going under. They are going to be replaced with new companies that create jobs … those jobs will be from bringing back all the items outsourced to China.

Lol, no they won’t. You just can’t stop posting.

Lets see about that – Donald Trump has gone back to the “China screwed up!” right after sending Pompeo to town with “China totally did this on purpose!”

So what happen to the IPO Bubble that was supposed to make everyone in the Bay Area millionaires? The prediction that house prices will go to the moon as a result? How’s Uber, Lyft, Pinterest, Slack, etc?

My brother just retired from a paper mill ( 47 years and missed 1 week) . He said all the young knobs were giddy over walking away from All their debts including car loans. They have figured out that defaulting together beats voting for the same shit show separately. They are just following numbchucks and the top captains of industry example of grab everything you can while you can.

A big part of the problem in car markets is the “You must buy what we want to sell” attitude. Great plan if you have a captive audience falling for your sales pitch and locked into financing. The people who wanted it have no more buying power. But those with money to choose (ie, Savers) do not always want to get “your” product. So if you don’t make what they like you are stuck with unsellable crap full of unwanted electronic junk toys that none of them will pay for…they just hang on to what they have or shop for another one that still runs.

Please address those responsible – THE GOVERNMENT. Government dictates what the vehicle manufacturers produce.

Nope. Capitalist. Look at toilet paper

LOL parroting exactly what’s been put into your brain by 40 years of anti-state propaganda funded by wealthy people who don’t believe they should pay tax…

“It’s all the fault of [bloated, inefficient] government and regulation!” – over and over ad nauseum like a needle stuck on a record.

@MD:

Just like you’re parroting what’s been put into your brain by 100’s of years of “we know better than you” talking down to the great unwashed andfunded by wealthy people who divert tax dollars into their own pockets……

Here’s a short list of Federally mandated safety equipment:

Backup cameras

Airbags (SRS – first word being “supplemental”)

Tire Pressure Monitors

OBD

Lots more…. but 3 of the 4 listed above, while required, can be mitigated by a reasonably competent operator.

folks we’re still in the “deer in the headlights” moment. Everybody I talk to thinks this is temporary. Not on your life I said. Why? Because it’s an election year. Who really knows how bad this economy( you notice I didn’t Say the stock Casino) will get by Nov. It doesn’t surprise me that some car dealers are holding firm on price.

Car dealers can hold as long as they want. I don’t need a car at any price. However, they can’t eat the car so eventually they will need to sell it. Maybe the FED will buy them as Cash for Clunkers 2.0.

1) There will be no inflation in the next 5 to 10 years, because the 10Y/10Y is 1% and 5Y/5Y is 0.7%.

2) But there was inflation in the automotive industry since silicon

valley took over at the bottom of 2009.

3) Higher industry CPI reduce the real value of auto loans.

4) Fred : New and used Auto and Truck Loans index, adjusted to

industry CPI peaked on Sept 2009 @ 182 and tumbled to 93 on Mar 2020.

5) Since 2016 this index is shortening its negative thrust and falling less.

6) Most of the contamination is behind us.

7) This index had a bubble that collapsed and reached it previous

four years trading range from 2004 – 2008.

8) When Mountz bots will collide in their warehouses due to cyber attack, and delinquent cars and trucks will be plucked by banks repo,

both high tech and the auto industry will suffer tremendously.

9) New type of primitive & inexpensive form of transportation will emerge. They will serve their customers, without wall street and SF intellectual elite, or gov influence.

I am clueless as well. Transportation is cheaper than ever.

In comparison to many other massed produced goods?

Really? Let’s see, roughly….$5K bomber car equals 5Th. loaves @ $1 per. Later-$25K computer cutesy car equals 12.5Th. loaves @ $2 per. Cheaper only in some perspectives.

“New type of primitive & inexpensive form of transportation will emerge. They will serve their customers, without wall street and SF intellectual elite, or gov influence.”

Now I know you’re a quack. ;)

Wolf does it I believe. It’s called walking.

Walking..shoe leather. :-) My 1979 Trail 90.

TBAC report and meeting minutes are out today, and apparently some parts of the bond market are having strong reactions.

I use bond ETFs prices as an indicator. Take a look at VEB and VCLT for 2% drops in value. In contrast, junk bond ETFs like HYG and JNK have barely budged. Maybe those Fed SPVs started buying the used-to-be-not-junk bonds?

Meanwhile, part is the stock market is up, under these condistions? Makes little sense to me.

Yes, watch Countrywide 2007. The primary dealers would love this subprime collapse. They have been eating sales since 2014.

The problem with the classical liberals on this site are their elitism. They don’t take any other ideas, just the ones Mises, Hayek and Rothbard all financed by the Rockefeller Foundation fwiw spewed a 75-100 years ago. They are as bad as Keynesians outside post-keynsians, who admit capitalism is in trouble. Roberts, socijism, Engel, timbers…..over and over again. Same bs

Here is a message idiots: profit in capitalism is all about paying debt obligations. Period. It’s a ponzi scheme. It always has been. The Scientific Revolutions made it viable for awhile, but the low hanging fruit is gone. Admit it. No gold standard, expensive credit system is gonna change that(and frankly, the gold standard inflated credit as well).

Move on.

Social Nationalist, I am that stupid.

I come from a land of chaos, yet you seem to have it all figured out.

As everything is obvious to you, rather than calling everyone stupid, can you please enlighten us all?

I understand that your handle “social nationalist” sums it all up but I have not idea what that means.

We have a number of comments that: ‘nothing has changed’

Even a train wreck takes time. If the loco on a slow half- mile long train goes of the trestle, the poor saps in the caboose won’t know about it for several minutes.

Indeed a motorcycle is a luxury discretionary item. Therefore the owners will have some financial strength or at least credit. It will tested in a recession but not within two months.

A car lot refuses to lower the price on a new car. Unless they bought it last week, they are into it for the manufacturer’s price, which was established before the crisis. A new car is essentially ‘new’ for up to a year and a bit beyond. It’s not like day- old chicken that must be moved. Assuming they can pay their rent etc. the only thing that can lower the price below dealer’s invoice would be pressure from the manufacturer. The only thing that will make the manufacturer do that is similar pressure on it. That can happen. It may happen. But not in two months. Yes, Ford is in a squeeze but it drew down all its revolvers and has billions on hand. It is not going to force a fire sale on new product anytime soon, let alone two months after the slowdown.

This doesn’t apply to ex-rental or off- lease or just almost new second- hand because the buyer is not up against the determination and necessity of the manufacturer to protect the new price. It hasn’t made financial sense to buy new for years, less now.

Fire sales only happen when the owner has no choice ( like having nowhere to store oil he unexpectedly owns)

Since it can take 6 months or more to foreclose on a house, it doesn’t make sense to expect fire sales of RE two months into a crash. Or to expect a sudden halt in construction of basic houses where the lot has already been purchased by someone. With the cost of the lot easily equaling half the total cost or more, it is very expensive to let lots sit. The decision to build comes when the builder buys the lot, which in the vast majority of projects will have been before 2020 before anyone heard of the virus.

There is water in a hose after the tap is shut.

So let’s give this six months before deciding that nothing has changed.

Very true.

In addition, the sentiment hasn’t changed much yet. Optimism doesn’t vane as the markets rebound, economy reopens etc.

But let’s see what happens when the next leg lower starts, especially it it really will be the 3rd of 3rd (as Michael Engel predicted :)

nick kelly …

Things have changed, but we will get a breather for the summer. Note how the economy is being re-opened just as the weather warms up. The warmer weather should keep the virus in check such that the economy can perform decently. The virus will return sometime after the election. Their needs to be a medical treatment or a vaccine before that time, or things will change for the worse.

Posted by Nick Kelly: “Assuming they can pay their rent etc. the only thing that can lower the price below dealer’s invoice would be pressure from the manufacturer.”

One thing in the “etc” for a dealer is the interest cost of its Floor Plan. The Floor Plan being the financing from the bank to put all those cars on the lot. You don’t think the new car dealer shelled out his cash for all those cars; its financed.

So, the invoice paid by the dealer is with borrowed money. On the back end when the car is sold a percentage is paid to the dealer from the manufacturer, called the Hold Back.

New car dealers can easily go below invoice if they choose because the Hold Back is paid when they sell.

For most sales the Hold Back is sacrosanct. If they have a car for a long time and that floor plan finance charge is being carried, then maybe. Also, if a drek walks in and he can get financed at 30%, then what the hell, burn the hold back to get him done.

New car sales 101: Hold Back, Floor Plan

I knew there was much more detail to the car biz, just trying to make the point that it’s too soon to expect fires sales on new cars.

BTW: in times of earlier stress, much less than it looks like this is going to be, the manufacturer aids dealers financially. They will do this rather than seeing the lot dump new product. Have you ever seen a brand new car offered for sale by a bank repo?

Apart from that aid, which we may never know the details of since the information is not public, we DO know that the dealerships are being allowed at least forbearance on their loans, and are getting actual gov cash for salaried mechanics etc. They aren’t going to be forced to the wall in the near term.

101 of the biz bailouts.

\\\

I have noticed certain car industry suppliers subtracting all their jobvacancies from their site, to the point where for a 30k employer there are 10 positions open (EU+USA+China). This is not a good sign as it indicates either panic in management (overzeolus austerity policy) or low levels of cash, or even worse…both.

\\\

It is a frequent story that workers are sent home at 50-70% of base pay, or reduced workweek for reduced pay. It is now frequent news that temporary or subcontraced employees have recieved info that their contract is termiated (Europe).

\\\

Though more serious companies are still in hiring mode, as they have alocated budgets for development. Who is wise spends money on development before the market rebounds. Not sure what the situation in the US is.

\\\

VW group is looking what to do with it’s 370000 emplyees given the crisis and switching to EVs (engine building division which was key in tech developmnt is now obsolete).

\\\

In a speciifc division of one of the suppliers, the CEO is sending a henchmen (high level manager with high levels of autonomy and authroity) to “clean up the sleepers”, and “get the projects going”. It seems that some companies will use the oportunity to optimize…

\\\

Every company is treating this situation differently, some for the worse some for the better. Time will tell who was right.

\\\

Keeping my nearly twenty year old PU, expect the value to double in the next year but that is just a gut feeling. My favorite used car indicator is registration fees, and they are climbing in my state.

So CACC is going to ZERO?

I doubt it. They securitize their subprime loans into ABS and sell them, and much of the risk is transferred to the holders of those ABS, in a pension fund near you :-]

Ah, thanks for the reply. I’ve been in and out of puts and also short the stock thinking it was another DSL and FED. ALT-A lendors that both went to zero. Seems similar. Andrew Left with citron has a report on there saying these guys are a zero and their entire business model doesn’t exist anymore. He’s not always right, in fact he’s had some pretty horrible calls lol but his thesis did make sense.

Short_Seller_Blake,

I agree that the shares should “logically” take a big hit (but forget logic in this market). I just doubt they’ll go to zero. These people have been around for a long time, and they know how to slough off much of the risk to others.

Motorcycles, classic cars, 2nd cars, boats, Rv’s, worthwhile collectibles will follow this pattern:

1- 3 months..Prices firm

3-6 months…prices down 25%

6-12 months prices down 50%

12 months plus….Just give me something before it is scrapped.

This is what I experienced in 2008-09 and curious if it will be faster this time. I imagine so.

More economic news out. The current leader of “greatest economy ever” will join previous leader of “greatest economy ever” as being the only ones in all U.S. history to never achieving a 3% growth rate. But that could change if he gets another 4 years, which the other is doing their absolute best in helping him to.

Possibly. If the Commucrats screw up as expected and put the Renuticans back in the WhoresHouse, his sidekick might have to finish the term. That boy looks like he’s been eating too much, taking too many drugs, or both…and the stare into space doesn’t seem to go with the job.

I like Comiecrat better. LOL

risk in Subprime is mispriced….What we bought subprime ABS for in 1998 vs today is hilarious…debt sleeps with the devil, it woke up early….

LTV and Risk are going to have to look at buyers differently, we installed a check verification in our app just to see if they had POI to keep approval rate higher