I’m not worried about banks or investors in subprime-credit-card backed securities. If they take a beating, fine. But what does this bifurcation tell us about consumers?

By Wolf Richter for WOLF STREET.

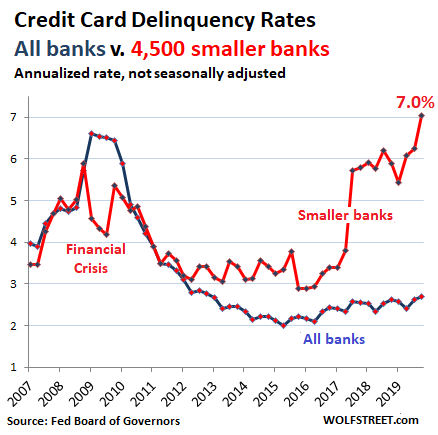

The rate of credit card balances that are 30 days or more delinquent at the 4,500 or so commercial banks that are smaller than the top 100 banks spiked to 7.05% in the fourth quarter, the highest delinquency rate in the data going back to the 1980s (red line).

But at the largest 100 banks, the credit-card delinquency rate was 2.48%, which kept the overall credit-card delinquency rate at all commercial banks at 2.7% (blue line), though it was the highest since 2012, according to the Federal Reserve. What’s going on here, with this bifurcation of the delinquency rates and what does that tell us about consumers?

Clearly, those consumers that have obtained credit cards at the smaller banks are in a heap of trouble and are falling behind at a historically high rate. But consumers that got their credit cards at the big banks – lured by 2% cash-back offers and other benefits that are being heavily promoted to consumers with top credit scores – do not feel the pain.

A similarly disturbing trend is going on with auto loans. Seriously delinquent auto loans jumped to 4.94% of total auto loans and leases outstanding. This is higher than the delinquency rate in Q3 2010 amid the worst unemployment crisis since the Great Depression. On closer inspection, there was that bifurcation again; prime-rated loans had historically low delinquency rates; but a shocking 23% of all subprime loans were 90+ days delinquent.

During the Financial Crisis, delinquencies on credit cards and auto loans were soaring because over 10 million people had lost their jobs and they couldn’t make their payments.

But these are the good times – with the unemployment rate near historic lows. And yet, there are these skyrocketing delinquency rates in the subprime subset of credit cards and auto loans. It means these people are working, and they’re falling behind their debts.

Consumers with subprime credit scores (below 620) can still get credit cards, but under subprime terms – namely interest rates of 25% or 30% or more.

These rates comes at a time when, according to the FDIC, banks’ average cost of funding was around 1.0%. The difference between a bank’s average cost of funding and the interest it charges is its net interest margin. For banks, subprime credit-card balances, with interest rates of 30%, are the most profitable assets out there.

To get these profits, banks take big risks. Even when a portion of those credit card accounts have to be written off and sold for cents on the dollar to a collection agency, they’re still profitable overall. In addition, banks offload part of the subprime risk to investors by securitizing these subprime credit-card loans into asset backed securities. And investors love them and chase after them for the slightly higher yield they offer.

So I’m not worried about the banks or the investors. If they take a beating, so be it. But what does it tell us about the consumers?

The largest 100 banks have a delinquency rate of just 2.48%, which is low by historical standards. With their sophisticated marketing, they go aggressively after consumers with high credit scores and high incomes, and to get them, the big banks offer big benefits, and so a bidding war has broken out for these high-credit-score consumers, with “2% cash back on every purchase” and other benefits that small banks cannot offer.

These big banks have most of the customers and most of the credit card balances (assets for the banks). Their special offers rope in the lion’s share of consumers with top credit scores. They also issue credit cards to consumers with subprime credit scores. But since these big banks have the lion’s share of prime-rated customers, their subprime customers, when they default, don’t weigh heavily in the mix.

Smaller banks can’t offer the same incentives and don’t have the marketing resources the big banks have. But subprime-rated customers are easy to hand a credit card that comes with few incentives and charges a 30% interest. And those credit card balances, producing 30% interest income, do wonders for a small bank’s bottom line. Proportionately, these small banks end up with more subprime customers. And in this way, they become a gauge for subprime credit card delinquencies.

So why are these delinquencies spiking now? We haven’t seen millions of people getting laid off. These are the good times.

It’s a sign of the sharp bifurcation of the economy for consumers. One group of consumers is doing well. They have rising incomes, and they can afford the surging home prices, the surging healthcare costs, and the surging new-vehicle prices. Those price increases are not reflected in the inflation measures. For example, the price of a Ford F-150 XLT has skyrocketed 163% since 1990 while the official CPI for new vehicles over the same period has increased only 22% thanks to “hedonic quality adjustments” and other adjustments (here is my pickup truck price index chart that overlays both).

Same with used cars. The official CPI for used cars has declined by 11% since 1995, an amazing feat of hedonic quality adjustments, as actual used-car prices have soared since 1995.

There are other consumers whose incomes have not budged much – maybe it went up in line with CPI, but CPI doesn’t reflect actual price increases of cars and homes and other items. Everything big they’re trying to buy or rent or use has soared in price – new and used vehicles, housing, healthcare, education, etc. And those consumers, though they’re working hard, are getting squeezed. That’s the bifurcation.

These are the people that are strung out. They have jobs but are living from paycheck to paycheck, and not because they’re splurging but because, at their level of the economy, prices of basic goods and services have run away from them.

And this can happen from one day to the next, for example when the landlord raises the rent by 15%, or when the car turns into a hopeless heap and has to be replaced, or when the insurance premium jumps 25%, or when the kid ends up in the emergency room. Or a combination. And suddenly, there is no money left to make the minimum payment on the credit card.

And this is happening while people are working. This subgroup of consumers that are getting squeezed is growing, and their problems are growing, and their credit-card delinquencies and auto-loan delinquencies are spiking into the stratosphere like never before – while many other consumers have the best years of their lives, relishing with gusto the out-of-control “speculative energy,” the blistering highs in the stock market, and the surging prices of their homes, vacation homes, and investment properties. And that’s the bifurcation that we’re seeing in the chart above.

My “Credit-Card Spread Index” blows out. Heck if I knew what that means, but it doesn’t mean anything good. Read... Credit-Card Interest Rates Soar to Record High, Bond Yields Drop to Record Low: What Gives?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Because the landlord is just a mean guy/gal…or maybe his/her property taxes just shot through the roof.

Which is a topic missing from your essay. Especially considering that the aggregate of all taxes easily steals 50% of the gross income of the typical middle class worker. And is continuing to increase overall.

“And this can happen from one day to the next, for example when the landlord raises the rent by 15…”

And yet because of tax laws, anyone who is rich need never pay more than 15% in taxes.

And that’s just rich POEPLE.

Corporations – which Ivey League educated folks tell are also people – I suspect can pay even less, because some folks actually tell us corporations – a legal construct – are people. In the exact say way that parking laws – a legal construct – are also people, endowed by God with Constitutional rights, according the Ivy League folks on the Supreme Court.

There are definitely tax loopholes for rich people, but there are some for regular folks too. A Roth IRA is a good one. You can buy a REIT in a Roth and no income taxes are paid by the REIT or you forever. Hard for a rich person to get that deal.

Also, don’t forget if a rich person is a shareholder the corporation is getting taxed usually at 20% each year and then Fed’s get another 15% when sold.

Actually, the whole ROTH IRA thing is kinda bogus. It is much better to compound your wealth tax free in a Traditional IRA or a Good 401k (preferably one that has an SDA Component).

Most Folks are also fairly oblivious that they can enjoy much of the tax free aspects of a ROTH by just buying Stocks in a “taxable brokerage acct.” due the fact that most equities pay Qualified Dividends and are tax free for most regular income earners, as are Long Term Capital Gains. There’s also the IRA Rollover once you have compounded your money tax free.

Folks should go over the MadFientist website where he breaks all this down. I don’t however, agree with whole Boglehead style of an investing approach that he takes. However, I learned a lot over there as I have also learned a lot here on Wolfstreet.

The Colorado Kid,

“… It is much better to compound your wealth tax free in a Traditional IRA or a Good 401k (preferably one that has an SDA Component)…”

There may be a little bit of confusion in terms of the terminology here, of “compound your wealth tax free.” Traditional IRAs and 401ks are not “tax free.” They’re tax deferred. You will be forced to pay taxes on the money you put into them, and on the money you made in them, when you (will be forced to) withdraw the money when you hit certain age levels.

You’re assuming the “regular folks” (whatever that means!) have the wherewithall to put $$$ into an IRA. 57% of Americans don’t have the cash resources to cover a $500 emergency expense. A person in NY making $75,000 has a marginal tax rate of 36% so I really feel it for you rich guys having to pay 15% on your CGs.

No. Read up on Carried Interest.

This “corporations are people” story is misleading. For certain legal situations they are indeed treated as people, but not for everything.

I do agree, however, that if they are treated as people ( a legal privilege) for some things, they should not be exempted from being treated as people for tax purposes.

There should be some kind of alternative minimum tax for corporations since there is one for people…

wkevinw:

There was a corporate alternative minimum tax until just recently. The Trump tax act repealed it, effective tax year 2018.

I’m guessing you probably knew that, but perhaps some readers don’t, so thought I would throw that out there.

AMT for corporations was avoided using several (questionable!?) loopholes:

– off shore sheltering, – options are sheltered – accelerated depreciation.

So, the AMT was easily avoided before the 2018 change (removing corporate AMT). That change had a very small impact overall.

Corporations such as publicly traded C-Corps are taxed at the corporate level, then at the share holder level. That’s called double-taxation. Who really believe this is fair? As for rich people paying 15%, please tell us how this is done, you’d make a fortune selling how-to books. Last I checked, the highest income earners in California are paying 50.3% in income taxes. And let’s not forget AMT (alternative minimum tax).

It’s called Carried Interest. The super rich use it to classify their income as capital gains, thus never paying more than 15% (it might have gone up to 20%, as I don’t have the pleasure of taking advantage I am not abreast of the latest). And I don’t believe it’s not going to show up under any income tax figures you guys are reporting because it’s moved into capital gains.

Pardon me, But Many/most of the biggest corporations pay almost no income taxes and even get tax subsidy in their income, because they offshore their profit to zero or near zero tax nations.

Timbers,

You have sort of half-heard the story on carried interest…it really only applies to the general partners running VC and PE firms, which is a small, small subset of “rich” people.

Not thrilled with favorable treatment of CG myself…but CG reform could lower income tax while equalizing CG.

Trading some billionaire hustler for some DC hustler is not really a step forward.

BTW – define “rich” for us…the Left tends to vastly exaggerate what even utter expropriation of the mega rich could raise…eternally necessitating the continued downward definition of “rich” – in order to fund frequently crooked, almost always negligently overseen society wide schemes.

Timbers,

Carried interest is taxed at capital gain rates, for the wealthy, this is 23.8%, not 15%. This is far below the top rate for regular income of 37%, but doesn’t apply to earned income, like for pro athletes or entertainers. Of course most extremely wealthy people take income in capital gains or dividends at this same rate rather than regular income.

If you want to really talk about who is getting screwed by the tax code, it is the upper income married couple in the 25-37% bracket range who work for a living, they pay more proportionally than most billionaires and they also are paying social security taxes on a portion of their income. For instance, the marginal tax rate for a married couple making 170K (well off compared with the median, but lower middle class in NYC or SF) is slightly higher than the rate for Bill Gates living off dividends. That’s absolutely nuts.

I’d love to see a flat rate of 25% or so with no exemptions starting at around 25K per capital, with no payroll taxes, just a single income tax, for all kinds of income.

Cas127, when you are in that income bracket, everything can fit into vc & pe, weather it is, or not. Hence this tax break to the super rich is vastly under stated.

Happy1, are factoring in that deductions against this income can be taken, that wages can’t take? I think you are mistaken in suggesting the rate you mentioned is comparable.

Timbers,

The average rate for the ultra wealthy that I am quoting comes from an analysis in the Washington Post that compared the income rate of the 400 wealthiest families with those of the bottom 50%, and found that the rate for the ultra wealthy was about 25%, slightly less than the overall rate for the bottom 50%. I would provide the link but that tends to put my posts in temporary purgatory but it is easily found on a Google search.

The Post article is somewhat misleading as it does not include the value of transfer payments to the lower 50%, if the value of those payments is included, it would obviously blunt the effect of taxation on the lower 50%.

AMT limits the value of deductions for anyone earning more than a few hundred K dollars including the ultra wealthy. There are a few strategies to limit taxation such as municipal bonds but it is hard to have become a billionaire on the basis of municipal bond payments.

The real injustice is that the merely wealthy, in the top 1% range, are paying a higher rate than the 400 wealthiest families.

Sigh; here we go again. There are several sources for this kind of stuff.

Top 50% of income group (over $41,740) pays 97% of all income tax.

Bottom 50% (under $41,740) pays 3%.

Top 1% (over $515,371 income) pays 37% of all income tax.

Top 5% (over $208,053) pays 59%.

Top 10% (over $145,135) pays 70%.

etc. https://www.ntu.org/foundation/tax-page/who-pays-income-taxes

Sign….here I go again. Your break down of the stats is EXTREMELY misleading. You cut if off at $515k. That’s not the level the rich can use a tax law to ensure they NEVER EVER pay more that 15%. You need to make millions.

The top 1% make about 20% of the income. So they make 20% and pay 37% of the taxes.

If you go by “disposable income”, they make much more than 20% of the “disposable income”.

Roughly speaking the progressiveness of the the individual income tax does what is designed to do. Whether that’s what people want is a different discussion.

Nope. I not talking the top 1%, I’m talking the top 0.1% or 0.01%, at which point the progressive tax rate most definitely does NOT do what it was designed to do, because the rate is never more that 15%.

So here it is….it’s called Carried Interest. The super rich use it to classify their income as capital gains, thus never paying more than 15% (it might have gone up to 20%). And I don’t believe it’s not going to show up under any income tax figures you guys are reporting because it’s moved into capital gains.

Timbers is correct that at the 0.1% level, the top of the top, they pay a slightly lower rate than the 1% because of much of that income being mostly capital gains, whereas the 1% are paying more 37% bracket on earned income. Of course what I would favor is cutting the earned income rate to the capital gains top rate of about 25% rather than raising taxes on the extremely wealthy, but everyone has a different take on that. I guess what I’m saying is please tax me like a billionaire rather than a pro athlete.

It has been a while since I’ve commented on this, but here it is:

A Modified Flat Tax levels the playing field. Start with a ‘Livable Wage’ that has no federal tax liability. Granted, a ‘Livable Wage’ is different in Wolf’s hometown versus mine, but let’s go with $2,500 per month.

So after the first $30,000, all income – regardless of what type of income it is – has a 20% tax. Wages, dividends, carried interest and capital gains – both short term and long term – are taxed at a flat 20%.

Those that are just getting by pay nothing to the IRS. Everybody else is taxed the same after the first 30k.

On credit cards: They come in handy sometimes, but they can bite you if you don’t, or can’t, treat them with the monthly payments they demand. Yeah, that’s an over-simplification, but it pretty much covers it, eh?

And to underscore a point…, ‘the Top 1% pays 37% of all income tax…,’ And how much in total wealth do they hold compared to the 99%?

Timbers. You seriously should go into tax consultation. How anyone rich or poor can turn regular income into capital gains to cut their tax liability down to 15% or even 20% without going to jail is news to my ears. I’m sure top income earners everywhere, pro athletes, entertainers, etc will pay you millions even for just one year of tax consultation. Keep on smoking it!

This article underscores the insidiousness, nay criminality, of the un-elected, responsible-to-no-one, Fed claiming there is no inflation. Inflation is CRUSHING many of the non-elite. But the Fed seems to have no idea – too busy partying with Bezos and with their unwavering faith in their faulty yardsticks (CPI) and bogus models.

The FED couldn’t care less about “the little guy” everybody knows that

Not true, if you listen to the Congressional testimony you know there are several consumer issues pending at the Fed; faster transfer of funds. It does amaze me that you can buy and sell stock certificates in the blink of an eye, but it takes three or more days to transfer a few hundred dollars between across town banks. The Feds mandate is market stability, and employment, as well as maintaining an inflation buffer. They no longer support the “dollar”, or “fiscal” policy concerns, by their own statement. You could also say their policy toward commercial banks, inverting the yield curve, is more consumer friendly, than supportive of bank profits or lending. If their policies have any direct outcome from 2008, they support mortgage holders, and by extension renters. While we might disdain policies which create subprime auto loans, an automobile is all that keeps many people from poverty, and keeps those who are there in some kind of shelter (the motor-homeless). The destruction of the middle class came about through globalization, an economic policy the US Fed has been slow to accept. Fed raised interest rates while ROW was running NIRP, it was our populist president who put a stop to that.

The underpinning of Globalization is Neoliberalism–it’s the Neoliberal mindset that underlies the decimation of the middle class. All sorts of events and other ideas are connected to and gave rise to Neoliberalism, but it’s still a more accurate assessment to call Neoliberalism out than to blame Globalization.

If you need more convincing of what you already know, read the research Oren Cass is doing. I’m not qualified to peer-review it, but I dare anyone to say he’s wrong!

https://twitter.com/oren_cass/status/1230505649794166785?mc_cid=92a1db46a0&mc_eid=b71d3df985

Wow, you must be the “good” Jerome, haha.

The FED Core CPE is friggen totally bogus as is their keeping yields below the rate of their bogus Core CPE.

If you read Piketty’s book “Capital In The 21st Century” you will see where they are going with this and the fervor with which they doggedly pursue inflation. If they can get inflation going, they can, like post war France, inflate away all the debt. That, along with some de facto strategic defaults with entitlements (like, for instance, when they raised the SS FRA from 65 to 67) they believe, will pull us out of the doomloop that we are in now.

These Fvckers are nothing if not supremely arrogant.

DC’s bullshit really only worked well when they had a more complete monopoly over the megaphone (the 3 network, pre-internet era) when they could steamroller their preferred policies thru and pinned related failures on patsies.

With the pushback empowered by the internet it is much easier to poke holes in the Potemkin villages of their foolish plans and the poisonous consequences of the implementation.

The NY-DC Establishment Nexus is about to get it in the neck – from both the Left and Right

Or was this bitter-dry sarc that my brain-dead-in-need-of-a-beer mind missed the first time around?

Wolf- I wanted to get this out to your earlier, but I couldn’t find my new Ipad. I looked in the garage for almost an hour. Had to go through dozens of plastic bins. Then I looked in the cars- I park them outside in the driveway for obvious reasons. Could not find the darn tablet there either!

So I drove out to the storage locker and looked there. Went through both lockers. Nada. So I drove back home and found this computer. In one of the spare bedrooms. It was buried under a pile of stuff on the bed.

Anyway. About this credit card default thing. I think it is totally overblown. And if things get a little tight, you can refi your house and pay off the balances.

And as for me, I can quit anytime I want. Really!

Icanwalk,

How can these subprime borrowers who are delinquent on their credit cards refi their homes when most of them are renters?

Oh, if I was a financier, I would see a totally new market to refinance leases to extract equity. We could sell the paper, carry almost no risk past the float, and make brazilians!

Regards,

Cooter

/P.S. This post brough to you by the letter “S” and Sarcasm.

This shows who is getting the Fed’s money first, and who is getting the money last!

Basically, budget retail online or otherwise is going to have to deflate relative to the money supply faster than sub 70th percentile Americans can fail to get raises. The story is, they can’t move enough product to pay off their own debt unless someone gives the consumers the money they need from them first! And they say ubi (just giving people money) is unfeasible, but it’s not so crazy when it’s already being done! Because who’s dumb enough to think all that subprime debt is actually an asset? Just savings looking for a hole to crawl into, but let’s still call a moldy acorn wealth. Har har, the fed will be doing hard mmt one of these days just to keep inflation on t-shirts and crackers at 3%, housing at 5%, and cpi at “2%” while a few get to salivate over their “assets”. The real economy is looking great.

Well, the people at the end of the line have been waiting patiently for a trickle down effect. It’s just another promise that won’t be honored.

Next time, who will the shaftees vote for:

1) the guy who says – “give me some more money, then I might give you some if everything works out OK”,

or,

2) the guy who says – “take this money, you’ve earned it”.

Bobber- Basically correct about the “trickle down”. Fed officials have publicly said that they have been trying to raise asset prices to get the real economy going again. It has been slightly successful.

The globalization effects of increasing the supply of (cheaper) labor (in various ways) is the cause of the problem. Low-middle income people need employment income to improve their lifestyles, plain and simple. That’s how they receive their money (not by financial assets/investments).

But a very good question is why long-idled labor has not been able to be redeployed into inflation afflicted sectors (home/apt prices soar – but new supply is very very slow to be built…medical inflation soars for decades but employment increases only seem to make the price pathologies worse…)

The one common element seems to be the more subsidized a sector is, the less responsive it is to normal price signals (double medical industry supply = doubled prices, because the gvt will ratify all price increases…doubled housing prices because ZIRP keeps monthly mortgage pmt constant, etc)

CAS127, yes on “the more subsidized a sector is…gov will ratify all price increase”

In addition to medical exactly same on Higher Ed and housing.

If you actually look at a mortgage calculator, what people who buy a house now pay monthly on it vs what someone would have paid 20 years ago is still up quite a bit more than wage increases. Interest rates being down, that monthly amount is still up less than than the grand total value of the house. Builders could care less about the mortgage payment. They sell the house for the one time price. Lowered interest rates, therefore more affordable housing payments relative to house value, therefore more demand driving up home values, should be increasing the financial incentive for builders to build more homes. We should be seeing a flood of home building but we aren’t seeing supply reacting very strongly even after all these years. What does that tell you… Something else is going on.

Cas127 @12:09pm

A small real estate developer in my California suburb has been fighting restrictive zoning and NIMBY’s for years to develop empty land and build several hundred apartment units. Last I heard, the issue was still tied up in court.

Obviously its the incompetent FED destroying my legacy. NEGATIVE RATES NOW! AMERICA CAN BE GREAT IF ONLY WE PRINT PRINT PRINT!!

the subprime borrower is one step away from being cut off from credit the next tier up is not far behind, The couple purchasing the 500K home with nothing down thanks to the new VA home loan caps or buying , his and hers loaded F150 trucks all depend on American credit to float their life style. The subprime borrower is closer to the streets maybe already there but not far behind is a larger group of Americans one or two paychecks away.

Yep, and they make median wage and blame the minimum wage for raising their cost of living. That’s the only reason the F150 costs so much and the natural explanation for why their wage increases average 1.5% a year. Not that they ever bother to check the math anyway, but hey, as long as you know you’re working hard.

Since the average balance of a delinquent customers is higher today and the delinquency percentage is already higher, it can only get worse.

I think you answered your own question…

” For banks, subprime credit-card balances, with interest rates of 30%, are the most profitable assets out there.”

Why the bifurcation? Because it makes somebody a ton of money. When will defaults become a big enough problem that the overall economy starts to tank or there is another financial crises? With the way the Fed is printing money to paper over the problems, probably never.

Real wages have been more or less stagnant since the 70s. It’s an aggregate statistic that doesn’t, by itself, explain the bifurcation in default rates, but it seems like it plays a part.

Low wage earners have fallen, and they can’t get up.

Read most of Berkshire’ s annual report. Opening pages shows that a very intelligent person made a lot of people multimillionaires with one skill. The ability over his career of not doing much stupid stuff and growing on average a $1.00 to $1.20 each year.

Poor users of credit do the opposite and turn a $1.00 of debt into $1.20 each year with compounding results to disaster.

I have Paypal 2% cash back credit card.

Their security is fantastically bad. I’ve had my card “stolen” in the internet 3 times.

It was so bad, when I switched my monthly auto payment to my gym not once but twice – from one card, to Paypay 2% cash back credit card, both times, the gym owner soon called me to say my payment was denied…it was due to my Paypal 2% cash back being stolen.

I’m too embarrassed to try to put my gym auto payments on to Paypal a third time.

And yet Paypal keeps sending me a new card, and eating the fraudulent charges.

Thank you, Chairman Powell.

Never put your card in the internet without protection.

You don’t know where it has been.

I recommend Privacy.com. It’s ridiculous that the power to decline charges is NOT in the hands of the card-holder. With privacy.com it is.

If your card number is “stolen” and used on the internet (pretty much the only place stolen card numbers can be used today since most card-present transactions now require chip cards which can’t be duplicated), it’s not necessarily PayPal’s fault. It’s more likely that your number was stolen from other merchants who had possession of your card number.

Oh, and if you don’t like PayPal , Citi has a 2% cash-back card too.

Blame Synchrony, they’re a terrible issuer!

I second this.

Close the account. The money in my paypal account was stolen many years ago. I recently opened another account for online selling—HUGE hassle to get MY OWN money out. Evil!

About every two years (when I am NOT about to travel) – I call my TWO credit card companies and tell them this …

This is embarassing, but I went out drinking with friends. Early in the evening we decided to cab home. We were down town and craweled some pubs. I woke up this morning and my card is gone. I am really not sure where or what happened to it.

They will WHACK that sucker in a heart beat – give you a NEW number, so even if its stolen, it ain’t worth anything. New cards in a few days. If you don’t have cash for a couple days, bugger off.

The dumbest thing anyone with a credit card can do – that buys online – is keep the same number for a very long time. BAD idea – one hack away from pain.

See Wolfs old post about the credit agencies and how to freeze your credit – that is priceless stuff (had a fraud alert since the 90s due to old scammer roommate).

Regards,

Cooter

P.S. I am about to cycle my two credit cards and debit card – in about two weeks.

For many people changing card numbers is a PITA because of recurring payments.

If you’re afraid of using your card on the internet, in the US many banks will let you generate a secondary one-time-use card number associated with your account on their banking site that you can use for ordering online or over the phone.

Mkt adjusting to negative rates … things like Coronavirus only helping give FED ammo to overlook bubbles and further reduce rates (int’l growth slowing) + douce markets with liquidity.

I obtained a 12-month 0% credit card that gave me $250 dollars for spending $3000 dollars within the first three months.

I can’t even bring myself to spend that $250 on stuff I do not need or want.

I did it for the laughs but I just feel dirty.

The real question is, what did you spend the $3000 on?

VeryDirty, but amused.

I spent the $3000 dollars in a month surviving in California.

‘Murica, @#$% ya!

more like

Cali’, @#$% no!

But what does this bifurcation tell us about consumers?

That all consumers are created equal, but a few are a lot more equal than others.

The poor will always be with you, because the rich have insisted on making it federal policy, and that policy is genocidal. What does it tell you about the nature of a society that devalues living people to the status of commodities? And yet, the focus on financial valuation to the exclusion of normative valuations is ultimately self-defeating and can only result in its undoing. And it will deserve it.

Between my brother and myself we have 4 children in their 30’s and 40’s. Three went to college and got technical degrees and go to work everyday and have good material comfort and retirement savings.

One of the four did not take advantage of his opportunities and has addiction issues and a criminal history. He is in jail and has been a burden to society the last few years.

I think we are still a country that if you are willing to put in the work and don’t do stupid stuff you can have a nice standard of living.

“I think we are still a country that if you are willing to put in the work and don’t do stupid stuff you can have a nice standard of living.”

To have a greater than survival standard of living as a not connected employee in ‘Murica’s private sector you need a very strong intellect a CRAZY work ethic or both.

Globalization and money printing has eaten the lunch of everyone else.

3 out of 4 ain’t bad.

I think we are still a country that if you are willing to put in the work and don’t do stupid stuff you can have a nice standard of living.

And you keep telling yourself that, while the facts say the US middle class is headed for extinction.

I don’t think extinction as the rulers need their scribes, engineers and physicians. There will always be a middle class, even though it is only the middle in between the masses of serfs and slaves and their masters.

I am sure there are areas of the country that it’s pretty tough. Where I am there are a lot of opportunities and cost of living is pretty low.

My best friend is 49. She has made a good living with a 2 year degree. Has a nice home and beemer on one income and good retirement savings.

She has 3 brothers, sisters. All make a nice living have nice homes. They all work for corporations which can be tough, but that is where the pay is. All got the strong work ethic from Their parents.

Partly true.

A large portion of what used to be middle class has moved up with the knowledge economy, programmers and lawyers and specialty medical people and engineers and accountant types with above average ability. If you are living away from the coasts, life in this category is better now than in the 80s, except for costs of college. It’s much worse in places where real estate has exploded, like coastal CA.

No question that the white collar middle class and unionized working class has been decimated by globalization of production and elimination of basic white collar work.

I spent some years caring for the children of those yuppies in my own home.

Their well of parents would bring them early. Often I would have to take them out for new shoes because their feet had blusters from outgrown shoes. Often they were dehydrated and came with medicines. I could write a real book on this subject….my own family will murder me if I ever consider doing that again.

So give high praise for the work ethic of the young urbans in their comfy house….their little ones paid a serious price for it.

One died at 20 and I alone had the stories of her childhood at the memorial service. The parents had the antiques and the boat.

All it takes is one poorly-understood and stigmatized illness such as MS, Fibromyalgia, ME, etc. and decades of hard work and careful planning can be flushed down the drain in a few months.

Nobody thinks it can happen to them, until one morning they wake up sick and never get better. And when they make a claim against their disability insurance policy, they find out the reality of “Delay, Deny, and Hope They Die.”

In the US it is survival of the fittest and luckiest. The Devil will definitely take the hindmost, over and over. Better hope them old legs don’t get tired…

ok boomer

Agree with you OS: pretty much same with me and my siblings (first two of us ”war babies” last 3 boomers) next gen has 12 first cousins, mostly well educated, formally or auto-didactally, only one drunk/junkie that I know of. ( not in touch with 4 of them)

Did we/they achieve the “American dream” that our children will be better off, as did, in general, our parents and grandparents? Time will tell, as my children, nieces, and nephews still have at least 4 or 5 decades to go; I really hope so, but, with the current challenges, both financial and environmental, I am not as sure of this as were my ancestors.

Nice parable……you should start a religion.

Poor people have always been, and will always be with us. This happens whether or not there is any “federal policy”.

Until the past ~300 years, most people lived in poverty or extreme poverty. The advancements of modernity have objectively improved this situation.

Things are getting better, despite what many want to believe.

https://ourworldindata.org/extreme-poverty

But pointing to technological advances over hundreds of years does not address the decline and pathologies of the last 20.

It isn’t “Hooray, we live better than 1897”, it is, why the hell do we live worse (with worse apparently to come) than 1997.

And…one symptom of decline since 1997, is there are a helluva lot more people saying, “Well, at least it isn’t as bad as 1897”.

When times are actually good, people aren’t fishing for times when it was worse – they focus on the present and future.

cas127, actually, in the 1800’s we had DEFLATION for pretty much the whole century and with REAL GDP of something like 8%.

For the Pikers out there, this meant that even if you didn’t get a raise at all, your expenses just kept decreasing.

Here where I live in a historic Colorado Mining Town, a miner in the 1870’s would make a $1.75 a day. His lodging would cost about .20 and a steak dinner with a beer at the saloon would cost .15. He could easily save a Dollar (of the silver variety) a day.

It was a hard and dangerous job and many died and if you did expire on the job and you had a Son who was 12, he could earn a mans wage of $1.75 a day running dynamite into the mine.

Back in ’97, banks were paying 4-5% interest on savings and no trade wars (inflation accelerant). Something to consider.

No, in the US, more people have moved up than down, even in recent decades.

https://www.aei.org/wp-content/uploads/2018/01/middleclass1.png

WK,

1) Starting the chart in the late 60s obscures the fact that what one earner might have generated pre 1980, required 2 – husband and wife – post 1980. There was a huge surge of women into the workforce for economic reasons post the 74, 75 and 80 to 82 recessions.

Something significant was given up to get that 100+ group increase.

2) I also find the post 2000 increase in 100k+ pretty hard to believe.

Again, I wonder if the “household” measure is painting a misleading pic.

If college grads can only find 20k jobs and have to move back home – the share of 100k+ “households” may go up but only because household formation collapsed (which it did).

25 year olds living in the basement are not a sign of a healthy economy.

The methodology of surveys can obscure a *lot* of component tends.

This is very true, the world as a whole is far better off than 100 years ago, and the poor people of the 3rd world are also far better off overall than even 50 years ago, especially in China.

But the middle class in America is unquestionably not better off than 50 years ago, when a single income family could afford a home almost anywhere in the country and afford college for 3 kids.

Middle class wages in America have not kept pace with inflation since 1970, and home price inflation on the coasts has made those areas refuges of the wealthy and the poor who are willing to live 10 to a room.

The author makes the point the problem is less the poverty and more the attitude – and human nature.

———————————-

― Kurt Vonnegut, Slaughterhouse-Five (1969)

“America is the wealthiest nation on Earth, but its people are mainly poor, and poor Americans are urged to hate themselves. To quote the American humorist Kin Hubbard, ‘It ain’t no disgrace to be poor, but it might as well be.’ It is in fact a crime for an American to be poor, even though America is a nation of poor. Every other nation has folk traditions of men who were poor but extremely wise and virtuous, and therefore more estimable than anyone with power and gold. No such tales are told by the American poor. They mock themselves and glorify their betters. The meanest eating or drinking establishment, owned by a man who is himself poor, is very likely to have a sign on its wall asking this cruel question: ‘if you’re so smart, why ain’t you rich?’ There will also be an American flag no larger than a child’s hand – glued to a lollipop stick and flying from the cash register.

Americans, like human beings everywhere, believe many things that are obviously untrue. Their most destructive untruth is that it is very easy for any American to make money. They will not acknowledge how in fact hard money is to come by, and, therefore, those who have no money blame and blame and blame themselves. This inward blame has been a treasure for the rich and powerful, who have had to do less for their poor, publicly and privately, than any other ruling class since, say Napoleonic times. Many novelties have come from America. The most startling of these, a thing without precedent, is a mass of undignified poor. They do not love one another because they do not love themselves.”

― Kurt Vonnegut, Slaughterhouse-Five

Excellent.

Things have changed since Vonnegut’s day. They’ve gotten worse.

But Vonnegut also wrote Harrison Bergeron (sp?) which is a powerful indictment of the Left.

Perhaps the mark of genius is to honestly but skilfully contain multitudes.

@cas127 Vonnegut was subtle, clever and entertaining. It gave him leeway to make light of everyone – himself included, “…a fool at one end, a fire at the other.”(his cigs)

The first universal credit card was introduced by the Diners’ Club, Inc., in 1950. Another major card was American Express Company started 1958. Give human beings the chance to have something now vs save up for it and it is like shooting fish in a barrel. This fundamental human trait has been exploited for a long time. One group of people getting rich off another. The Fed is just a facilitator, perhaps a bit extreme these days. Russians didn’t have wide spread use of credit cards until recently. Want to live like they have for the past century? Didn’t think so.

Everything happens for a reason, and sometimes that reason is you are ignorant and you make bad decisions.

Delayed gratification is one way a regular working class person can become wealthy. Teach your children well.

Diners card and AMEX were originally targetted for the wealthy, as well as businesses, payment due monthly IIRC.

My first credit card was a union branded card 1979, the second was US Naval Institute branded circa 1982s.

With decent credit, good payment history etc, I am now a certified sucker for the credit card industry.

“Delayed gratification is one way a regular working class person can become wealthy.”

yes, keep passing that kool-aid around ……………

the corporatocracy, FED, and globalists thank you …………….

This is sarc, right?

I might agree on the Greatest Generation (Great Depression *and* WW 2), but the Boomers?

The *$#3–&! F*cking Boomers?

They inhereited the most powerful and wealthiest nation the world has ever known…and they are leaving it a historically indebted mess, also having spent two *decades* “leading” a war against two opponents with the industrial base of Barstow.

The Boomers have grotesquely mismanaged the nation while sucking it dry.

I’m sure individual Boomers are lovely people and there is some competency sprinkled amidst the decay (some writers here for instance)…but history is going to judge the Boomers very, very, very harshly.

Living within ones means is the secret to financial success in life and it applies at all levels.

I have several colleagues with income near the top 1% who are living paycheck to paycheck, they buy or lease very expensive vehicles on a rotating basis, pay for very expensive private schooling from K – College, and in some cases maintain expensive vacation residences or have an expensive vacation habit. They earn 7 times the median income but will work until their late 60s because they didn’t learn to save.

I also know many people near the median income, including family members, who are set to retire on time because they have lived under their means. This despite not always being fully employed.

I’ve also spent time volunteering to help the poor with their finances, and I’m repeated astonished by poor financial decisions on a part of a subset of those who are poor, who simply cannot control their spending. This isn’t all the poor, there are others who are in those circumstances for health or family reasons, but many many are unable to make basic changes in spending that would put them on a track for financial stability, if not outright wealth.

Happy1,

I don’t disagree with your view on frugality – it is within everyone’s personal control and far too many people use poorly thought out spending as a doomed substitute for some other gap in their lives.

But…there are also macro factors crushing a higher and higher percentage of Americans and those factors are much less within personal control.

The world is much, much more competitive and America has adapted poorly…and what passes for leadership in the US is the exact opposite…DC eagerly engages in short term fixes (leading to long term disasters) in order to paper over difficult – but addressable – problems.

So we get stagnant (at best) incomes, soaring housing costs driven by DC money printing (to save its own political neck), and employment growth from 2000 to 2016 that was the worst for many, many decades (and if you look at the post 2016 growth, it is much more in the 20k to 25k job categories than anything else…that ain’t going to do much in CA/NY/etc.)

For every action, there is an equal and opposite reaction…in physics and economics.

Cheap money begets more debt….no kidding.

The book will be written that lower rates is stimulative…only in the short term. They then, protracted, become destructive for they encourage over borrowing and misallocations.

This is so fundamental, it is remarkable these central bankers don’t get it. They have set the stage for systemic collapse. And all the “happy buttons” have been pushed and stuck in the down position.

The Fed creates fake demand for treasuries and stuffs them on their balance sheet. The 30yr yield is BENEATH THE INFLATION RATE!!

Cheap money allows conversations about Sander’s plans that, in a real interest environment, would be scoffed.

AAPL is starting to fall hard from the tree

Uh oh. I think this year will be a Newton moment for the fruit

Great observations. I have one analytical comment. It looks like the surge in delinquencies started early in 2017. This is when the economy as a whole started another speculative surge as a result of the election (i.e., the Trump bump). I wonder if the 4500 smaller banks attempted to expand their credit card portfolios by loosening the requirements, in which case the increase in delinquencies is more a reflection of changes to bank credit policy than the subprime consumer. If there was no big increase in subprime credit balances near the start of 2017, then it appears the subprime consumer clearly is deteriorating rapidly.

I’d imagine the CC industry is just as competitive as any other. Therefore the smaller (not the top 100) issuers need to “grow” their portfolios. How? Dip farther into the borrower risk pool with looser qualifications. Taking on higher risk means higher delinquency.

Maybe I’m just getting too simple minded, but I’m not sure where the mystery is

Agree with that concept credibleCB, and the one from KCEF a couple above.

Delay the gratification and put the money out of easy reach means someone ”living small” or as small as possible while maintaining a full time job, even at $10 or so per hour can have $10K in a couple of years out of any school…

Then, just say no to the credit card offers, etc.

The foundation of the problem long term however, is the plain fact of the Fed ”allowing” inflation to gobble up any real wage advances, as they have done since the beginning of that institution.

Old days, folks put their gold into jars in the dirt and it was worth more money or bread or whatever after every inflation, then came the ”gold standard”, then the law saying USA citizens could not own much gold when it was $45 per oz,,, then came Nixon taking us off any basis for the paper money, and here we are with every other currency allowed to grow against our US dollars at the instruction of the oligarchy.

IMHO, this won’t stop until we get rid of the Fed, and then make all the financial laws concurrent with the financial education of ALL folks able to sign contracts, including of course credit card contracts.

“even at $10 or so per hour can have $10K in a couple of years out of any school…”

Hmm…let’s do the math…it is going to be close.

2k hrs at $10 per hr = 20k gross per yr.

Round SS to 8 pct and 1600 goes away (18.4 left)

Assume effective 10 pct Fed Inc Tax and another 2k goes away (down to 16.4).

Assume median one bedroom rent is 750 (rents have been soaring) or 9k per yr (7.4k left)

Assume 2.4k for food (which is pretty darn careful spending) and we are down to 5k.

A small car would be 250 per month without incl dp, so another 3k goes away (leaving 2k)

That 2k would have to go towards everything else (gas, insurance, etc)..or savings.

Without a mandatory roommate or mass transit…you probably can not save 2k per yr on a 20k per yr job.

And if you have to live in a major metro (where most of the jobs are) then rents can be much higher and there is no chance.

Before the Great Fed Housing Inflation maybe, but not now.

Why confuse kool-aid drinkers with reality?

their really believe is if you can’t get ahead, you aren’t delaying gratification enough …………..

as the boss says ………… you want to get rich …… dig harder

Plenty of places with apts or houses to share for $3-400 per month still available even today, and those places usually have jobs available for $10 or even more for relatively unskilled work needing no diploma, etc.. And a lot more fun to live with roomies than alone, though it does take some maturity, eh.

Fact is that I actually am acquainted with folks who did what I said recently, (and are now buying a house) even though I personally have had a ”living wage” in CA in recent decades, defined as approx $10K per month ( today) as long as not in SF bay area, and the same money in other areas where it paid for the high rent district, etc. I am on the other side of this, having never seen a temptation I could afford that I didn’t enjoy.

Try looking at the job lists on CL for various areas, it will add some perspective.

“Plenty of places with apts or houses to share for $3-400 per month”

Nowhere in coastal CA or NYC metro unless you are talking 4+ “fun” room-mates. Many inland metros would require minimum of 3 roommates – check Zumper/Apartmentlist monthly rent surveys to see what ZIRP has wrought.

“lot more fun to live with roomies than alone,”

Only on TV sitcoms…how many people in their 30s do you know who have roommates?

Fed tax should be less than $1000 due to the standard deduction.

I might give a little on Fed Inc Tax…but there are many expenses that could gobble up the savings…utilities, auto repair, insurance deductibles…it is just very, very hard to save even 1 or 2k on 20k unless you make lifestyle sacrifices those from 1955 to 2000 probably did not have to make in order to save.

ZIRP and government overhead (implemented and accrued by others), poorly thought out trade agreements and misfought wars…they all come at a cost.

And that cost is decline.

Just another sign that recession is coming. I don’t think there is any stopping it now, not free money, not tweets, not fake news….People are tapped out, and with this virus people will be out of work, money for food and the rent, and not buying junk they don’t need. Health is more important than more stuff.

That’s true, and may of the upper middle class people (like myself) are not necessarily protected. This is the problem with the conventional thinking is that it’s just the blue collar middle and lower middle classes who are at risk during a serious turn down. In fact. many white collar workers have big overhead in houses, private schools, gold club memberships, 2-3 children, etc. If jobs and income sources start to evaporate, then these people will be in the same boat as their lower middle class citizens who have far less overhead. I am not sure how many people realize how fragile the system really is at times. A few threads pulled at the right places will take the entire sweater apart!

Stephen: gold club or golf club membership? Either one makes weird sense.

The point about wealthy versus the poor makes sense. The poor know how to get by and struggle. Good times or bad they dress the same, their income opportunities stay the same. Higher up the food chain, perception of ability rests more on appearance etc. Also ego, hubris, seen as a looser by peers. Hard to tell success by t-shirt, jeans and Adidas or New Balance.

Here in Tulsa I noted that one could estimate earnings by headlights burned out, women dressed up, driving upscale cars with windows open in summer; ie. either divorced, widowed, laidoff and no spare $$ to fix the a/c or headlight.

Actually, I meant to say golf club memberships. And, where I live in FL, golf memberships ARE a big deal. Yes, perception is big, but people invest lots of money in golf here. A simple drive around Captiva / Sanibel will tell the story. Lots of tourism based on golf as well. Yes, we have it very nice here, but I have never thought that we lived in isolation from the ponzi financial system. This place can fold faster than a cheap suit in a rain storm.

J7915,

“…driving upscale cars with windows open in summer; ie. either divorced, widowed, laidoff and no spare $$ to fix the a/c …”

As you might know, I used to live in Tulsa for a long time (Booker T grad, TU MA, and worked there for many years). So when I drove home from work in my nice demo at 8 PM or whenever during the summer, I drove with the AC on and with the window down. The hot dry air relaxed me and helped cleanse my mind and get rid of the stress that builds up from running a big Ford dealership, and the cold air from the AC kept it comfortable. It felt great (try it someday). And I miss that here in San Francisco. Now you just explained to me why people thought I was a divorced, laid-off, poor schmuck…

J7915:. Your last paragraph reminds me of my Father!

Dad, a mining engineer, a child of the depression, never liked throwing anything out that still had some life left in it.

One day he was down on his knees in the front lawn, weeding.

He was wearing his favorite comfortable badly worn old clothes from the 1950s. Sort of like the ripped jeans kids wear today. He certainly looked like a homeless hobo! Worn hat, holy gloves, knees shot, seat ripped, badly worn shoes!

Anyway a salesman came by, upon seeing Dad, hesitated, before finally asking Dad if the owner of the house was at home! Dad politely replied he was the owner to the disbelieving saleman!

My Father loved telling that story, as he would laugh and laugh about it to no end!

Dad knew who he was! He didn’t need to impress people with fancy things! All one had to do was talk with him briefly to discover who he was!

Very true, so many people living beyond their means with the trappings of wealth but very little savings.

The Fed is our 4th branch of government.

It is now out of control as is the treasury adds $1+trillion to the deficit that is monetized by unlimited funding.

Inflation is the reality hidden by BLS manipulation.

Cheers?

B

How is this a mystery, exactly? “Full employment” isn’t, and the share of productivity going to labor is too low.

It is only a “mystery” to the people who do not want to tell you the truth.

It’s not just about the obscene interest rates they charge, it’s also about the fees. I just got a notice that the late payment on my 25% card will go up to $40. This fee could be the daily take home pay of a low wage worker. Who in the govt is looking out for consumers? NOBODY.

In fairness, part of the surge in these rates is trying to stop bad loans. In 2016 they were fairly low rates for them. Bad loans=profit loss in the long run. Eventually reserves will crash down and the bank dies.

They are the next S&L

I don’t know what the right answer “should be”. Having a credit card isn’t a necessity, so the late fees and high interest can be pretty easily avoided.

However, there used to be pretty strong usury laws. I don’t know what happened to these. They were only a kind of “catastrophic insurance”, e.g. maybe 15% interest (still relatively very high) would be OK, but nothing above that.

Having a cc is necessary if you drive. Many gas stations do not have a person, just pumps that only take credit or debit cards.

As for why the interest rates to those who’s credit score is low is the risk of loss. There is a reason their credit score is low. YET in order to live in our fast complex world a credit card is a signal that you are part of the society. No card, you are a nobody.

You can’t help a person who doesn’t want to help themselves. You can lead a horse to water but you can’t make them drink. All that can be done is provide the opportunity.

Illinois has a bill going through legislature, that would only allow attendants to pump gas!

JB may also require The Squeegee Men on every street corner to boost the Illinois economy.

Look Warren up in the book “Profiles in Corruption.”

///

It is interesting to see how globalisation allows parallel worlds to coexist, and how little is a national economy (if such a concept exists) interconnected. Once upon a time if one layer was in pain, the entire society suffered. Today due to global markets this is not true anymore. Some markets are interconnected like realestate, that are local and bound by geography. But in general the existing markets will allow income stratification beyond our wildest dreams. And the worst will happen… absolutely nothing, no change. And the numbers, no correlation between layer credit defaults, potentially confirms my view.

///

LouisDeLaSmart-It’s because of “global mobility/tradeability” of certain goods and labor (and capital that chases returns from those).

It’s a debt bubble underwriting the expansion. Once it bursts, down goes the U.S. economy. Not even corporate debt means so much. Thousands of these banks will die in a black swan.

Wolf,

You really did answer your own question…the big banks are able to more or less successfully segment the mkt – leaving the worst risks for the smaller banks (the real question being why the small banks keep reaching for the hot stove with the bandaged nubs of their oft incinerated hands…ZIRP is a helluva drug).

And you are 100 pct right about the default rates being a huge warning sign during the “good” times – but the Feds for decades have shown themselves as utterly incapable of doing anything but mash America’s forehead against the big green “print” button.

This creates and perpetuates the debt-driven inflation cycle that simply spirals more and more out of control.

You can see the friggin brain trust at the Fed in 2001…”Eureka, fellow elite, if we slice interest rates in half…the price of housing will be sliced in half…stimulating the economy!”

And then the Fed remains utterly impenetrable to empirical evidence (doubling housing costs) for the next two decades.

The same dynamic applies if you think the Fed focused on the theoretical wealth effect – after endless empirical evidence that their interest rate manipulation is having counterproductive effects – they simply refuse to course correct, the only response, ever, is “more cowbell”

DC could have addressed the underlying pathologies decades ago (US lack of competitiveness vis a vis China, Chinese domestic policies preventing recycling of export proceeds back into American goods, etc) but DC refused to do much of *anything* other than spend (which purchases political power) and print (which temporarily negates the impact of endless deficit spending by forcing interest rates down – at the cost of expropriating the savings of its citizens).

Until the fundamental pathologies are addressed (DC being DC included), things will only get worse until DC loses all control.

The US will fragment, based around alternative currencies considered to be more honest stores of value.

DC may try domestic occupation, but the political class is heavily outnumbered (that is a big part of what makes them the political class) and having pissed away the dominion of the dollar, they are unlikely to recapture it using more transparently brutal force.

Cas127,

There is an old and valid rule about headline writing: “If you ask a question in the headline, you MUST answer it in the article.” I follow that rule, though I don’t guarantee that I come up with the right answer :-]

More seriously: I have been reporting on this rise in subprime delinquencies in auto loans and credit card loans for at least two years. The very unusual dynamics of it – delinquencies surging at a time when there is no unemployment crisis – have always troubled me.

More recently, I started looking at this in layers, not in aggregate numbers, to figure out where this is coming from. And I think that’s where the answer is. In aggregate, American consumers are doing well, and that’s what all the aggregate numbers show, from consumer spending through consumer credit.

But once I started digging into the layers, it became obvious how one-sided this health of American consumers really is, in every aspect – income, spending, debts – and how price increases affect these layers differently.

And that’s a real a problem. And monetary loosing is just going to make it worse.

Yes.. the layers – and then there are the Unicorns and Zombies feeding the upper layers with leveraged loans and more borrowing.

So much debt. Housing, vehicles, credit cards all being supported by other borrowing by government and corporations alike.

When this comes apart it is going to be spectacular! Bubbles bubbles everywhere waiting for a pin prick or a strong wind.

“all being supported by other borrowing ”

The inherent threat of Cascade failure/correlated default is fatally underappreciated in debt-founded systems.

The big banks only look safe because no one knows who their borrowers’ borrowers are.

Ditto the self-licking ice cream cone of bootstrapped collateral valuation – bigger loans can be made today because yesterday’s loans “increased” the value of the collateral.

How exactly…well…er…umm…hmm.

A rule kinda like Chekhov’s Gun?

Yes.

Didn’t really explain why banks would actively seek CC customers who earn 2% back on purchases? I see no moral necessity to honor CC debt assuming their losses are covered by high fees. Like why get vaccinated when the 95% already are? The system removes moral hazard, individually I have no responsibility. The flip side wants to the tax the 1%ers, and surprise, they want to be taxed! The offset for them is they, or their corporate image, is absolved of product liabilities, and they open up a whole new line of (subprime) consumers. Those who assume the liability are subsidized, like farmers, while those who accept risk (consumers) are indemnified of personal financial responsibility. Their subsidy should always exceed their losses, which may be why companies keep growing despite falling revenue and profits.

Why the 2% pay back? Probably that the banks get 3% or more from the merchants OR they are hoping you fall behind so they can get the userous fees OR they claim all your debt as an asset to offset some other lending OR all of the above.

Merchants have told me banks get 5 to 6% on credit cards, less, usually 3% on debit cards, and that’s one reason banks give out the pay backs on the credit but not debit cards,,, as well as one reason many merchants only take debit cards, or charge more for credit cards than debit.

I’ve wondered when an alternative will sweep the whole credit card industry aside, it would seem that a smartphone based payment system could undercut these fees easily, I don’t understand why this isn’t happening.

Happy Too? When we start trading credit units instead of money. People will be trying to figure out how to boost their credit score to buy a better car.

The larger banks have better quality credit card loan portfolios, fewer defaults.

About 1990 small S&L banks became insolvent after commercial real estate speculation. The Federal authorities auctioned bank owned properties.

Don’t forget the ‘deregulation’ of the S&Ls that forced them to borrow short at high rates and lend long at fixed rates (to ‘protect’ consumers), a normal pattern of deregulation legislation.

“Saint Peter don’t you call me ’cause I can’t go…

I owe my soul to the Company Store”

The economy is now one giant company town owned by the banksters on Wall Street. Get sick, injured, or go on strike, and the disobedient or injured worker is evicted from the Company house, credit for food is cut off from the Company store, and they are blacklisted from working any other mine.

This isn’t just a folk song. This is the way coal towns operated not so long ago, and it’s hardly different from what millions of workers experience today.

Merle Travis was definitely a ‘folk,’ born in Kentucky coal country.. He was a heckuva guitar player–Doc Watson named his son after him. He made a decent chunk of change in Hollywood. You can see and hear him sing “Re-enlistment Blues” in “From Here to Eternity.” Easy to find at YouTube.

You got it!

…and nobody has mentioned the criminal payday/title loan sharks operated by the big banks.

Obama tried to regulate those but Trump let them off the leash again.

I took shelter from the rain inside one once and witnessed the most horrible shaming and abuse of a middle aged black woman by the staff I swore to spread this story everywhere.

The human cost of this is horrible. Those places should….well, Wolf, I think you know what I want to say.

The whole economy may be approaching the famous now much-discussed Minsky Moment, from maxed out leveraged longs in the markets to subprime credit card and car loan borrowers in one wretched unified event.

If I remember correctly Hyman Minsky mentioned “a sudden decline in market sentiment” as the prime cause for rapid loss in asset price.

Personally I don’t see this “sudden decline in market sentiment” anywhere.

Even before the Covid-19 outbreak became known outside China, manufacturing worldwide was in a slump, car sales worldwide had been declining for a couple of years, LNG prices, the last great hope of the energy sector for big gains, remained comatose etc. While hardly indicators of a crash, this stuff would have suggested at least some caution. But no: financial junk was being bought with unbrindled enthusiasm.

Covid-19 has in fact pushed “market sentiment” to new heights, the two justifications being the big gains to be had after this thing has blown over (business back to normal for us with a couple of brain cells still alive) and especially how financial markets came to believe this health crisis would be another occasion for a massive flood of fresh liquidity… conveniently forgetting we are already in full stimulus mode worldwide and that flood of liquidity was failing to help sell more cars and smartphones.

If you think the inmates are running the asylum, welcome aboard.

And if you think we haven’t seen the worst of this stupidity yet, welcome to the club.

Perhaps after today ( Black Monday) you will spot it

I hope you are right because way too many people need that undeserved smug smile wiped from their faces, but given what we’ve seen over the past five years I am not exactly holding my breath.

absolutely correct, staring into the vortex this AM all you see is happy faces and calls at a premium to puts.

MC101:

Ah,…….today Monday 2-24-20 Dow down 1,000+ with futures down another 1,000+……………….

And the week has only begun….

Careful…….

(I’m always a few days behind reading WR blog)

This is one reason the Fed won’t let the stock market tumble. If the prosperous become less prosperous because their stocks are worth less, then the economy will take a major hit

Wolf – this is what your short is up against:

https://www.investopedia.com/terms/p/plunge-protection-team.asp

Willy Winky,

Please READ the stuff you’re linking. And NOT JUST THE TITLE/URL.

All they do is “report to” and “advise” policy makers and presidents about market events. They couldn’t and didn’t prevent the three crashes I’ve been through: 1987, 2000-2002, 2008-2009. But the rumors and BS about it are endless and a lot of fun to spin. But not here.

Wolf,

Can the workings of the PPT really be “spun”? How would we know what they do or don’t do?

from investopedia:

The concept was to create an informed, but informal, advisory group on the markets for the president and regulators. Charged with “enhancing the integrity, efficiency, orderliness, and competitiveness of our Nation’s financial markets and maintaining investor confidence.”

Why do they need to maintain investor confidence? Why not assume they are bunch of larcenous corporatists, intent on bailing out banks and favored entities.

Why not assume they are bunch of larcenous corporatists, intent on bailing out banks and favored entities.

They are larcenous corporatists. That part you got right.

But the Working Group on Financial Markets doesn’t bail out banks and favored entities. They design strategies and tactics involving stock index futures and loans, for example, with the expectation that such manipulations and treatment of favorites may prevent a downturn in equity markets from becoming a meltdown. The actual implementation of those strategies and tactics is assumed to be up to banks, the Fed, and the Treasury.

As the Wicked Witch of the West said, These things must be done delicately, or you hurt the spell. They can’t just hand out trillions. They have to use byzantine channels so the public doesn’t get too outraged.

The PPT is regularly accused of exceeding its mandate, although it’s hard to see what the limitations of that mandate to advise may be, or what the limitations imposed on the above financial entities may be, if any. Direct purchase of stocks would look bad, but the government may wind up owning shares in the firms to which it provided loans as they will receive warrants as collateral for these loans.

Ultimately it’s up to Mr. Market to decide to hold or buy stocks to support prices, and sometimes he doesn’t. Sometimes these manipulations are overwhelmed by Mr. Market’s adverse actions, and then you get a crash. Then the Fed steps in with QE and related programs and waits for the usual mechanisms of extraction from the Real Economy to catch up with the losses, and that can take years. It’s been twelve years since the last meltdown, so the losses then must have been humonguous.

Crony capitalism? Sure. Welfare entitlements for the rich? Of course. Do you think they’re going to generate explicit statements about the nature and extent of their machinations and what it’s costing the little guy? Don’t be absurd. All you really need to know is that one way or another it’s going to result in a vast upward transfer of wealth.

In other words, you’re paying for it. Don’t expect them to thank you. They’re entitled.

cb,

Just look at the last two crashes. By 2002, the Nasdaq was down 78%. Plunge protection my ass.

You believe in whatever deities you want to, including in the PPT. All they do is “report” and “advise.” When the market crashes, it crashes.

Wolf,

Hard to believe but I am semi- on the side of una here – just because the initial dramatic crashes occur (and are not intercepted by PPT or whoever) does not mean that the G does not subsequently engage in pathological “fixes” that favor certain interests (Una would say the Top Hatted Capitalists who run things behind the scenes, I would say the Political Class that hides a stiletto behind a perpetually phony smile – the truth is that the two blend together) – but the underlying point is that the “fixes” really are not serving the vast majority of American citizens. And haven’t for a long time.

And I think you would agree – it is simply the response time of the G to crashes that is in debate.

cas127,

When stuff drops far enough, even I turn into a buyer. The market is not going to zero. Individual stocks will, as companies fail, but others will be OK, and will be great buys at a certain point. Lots of investors will pile in when they see that moment, from Warren Buffett on down. Big money and little money. This is what stops a crash, and not the PPT.

Wolf,

Hmm…I think we may just be talking past one another.

I don’t disagree that there is some price at which non-G buyers will come in (although a 50 pct drop in 2008-9 in the SP 500 and its 40 pct overvaluation now are equally signs of likely unhealthy destabilization) but in a way, ZIRP *is* the PPT (writ slow).

ZIRP was gvt’s response to the financial collapse (-50 pct) and real economy cratering (-15 to -25 pct) and it was intended to reverse those losses.

My point is that ZIRP’ing does not really fix much, it simply creates the next valuation bubble (but it does create political cover).

The fact that the market crashes does not diminish that the PPT is part of the apparatus that favors some entities at the expense o common Americans and America at large.

They are a group, ironically tax funded, that exists to manipulate the market – rather through policy advice to the FED, Treasury or who really knows? Do you really think you know? Wether they directly intervene or just give the “Nod” to intervention makes no difference. Their purpose is to distort the market. The fact that Mr. Market may over-run them on occasion does not change their manipulative, larcenous intent.

They are, along with the FED, are ruinous to a free market.

I suggest as a future topic, Wolf do something on Carried Interest, and how it’s used by the super rich to evade income taxes. I’m astounded as the lack awareness of this by folks here, many who actually believe the rich pay income taxes at the reported tax rates, in their income. They most definitely do not.

timbers,

Don’t lean too heavily on carried interest – I think you vastly overestimate its applicability.

There are *many* legal tax dodges but the truth is the well to do (not really rich) carry the overwhelming majority of the Fed Inc Tax burden.

And the supply of billionaires to expropriate is too thin to fund the insatiable spending machine that gvt has become.

There is a reason while gvt had to invoke ZIRP…it transfers the earning power of vast sums away from those who own/earned it…to a gvt which cannot manage itself and has not been able to for decades.

And that gvt likely considers itself to be at Max Tax (if it didn’t fear rebellion, it would be hiking) – now having shifted to the printing press (appropriating via inflationary offsets, the full consumer cost savings gains that the China explosion would have otherwise brought).

There is plenty of perfidy in the private sector…but there is more, and more profound, in the public sector.

One of the staunchest defenders of the carried interest loophole is Senator Charles Schumer D-NY. The investment industry is very important to NY State’s economy and as a source of donations to his political campaigns. When the issue of closing the carried interest loophole to help pay for Obamacare subsidies came up in 2010(?), he opposed it.

Wolf, you showed up in my Newsfeed!!

https://www.marketwatch.com/story/proof-that-the-booming-economy-isnt-working-for-a-chunk-of-the-population-2020-02-23

(And as an aside, I want to thank you for kindly explaining some of these complicated issues without condensation or “mansplaining”….as is the norm from some men on other shall-remain-nameless sites.)

I am kinda at a loss as to how economics/business topics can be mansplained…could you give us an example or two, little lady…

CAS127:

Just using the term, “..little lady”….puts a great big target on you….LOL!!!!

Yes, depending on the degree of humor or humorlessness, things might have gone poorly for me.

It is always surprisingly a bit of a crap shoot if people on line can tell if you are putting them on.

I just try to explain it in a way that even I understand it. That’s tough. Once it passes the test, it goes :-]

And yes, I gave Shawn Langlois at MarketWatch a shout-out on Twitter.