My “Credit-Card Spread Index” blows out. Heck if I knew what that means, but it doesn’t mean anything good.

By Wolf Richter for WOLF STREET.

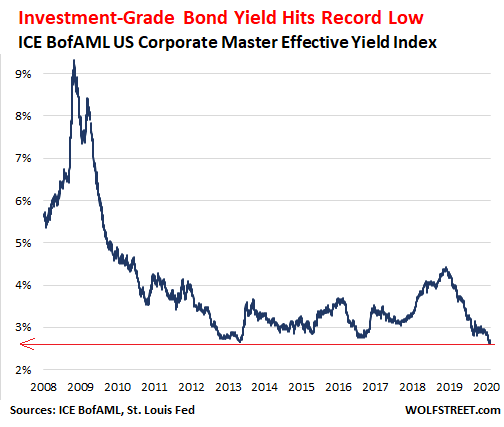

The average yield of investment-grade bonds (as per ICE BofAML US Corporate Yield index) dropped to a record low of 2.62% this week. This comes after the Fed cut its policy rates three times last year, from already low levels, to even lower levels, and after it bailed out the repo-market with over $400 billion over a period of just three months. Bond yields across the board have fallen, and it made borrowing for companies extremely cheap:

If these ultra-low borrowing costs for investment-grade corporations are adjusted for consumer price inflation, with CPI at 2.3%, this borrowed money is nearly free, and investors have a near-zero “real” return.

But consumers borrowing on their credit cards sit at the other end of the spectrum, getting hosed.

We won’t compare the interest rates that consumers pay on their credit cards – which are unsecured loans and often owed by riskier borrowers, including subprime-rated borrowers – to the interest rates that investment-grade companies pay on their bonds, which are a mix of secured and unsecured debt rated from barely investment grade to triple-A.

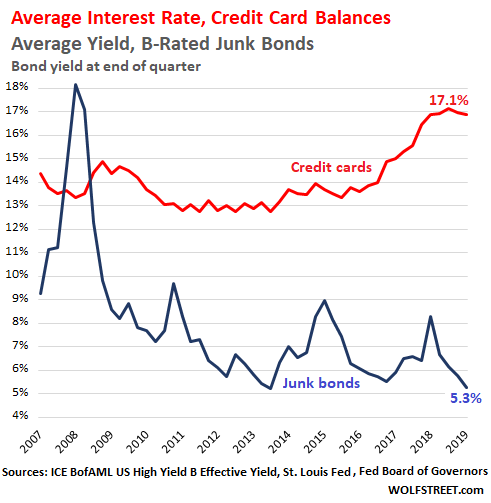

Instead we’ll compare credit-card interest rates to B-rated junk-bond yields (here’s my plain-English scale for the three major corporate credit ratings agencies). This is still not apples to apples, but it shows the trends of where those interest rates have been going for consumers, and it’s, hahahaha, not down!

According to the Federal Reserve Board of Governors’ consumer credit data, the average interest rate on credit card accounts with balances on which interest is assessed – so not counting the theoretical interest rate on credit card accounts that don’t carry balances – was 16.9% at the end of 2019, after having reached 17.1% earlier in 2019, a record in the data series going back to 1994.

The chart below shows this disconnect between the average B-rated junk-bond yield (blue line, ICE BofAML US High Yield B Effective Yield) that plunged to record lows; and the surging average interest rate on credit cards (red line) that soared to record highs. They should move roughly in the same direction with some gap between them, but they’re moving in the opposite direction:

This is the bitter irony: Average credit card interest rates are at record highs while the Fed has spent years repressing interest rates to record lows for just about everything else.

Within this, there is a broad range of credit card interest rates. Some credit cards may charge less than 7% while others charge over 30%. It remains a mystery to me why anyone these days would borrow at 30% or even at 20% – but hey, enough people do, so it’s a thing, and that’s what matters here.

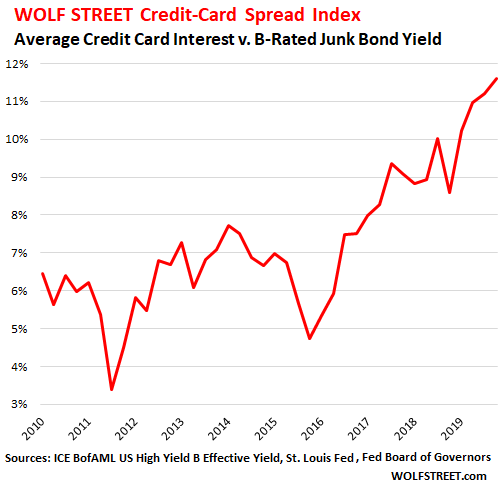

The WOLF STREET Credit Card Spread Index.

In the bond world, “spreads” measure investor appetite for credit risk. The spread is typically measured as the difference in yield between a category of corporate bonds, such as B-rated junk bonds (considerable risk of default) to Treasury securities of equivalent maturity (near-zero risk of default because the Fed will print the government out of trouble).

If this spread between junk bond yields and Treasury yields is wide, it means investors demand a large premium to take the additional credit risk; for example, during the Financial Crisis, the spread between the average B-rated junk-bond yield and equivalent Treasury yield widened to over 20 percentage points, which was financial panic mode.

If the spread is narrow, it means investors are willing to take large credit risks for only a relatively small amount of extra yield. They’re “chasing yield.” For example, currently, the spread between the average B-rated junk-bond yield and equivalent Treasury yield is only 3.62 percentage points.

My newfangled WOLF STREET Credit-Card Spread Index doesn’t track the spread to Treasury securities, but to B-rated junk bonds. It compares the extra interest credit card holders are paying over somewhat equivalent corporate borrowers. And the index has totally blown out: the spread has about doubled over the past decade, from around 6 percentage points in 2010 to nearly 12 percentage points at the end of 2019:

Heck if I knew what that means. But it doesn’t mean anything good.

My Credit Card Spread Index shows, among other things, that consumers are increasingly willing to borrow at usurious rates, despite near record low rates elsewhere in the economy.

But why are consumers willing to borrow at 20% or 30% in the first place? Or even at 16%? These high interest rates almost guarantee that these already strung-out consumers won’t be able to deal with the debt. No one forces consumers to borrow at these rates, but they do. This is a peculiar phenomenon.

The fact that there is demand to borrow at these high rates allows rates to go higher. If consumers decided that the maximum rate is 12%, and no one ever borrows anything above 12%, that would be the peak rate because demand would collapse above it. But that’s not happening among consumers. They rather spend the money and worry about the interest later, which translates into demand for usurious credit that many lenders are eager to supply. And so my Credit-Card Spread Index blows out.

Nearly a quarter of all subprime auto loans are 90+ days delinquent. Why? Read… Subprime Auto Loans Explode, “Serious Delinquencies” Spike to Record. But There’s No Jobs Crisis, These Are the Good Times

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It is nearly impossible for anyone under a certain size to get a loan nowadays. Ask any small business or private individual. If you are in excellent financial health, you might be able to score a mortgage or car loan, but good luck with anything else. The credit freeze has been terrible.

If the BLS is to be believed, consumers of limited means, the bottom 50% or so, spend more than they earn. Some of this is made up by transfer payments like SNAP, but some of this is consumer debt, and the only lenders are charging well over 10%. If your car needs repairs, you have to fix it or you’ll lose your job, your housing and probably everything else. Maybe the Federal Reserve needs to open a retail window.

“needs to open a retail window”

Don’t give Bernie any more ideas.n

A Fed Retail Window is not as dumb as it sounds.

Its just MMT via loans instead of straight cash/helicopter money.

Its what primary dealers already have – discount window/QE/NIRP.

Funny isnt it – the banks/govt have arranged a world where primary dealers borrow from the Fed at near zero, but CC holders pay 17-21%.

Postal Banking would suffice.

But that would put out of biz a lot of our most respectable businessmen, like pay day lenders and scalpers.

So you can figure out we need someone like the B to take our angels of altruism in Congress.

We did have a Postal Savings Bank from 1910 to the mid-1960s. Then it was abolished because the private banking system had become so well-regulated that depositors no longer needed protection from parasitic and/or crooked banks.

Heh.

Those payday lenders would become operators of the ‘postal banking’. Or it would literally be run out of the USPS, which loses a typically .gov amount of taxpayer $ every 90 days. . . despite its superior lane density and monopoly status.

Roaring Mouse,

“…Or it would literally be run out of the USPS…”

Yes. That is exactly what Postal Banking refers to – low cost banking. basically free or close to it, run by the Postal Service, that working folks can access without being fee’d to death.

Like a public utility in a way, I guess.

“Capitalism” is a racket; all you need to play is the balls………..

I have been complaining for a decade at least how the system is taking advantage of savers. Both Democrats and Republicans have played a roll robing the the middle class in this regard. There is something really wrong here. We need postal saving again for the health of the country. The Zombie corporations and the politicians backing them need to go. Really, the problem is both parties just do not get it.

i wonder if Bern would walk back the Bush rule on not allowing CC debt to be written off in bankruptcy, or is that already gone?

“Maybe the Federal Reserve needs to open a retail window.”

– I love this dry humor. Loyal readers of this site know that the only welfare queens who benefit from the Fed’s largesse are the ones who borrow in sums greater than 9 digits.

Donald ??

“Donald?”

Oh good grief Charlie Brown. Donald is small potatoes (paging Mr. VP Quayle) compared to the players currently enjoying the benefits of the world’s largest QE liquidity drug dealer. TDS always brings out the gems/jerks but Wolf thankfully runs a classy place.

I think 635 was being Ironic Press.

Av8r,

Thanks for helping press

Perhaps in the US things are different, but I get a steady stream of loan offers from my banks both through my email mailbox and the apps.

I suspect anybody and any company with a minimally trustworthy credit rating gets this stuff whether they like it or not. Those in the lower half of the credit ratings (we haven’t got a FICO score here) are probably passed directly to the rapidly multiplying shadow banks.

It has never been easier to get into debt.

But on the other side car loans and credit cards are seeing interest rates steadily creep higher the lower interest rates and effective yields are pushed. If you are a prime borrower Toyota Financial Services will give you a loan for Yaris Hybrid for 8% EAPR. The average yield (not coupon) on Italian 10-year bonds is 0.9%. Wolf is absolutely right in saying that there’s something very fishy here, and I am not talking about delicious and nutritious (with just a tiny hint of mercury) Basque cod.

Just bought a used a Sienna with 15k miles on it. My credit union offered 3.5% for 48 months. CarMax offered 2.79% for 60 months. Money is still relatively cheap. If the economy tanks out, I’ll sell my house, pack up the kids, and drive the van to a nice spot down by the river.

“Money is still relatively cheap. ”

You are talking about a secured loan with Lo-jacked collateral that can be quickly repo’d – and you were probably targeted by higher income/strong credit history.

Unsecured credit is a different ball game – although not quite as bad always and everywhere as made out by some…

Right, MC01, I do need to update the Cod Index.

Thx, Wolf, this is informative. We all know this is going on; but quantifying it is the QED that speaks volumes.

I would have also appreciated a reminder, in a post like this, of what “investment grade”, and “junk” bond ratings are. Of course, a triple-A rating can go to junk in a heartbreak when you get a crash…..but wait, the Central Banks will never let that happen again, right ?

Cod Index:

Across the river in St. Paul, a new restaurant, Estelle, has just opened. They focus on Spain, Portugal and Italy.

“Salt cod croquettes are another example. The cod is soaked in water for two days to desalinate it, then carefully poached in water. Potatoes are cooked in onions and garlic and mashed. The secret ingredient? An eggy pate a choux.

All three – cod, potatoes, dough – are combined in equal measure, then rolled, battered with panko and fried until the exterior is tantalizingly crispy and golden and the interior is creamy and fluffy, with the cod flavor sneaking through in whispers rather than shouts. Don’t miss them.”

If you’re ever in the Twin Cities, Basque cod is on the menu.

http://www.startribune.com/new-southern-european-restaurant-estelle-is-a-gem-in-st-paul/567801152/

My only recommendation is always tip the server in cash. Leave the high interest rate credit card to pay the house.

Here is my color-coded plain-English scale for the three major corporate credit ratings agencies:

https://wolfstreet.com/credit-rating-scales-by-moodys-sp-and-fitch/

I am looking to get a small BMW for my missus. They quote 12.4% APR, for a 48 months hire purchase job. This is in UK.

It’s not too bad. Doable.

Where I am there has recently been some tightening of regulations in respect of consumer loans (far too late, as household debt here is beyond belief). I assume it is as a result of this that I have noticed what I suspect is a shift of focus.

I have a little company, and I didn’t get such stuff directed at the company before. But recently I’ve been getting a few not particularly sophisticated approaches from enterprises that want to talk to me about sorting out some financing for my company. That’s more or less the inverse of what’s currently going on with my private mail, where all those offerings of credit cards and unsecured consumer loans that were dropping in constantly have just about dried up.

Otherwise, the Skrei season is soon coming to an end for this year, so fresh Real Cod ™ is soon to be off the menu for a few months. For pure eating pleasure I recommend freshly caught cod’s liver, chopped and stewed in cod stock with onion and black pepper (the magic trick is quickly cooling it with cold water and reheating it three times during the cooking process). Pure bliss.

Yeah, like Alipay. Can anyone do the rate comparisons between AntFinancial and our personal loan rates? Are the socialists cheaper?

Impossible to get a loan, yet Hedge Funds and REITs can tap into 1.5% REPO money. How’s that for a bifurcated rigged arrangement for some?

It seems as if those bottom 50% are all living “quiet lives of desperation,” but somehow this façade of an economy keeps on rolling merrily along.

I’d say the bottom 70% minimum are struggling The bottom 20 percent are desperate

It’s been nearly impossible for some time In 1998 I was part owner of a 17 acre subdivision in the Hamptons that we bought at a bankruptcy auction for cash in 92 and went to Bridgehampton National to get money to build multi million dollar homes and was sounded rejected Good credit and great collateral Go figure There loss I borrowed from my partner, a lawyer in his 70s with lots of cash and he did very well

Frederick,

Good for you. I always wanted to be a part owner of a Hampton subdivision. It was that or own a bank. Haven’t got there yet, but I’m still working on it.

what did a 70 year old do with all the extra dosh? i’ve been trying to figure out this mindset for quite some time. he obviously had plenty of cash to ride out his golden years.

Wolf,

Wanna start a credit card company?

Seriously, the credit business is not that conceptually difficult – borrow at 4, lend at 24 or 20 or 16…

So the real question may be – where are the flood of competitors? That would drive the spread down.

For credit cards, network effects/locked in relationships with established oligopoly of Visa/MC/Amex/Disc probably has a lot to do with it…and regulatory headaches are many (despite absurd lend on rate).

But there is a lot of room for competitors to offer some capped level of CC consolidation debt – no network hurdles there, just need to get debtors in the door with 25-x rates.

These are bad risk debts…but the current spread is huge. Maybe there is some contractual impediment to consolidating CC debt (although it is hard to imagine CC cos refusing loan payoffs).

Maybe the adverse selection problem is really bad (CC consolidating borrowers are more likely to default since the consolidation loan can’t be used as cash substitute the way a credit card can).

But a cap on amts that could be consolidated might address that risk – although it would also cap rate savings to borrowers.

I would fund the credit card business with the Fed subsidized repo market.

It might be occurring as we speak.

Good question. Just guessing: A card that offered 10% FIXED would be hard to distinguish from others that offer 10% as the habit-forming TEASIER. Would the customers believe that the 10% would never rise? Would the company be able to resist the temptation?

There *is* a lot of room for competitors – in what is not really a conceptually complicated business.

And there is nothing stopping nonprofits from getting into the unsecured relending business.

Maybe that ought to be tried before MMT helicopter “loans” (wink wink) on a ntl basis…

A major problem as I see it; occasional CC user for form and keeping a “credit” history current:

Charge commensurate rates for commensurate risk histories. For myself a history of more than 50 years CLEAN should merit a large discount in rates fore whatever reason I use the CC.

Example with multi thousand dollars of “open” credit line when using the CC for a major auto repair involving maybe several thousand dollars the interest rate should be no higher than say, 6% or less. No. I’m still charged the incredible rate of 16% plus. It seems there are no CEO’s/Boards of these CC companies that have any brains at all. I know there are CC’s that offer “cash-back” etc. incentives but lots of us just want the best rate up front without the gimmicks. I guess I’m just old fashioned. But, it does incentivize me to NOT use the CC.

That is an eye-opening chart! Can it continue to climb even higher?

Those closest to the cheap and easy money (banks, wall street, hedge funds, the uber rich) get even richer.

Those at the end of the line get destroyed.

Which leads to the “wealth gap.”

The solution is higher interest rates and making it hard to get credit.

Note: Hard = you actually have to make a profit and be able to pay the money back.

“This is the bitter irony: Average credit card interest rates are at record highs while the Fed has spent years repressing interest rates to record lows for just about everything else.”

Actually there’s plenty of economic activity near the bottom of the pyramid fueled by these ultra-loose monetary conditions.

This stuff has a nasty habit of turning truly toxic but just like toxic waste it gets pushed out of sight: it’s in the shadow banks’ accounting books, in the small local banks that never make national news and finally sliced and diced and packaged into Asset Backed Securities (ABS) which are sold to pension funds and other poor devils driven nuts by the scramble for yield. This stuff has always existed and has always turned toxic but lately it has a nasty habit of lasting longer than it used to and hence cause much more damage: just look at all the two-bit real estate speculators around. Or the poor bloody infantry of the franchise world, those firms that dump a few cool millions to open a few Burger King restaurants that are perpetually deserted. Or all the retailers selling exactly the same cheap clothes as Mango and Zara. Take your pick between PCB and chrome plating sludge.

We live in the Jurassic Age of finance. The predators rule, until they don’t.

petunia, I always enjoy your comments. I read this one and tried thinking what to call this financial age….Finanzoic? Monetozoic? Neoliberalanthromiocene? Debtopithecus? Hat is off to you.

The Keynesian.

Ended by the Sweet Meteor of Monetary Doom.

Ucas127:. Hope you know that Keynes played a major role at end of WW1 in ensuring that WW2 happened!

Very few are aware of how much grief this misguided soul caused in the last century and into this century!

As usual, corporatists profit from the blatant perversion of Keynes’ policies while making him a scapegoat for their own rapacity. Whatever it takes to perpetuate the frauds.

The meteor is heading out… to the moon. It’s the Federal Deficit and the fuse has been lit during one of the longest “economic expansions.” Keynes is spinning in his grave.

Notice that the GOP no longer cares (or even mentions) the deficit, not that it “matters”.

Talk about “monetary doom” Mr. Cas. Take off the rose (Orange) colored glasses.

Meteor inbound? :-)

Modern Monetary Theory is Keynes squared.

Even Keynes knew stimulus deficit spending had to be terminated at some point. Not now.

“Modern Monetary Theory is Keynes squared”

Agreed – and there is a strong flavor of literal fascism involved when you can actually pin MMT’ers down as to what the hell they mean by “countries can’t go broke…”

1) because gvt can throw you in jail/shoot you in head if you refuse to use a currency they can freely forge,

2) and, after 200 pages of obfuscation, MMT’ers will finally admit that a nation can be *ruined* through printing inflation…just not “bankrupted” – that is some Clinton level “is is” bullshit right there.

MMT has and is working brilliantly to fund wars and occupations and tax cuts for the rich and corporations.

If anyone suggests using MMT for people instead of wars and the rich, you guys come out of the word work poking fund at it.

And then you say the wars, occupations, military doesn’t cause deficits but SS & Medicare does.

I recommend you look at facts for a change.

MMT is a proven success. You just say it is not, when someone says let’s use it for things you don’t want.

When that Japanese bank finally blows up we can pick up the MMT topic with some facts.

“When that Japanese bank finally blows up we can pick up the MMT topic with some facts.”

You and I could be dead, before that happens.

In the meantime, my statement stands as 100% accurate…until we’re both dead, I guess.

Well said, timbers. Well said, historicus.

So what’s going to be the metaphorical asteroid the next time around?

probably the one that, in retrospect, should have been obvious.

What should we do in investments then, buying gold, or bonds, or stocks, or commodities, or what? What’s the best way to invest our money in this low bond rate period? Thanks.

Well… Low interest rates, if not for the fed, would indicate that there is too much in savings. Even if this is artificial, the market indicates your savings are not wanted. Stocks are overvalued and yet in unperterbed circumstances could go up indefinitely but more likely not. Gold is subject to too many taxes. Basically, they’ve decided you shouldn’t bother investing if you want risk free returns. Invest in your own business then.

“Invest in your own business then”

Mostly agree – but keep your start-up and overhead costs under control.

Demented gvt policies have created a macro economy tap dancing (pogo sticking) on a razor’s edge.

Alternatively, there has been a rise in revenue royalty financing (loans to SMB, repaid off the revenue line – so no accounting games, and interest returns well in excess of bank deposit rates).

It would be nice if something along these lines were made available to individual investors to put money in (safely). It avoids the oppression problem of being a minority shareholder in a private company…but would hugely expand the investment opportunities in SMB for smaller investors.

So far, this is still a tiny, obscure corner of the invt mkt – there is so much lendable money sloshing around in the traditional lenders that borrowers have not really had to be open to new ideas. They just put up with the traditional BS of their traditional lenders.

The central banker cattle drive is into equities…..but you are about 23,000 Dow points late. Didnt you get the Fed memo about perpetual QE?

“central banker cattle drive is into equities”

Perfect image.

Cowboy “Zimbabwe Ben” Bernanke’s cattle drive…

Dirt:: Not making any more of it other than in the South China Sea (or whatever name is fashionable with you,,)

My understanding, long term, only things that actually keep up with inflation are waterfront (maybe ocean or gulf front actually, not sure about all these manufactured lakes, etc.,) property, fine art, and fine jewelry.

Of course, growing up in small town and farm,,, this is my clear preference. Grand ma, who lived through the great depression in mid life, said I need a trade and a profession: She recommended grocer and plumber, because ya gotta eat, with usual results thereafter.

If global warming is for real, even those multi-million dollar condos in Miami Beach won’t be safe investments.

Agree, same story for the very expensive investor properties over here in the Netherlands on the North Sea coast that are selling like hotcakes for ever higher prices; speculators can’t get enough of them. While our government refuses to build anything except very expensive and big abominations in the suburbs, they are pulling out all the stops to build more investor properties in every last piece of nature they can find. Many of these properties will likely be flooded before the end of the century even in the base case scenarios, and much sooner if the worse case predictions come to pass (which looks increasingly likely).

But who cares, FED and ECB will make sure the mortgages remain above water, RE values can only go up ;(

Years ago in between jobs when I was moving I let some balance run up on one of my credit cards. I was making monthly payments but things were a tad tight until the new job started paying. Always paid more than minimum and the card had a limit of around $11K or $12K. The minute the balance got up a good ways the interest rate auto adjusted skywards. Quickly.

I paid it off ASAP and returned to never carrying a balance. It reaffirmed my hatred for banks and similar institutions.

What give’s? Well that’s easy. The banks and hedge funds get free money, from the government, the federal reserve. They need help you see, its tough out ther, banker’s and broker’s bonus’s are looking a little weak for 2020. So, its open season on debtors that is average people, pillage at will. Actually, they like low score debtors and delinquent borrowers-all those penalties and interest on top of penalty and interest. You should buy their stock. What’s different from 2008, banks got bailed out and delinquent mortgagee’s lost their homes, or had so much interest and penalties tacked on, well, they’re still working, for the banks. And the house they lost, well its now owned by a Hedge Fund and rented out to them. Their first born, they have a lot of student, and no life an live in the basement.

And the bankers, the brokers, well they got their bonuses, their fourth house, and now its a new day, the suns coming up. Morning on Wall Street, Twilight in America.

What I find even funnier, is that the whole point of the deregulated financial system is that it is meant to be the best way to allocate economic resources to where they are needed the most.

So let’s look at the results – we have billions being plowed into food delivery services, and mattress companies, yet nobody can afford a home and our infrastructure is falling apart.

This is just stupid. It is akin to the proverbial hole digger with ten incompetent supervisors around them, except that the hole digger is collecting their meals on a bicycle while they commissions some more reports on how to dig the hole. Even in freedom loving USA, 30 years back, someone pragmatic would have eventually put an end to this insanity.

Skewed cost of money brings misallocations. That is why what Central Bankers are doing is destructive in the long run. They steal from the future to fluff the present.

When you want a drink, you’ll agree to anything to get one. When that transaction is complete, you’re left with a reason to drink!

Wolf,

Great article and charts! But….you are (erroneously) assuming that many people who borrow on credit cards:

1 – understand they are borrowing money

2 – know the interest rate they are paying

I do a lot of volunteer work in this space, and I teach personal finance at a community college. Many people don’t even understand that when they carry a balance on their credit card they are borrowing money.

In addition, most people under 25yo (and many older) don’t know the interest rates on ANY of their loans. Auto and student especially. Ask any students or recent grad what interest rate they’re paying. I’ll wager far less than half know.

Next time you get into this sort of conversation with a non Wolf Street reader, ask them if they have any debt. Then ask them how much they owe and what interest rate. Odds are they cannot answer both of those.

There are a number of reasons for this, such as

– people rarely shop for cards based on interest rate (they look at points etc)

– people often don’t expect to run up balances (it’s only for emergencies)

– lower income borrowers have limited choice of cards (I’ll sign up for whichever card approves me)

– there is a standard argument to “build your credit” (I need to use it in order to build my credit)

All good, true points.

It is amazing that classes like Home Economics and Personal Finance are usually the least respected in high schools – where they still even exist.

They will have 10x the practical import of the more traditionally respected classes for 90 pct of the students.

It is almost like financial education has been intentionally crippled…

Certainly agree with your final sentence: “It is almost like financial education has been intentionally crippled…”

Teaching construction tech classes at a couple of high schools a while back, I was appalled at the financial ignorance of the students AND their total lack of basic math skills; and, students had to be minimum 16 years old, though the classes were open to older adults too…

Most of the kids thought they were going to be able to have a life, usually with kids, on $10 per hour, a total fantasy at the location/time when monthly rent or mortgage was approximately $1,000 per bedroom.

Most of the kids picked right up on the basic math when it was part of actual building process, though some were so far back they could not even add or subtract whole numbers to start.

If teaching that course today, I would make Wolf’s work REQUIRED reading, with frequent tests. LOL (at least as long as I could get away with it before the administration shot me down, eh )

Maybe the internet might make things a little better, since it is capable of disseminating practical, useful info (Ave pay, rents, taxes, by metro, etc) to a wide audience.

In contrast to the MSM, which simply pumps its self-interested pap into the gullets of a wholly passive audience – thank God, they are such noble, selfless, brilliant gatekeepers…otherwise, what would the country have become…

V Vet,

In BC Canada I taught carpentry/construction for about 15 years in high school. I also taught a few math classes, etc. We offered what is called applied math, often referred to as dummy math. Instead of a final exam I had students design and draft a tiny house, cost out all materials, and finance it all with a standard mortgage. Anyway, the kids did just fine and even the artist types took it and ran. They had some class time to work on it, but had to complete it on their own time.

I had almost forgot that once they figured out their monthly mortgage payment, they also had to figure out how much of an hourly wage they needed to earn to pay for it all, including food, transportation, entertainment, heat and lights, clothing etc. They learned about payroll taxes…the difference between net and gross pay, the works.

I had a mom phone me after I contacted her that I was failing her son because he did not complete the project. He would not graduate. She asked me, “What should I do”? I told her she had just one question to answer. How would she feel about her son living in the basement for the next 10 years, in the home she shared with her new husband. I think it took about 2 days for the project to be handed in and he received a ‘pass’, minimum standing for being late. :-)

Anyway, the kids learned all about finance and mortgage rates, and were able to use their phones for this part of the project. Win, win, win. The lazy kid graduated and moved to Alberta and found a job. The mom was happy. I thought you would get a kick out of this story. As an aside, in BC teachers have autonomy and are able to decide what and how they teach their subjects as long as outcomes are met. In other words, no one tells them how to do their job….just do it and get it done.

I also very much agree with you comment about land, etc.

In 2008 the same credit dynamic was working, people paying health care costs off CCs, and then consolidating them with REFIs. https://www.tctmd.com/news/nearly-half-diabetic-patients-struggle-pay-medical-bills Then one day you are homeless and sick.

I seem to recall reading an article a couple months back about a hotshot kid who made some good money after dropping out of college in the early 00s. He worked as a loan officer selling cash out refis. He was shocked to learn most people weren’t doing it to get granite countertops or a new SUV or boat. Most people were trying to pay off medical bills and other such debt.

I have reached the point in all things market related that it would be better just to make things up. Up is down and down does not exist. Make us feel good. I saw Elvis in a Uber yesterday.

I saw Zimbabwe Ben Bernanke waiting in line at the welfare office in Vegas.

Behind Buffett and ahead of you.

Many people have been trapped by staying with the same card issuer for too many years and having that account interest rate reset upward as the Fed screwed with interest rates. Personal experience with Chase Freedom card. Jaime Dimon …. Dead.

My high rewards credit cards have outrageously high rates, I don’t care they are auto paid every month.

I wish I could articulate a more eloquent statement, but an exhausted “wtf…” is the only thing I can muster.

Thru history the rich always screwed the poor, needy and /or uninformed somewhere.

CC interest rates is govt sanctioned stealing, no doubt about it.

The shady underbelly of our most respected(!) institutions.

Where is the rule on usuary.

There are limited defenses: don’t borrow on CC; pay CC in full on time monthly; default (comes at a cost).

Its a jungle out there.

Well you say ‘government sanctioned’ – but how so? This is just predatory, unfettered capitalism.

When governments intervene with regulation they are screamed at as ‘communists’, due to the way decades of neoliberal propaganda have trained them to think (ie to direct their ire at entirely the wrong set of people…)

Andy is correct. When gov’t turns a blind eye to racketeering, it is sanctioned stealing. And agree with other commenters that a lot of this CC debt is to finance people’s healthcare racket expenses.

But hey, aren’t these rackets two of the biggest boosts to GDP lately?

The image that comes to mind.

Sadly a “SCREW”.

One person turns the screw with a screwdriver.

The turning screw is inserted into another person.

Causes much personal suffering.

Not a pretty picture.

Re: Meteor inbound/too much liquidity has ruined the markets etc. Could we look to Japan as a case study? They had a massive asset bubble that burst and the govt fiscal spent their way out of it – as much as possible, point being they still have the 3rd largest economy and despite big problems are pretty ok. So maybe its possible our world ponzi economy still has many years to go before it runs out of asset stripping and printing to keep it zombie stumbling onward??

“our world ponzi economy still has many years”

Gvt ponzi ZIRP has been expropriating the interest of the savings class (made up of the most prudent and future oriented part of the population) for about 20 yrs – mainly to keep the kleptocratic DC way of life alive.

Every member of that group spends part of every day now thinking of ways of ending DC’s fiat monopoly and the long-standing abuse it has engendered.

Considering that savings get accumulated by the planners and the prudent of the world, I would not bet against them ultimately disintermediating the shit out of DC.

On the day when that solution goes live, there will a thunderclap, and DC’s reign will be over in an instant.

DC has courted ruin…and it is going to find it.

I think it is more a supply problem than demand. I think your data shows HELOC balances quite low as well and that people are deleveraging–well, some people. People with little access to capital also find no one, in this dollar shortage world (which despite “printing” seems to be the problem, hence REPO ops by FED, which only goes to a certain subset of haves, who then refuse to make it available to fringe borrowers). If banks won’t lend to each other, why are they going to lend to the worse borrowers out there?

Time to bring back usury laws.

At least this helps my conscience tell me who to vote for next November.

“At least this helps my conscience tell me who to vote for next November.”

One lever is for a multi-billionaire (ex Democrat), versus another lever for a multi-multi-billionaire ( ex Republican).

Choose wisely…… Politburo style

The Republicrat duopoly is a two-headed snake serving the same master: predatory capitalism. If you want to participate in this Wall Street puppet show, feel free, but don’t be under any delusion that any of the candidates gives a damn about anything other than further enriching the already super-wealthy and enabling the oligarchy to further concentrate all wealth and power in its own hands.

It’s a bizarre new world where the duopoly emerges more fully from behind the curtain. Interesting that Bloomberg supported W. Bush in 2004 and spoke at the RNC, whereas Trump-at least in part-won the nomination by bashing the Bushes and the Iraq War. As someone who has watched cable news for the last 15-or-so years, it was a sight to see people like Rachel Maddow become not altogether unfriendly with the likes of John Bolton. What was that saying about strange bedfellows again?

Gershom,

I have a friend who is a college professor of English literature, and from what he says all of his students agree with you. It was shocking to me, but I guess if you are getting the shaft with student loans, maybe it is understandable.

Subprime auto loans are very expensive for those with the worse credit. Predatory payday lending was banned by some states.

Predatory payday lending was banned by some states.

Your DOTUS hates it when they do that, so he’s been taking payoffs to gut the CFPB and make predatory lending federal policy:

https://www.propublica.org/article/trump-inc-podcast-payday-lenders-spent-1-million-at-a-trump-resort-and-cashed-in

https://www.usatoday.com/story/opinion/columnists/2019/02/14/donald-trump-makes-predatory-lending-great-again/2872953002/

The US economy is completely dependent on increasing debt just to keep from crashing. Consumer interest rates must be kept high, especially for the desperately poor, in order to maximise profiteering, so usury laws are evaded when they’re not actually dead letters. Conversely, interest rates must be kept low for CEOs so they can indirectly liquidate their companies with debt. Investors must also have low interest rates, not just so they can juice the stock markets but also because they’ve already leveraged their expected gains to juice the markets even more. You can’t raise their rates without causing a crash. You can’t limit their profiteering on consumers because they use those proceeds to make their own payments so they don’t have to touch their stock speculations, which would also cause a crash. And so forth.

The system holds together so long as enough players can make their minimum monthly payments, which won’t last much longer because those supporting the system at the bottom are getting crushed. The shock waves will travel up the food chain. I figured 2026 at the latest, but it looks like the cracks are already widening.

I’m just a spectator so your worries about me are unfounded. I’ll be just fine unless somebody hits a foul ball in my direction and I can’t get out of the way.

Unamused, spot on. Under 45 minimum payment debt slave over 45 hanging on to antiquated ownership set for reverse mortgages to retire. IF we could just have a pandemic we could get rid of all old people balance the social obligations, get rid of the conservetive voters and get bernie in. Nobody would be evil enough to do that.

This is the bitter irony: Average credit card interest rates are at record highs while the Fed has spent years repressing interest rates to record lows for just about everything else.

For how much longer will We the People meekly submit to the debt serfdom the financier oligarchy and its Fed accomplices are imposing on us?

Gershom:

It will last as long as the state of “no historical memory” exists……Sheeple….

But why are consumers willing to borrow at 20% or 30% in the first place? Or even at 16%? These high interest rates almost guarantee that these already strung-out consumers won’t be able to deal with the debt.

In our oligarch-looted economy, one in four people are using their credit cards to pay for essentials like food and rent. Of course they can’t afford this, but the Fed’s debasement of the dollar caused by its deranged money printing since 2008 has made housing unaffordable for most of the population and pushed up the cost of living despite our fake CPI inflation statistics and the Fed’s ludicrous claim that low inflation is a problem. Meanwhile, savers have been bilked out of an estimated $2 trillion in interest earnings, while the financier oligarchy who are the sole beneficiaries of the Fed’s “No Billionaire Left Behind” monetary policies have amassed unprecedented wealth and power at the expense of everyone else. And yet not one candidate even dares to mention this criminal private banking cartel and its swindles as the primary reason so many Americans are broke, deeply indebted, and stressed out.

“Of course they can’t afford this, but the Fed’s debasement of the dollar caused by its deranged money printing since 2008 has made housing unaffordable for most of the population ”

The direct link between the halving of mortgage rates and the doubling of home prices/rents is the truth that dare not speak its name in American politics.

The Feds have a limited number of sub rosa tools to manipulate the economy/offload blame on others…money printing/interest rates are a biggie and absolutely central to the power of both parties (which hate each other, but find common prey in the citizens).

That is why an endless ocean of irrelevancies will be yabbered about over decades in American politics, but interest rate policy will not hit the debate floor.

Not just American politics, it’s the same or even worse in Europe. In Netherlands mortgage rates are now 10x lower than 25-30 years ago (from 10-12% with 20-30% downpayment to about 1.0% now with zero downpayment). Home prices increased accordingly (in my city often x10 or x15) and rents outside the social housing sector also increased hugely, especially in the last few years. And despite surging rents, the actual space you get is getting smaller every year too, it’s a new version of livestock farming that the Dutch government can’t get enough of.

A growing chunk of the population is unable to buy a home despite record low rates and has to spend over 50% of their income on rent, if they can find some place to live at all, because all the “new arrivals” get a free home first. While renters are punished, speculators can lend money for extra properties for less than the official CPI, and they are gobbling up properties like there is no tomorrow. In my city most of the homes over 300K (basically that’s anything that is slightly acceptable) are now purchased by both small and large speculators; they fully control the market.

Large and small business similar story: multinationals sometimes even get paid to borrow money, small business can’t get any loan even if they have a long and healthy financial track record. Rates are so low that the banks are not interested in loans of a few 100K euro for business, far more interesting to loan money to RE speculators.

The central banks are destroying the economy and the social fabric. Unfortunately, as long as the game is still running a majority is profiting from these policies so it’s difficult to turn the tide; for too many a return to economic sanity is no longer an option :(

So you agree with John Williams numbers on inflation then Dont let the big, bad Wolf hear that

Some poor uneducated people are just oblivious Years ago I was doing some renovation work for a poor elderly black woman and she told me about some aluminum siding firm that she had contracted with to reside her home When I looked at what she would be paying over the life of the loan it was totally outrageous She had NO clue how much she would be paying over 15 year term of the loan I got her my friends lawyer who got her out of it

Some poor uneducated people are just oblivious

And easily exploited. Hence the need to keep them poor and uneducated by promoting social divisions, gutting public education, corrupting the news media, converting the middle class into gig workers and debt slaves, and making sure people are weaseled into voting to screw themselves. That will Make America Great Again, one disempowered, impoverished demographic at a time.

If you don’t hang up the phone when you drive you won’t be able to dodge the potholes.

Nobody benefits more from poverty than the left.

Nobody benefits more from corporate disinformation about poverty than the right.

The entire War on Poverty was a jobs program for professional liberals.

The War on Poverty was lost because the rich can afford the best weapons.

In the black community they always speak of needing a “program” to fix problems.

Corporatists cause the problems, blame the victims, and smear anybody who says otherwise.

Your turn.

Unamused,

Don’t lecture a Puerto Rican girl from a Puerto Rican neighborhood in NYC about the underclass. I saw the destruction caused by the War on Poverty from its inception. I can tell the stories first hand. I know makers and takers, as they say on Wall St.

The right may benefit from the failures and rhetoric of the War on Poverty, but it doesn’t make them wrong.

“gutting public education”

To judge by the millions and millions of government employed teachers (Dem foot soldiers) and the fact that their per hr worked total compensation is well in excess of that of the non political courtier class,

public education is far from gutted…just vastly misappropriated.

Government schools are funded by a wealth tax that ignores the debt required to acquire that wealth (the mortgage on the home) – there are very, very few taxes so privileged.

Underfunded schools (on a ntl basis) are a very carefully crafted political myth.

@Cas127- Consider that the gutting might not be in the funding, but in the content that would make people financially self-sufficient. Personal finance should not be a subject taught only in the school of hard knocks. Parents can certainly help, but most need the same class themselves!

Agree with you Petunia,,, been there done that: blind in both eyes for a time, due to stress doc said, I moved from liberal to conservative state to get ”out in the country” and away from at least some of the stress, and then applied for help; although I received help, the admin folks in the conservative area did everything they could to get me off the dole ASAP, including getting me several job offers, etc., (one of which I took ASAP, but it took a while),,, and only then i found out that in the other, liberal, state I would have received a whole lot more ”help” and been encouraged to stay on the dole for ever… hated the experience, and, luckily, got my health back and have never done the dole thing in the last 45 years, thank God.

My clear understanding since then is that well over half of the ”welfare” dollars actually goes to support the very middle class and above folks doing the admin, etc., etc.

@ Unamused and Petunia –

Both parties are complicit in all of the ills that you both mentioned.

Petunia is right that government “programs” tend to be ineffective. Consider that participants in government “programs”, once created, are not in business to put themselves out of business.

Unamused is right that cutting the programs, without anyone taking alternative steps to fix the issue, just makes things fester.

Unfortunately the common-sense solutions don’t benefit either party’s donor class, and thus don’t get supported. This is also why personal finance has disappeared from high schools, and why mass media don’t cover similar issues of public interest with any real honesty.

I’m not saying anything you both don’t know, just suggesting that you look past the left/right issue and realize that neither side of the ruling elite has a solution because neither side wants one.

Between the two of you there’s enough common sense to write a short textbook. I’ll publish it if you work together on it!

The elderly are targets of scams on a regular basis. My mother-in-law lives in a retirement community and says she gets a scam call every day. She got one the other day with some little boy crying on the other end, pretending to be her grandson, saying he needed some money to get out of trouble. Luckily, my mother-in-law remembered she didn’t have any grandsons.

I repaired a roof for a nice very old German lady living in a big old house in Queens, NY She had a recurring leak and I noticed someone had done a quick Rub Goldberg repair job on her chimney flashing I asked her about it and she told me she paid some nice men a thousand dollars to repair it This was in 1978 so it was a lot of money For nothing She was great served me a nice hot lunch Lots of crooks out there willing to cornhole a nice old grandma

Don’t worry. The government will “extinguish ” the debt … one way or another.

It is clear that anyone paying interest on credit cards CAN NOT pay down the balance. They are essentially broke.

A chart of delinquencies is key.

The Fed has TAUGHT people to borrow, and now they are screwed, much like student debt.

It is clear that anyone paying interest on credit cards CAN NOT pay down the balance. They are essentially broke.

Welcome to Amerika.

I can’t say this enough, that senators from both parties confirmed as Treasury Secretary the criminal who headed up Goldman Sachs during the period of their record fraud settlement. Al Capone as head of the Justice Department?

Hello. Who runs Amerika?

The Owners. – George Carlin

Hello. Who runs Amerika?

Hi there. It’s an organised crime syndicate. Mafia Don and his mafia dons.

Bipartisan organized crime syndicate.

Billy and the DNC triangulated and sold out. Dems who didn’t are somewhat ahead in the primaries for now but are certain to be quagmired by sellouts on both sides. Looks like you’re going to stay stuck.

Donny boy doesn’t run this country That’s for sure

“it’s a big club and you ain’t in it”. GK. I would bet that the higher rates are do to folks at the bottom rung just walking away from their debt.

Debtor prisons are making a comeback. Those won’t be as profitable as the loan sharking until there are a lot more of them, but loan sharks can take care of that.

Unamused:

America of today is still a grand plantation where the “whip” of old has been replaced by the plastic credit card.

Total credit creation only allowed to go up. No matter how bad a sector is, the direction of total credit creation is ….up.

Japan stock mkt implosion in 80’s while accompanied by huge deficit spending and central bank monetization. I actually went back and looked it up and found that private credit creation declined faster than public credit creation. Total credit went down….hence, deflation. The federal reserve has promised that they ‘won’t make that mistake’ here.

1 fed wants gov’t and central bank partnership when recession comes.

2 fed says it wants to fight climate change bullshit

3 fed says it may let inflation run a little ‘hot’ for awhile if necessary

when the recession comes, there will be no more than a minor correction and it will be the biggest buy signal ever.

1-2 trillion dollar infrastructure, green energy bullshit financed by fed at low rates.

= mkts cannot do anything but go higher.

because more money =equal higher asset prices. it’s tautological.

No, i don’t back this. I’m just a realist. This is what is going to happen.

The federal reserve board is the very face of evil on this planet.

They will wreck more lives than any dictator in history.

Somebody wants to borrow and somebody wants to lend. Life’s no fun if you can’t eat out. You only live once.

Nah I have the money to eat out and frankly I prefer home cooking Don’t trust other people with my food either to be honest And I’m having a ball lol

It’s a Crony Economy and you ain’t in the club!

I always wonder what’s the rough percentage of people who use credit cards for the sake of borrowing out of necessity, versus those who use them only for card benefits such as fraud protection/rewards/cash back.

I would think the majority pay back the balance every month and don’t incur any interest, and only those who don’t have enough savings and have to resort to debt are willing to borrow at these usurious rates.

What’s the ratio between these two categories?

Or are some people actually financially illiterate and borrow with credit cards even if they are capable of paying off the balance each month?

The shadow knows and so does the mkt.

Credit creation is going to explode.

Why has the “WOLF STREET Credit-Card Spread Index” blown out?

If you are a junk company the financial world believes, and so far rightly so, that the central banks have their backs. Between this and TINA they are willing to accept a smaller yield.

Given the state of the job market for the bottom 60%, combined with the the inflation rate for things that matter, we have more desperate subprime precariat folk than we have had in a long time.

As the precariat grow more desperate and usury goes unpunished the credit card rate keeps increasing.

In saner times I would expect the junk bond rate to meet that credit card rate shortly as the precariat come to the end of their rope.

Given the current climate who the heck knows.

The ridiculous level is off the chart.

But think of the page views man! They are the beating heart of the financial colossus that is Wolf Street!

At $1 CPMs…we are literally talking dozens of dollars here!

I have 2 credit cards and don’t care what interest they charge. I pay them off before interest accrues.

IF they start playing games to charge interest, like from the purchase date, they will be cancelled instantly.

I’d replace them with a periodically funded small bank account with a debit only card used only for the convenience of on line payment.

Just another example of the bifurcation in economic opportunity. The Cantillon Effect in all its glory.

How cryptic.

In Cantillon’s theory, expansionary monetary policy constitutes a transfer of purchasing power away from those who hold old money to whoever gets new money.

In practice, those who hold old money also get the new money. So much for the Cantillion Effect.

The nonfinancial sectors need debt relief much, much more than the financial sector, yet the Fed shoots off new money solely into the financial system, to Wall Street and the TBTF banks. It is the financial institutions that have gained anything from these transfers of purchasing power, building up huge hoards of excess reserves.

So try deleveraging. As we have seen, investment by American employers will be timid and economic growth will be faltering at best. The stimulus imparted by government deficits attenuates the downturn. The much larger scale of government spending now than in the 1930s explains why this far greater deleveraging process has not led to as severe a Depression, but deficits alone can no longer be enough. The level of private debt has to be reduced, and that can only be accomplished with even more public debt, and your DOTUS has already given away the store. So good luck with that.

In ancient times private debt was reduced with a Jubilee, but the securitization of debt since the 1980s makes this impossible. Whereas only the moneylenders lost under an ancient Jubilee, debt cancellation today would bankrupt many pension funds, municipalities and the like who purchased securitised debt instruments from banks. You’re kind of stuck because the FIC now holds the economy hostage. You’d need to unwind all the existing debt securitisation and prohibit it in order to cancel the debt overhang. Good luck with that.

“Quantitative easing for the public” could work. This means monetary injections by the Federal Reserve, not into the reserve accounts of banks, but into the bank accounts of the public, on condition that its first function must be to pay down debt. This would reduce debt directly without disadvantaging savers, and would reduce the profitability of the financial sector without affecting its solvency. But the FIC likes its profitability, so good luck with that too.

In short, the FIC would rather detonate the whole system than solve the problem. So the only viable solution is distance from the system. I’m out of range, thanks.

You know, GDP figures look a lot different when you account for debt. It gets worse when you account for ecological assets, and make the appropriate projections, because all the GDP figures go to zero.

” You’d need to unwind all the existing debt securitisation and prohibit it in order to cancel the debt overhang. Good luck with that.”

This was the main problem after the Dutch Tulip Bubble (+/- 1637) ran its course. Half the population participated somehow, using verbal promises or something written on a piece of paper in the taverns where most of the trading took place. It proved impossible to settle the debts despite a government commission studying all options for over two years. In the end the public lynched a few politicians and somehow the economy got started again. Of course people never learn, the current Dutch Housing Bubble is about as bad as Tulip Mania with relatively even more fake money sloshing around.

This time we need to discard more than a few of the people responsible for the madness otherwise the lesson won’t stick.

As to ecological debt, this will get settled too, in fact I think it has already started :(

Unamused, I suspect you’re knowingly misleading a bit in your introductory comment. Just because those who hold most of the old money get all the new money does not mean that their old money doesn’t get watered down as well, it’s just that, since they get the new money and nobody else does, then their slice of pie gets bigger.

Your last paragraph, though, describes the one thing that most makes me want to tear my hair out: That we measure wealth by how much wealth we consume rather than by how much wealth we conserve. It’s a truly staggering feat of mass delusion to have succeeded in conflating the consumption and destruction of wealth with wealth itself…

I suspect you’re knowingly misleading a bit in your introductory comment.

I was being intentionally simplistic for mass consumption. Your explanation is more expansive and therefore more correct. Too bad I can’t recruit you.

Your last paragraph, though, describes the one thing that most makes me want to tear my hair out: That we measure wealth by how much wealth we consume rather than by how much wealth we conserve.

You may be pleased to know that where I come from we do measure our wealth by how much we conserve. Our ROI averages 8% by preventing the product of our labor from becoming parasitised and relying on carefully selected technologies. We do not use credit, fossil fuels, in fact most things most people take for granted in modern societies. We participate in the larger money economy less every year, in the hope we can avoid its problems until we too are overwhelmed, thereby buying ourselves some time.

I wish I could make some sort of similar claims to my credit, but I’m afraid I’m just more of a hypocrite, myself. My own puny attempts at damage limitation are frankly embarrassing, all things considered.

Would love to see some references cited for the frequency of the use of the Jubilee in historic times, in order to reduce private debt (re your statement above, Unamused; but I might have phrased its purpose a bit differently…).

Sure, we can start with the Bible, but we want additional records in order to establish to what extent, and where, the Jubilee has been in actual practice.

What, for example, is in Hammurabi, and Gilgamesh, re the Jubilee, or antecedent and similar ideas ?…..historians ?

The Cantillon Effect:

One more thing I had to look up while reading Wolf Street. I seem to learn something here everyday

“Credit-Card Interest Rates Soar to Record High, Bond Yields Drop to Record Low: What Gives?”

The most logical sounding conclusion for me on this would be: credit card backers believe “it” is going to hit the fan sometime this year with consumers tapping out, defaulting on their credit cards en mass, and this occurring possibly in conjunction with a significant market correction. Believing this, they are charging a proportionally higher premium for an asset (consumer credit card debt) that they now believe is becoming increasingly risky and thus demands a higher premium to hold. Simultaneously they are preserving capital via de-risking their other investments/assets by switching them to safe assets (US treasuries) despite the sub-inflation yield on them. These acts also reinforce each other precisely because the lost yield on preserving capital “begs” to be offset by a higher yield on their risk capital to maintain profits while “battening down the hatches.”

Of course one should never over rationalize what could just be explained by “blind greed that can be successfully gotten away with” – so that is also a perfectly viable and simple explanation.

1) XLF, the financial sector ETF, made a record high, perhaps because of C/C high interest.

2) An upthrust job is to send prices down. If it doesn’t happen,

its a fail UT.

3) XLF weekly had an upthrust. If XLF price will close lower on Fri,

XLF will also have a selling tail.

4) In the last few days XLF is moving higher on falling volume, losing momentum.

5) Yesterday new all time high @ was an upthrust above May

2007 previous all time high, from 13Y ago.

6) Thanks to the Fed liquidity, the financial sector is doing well even with falling % rates.

7) $BKX the global banking sector is doing well, but not as good as XLF.

8) $BKX failed to exceed the 2007 high.

9) The Dec 2018(L) entered the long term trading range from 1998 and bounced back up !! 1998 was HK.

10) Berkshie Hathaway/b last week was testing its Jan 2020 all time high.

The $100B buyback is doing a good job, transferring WB A shares to BRKb.

Whom, pray tell, has had a credit card with the interest rate of below 13% during the last 15 years?

Gee, borrow for next to nothing, lend out at 17% -35% …..and this is somehow a mystery?

I don’t understand carrying a balance on a credit card. I use mine for everything and pay it off every paycheck. I get cashback rewards, pay no interest, and the credit card company gets transactional fees. I do this despite the fact that the credit card company gives me a special rate every six month of 1.99%. That amount of interest is still too high to pay.

I have twice gotten timed- or otherwise glitched- out, in trying to update the cod index. Cod is up 100%, that will have to do for now. Inflation felt by the common man !!!

Thx all; Note to self: remember Estelle in St.Paul.