Why is this happening?

By Wolf Richter for WOLF STREET.

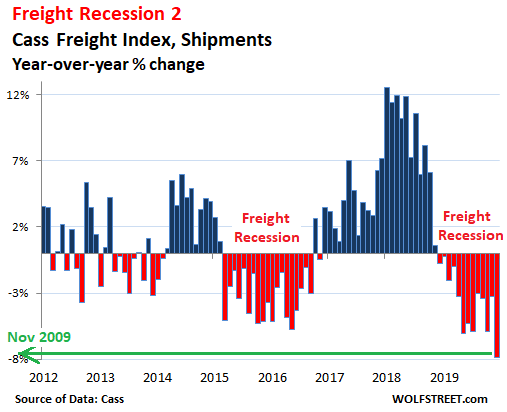

Shipment volume in the US by truck, rail, air, and barge plunged 7.9% in December 2019 compared to a year earlier, according to the Cass Freight Index for Shipments. It was the 13th month in a row of year-over-year declines, and the steepest year-over-year decline since November 2009, during the Financial Crisis:

The Cass Freight Index tracks shipment volume of consumer goods and industrial products and supplies by all modes of transportation, but it does not track bulk commodities, such as grains. As always when things get ugly, the calendar gets blamed – Christmas fell on a Wednesday, as it does regularly.

More realistically, December was also the month when Celadon Group, with about 3,000 drivers and about 2,700 tractors, filed for Chapter 11 bankruptcy and ceased operations — the largest truckload carrier ever to file for bankruptcy in US history. It rounded off a large wave of bankruptcies and shutdowns of trucking companies in 2019, most of them smaller ones, but also some regional carriers, and on December 9, Celadon.

Rail traffic in December capped off a miserable year, with carloads down 9.2% year-over-year in December, and container and trailer loads (intermodal) down 9.6%, according to the Association of American Railroads. For the 52-week period, traffic of carloads and intermodal units fell 5%.

The 7.9% year-over-year drop of the Cass Freight Index pushed it below a slew of prior Decembers, including December 2011. The top black line represents 2018, the fat red line 2019:

Cass derives the data from actual freight invoices paid on behalf of its clients ($28 billion in 2018). So this data is not based on sentiment surveys. It’s based on a large sample of the actual shipments in the US, involving real money, sent by numerous companies across many sectors.

The shipment boom in 2018 was a sight to behold. It had been fired up by widespread efforts to front-run the tariffs by loading up on merchandise. So some backtracking was to be expected. But not this plunge in shipments to multi-year lows.

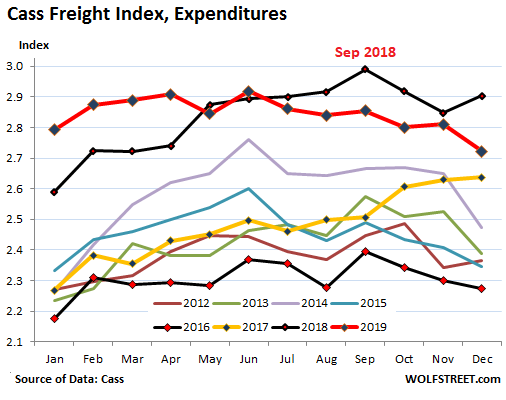

Freight expenditures fall, but remain high.

In 2018, shippers such as industrial companies or retailers or manufacturers groaned under the surging freight expenditures – and complained about it in their earnings reports. Total freight expenditures paid by shippers are a mix of freight rates, including fuel surcharges, and the volume of shipments. Some freight rates have remained high, and some companies such as UPS and FedEx have raised their rates, despite this environment of falling shipment volume. Other freight rates have come down under pressure, particularly in the trucking spot market. And for months, even as shipment volume was dropping, the total amount that shippers paid remained stubbornly high. But now this is starting to change.

In December, total freight expenditures – the amount shippers, such as manufacturers, retailers, or industrial companies, spent on freight by all modes of transportation – dropped 6.2% from a year ago.

That’s a steep drop, but expenditures are still dropping more slowly than shipment volume, indicating that there are pockets – FedEx, UPS, etc. – where freight rates continue to rise, and this leaves the Cass Freight Index for expenditures in December at still high levels, though dropping sharply (2019 = fat red line). Note the yellow line (2017) and the top black line (2018), as an indicator of how much freight expenditures surged in those two years:

What is causing this sharp decline in shipments?

Retail sales, powered by ecommerce, are holding up. Ecommerce is red-hot and brick-and-mortar retail is dismal. Retail sales, including ecommerce, rose 4.0% in the fourth quarter, according to the Commerce Department.

Total construction spending has bounced off in recent months from lower levels. In November, it grew at an annual rate of 4.1% year-over-year, but remains below the peak of February 2018.

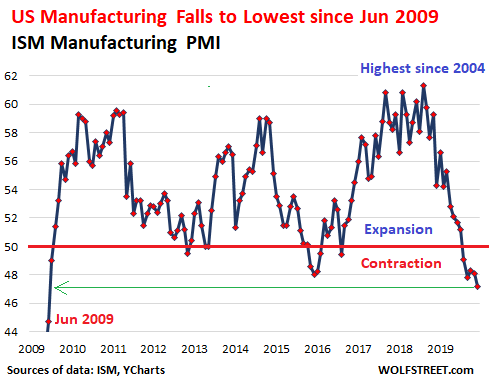

But manufacturing is weak and getting weaker. One of the data points on this theme – and there are many others: The ISM Purchasing Managers Index for December dropped 0.9 percentage points from November to 47.2%, the fifth month in a row of contraction, and the fastest contraction since June 2009, with employment, new orders, new export orders, production, backlog of orders, and inventories all contracting:

The Oil-and-Gas-Bust.

The oil-and-gas sector is now undergoing phase 2 of the bust that started in mid-2014. The price of oil is still down by nearly half from where it was then. The price of natural gas remains in total collapse mode. And the cashflow-negative fracking industry is getting morose, trying to curtail the bleeding, by cutting investments, cutting purchases, cutting employment, trying to persuade investors that they should send even more money their way.

And now this solid recession indicator is starting to concern me again. Read... It’s Time to Pay Attention to Commercial & Industrial Loans

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

How does the flooding in the bread basket affect the volumes of freight ? A lot of land out of use, thus less grain etc

please read – this doesn’t count bulk shipments of grains

we the onliners are trained – FREE SHIPPING – or we shop for best NET PRICE else where

while I like amazon – I’m finding many smaller shops can’t/won’t use them since they are sucking their profits

so I go to ebay or directly to store site(not biggies either)

I use ebay much more than amazon, same stuff same price…..and keeping the little guy alive.

I broke up with amazon last year and figured buying local would be more beneficial to my local economy. I like your idea, I might do that for hard to find items locally.

My marginal propensity to consume is way low, and I still work at lowering it, too. My “bucket list” was mostly (over)done by 35, although I was essentially homeless then because of it. (80’s recession was nastier than people think, things just suddenly changed). No more really easy to find 40 hrs at a a buck or two above minimum wage….fewer small companies, no more living in a van on city streets and not being harassed. I’m sure people at that age still live 4 to a home, 2-3 to an apt.

Most of my spending now (besides unavoidable rentier stuff) is at the last owner owned coffee shop in the area, and I will not ever use auto checkout or online shopping. If you don’t need much, you don’t have to worry about “good prices” as much, so pay up and tip well.

Good article….so when arrives the recession? The train wreck or cancer choice still seems possible for a while…..and cancer lets more get theirs and get out, but to exactly where is a mystery to me.

NBay,I experienced the 80’s and saw the same(reagan looting social security/medicare and wasting it all on drug wars(phony and real) and give aways to MIC). Whining Millennials have no idea how good they have it

In terms of grains — they’re not included in the data. In terms of farms getting in trouble and not buying equipment and other goods they use in their operations and households, that would be included.

How about BDI?

Cass mentions monitoring expenditures and volumes in a sentence. Are they two different things?

Also Jan 1990 is used as the base for the index as 1.0, and there are data points at or under that, not sure why.

I guess one thing I’m also trying to I’m trying to get at is how much is people buying less, and how much are the folks in the shipping biz taking it in the shorts (like most everyone else nowadays), and is it even a meaningful part of the index.

If this isn’t an easy explain, please forget it, I don’t speak biz lingo well at all.

“Cass mentions monitoring expenditures and volumes in a sentence. Are they two different things?”

Yes. This is measured from the shippers point of view, when the shipment goes out: volume is the combined stuff they ship to their customers; expenditures are the dollars shippers pay the trucking companies, railroads, etc. for the getting the stuff to the destination.

If you want to learn about about what 2020 looks like. Watch the FTR update webcast. They do a decent job. It is free and they don’t spam the heck out of you for consulting business. I am in no way affiliated with them and do not use their consulting business. I use them as a free service to better understand what is going on.

https://freight.ftrintel.com/webinars

Great info here…it seems facts and logic as put forth in this article do not matter anymore to the financial world at large…until they do….who knows when that day will arrive? After the election? Or, possibly before? Who will not have a chair when the music stops.

Tribacria, “when the music stops” oh boy, I hate to think what would happen over if a Greek-style recession comes on.

I don’t hear any music ! just that crash noise ..gonna be a hard rest of January the way those charts look.

here in Arizona – all companies sell in december to reduce inventory

since come jan 1 – state levies INVENTORY TAX after $60,000 deduction in value

so come january – they all restock

Joe, how new is that law? If it was there in 2018 it wouldn’t affect year-over-year comparisons, unless a lot more businesses moved to Arizona compared to years prior.

So if you have to buy a new car do it in Dec?

I was in Tucson off and on ’07-’14 and full time ’09-’10.

Is that $995 “Desert Package” on everything worth it or just dealer BS?

The economy no longer factors into stock market valuations, market index etf’s now act as a (somewhat) stable currency where one can store wealth. Investment income (yield) is no longer a thing, that concept belongs to the old times, Bernanke decided income from investments were no longer a valid concept so he eliminated yield from the investment equation.

One of the functions of a currency is to be a store of wealth. Now that the government and the central bank have pivoted to an official policy of currency debasement the US$ no longer serves this function so people with savings seek out other forms of currency (gold, bitcoin, equity index funds) that cannot be created by fiat. Equity etf’s are very liquid and can be exchanged for other currencies without a commission.

Stock etf’s are going up in value relative to fiat currencies because they are not being debased to pay for government deficit spending. If your stock etf currency gains value due to corporate profits, well that’s just gravy.

Bitcoin and gold don’t need to create profits to have value and neither does SPY or DIA as long as they are supply constrained.

Van down….

Jeezzzz!!

Do I have to take all that into consideration when I go the grocery store to buy a quart of milk?????

I still use the “green stuff”; looks like paper, feels like paper and it’s……

And still save change in old jam jars……..

So far so good…(89)……

As public companies disappear into PE or merger land (and they do continue to) one could also make a case they are becoming rare, like PMs, only much more liquid. Good luck.

Admire the van thing, I lived in a Ford bread van for 4 years, 72-76, but everyone left me completely alone back then, even on a main street. Just ran a cord to friend’s rental houses, used bathroom, and paid $25 mo, moved it around mostly to not tick friends off, never a cop problem. Drove a beater car. Don’t know how you pull it off today.

Wolf, its really no use to keep harping on all these bad news (in your last few articles) to attempt to “talk the market down”, regardless of how rational or substantive they seem.

I’ve always said the market is a BEAST that does not follow logic at all, so my advice to you is to swallow your pride and cut your losses on your SPY ‘big short” because the technical behavior looks to be hitting new highs every other day/week.

I’ll admit I traded against you and have closed out my short-term SPY long calls yesterday for a profit (so I can talk about it now). It wasn’t intentional to rub it in, but I figured if your short attempt made it into broad news online, the market will tend to do exactly the opposite of your broadcasted intent. From experience, I can say that once I close out my bullish positions above, the market will often go even higher, but I’m content to take a good short-term profit and then wait for the next pivot to show itself.

However, I have to warn you (half-jokingly) that there is a tendency for the markets to immediately turn your way AFTER you take your loss; but if you don’t, then it will tend to continue rising and make your losses progressively larger and increase your mental torture.

Unfortunately, this is a common frustration with the Beast, and I suspect AI algos are also now watching every move to extract their pound of flesh.

If a potential WW3 with Iran cannot derail this market, then this bull still has some strength, but you can never tell when it turns or even WHY. Sometimes, a ridiculous non-event (like maybe Trump tweeting that he is having a toothache) may start the crash. lol.

I’d like to tell you “I told you so”, but really… if you just go back to some of my previous comments weeks, if not months back, I did say that this market will potentially “melt up”… up to a point when all the FOMOs capitulate and get on board, and then it will crash hard to wipe out all the retail investors.

Again, if the FOMOs don’t join this party, then this market will continue to ride higher for months or even years…NO ONE individual will know the exact timing of the top because its behavior will change according to what most everyone does in order to extract the maximum pain from 90% of market participants. It always does and always will :-)

PS: A good short-term tactic to manage risks now maybe to GLSSLVWSLA1SD, but I won’t say what this is coded for, until AFTER I’m done using this particular trade based on current market conditions :) Good Luck Wolf, you;ll need it.

Kevin,

“…to attempt to “talk the market down”

Hahahaha, thanks for assuming that my site is big enough to talk the world’s largest market down. Not happening. And so I’m not even trying. Just looking at economic and financial stuff.

As you know, I’ve been pointing out forever that retail is strong (including in this article) and that services are strong — often in the same article about manufacturing and transportation, which are weak. So you think I’m trying to talk the market up in one paragraph only to talk it down in another paragraph. GET REAL!

Looking at the Cass Index freight chart it does not look bad to me. 2019 is worse than 2018, that is clear, but 2019 is better than all of the other years except for one point where it drops below 2011 and a couple points where it drops below 2014.

Am I missing something here?

Yes, you’re missing it totally. If that’s what you’re seeing, you’re not looking at the “Cass Index freight chart” if that means the “Shipment” chart. Look at the second chart from the top. Each line represents one year. The chart goes back to 2011. The fat red line is 2019. Dec 2019 is below Dec 2011.

I am looking at the chart “Cass Freight Index – shipping volume by truck, rail, barge and air”. After re-reading your post I see that you are specifically focusing on December 2019 and previous Decembers. You picked the worst month for the comparison and maybe that is valid. We will have to see how the 1st 6 months of 2020 turn out. At that point we should know if this is a real downward trend in shipping volume.

Sure, it’s for December. This whole article is about December. I wrote about November a month ago. And I wrote about October two months ago, etc. I cover this data when it’s current every month. So maybe it’s the first time you have seen my coverage of this data, and you missed the prior months, but you can go back a long time and find the others (look for the mid-month dates):

https://wolfstreet.com/category/all/transportation/

Ah I see. Yes you are correct, I’m new to the site and I like it.

Wolf, my real name is Kevin, not “Kent” (that Real enough for you? lol)

Anyways, us talking about the markets here certainly does nothing consequential; my point is most folks with an open position tends to lean into biased viewpoints (consciously or unconsciously, but mostly unconsciously) because they need the psychological salve.

That’s why I said if you want to trade, its best you don’t talk about your trades… because talking will influence yourself more so than any market movements, and often lead you to do stupid things like holding on to a losing trade for too long.

Believe me or not, I learnt this the hard way from personal experience, and I dare say the lesson for me is well worth it in the long run. I thought you too have learnt it, after admitting that “you got your face ripped off” in your last big short years back, but apparently I was wrong.

If I were in your “big short” position now, I’d take the loss quickly and keep the bulk of my resources ready for the real opportunities.

If you loose too much now, you’re not going to have enough later on to move the needle.

Right now, the only ones who can “talk up or down the markets” is the FED and Trump; and you’re on the wrong side of both.

You may have courage to make a public stand on your beliefs about the market, but it takes more courage to nail your Ego to the wall and admit you are wrong and take a small loss before it balloons.

I liked your articles so I’m quite ambivalent whether you want to take my sincere advice or not.

The longer I delve int the markets, the more I think every person just have to learn it the “hard way” for their lessons to really stick, so whatever I say may be all drivel anyway; and perhaps that’s why every generation have to make the same avoidable mistakes and go through the same market cycles of euphoria and despair, because every new and cocky generation never wants to learn from the mistakes of others.

Take it however you want it, but still, I wish you well Wolf. You are one of the few saner voices in an insane world.

Kevin,

Apologizes for screwing up your name. Fixed.

Yes, Wolfs call was not the best, I dont know why he shorted the market but I will give him credit for taking a public stand. Markets go up and down so its hard to predict them, and if it goes your way, usually its because you got lucky and not some genius insights you have.

Wolf is more sophisticated than this, but I agree that the tendency recently has been into the negative side reporting.

Memento mori,

I am short the market but I am also longer stocks than i am short the market. Will you give me credit too please ?

You have to risk it to win, and as long as decisions are made rationally within their current context, you shouldn’t say oh I should have known the future if you end up being wrong. Besides, what’s wrong with holding a short position for six months? Margin interest isn’t that ridiculously high and who calls tops perfectly anyway. Come back in June.

rhodium,

Thanks for coming to my defense :-]

Some technical things: There is no margin interest. I sold short and received cash from that sale. That cash is sitting in my account. It’s not leveraged. I also have additional cash in the account to absorb any losses if I have to buy back the shares (using the cash proceeds from the short-sale plus some cash to cover any losses).

IMHO shorting Tesla shares is nuts, and I said this many times, including in the article of my short and explained the reasons, but shorting an index when you’re sitting on liquidity is just the opposite of buying it long. If you make 2%, I lose 2%. And the other way around.

He shorted the market what, a week ago? Typical impatience.

I guess there’s some bad financial news that the markets would respond to if not for the permanent flood of FED liquidity eliminating price discovery.

Just returning from a business trip through several northeast states along I95 corridor. The highways are overflowing with large 18wheeler trucks…. but the traffic is so bad that they don’t get anywhere during daytime hours. The middle of the night is the only time they can (often, not always) reach highway speeds, assuming no accidents which is far from a given at 3am.

Truck rest areas are full, as those bankrupt states attempt to extort revenue from truckers “driving” too many hours. So truckers park and sleep from 6am to 11am, drive slowly a few hours to the next stop, then rest from 3pm until 9pm… when they go out and try to make up lost driving time.

Truckers always were away from family for days at a time, but now they are forced into nocturnal driving times, passenger cars driven by “persons returning from the bar”, and police that need to issue tickets to fund their state budgets. Drunk drivers have incarceration costs and they vomit on police. Truckers are sober and pay fines… so guess who the police try to ticket.

Anyone who thinks this doesn’t get reflected in intangible shipping costs is mad. Trucking companies have a tough time raising shipping prices, so the costs appear other ways (work slowdowns, fewer drivers available, strict self enforcing limits to driving hours, etc).

Amazon has a certain sweat shop like reputation in the warehouses, and amazon prime trucks are reportedly similar working conditions. Wonder how long before amazon truckers unionize, or there is a major accident?

The economy is having trouble in some areas / sectors, booming in others… but trucking problems in northeast states is about neglected 3rd world highway conditions and state police struggling to shore up budgets.

Truck drivers in the northeast are struggling to deliver 1st world shipping on neglected 3rd world roads.

PS — there is a train bridge in lower CT that opens by itself at random times. It was neglected for decades, and the last guy that knew how to repair it is in his 90s and lives somewhere in Pittsburgh PA. Connecticut has been unwilling to fund repairs for decades, despite very high taxes — so now the state is cobbling together on and off funding to prepare the bridge for replacement… replacement was scheduled to happen in 2016, but CT is essentially bankrupt so it couldn’t get matching federal funds.

So freight train service to northeast has the same neglected infrastructure problems as the I95 highway.

Given the weird hour, I made my company pay for car service to the airport. The driver was quite frustrated by road conditions. Connecticut has some of the highest taxes in the country, but has spent its way into bankruptcy. I just arrived at JFK airport in the heart of New York City, it is a 3rd world disaster zone and has been for decades.

Meanwhile, Connecticut muni bond holders think they are going to get paid… HA HA HA HA

New York and New Jersey are not any different. Neglected roads, neglected train tracks, already very high taxes. California and Illinois finances make the news now and again. Prosperous state governments that should be rolling in money have diverted funds away from basic maintenance for decades.

The credit problems with shale oil is well known. The next credit problem that will “surprise” Wall Street are muni bonds.

I wonder what the Red States will do when the “bankrupt” New England Blue states stop sending so much money to DC. Currently, the Blue States send more to Washington than they get back. Texas is the only Red State that is not on the dole to the Blue States. This is not due to any prudent financial policies. Texas literally pumps money out of the ground. Take this away, and it will be standing in line with the rest of the Red States, waiting for its handout.

Roddy … I think your beliefs about how much money northeast states pay/receive is out of date or just wrong.

In CT, 9 out of the 10 largest employers in the state are tax exempt. The 10th is united technology which is soon to merge with Raytheon and leave. GE left a year ago. GE made news, but others like Praxair, Aetna and several Pharmaceuticals fled also. CT chased jobs and corporate taxes away, and then penalized the individuals who stayed with ever higher taxes to support a bloated non profit sector.

CT’s biggest employers are the state, the federal government, and several university systems. CT is home to the coast guard academy and the largest submarine base in the world, and it has a very large FBI office. If you think the federal government isn’t sending money to CT, your info is not just out of date, it’s just wrong.

Yale university receives hundreds of millions in student loan subsidies from the federal government. Billions in federal research grant money. They are the largest land holder in the city of new haven, and they don’t pay a penny in property taxes — so private property owners get over taxed to make up the shortfall. That has nothing to do with the federal government at all, its just Yale being greedy and selfish.

NY state used to have lots of manufacturing upstate. The Hudson valley area was home to paper mills and towns full of high precision metal and machine fabrication, etc. they are all gone, and their tax revenue with them. Rochester was home to Eastman Kodak and owned cameras and film the way Detroit used to own the car market — and Kodak invented digital camera technology.

NY state gave billionaire Elon musk $700 million in subsidies to build a battery plant outside Buffalo (a plant that sits idle according to 60 minutes). While giving political favored Tesla $700 million, they raised taxes on small businesses. That was Albany, and has nothing to do with federal government money at all.

Very little industry exists in NY outside of New York City, which is buried beneath a welfare welfare system. Wall Street pays 70% of NYC taxes and more than 50% of NY state taxes… according to presidential candidate Bloomberg.

Every time you read someone on this blog complaining about the Fed subsidizing big banks and investment firms… that means they are subsidizing NYC. That is trillions of dollars in federal money flooding into NYC.

Please do a little fact checking before you comment next time. I am not as familiar with NJ and perhaps they get less money from DC… but holy smokes are you wrong about NY and CT

Here’s one take on the relative outflow/inflow of federal tax revenue by state as of 2017:

https://www.theatlantic.com/business/archive/2014/05/which-states-are-givers-and-which-are-takers/361668/

Truck guy — does that article account for indirect federal subsidies like the Fed pouring trillions into NYC banks? And the effect that money has on IPO issuance in Silicon Valley?

The Atlantic has a very left leaning political agenda, and it is picking and choosing what taxes and subsidies it counts toward its partisan conclusions.

The concentration of money center banks in NYC means trillions in federal reserve subsidies. A concentration of big universities, as in Boston and San Francisco, means billions in loan subsidies and research grants. as just one example, Google was born from a DARPA grant.

Any “study” that does not include these federal monies is misleading and wrong.

Whether a state is a net tax “payer” or subsidy “receiver” depends a lot on how inflated the state has gotten by the Fed and bankers. The blue states are the most heavily cost-inflated, high cost-of-living states. The red states have been resistant to financial inflation and have lower costs of living (yet frequently higher quality of life). In the high-cost blue states, workers have to be paid more (otherwise no one could afford to live there), so more workers wind up in higher tax brackets. The “payer” vs. “receiver” thing may have as much to do with tax-bracket creep as economic strength or policy choices.

Yak- Corporations crush small business like bugs, even without offshoring. There is one owner operated coffee shop in our area and easily 40-50 Starbucks and Peets. My friends and I go to that one shop as do others who feel the same, it’s a 10 mi drive one way for me, and I can see a Starbucks from my apt.

All your verbal tap dancing doesn’t change this simple fact.

Corporations are practically sovereign facist regimes allowed to soak up all the benefits of being in this country. They can even be “people” legally if that suits their immediate agenda. To call them a “business” is a very bad joke.

Very true and these facts are evident in the exodus from these disaster areas I lived in NY my whole life and left in 2015 after 51 years of getting screwed

I’m originally from upstate NY… my family has moved away, but every time I visit places from my childhood it makes me want to cry.

Great businesses, great jobs, and “five” seasons if you count lake effect snow.

All destroyed by greed and corruption in Albany

Yak now,

If you look at the link truckguy gave, it might not show what you assume it might regarding NY and CT. IMO, it may only be helpful for a handful of dramatic standouts, which are not the states you talk about (NY & CT).

Note: the Fed payment of interest is only in the ball park of $50 billion now? And the 2008 bailout was…in 2008.

IMO, much of the loss of business you talk about, is more a part of the Federal Government long established policy of moving business out of American and into lower paying nations – offshoring.

Wolf is my vote for the primary cause of this – he discussed a year or so ago, our Federal tax policy aggressively promoting this offshoring of job, which IMO is what caused the decimation in upstate NT and other areas, like CT, you talk about.

And yes, state subsidies to gigantic corporations are bad.

I looked at the two top states in the Atlantic article and knew it was completely wrong. Virginia should be number one in net federal money by miles. Norfolk, pentagon, several bases… plus the HQ of all the big military contractors. Then the telecom industry and related subsidies in Richmond. And then consulting / service groups like Booz Hamilton, McKinsey, Deloitte and can’t omit the biggie SIAC. The Atlantic didn’t do their homework.

Maryland is second. Annapolis, more military bases, numerous agencies from housing to homeland security… and the rest of the big military contractor HQ. And the bedroom communities of millions of federal bureaucrats who are paid by the federal government and pay taxes in VA or Maryland. Johns Hopkins and the NIH collect billions in federal research grants. The Atlantic screwed up,

NY should be number three based on Federal reserve money to big banks. A lot of bankers make their homes in northern NJ and CT.

Ruddy made a really bad comment and I called him on it. Truck guy then added a link that is straight misinformation.

And neither of their comments explained the trucking / freight problems in the northeast… which i tried to explain are more the result of neglected 3rd world roads and rail lines. The national economy might be doing many things, but the shipping problems in the northeast are not about economic activity.

The mass exodus of people from those states, both residents and corporations (aka jobs, aka corporate tax base) are not somebody else’s fault. The states did it to themselves.

It is not offshoring or federal taxes or the boogey man. It’s really greedy and corrupt state governments, and their public unions who get full pensions after 20 years (private sector workers have to work about 45 years — age 20 to 65)

Yak now:

“The mass exodus of people from those states, both residents and corporations (aka jobs, aka corporate tax base) are not somebody else’s fault. The states did it to themselves. It is not offshoring or federal taxes or the boogey man.”

The long established bipartisan Federal policy of offshoring jobs and corporations is of fantastically massive impact, not to compared to ghosts, goblins, or Lord Voldermort. It is HUGE and it is REALITY, and IMO completely dwarfs what state and local governments do.

In others, don’t agree with you on dismissing it as the number 1 driver of loss of jobs and corporate exit.

Timber — NY state levied higher taxes on small businesses, while giving $700 million to Tesla… who made big donations to the governor’s campaign fund (lobbying is just legalized bribery) . Imagine if NY state used that $700 million to subsidize small business. Less bribe money for the governor, but a broader tax base for NY and better economic conditions for voters. It’s a state choice to screw small business and reward big companies that can pay big bribes.

CT has a law to tax global income of corporations headquartered there, not just income from CT. Corporations left. Yale pays nothing and gets massive subsidies both from the state and from the federal government… ergo the top employers in CT are now all tax exempt entities. CT hollowed out its own tax base.

Federal tax code to offshore manufacturing effects all states. It is CT, NY, IL and CA state policy to tax and harass small business while subsidizing political contributors.

And these same states are bankrupt because they attack their own tax base. It is not lack of net federal transfers that overwhelmingly favor VA, Maryland, NY and CA.

I’m not disagreeing with your offshoring issue. I’m saying the neglected 3rd world roads and rail lines in the northeast are that way because of those state’s own policies

I wonder if migration of retired people from blue states when they work (and pay for social security and medicare) to red states when they retire (were they receive social security and medicare) is distorting these numbers. It would be interesting to see what the numbers look like excluding these(since in some ways this is just the government paying back a loan as far as I understand) or make a correction for this type of migration. Also QE and artificially low interest rates(which is a form of tax subsidy) probably dis proportionally helps blue states. Additionally the low interest rates are gonna lower fixed income revenue of retirees. If we assume red states have a higher fraction of people earning fixed income, this would also lower revenue generated by these states(I have no clue if this is true).

It’s well known that mostly wealthy blue states pay more in taxes on the federal level and that mostly red states with lower incomes are net receivers of federal tax revenue.

At the state finance level, red states are by and large running state finances better, with a few exceptions in either direction.

The reason that upstate NY, CT, and IL are emptying out has nothing to do with federal policies that encourage outsourcing to other countries. Texas, Nevada, Florida Tennessee, and other low-tax states are growing rapidly, with very few exceptions.

High tax states are growing slowly or shrinking, with very few exceptions. People are voting with their feet. CT, NJ, and IL are headed toward smaller population and bond default. Upstate NY is shrinking. NYC and CA are spared only because they are world HQ for finance and entertainment and tech, and NYC is shrinking this year and CA has had net negative migration of US citizens for many years.

Most of this movement of people away from these states is probably for job opportunities, some is for weather, lower cost of living, less crowded life, but there is also a very conscious movement of people with significant wealth and assets away from places that confiscate these assets with higher taxes, or will confiscate them eventually because state level finances are in deficit, and state level governments keep adding or protecting costly entitlement and pension costs. I predict that this will accelerate in the coming decades.

IL is the poster child for this trend, but NJ and CT are very close behind. The other side is TX, FL, TN, and the rest of the interior west and Sunbelt to a lesser degree. Anyone with wealth who lives in IL is looking for an out.

can the fed buy municipal bonds?

From this small business owner a great big THANK YOU!

yes preacher as it turns out they do, along w/baseball cards, pretty rocks, shiny turds and rings that pinch your finger when you make a fist.

CT just changed its estate tax to match the Fed exemptions after 2023. Meantime they are increasing the exemptions starting this year. Unlike NY and NJ, we realized we needed to keep the rich. Didn’t Tom Brady just move to Greenwich, or is that fake news?

Glad to hear Tom Brady is helping CT by moving there. Meanwhile, from Hartford Courant:

Connecticut lost $16.33 billion in annual federally adjusted gross income between 1992 and 2016

And from Bloomberg, 2018 numbers:

Connecticut lost the equivalent of 1.6% of its annual adjusted gross income, as the people who moved out of the Constitution State had an average income of $122,000, which was 26% higher than those migrating in

People who pay the taxes are fleeing and people who don’t pay the taxes are replacing them. And overall, the state is shrinking. How does this not end in bankruptcy?

Won’t this lead to a race to the bottom in the tri-state area. I wonder if market forces will lead to smaller state government. Seems like the wealthy don’t need to live in highly taxed states and since they make up such a huge fraction of tax revenue, they have a ton of leverage.

Do you wonder why subcompacts are not selling, while trucks and SUVs are? One pothole can destroy a small lightweight car. The 16 inch rim is almost standard. This is also why mountain bikes are popular for street cycling. Even hybrids come with extra heavy weight wheels.

The Blue states that you complain about receive less money from the Federal government than they pay in, while the Red states receive more money from the Federal government than they pay in:

https://wallethub.com/edu/states-most-least-dependent-on-the-federal-government/2700/

So of course they need higher taxes in order to pay their bills. The Trump tax reform bill has made this situation even worse.

It should also be mentioned that, even within states, Blue urban areas pay more money into state government than they get back, while Red rural areas pay less money into state government than they get back. So liberal urban areas are subsidizing conservative rural areas even within states. This partially explains why many cities also have higher taxes and experience difficulties in paying their bills.

That’s the article referenced in the Atlantic article I linked to a few dozen posts above. One poster claimed it didn’t take federal employee salaries into account, even though it does. Also, I was hoping that poster would include data supporting his assertion military bases are skewing the results.

Nah, Truck-He just pointed out how he had called out one guy for posting false information and said your link was just misinformation. Took a lot of words to do all that, too.

Shipping companies should get into the business of moving banknotes across the world and make sure electronic transactions no longer work (promise politicians and bankers their cut and they will quickly agree). In that case there will be plenty of business ;)

Railroad coal shipping volumes are way down due to switching to other fuels.

As oil pipelines are completed there is less need to haul oil by rail car.

More efficient shipping algorithms, artificial intelligence and distribution centers reduce deadhead empty space trucking haulage.

The Panama Canal was widened doubling capacity. It allowed larger container ships from Asia to reach Houston and the East Coast US ports. Shipping by boat is cheaper than by rail or truck from LA/Long Beach.

The service sector is showing strong growth in spite of a US mfg. slump.

I guess the trucking and shipping industry is suffering from that massive “wide spread labor shortage” the Fed just told us about in our economy, in it’s latest economic report. That’s why our wages are rising so fast. For example our wages where I work are rising so fast I can’t see them rising, at a whole 0%! After all, we have the lowest unemployment rate since millions of years. Haven’t you all noticed?

Yup wages were rising so fast in 2015 that I just decided to forget it and retire (sarc off)

Wages for many government workers in Netherlands increase by 10% or more within 1-2 years; but because these are government workers, it has almost zero effect on shipping volume (besides, much of the extra money has to be spent on surging rents, healthcare, tuition etc. costs).

I’m pretty sure the same is happening in many EU countries, especially in the south – governments are partying with the cheaper than free money (thank you very much, ECB and EU savers!!).

But…but…healthcare cost aren’t inflation – they are increases in GDP!

So are increases in car insurance. And home owners insurance. And healthcare insurance. And real estate taxes. If any of those go up, our services are getting better and we’re getting more of them. The Fed itself has told us this to be true, so it is true.

That’s why the Fed is so smart and everything is awesome and we all getting better served and richer and wealthier and happier all the time!

Remember, here in the U.S. there is no inflation. Just like their is no unemployment and a labor shortage causing wages to be surging!

And if you’re not working and not accepting all those high paying job offers you are getting due to the “wide spread labor shortage”, the Fed won’t count you as unemployed because you’re lazy and choose not to work and besides that movie you sold on ebay last month means you’re self employed anyways.

So to recapitulate Fed World:

1). There is no inflation. Assets are going up because they are undervalued.

2). There is no unemployment. There is a widespread labor shortage.

3). If we die sooner, it just proves GDP is rising and we’re living better because we’re wealthier.

Hey….who did you vote for last election 2016? The guy who wants to give all your work and effort to the rich corporations advising him, or the Gal who wants to give all your work and effort to the rich corporations advising her?

Your comment was a great start to my day, along with a freshly pulled double shot espresso!

Yep, the three fastest inflating areas of healthcare, education, and new home building, have ALL been INFLATING AT 5-10% per year for decades bow.

Together, they make up over 30% of the GDP!

But they sure don’t make up 30% of the “basket of goods” used to calculate the CPI

So when healthcare and education and home building costs are ALL INFLATING AWAY at 5-10% per year, this counts towards a BOOMING ECONOMY AND GDP GROWTH! And does not count towards INFLATION.

GDP is booming!

Inflation is low!

Everything is awesome!

Everything is awesome!

Everything is awesome!

Everything is cool when you’re part of a team!

Everything is awesome!

When you’re living out a dream!

The Gal wouldn’t post her Shakespearean $275K speeches, so the losers there were the literary bunch. The guy’s rally goers get to yell and scream like they are at a football game, so they did a little better. No idea what the corporates think, and I imagine they prefer it that way.

Ha! I like this game…

Our wages have gone up so much that our landlord noticed and demanded a piece of the pie through raising our rents! Yay, money for everyone!

#thatsnothappening

#wellrentISgoingup

#andhealthcare #stillgotstudentloanstoo

The reason is simple. the economy is in recession. As prof Krugman likes to say , “my spending is your income and your spending is my income.” trucks are not going to deliver anything that is not produced. the Trump trade was successful…in depressing the economy.

From this story and the on-going manufacturing decline, you would think the predictors would be predicting recession. Au Contrare: I saw an interview with Steve Hanke, Professor of Applied Economics, Johns Hopkins University, who says that the annualized growth of the US money supply in the last quarter was over 7% and for December was over 11%. His perspective is that a recession is highly unlikely with the money supply growing so fast and that higher inflation is just around the corner if these numbers continue at this rate. We’ll see!

I doubt we will ever see higher inflation numbers, but inflation in hedonics and other statistical trickery is a sure thing …

Services (70%) of the economy are doing well so far. As I pointed out elsewhere in this thread, finance and insurance services alone are about 20% of the economy, and that sector is rocking and rolling. Healthcare, second largest services segment, is growing and now accounts for about 10% of the economy. Then there are IT and information services, and lawyering, etc. and they’re all growing.

The last time we had a recession, it was financial services that imploded and dragged the overall economy into deep trouble.

“Healthcare, second largest services segment, is growing and now accounts for about 10% of the economy.”

At the expense of a majority of the population. This right here is the problem.

Yes, and topic of many articles here :-]

The economy has moved to a situation where financialization is a big fraction of all activity- also known as “service industries”. So, the GDP, job markets, etc., look OK because of service industry activity.

I think the “real economy”/manufacturing/tangible goods (transportation/shipping) suffer from a couple of things. 1. see above- the economy can’t/won’t support new tangible capital equipment (business investment for these items has been weak for years- see stock buybacks, lack of opportunity perceived in the old/industrial economy, etc.) – people aren’t buying as many houses, cars, etc. per capita. 2. miniaturization- a lot of the tangible goods we buy, e.g. electronics are smaller- tv, phone, etc.

So, volumes (and weights) of transported goods have been in a secular downtrend for 10-20 years.

I doubt shipping of privately purchased tangible goods like like small electronics (2) is relevant in the big picture of the international economy. Besides, most people make up for this by buying many times more of such stuff then 10 or 20 years ago (sometimes out of necessity because of continually declining quality/lifetime).

Which makes me wonder, how would the recent refusal of China (especially) to accept the waste of the developed world influence shipping statistics? The garbage that is supposed to be “recycled” is piling up all over Europe (and Africa, for the really nasty stuff).

The small items are only a part of it.

Housing starts per capita in the US are about half of what they were 60 years ago. That’s a lot of lumber, wire, roofing, etc. not being shipped. There is a similar story with vehicles (the largest user of carpeting and glass).

You don’t get more tangible goods (especially capital/durable goods) in the type of economy (financialized/low interest rate distorted) that we have today.

Housing is a big part indeed. But while housing starts may be half the number, maybe the homes are bigger nowadays?

In my country new homes are at least 4-5x the size of 60 years ago, measured in m2 per person; although lately the size per person is going down a bit due to staggering price increases. And the number of households keeps increasing (over here mainly due to more singles, and all the youngsters migrating from Africa/Asia who instantly get a free new home).

I think we have more tangible goods relative to what the number should be because production is pulled forward by ZIRP/NIRP policy. But for capital goods I agree, why bother producing something of value when you can make far more money buying back your own stock …

Dow is going to 30k soon, don’t short this market, the Fed is unhinged, unless some people in Congress start making noises about what the Fed is doing, which I don’t expect, this thing is going higher.

There are no flies on you !

What’s more, the Shiller P/E is only 31, which is low when compared with the dot com peak Shiller P/E of almost 45… and to think that the S&P 500 has almost doubled in value since then.

It is worth noting that we do not YET have widespread middle class participation (let alone speculation) in real estate buying or the stock market. Are you reading this Jeremy Grantham ?

Interestingly, one of my residential tenants remarked to me last October in a very upbeat way about the performance in her 401k.

So maybe we will have more grass roots participation in equities ?

All is very good. But be careful, Tesla stock collapsed almost 3% earlier this a.m.

So clutch onto your t-bills and popcorn…. if that’s the kind of thing that blows your wee skirt up.

akiddy111,

“…the Shiller P/E is only 31, which is low when compared with the dot com peak Shiller P/E of almost 45…”

Good lordy, so much uninformed nonsense to support your theories. It was during the dotcom BUST and during the FINANCIAL CRISIS, not before, that the S&P 500 PE ratio spiked into the stratosphere. You know why? Because companies were reporting HUGE losses, which makes index PE ratios spike despite collapsing share prices. Look at the DATES when the PE ratios began spiking!

Another great reason to avoid including loss-making enterprises in P/E ratios for major indices! /sarc

Top 10% of the population in the US holds 85% of the stock market.

I am not convinced that a high stock market is doing anything for the majority of the people.

https://ritholtz.com/wp-content/uploads/2019/12/image001-3.png

You are right!

The bottom 90% hold around 10% of the mkt.

The financialization, buy-back shares have helped the mkt indexes to keep going up along with ultra accommodating Fed!

The service economy is flourishing but manufacturing/productive is limping south!

The HIGH mkt doing zilch for the bottom 90% but when tht mkt they are the ones who will hurt most, in the down cycles!

In Netherlands at least the average citizen is all in for the housing market; even some people on social security are buying homes with a 102% mortgage, and youngsters living with their parents are “saving” for their first home by speculating in REITs. Everyone who can get a home loan has one or has recently refinanced at near-zero rate. And most of the boomers with money to spare are buying investment homes hand over fist. Even foreign speculators are joining the party, which is was unusual for most of the Dutch housing market until a few years ago. The TV has advertisements for native and foreign REITs (both commercial and private homes) every day.

For stocks our news media keeps trying to funnel everyone into stocks with upbeat stories and scary warnings about the coming negative rates, but I don’t think that is working well. Most of the people with significant money have been burned before (most EU stock indexes still below their 2000 top), and the younger ones with less money seem to be more into Bitcoin and other sure things ;)

If it’s “so ugly” why is the stock market breaking records?

Lack of inflation is primary cause of all of this.

Freight shipments are not a reliable trading indicator either.

If you shorted the stock market trying to play this, like Wolf did at beginning of the year …..

you are staring at very large losses.

Animal spirits TRUMP economic forecasts every time.

lack of inflation for those who live in the parallel universe of the MSM and survive by “financing” everything instead of paying for it. Or maybe for the elites, though their inflation numbers are really high if you look what they are spending their money on ;)

It cannot continue and it will not; but I learned years ago already not to step in front of the central bank steamroller ;)

“Animal Spirits”…….didn’t that one miss “the list”.

I’ve always gotten a kick out of it…..so inspiring!

How’s inventory?

I just went to Walmart, Costco and Staples. the other day. Shelves are full. How did it get there. UPS is so busy, I still have to see my regular delivery guy. They and USPS have people delivering 2-3 times a day instead of once.

I am beginning to suspect either the numbers are not measuring everything or the economy just went downhill.

Just ordered 35lb of cat litter, WMT, free shipping AND they offered a dollar off if I would wait until the 21st for delivery. I took it, they are delivering today.

Walmart in TPA bay area last Friday had some stuff, but many items missing that spouse and I have purchased there previously… NOT, to be sure like the one in central southern middle Tennessee that was pretty much bare shelves regularly from Sunday night until midday Tuesday. Hence, Walmart world not a good indicator of anything IMHO; very different situations, and besides those, we have likely been in a couple dozen while traveling across our beautiful USA six times round trip since spring of 16 with similar spectrum of results.

But otherwise enjoy many of your insights i-fan

As the owner of a trucking company it is slow here and rates are low for loads going cross country, I looks for more carriers going bankrupt this year.

I have always heard that trucking was the barometer for a upcoming recession but the last few transportation recessions the rest of the economy seemed to do just fine.

R.W.

Your observation about a transportation recession not leading to an overall recession is correct. Here is why: Services are 70% of the economy. Finance and insurance services alone are about 20% of the economy, and that sector is rocking and rolling. Healthcare, the second largest services segment, is growing too, now about 10% of the economy. Then there are IT and information services, and lawyering, etc. and they’re all growing. The last time we had a recession, it was financial services that imploded and dragged the overall economy into deep trouble.

Wolf.. Good article.

Since the phase 1 trade deal was signed yesterday everything will now be great and best ever.

Problem have all been resolved.

LOL LOL LOL

It was all due to perfect conversation and negotiating.

Few people on this planet possess such skill, you can count them on one hand…..maybe less.

Why is this happening?

The Real Economy never recovered from the recession that began in 2007. It’s just limped along well enough on skyrocketing federal debt to make it look good.

The Financial Economy not only recovered but has been fully enabled to exploit the Real Economy with new and improved extraction mechanisms like the Medical Industrial Complex and the Education Industrial Complex.

From 2000 to 2001, the Federal Reserve, in a move to protect the economy from the overvalued stock market, made successive interest rate increases. It doesn’t do that anymore because it would disappoint the Financial Industrial Complex and make ambitious politicians look bad.

The Japanese recession which began in the 1990s never ended and never will, but will continue to limp along until the status loses its quo.

It could easily be argued that the 2000-2001 recession that began with the bursting of the Dot Com bubble never really ended for similar reasons, but that is another story and shall be told another time.

It just might amuse you to realize the actual numbers, not percentages, of the dollar value of the assets that rich folks own graphed against the publicly acknowledged inflation rate. It’s close to hilarious, and should generate at least some appreciation of the FED as the servant of the oligarchy.

And that would be the why,,, the basic foundational why of why our money keeps getting more worthless, even as shown by the official BLS inflation calculator.

An other major why would be the close relationship between the folks manipulating the so called financial economy and their paid puppets in the political arena obeying their masters to pass legislation to legalize bribery, corruption, et cetera ad infinitum…

Pretty much agree with most of your post to which this is A reply.

1980 is my favorite start point for the endpoint.

BTW, when are you going to cop to having a cold fusion machine?

Ecommerce should drive industry inventory reductions without reductions in industry revenue since inventory stocking becomes centralized further vs. brick and mortar.

At least for the retail dimension of the transports volume this could be a significant factor.

Another is moving of production out of China and to say Mexico reduces in transit overseas volume and inventory movmentment/management volumes from Port hubs.

I look at those charts I see FED stuffing the money channel leading into a recession. They put another 75B in today, half of it MBS. One thing Fed has achieved since it opened REPO is putting a cap on longer term rates. There is no historical correlation between the economy and interest rates. Some analysts are saying it’s time to short the bond indexes. Banks and Fed are at odds over this, yield curve and all. Here, take this money and buy some stock you’ll feel better.

Primary Dealers & Directs have to pay the Treasury 49.22B today for auctions they bought earlier. Repo overnight matured 47.5B. Term rep 27.668B matured.

Tomorrow, 50B term repo matures plus the overnight today 39.35B.

Where’s the money coming from? Of course the Fed.

rail and trucking stocks bottomed awhile back. this is all lagging information. irrelevant for the most part.

Right now, for the stock market, reality is irrelevant. Look at Tesla. But for reality, reality is not irrelevant :-]

Related, took a quick look at the Dow Transportation Average to see how it aligns with this data. The Transport stocks index is up about 16% since the first week of October. Exemplifies the significant divergences and low overall correlation between the real economy and the stock market these days.

The government passed a 100 billion stimulus for 2020………the china deal will add 100 billion of stimulus in purchased goods………the new nafta will add 20 billion or so……..trade deals with South Korea and Japan will add another 20 billion or so……..dollar appears to be weakening……….demographics have bottomed………election year spending……….

The market is a joke just like 1929 and 2000 but expecting a recession…….no……..

Bulls end one of two ways……a jolt or a recession. #2 is out……..#1…….not to be seen……..and it never is.

Does not the chart mostly show the last two years to be an aberration?

The charts show a boom in late 2017 and most of 2018. And then the boom fell apart. Now sipments have fallen below 2011 levels. That wasn’t two years ago. That was 8 years ago.

9 years ago now Wolf,,, welcome to the 3rd decade of the 21st.

So in January 2020, would you say that January 2019 was “2 years ago?”

Maybe it’s just semantics here :-]

1) AMZN disrupt the DJT.

2) AMZN shipping in Xmas are done by vans, from warehouses in/near major cities, to their end customers.

3) Election year 2020 , the invisible war chest will plunge : Deposit with F.R banks UST, general acc down from $400B to $367B, on the way perhaps to $(-) 500B, to avoid headaches.

4) The DOW today went too far, thanks to Visa @ 201.50, MSFT @ 165.26, with plenty selling tails, BA.

I have a theory. Because of the tariff war the USA has been converting from international length supply chains to domestic length supply chains; from international labor pools to domestic labor pools. Labor shortage seems to have developed – more jobs AND higher wages. Instead of China/Asia delivering goods to the west coast forcing a distribution throughout the USA, more ideally situated domestic producers are handling delivery of goods which I infer means fewer delivery miles.

PS

I would assume going from international to domestic would mean fewer middlemen. This would mean less shipping between middlemen and perhaps even subdued inflation?

Gotta agree with the RR here,,, and the way i am seeing the shift as a construction estimator is the growth in interest in facilities likely optimum for light assembly/manufacture/warehouse functions in the commercial arena, even in CA, but especially in the low tax states mentioned in this article.

Hope SO, because i get really tired of having to ”vet out” the SO many products that appear to satisfy my needed/wanted “stuff” as to if actually made in USA, or just ”designed” ”engineered” etc., in USA and made elsewhere…

ICYMI, sooner or later the rich folks owning all the global transportation modalities and the only ones really profiting in dollar denominated gains, , will understand how they have screwed themselves by not insisting global trade MUST go ”on top” of local manufacturing, etc.,,, and then only when local cannot produce enough to satisfy local demand.

I know of a duck call factory that fits that theory well.

Cass Freight data looks like it’s all over the place.

https://fred.stlouisfed.org/graph/fredgraph.png?g=pW4a

In my opinion, we really should look at inventory to sales ratios.

https://fred.stlouisfed.org/graph/fredgraph.png?g=pW4t

We just are too inventoried right now. That’s why reordering is slow.

Iamafan,

No, it’s not “all over the place.” You just missed how seasonal transportation is, and then chose the worst possible chart format to show it.

As I have pointed out many times, there are very strong seasonal patterns in transportation (like retail and some other things). That’s why the format of the chart you linked is utterly useless. And that is PRECISELY why:

1. I use a YOY chart which shows the comparison to the same month in the prior year, which eliminates seasonality,

2. In addition, I use a stacked chart going back many years, which shows the seasonality, and then it shows the movements BEYOND the seasonality so that we can see what is going on.

Your second linked chart is the manufacturers’ inventory to sales ratio: it tells you neither the sales data nor the inventory data, but only the ratio between them; but the ratio can go up for two opposite reasons:

1. because sales are rising more slowly than inventories are rising;

2. because sales are falling faster than inventories are falling;

In other words, the ratio itself is useless unless you also look at the sales and inventory figures to know what’s going on.

And the chart you linked only covers 1/3 of total business inventories. The other two-thirds are retail and wholesales.

So the manufacturing inventory-to-sales ratio serves only a very limited purpose and by itself is NOT indicative of any broader moves.

I was only interested in the inventory for resale, since 70% of the real economy was consumption. I already assumed that manufacturing was weak.

I grant the mathematical fact that either the numerator or denominator can change. But we probably already assumed that retail sales were up meaning sales were up. If the ratio of inventory to sales is up, given sales is up, then I can assume inventory was way up.

I am not sure how to explain the very weak transportation numbers, when other sectors still look ok.

Iamafan ,

You’re correct at pointing inventories as one of the factors in this transportation drama because they have ballooned during the tariff front-running. In total, there are now about $2 trillion in business inventories in the US.

The issue is particularly problematic with durable goods inventories in the entire chain. The ratio is secondary. The primary issue is the dollar level of inventories in the entire chain. The ratio will only tell you if growing sales justify these high inventories of if they don’t. And as you suggested, now they don’t.

The Shiller P/E averaged 43 in Q4 1999. Earnings were growing, not declining in Q4 1999.

Multpl.com is one of several resources i can point to to support that, but the above factoid is generally known by historically informed and experienced people that have, both, lived through and followed such stuff.

BS. On a monthly basis, it peaked in March 2002 at 46.71. In 1999, the highest point was in April 1999 at 34.0

During the Financial Crisis, it peaked in May 2009 123.7. In September 2008, just before Lehman it was at 26.8

So yes, check out the numbers at the source you cited:

https://www.multpl.com/s-p-500-pe-ratio/table/by-month

Thank for the link and the info!

John Hussman has his own ‘modified’ Shiller PE ratio but no data chart similar to the one in the above link.

Btw; this mkt is again reminder to those of us in the mkt for a long time ( Been in the mkt since ’82) that

MARKET can be irrational more than one can remain SOLVENT!

I have been whip lashed more times than I can remember since March ’09. It is very difficult to over come ‘irrationality & illogical’ thoughts when my brain has conditioned for rational thinking towards the mkt, before 2009!

Besides, the SHOCKS’ I went thru!

-I failed to appreciate the effect of low, prolonged rate along with QEs 123 and now QE4 on asset prices!

– The Fed had NEVER bought the MBSs in it’s history before!

– Effect of suspension of Mkt to Mkt accounting standard

Never lost my shirt and have enough, not to worry my livelihood! I still believe in the ‘REVERSION to the mean in the END, after all the kicking the can by vested interests!

it’s difficult to win a game when your competitor keeps changing the rules … the best strategy in such cases is not to play but even that has a high cost.

Sunny129:

“Effect of suspension of Mkt to Mkt accounting standard”

That was HUGE!

Looking back u can see at that advent the market began it’s climb from (DJ) approx 6,000 to what it is today. It never looked back.

Return MtoM true values and look out below!!

Wolf,

akiddy111 spoke of the Shiller P/E, but the specific data series you linked to is the regular S&P 500 P/E ratio.

(I don’t know whether akiddy111’s figures are correct. But I believe the difference in the two calculations is that the Shiller P/E uses a trailing 10-year average P/E ratio of the S&P 500, with inflation adjustment, rather than just the trailing 12 months with no inflation adjustment.)

Yes, we addressed that a little further down.

The new AMZN teleporter is making a dent.

Are Amazon shipping numbers private ? Do they hit the Cass freight numbers? How are they invoiced if they are in-house?

These Cass numbers are based on what shippers ship and how much they pay for it — no matter how it gets there or on what platform the item was sold.

Phase I was signed.

Phase II ==> a change of character.

The DOW may have reached its peak this week.

The freight volume chart shows clearly that the period from Dec 2017 to May 2019 was a huge outlier. That makes for tough year-to-year comparisons.

December 2019 might have just been a return to normal. Other than 2017 & 2018, all the December data cluster within 2-3% of the 1.05 level.

And November 2019 was solid compared to anything other than November 2018.

Wolf,

If you read my comment you would have seen that i was referring to the Shiller P/E or also known as the cyclically adjusted price-to-earnings ratio, Or CAPE for short, or some might know it as the P/E 10.

I have worked really hard educating myself over the last 23 years on as much as i can on all things Global Macro Finance to write uninformed nonsense and BS.

https://www.multpl.com/shiller-pe/table/by-month (refer to Q4 1999)

Respectfully.

OK, I didn’t see that, but had I seen it I would have jumped all over you even more because…

You shouldn’t even cite the Shiller P/E ratio to support your timing purposes because it’s earnings portion is not a measure of current earnings. Its earnings portion is based on average inflation-adjusted earnings from the previous 10 years, not the current year or the current quarter.

Akiddy, others here appreciate your comments (in full detail) even if Wolf himself is sometimes reading a bit too quickly to appreciate the nuances. ;)

I don’t see where he got all lathered up about market timing. Your original comment was just that the S&P500 is currently not as massively overpriced yet as it was in 1999. (But on the Schiller PE, market is currently more overpriced than in 2007-2008 … and has been since late 2016.)

Personally your comment triggered a useful thought: I’d love to see a historical chart of the aggregate debt / earnings of the S&P500 along with the P/E ratio. Charts of debt/EBITDA are common but not looking at the true picture. However, since a handful of companies have a lot of net cash (negative debt), the median might be more useful than the average?

Debt/Equity and Debt/Assets aren’t too extreme yet but that could just be due to the equity bubble. What matters is debt-servicing capacity (especially under stress during next recession)… that’s hard to tease out without a lot of digging?

That being said – do you guys know Warren Buffett’s favourite measure of the stock market?

The Total market cap of the stock market dividend by the GNP for the US.

Have a look here but hold your nose and hold onto your hat before you do, because it’s the highest it has ever been. Uh, ever.

https://www.gurufocus.com/stock-market-valuations.php

Also if you analyse Berkshire Buffets is actually like 50% invested in cash with his massive $130bn cash pile!

I’m going to repeat the most important thing from comments early this morning, because shipping isn’t just about financing terms.

Many places in the USA that represent most of the USA’s economic activity have collapsing roads, railways and airports.

The federal reserve can print currency, but they can’t print good roads.

After your eco friendly car hits a nice pothole, no amount of free credit will fix a flat tire or bottomed out transmission. You won’t buy goods or services, you will sit at home unable to get anywhere. Your mechanic won’t get to you, and he won’t have parts even if he did.

The USA had good roads and railways for years, and people took transportation for granted. Decades of financialization has made people forget that amazon prime can’t deliver if the road is out. The drone delivery service is about amazon trying to work around 3rd world roads and 3rd world traffic jams.

I appreciate Wolf’s blog, but I think his finance focus has made him miss the big picture. Bad roads cannot be fixed by the Fed altering credit terms. Period. No buts.

‘The federal reserve can print currency, but they can’t print good roads’

Mkts are levitated by dominant ‘financialization of our Economy at to the cost productive (manufacturing) segment care little for the ‘deteriorating infra structure’

No good earnings are necessary when ‘buy-back’ can be substituted!

There is no equity market when the price discovery is actively suppressed by Fed. We just have CASINOS where betting is game and nothing else!

Whether your stock portfolio incurs unrealized gains, and whether you can pay your rent/mortgage are two different questions.

Wolf’s home town San Francisco has unbelievable IPO wealth, and they have some of the worst homelessness problems in the country.

This weeks JPMorgan health stocks conference in SF was a mess because of homelessness and related crime. Two massive doctor conferences that were held in SF for years moved to another city because of the decrepit conditions. And Oracle, which lists SF as it’s home town, just announced future oracle world conferences will be in Las Vegas, not SF.

None of those decisions to flee SF were based on stock market levels. They were based on SF policy that harasses tax payers and rewards law breakers. Stock market doesn’t matter.

Homelessness and related crime – yes.

But what THAT, has to do with deteriorating infrastructures just NOT in SF but in whole of USA including all major metros. ?

‘Whether your stock portfolio incurs unrealized gains, and whether you can pay your rent/mortgage are two different questions.

If one is putting the needed ‘ the living expenses + emergency funds'( minimum up to 3 yrs) foolishly into Equity investments, not surprisingly, s/he is playing ‘Las Vegas’

Again nothing to do with ‘ bad roads/bridges ++

As one of the ones who almost broken the law by becoming homeless, I have to say that San Francisco’s failure, and the rest of the Bay Area as well to addressing the unaffordable housing is a problem. Then add San Francisco’s refusal to install public restrooms because of cost is another problem. The more venture capitalists flock to the Bay Area the worse it becomes for most of us living here.

I think I’ve wasted too much time already explaining the obvious to you sunny129. You are either too dumb or you are just choosing not to see what is in front of you.

Failed infrastructure is the problem. Stock prices, at any level, don’t fix infrastructure. Fed funds rate, at any level, won’t fix infrastructure.

@YakNow – I did a lot of driving around various parts of the USA this year, and I did not see infrastructure being notably worse than any other time in the past 25 years. This includes state-level and local roads as well as Interstates.

Traffic is cyclical and we’re near the peak of a long boom, so yeah, traffic could be on the bad side.

But other than heavy traffic during rush hours, I have had no unusual trouble driving around Boston, New York (City & State), CA, Arizona, you name it. One local road that developed a bad case of potholes within 10 miles of my home had them fixed within a few months, which isn’t bad for a government bureaucracy.

Trucking congestion may have been an issue in 2018 through mid-2019, and it does tear up the roads more than usual, but as you can see from Wolf’s charts, they’ve been fixing that ;)

Like any industry dependent on the government, there is an infrastructure-industrial complex with incentives to sell the “decaying infrastructure” meme. But I haven’t seen hard data to believe it. I could easily believe “maldistribution of infrastructure” – areas of neglect – but that’s not the same thing as “national emergency”.

Now, given the high demand for road usage in some parts of the country, there’s also an argument for either improving the infrastructure to meet the demand and deliver economic growth, or rearranging the demand to make better use of existing infrastructure. California is a poster child for stupidity in this area because cities are incentivized to “build jobs, not housing”, forcing long commutes which waste resources and road space.

Taxes and short term thinking. I do not think anyone forgot. I think it has to do with getting elected. The reason why the necessary maintenance, repairs, and expansion of the infrastructure has been deferred is because it cost ***money*** and at the state and municipal levels require taxes. Politicians have for decades shorted infrastructure to avoid any tax increases, or have shuffled off the funds to some other pet projects, or just pocketed the money.

This started as least as early as the 1980s. So I do not think that financiallization has anything to with it. Unless a connection could be made with the fantasy worlds of modern finance and modern state and municipal budgeting.

Sorry. Respectfully disagree.

Productive ( organically based) Economy – manufacturing -needs better infra structures but increasing financialization by Wall ST/ Banks aided by Fed, at a cost to remainder including productive economy, doesn’t care. Besides our Multi-nationals shipped (gave away) our factories and jobs to overseas including China since 2000.

Maximizing the profits at any cost, aka animal spirits supported Fed’s policies. In Fixing the roads (infra structures) there is NO immediate PAY-BACK in contrast to ‘toll roads or bridges’ which produce revenue.

Govt is spending Trillions in ME wars, going no where, but no money for fixing our roads which were built in 50s, just like most our bridges and railway lines!I

It is a horrendous public policy failures. Shockingly there is no outrage by the public or the MSM!

Jbird… the decline started long before the 1980s. It started when FDR convinced Americans to put their future in the hands of big bureaucracy instead of their own friends and family.

The depression was caused (in the 1920s) by the federal reserve boosting the money supply irresponsibly. The federal government caused the Great Depression.

And in fairness to comrade FDR, it was Woodrow Wilson who convinced America to meddle in foreign wars … ignoring the advice George Washington gave , and presidents followed until Wilson. Federal income taxes and federal reserve were made necessary to pay for all the “free stuff”

Yak, I rate Wilson as worst president for all the reasons you state. The WWI thing has always been downplayed by most other raters / historians.

FDR convinced Americans to do what you describe because a) They had just lost all their jobs and accumulated savings, and b) “friends and family” are irrelevant if all of said friends and family are also out of work and destitute.

Classic!

Much better than all the beating around the bush you did in your comments far above. If that isn’t laying out a black and white agenda clearly, I certainly don’t know what is.

No grey areas exist in your mind, that’s for sure.

Back in 1999 and 2008 Buffett held huge sums of cash and was getting screamed at by his holders due to his relative poor returns. He claimed that he never invested in anything he could not understand and avoided tech due to this posture.

A few years later everybody was scared when rates were near 1 or 2 percent and he was lending that stash of cash to GE money at 10% and receiving warrants equal to 10% of the company.

Right now the old man is holding tons of cash…….claiming he’d like to invest but everything is expensive……while his eyes twinkle.

In 2015-16, I count 19 consecutive red bars.

Today is only 13 bars. 6 more red bars to go.

I don’t remember losing my shirt in 15-16′.