Fueled by cheap money and by dashed hopes of high oil prices.

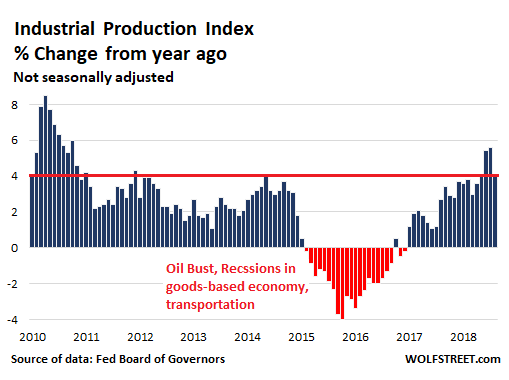

Industrial production in October rose 4.1% from a year ago, the Fed Board of Governors reported this morning. This was in the upper portion of the range since 2010. It was powered in part by the blistering oil & gas production boom that followed the Oil Bust of 2015 and 2016.

This chart shows the percent change in industrial production from the same month a year earlier. The red bars – industrial production falling year-over-year – coincide with the recession in the goods-based economy, the transportation recession, and the Oil Bust:

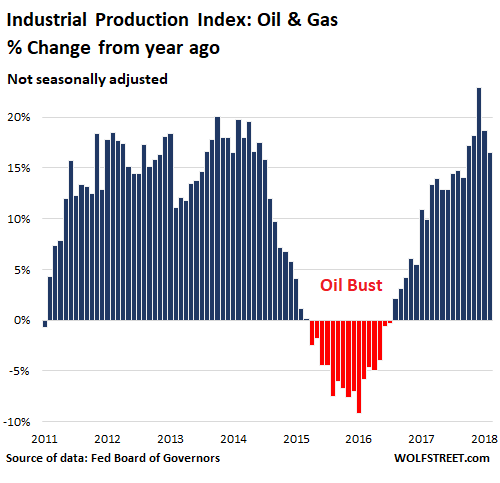

As part of the overall index, manufacturing rose 2.7% from a year ago, utilities 1.7%, and mining, which includes oil & gas extraction, jumped 13.1%. Oil & gas extraction on its own soared 16.5% from a year ago.

On a monthly basis oil & gas extraction edged down a smidgen over the past two months from a spikey record in August, when it had soared 22.9% year-over-year.

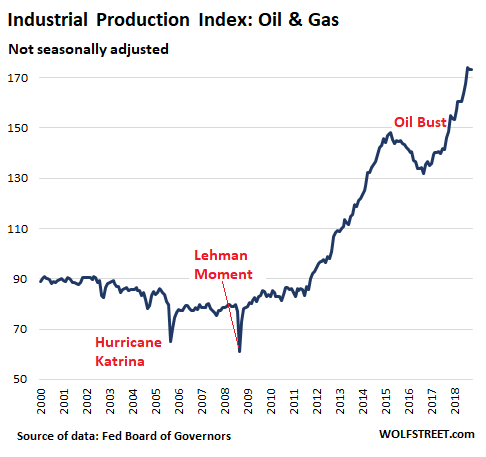

The chart below shows the Industrial Production sub-index for crude oil and natural gas extraction. Note the brief effects of Hurricane Katrina when production along the Gulf Coast was shut down, the Financial Crisis when everything came to a standstill, the subsequent fracking boom, the oil bust in 2015 and 2016, and then the renewed boom. Since the trough of the oil bust in September 2016, the index has surged 31.5%:

It has been a wild ride in the oil & gas sector. At the end of 2008 – following the Lehman Moment – everything came to a halt for a couple of months, but then activity rebounded. Starting in 2011, the fracking boom, fueled by waves of new money trying to find a place to go, took off. At the time, oil prices (WTI) ranged from $75 to $113 a barrel. But in July 2014, oil prices began to dive, and in 2015, the oil bust hit production. At the end of 2016, the oil and gas boom took off again. This chart shows the year-over-year percentage change. Note the 22.9% spike in August:

The oil and gas boom is economically important not only in the oil patch but in the broader US economy, with high-paying jobs in the oil field, transportation, manufacturing, specialized services, and high-tech. An oil boom requires equipment of all kinds; it fires up manufacturing; pipelines have to be built; all this equipment has to be transported, triggering a transportation boom, and the like. It usually leads to a construction boom as well, with all the secondary effects.

The US has been the largest natural gas producer in the world for several years. In August 2018, at least for that month, the US became the largest crude oil producer in the world. For better or worse, this sector has become a powerful player in the US economy. It’s fueled by cheap money and by hopes of high oil prices. Alas, the cheap money is evaporating, and hopes of high oil prices have taken a serious beating in November. Boom and bust, always. Hence the old rule in the business: Never drill with your own money.

Mortgage rates are climbing faster than the 10-year Treasury yield. Read… Mortgage Rates May Hit 6% Sooner, as Fed Sheds Mortgage-Backed Securities, But What Will that Do to Housing Bubble 2?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I guess we are oversupplied at present, hence the drop in prices. Now that the high yield market is backing up it should put a floor under prices but investors are still throwing money at frackkers (Wolf). Perhaps the inflation argument is gaining traction, even if the cost of Turkey dinner this year is at new lows.

Not only an oversupply situation in North America.

The oil supply glut is global, as OPEC (Saudi Arabia) has called for the cartel members to restrict the supply by lowering production quotas.

Add in the gloomy fundamentals of a slowing global economy and the down trending of oil use. Just not using as much.

Now you have a perfect recipe for an oil sector bust.

Much lower oil prices to come before supply/demand is balanced.

This is just the beginning of a new deeper, global recession.

->Fueled by cheap money and by dashed hopes of high oil prices.

By now it should be obvious that the ‘scarce capital’ paradigm is bogus. There’s so much of it around there’s no longer any good places to invest it. Making it cheaper does nothing to solve that problem, but it can make it a lot worse by incentivizing even more misallocation.

And it’s amazing how expensive that cheap credit can get when there are so many splendid ways to waste it.

Capital availability is always purely a function of market confidence. And the market has been very confident for many, many years now.

Scarce labor and wages are my real worries.

->Capital availability is always purely a function of market confidence.

So rising interest rates are no problem. Same with taxing those with more money than they know what to do with. Glad to hear it.

->Scarce labor and wages are my real worries.

Only dirt-cheap labor is scarce, mostly where variations on the 13th amendment can be enforced. Where labor can be abusively exploited you can get it by the boatload.

After all, profit maximization requires that workers are never to be allowed to benefit from their own labor, so there’s no point paying anybody anything that can’t be re-extracted immediately.

Rising interest rates do little to offset confidence as long as rate policy isn’t lucy, charlie brown and a football.

Trust has and always will move coin to the most productive faster. It is a frustrating fact for those who desire to be the overlords of wealth redistribution, so the nonviolent ones develop schemes insidious enough to make even the robber barons blush.

Unamused, you tend to present “moral” considerations. Capitalism disregards morals, aside for the moral of allowing “invisible hands” to deal the cards.

Oil Bust 2.0 incoming?

With oil-services companies approaching financial crisis lows I think it may be time to invest in the larger oil services companies such as Schlumberger (SLB) and HAL. Since these guys don’t actually sell the oil, (only find it and drill it), I think they would be the best to profit from the next ‘boom’ turn around.

The only question is how low can these guys go?

Slb and hal would do well (not spectacular) if the boom continues, theoretically. But they do not really “find” or drill. They mostly just provide services to the well operators. If oil markets continue to fall they will keep going lower.

You could even say this is a big frackling problem.

Undulating Plateau, or boom bust cycle (take your pick). There is a saying that indicates this quite well, “Most oil companies cannot afford to produce oil below $70.00 per barrel and Society aka ‘consumers’ cannot afford to pay for oil (or products) at $70.00 per barrel”. As this big drop settles in many oil companies will try to make up for their losses with as much volume as they can pump, until……. creditors turn off the money tap. Shale is particularly vulnerable as a well pumps out about 70% in just the first year of production. Production costs are mostly in so operators get out as much as they can as fast as they can with a surge in fracking and even faster development to the detriment of total well output.

The old joke of making up for losses with volume doesn’t work with Shale.

Our industrial society ballooned when oil was $5.00 per barrel. Some conventional producers are profitable at $20.00 per barrel and industrial society still does okay, wages just turn stagnant. Expensive oil (unaffordable energy) has been held at bay for the last 15 years with credit and debt. Shale companies have not made money at any price; even $100 per barrel. Their end is nigh.

Oil Sands will keep producing as they are long long term production vehicles and development costs are mostly in before any production even happens. Think of a 50 year timeline for a plant. Companies like Suncor are still making money at these low rates. The big factor is that once an Oil Sands plant is in operation it costs more to shut them down and keep them shut down than it does to just keep producing. They’ll keep producing, but new major projects might go on ‘hold’ for awhile. My son works there going flat out and turns down overtime every shift, even in this market.

regards

for better or worse oil has become the dominanat producer in usa blah blha? lol ..come on…oil OIL IS THE DOMINANT $$$ producer above and beyond ANYTHING you can name! any sector any time frame for the past ..since at least, AT LEAST ww2, maybe space and nuclear can be more per capita but over the long term OIL is IT…everyone ..including me, just forgot…maybe this is the last gasp? i mean the us via exxon rex tillerson mibil just bought into 20% of roszneft/russian oil…!

hahaha and also cocaine…but i admit, its fun as hell batting around this shit on our level…wht else we gonna do?

How big part does a global slowdown have in the oversupply of oil ? As the wheels of the economy slows down, the demand for oil is reduced.

Take the auto industry for an example globally. Chinese autosales do decline, not because of the much prpagated “trade war”, but because consumers are maxed out and rising interest rates. What is the situation with declining auto sales in the US etc ? The Germans do feel the bite, too.

Housing in the US is starting to feel the heat of rising interest rates already at these laughable low levels. What if rates were to reach sane levels ….

Realist,

I just read this while having a coffee break. From Gail Tyveberg’s blog of a week ago:

“One point of confusion regarding whether today’s oil prices should be of concern is the fact that the maximum affordable oil price seems to decline over time. This happens because workers around the world increasingly cannot afford to buy the goods and services that the world economy produces. Inadequate wage growth within countries, growing globalization and rising interest rates all contribute to this growing affordability problem. To make matters confusing, this growing affordability problem corresponds to “falling demand” in the way economists frame the issues we are facing.

If we believe the technical analysis shown in Figure 2, the maximum affordable West Texas Intermediate oil price has declined from $147 per barrel in July 2008 to $76 per barrel recently. The current price is about $62 per barrel. The chart suggests that downward price resistance might be reached at $55 per barrel, assuming no major event occurs to change the current trend line. Any upward price bounce would appear to leave the price still much lower than oil producers need in order to reinvest sufficiently to allow future oil production to be maintained at current levels.

Thus, our concern about adequate future oil supplies should perhaps be focused on keeping oil prices high enough. It takes a growing debt bubble to keep oil demand high; perhaps our concern should be keeping this debt bubble high enough to allow extraction of commodities of all kinds, including oil. Figure 1 seems to show a recent downward trend in Debt to GDP ratios for the Eurozone, the United States and China. This may be part of today’s low price problem for commodities of all types.”

Is there any sign that the fracking companies are finding capital harder to come by? Still seems to be full steam ahead in the Permian particularly.

What’s the thinking of the financiers paying for all this? They surely would not be ignorant of the fact that the companies they fund are losing money. Do they all hope they can be first to the exit and protect their capital? Otherwise what is the game? It seems rather risky to me and I’m puzzled it has gone on so long. If it were me, I’d be standing well clear.

All Western governments are stockpiling oil reserves due to WW3 central planning. Goldman was openly stockpiling at least three years ago telegraphing down-the-road markets to Trade Wars & Hot War preparation.

Pre-Second World War they were likely stockpiling everything under the sun including crude. Do we have shipping stats from pre-WW2 and onwards?

MOU