The inflection point: sellers got the memo and cut prices.

The area of Silicon Valley and San Francisco – comprised of the counties of San Francisco, San Mateo, and Santa Clara – is one of the most expensive housing markets in the US. Atherton, a town in the heart of Silicon Valley, has been named the single most expensive zip code in the US. And when that housing market gets tough, the tough start cutting prices.

And that’s what’s happening.

Sales have slowed. Buyers have lost their enthusiasm, and they’re taking their time. Mortgage interest rates have surged, making home purchases even more expensive. And everyone has figured that the situation on the ground has been a housing bubble accompanied by a tech and social media bubble peppered with all kinds of other specialty bubbles, such as the various “sharing” bubbles, and that they won’t last.

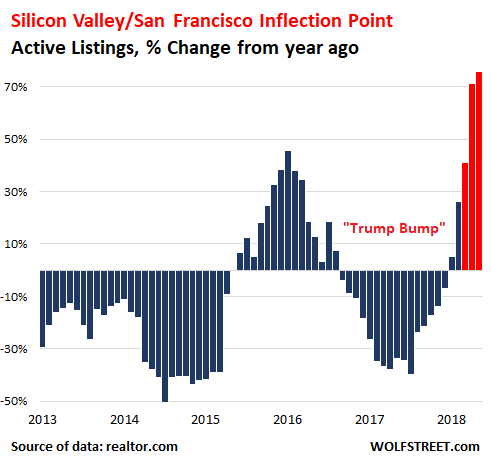

So it’s time to unload. Sellers are putting their homes on the market, and active listings in those three counties combined – San Francisco, San Mateo, and Santa Clara, which cover the area from San Jose to San Francisco – surged by 76% in October compared to October last year, to 4,149 listings, according to the National Association of Realtors.

The red bars in the chart mark the inflection point for this housing market. Note the “Trump Bump” — the phenomenon that caused the already teetering housing bubble in the Bay Area to become re-energized after the election in 2016, with listings drying up and prices surging one more time. But that is over now (data via realtor.com).

Suddenly, there is plenty of inventory on the market. This follows the well-established pattern: there is a perceived and much hyped “housing shortage” during boom times, but when the market slows, suddenly, all kinds of inventory comes out of the woodwork. In other words, eager sellers show up, and that’s good. Having eager sellers is one half of the market. Now if there just were eager buyers.

Despite the surge in inventories, sales across the Bay Area declined by 3% compared to the already low levels last October. Back then, the low sales were blamed on lack of inventory, ironically, and sky-high prices not so ironically. Now there is plenty of inventory, but the median selling price has ticked up too, and sales have slowed further, as inventories are piling up.

What’s the next step? Cutting asking prices.

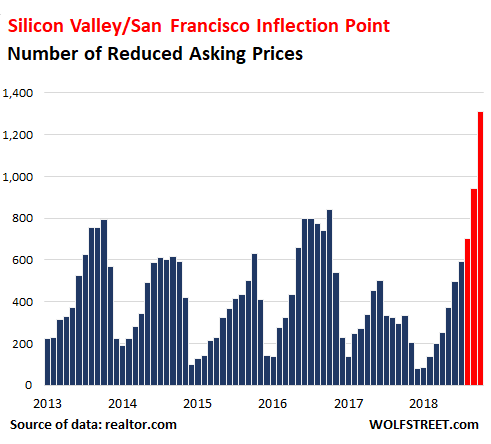

And so the price cutting has started. In the counties of San Francisco, San Mateo, and Santa Clara, the number of price reduction started seriously jumping in August, hit a post-housing-bust record in September, and blew through the roof in October, nearly quadrupling year-over-year to 1,312 properties with price reductions:

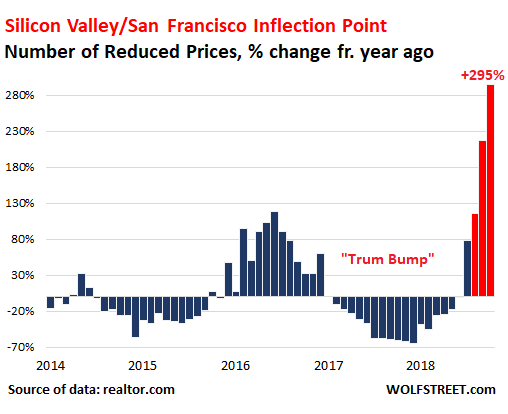

In percentage terms, this move becomes even clearer. In September, price cuts surged by 218% from September last year and in October by 295%. This is what an inflection point in one of the most overpriced housing markets in the US looks like – it’s when sellers begin to get the message:

Even as inventories pile up and sales slow down, the median price across the entire Bay Area rose 7.9%, according to the California Association of Realtors. But in Silicon Valley and San Francisco, the price increases are petering out.

In San Francisco, the median price of single-family houses rose just 0.4% year-over-year to $1.6 million and the median condo price rose 3.7% to $1.275 million. “Median” means that half of the homes sell for more and half sell for less. In San Mateo County, the median house price rose 4.3% to $1.588 million, and in Santa Clara County, it rose by 3.2% to $1.29 million.

Given these big prices, even a 10% cut in the asking price of the median home represents a $160,000 reduction in San Francisco and San Mateo and a $127,000 reduction in Santa Clara County. And this is just the beginning – the inflection point of a long slow process. Sellers are still lagging the market, and by the time they finally catch up with the market, the market will have moved lower.

Mortgage rates are climbing faster than the 10-year Treasury yield. Read… Mortgage Rates May Hit 6% Sooner, as Fed Sheds Mortgage-Backed Securities, But What Will that Do to Housing Bubble 2?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Rising interest rates

DJT new tax laws limiting mortgage interest deductions for $750,000+ mortgages and a $10,000 cap on property and state income taxes

The great QE unwind

And….

Mel Watt in forced retirement come Jan 2019

It is going to be et epic!

Does the cap on mortgage interest deductions apply to the whole loan? For example, if someone has an $800,000 mortgage, can they still deduct the interest on the first $750,000? And what happens when a 750+ mortgage is paid down into sub 750 territory? I’m just curious how this works.

If the home loan was secured before 12/15/17, your limit is $1,000,0000. If after 12/15/17, the limit is $750,000. For example, if you have a home loan secured in 2018 with an average principal balance of $800,000, then you can deduct 93.75% of the mortgage interest (750K/800K) paid in 2018.

This entitlement looks like the poor subsidizing the rich. Not limiting the mortgage deduction created a crazy incentive to malinvest capital. It would be fairer if the cap was made closer to the federal poverty level (FPL).

This country looks like the poor subsidizing the rich ….

fixed that for ya!

@Alex-

>This country looks like the poor subsidizing the rich…

Is it different anywhere else around the world?

Folks, if you have a brain in your head and have substantial equity, get out NOW, put the money in Treasuries, and rent an apartment if you want to stay in the Bay Area.

I know the Fed is still fighting the war of 1929, but the current collapse of the Ponzi will dwarf the Depression.

Remember people losing 600K, 800K in equity during the Bay Area housing collapse in 2009? Gonna go there again? Don’t. The Fed won’t dip a single toe in this disaster.

You are warned.

Housing is local, even within the Bay Area. I believe housing prices in places like Palo Alto and Cupertino were hardly impacted by the 2009 downturn, and have risen even more than their neighboring communities.

This is among the most pervasive pieces of misinformation that floats around. Maybe someone can find a link, but I’ve seen charts in the past (from Paragon?) showing >20% drop in Palo Alto et al.

Kevin is right. There is no “immune” area when there is a crash. However, more desired area may have smaller drop in price comparing to less desired area during a crash.

During the 2000-2003 downturn, houses in Palo Alto dropped maybe 10%. Houses in East Palo Alto dropped maybe 30-40%.

What’s the difference? First thing is that houses in a “good neighborhood” tend to be owned by people who want to live there, and who are unlikely to be forced to sell by a general reduction in rents.

Houses in a “bad neighborhood” contain a disproportionate number of renters and people who are just barely making the mortgage payment every month.

The pattern is that, during a boom, the less desirable areas increase in price much faster that the average, and during a bust they drop more.

Yes, it is very much true that these things are local.

If you want to look at average Silicon Valley housing, do not look at Atherton. Look at Sunnyvale or the City of Santa Clara.

Or the FED will just reduce interest rates back to zero and start the bubble all over again.

It seems this will extend to Seattle with the new Amazon HQs going east. They say the announcement is already affecting prices, downward in Seattle and upwards in NYC and Virginia.

I would say more than that.

The California Equity Locust (CEL) that has invaded and destroyed so many other states affordable housing for locals, is about to become an endangered species.

Well, some CELs do matastasize …

There is a project about six miles to the west from my hovel on Lake Michigan that is supposed to have 5000-15000 employees.

I have not seen any increase in RE sales in my area. I find it hard to believe that the crap wages paid by Amazon will do anything much to goose RE prices. AMZN has a 200,000 sq ft operation just twelve miles south of here that has most on food stamps to supplement the lousy pay.

Agreed – an average wage of $150K won’t go far in either DC or NYC. Will only pressure rents. Gawd, DC traffic and Metro congestion is bad enough now.

So does this mean Google will cut wages for new hires and freeze wage hikes for existing?

Sounds like my city or origin, Racine, or perhaps Kenosha? My best friend from H.S. who remained there has described effect of the construction on area roads. Now that the guy who pushed the giveaway, Mr. S.W. has been handed his discharge papers, who gets to clean up the financial mess? Ah of course, the Wisco citizen/taxpayers?

More “Making ‘Merica Grrreat Again!”

https://www.nationalreview.com/2018/07/wisconsin-foxconn-plant-bad-deal-for-taxpayers/

What a time to be alive. The conventional wisdom was housed never went down in price but now they can go up and down it seems willy-nilly at times but I was foolish to believe market incentives and supply/demand didn’t apply to real estate. Good thing I got out when to going was still good.

Conventional wisdom also assumed population growth. A bunch of small cities which are already declining will become ghost towns once their Boomers die/move and accompanying retirement capital inflows dry out.

Some of these small cities will be ripe for those Millennials who wish to go back to the Garden !

Detroit?

I was visiting a friend up in Northern NY, Western Mass area. I didn’t realize how many of these towns there were. A bunch of people living off the social security or pension checks from the factory that left 30 years ago. All the young people have either moved South or working in dead-end service jobs. Or on drugs.

The buyers have probably also got the memo and will be waiting for much more significant price reductions. Hence a long decline ahead

I’ve been sitting on the sidelines for two years as a first time home buyer. It’s funny because two years ago I thought prices were already getting crazy and this is in a so called more affordable city in a non coastal state. We’ve got an above average down payment saved up but home prices have grown way faster. Any suitable, affordable homes are gobbled up by investors with cash and flipped. They’ll redo the interior, add some square footage, and try to sell it for 35-45% more. First time buyers can’t compete. If it takes as long as previous cycles we’ll have to rent for another 2-3 years I fear before things get back to normal I hope. Thank the Fed for greasing the wheels …

“before things get back to normal I hope.”

Assuming the Fed will ever allow it.

“Thank the Fed for greasing the wheels …”

You will soon be able to thank them again as they will be at the ready to grease it again!

Grease it with what .. (P)ropietarily (I)ntegrated (G)rifter fat ??

Seriously understand your sentiment. Who knows…..

I’m not middle aged yet but getting close. All this accumulation of personal and public debt concerns me. Maybe I’m just too pessimistic, but I worry about the future generations having to somehow pay for all this. We keep kicking the can down the road….

Andy I’m in the same situation. I’m upset. I don’t believe the issue is that home prices have risen thus pricing us out of the market, it’s that the government’s money creation has devalued our savings thus destroying the fruit of our labor. This was done at our expense to save other people (took our money and gave to someone else). I got no answer other than to stay grateful for what I do have, be true to my values, and keep working hard which is what I’ve done since I was 15.

Don’t worry guys, its just the housing cycle taking the cue from the stock market. I mean 10% drop is not even “correction” territory, if you use the parlance of equities markets.

In comparison, the recent swoon of the stock market indices from their early 2018 peaks is at its worst, more than 10%. As we all know, many of the FANG stocks are facing far worse drop-offs since the beginning of this year.

People are prepped for a housing downturn this time around. There are lots of fore-warnings in the news and on various blogs (not least of which, including this one with WS).

Again, it boils down to counter-intuitive mass psychology…. when most people are already fore-warned and jittery, then there won’t be any housing crash like what we had back in 2008.

It is only when the herd is ALL stampeding in one direction, then will you get to the great crash.

The way I look at this current behavior is that a big enough proportion of home owners / investors are trying to get out quick, so these will become the “early” sellers without the finances nor holding power, and thus this will drain enough of the excess to stabilize prices once these “weak hands” are flushed out.

Most of all, people in the streets still REMEMBER the last great housing crash in 2008, so if they remember it, then there WON’T be another housing crash. Get it?

If the prices drop somewhat more, I’m buying in again.

I will only get worried when I see lots of people hustling to get in on the property ladder or eavesdrop on one too many street conversations about how so-and-so made a killing on their property portfolio. Then, I know the herd is all dancing to the same tune.

The only reason the market declines are small is that the algos have not been revised. They will be.

Ppp, I don’t see how algos are a factor in real estate transactions. As far as I’m aware, there are no algos doing competitive bidding against humans buying /selling houses in the real world.

If you’re referring to computer algos trading in the Reit ETFs, its influence would still be like pushing on a long string.

The well-developed algos don’t determine prices or set any actions based on fixed price targets. They take the cue mostly from the market pricing itself.

That is, people buying/selling at various prices will be the input parameter into those algos, so most algos are “trend followers” rather than trend-setters. They may accelerate a trend or aggravate the situation but they don’t start it unless its a programming bug that causes the equivalent of the human ‘”fat finger” effect.

In other words, for real estate, its still very much the human behavior that you have got to watch, and not algos on your computer screen.

I meant the stock market portion of his comment. I wonder how many stock algos are simply complete corruption, designed to STILL buy every dip, even tho this quarter was a disaster and every sign shows slowing. A realistic Dow is 6000–look what it was at close today. It is sickening. What a sick, doomed society this is!

Clearly remember reading comments like this in 2007 to an article by Rober Shiller. Since everyone knows it cant crash. Common assumption back then. Then year later someone added comment “What a difference a year brings”.

andy, a great many bears are wrong for almost 10 years now and counting.

You would have made a huge bundle by now, if you had ignored all those bearish predictions since April of 2009.

Having said that, the bears will get definitely it right…. eventually. The problem is you still missed out on all those years of growth :-)

Then, when the once-in-a-lifetime crash does come (say next year, according to your finely tuned crystal ball), do you have what it takes to short the market on its way down?

If you do not have the resources nor the wits to short it on the way down, then what makes you think you’d be ready to ride the next wave up?

And whats the point then if you are always hoping for the worst while the market is riding up and then when it does come crashing down, you’re also too afraid to catch the wave? That’s like an old grumpy intentionally being contrarian to the market to get his dose of Schadenfreude, but without making any real money in the process :-)

@kevin so what do you suggest for potential homebuyers? Just jump right in now? It’s ridiculous for someone to buy high now when they can buy low later. Not sure what you’re really arguing

https://fred.stlouisfed.org/graph/?g=m5To

If this doesn’t look like a bubble then what does?

And?

Whats your point Iamafan?

Thats a long-term chart and all long-term charts look pretty similar to this, given inflationary effects as well as increasing population over the last century.

If you believe the apocryphal story about the Dutch buying Manhattan island from the Indians for $24 in 1626, then how would you view real estate prices in the 1950s comparatively?

Wouldn’t that be an even bigger bubble and would you consider it safer to be sitting on the sidelines from 1950s on?

It’s all relative value and there is no definitive signpost that says a market is in bubble territory or is cheap, except on hindsight.

50 years ago, if your house is worth a half a million bucks, thats something to brag about, but now there are many worth more than a million dollars.

Likewise, look ahead 100 years later, if the median price of SFH were to be $5 million by then and you’re still alive, you would still be technically correct to say that it is in a gigantic bubble based on a long-term chart, but you’d be none the wiser…nor richer.

So the people who used HELOCs to buy stocks are getting a margin call?

Do people really do that? That’s deranged.

“People are prepped for a housing downturn this time around.”

What exactly is it that homeowners have done to be better prepared for another housing downturn? Save more? Borrow less? Start living within their means? Use interest rate hedges?

Several issues colliding here: QE reversal, interest rates up, housing prices too high, SALT deduction reduced, and probably the biggest: no more cash sales. Check this WSJ link that says cash sales are down across the whole US 70% after they started targeting them and have now been expanded and the threshold lowered.

https://www.wsj.com/articles/u-s-expands-coverage-of-real-estate-anti-money-laundering-program-1542322224

Thanks for that link. Fascinating. Just one clarification though, it’s shell company all-cash purchases that are down 70%, not all cash purchases in general.

Hallelujah

About time. I’m looking around dumbfounded here in Silicon Valley the last 5 years. Complete insanity in these prices. And a lot of the houses themselves are a joke.

And remember Wolf’s piece last month. As the tech equity deflates, so will the employee options. No one will have the $$$$ for these houses. It’s not just the mortgage rates.

It’s a big big bubble.

“In percentage terms, this move becomes even clearer. In September, price cuts surged by 218% from September last year and in October by 295%.”

By how much is an equally important data. Given the price appreciation a crash is the only way to get the prices to meaningful levels

“Sellers are still lagging the market, and by the time they finally catch up with the market, the market will have moved lower.”

I can think of 2 reasons why it takes a long time for a significant price drop to happen…

Sellers are strongly anchored to their prices

No seller wants to be the first to drop price significantly

If the Fed does not intervene, this can well turn out to be Housing Bust 2.0, given the bubble (which could not be spotted earlier has suddenly appeared like a rainbow) and go the Hemingway way – “slowly at first, then all of a sudden.”

But then, there is Fed waiting in the wings to meddle (read stop hiking) as usual, dropping hints (https://www.cnbc.com/2018/11/16/cnbc-exclusive-cnbc-transcript-us-federal-reserve-vice-chairman-richard-clarida-speaks-with-cnbcs-steve-liesman-today.html).

If the bust picks up speed you can bet your last dime Bullard and co will join the chorus and the chorus will get louder. Scoundrels doing god’s work!

No seller wants to be the first to drop price significantly

People often forget that it also costs money every month the property is sitting there and at some point those running costs will exceed the loss on the sale, which is still to come.

The only ways to get out “alive” from a property crash is either a) to get in front of the market fast, eat the loss, and sell or b) to have such an obscene mortgage that the lender will rather employ you as the live-in janitor in your own house so as to not recognise the loss, while you hopefully recover from your margin call.

Silicon Valley mortgages are non-recourse are they not?

That makes the whole situation …. more dynamic, I’d say.

“People often forget that it also costs money every month the property is sitting there and at some point those running costs will exceed the loss on the sale, which is still to come.”

I have always wonder about it. By waiting when prices are falling it is triple whammy-running cost during the period you did not sell, loss on the investment income that you could have made by taking an offer that is less than your anchor price and you might very well end up with a lower price. That is the way it is-psychology rather than logic at work.

Similar thing you can see in stocks-it may be wiser to sell at the beginning but somehow most people cannot come to do it immediately and then when they throw in the towel the loss is much more.

Probably got to do with the way we are wired.

“Sellers are strongly anchored to their prices

No seller wants to be the first to drop price significantly ”

since many tech companies don’t actually generate profit, their business model is predicated on an ever rising stock valuation. if their stock price crashes, they will immediately start downsizing. that will bring prices down very fast because most of those laid-off will only have enough money to pay their mortgage for a few months before going into default.

Is there any actual technological innovation happening in the Bay Area today? It seems more like just a lot of Ponzi companies dazzled up in public relations and marketing, all designed to rip off investors before the insiders sell out and move to Aspen. And even worse, the Bay Area real estate bubble is built on top of this scam.

Tech companies today are either 1. The greatest surveillance organization ever created or 2. operating at a loss so they can eliminate competition and middle class jobs.

I remember during DotBomb v1, every other startup was the “Amazon of X,” (when Amazon was primarily a bookstore). Now it seems most startups are the “Uber of X”.

Case in point: Lime Bike and Bird Scooters. They are (no joke) $billion valuation companies, and all they do is rent bikes and scooters with a smartphone app. This can only be the greatest practical joke ever played.

I have been saying it for a while on Wolfstreet on the mass hallucination of house pricing in the SF Bay Area.

Just wait for the other shoe to drop – Stopping H4 EAD Work permits for mostly wives of immigrants in tech sector.

And the family wages needed for affordability go down. It has not yet withdrawn but USCIS has indicated it will not be issuing the H4 spouse EADs based on new rules.

Here is an older story from NYT:

https://www.nytimes.com/2018/04/06/us/indians-h1b-visas-trump-immigration-wives.amp.html

Love it. There is absolutely no sane country that would allow 75% of its best jobs in a premier industry to go to foreigners. Absolute insanity.

That is the pattern of colonialism, however. Since the “good” old days of the Fifties and Sixties folks like Lewis Powell wanted to pull the punch bowl away and disapproved of unions and the people who benefited from them. They have fixed that problem now. The consequences of the fix are not as great as they were advertised, however.

I love how the liberal media, doles out this sob story of the wives of H1-B tech workers losing their jobs as the H4 visa is phased out. Never a word about the job that is being taken away from an American when this happens. Then again, the NYT is not much of a newspaper anymore, some billionaire like Bezos will come and scoop it up and it will be propaganda tool for the rich and connected.

NYT has always been that way. Calling it the “liberal NYT” has always been a joke amongst the right, which has been pushing the Overton window to the right steadily for fifty years.

Freedom of the press belongs to those who own one.

As an aside I would like to recommend the third volume of Jacque Vallee’s diaries, titled Forbidden Science. The second and third volumes are very particular accounts of the rise of the computer industry in San Francisco and Silicon Valley as Cold War era federal research moneys blew through from Stanford to San Diego. Vallee knew some big players and participated in the tech and venture capital booms.

We are still in the early stages of the housing cycle downturn as evidenced by the fact that prices are still rising, even as the number of price cuts have soared. However, with the weight of rising inventory prices will eventually capitulate as well. The housing market moves rather slowly. The downtrend is likely to be a multi-year process.

Please remember that price increase calculations are annual. The first 6 months of the year, prices continued to go up and since then, they have been going down, rather sharply in many places. So, yes, YOY prices might have increased or stayed flat, but I would love to see how prices did Month over Month. My gut feeling is, they must have dropped about 5-10% since then.

Significant inflation causes all sorts of problems in a society. When the money supply is not stable, it is very difficult (impossible some times) to know the real value of things.

To Iamafan who calls mortgage interest deduction an entitlement. Let me tell you a little about our neighborhood. Believe it is about 100% owner-occupied. People here spend money on new roofs, backyard sheds, lawnmowers, leaf blowers, decks, patios, pools, tree services, landscaping, new driveways, gas grills, fences, porches, wood floors, furniture, new kitchens, new bathrooms, washers, dryers, ac and heating units, water and sewer, new brick chimneys, updated windows, doors, tile, paint and lots of paid labor for maintenance.

We pay north of $10K in property taxes supporting lots of gov jobs. And what’s the upside to all this economic activity spawned by home ownership? We get to take pride in our neighborhood and deduct the mortgage interest. Malinvestment? Let’s hear about where you live and all the jobs your residence supports.

Suspect you are a prominent NYT economics columnist, because you believe there would be no difference in our neighborhood’s appearance nor economic activity if it was 100% rentals.

Fairly certain the middle class pays enough taxes already. If you want to be a crusader, how about going after taxpayer dollars wasted.

he is right it is an entitlement. Without it house prices and taxes would be lower

So you live in a high tax state (most likely run by democrats with insane public unions).

And you expect a federsl government deduction on your income taxes to offset your high property taxes.

Does it ever occur to you that is was your choice to buy this house knowing full well the property taxes and the estimates of the costs of insane public unions?

That is was you choice to keep electing democrats who will do nothing to curb the insane public unions and will raise your taxes to infinity.

And that other people that have made wiser decisions than you should some how subsidized your poor choices.

Your state. Your decisions. Live with them.

What’s that old saying? If you don’t have anything intelligent to say then don’t say anything?

Right bc definition of an entitlement hinges on who receives the taxpayer charity. Poor people = entitlement, middle class home owners = not entitlement.

Should renters who are locked out of the market (mostly younger) subsidize more affluent, older people?

->Should renters who are locked out of the market (mostly younger) subsidize more affluent, older people?

That’s federal policy, written by much more affluent, older people.

100% correct. Any differential tax treatment is a subsidy/entitlement.

One of huge pet peeves are the people that say “renters don’t pay property tax”. Well, at least in my county, renters pay a lot more property tax, because non-owner-occupied residential is taxed at almost 3X the rate (technically same rate, but no rebates).

Another regressive aspect of the property tax is that retail is always appraised much more aggressively than other commercial (e.g. medical, office, warehouse).

->Fairly certain the middle class pays enough taxes already.

And will continue to pay them, long after there is no longer a ‘middle class’.

Somebody has to come up with the money for corporate welfare, tax gifts for the rich, offshoring subsidies, tribute paid on the national debt, and military adventurism, and it was decided that somebody would be you.

->If you want to be a crusader, how about going after taxpayer dollars wasted.

If it’s any consolation, taxpayer dollars are rarely ‘wasted’ on taxpayers.

I have a great bargain on a whole fleet of F-35s I’d be happy to sell to him ..

Si vis pacem, para bellum

->Si vis pacem, para bellum

Auferre, trucidare, rapere, falsis nominibus imperium; atque, ubi solitudinem faciunt, pacem appellant.

Ultima ratio regis bellum est.

The F-35 is a pretty good argument. . .

It amazes me how people buy houses based on their ability to pay a note and then 5years later when the market experiences a downturn they regret that they over payed and sell the house for a loss. If you buy a house you need to be willing to accept the monthly payment cost for 20-30years not just 5years!

Either way I’ve seen this cycle now 4 times in my lifetime and each time it’s a massive buying opp if you have youre finances in order because Homes typically undershoot intrinsic value in a crash as much as they overshoot in the boom times.

My advice is don’t buy unless you’re ok with 30years of monthly payments on a fixed rate. Don’t buy on variable rates, guaranteed to hit a downturn or rate surge in your lifetime! GAURANTEED

Home buyers need to think like a business and evaluate not just their monthly P&L statement, but also their balance sheet. The monthly mortgage service may be OK when they initially sign up for debt to purchase a house, but if the market turns, that asset on their balance sheet can also decline in price. They wind up trapped and can’t sell without either defaulting or coughing up enough cash to make the bank whole on the note. I would personally never buy a residence without at least 50% equity from the very beginning; it’s just too risky in getting trapped and having to move.

A few comments express the view that this is a normal cycle- and so buy the dip, because houses will rise to still greater heights on the next upswing. .

This theory seems to hold water if applied to the last forty years or so, a considerable portion (50%) of a human life. Humans tend to think 40 years is a long time. long enough for almost anything that rises and falls to complete one cycle.

The underlying cause of the wild ride up is not cyclic however, and that is the mortgaging of the United States. Forty years is not a long time in this context, in fact the wave we are riding only began about forty years ago.

When Reagan took office, the accumulated debt of the United States since 1776 was one trillion dollars. This was shortly after the US dollar was decoupled from gold. Reagan was the first post-war politician to ignore deficits and just four years later the accumulated debt of the US was two trillion dollars.

Now it’s 22 trillion and one trillion is just the new annual deficit, hardly a political topic at all. Via Freddie and Fannie a lot of the 22 T has supported housing in downturns, resulting in a short wave length for the market gyrations.

The underlying supporting wave hasn’t gone through even one cycle.

With the interest on the US debt becoming a significant budget item it may be closer to the crest than its trough about 45 years ago.

Forget rational economics. The current monetary system is/has been contaminated since 1913.

You talk about a 1T debt on Regan’s inauguration, that was already a prime example of the system’s inflative characteristic. 1->2 , 2->4, 4->8 , 8-16, 16-32Trillion are the natural mathmateical series that will play out. Takes about a decade for the debt to double.

So long as the average human can cope with the currency loosing about half its value every decade the system will continue for ever until there’s a civil or global war.

… asset prices will be loosely coupled to the overall money supply as these monetary expansions progress. Sometimes assets are overvalued and sometimes undervalued, but rest assured the nominal price will increase steadily over the long term. Doesn’t necessarily imply value is increasing at all, just a reflection of monetary expansion.

Knowing how to value an asset in a fiat currency is what separates the wealthy from the poor. Education is the key to understanding these cause and effects.. why we see growing inequality between educated and under-educated classes. E.g. The working class gets suckered into unaffordable mortgages and then dump their properties en-masse to shrewd hedge funds that buy them below market value.

I don’t like the direction of all this, personally, but these are the broad brush strokes we are bound to with the current monetary system in place.