Mortgage rates are climbing faster than the 10-year Treasury yield.

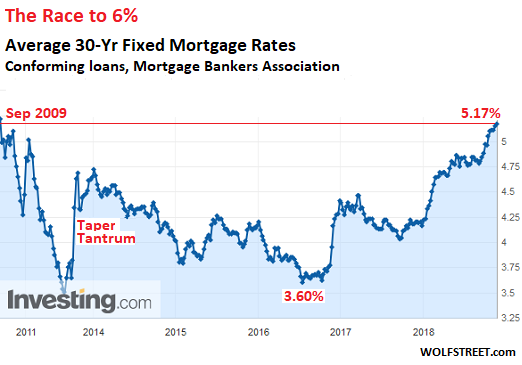

The average interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) and a 20% down-payment rose to 5.17% for the latest reporting week, according to the Mortgage Bankers Association (MBA) today. This is the highest average rate since September 2009 (chart via Investing.com):

Many people with smaller down payments and/or lower credit ratings are already paying quite a bit more. Top-tier borrowers pay less.

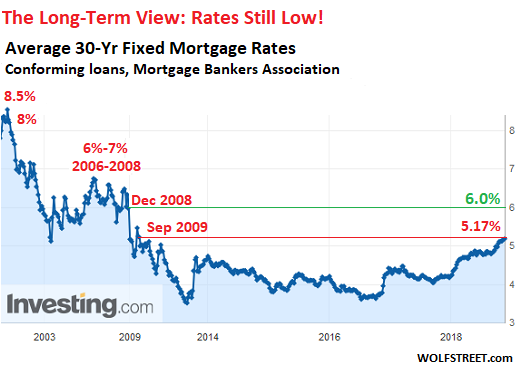

Thus, mortgage rates have moved a little closer to the next line in the sand, 6%, which is still historically low. At that point, the interest rate would be back where it had been in December 2008, when the Fed was unleashing its program of interest rate repression even for long-dated maturities via QE that later included the purchase of mortgaged-backed securities (MBS), which helped push down mortgage rates further.

Now the Fed is shedding Treasury securities and mortgage-backed securities, and we’re starting to see the impact on mortgage rates: The difference (spread) between the 10-year yield and the interest rate of the average 30-year fixed-rate mortgage has widened sharply.

Since the beginning of the year:

- The 30-year mortgage interest rate has risen 95 basis points, or nearly 1 percentage point (from 4.22% to 5.17%).

- The 10-year Treasury yield has risen 71 basis points (from 2.46% to 3.17%)

- The spread between the two has widened from 176 basis points on at the beginning of January to 200 basis points now.

In other words, mortgage rates are climbing faster than the 10-year Treasury yield, now that the Fed has begun the shed mortgage-backed securities. This is expected. It’s part of the QE unwind – it’s part of the Fed exiting the mortgage market and pulling its support out from under it.

But 6% is still low:

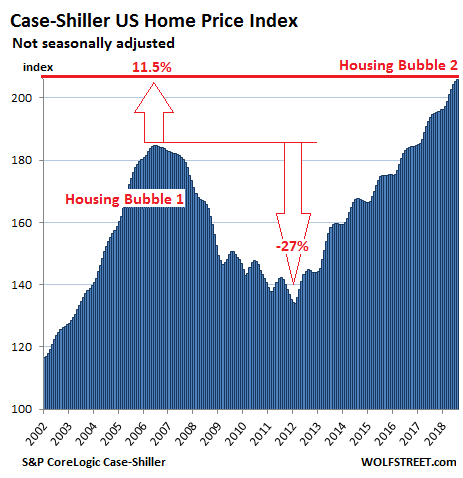

Home prices in many markets have risen far above the home prices back in 2008 and 2009, and far above even the local peaks during Housing Bubble 1 in those markets now that they have developed into a fully blooming Housing Bubble 2.

Home prices as a whole averaged out across the US have surged 11.5% above the crazy peak of Housing Bubble 1:

Even current mortgage rates – as low as they still are, historically speaking – are having an impact on the housing market and are putting pressure on it at the margin, with some potential buyers being locked out and others scared off as they’re finding today’s inflated home prices don’t mix well with even slighter higher mortgage rates: What was barely affordable for them, with a good amount of stretching, has become unaffordable.

And the cooling effect is already becoming visible in the first data sets for some of the previously hottest markets [Declines Hit the Most Splendid Housing Bubbles in America].

But for real pain to set in, the average 30-year fixed rate mortgage would need to get closer to 6%. This is likely the pain-threshold for the housing market. 6% will block enough potential buyers from buying at current prices to where sellers will have serious trouble selling their homes unless prices drop enough.

The cure for this market will be lower prices – even if it means rising defaults and considerable problems among mortgage lenders, particularly the non-bank lenders (the “shadow banks”) that have very aggressively moved into the mortgage market over the last few years. Quicken Loans has now become the largest mortgage lender in the US, ahead of Wells Fargo. These shadow banks are less regulated and have taken more risks than the banks. The Fed is already worried about them but worrying is all it can do since it doesn’t regulate them.

So when will the mortgage market get to the pain threshold of 6%? Given that the spread between the 10-year Treasury yield is widening, and that therefore mortgage rates will rise faster than the 10-year yield, and that the yield curve will remain relatively flat but won’t invert, there is a strong likelihood that 6% is only about three rate hikes away – and that will likely be accomplished by mid-2019.

Seattle home prices fall sharply. New York condo prices are nearly flat for the year. First feeble declines in San Francisco, Dallas, Denver, etc. Something is afoot. Read… Declines Hit the Most Splendid Housing Bubbles in America

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Great article! We’re hoping 6% comes to fruition by 2020.

We’re millennials and in the market for a house on the Peninsula ( San Carlos, Belmont, Foster city, San Mateo) in the SF Bay Area. We’ve been priced out thus far because we’ve been wary to take a mortgage more than 2.5 times our income.

Our budget is 1-1.2 million for a fixer upper in a good school district. Targeting winter 2020 for the purchase. Any advice from veteran real estate investors who know this market? Might this happen? We’re 29 (with a young child). I’m deeply afraid of going into so much debt. A 5k or 6k a month mortgage seems so risky, is this really sustainable over 30 years. But our rent is currently 3k for a house, so it doesn’t feel so bad. How are others doing it out here? When our parents bought, their mortgages were so cheap in comparison.

Keep renting or leave. Nothing is affordable.

Not quite true. I have a house that I am selling that will go to a “buyer” that has a down payment of less than a puddle of urine on the sidewalk.

Of course it is funded by FHA so he need not worry. The payments will not cover amortization over the thirty years, but hey, the tax bill takes preference.

The all brick quite decent house with a brand new roof now, and gobs of other expenses and new appliances and HVAC as of five years ago will go to an alien.

The rate for this loan is just under four percent.

I bought it from the goomint for 65% less than the taxcows ponied up for it two years prior. Chow down on yet another loss for we productive fools.

I forgot to mention the price on a 1400 sq ft real brick house with full basement and an enclosed big yard and a 2.5 car garage in very good condition.————-

Under 100k.

In the SF Bay Area?

I suppose that’s possible, love to see the address on this miracle property. east P A?

It’s like taking a leap the first time, step off and go or it just doesn’t happen.

In 2007, we bought our first townhome. The pricing was relatively cheap now that we look back. But I think we were still pulling $3k plus mortgage then. We bought it at the high end, then watched a 20% drop in value. We refinanced on the way down, but it still sucked. We thought at that point we were paying too much on the mortgage. And may be we would have been better off waiting three more years, but in the end it didn’t matter.

The bottom line is this, don’t worry about the pricing because you will probably live there for ten years plus, and things should even out. Pick a decent school district and suck it up. 6% coming to fruition doesn’t mean you will get a single family place in a good school district. Unless there is a wave of foreclosures, you will likely be still hunting for a place when the time comes. The one issue with the peninsula is limited space, and Any new construction are geared toward apartments.

Let me tell you a little secret to attaining wealth…. buy an investment property with positive cash-flow somewhere else (it can literally be anywhere on the planet)….and then rent where you live. Profit.

^This!! Your $1 million will buy 2 to 4 positive cash flow rentals in a college town (research this because overbuilding of rentals is a problem in come college towns). Let the income supplement the rent for your primary residence and plan to hold the rentals long term.

Better yet, drop your million into a small portfolio of solid dividend stocks and apply the dividend income to your rent.

(Disclosure – this is coming from a never-again homeowner)

They are borrowing that $1 million.

2020 is a long time in any real estate market. Wait till your ready!

My guess is 6% is unlikely to be a magic figure that will bring down prices. Prices will come down when the seller cuts his well-entrenched anchor to his price, which happens as Hemingway said “slowly at first and then all of a sudden”

The only question then would be how is the Fed going to reflate this?

Mortgage rates are not going to hit 6%. The Fed has supposedly been tightening for a couple years now yet the FFR is only about 2% and the Fed balance sheet is still over $4 trillion. In other words Fed policy is still set at emergency, depth of recession levels. If you are waiting for rates to normalize you will be waiting forever.

The Fed has two mandates, enacted by Bernanke and now made permanent. The new mandates are 1) monetize the government debt and 2) inflate asset prices. Raising interest rates would not facilitate either of those mandates so guess what, aint gonna happen.

But, you say, the Fed has been raising rates. To that I say, really? With inflation heating up and unemployment at 3.7% we have already witnessed a Fed chairman on CNBC, this morning, providing dovish forward guidance. This so called tightening cycle is going nowhere. Ten years after the crisis monetary policy is still sitting at emergency levels. There is much debt yet to be inflated away. The dollar is going to zero.

van_down_by_river,

There was no “dovish” forward guidance. Looks like 1 rate hike in Dec and 4 rate hikes next year. If that comes to fruition, it would push mortgage rates to 6.5% by the end of 2019.

This rate hike cycle has now lasted 3 years, it’s very slow, slow enough for everyone to adjust — that’s the idea. They’re looking at a 4-year or perhaps 5-year rate hike cycle. They’re doing in one year what Volcker had done in one meeting.

This Fed isn’t into shock therapy. It’s into the art of boiling frogs.

No offense but the fact you are actually asking this question shows how out of touch young people are. What do you even do for a living out there in SF? Do you realize your JOB is what keeps your financial head above water. Do you think there won’t be MAJOR impacts in employment as the current housing bubble pops everywhere? The smartest thing you and your family could do is MOVE! SF will be a nightmare. There will be plenty of much wealthier people ready to jump in and snatch whatever you think you can afford. The “lifestyle”i s not worth it. And the schools are a bunch of liberal indoctrination pogroms!

Your parents mortgages were so cheap because the country wasn’t in $20 trillion of debt, interest rates were high thus kept the price of housing stable etc. There are a whole host of reasons why previous generations were much better off and had it a lot easier at affording the American middle class lifestyle or “dream”. The FED has ruined your future and your childrens’ future. Do your child a favor and move out of CA. Give them a real shot at financial stability and prosperity.

Well last bubble pop there was a pecking order. Normal people got to buy in 2012/2013. As you not the deepest portion of the recession was bought out by larger investors.

But the 2012 people still got some deals. Clearly if you pose your job during the next recession this will all be a moot point.

I could see tech getting bad. I am hoping my new work place is resilient since it is half military contracts. And that money flows like water under Repubs. Probably for the next 6 years even…

But if commerical buisness tanks they could still shuffle people out…

“Our budget is 1-1.2 million for a fixer upper in a good school district”

How fucked up is that?

A million dollar house used to be a fucking mansion not a fucking fixer upper? I don’t belong here……I don’t fit in the economy any longer. I fear a reality is coming to this type of delusion.

I am with you! This idea that people can weather this coming storm and buy a fixer upper for $1M in 2020 while the rate hikes continue is ludicrous. So much of the economy will be shaken to the core by the interest rates doubling or tripling from 2012. Reduce debt, rent until the dust settles, which will be about 2025, not 2020. Good luck and keep your powder dry.

You shouldn’t even care about the school district because all public schools in big cities and their suburbs are not that great. Buy a cheaper home in a known average school district because it is very likely you will need to send your kid to private school anyway. The price differential in a cheaper district will be the money to fund your kid’s private school education.

There are some amazing public school districts in the Bay Area. I’ve been a student in them and a teacher in them. Worth at least 25-30K a year, per child. Factor this into your mortgage payment – because it is already built into the price of these homes. If you do not have kids, you’re helping out your neighbors.

Don’t forget to add property taxes on that $1.2 million fixer-upper. This could run you over $1,000 a month.

Plus your mortgage payment of around $7,000 a month at 6% 30-year fixed. Of this, interest the first year comes out to about $6,000 a month, much of it non-deductible.

Then you have the expenses of a fixer-upper (fixing it up and maintaining it).

So you have to be willing to pay $8,000 and up per month to live in what may be a not very large fixer-upper.

That said, life moves at its own pace, as you suggest, and you have to make decisions based on your situation, and not some market data.

California is a non-recourse state. So the ultimate risk is with your lender :-]

Talking of fixer uppers, new homeowners underestimate how much home repairs, upgrades and maintenance cost. Our budget earlier this year was 60k. We ended up spending 100k for basic stuff (electrical, plumbing, flooring, replacing 30 year old light fixtures and water damaged cabinets). Contractors were in short supply and we did about 20% of the work ourselves.

Another 5k on landscaping of which 2k was just to pull out several trees that were damaging the foundation or threatening to fall on the roof.

Upgrades and ‘repair and maintenance’ are two entirely different things.

“We ended up spending 100k for basic stuff.”

If you ‘ended up’ spending 100k on ‘surprises’, then you didn’t know your ‘basic stuff’.

The conventional advice is to buy between Halloween and March, when the prices are lower. If you find a good house which fell out of escrow and has been sitting for a few weeks, you might get a better deal.

The other conventional advice is that, if you can’t buy a house, you should buy a condo. That way, you have at least got one foot on the escalator.

Finally, the conventional advice on interest rates is that medium-high rates are the first-time buyer’s friend. It does you no good to qualify for a 3% mortgage if everybody else in town also qualified. The resulting feeding frenzy will push your purchase price up and up. Getting a good price with a 6% mortgage is actually a better deal.

– – – – –

Unconventional Advice: The SF Bay Area is never going to be cheap. I have friends in Sydney, Australia who refused to buy 20 years ago, and decided to wait for prices to come down. They are still waiting. Maybe you should move somewhere else. I used to live in Sonoma County (owned a big house) and in Palo Alto (rented), and now live about an hour south of Seattle, in the outer suburbs.

Assuming that you both have jobs which are mobile, you should consider moving to Eugene, OR, or Bellingham, WA. In addition to low housing prices, you will enjoy that nice California weather as Global Warming kicks in. . .

Good luck on mobility if you are stupid enough to get into manufacturing. My mobility is rather limited by having many machines that go from 30,000# to 200,000#. The heavies are very old as no one makes them any more. They sit upon a reinforced concrete base that is a meter deep.

You techies don’t quite get it that when the base of your crap is gone that you will be worth a good deal less.

The SF area has by far the highest price / median income of any area of the country.

Sales are stagnating, houses are being withdrawn from the market while inventory is rising.

Combine this with the end of the tech play on Wall St, and the resulting major decline in bonuses and you have a guaranteed perfect storm for a major decline in prices.

I honestly can’t tell if this is a joke posting or not.

steven & Bay Area Girl

That’s funny: Now that you mentioned it, I re-read that comment, and I can definitely see that you may be right, and I can see the potential humor, making fun of this whole situation here in the Bay Area. And it’s really hilarious.

But in my first reading, I took it to be serious and never saw any humor in it, and didn’t even suspect it.

Bay Area Girl, please let us know if this was humor. If it was humor, it was expertly done!

(i thought it was a joke, too.)

Oh man, BA girl has got us there. In a good school district mid peninsula for 1.2 M, a millennial, all the right amount of naïveté, this can’t be real.

I don’t know if her post was a joke, but Wolf’s breakdown of the monthly cost was hilarious! $10k per month For a fixer? (I’m adding in repairs and utilities for fun).

House prices and affordability are mostly a factor of supply and demand. When there is limited supply vs demand the affordability will always be a problem.

When interest rates go up for housing the cost to the borrower goes up. So having them go up may mean the asset price may come down but the cost to you will remain the same. What might make them more affordable would be if enough demand is destroyed while you are lucky to not be a part of those cuts.

Another thing that could make housing more affordable would be an increase in supply. From reading Wolf, it appears that almost all of that supply is in upscale apartments and not SFR. But because these are all by huge corporate backers, they may remain high even in the face of a lack of interest by the public until the money runs out and the courts take over. This can easily take years.

The high cost of housing on the coasts and in the big cities is due to the lack of space vs the amount of wealth accumulated. To many people for the amount of space.

Zoning plays a large part in the cost of housing in all cities.

it’s really hard to time the market but clearly we are in a bubble today. the decision to buy needs to be based on your desire to stay in the same place for a long time. renting often makes sense but you need to accept that landlords redevelop buildings and kick out even good tenants. rent hikes in sf are a given. buying will shield you from that instability but put a tax target on your back. if it was me, i would keep renting until the next crisis. if i was still was employed after the crisis, i would then shop carefully for someone who was panic selling. how do i know that strategy? because someone did it to me after the last crisis.

“Renting often makes sense but you need to accept that landlords redevelop buildings and kick out even good tenants. rent hikes in sf are a given. buying will shield you from that instability but put a tax target on your back. ”

In a normal market, you’re right.

If you’re in a rent-controlled SF apartment, a lot of those risks are mitigated already. My rent can only go up by a fraction of the CPI, SF has the strongest tenant laws in the country; could I be Ellis Act’d tomorrow? Sure. But in reality, I would cut a deal with my LL for a nice payout and be on my way. It really is its own animal.

I am in the market for a home, but with these ‘gifts’ from the progressive political landscape, I don’t feel that I am wasting money or time by renting, like some people keep implying. I invest and save the difference. I just feel the next leg here is flat to down, versus another 15% gap up like it has been since 2010.

And if the bubble doesn’t deflate, I’ll find somewhere else to live. SF is great, but it is not great enough to justify these prices IMHO.

Bay area is great?

What about the last week in which the smoke makes going outside hazardous

What about the traffic which was rated the worse in the country.

What about the filthy neighborhoods in SF which have to be power washed frequently

What about the massive homeless problem?

What about problems with car breakins

What about the highest income tax rate in the country?

SF is a great city if you have a bunch of money and do not have to commute

huh. i didn’t realize sf had rent control. i’m in a similar situation in new york. however, in my case i don’t see it as progressive “gift.” the land my bldg is on was taken by eminent domain and by that famous progressive governor nelson rockefeller ;). then in order to get a number of nys state perks including tax abatements, the developer voluntarily entered into a government housing program. after a few decades, it proved worth the developer’s money to bargain with the tenants to get out of the housing program. that’s how i got my deal. that’s the way the game is played in america. usually, these things benefit the rich sometimes middle class schmucks like me get lucky.

Think of it more about housing than buying a house, ( a house is a liability) and buying transportation is not the same thing as buying a car. There may be better times to buy a house ahead.

I am not in you area. I am from New York area.

In 1980 I gave up a 8.5 percent mgt to assume Ann existing one of the seller at 10 percent.

Exactly after I purchased my home interest mgt rates went up steadily to about 17 percent .

People with a job paide higher for their houses and higher mortgage rates.

Those with higher paying jobs keep paying.

Feels like the same is happening now.

Good luck to you

Very. very wise.

You’d be crazy to pay twice what you already pay in rent. Save that money and retire early.

@Bay Area Girl-

>I’m deeply afraid of going into so much debt.

Don’t buy now… it’s likely game-over for some time!

You really need to watch this video with your husband.

“The Coming Retirement Crisis”

youtube.com/watch?v=5OFaZcC0lRU

My recommendation is to stop thinking about buying a single family home , esp in the peninsula where there’s an obvious shortage of supply with booming demand. Even in a down turn it’s still competitive so banking on higher rates or recession is still a gamble – especially considering you yourself could be unemployed if the recession gets ugly.

You’re much better off buying rental real estate 2-4 units and live in one unit. Rental property trades at much lower $/sqft as it’s priced on CAP rates vs buying hysteria. Doesn’t mean all rental property is good, but if you spend some time looking you’ll be sure to find between value for those zip codes.

Based on my research rental property trades at about half the price per sqft in the east bay. And you can find them in great neighborhoods.

Over time you can convert the house to a single family when you’re more financially grounded. But meanwhile you have rental income to subsidize your housing

Two rules:

Buy low…sell high.

Never look back.

According to Federal Reserve’s FRED database, the spread between the average 30-year fixed mortgage and the 10-year treasury has a normal range between 1.5 and 2.0 percent. It was on the low end of the range earlier this year, but on the high end of the range in 2016. I don’t think this year’s drift up to 1.75% is related to the Fed’s shedding of mortgage securities.

Another possible cause for a widening of the spread is that, in a rising-rate environment, fewer borrowers will be prepaying or refinancing existing (lower-rate) mortgages. The effective duration of the newly-issued mortgages is therefore somewhat longer. From the investor perspective, the mortgages are funded by purchases of mortgage-backed securities, and a longer duration on the underlying mortgages pushes those bonds higher on the yield curve.

FRED Graph here: https://fred.stlouisfed.org/graph/?g=m4j7

Excellent comment by wisdom seeker

That’s a very interesting chart. I was wondering what the spread looked like historically as I was reading the article.

The prepayments on FHA and other govt backed mortgages will likely go down to zero because those mortgages are assumable and it’s cheap <3% money. This means that those mortgages issued in the last 5 years or so will be around until the very end. If the fed owns tranches at the front of the payment stream those will be paid off and disappear. The tranches at the end will be around until the end or until the interest rates drop below their average coupon.

I always like your comments on womens’ goods. They give me a basis on retail that I find to be of real value.

OTOH, the ridiculously low mortgage rates on the FHA crud that the FED holds are toxic. It was easy to go on the web and find houses that were on offer for -45% to -90% of what the FED held MBS was gobbled up in order to save the maggot banks.

The FED book has never been audited and I contend that it is junk that only can be justified by their unconstitutional gift of creating credit from the aether.

I don’t understand your comment because all the agency mbs held by the fed is insured by the agencies. It could stink for a mile and the fed will still get their money.

I did not realize there were any assumable mortgages still being done in the last two decades. Are there others besides FHA?

Yes, I think GNMA.

Agree. The mortgage spread is increasing, because durations are increasing.

Wisdom Seeker,

In the relatively short time span of the data you linked (only goes back to 2004), the peak spread was 300 basis points!

Yes, I’d love to see a longer data series for average mortgage rates. On the other hand, the old mortgages weren’t federally guaranteed, so the older historical spreads might not be relevant to today’s marketplace.

The peak spread of 300 basis points was during the First Great Financial Crisis of 2008, when it was hard to get a mortgage at all, and Treasuries were being bought madly by panicked investors. So the spread blew out.

The fact that FRED has this data is interesting because it hints at what the Fed finds important to monitor. And it will also be interesting to see how wide the spread gets in the Second Great Financial Crisis! ;)

The Fed is still oblivious to what the real economy is. Listening to Powell’s speech at the Dallas Fed yesterday, It’s obvious that nothing has really changed, and this will be problematic for the U.S. housing market.

No, the Fed is not oblivious to the real economy. Housing is in a bubble, other assets are in a bubble, that the Fed created, and the Fed is belatedly trying to tamp down on those bubbles and deflate them a little. That’s what that talk about “financial stability” is all about.

I would respectfully disagree, but that’s what makes a debate.

“At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.” Ben Bernanke – March 2007

That was said for public consumption, to calm the worried spirits, by Bernanke, 11 years ago.

Hank Paulson did the opposite and credit froze the moment he said it. He said, when he was asking Congress for unlimited bailout powers, that the world would come to an end if he didn’t get it. He didn’t get it…. But it totally spooked everyone, after they were already worried. And everything just stopped, that day!

A big gun like this needs to be very careful with what they say because they can cause the very crisis they’re worried about.

Aaron,

Another thought. I think it is a big mistake to assume the Fed doesn’t know what it is doing.

You may not like what they’re doing, and you may think it’s the wrong thing based on what you would like to happen, and you may get hit hard by the Fed’s actions or inactions, but that doesn’t mean the Fed doesn’t know what it is doing.

NOT a BUBBLE

What about all the zombie companies which are kept alive only by the largesse of the Central banks.

What about BOJ , whose portfolio exceeds Japans

GDP

What about the tech stocks , many of which trade at market caps of billions of dollars while generating negative FCF.

What about Italian debt , which is close to default , but trades only at a small yield premium to the US

And last what about San Francisco, where the median house sells for almost 1.7m, while the median household income is ~ 110,000$

This refers to Wolf’s comment below:

“That was said for public consumption, to calm the worried spirits, by Bernanke, 11 years ago.”

Wolf seems to be giving more credit to Bernanke than he deserves…

Here is one of the best of Bernanke for public consumption…

July, 2005

“We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though.”

There are more here…

https://www.businessinsider.com/bernanke-quotes-2010-12?IR=T

So it would be naive to assume that it was all for public consumption.

Whether the comment was meant for public consumption or not, it doesn’t change my point. My point is that the Fed should not be trusted. It’s blatantly obvious they suck at price stability. Boom, bubble, bust, rinse, repeat.

If those comments were merely for public consumption and they really do know what they are doing as Wolf suggests, then that is even more dangerous. It would only confirm that they are a cabal of crony capitalist hypocrites.

Maybe another good discussion is how normal 401(k) holding folks can shift out of any US based Assets/Equities to protect their existing holdings.

Face it most plans are limited in selection but you have to do something rather than just rude it all the way down thenlisten to people who say, “If you wait long enough it always comes back”, NOT and Idiot.

Limited in options and virtually all options have high fees. Example, many 401Ks have a Fidelity govt moneymarket as the low risk option – spaax has a 42 basis point expense ratio. Vanguard does the same sort of fund for something like 25-30 basis points less!

Have wondered if some of the expense get passed back to the employers?

Agree David…Moved 401 to Vanguard because couldn’t get free of equities at previous provider. But learned gov’t securities funds are simply that–Funds. They don’t carry any of the guarantees implied by the underlying securities. So they invest the money into Treasuries, take a fee, you get about 0% return after inflation, and are exposed to the risk of Vanguard’s general financial condition. What a deal.

On the topic of fun typo’s…the paragraph that begins “In other words” contains “the Fed begins to shed mortgage-BAKED securities” :-]

MB732,

That goes on my list, right next to “brick-and-mortal retailers” :-]

Thanks.

Several years ago I self up myself with a “Self Funded IRA”. Now I can managed my retirement with a number of options, rather than just the market. BTW, I have few funds in the market now, most of the IRA is invested in Rental Properties.

@MB732 In the spirit of funny typos, I liked “rude it all the way down”…it will be a rude ride for sure

My thought was to at least maybe shift things to emerging markets or something? Thoughts?

the basic problem is this. All of these bubbles are related, if the Feds could ramp down one bubble without affecting the other, they would do it in a heartbeat. But their lever on the printing press means that while they are deflating the housing bubble, they are going to deflate everything else as well. Worse, they have no idea exactly what level of deflation is necessary, so they will overshoot like Janet and Ben overshot when inflating the bubble.

My guess is that they have already raised rates a little too much a little too fast. Part of it is human nature, the Feds looks at the near term data, but those effects bake in what was set up two years ago, so they overshoot. When the economy crashes, the root cause will be obscured again, because all of the prognosticators will blame the country’s political leadership, and they do share part of the blame, but only a small part. And Jerome is going to essentially replay the role of Greenspan and raise rates until he goes overboard.

It’s too bad really, human nature is basically such that people think they know the best in terms of timing and actions, they don’t take into account all the other people around them. Usually, the more powerful, the more educated they are, the more insular they become. Relying solely on data that has a built in lag and a model that is not perfectly predictive.

Two examples of this problem right now are Japan and China. From the outside, the cause looks different, but if you boil it down, it’s all because of the people that were and are in charge. They were perfectly smart people, but had too much faith in their own intelligence and ability to control things. The more control they had, the bigger the disaster, Japan is fortunately past the worst point, but it will be stuck with anemic growth for the foreseeable future. China will be the most spectacular crash ever seen, and the effects thereafter will be very unpredictable, my guess is that it will lead to a serious armed conflict and probably reset the world order for a century or more.

belated is the operative word. Historically has the feds waited this long to tighten? (late cycle)

FWIW, BBG today cited the “official” price inflation rate at 2.3 percent. Do an arithmetic scale on a graph of that crap as compared to bank rates for savers.

“The cure for this market will be lower prices”

But then is it possible that the cure will be allowed. Also if Quicken Loans was to go bankrupt will it cause a contagion. Is it likely in that event that the Fed will simply be a bystander? Once a meddler always a meddler and they have been meddling since 1987.

In short, many questions. Given that despite all then gyrations (in the markets and house prices) nothing has happened as yet, answers will arrive when the movie really starts.

Well, the Fed is expected to help the BANKs that lent Quicken.

Quicken itself is not too-big-to-fail.

I used to work at quicken. Their business model doesn’t really carry any high risk to run into a bk scenario

Once the mortgage is closed – they sell it faster to BoA or JPM for a markup faster then a waffle in a toaster ( or they used to anyway)

Dan is an amazing operater and limiting his risk he has done. He basically makes more or less cash. Either way they are a great company that doesn’t over extend itself

Time for a big price correction. Can’t wait. The only problem is that it can take a couple of years before the prices get genuinely worthwhile.

This will only come from additional supply which would have to come from lots of people losing their homes due to defaults unless for some weird reason the big PE firms who hold so many used as rentals are forced to sell. Then the supply increases and the affordable homes increase. Otherwise it is just the same payment buys an asset at a lower price, sort of like a bond.

I guess it could come from a much lower demand also.. And that would mean that we are in a severe recession with high unemployment. Which would trigger the defaults..

Wolf said the FED knows what is doing. So what is the FED doing? Good for who? Bad for who? At what time in the future? To what degree?

Here is what I think the FED is doing. The FED is making you lose your jobs so that you will beg to have a job. This kills wage inflation, and this gives back the power to corporations and capitalists. F*** labor, that is what FED is doing. The point is, there will be people losing jobs and therefore losing homes. There will be supplies. And As Wolf said, the FED knows what they are doing so they will get us there.

You’re right in that the Fed doesn’t give one iota about you and me. It doesn’t mind at all impoverishing millions of people so that banks can get recapitalized and that the asset holders are made whole, after steep losses.

You ask the right question: Good for who?

My job is to try to figure out where the Fed is going, and what it will do next, and to whom.

Bingo!

Wolf, another great piece of research.

I’ve come to believe a couple of things. With respect to policy makers and government leaders…..they are generally ill informed. Sure the Fed has tons of research and sophisticated models, much of which provides them support for their actions. But most of this input is likely looking in the rear view mirror.

The economy has been and is changing dramatically down at the ‘little people’ level. One change people seem to overlook is how fragile it has become. One key factor is the lack of savings by so many in the country. The parents of the yuppies lived through the Great Depression and so were smart and active savers; even when money was tight. Savings is a critical buffer for people when things get tough. Without savings, consumption drops dramatically with even the smallest of impacts.

Bottom line, this American economy is incredibly fragile. That is why I expect job losses to snowball because consumption and demand will drop quickly as most have nothing to buffer the shock.

I’m not sure the Fed gets this.

Thanks again Wolf for your work. Very insightful.

I think less ill informed than just looking at things thru their narrow perspective and with their own interests in focus. The railway train going across a mountain pass can’t see that an avalanche has started down the mountain until it hits the train. Was the train’s perspective incorrect?

But everybody is getting a larger phone and subscribe Netflix!

Who cares of fragility and the rainy days if you have phone, netflix, facebook and porn!?

Good comment by Alex. I will now be watching my nephew ride the declining prices downward in the Bay Area. My suggestion to depart the area was met by scepticism.

$60,000 per year in just interest payments for the joy of signing on the dotted line? For the next 20-30 years? Can housing prices really appreciate that much to make it sensible? Respectfully, I don’t see how it is possible in a tech downturn.

Hard decisions to be made so early in life. Great comments today. Good luck.

Not even the young got sucked into this mess. My brother’s in-laws retired in some California town, they just mentioned looking to sell and retire somewhere else. With the prices and the fires it makes for one hot mess.

Paulo you intoduced THE true Bay Area housing deflator into this discussion. TECH DOWNTURN. Oh yes everyone now say that’s not possible, which leads me to ask where’s AOL et al?

Tech downturn?

In the immortal words of Yogi Berra, predictions are difficult, especially about the future.

That said, if I was a betting man, I’d predict the demise of the current tech bubble no later than 2019, when Uber and its billions in investor and operating losses jumps the shark with its IPO.

Yay, but those IPOs, Uber and Lyft will still transfer a huge amount of wealth before hand. But only if it happens, they may be pulled back due to market conditions.

I don’t know when there will be a tech downturn for sure (and obviously). But there will be one when interest rates rise high enough and prudent investors will do okay with savings, treasuries, etc., and folks won’t have to chase yield so much and play the stock lottery. That will also be the end of Shale and a whole bunch of what I call fluff jobs; jobs that produce goods and services people don’t really need all that much (including travel, tourism, etc).

My US citizen sister lives on Camano Island south of Bellingham. 10-12 years ago we were out walking along the beach and were looking at some of the most impressive houses; engineering and consumption marvels, really. “See that house” she asked? “That guy was a dot commer. See that one? He was also a dot commer, moved up from Seattle before the bust”. It happened, happens, and will happen in every industry one way or another. Hopefully, not all at once :-)

I’ve lost a few careers along the way during downturns. However, I had a back-pocket skill set that always always got me hired and kept me employed. That was carpentry. I was hired in aviation when pilots were driving taxis, because if there was no flying I could rebuild the office. I was 19 at the time and the owners paid me extra. I was hired to run a large fish hatchery because I could run the building programs and crews, etc etc etc. I have never had a mortgage that took more than 1/3 of my take home pay which also allowed my wife to stay home until the kids were teens. I retired at 57 and just built a small rental for extra fun money.

Don’t just live within your means when everything is going gangbusters. Live below your means and make damn sure you can pay the bills if you lose a job in the family. And what kind of jobs will always be needed? Nursing, Physicians, Builders, Plumbers, Electricians, Police, etc.

Think your industry is safe and secure? Answer this, whatever happened to tenure? That’s just one example. My best friend is a helicopter pilot and makes a fortune fighting fires. Guess what? They don’t haul passengers so they’re droning them (just starting)….machines will have a bigger payload, can fly at night, and don’t need a skilled expensive pilot. Everything is up for grabs, including SF tech.

regards

Aol, global crossing, henry blodget, bernie ebbers worldcom, george gilder, rambus, excite, lycos, napster, netscape… those were the days.

AOL got replaced by smarter, better tech.

My first purchase was with a mortgage at around 11% in the late 80’s

Young people have no context as far as rates are concerned

I paid on mortgages in the Bay Area for 28 years, at rates between 4 and 11.5 %. In most cases, rents in my neighborhoods exceeded my mortgage payments within a few years of my moving there. I got everything paid off at the age of 58 and feel that being relieved of the burden of mortgage/rent in my later years was worth the effort.

Just when I was thinking about another home…

Were it not for the easy access to credit the US economy would be in a recession. It was only the easy access to credit that got it out of the last recession. Easy access to credit will not prevent it from going into the next recession, and will not get it out.

It seems likely that most people are at least vaguely aware of this.

https://fred.stlouisfed.org/graph/?g=m4JZ

The other side of this problem is WHO is buying MBSes?

Looks like the Fed is the largest holder of MBS. The big banks may have been preferring commercial real estate and to some extent agency debt. But unless they can make more money, I doubt they are that interested in cheap home mortgages especially the current Net Interest Margin (NIM) and flat yield curve.

The foreigners also seem to allocate less long term securities into Agency. The latest TIC data, http://ticdata.treasury.gov/Publish/shla2017r.pdf , suggesting they only allocated 980 / 17,481 or 5.6% into Agency debt last June versus 11.15% in 2010.

Looks like the Yields have to rise.

I just bought a small fixer-upper in Harrison, Arkansas for 27K.

It is over 100 years old, but still solid. I am taking one exterior wall at a time to pull the old cedar siding off, insulate the wall cavity with rock wool, re-sheathe it, and add new windows and Hardiplank siding. And I can walk to the downtown square for coffee and breakfast in the morning.

A million dollars for a fixer-upper is beyond my comprehension.

@NotLee,

(Last comment for me). I bought my last fixer upper 15 years ago for $110,000. It is now new and beautiful, one wall at a time. I bought the place because it was on 141′ of riverfront that doesn’t flood, and is surrounded by forest of large trees (some are 4′ diameter). I haven’t a clue what it’s worth being on Vancouver Island…maybe 600K? If I was in the US I think I would look at where you are, maybe Tenn, or W Virginia. Once you have a house paid for it’s like you just got the biggest pay raise known to mankind, plus no worries. One can always visit the lifestyle places that are too expensive to live in. Anyway, cheers everyone (until the next article).

Thank you Wolf R. Awesome as always.

Wolf, as far as the Fed’s appreciation of “the real economy”:

I do not imagine that any of the Fed bankers put on middle-class disguises and go shopping at Walmart or Dollar stores, listening to fellow-shoppers’ check-out lines conversations, and browsing through the stores. (Cf. Shakespeare’s Henry V, wasn’t it, who threw on a cloak and walked through the tenting-tonight campfires of his troops on the eve of the great battle, to check the mettle of the soldiers.)

I’m in complete agreement that the Fed is studying the bubbles and trying to “deflate them a little”. The VLIRPs, ZIRPs, and NIRPs were a big economic experiment, and the unwinding is not nearly done. Numbers, statistics, and bankers are part of the real economy, but I feel that the the Fed’s studies are as close to the real economy as CG is to real life.

Paulo, I have the highest respect for you and the life you describe. While I am typically in agreement with your comments, I’m going to have to question “riverfront that doesn’t flood”….hoping of course that it does never flood in your lifetime !

Awesome article. Gives many of us hope of owning a home again. Just have to keep saving and wait for a lowering of home prices in the North Texas area.

Wolf, another master piece of the article. I used to believe the housing market was temporarily slow down but now I have to agree with you the housing market is going down and it could be dangerous. I owned a large stake of the house builder stocks and I think it is the time to get out the game.

SF is nice place and I believe it will still be attractive for IT talents. I think 6% interest rate could be still ok but, to be honest, it is painful for the recent buyers.

Last but the least, technology and well-educated immigrants are two key drivers for the development of the country as well as the bubble of the housing market.

If your dream house requires a 30 year mortgage you cannot afford that dream house. Only buy what you can afford with a 15 year mortgage. The idea you get more tax breaks with a 30 year mortgage is no advantage if you lose that house before you pay it off.

Wealth is acquired once you pay off the mortgage and own the house. Up to then the bank still owns it and your basically paying rent to own it.

And when you own a home if you want to risk that equity for another 15 years mortgage to buy another house go ahead, but remember you no longer own a home and all that equity is at risk.

Many times I would get offers to reinvest my equity and “put that equity to work”. I would simply tell those salesman my equity is at work now. It is paying the rent I no longer have to pay.

P.S. We are headed for years of falling prices because all the debt created since 2008 means future buying is done. The Fed created an economic stimulis to buy today instead of waiting for tomorrow.

thanks to wolf and everyone who comments here. i really enjoy this site for it’s mix of the anecdotal and the wonky! i think it has helped broaden my perspective on the economy.

Appears to me the housing market as well as the stock market have obvious cyclical gyrations. The exact timing is not so obvious though.

These are influenced by national and international circumstances. One constant appears to naturally be the wealthy and powerful manipulate the system to protect and enrich themselves at the expense of other less fortunate. This is natural human nature and has existed since the beginning of time.

As recently demonstrated in the 2007 to 2010 debacle, no matter how obvious and documented the slaughter of the common individual is, the cycle repeats itself. This has gone on for millennium and will likely continue as the story and system is controlled by those who profit. It is all complicated, but then again really simple.

And the “protectors” from what you describe include many of good intentions who are used as the face of those with less than good intentions.

Mortgage application volume is down 22 percent YOY, according to the Mortgage Bankers Association’s seasonally adjusted index.

Yes, but this is due to refinance mortgages. With interest rates rising, that refinance business is in a world of hurt. Wells Fargo has been complaining about it for two years, and has followed it up with layoffs in its mortgage unit.

Yes, I’m starting to get tons of solicitations for “Limited Time Special Offer CD’s” from local/community banks. Somebody’s capital requirements may be getting stressed.

This entire week we had a winning streak in rates. We are at 1 month lows as of today.

Yes, if you look at a longer-term chart, that’s precisely what rates do: they go up and down on a daily basis. But there is a long-term trend too.

Those Unregulated “Shadowbank’s”.

A lot of them get their money from FDIC covered bank’s.

When they go, Girly bumps up.

US Taxpayer will still get stuck with the bill.,

Yes, banks are clearly exposed to shadow lenders. And they will take losses. But the amounts per megabank are in the billions — a magnitude they can digest without collapsing. Smaller banks that lend to shadow banks might proportionately get a bigger hit.

All these loans are backed by collateral, when the loan defaults, the bank gets the collateral. The collateral is unlikely to be worth the amount of the loan, but the bank might get 50 cents or 70 cents even 90 cents on the dollar for it, so the actual loss on that loan after the collateral is dealt with would likely be less than half of the face value.

The larger shadow lenders securitize most of their mortgages via the GSEs (Fannie Mae, et al.). In other words, they sell them to the GSEs which then turn them into MBS, and those risks are backed by the taxpayer for now.

The current bond rally and strong dollar are reflective global flight to safety that is independent to the housing market.

In times like this, return OF capital is a lot more important than return ON capital.

This is remarkable. I read the whole thread, and there were only intelligent, thoughtful comments without any name-calling. Am I on the internet?

Yes, and many props to Wolf for that, in addition to his excellent reporting and analysis.

Wolfstreet and Naked Capitalism are the only sites I’m aware of where the comments add to, rather than distract and detract from, the already high levels of reportage and analysis.

Thanks to Wolf and Yves Smith for their hard, valuable work, including the skill with which they moderate the comments.

Did anyone here watch the full one hour interview last week with Jerome Powell at the Dallas Fed? It was very enlightening. First of all I totally agree with Wolf that the Fed knows precisely what’s going on and what they’re doing, but their job is and always has been to mask the truth as convincingly as possible. If you watch that interview (it’s on Youtube) the cold heartedness and dishonesty of the seemingly genteel Mr. Powell is quite glaring. The most revealing moment is when he dismisses our national debt problem as basically not a factor in his decision making on monetary policy. So, to me the obvious came to mind: pretend that the rising cost of servicing the debt doesn’t matter & everything is just peachy so no one asks the bigger question: aren’t we headed for a crash in the stock and RE markets? Which then of course leads to the question: and when those markets crash what are you going do to — are you going to do even bigger-than-before rounds of QE till the dollar collapses, or, are you going to try to preserve the integrity of the dollar and sit back and watch about half the world die?

A lot of people are predicting hyperinflation in the future, but why would the Fed do that, all things considered? That prediction depends on the presumption that the Fed are a bunch of idiots, and willing to put their bankster bosses out of business. No logic there. The banking cartel doesn’t care about the lowly sheep. They’re vampires and their job is to drink their blood till they’re good and dead. And in addition, the elites would love seeing a bunch of people die — Alan Greenspan has already voiced what most of them think anyway: this N.Debt was all the sheeple’s fault for wanting the government to take care of them. (Nevermind that many of us did not want that. Nevermind!) They also feel that depopulation takes care of a huge ton of problems! Well on that they’re correct.

Anyway, whatever happens, whichever way it goes, it’s going to be horrific.