The “up to” exacts its pound of flesh.

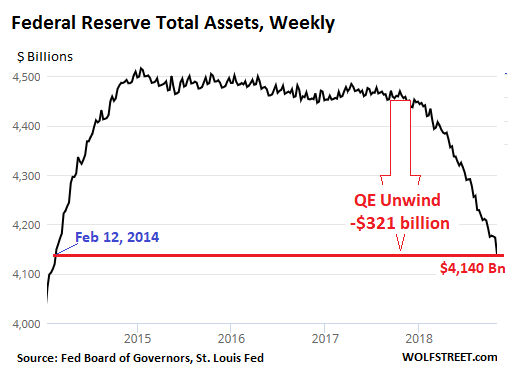

Over the four-week period from October 3 through October 31, the Federal Reserve shed $35 billion in assets, according to the Fed’s weekly balance sheet released Thursday afternoon. This brought the balance sheet to $4,140 billion, the lowest since February 12, 2014. Since October 2017, when the Fed began its QE unwind, or “balance sheet normalization,” it has now shed $321 billion:

The Fed acquired Treasury securities and mortgage-backed securities (MBS) as part of QE, which ended in 2014. Between the end of QE and the beginning of the QE Unwind in October 2017, the Fed replaced maturing securities with new securities to keep their levels roughly the same. In October last year, the Fed kicked off the QE unwind and began shedding those securities. But the balance sheet also reflects the Fed’s other activities, and the amount of its total assets is always higher than the sum of Treasury securities and MBS it holds.

October was a new milestone: the QE unwind left the ramp-up phase and entered the cruising-speed phase, according to the Fed’s plan. In the cruising-speed phase, the Fed is scheduled to shed “up to” $30 billion in Treasuries and “up to” $20 billion in MBS a month, for a total of “up to” $50 billion a month.

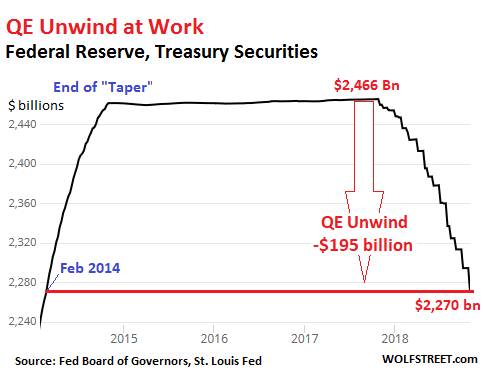

From October 3 through October 31, the Fed’s holdings of Treasury Securities fell by $23.8 billion to $2,270 billion, the lowest since February 19, 2014. Since the beginning of the QE-Unwind, the Fed has shed $195 billion in Treasuries:

The “up to” exacts its pound of flesh

The plan calls for shedding “up to” $30 billion in Treasury securities in October. But the Fed shed only $23.8 billion. Why?

When the Fed sheds Treasury securities, it doesn’t sell them outright but allows them to “roll off” when they mature, which is when the Treasury Department sends money to all holders of those maturing bonds to redeem those bonds at face value. Treasuries mature mid-month or at the end of the month. This creates the step-pattern of the QE unwind in the chart above.

On October 15, no Treasury securities matured. On October 31, three security issues in the Fed’s holdings matured, totaling $23 billion. Those were allowed to “roll off” entirely without replacement. In other words, the Treasury Department paid the Fed $23 billion for them.

But this was $7 billion below the “cap.” And it will happen again. But not in November. In November, about $59 billion in Treasuries will mature. If the Fed follows the plan with the “up to” cap of $30 billion, it will let $30 billion “roll off” and will replace the remaining $29 billion with new securities from the Treasury Department.

But in December, only $18 billion in Treasuries will mature. And that’s all the Fed will let roll off. This will play out many times going forward, unless the Fed changes its strategy, which it can if it wants to.

Mortgage-Backed Securities (MBS)

As part of QE, the Fed acquired residential MBS that were issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Holders of residential MBS receive principal payments as the underlying mortgages are paid down or are paid off. At maturity, the remaining principal is paid off. To keep the balance of MBS from declining after QE ended, the New York Fed’s Open Market Operations kept buying MBS in the market.

The Fed books the trades at settlement, which occurs two to three months after the trade. Due to this lag, the Fed’s balance of MBS at the end of October reflects trades in June through August. For October, the “up to” cap for shedding MBS was $20 billion. But at the time of the trades, in June the cap was $12 billion; and in July, it increased to $16 billion.

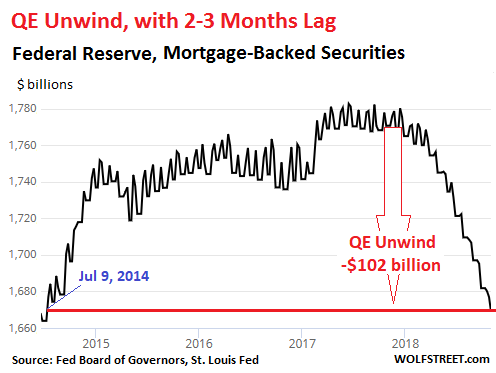

And this is what happened. From October 3 through October 31, the balance of MBS fell by $13 billion, to $1,669 billion, the lowest since July 9, 2014. In total, $102 billion in MBS have been shed since the beginning of the QE unwind:

So how does the QE unwind drain money from the market?

When Treasury securities mature, the Treasury Department redeems them, and whoever holds them gets paid face value, and the securities become void and disappear. The Fed is one of many holders of Treasury securities. It too gets paid face value when the securities it holds mature. If the Fed doesn’t reinvest this money in new securities, that money just disappears the same way it was created by the Fed to buy the securities during QE.

The Fed creates money, and it destroys money. But it doesn’t sit on trillions of dollars in a cash account.

Since the US government runs a big deficit, the Treasury Department has to raise the funds needed to redeem maturing securities well in advance by selling new securities at scheduled auctions. In other words, the bond market gives this money to the Treasury Department to redeem the maturing bonds. And the Treasury Department gives this money to the Fed for the maturing bonds it holds. And the Fed destroys this money. This is how the Fed’s QE unwind drains money from the market.

People have tried to figure out how to trade this. But there is not a specific day when the Fed’s QE Unwind drains tens of billions of dollars from the market. The drains runs from the bond market through Treasury auctions and then the Treasury Department’s cash account to the Fed. Throughout the process, the timing of the drainage gets disbursed – as does the impact on the markets.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I do have great difficulty understanding QE & it’s collateral effects (and I’m a retired CFO).

I devoutly hope the Fed is moving judiciously to recover from having bent itself (and the US economy) inside out responding to the 2007-8 disaster. I sincerely hope this give the Fed increasing capability to respond to future problems.

The ECB does not appear to be doing this, and when the next disaster hits, it will have little or no firepower.

The Fed made a mockery of asset markets plain and simple. Stocks, real estate, junk bonds. Pick your poison. By intervening in markets and preventing real price discovery (while the govt was also suspending the rule of law for elite criminals profiting from control frauds) the Fed took one mess and made another, larger mess, the consequences of which will likely last for decades. They are certainly taking their sweet ass time rolling off that balance sheet. Wake me up when the balance sheet is below a $trillion. Then we might have something resembling actual markets with real price discovery. For what it’s worth, Volcker hit the nail on the head…https://www.theinstitutionalriskanalyst.com/single-post/2018/10/28/Volcker-Rebukes-Bernanke-and-Yellen-Feds

Aaron,

I could not agree more.

The Fed should have been shedding at double its current rate more than two years ago. They were so late to begin they will not be able to meaningfully shed their MBS holdings in the next five years; but will likely be taking on more under the pretext of mitigating systemic risk in the next 24 mos.

Further, if they were remotely interested in the health of the economic system rather than supporting the players; they’d not telegraph moves but dump securities at opportunistic and random moments to keep asset inflation in check and discourage gaming the system.

Interest rates are a different part of the picture, but the part being discussed in this article is easy to understand.

There were some major financial institutions hurting for liquidity and sitting on lots of MBS that nobody wanted.

So few wanted them that there wasn’t even enough of a market to say what they were worth.

The FED bought those MBS at FULL FACE VALUE, when they could not have gotten $.30 on the $ in the failed marketplace, plus Treasuries for a total of $4T.

That $4T was deposited at the FED giving all the institutions involved more than adequate reserves, plus they got interest on those deposits.

Essentially NONE OF IT ever got into the economy, and thus it NEVER DID ANYTHING!

The reason you don’t understand it might be that it really wasn’t “QE”, it was a bailout in disguise.

“QE” never happened!

Paul,

That’s not how it worked. The numbers are off too. Plus, you’re mixing up the Fed’s temporary bailout programs (such as the Bear Stearns purchases that ended up in the Maiden Lane accounts) with QE purchases. Totally different things.

>Paul

Thank you for your succinct explanation. Yes, the radical and totally unprecedented policy of QE was essentially a bailout for the banking cartel. Great for Wall St., but not so much for Main St. The Fed is a private institution representing the interests of the banking cartel. Once that’s understood, everything else makes sense. FASB Rule 157 (mark-to-market accounting) was suspended and assets were valued at “mark-to-myth”, allowing “zombie” banks to “survive”. There was no “creative destruction” this time around. There were no “perp walks”. Only Iceland got it right after the GFC by jailing the culpable banksters. The Fed’s actions allowed further power consolidation in the financial sector, instead of having it severely limited or removed, as it should have been. QE also enabled ginormous asset inflation via ultra-low rates (bubble-nomics). This was the plan of the Fed; to re-inflate housing and stocks and boost the economy (albeit temporarily) via the alleged “wealth effect”. Since only a minority own RE and stocks now, only the top tiers of society benefited.

http://www.washingtonpost.com/wp-dyn/content/article/2010/11/03/AR2010110307372.html?noredirect=on

“For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – BB

However, a recovery plan based on credit creation doesn’t lead to a virtuous cycle, but rather only sows the seeds for another bust. “There be dragons” (consequences), and we’re on the cusp of this now in 2018 as the Fed tightens via QT until “something breaks”. Highly indebted economies are very sensitive to interest rates. We as a nation have drunk the kool-aid and allowed the Fed to replace savings and investment with debt-based growth, which only pulls demand forward for a time. Debt is not wealth and fiat currency is not a store of value. Got gold?

“Once a nation parts with the control of its currency and credit, it matters not who makes the nations laws. Usury, once in control, will wreck any nation. Until the control of the issue of currency and credit is restored to government and recognised as its most sacred responsibility, all talk of the sovereignty of parliament and of democracy is idle and futile.” – William Lyon Mackenzie King

You forgot the part about flipping distressed properties to their hedge fund cronies.

” Essentially NONE OF IT ever got into the economy, and thus it NEVER DID ANYTHING!”

Except blow major bubbles in PAPER ASSETS and PROPERTY.

The “WEALTH EFFECT” for Those who held Speculative Paper Assets and Speculative Property.

The only reason anybody could claim QE did nothing. Is if they still dont understand it.

Bit like a guy who locks a dog in a house for a week, then beat’s it, as he cant understand why it craped on the rug which he has taught it not to do.

Thank you so much for that response! I figure I’m just plain stupid and can’t understand just because! If I can’t understand what is happening I deem “it” crooked…..plain and simple…It probably isn’t but if it is too complicated for professionals to understand then, “Huston, we have a problem!!”

To Wolf R.: I love your posts and read them thoroughly including all the comments but this post pushed me off the cliff!!

There has to be a way to explain all this in real layman’s terms….comparisons with everyday life…otherwise we might be left “muttering” to ourselves!

Sweden had for MANY years minus intrest rates -0,5%. Houseprices has shot up,,,,sweden has NO defence against an economy in downfall

Thank you, Wolf for breaking down the mechanics of what the fed is actually doing. I don’t find it anywhere else.

“But this was $7 billion below the “cap.” And it will happen again. But not in November. In November, about $59 billion in Treasuries will mature. ”

Any indications that these months of excess roll-overs above the “cap” may be used to “catch-up” prior periods when enough couldn’t be “rolled off”?

I thought that the $30 billion/month was selected because this was the average monthly roll-over of treasuries going forward. What good is the average if the distribution is that lumpy – why not just make it “up to $60b”?

“Any indications that these months of excess roll-overs above the “cap” may be used to “catch-up” prior periods when enough couldn’t be “rolled off”?”

I’ve heard only one Fed governor suggest that the QE unwind should be sped up — that it’s too slow. That was in March. I have not heard any follow-up on this. But if they were to speed up the process, the way they would likely do it is by removing or raising the caps.

Fantastic piece, thanks!

One would expect Treasuries’ yields to climb as a consequence of the unwinding. Yet, it’s not happening. The 10y is not surging higher.

Investors ought to demand 5%-6% for the 10y for such a long maturity. More for the 30y. They don’t. Which probably means that Treasuries are oversubscribed.

It also probably means that investors are betting that the Fed will buckle. If only they read Wolf Street they would know that the Fed prefers a bear market in equities and Real Estate, rather than contemplating valuations reaching the stratosphere.

Don’t forget Europe is still printing. Some of that money is ending up here.

That’s supposed to end at the end of the year though.

1Q2019 is when things are going to start getting interesting on the monetary front.

By 2Q the Fed Funds is supposed to be around 2.7%.

A lot of HY debt will be coming due and will need to be rolled over, for the first time in a very long time doing so in a rising rate environment with no QE and with safe short term yields starting to look pretty enticing from a risk/reward perspective.

Can the private credit market handle this? I highly doubt it.

Max Power,

The ECB’s printing has tapered to almost nothing and will go to zero in a few weeks. The ECB’s balance sheet has been about flat since August.

Japan has backed off too.

True about the QE program in Europe…

however!

Their interest rates are still very low and their economies have not grown much- which is (my opinion) the cause of the political changes.

Europe may be very painful during the next recession; very painful.

There’s still a lot of appetite for longer (five years and more) maturities which I find frankly baffling, for no other reason the stated purpose of QE unwind is to get interest rates to move higher and like it or not yields will be higher in six months and considerably higher in 2020. Common sense and old fashioned greed would dictate buying a mix heavy on shorter maturities (under five years) and simply wait for longer maturities to raise, then change the mix composition again. There’s no shortage of treasuries coming on the market.

I suspect a lot of people still think QE Unwind is just a momentary lapse in Japanese-style monetary policies and hence are buying longer maturities to have the cake and eat it too: in short they are betting sometime over the next decade QE will restart again and their treasuries will be worth a whole lot more.

But again, it makes little sense: nobody is so patient nowadays. Just look what happens each time AAPL swoons slightly: they don’t even wait for it to lose 2% before entering panic buying mode.

I would assume that long-term treasuries are protection against an economic crash that tanks the stock market and causes the FED to lower rates.

Yo Adam – Imagining a severe economic crash brings to mind the possibility of deflation.

Debt default takes money out of the system the same as QT, and makes the fractional reserve banking system run in reverse gear, even though that multiplier effect is much lower than it used to be.

If enough debt defaulted, and the government didn’t flood the market with funny money, a $ might someday be worth something!

The holders of those 30 year Ts would then be in fat city!

Are we talking about the same stock markets whose partecipants throw a massive hissy fit each time they don’t get it their way? The same stock market which forgets what happened the day before, often literally?

Because in that cause I wouldn’t put too much faith in their farsight.

Spot on, the lingering doubts about the QE unwind/rate hikes is what drives the yield spread. That despite a new generation that reached adulthood, and does not know what positive interest rates are for.

You are largely correct.

My concern is that maybe the FED simply sets a floor under rates but doesn’t cap them.

As WR has noted in several articles recently, some 80% of government borrowing is now supplied domestically as foreign willingness to buy Treasuries dries up, and some are liquidating, a process I expect to continue.

Given very low savings rates, continued corporate and private debt escalation, I believe that soon the result will be demands for higher rates for the lenders.

Add some comments about risk to this conversation, and we might start seeing rates like the early 1980s or even higher!

The 10-year has surged from 1.4% in July 2016 to 3.2% now. That’s a massive move which is now beginning to take down the housing market. When the 10-year yield hits 4%, it will push mortgage rates closer to 6%, which will be very disruptive to the housing market at current prices.

√

Some property “Owners’ have never seen interest rates like that (6%) or had to budget for them.

This must start to impact untenable “Discretionary Spending” at some point, with an “Economy wide” follow through.

In some low credit mortgage scenarios, 6% is attained.

Yes. I’m talking about top tier. But lots of people already face those rates.

Money laundering for the banks? MBS and the complicity of the ratings agencies. Interesting times.

Anybody have a realistic (non-tooth-fairy) solution for the problem with the rating agencies?

This problem will persist as long as issuing parties pay for the ratings.

The best option I saw was all rating agencies would report to a federal agency. The federal agency would do a random pick to do the work and pay the winner. And charge back the cost to the institution wanting the rating.

Again, thank you for that response……”money laundering for the banks”…..everyone else still taking it in the you know what!

We are still laden with the hangover(s) from the GFC. Until our “banking system” is cleaned up we will in my opinion continue to operate within a “criminal enterprise system”. Apologies for repeating myself.

Loose fiscal, tighter monetary policy

Any review of tapering needs to look at the aggregate actions of the cartel central banks. If one CB is slowing down the printer, only for another to pick up the slack, it’s meaningless.

Further, the rules are being twisted and deformed ever further. If the Fed hasn’t been buying treasuries anymore, who has? Mostly the commercial banks who enjoy new rules under which they can hold them at zero risk because they don’t need to m-t-m them and don’t need to post collateral. The money printing continues unabated while the next gigantic moral hazard is metastasising in the system.

->The money printing continues unabated while the next gigantic moral hazard is metastasising in the system.

Agreed. Nothing has really changed since 2008.

The cobwebs were never cleared and the distortions were never resolved, as we are led to expect happens in a financial correction and economic recession. They’ve simply been taken over and firewalled by the Fed to keep the disastrous effects from affecting the markets, allowing the markets to continue on their merry way. But they’re still there. It’s expensive to do that, but the Fed has assumed the costs.

Now the Fed is unloading those costs and that firewalled toxic waste back to the markets and the economy, a bit at a time so as not to upset the applecart. But in the meantime the old bad habits have generated more cobwebs and more distortions, the same kind that caused the 2008 debacle. It all looks good so far but it’s all a debt-fueled binge, just like before.

Economic distortions are always expressed, one way or another, and instead of being expressed as inflation, they’re being expressed as debt and asset bubbles all around. From here it looks like the US is doing the macroeconomic equivalent of paying off one credit card with another, while borrowing even more so it can pretend that it is rich.

Debt is growing faster than GDP, a lot faster. The economy isn’t growing out of its debts, like it did after WWI, because it can’t. Profits are largely siphoned off, misallocated, or buried in the backyard in offshore accounts, leaving the debts behind unpaid. That’s how the incentives are structured. The best the economy can do is keep up with the interest payments, but those are rising too, not only because of Fed interest rate policy but because debt has to keep increasing to keep the economy going and make it all look good.

So the Fed is unloading into an environment that is already awash with debt and getting worse. It can’t last. Sooner or later the Fed will have to reverse course, firewall the latest load of toxic waste with the last one, and just hope the containment unit doesn’t fail.

How does this not end in disaster? What am I missing here?

It amazes me on an ongoing basis how people and markets persist in behaving as if the exponentially increasing debt loads are remotely sustainable, and (willfully?) keep their blinkers on whilst looking at whatever GDP growth figures can be manufactured by draining and consuming the equity on the balance sheet.

The situation is also similar across different political regimes around the world, and yet people everywhere appear to believe that a solution to solve their downward spiral and to unlock unbounded future prosperity can somehow be brought about through political changes in their particular circumstances, usually involving going deeper into debt at an accelerated rate in order to spend on programs that can never support themselves in real terms.

I keep waiting for the moment people will wake up on a broad basis and see that the future is one of contraction and not of growth as we catch down to the reality of our drained balance sheets and our screwed up and depleted natural environment.

Saltcreep

You (and I) have a bias that too much debt will end badly. The question is “end badly for whom”?

Until there are actual consequences for bad behavior to responsible individuals, why should someone (or a governmental agency) change their behavior?

Individuals can declare bankruptcy roughly every 8 years.

The pain is generally felt by individuals other than the ones directly responsible for the debt:

o Credit card loss reserves (increased cost) are generally funded by incremental charges to incoming payment streams.

o Politicians cause/allow underfunded pension systems; pension recipients (who may receive reduced benefits) and general taxpayers (who fund Pension Protection Fund) pick up the pieces.

Throwing people in jail for debts isn’t the solution; there should be some forgiveness. However, there should also be some change in behavior on the “forgiven”. Petunia, a frequent commenter on WOLF STREET, has often spoken of the impact on her life from financial issues beyond her immediate & direct control.

I see no such response from politicians.

JC

“Until there are actual consequences for bad behavior to responsible individuals, why should someone (or a governmental agency) change their behavior?”

This point is pretty important, I reckon. The link between causes and effects is so (deliberately..?) obfuscated, distanced and drawn out in time in most cases that high level actions don’t carry with them any real sanction on perpetrators for significant negative consequences.

There are also built in incentives to conform and break with principles for all of us. I will quite freely admit that I too am an enormous hypocrite; For example I am scared as hell about climate change, and yet I live in a way which contributes to the problem and I have taken on contracts both from the oil industry and the automotive industry, quite simply because I’m also scared of the prospects of future loss of security and dignity for myself and my family.

Further, I reckon this is an effect of living in a highly complex and fragile society where people are dependent upon larger and more distant machinations, where we have little ability to sustain ourselves independently or locally. We then conform in order to try to preserve our security instead of standing by our views and principles through actions.

“How does this not end in disaster? What am I missing here”?

Picking any one catalyst as the cause of a bubble bursting is misleading, as it is merely the symptom of a much larger multi faceted slower breakdown, that starts to burst years before.

The market participants (and general public) labor under the misconception that the central banks will ride to their rescue. With mountains of liquidity injections, only this mountain is composed solely of debt!

Value destruction will be complete, causing a slow fall in asset prices as what is occurring now. Look for this slow motion train wreck to continue for years, as it has in Japan.

Widespread stagnation of global economies with much pain.

Does it really matter? I mean, even if they go down 1T, they will go up whatever necessary next time, maybe 8-10T. The debt clock will be around 40T and counting, rates will be 0 or bellow, that will be the new normal. I am old enough to remember when we hit 5T debt, the sky was about to fall, then 10T, all super-volcanos where about to erupt at the same time. And still here we are, above 20T and no one seem to really care, the talk is the same old, same old… I remember someone saying “everybody is talking about the breaking point, now I am wondering if there is a breaking point?” Wolf, maybe you can tell where that mystical breaking point could be found? Thanks for your thoughts.

“everybody is talking about the breaking point, now I am wondering if there is a breaking point?”

I too have been wondering this. Granted, I dont know nearly as much about this topic as the other commenters, but it seems that this will just keep going until the music stops. what happens then?

So everything is absolutely perfect. despite FED QE unwind, everything is going up. Fuel prices threatened a bit but now have eased off.

So everything looks so rosy and the future has to be mere perfect. Looking at the Japanese Central bank was able to manage thing so long, I guess we may not see a recession in at least five years time.

So technically FED has done a good job, I guess!

I like the Fed under Powell. They seem to want to do what they say, and say what they do. I think the US may come to appreciate what it has here in a crisis, and a crisis is coming (sometime). To me, despite all the talk, the other major central bankers have no creditibility, their future plans lasting as long as the first squawk from their political masters or wailing from market traders. The Fed’s integrity is growing or healing itself after Bernanke and Yellen.

To me, the interesting point will occur when the Fed needs to start buying US Treasuries again to cover the deficits caused by a Congress and Trump only being able to agree on spending more money and cutting more taxes. Supposedly they are already talking about another $trillion tax cut for billionaires (but of course promoted as a ‘middle-class’ tax cut).

This works as long as the market is willing to buy the ever increasing number of US bonds required to cover Trump’s ever increasing deficits. But when that limit is reached, the Fed will start buying again.

Poco

As long as you (we) view the debts as Trump’s or Obama’s this will never end.

We the people (the voters) are 100% responsible for this mess. We demand, allow & reward politicians who overspend. Net of credits, about half of all W-2 wage earners pay $0 Federal income tax (FICA & Medicare = yes, but they are not income taxes).

The last round of tax changes INCREASED Federal taxes on the rich, but governors in California, Connecticut, Illinois, New York are actively & publicly attempting to work around the SALT limitations (primarily impacting wealthy individuals). They do this to keep rich taxpayers in their state & paying their state taxes.

Even the tooth fairy can’t fix it so you have it both ways.

I enjoy these regular updates, and they are quite informative. But I do wish Wolf would include one graph showing the overall pattern since the 2008 crash. That way, we’d see the overall impact of the Unwind upon the total curve of what the Fed done. From the numbers, while $320 billion sounds like a big number, its less than %10 down of the total. I guess that means that haven’t yet officially entered a ‘correction’ scale dip.

QE took many years, and the QE unwind will take many years. As I explained in a prior article: even before QE, the Fed’s assets were growing at a rate related to the growth of the economy, and at this growth rate, the Fed’s assets would have reached about $1.5 trillion by 2022.

This is about when the QE unwind draws to a close — give or take a year — because the Fed’s asset will be close to where they would have been had QE never occurred.

People forget that the Fed’s balance sheet has always grown along with the size of the economy. This is not going to stop. And that’s what matters. So check out the article, bottom third:

https://wolfstreet.com/2018/09/06/fed-qe-unwind-250-billion-when-will-balance-sheet-normalization-end/

Wolf

Please comment about the interest that the Fed was paying to the Treasury on the 4.5 Trillion. Those are going to be less and less also… Right?

It’s the other way around: The Treasury Dept is paying the Fed interest only on the Treasury securities the Fed holds, currently $2.27 trillion. As the Fed sheds these securities, it receives less interest payments from the Treasury Dept.

But the Fed remits most of its profits back to the Treasury Dept. So part of the interest that the Treasury Dept paid the Fed, the Fed remits back to the Treasury Dept.

But the Fed is also paying the banks interest on “excess reserves.” That rate has been rising with every rate hike. Excess reserves are falling, but the interest rate is rising, and so the Fed is paying the banks a lot of money. This comes out of the money the Fed would have remitted to the Treasury Dept.

The Fed releases this data in January, and I’ll cover it. So stand by :-]

All those digits and in reality, empty, like our wages.

And now a word about lemmings.

The urban myth about lemmings offing themselves was popularised after this behavior was staged in the Walt Disney documentary “White Wilderness in 1958.”

However, the animals in the film are not wild animals jumping off the cliff voluntarily, rather they were bought by the producers and pushed over the edge of the cliff.

The lemmings were not happy.

Unlike lemmings, people can be bribed to happily jump off cliffs. Figuratively speaking, of course.

Unlike people, lemmings never have financial crises.

The FED setting rates is the largest price fixing scheme ever invented. We have laws against price fixing, but somehow setting the price of the most important input into economic decisions, aka money, is different? Nope. Economic freedom seems to have ended approximately a century ago the eve of Christmas eve … by globalists before globalism was cool.

Cui bono? That this is still debated shows how ingenious it was.

Wondering about the degree of collusion that exists across the CBs around the world. The US appears to be acting alone (after a break) and it cannot be popular.

Cui bono?

I’d be a hell of a lot more concerned if I saw central bank bureaucrats & governors getting filthy rich during their tenure at, say PEMEX in Mexico, PDVSA in Venezuela, PERTOBRAS in Brazil, or almost anything in China, India or Russia.

Until you can demonstrate that the MBS maturing is not being replaced with new MBS held in some other account the assumption about liquidity going anywhere is false. When securities are held at the Fed they have the US taxpayer guarantee (implied). It has nothing to do with more or less debt in the system. Corporate debt is having an issue, due to rising rates at the long end, not caused by Fed rate hikes but the dollar, which the Fed is propping up with rate hikes. The unwind has become a non-starter, rates are rising for other reasons, and debt in the aggregate is always expanding

“…that the MBS maturing is not being replaced with new MBS held in some other account”

Are you fabricating theories to fit your narrative? The Fed discloses all this data. All you have to do is look. The MBS that are part of QE are in one account. They’re not being shuffled around to avoid detection or something. You can download the spreadsheet of the Fed’s MBS holdings. This includes details such as CUSIP number:

https://markets.newyorkfed.org/soma/download/821/mbs

All this data is published.

How much MBS is there outside the Feds purview? Its akin to the problem of unregistered derivatives. In 2008 they didn’t know they probably don’t know now? Then it was a quality issue, now its more of an interest rate issue. How does this affect the legal definition of home ownership, as long as the Fed owns the MBS, that means taxpayers, and that’s as good as any GSE, for legal purposes. When MBS goes off the reservation title becomes a lot murkier. Sometimes i fabricate theories late at night when I can’t sleep.

How does the destruction (or creation) of money work from the perspective of accounting at the Fed? Does it just sit on the books? Or do they mark it down (or up)?

I’ve read a lot about how it works from the perspective of the economy at large. Curious about the other side of the ledger.

You can check out how this works. Here is the accounting manual of the Federal Reserve (220 pages of special central-bank accounting rules that deal with the otherwise strange things that central banks do on a daily basis):

https://www.federalreserve.gov/aboutthefed/files/bstfinaccountingmanual.pdf

“220 pages of special central-bank accounting rules”

My brain glazed over at page 26. I bet nobody ever reads it anyway.

You are supposed to read 1 regulation or group, absorb it, then another.

Thats how they trained us when banking was about PRUDENT banking, as opposed to today, where it is about defrauding people.

…Just to remember Black Rock was able to get 50k houses at pennies on the dollar. We were waiting to get a deal on a home after the crash and never got the chance. Even at the bottom, the places I wanted to Fl were still 2x what I was thinking it was with to me.

https://www.forbes.com/sites/antoinegara/2017/01/06/blackstones-big-bet-on-the-u-s-housing-recovery-files-to-go-public/#7494b95f3dba

—

Hate to say it, but as far as ‘Paying the piper’ I think all these guys are just hoping to kick the can down the road for 15-20 years as they would have profited handsomely and never had to pay Mr. Piper….and no, most people I talk to don’t have a clue what debt or potential catastrophe lies ahead for their grandkids. ( “what do you mean Timmy graduated 150k in debt. It was only 2k in my day” ). Great Aunt just got a double hip replacement at 86. 3 weeks in Hospital. Think the Medicare she contributed equals anywhere near what that costs?…Doesn’t know doesn’t care..I want mine!

There’s nothing wrong with your TV, we control the horizontal and vertical. Trust us to preserve your life savings and feel confident in investing in the generations of the future (who BTW, call you q-tip).

….and just when I was reading more about this scam….

https://www.businessinsider.com/a-massive-buy-to-rent-scheme-is-hitting-the-housing-market-2018-8

It has replicated like a pandemic, and even getting pension funds to fund them,…should end well. Thanks Wolf for the research and illumination on this largely hidden menace ahead.

Sadly I still have friends tell me “They fixed it and wouldn’t let it happen again”

…surely we are toast.

I see the 10 year rate popped back up to 3.21% today and the stock market had only begun recovering from the big October drop. That’s a sign to me that there’s a lot more pain ahead for the stock market, probably next week. Every time rates pop up, the stock market seems to take a dive a day or two later, for good reason.

The Fed needs to stick to its interest rate increases because that is the only thing preventing asset prices from rising to the sky, then bursting like a firework.

Rates come back down when the stock market players pull money out of stocks and park it in bonds and gold. Hard to say where rates would really be without the stock market selloff. The Feds purpose it to redirect those stock market profits into new bond issuance attached to fiscal stimulus, where it can again be recollateralized and used to buy stocks. It might be an orderly process (as they see it) however the global dynamics suggest there are already too many bonds in circulation and too little real investment.

Understanding QE.

The economic stimulus comes from Govt running trillion dollar deficit each year. This money is spent on stuff (weapons + medical expenses), salaries and pensions. One trillion dollars of real stimulus gets injected into the real economy.

If the govt had to borrow the trillion from the existing credit markets, interest rates would have go UP to accommodate all the new borrowing thereby partially negating the effect of the stimulus.

Instead QE has the FED print the one trillion and buy the debt from the govt. In doing so there is no extra supply of debt dumped on the credit markets (the fed bought it all) so interest rates DON’T rise. In fact with all this extra money in the system chasing limited debt instruments, reaching for yield…it causes interest rates to go DOWN.

This causes asset inflation and eventually consumer inflation.

Hi Wolf,

Any thoughts on why the Fed isn’t managing this roll off process better? That is, it knows how much treasuries are scheduled to mature each month. Why didn’t it e.g. buy enough 1-year treasuries in Oct. 2017 to ensure that there would be enough maturing securities in Oct. 2018? Or knowing that November has an excess, roll some of that over into short-term paper that will mature in Dec. and Jan. to help make up shortfalls in those months?

It seems like the Fed spent most of the end of last year, and all of this year, hand-wringing about how the yield curve was about to invert, when they could have killed 2 birds with one stone by buying short-term securities that would mature this year and next during the QE rollover. That would have steepened the yield curve *and* allow them to manage this unwind process better.

Any reason why this strategy wouldn’t work or would be harmful?

To me, it looks like the Fed is trying to extricate itself from the total interest rate manipulation since the Financial Crisis. It’s gradually trying to let the market find rates without at the same time collapsing the market. So if it started buying this and selling that, it would be steering the market in a certain direction. This is what it did after the Financial Crisis. But to me, “normalization” seems to be focused on allowing realistic, market-based yields to exist again.

Nah, I believe they have no problem with crashing the market so their employers can reload low priced securities.

Why does nobody think the FED is a criminal organization, must be their web site income depends on not saying this??

To be a “criminal” or “criminal organization,” you’d need to violate some kind of criminal law. So which US criminal law, or even state criminal law, is the Fed violating?

” If the Fed doesn’t reinvest this money in new securities, that money just disappears the same way it was created by the Fed to buy the securities during QE.

The Fed creates money, and it destroys money. But it doesn’t sit on trillions of dollars in a cash account.

And the Treasury Department gives this money to the Fed for the maturing bonds it holds. And the Fed destroys this money. This is how the Fed’s QE unwind drains money from the market.”

So let me get this straight? The Fed creates money out of thin air, and then vanishes it into thin air? Where can I learn and utilize this form of magic?

“Where can I learn and utilize this form of magic?” Become a central bank :-]

Old MBS rolls off and new MBS arrives, like the days of our lives. Some lives are shorter than others as rates cause MBS to mature sooner. read this weeks http://creditbubblebulletin.blogspot.com/

Please draw your graphs starting at zero to show what a pinprick their “unwind” actually is. 321 billion down, only 4.14 trillion more to go… which will never be reached or even closely approached before the next crisis.

Winston,

“Only 4.14 trillion more to go” to zero. Time for a little info.

Zero doesn’t even exist in the data. The Fed since day one (over 100 years ago) has always owned assets, including gold, and those assets have increased with the size of the economy.

The first publicly available balance sheet, dated June 1996 showed $430 billion in total assets. In today’s dollars, that’s $703 billion.

By June 2006, the balance sheet had grown to $845 billion. In today’s dollars, that’s $1 trillion.

Without QE, the Fed’s balance sheet would have grown to $1.5 trillion by 20222.

The QE unwind will never take the balance below where it would have been without QE. And to say that the balance sheet should go to zero is totally nuts.