Seattle prices fall sharply. New York condo prices nearly flat for the year. First feeble declines in San Francisco, Dallas, Denver, etc. Something is afoot.

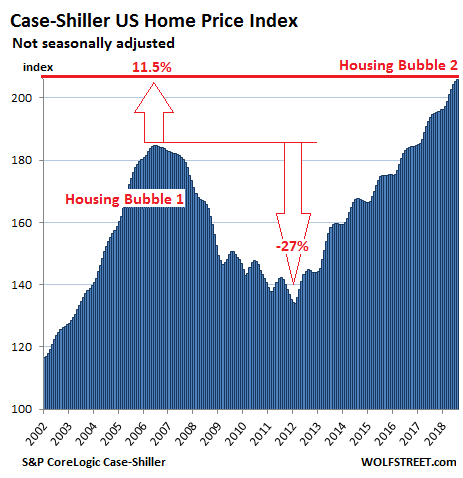

On the surface, it still looks strong. Single-family house prices in the US rose 5.8% in August compared to a year ago (not seasonally-adjusted), according to the S&P CoreLogic Case-Shiller National Home Price Index released this morning. This growth rate has been declining and now has fallen below 6% for the first time this year. The index is 11.5% above the July 2006 peak of “Housing Bubble 1” in this millennium, which was called “bubble” and “unsustainable” only after its collapse. But we forget, and now, this peak of the collapsed bubble has become the new-normal base of a “healthy” housing market. The index has surged 53% from the bottom of “Housing Bust 1”:

The Case-Shiller Home Price Index lags behind by design. It is a rolling three-month average; today’s release is for June, July, and August. The index is based on “sales pairs.” It compares the sales price of a dwelling in the current month to the last transaction of the same dwelling years earlier. The index incorporates other factors and uses algorithms to arrive at each data point, but it does not provide dollar-price levels, as a median price index does. The index is focused on single-family houses but has some special sub-indices for condos. It was set at 100 for January 2000; an index value of 200 means prices as figured by the index have doubled — which they have for nearly all metros on this list.

The index is not inflation adjusted but is itself a measure of inflation — not of consumer price inflation but of asset price inflation, specifically housing-price inflation. It shows to what extent the dollar is losing purchasing power with regards to buying the same dwelling over time.

For a few months now, we have seen the first indications in some of the hot local housing markets that fundamentals are deteriorating: Declining sales, rising inventories, increasing number of days on the market, and the like, though their prices as measured by the Case-Shiller Index hadn’t turned. Seattle was one of them, but now prices are decidedly turning in Seattle.

So here are the most splendid housing bubbles in major metro areas in the US:

Seattle:

Oh-la-la! After a historic spike, Seattle metro home prices performed a vile and unthinkable act: They dropped 1.6% in August from July, down 1.6% in just one month! This comes after they’d edged down a bit in July from June. Over both months combined, index lost 2%. This decline, after the spike, took the index all the way back to, well, April. The month-to-month decline in August is particularly interesting because the August readings (for June, July, and August) are seasonally not weak, and price increases were the norm in every August since the housing bust, except 2014 when the index remained flat.

So now the scenario is changing in Seattle. This likely confirmed the inflection point I noted last month. Over the past 12 months, the index is still up 9.6%, but that’s down from the 12.0% year-over-year increase of the July reading. The index is up 31.9% from the peak of Seattle’s crazy Housing Bubble 1 (July 2007), but that reading too is down from the 35% jump in the July reading:

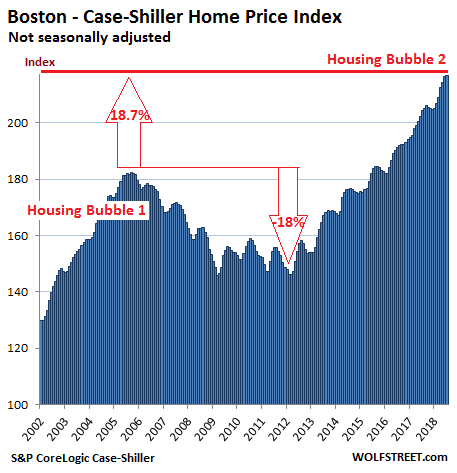

Boston:

Case-Shiller Home Price Index for the Boston metro in August is essentially flat with the prior two months. It rose 5.4% from a year ago, down from a 6% pace last month. During Boston’s Housing Bubble 1, from January 2000 to October 2005, the index soared 82% before dropping. It now exceeds that crazy peak by 18.7%:

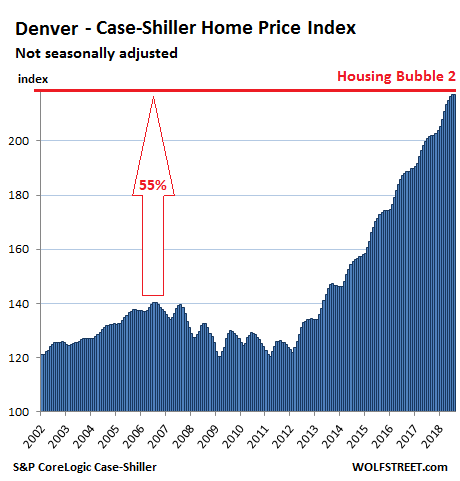

Denver:

Denver metro home prices declined a fraction in August from July, according to the Case-Shiller index, putting an end to the series of 33 monthly increases in a row. The index is up 7.7% from a year ago (down from an 8.0% pace last month) and 55% from the peak in July 2006. Note the flat spot at the top:

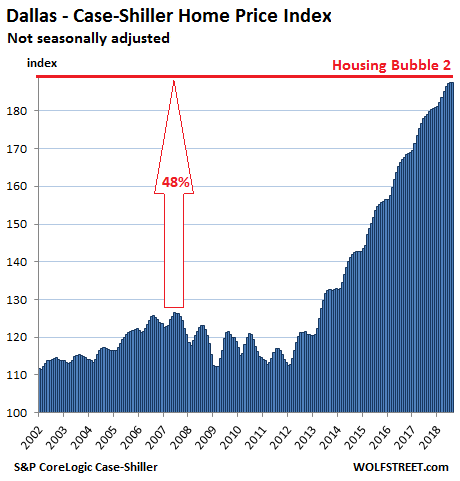

Dallas-Fort Worth:

Oh dude, Dallas too! Home prices in the Dallas-Fort Worth metro unthinkably inched down in August from July, putting an end to the glorious series of 54 monthly increases in a row. The Case-Shiller index is up 4.7% year-over-year, but that’s down from the 5.0% pace in July. Since its peak during Housing Bubble 1 in June 2007, the index has surged 48%. Note the flat spot at the top:

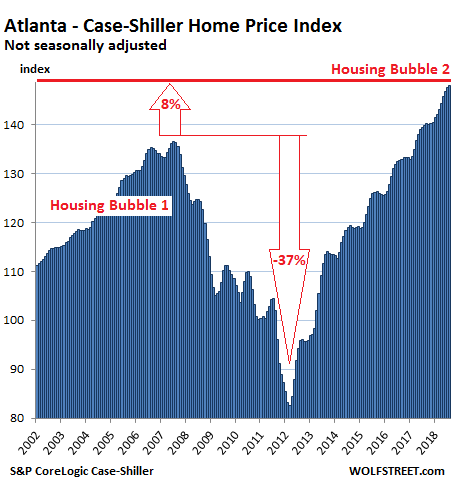

Atlanta:

Still on track: Home prices in the Atlanta metro rose 0.3% in August from July, according to the Case-Shiller index, and 5.8% over the 12-month period. They exceed the peak of Atlanta’s fabulous Housing Bubble 1 in July 2007 by 8%:

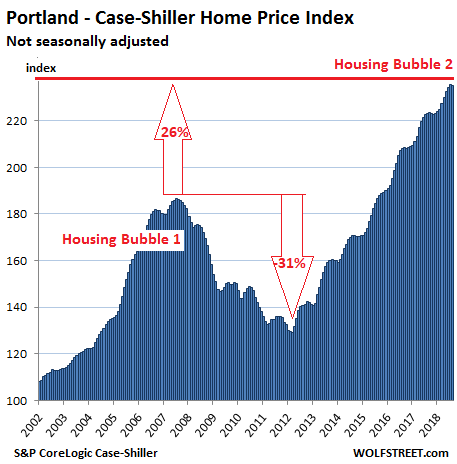

Portland:

And Portland has the malaise too. The Case-Shiller index for the Portland metro in August edged down a smidgen from a month earlier. The index is up 5.4% year-over-year (down from the 5.6% pace in July), 26% from the crazy peak of Housing Bubble 1 in July 2007, and has soared 135% since 2000:

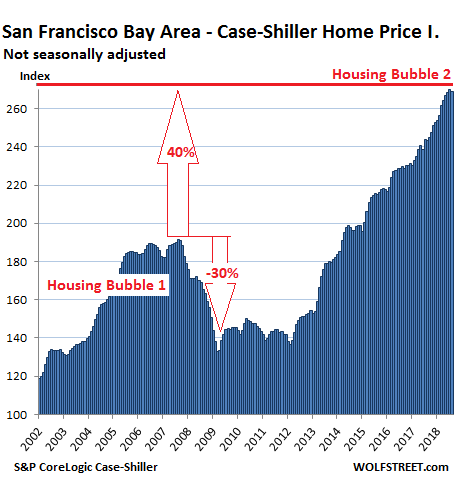

San Francisco Bay Area:

And in San Francisco! The Case-Shiller index for “San Francisco” includes five counties: The city/county of San Francisco, the northern part of Silicon Valley (San Mateo County), part of the East Bay (the counties of Alameda and Contra Costa), and part of the North Bay (Marin County). In August, the index fell 0.3% from the prior month, but was still up 10.6% from a year ago (down from the 10.8% pace last month). It’s up 41% from the peak of Housing Bubble 1 and up 169% since 2000:

Condo prices for the five-county San Francisco Bay Area, which the Case-Shiller index tracks separately, follow a similar trajectory as house prices, except they have now declined for the second month in a row on a monthly basis, and are back where they’d been in April 2018.

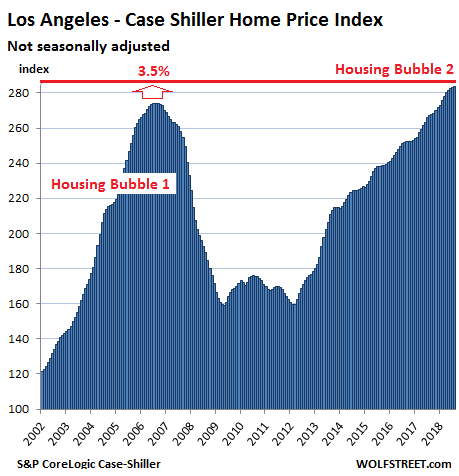

Los Angeles:

The Case-Shiller index for the Los Angeles metro rose a tad in August and is up 6.2% year-over-year (down from the 6.5% pace in July). Between January 2000 and July 2006, the index had ballooned 174% before its collapse. The index now exceeds the nutty sugar-loaf peak of Housing Bubble 1 by 3.5%:

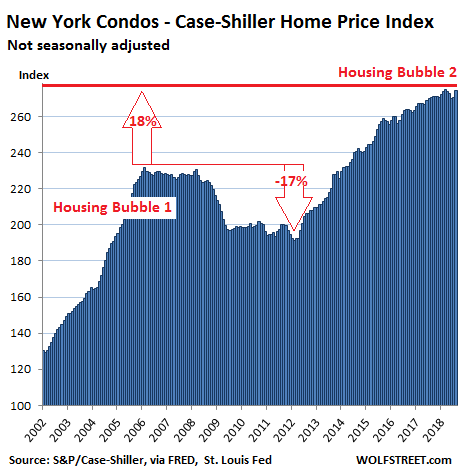

New York City Condos:

Condo prices in the New York City metro jumped 1.4% in August from July, after several months of declines, according to the Case-Shiller condo index. This took the index back to the February level. It remains down a bit from the peak in March, but is up 1.3% year-over-year. Note the rough flat spot at the top now extending back through February this year:

The Case-Shiller data covers other cities that have not yet reached prior bubble highs, such as Miami and Las Vegas, and so these cities don’t yet fit into the theme here of the “Most Splendid Housing Bubbles in America.” Some day they might. But by then, the index for some of our lead contenders here might already be heading south. And this would be typical too: during Housing Bust 1, prices in some cities turned in early 2006 and in others in the latter part of 2007.

However, there are many equally or even more splendid housing bubbles in cities that the Case-Shiller data does not cover, such as the blisteringly hot Nashville metro. So these cities cannot be included here. We miss their continued absence.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If you’ve been “fortunate” enough to purchase a home in my state in the past six months there’s a good chance that it’s already worth less than what you paid for it. ouch

This only hurts if you were in some way reliant on the value of your house being higher year over year.

Generally if you are being reasonable when buying a home. You should be okay in most scenarios where the value falls for an extended period of time.

Because you bought the house to live in, and were comfortable living in it for more than 5 years and hopefully more than 10.

Granted even the conscientious buyers can get bit by a long term loss of value if there is a perfect storm. But losing value alone should not be a reason to fret.

My x bought a house in 2005..(i begged her not to) and bragged about how much it was going up every month until it didn’t.

she sold it in 2016 for $30K less than she paid for it.

The house we sold in 2005 history…..i’m looking at zillow.

2005 sold $459K

2011 listed for sale $195K

2018 sold $440K

so maybe in a normal market the buy and hold works but not in socal……..timing is everything.

AND if the government and the FED would stop playing their games maybe we could find out what assets are really worth.

I’m in south Orange County, our home lost about 30% by 2011, but today would be valued about 95% of 2006’s high. So recovered most of the drop. Pretty close to your 2005 / 2018 data.

Lion, remember that there are nominal, not real prices. At 95% of the 2006 price you are still more than 30% off the 2006 peak in real terms.

Nominal “price recovery” is almost meaningless. Today’s median incomes have risen 30% in nominal terms since 2006.

“Today’s median incomes have risen 30% in nominal terms since 2006”

take out the very top and take out the very bottom (who HAS gotten a 30% increase due to minimum wage insanity) and that figure is probably negative. I haven’t had a raise since 1997….self employed. I’ve actually had to lower my shop rate to compete with china and these shitty trade deals.

I don’t know a single person who has had a 30% raise since 2006…..not one.

How can you possibly be reasonable when buying at the top of a real estate bubble? And you’ve tied up cash on a down payment that you will not recover until (if) the housing market ever comes back?

Begbie that’s how it was in 06; a long slow bleed and then things got bad in 07-08.

When housing bubble 1 was happening, I was a novice to the whole market. Just out of grad school with a good job and two six figure incomes. My initial feeling when looking for a house, was “Who can afford this?”. This was in 2008 BTW. I mean, I couldn’t wrap my head around the fact that we were in the upper end of income for our area of FL, but the numbers just didn’t add up to buy a modest house or even a condo.

Fast forward to today, and I’m having the same feeling. Although I’m now a happy permanent renter, I look around my area and see that it would be really tight to buy anything. I see the people who do own homes… nice neighborhoods with newer construction… these are couples making 50% or less than us. It just does not add up. Something has gotta give.

Freedom

Here is what’s going to give. Those who make less than you but dare to borrow more than you do and live in a larger house, will default and walk away once it busts. Then the “soeicety” will look around and find that you have the savings. So they will ask you to pay your “fair share” to rescue the banks and the country. That is the game, and that is what gives.

After experimenting with various lifestyles (from trailer park to McMansion; $500 beater to high-end sports car) , I’ve learned that I am a content minimalist. Give me my friends, my books and good running weather, and I’m happy as a pig in s#!*. So, society can do as it pleases with housing and bailouts or whatever.

hear! hear!

Opting out. A great concept.

You rule!. I wish I had had the guts to be true to my minimalistic nature 20 years ago, instead of being pressured into things that don’t really make me happy.

I know a couple who lived 48 months mortgage free and the bank even paid their taxes.

This is not capitalism by any stretch.

That’s nothin! One guy in my parents gated community lived mortgage free for 8 freakin years before finally being foreclosed on. Also stiffed the HOA $25K…..and get this another family also lived mortgage free for 9 years, sued the bank, and just got paid a settlement of almost $50,000 (so they say) and also stiffed the HOA. The settlement did make them turn over the house though and they rented down the street. Lucky bastards.

Responding to this Oct 30 post and more appropriately the Oct 31 post, you are not alone. In fact this is a symptom of the existing culture of the 21st century. See https://www.youtube.com/watch?v=nnYhZCUYOxs for an explanation and why it will remain the same.

Because of the fallout from the last bubble its impossible to gauge the financial health of many neighborhoods.

What I mean is plenty of people in a neighborhood may have been able to purchase what is now an overpriced home for less than the cost of a 2 bedroom condo.

Also a lot of people are willing to commit a large sum of their income to housing. These are the people you are probably rightfully concerned about.

Two six figure income households though can still swing a fairly expensive home. At least in the $700-$900k range on average in SoCal.

Should they? That’s a different question, but dual professional income households, willing to commit a tremendous portion of their income to housing, are probably a large part of what has let current prices inflate so high.

>Also a lot of people are willing to commit a large sum

>of their income to housing.

Yes, as long as home prices continue going up. Otherwise they’ll just return the keys. Shameless.

*California = Walkaway State.

Many of my friends are living in million dollar mcmansions.. driving 100k teslas.. but get little more than 6 hours of sleep and kids are in day care every day for 10 hours or so..

They need 2 income to support their lifestyle

Such a miserable lives and I pity the kids especially

>>>”dual professional income households, willing to commit a tremendous portion of their income to housing, are probably a large part of what has let current prices inflate so high”

Most buyers in CA, esp dual income professional, are porting equity from another home that has seen significant appreciation. If you look at Census migration data, people moving to CA are largely high income, coming from places where housing costs are high. Those leaving CA are low income, and move to lower cost areas.

I am sure there a few first time buyers paying $800k, but that is probably a low percentage of overall sales at that price level and above.

what did you study, I did economics what pays 2 6 figure incomes. The true value of a house is how much rent you will be collecting or how much rent you wont be paying given you own the house. say the rent for the home or something similar is 26000 dollars a year in rent, divide 26 k into 0.05 (your preferred return) and you get $520 000 is the true value of the house.

I would guess healthcare field.

Molecular biology / biochemistry. Specializing in genome engineering. Cancer med development.

Nathan, I agree about the “true” monetary value of a house. But, there is a lot of hidden expense that further cuts into that value. Seems like everywhere has an HOA now, so there’s that cost plus the lost return on investing that $. There’s maintenance big and small. Lost time on things like lawn care. Pest control. There are taxes. But a huge one for me is immobility (especially in a dropping market where it becomes challenging to sell a house). I’ve moved so many times to my career advantage. I can’t imagine what it would be like if I tried to buy a house every time I settled down. Once was enough. Learning experience.

6-7 years post secondary + student loans. That salary should be very high, indeed. People, all wage earners regardless of collar colour, are underpaid compared to the financial/owner cartels taking their suck off the economy. (Halloween theme). What is expected as normal that people will and do pay for housing, as a portion of their salary, is outright criminal, imho. Scary.

Thanks, Nathan this formula is very helpful. I appreciate your expertise. Peggy

Should have bought in 2011 or whenever housing became affordable for you. You’d be sitting pretty now and not wasting thousands on rent each month, it would be going towards paying down the principle and then you’d open the home outright eventually.

I’ve moved twice since then.

Also, and this is a big one for me, time is everything. It’s our only truly valuable resource in a life. I hate wasting time more than anything. So I choose to keep my commute to basically nil. I can easily rent in this zone in most regions where I would work, but purchasing becomes extraordinary expensive in proximity to desirable employers.

Wolf,

I see you have excluded Chicago. As a resident of the City, I am well aware of the various issues that have limited our participation in this price advance, boulder would still appreciate some quantified data.

Please and thanks

Hi Richard,

Also a Chicagoan. Chicago has the 2nd most construction cranes being used in the US today (Seattle is #1). I am sure you know that the construction boom in Chicago is huge, with more plans to increase it (Lincoln Yards).

However, as far as homes go, Chicago is only building luxury homes. All this is going to blow up in their face. Especially since 26,000 people have moved out of Chicago last year. Chicago is building 77,000 luxury units.

Yet our HOA and Property taxes remain so high even compared to NYC.

To make a long story short, Chicago is not in a bubble like the cities mentioned above. My own theory suggests that chicago is in a bubble for new homes. Not for existing homes. These new luxury condo prices are going to collapse, while you’ll see the prices of existing homes go down, but not as drastically.

I’ve been looking for people from the Chicago area to have these conversations with. feel free to email me at [email protected]

Wolf, any feedback from you if you looked into it at all would be helpful. Love the work that you do. Would also love the opportunity to speak to you as well.

Joe,

You’re correct. After a truly magnificent Housing Bubble 1, the Chicago metro never quite got to an overall Housing Bubble 2, though it is trying.

Given the vast size of the Chicago metro, this has a big impact on the national home price index. Metros like Chicago that have been lagging behind in their housing bubbles recently are the reason the national index hasn’t spiked like specific indices have.

This suppression of chicago bubble 2 is the direct and sustained result of real estate taxes that now exceed 3% of market price in the metro area and 2% in the city proper. People can afford x$ per month and taxes are taking increasingly larger chunks of X.

In conjunction with the slowing of home price growth: –

We have the Smart Money Flow Index back at 1996 levels!

Now why would the smart money be fleeing the markets at this high of a pace? Could it be they see something that the vast majority do not?

Like maybe an impending steeper correction or crash?

Synchronized popping of all housing bubbles is well underway, with the surprising laggard being USA. Even central bankers can’t time it perfectly in synch, but I bet they’d say they planned it this way.

Nevertheless, house prices everywhere from USA to China will do nothing but drop from now on.

Own real estate in SW Fla. So far so good.Rentals on the beach in high demand in peak season usually pre-booked 6 to 8 months in advance.Do not rent our unit but requests to do so are many. In our area rental income covers condo fees taxes and mortgage expenses.Building around us is annoying .Small cottages on the water are being flattened 4, 5 ,6000 (some even larger)sq ft units popping up blocking the view from the boulevard.Restaurants are packed from December to April decent volume in the pre season as well. Might just be the boomers wanting to be warm.

Wolf, thank you again for sharing your incredibly informed mind.

When prices go down, especially in expensive purchases like RE, sellers intensify the incentives. Either directly to prospective buyers or indirectly to their brokers.

I doubt the commissions sellers pay to brokers are published anywhere but it seems obvious that brokers respond positively to commissions.

Is there an indirect way to assess whether or not sellers are jacking up commissions in order to incentivize brokers?

Developers of new housing rely on their in house staff to maximize profits until a market turns.

At that point they start offering “Broker Co Op” or a commission to any agent who brings in a buyer.

They also start offering “Free Upgrades”.

Two local subdivisions are offering the office that brings a buyer 5% which is twice the usual commission.

Three more are offering 3% commission.

Three also offer “Free” upgrades.

Individual sellers just reduce the price to where a house will sell.

Buyers know the market, as an agent I’d be wasting my time showing an overpriced house to a client.

It doesn’t matter if you offer a 25% commission, buyers have access to enough information that they can tell if a house is overpriced.

The market is in a downturn and it is no secret, it still makes sense for some people to buy for personal reasons, but the days of 15 offers are gone.

My annecdotal observation: I live in a well-to-do suburb of Washington, D.C. in Maryland, in a neighborhood was built in the 1950s. For the last few years the trend has been for builders to buy the original ~1500 sq. ft. homes for about ~600k, knock them down, and then put up a 3000 sq. ft. McMansion that they sell for ~$1.5M. Up until a few months ago those new McMansions were selling almost as soon as they were completed. On my drive home I currently count 4 new McMansions that were finished months ago and have not sold yet with another 2 under construction.

but if build is $200 per s.f. x 3000 s.f. = 600K, plus land 600K, plus carry, permits, fees? these numbers do not pencil, and $200 s.f. is low

yes, 1.5m and up is rarified air.

oxygen getting thin up there.

That’s nearly $10,000 a month all in cost to finance.

Who in the world is buying a home at that price point? The orthopedic surgeon/cardiologist couple with no other debt?

Move up buyers. Generally not first time buyers. Average demographic in this neighborhood is likely 50+. So your 10k per month vastly over estimates the monthly outlay.

The tax code and leverage for real estate investing incentivizes people to buy more when they move up (defer taxes, roll over the gains and take more leverage)

Same story in my area of Dallas (near White Rock Lake). There is a VERY mild slow down in sales but things are still selling. Recently there have been a number of 10k plus reductions in price but we are still in the 900k-1.2 mil range for new construction after tear down. 1800 sq ft being replaced by 5000 sq ft home on tiny lots. And taxes are high – a 1 mil house property tax is around 24k a year!

Beans,

That matches what I’ve seen in the Bluffview area of Dallas. Lots of 1,500 sq ft cottages being torn down and replaced with homes that seem to take every square millimeter of the lot. Some of the newer ones seem to be staying on the market a bit longer than last year, but they are still moving. I see the occasional “new price” sign, but so far that’s about it.

The property tax issue is big, especially for people in the remaining 1,500 sq ft cottages. Their houses haven’t changed in value, but the lot value has gone from $40K to $400K, leading to a real tax squeeze for some folks.

I live outside of Philly and my daughters best friend is in sales for Toll Brothers. We were all hanging out 2 nights ago and I asked her how business was. Her response was very quick, sales are way down, market has turned. She also pointed out rising rates as a core issue and then went on to say she did not understand how it was such an issue when the rates are still historically low. I agreed they were low, but pointed to the inflated prices in combination with rising rates as the issue.

I was quite surprised with how quick she was with her response to my query.

It’s not just rising rates but high prices as well.

I guess buyers are gradually waking up tot he fact that these prices are not sustainable and thus holding out to buy homes even if they can afford one. I am one of them.

Sothern calif is hit hard I guess, now front page in msm: https://www.cnbc.com/2018/10/30/southern-california-suffers-its-worst-housing-slump-in-over-a-decade.html

Toll Brothers builds to appallingly bad standards, even in its “luxury” niche: poor quality materials, poor fit and finish, shoddy workmanship overall. I’ve seen brand new/for sale million-dollar-plus Toll Brothers condos in Brooklyn with electrical outlets and shelving that weren’t level or plumb. I don’t know about the quality of their single-family home production, but if it’s anything like their “luxury” multi-family construction here in NY, then pardon my vulgarity, but “Ptui !”

No ill will towards your daughter’s friend, but the company’s products are dreck, and if they get taken out in a housing downturn, it wouldn’t be much of a loss to the country’s housing stock.

Are any of the big builders notably better quality than the others?

My experiences with pulte and KB homed on the west coast lead me to ask: are any of the big builders of any quality?

Mass production without any qa/qc. All my friends who bought from these outfits have had to sink thousands of dollars into maintenance. my parents’ home is 17 years old and falling apart.

A friend of the family worked for the Toll Brothers. The experience inspired him to create this slogan:

Toll Brothers Homes: Guaranteed for five years. Then they fall apart.

My mother was fond of repeating our friend’s slogan, especially while driving past one of Toll’s many developments in eastern PA.

Are there no building codes in these locations? For instance, will they allow use of uncertified lumber?

It’s not just that houses are overpriced here in Seattle, what makes it all so terrible is the appalling state of the decrepit housing stock up here. You would not want to be stuck living in one of these horrible little shacks selling for $1,000,000+. What I see are sad, decrepit, damp, run-down, moldy shacks on noisy streets without sidewalks, often without any insulation (or worse – asbestos contaminated vermiculite). Not only am I unwilling to pay $1,000,000 I wouldn’t be interested in many of these houses if they were offered for free – more comfortable living in a clean, dry van. Anyone wants to move up here and live in one of these dumps… well that’s their problem not mine.

In Seattle, the dampness and moisture gradually destroys the homes. Moss is everywhere – on the sidewalks, driveway, siding, shingles, etc. The moisture rots the wood all over the house, especially underneath, and sometimes from the inside out.

A related problem is that many Seattle homeowners bought their homes lately without inspection. This includes Chinese that bought sight unseen. Several of them may find that the repair cost could be several hundred thousand dollars. Mold and rotting wood isn’t easy to see or to fix.

In this tougher market today, buyers are doing inspections, so there’s no passing the problem to the next guy.

No doubt. I lived in Portland for 10 years and my next door neighbor, who as window/siding contractor, always told me the weather in the PNW was the worst in the country for wood-framed buildings/ homes.

Houses in Northern NJ are among the most expensive in the country

But housing prices relative to incomes in Northern NJ are probably less than half than those in Marin, Santa Clara or Contra Costa County around SF

NYC has land on all sides of it, and all things considered a very efficient transit system (current articles notwithstanding).

You can live in Greenwich and pay through the nose, or you can move to Nassau or Bergen County, pay in the 600-800k range for a nice home, a great school, and on a actual commuter rail line into the city.

SF has an ocean where NJ is, Marin (one giant NIMBYpocalypse) to the north, and has zoned itself into paralysis. Also, BART is a joke (the fact that they try to call it commuter rail when its a bum-infested subway that happens to go to the suburbs is funny). And no one wants to build up for seismic reasons (which is also just cover-fire for NIMBYs).

Live in Oakland. Agree with your bay area comments. BART is a milieu of sometimes disturbed homeless persons, and commuters. Also worth noting in the last few years are the arson attacks of new housing developments in the Town.

@Wolf, what are your thoughts with respect to Land Value Taxes (LVT)? Which jurisdictions (globally) have implemented LVT well?

100% spot on

I commuted for 20 years on NJ Transit. Comfortable leather seats ,very dependable and far cheaper than driving and parking in the city

Our property taxes were very high at about 2% of the market value, but until this year we able to defuct these taxes on our income tax returns making the after tax cost around %1.5.

We had great schools , rated among the best in the country

We did have crappy weather

I recently moved to the East Bay of SF to be closer to our daughter..The BART is equivalent to an above ground NYC subway. The traffic is worse than Nj,NY if that is even possible. We have a small homeless problem even in the SF suburbs. Ca rated 44 th in the country on terms of schools, but it a pretty good bet that the affluent suburbs have very good schools

All in all , my opinion is that the SF area is close to nirvana provided you have lots of money(> 5m) and you do not have to commmute and can leave from mid Dec-mid Feb

A few condos in my complex in San Diego are going on 2 months on the market with 4 price changes in -$10k increments.

Buying interest seems very low. Granted its a crappy time of year and buyers seem to finally be taking a wait and see approach.

in san diego a house in my neighborhood is on sale for last 7 months despite multiple price reductions

It is priced at 1.2 million

The Denver market made a noticeable shift in August, when the buying frenzy stopped. For Sale signs are now up for 1 to 2 months, rather than a few days.

There also are several times more for sale signs than just a few months ago. According to Zillow prices are being adjusted down, but are still at over inflated levels.

I’ve lived in and owned houses in Denver since 1979. Denver is a very cyclical real estate market. There have been 3 big downturns since then 1988-89, 2001-2 and 2008-9. The 88-89 one was a doozy, caused by oil prices going to $10/barrel and people leaving the city in droves due to no jobs.

If interest rates continue up for another year I expect the downswing will start again in earnest and unfortunately lots of people will lose their homes. The secret here is to wait for the next bust to buy, because it will happen. Then the cycle will start again.

There is enormous demand for affordable high-quality housing, so it seems like yet another media-induced psychosis that so many people think higher house prices are good rather than bad for people. We don’t cheer for higher food prices, higher auto prices, or higher gas prices! Higher housing prices only benefit owners who want to sell units they don’t live in, realtors who get a percentage, and property-tax-dependent governments.

While I am starting to believe that housing has turned, I have to say that from a signal-to-noise perspective these graphs don’t prove the point yet. Nearly all of the charts show intervals of flat-to-down index levels over the past several years, within the larger uptrend. The current wiggle isn’t conclusive and most of the supporting data is either highly localized or very anecdotal so far. With rates rising and prices already high, there should be a flattening, but that doesn’t necessarily imply a popping of the bubble just yet.

Part of what made 2005-2008 a historic bubble was the combination of rampant speculation and fraudulent lending, which caused outsized losses once demand slowed down. But most prior periods of house-price appreciation did not result in historic crashes, and it’s not yet clear whether this one will. Lenders have been more prudent, as have builders. On the other hand, there is a new class of real estate investor/speculator, and the corporate housing owners as well. But unlike in 2008, today there remains a large pool of pent-up demand that just needs modestly lower prices to achieve their American Dreams.

So a housing slowdown could easily bring hard times for many people, but there are many others who will benefit from higher interest rates, more affordable home prices, and lower property taxes.

>We don’t cheer for higher food prices, higher auto prices, or higher gas prices!

People consider for right or wrong that housing is an appreciating asset. Just about everything else is a consumable or a depreciating asset

+1. Nicely explained.

You are correct in that there is definitely a seasonality trend around these numbers. However, there is quite a bit of real time data as well as some anecdotal data to support the notion that we are experiencing a change in the long term trend of the housing market. See for example ECRI’s Leading Home Price Growth Index which has now turned negative. Also, Robert Shiller (the guy who came up with the index Wolf uses) was on TV a few days ago saying he also believes the real estate market has now turned.

This said, due to very different fundamentals of this market between now and the last housing downturn few are calling for a “crash” of the market. A drop in prices over the next couple of years seems like the most probable outcome. A 20% reduction in prices spread over a couple years for example would mean house values would be 50% below the 2006 peak in real terms.

the boom is over, but if more than one person wants it, that’s a sale….

A condo in Sunnyvale (Bay Area) has been on the market for 20 days. Price tag $1,298,000. But Redfin’s estimate is $1,593,874. Why so much higher than the asking price? Because a unit was sold for close to $1.6M several months ago. They used to sell in days and now they sit on the market for weeks if not longer. Honestly it continues to astound me how fast prices are falling.

I’m in Franklin Tennessee which is Williamson county about 15 minutes south of Nashville. Sometimes I think the amount of people moving here will hold up the market but I heard a few weeks back that some builders are sitting on inventory, which is astounding for this area. The thing for me is that even with the prices being so high, these houses are still in the 450-500k range and based on living in socal for 20 years these are a steal.

Still. I get this feeling that things are slowing, primarily because everyone is starting to think that prices can’t keep going up forever, and that’s causing people to wait and see.

Miami.analytics website is interesting. She has 50-100 months inventory in some well heeled areas. Prices grinding lower. Bank of Ozarks on the hook for million dollar condo developments etc

Some areas of London I have as 2 years of inventory on the market

sorry analytics.miami

It’s good prices and slowing down or even dropping a little. It was going to too much too fast. As long as people have jobs housing won’t tank, and will stay steady or keep inching up on average. Everyone who bought a house in the past 7 years was qualified and now has lots of equity built up in their homes.

There’s a whole lot of supply coming online in most prime US markets from here to 2020, all developments that have gone too far to be cancelled.

That alone is bound to put a whole lot of downward pressure on prices in those markets at a time when mortgages are inching forward. As valuations are still extreme, and will remain so until developers can afford to “extend and pretend” thanks to an ebullient leveraged loan and junk bond market, even 50bps more every six months on prime mortgage rates are bound to stamp out a lot of enthusiasm from prospective buyers at a time of increasing supply, mostly concentrated in the high end segment.

It will be interesting how the burgeoning US shadow banking sector will react and if it will be able to handle stagnating or even dwindling mortgage originations: like its Chinese counterpart/inspiration it’s a sector built on the assumption of perpetual growth, with the added twist of high expectations of eternal financial repression.

Finally there’s the age-old problem: nobody, bar prospective homeowners, likes declining real estate prices. Local governments don’t like them (lower tax revenues), banks don’t like them (lower fees), retailers don’t like them (lower HELOC’s mean lower sales), the powerful construction industry doesn’t like them (cheaper houses mean lower margins) and homeowners don’t like them (smaller equity, lower “wealth effect” etc).

All these segments will be upon the Fed like a swarm of angry hornets the minute home prices stagnates: see the infamous Wall Street crybabies throwing a tantrum if stocks don’t hit new demential heights and Chinese mom and pops “investors” beating on their pans to demand a bailout for anything.

How the Fed will react is a very interesting question.

Strongly Disagree re “Finally there’s the age-old problem: nobody, bar prospective homeowners, likes declining real estate prices.”

Long term homeowners with no intention to sell would be happy to see stable or moderately lower prices, precisely because it means lower taxes, more money to spend on other things, and so on. Remember that a large fraction of homeowners have no mortgage and many others aren’t interesting in playing the market, just trying to live comfortably at a reasonable cost.

Renters likewise would be happy to see lower housing prices, since it implies adequate supply and that will translate to lower rents.

Now, if you meant that no politically-organized groups like declining real estate prices, I’d buy that.

> It shows to what extent the dollar is losing purchasing power with regards to buying the same dwelling over time.

Er, this is a questionable way of putting it.

The terms “purchasing power” and “inflation” are generally used to refer to the loss of value relative to *all other goods*. If you’re only comparing with a single class of goods (housing) how do you know that land hasn’t become more scarce?

That’s why Case-Shiller is not an inflation measure [of the dollar]. You might argue that it’s a deflation measure of land. But you really can’t infer anything at all about the dollar using only the Case-Shiller index. You might be able to distill dollar inflation data from it by factoring out a whole bunch of other stuff (a process which requires a whole bunch of other data).

The confetti shower of trillions in printing-press FedBux lavished on the Fed’s Wall Street cohorts created the most gigantic speculative excesses in human history. The bursting of the central bankers’ Everything Bubble is going to mean the wipeout of trillions in fake valuations created by trillions in fake money conjured out of thin air, while debasing every hard-earned dollar, GPB, Yen, Euro, etc. in your wallet and mine.

Brace for impact.

Part greater fool theory (hi leverage asset plays), part fundamental habitation needs (where do I go if I sell fear = lack of inventory), part suspension of the laws of price discovery through interest rate manipulation and endless monetary inflows.

The laws of price discovery is being allowed to return through the normalization of interest rates and concurrent QT. Jarring to most blinded and boozed asset markets.

The tearing off of faces isn’t what most new homeowners had in mind when they pushed their down payments across the table.

Stay tune as the current block buster human theater production of “Rude & Entitled” will soon be replace by “Fear & Remorse”.

I always like to read the comments for local inputs, and surprise the few Fl posters don’t mention the ‘Red Tide’…certainly you never hear any major media outlet mention it. We went down and stayed LAST year and never a mention anywhere, much less our hotel, but when we got there, we honestly had to leave after 5 minutes, burning eyes, dead fish down the beach. This year was 100x worse! Dead manatees, and both coast in a sea of dead fish…and seems to be getting worse each year!

—

Friend in SanFran bought in 2009 and has doubled, he makes great money and won’t leave until his child graduates but hate, hate, hates it. Homeless, needles, feces truly everywhere in that city. It’s only a mis-demeanor if you break into a car and steal less than $999. Friend at Safeway says homeless load up on steaks and run out all day. No one wants to get hurt, and only a slap on the wrist if caught….Yet how many people bought into that pit in the last 10 years?….and probably largely cash or large down buyers.

Yes, keep spreading these needles-and-feces stories about San Francisco. Maybe finally people who’re tempted to move here give up. This place has gotten way too crowded, with way too many people moving into the city every year, and not even the worst needles-and-feces stories can stop this huge influx.

I can see it now: the Wolf-Richter Needles-Feces Index. Counterweight to the Case-Shiller Housing Index. Riksbank Prize material, for sure.

In the immortal words of Yogi Berra, “Nobody goes there anymore; it’s too crowded.”

Two house listings caught my eye this week because of their similarities, and I wonder if this is a trend.

The houses are both extreme fixers that were purchased about 6 to 7 months ago and are on the market again with zero work done except for the addition of zoning approvals.

I saw the inside of the first one (on Ordway St.), and it looks as bad (or worse) from the inside as the outside.

https://www.zillow.com/homes/for_sale/1110-ordway-st,-albany,-ca_rb/

https://www.zillow.com/homes/1419-10th-St–BERKELEY,-94710_rb/

I know that two data points do not make a trend, but I have been following this local market for the last 2.5 years, and I rarely see this happen. (Two within the same week seems remarkable.)

I’m wondering what is happening; one would guess that flippers are backing out of projects for various reasons (e.g. market is changing, rising interest rates makes additional borrowing expensive).

From what I hear, I think your hunch is about right — flippers backing out. It’s getting tough for them to make money in this market, and the risks are rising for them.

The buyer of my old Sunnyvale house did a similar listing, after plans and permits were issued but before remodeling work began. No one bit, the place was taken off market, work commenced, and I don’t know at this point whether it’s been completed or not.

https://www.zillow.com/homes/for_sale/375-Orchard-Ave-Sunnyvale,-CA,-94085_rb/