If you blinked, you missed it.

The price of natural gas for December delivery plunged 19% on Thursday, the biggest percentage plunge since February 2003.

This comes after futures prices had skyrocketed 20% on Wednesday to $4.931 per million Btu intraday, before settling at $4.837, the highest settlement price since February 2014 – when “polar vortex” entered into everyday language in the US. It was a gain of 19% for the day, the biggest percentage gain since 2004. Today’s plunge took the price back to $3.899 at the moment, where it had been on Monday. If you blinked you missed it:

The spike yesterday was driven by “a sharp cold revision in the winter weather outlook,” according to a commodities strategist at Morgan Stanley, cited by Bloomberg. “We see modest downside from here assuming current weather forecasts, but a very wide range of potential short-term prices,” he said.

The weather outlook hasn’t really changed overnight, but instead of a “modest downside” move, natural gas performed a historic plunge today.

Speculative fever goes both ways. Today was impacted more than anything by the hangover from yesterday’s spike that completed a 45% run-up since November 2. Time to cash out.

And then there was the Weekly Natural Gas Storage Report, released this morning by the EIA. It was a cold shower, after the drunken party yesterday.

Turns out, thanks to surging production, 39 billion cubic feet were added during the latest reporting week to underground storage facilities across the US. Over the past five years on average – with the colder season having already started at this week in November — natural gas levels in storage would drop by 15.6 billion cubic feet during that week.

It wasn’t a total surprise, though it was higher than the 34 billion cubic feet projected on average by the 10 analysts surveyed by the Wall Street Journal.

Nevertheless, total natural gas levels have ended the “injection season” – generally defined as April 1 through October 31, when levels rise for winter use – at the lowest level since 2005.

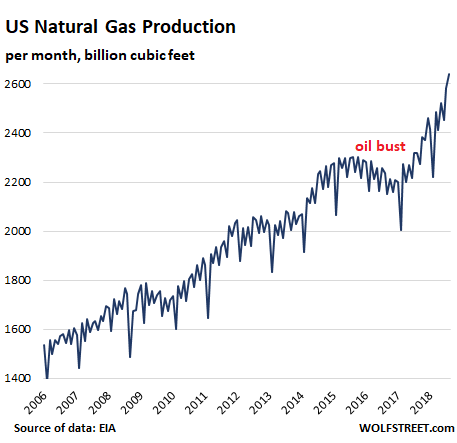

To add to the mix of conflicting fundamentals, natural gas production in the US has surged as a result of the fracking boom, and even the oil & gas bust, when a number of smaller producers went bankrupt in 2015 and 2016, has only made a smallish dent into it:

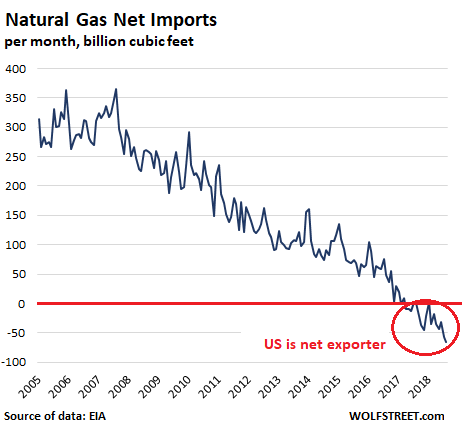

And natural gas exports have surged. The US imports and exports natural gas from and to Canada, based on regional and seasonal demand. It also exports large amounts via pipelines to Mexico, and in recent years has started to export liquefied natural gas (LNG) via tanker to destinations around the world. In February 2017, the US exported more natural gas than it imported for the first time, and thus became a “net exporter” (exports exceed imports). That trend has since grown, with net exports reaching 65 billion cubic feet in August, a drain on what would otherwise be a natural gas glut:

But production, exports, and medium-term weather forecasts neither explain the 45% surge after November 2, nor the 19% plunge today, that wiped out over half of the surge this month. It was just all good speculative fun. Easy come, easy go. On a fundamental basis, given the continued spike in production, it would take a very cold and long winter in the US to cause a natural gas shortage.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Manipulation.

Same thing happened on gold this week.

Not really.

There is no mass mining of gold scam going on were miners and investors end losing money.

Like it happens with fracking oil and gas.

Sudden gold spikes and downs tend to be affected by economic expectations and fears.

The FED new hikes are better investment that buying gold.

Why is the US still importing if it has so much local gas production?

raxadian,

“Why is the US still importing if it has so much local gas production?”

The NG producing regions are not always well-connected via pipelines to the urban centers where NG is needed. Boston is an example. Boston regularly has to import expensive LNG during harsh winter periods because there are capacity problems in the pipelines from US producing regions. These are getting better as the pipeline infrastructure is being built out, but it takes a while.

The same happens in Canada, with some Canadian regions importing US NG, and other regions exporting to the US.

The fracking boom in NG came so fast (a decade ago, really), and it occurred in regions where there was no or little NG production before that the infrastructure to carry away the NG to consuming regions has been woefully lagging. But it’s getting there.

That’s a good point, and brings up the CNG debate again. Before there was the EV there was CNG for automobiles, trucks, buses, etc, which brings up the socalled transportation debate. The argument goes that CNG will never replace gasoline in cars because there is a lack of RURAL infrastructure. The benefit is local. Large muni governments use NG for transportation, with their own infrastructure, and no retail outlets. So far it has been a government monopoly furthered by 44 who believed in the EV. NG sells at about 1/2 the BTU dollar basis as gasoline. If there is infrastructure for LNG for export, why the hell can’t an urban commuter fill up with CNG. (FYI last time I looked you could buy your own compressor) In terms of government manipulation there is none better, could it be the charade is about to end (along with the EV, you don’t need a Tesla, you can convert that old Buick for a few hundred bucks,) and bypass CAFE standards. Of course if there are supply shortages now imagine the line at CNG stations if half of NY area drove those cars. Yet prices remain dirt low. Think of that while you watch those LNG tankers sailing away. When the price comes into line with other energy sources, then one assumes CNG cars will become available.

From what i understand, it was blowup of the long oil, short natty pair trade that’s been profitable for a while. The pair trade ramped up with 45’s pre-election Iran sanctions drum beat. Between all the exemptions to the sanctions and the global slowdown, the long oil trade didn’t quite pan out. Everyone started headed for the exits; those that didn’t get out in time got pushed out by Mr. Margin Call on both trades.

Chicken Dinner! Perhaps Trump suckered Putin and Saudi Arabia into increasing production via Iran trade sanctions then pulled the plug? Long oil short natty speculators were caught on the wrong side and BOOM!

That must have completely destroyed a few people…

Natural gas has never been so inexpensive even when demand for oil has peaked, this remains as a byproduct of its extraction and demand. However, such an enormous fluctuation makes one believe foul play is afoot. More remains to be seen.

There are plenty of dry gas fields ( Marcellus, Barnett, Haynesville Shale, etc ).

I should have been cleared and stated it greatly expanded the supply, but your point still stands.

-The beginning of a new super cycle-

$4.9 is the peak. The next theoretical bottom looks like a day or two below $1.7 within 3 years but probably 1-1.5 years. I won’t be surprised to see $3 tomorrow, but $3.5 seems reasonable. Don’t forget, much of American gas can be sold at a loss with 50 years break even at $3, and only $40 oil will change that in today’s dollars.

We are looking at 80% chance of a weak el nino this year. If cold intrudes, New York will be the brunt of it. The east coast has equal chances at above or below average temperatures, though it looks like above average temperatures for Dec and Jan with the odds of cold arriving in Feb.

The polar vortex occurred during enso neutral. If we are looking at neutral conditions, perhaps you will find the vortex intrusion again.

Theories lead to theoretical outcomes.

I won’t be surprised to see snow this Winter.

Which is a reasonable assumption.

We are looking at a 100% chance of warmer or colder periods.

Although odds of precipitation are especially pronounced.

Warmer intrusion will inevitably occur by Spring.

First the Nat shorts were taken out to the wood shed. Followed almost immediately by those who sought to profit by placing longs. Fun.

Good question. Are there algorithm traders in the commodity space too?

If there aren’t then it also wouldn’t surprise me to see bears strolling out of the woods to do their nr 2’s.

The first high frequency trading line was built for the commodities traders in Chicago. It goes from Chicago to New Jersey, where all the HFT computers reside. The next link is from NJ to Wall St. firms, with the big money “co-locating” on the floors of the exchanges.

I’ve heard rumor that it was a pairs trade too of long oil (so now its safe to end long oil) and since the parabolic spike in gas seems to be over and the 3+ year slide in gas prices may be done too. I do know that the last time I looked at Druckenmiller’s portfolio he’s now holding NBR Nabor and OIH for what its worth..

The “paper” or derivatives market for Oil & Gas is thought to be as much as 800xlarger than the physical commodity. To over simplify, every physical unit may be levered or paired 800 times. It is not hard for people to blow themselves up with this much leverage and complication when they get mispositioned. Consensus was massively Long Oil and Short Natural Gas and leveraged. Notice the E&P stocks hung in ok given the craziness. Most hedged forward production.

” it would take a very cold and long winter in the US to cause a natural gas shortage.”

The north-east is in chaos right now due to unexpected snows. I know you’re all focused on the fires out there, but what happened today was unprecedented. Never this much snow, this cold, so early.

Cars crashing, roads shut down, chaos chaos chaos! This hasn’t happened in over 50 years!

Given that Manhatten was involved, you can expect to see natural gas possibly move up in sympathy. Maybe there is something to this solar minimum stuff.

Yes, there is something to the solar minimum stuff, especially since the outgoing maximum was very poor in sunspots. Scientists who study these things have been voicing their concern for over a decade. Regardless of the carbon dioxide fad, it is the sun that dictates climate, and it was a seriously minimal solar minimum that caused the last Little Ice Age. Just sayin’…it is something we need to consider, as the negative impact of cold is far greater for humans than any increase in warmth (which in the past was a net positive).

http://www.realclimate.org/index.php/archives/2016/11/record-heat-despite-a-cold-sun/

some other scientists with names and stuff.

Wonder if they consider the Earth’s core temperature characteristics as part of their thesis?

It has been freezing for the last two days here down south. Had to put the heat on two days ago. I spent the morning looking for my “warm” shoes in the closet, usually it’s flip flop weather.

What the heck is an “unexpected snow” in November? Is that like an “unexpected heat wave” in July?

->It was just all good speculative fun.

Nod nod wink wink.

This one of the followups to the triggering event you previously referenced? Plunderers stretching their fingers, so to speak, before the real political drama starts?

Something like that. Slippages and spikes, which makes for ‘volatility’, which is traditionally an indicator of an impending fall. The dominos are wobbly and starting to topple here and there.

There are lots of small signs that investors are nervous and eyeing the exits. For example, the whining over measly quarter-point rate hikes tells me the stock touts aren’t all that confident in the stability of the market, and for good reason.

After so many years of NIRP/ZIRP, investors have run out places to put their money that can generate any return, because their customers are maxed out. But they still need new sources of returns to pay for the debt they’ve run up and the higher interest rates, and they’re not going to get them. Europe can’t even raise rates.

“Europe can’t even raise rates”.

Real world rates have been ticking upwards for months now. If you shop around and have more than a few pennies to your name you may even see something akin to interests on your plain old boring bank account.

The European Council (where the ultimate monetary power rests in Europe) has two choices: follow the Fed, progressively tighten monetary conditions and hope for the best or double down on monetary excesses each time there’s a slowdown such as the present one and wait for the unsustainable investments and poorly assessed risks to cause a decade long slump and a lot of work for bankruptcy courts.

Given the present obsession with growth at any cost I am not holding my breath.

->Given the present obsession with growth at any cost I am not holding my breath.

Agreed.

‘Growth’ in itself is something well worth examining, as is the obsession.

What kinds of ‘growth’? And by what means? And to what ends?

Judging from the state of things, it’s clear these questions have never been properly answered, and it’s a bit late for a do-over.

Am with Unamused’s interpretation of ‘speculative fun’ wink…

Respect for Wolf’s tireless efforts to keep discussions professional and off the slippery slope of rigged-markets talk.

Some days must be harder than others…

Any commodity funds blow up lately? Fat fingers?

Some energy trader with a big fund blew up in the last couple of days.

Looks like this one did:

https://youtu.be/-qGvPRX270A

\\\

The natural gas infrastructure is slowly but steadily being built elsewhere in the world:China, EU, Russia, Turkey etc. I will only mention here 3 projects with Gazprom, I will not talk about US built LNG terminals in Poland and planed ones throughout Europe, the TAP pipeline, existing lines to and through Europe, current exploration sites in Cyprus, potential new projects in Korea and Japan etc.

\\\

1) Strength of Sibera, Gazprom, 38 bilion cubic meters per year, set to complete end of 2019, customer China

2) North Stream 2, Gazprom, 55 bilion cubic meters per year, set to complete next year (adding on top of first line of North Stream 1 with same capacity), customer Germany and rest of Europe

3) Turkish Stream, Gazprom, 32 bilion cubic meters per year, set to complete end of next year, with a potential second branch of identical capacity, customer Turkey (and other parts of South-Eastern and central Europe). Turkey already has the Blue stream of 16 bilion cubic meters.

\\\

Assuming a 100% utilization rate of capacity in the next tow years Russia will deliver 38+55+32=125 bilion cubicc meters * 35.5 =

= 4,437 bilion cubic feet = 4.4 trilion cubic feet of gas…of new potential export capacity.

\\\

Now some of this gas is not new, and it’s a will be redirected from existing pipelines going through Ukraine, or through other Baltic nation states for reasons geopolitical nature. Still, these are game changers coming soon to the global market. And the US is not in the game.

\\\

Louis, as I’ve previously hinted in my WS piece on LNG carriers US energy companies have long looked at Europe and Japan as two “captive” markets for their natural gas exports. In fact the first LNG carrier was built to ply the Gulf-UK route shortly before Shell hit the jackpot with the Groeningen gasfield. To this day Gulf Coast refineries are wont to “dump” their excess production upon the so called ARA (Amsterdam-Rotterdam-Antwerp) market because they historically could get better prices for their ULSD (Ultra-Low Sulfur Diesel), gasoline and IFO380 (a low-sulfur bunker fuel) than at home. Not any more.

IFO380 in Rotterdam has been the same price as in Houston throughout 2018 and has been falling faster in price in the former market than in the latter and the export price for US-produced LNG has not yet recovered from the 2016 commodity burst and at last check stood at a miserable $5.33/tcf (thousand cubic feet).

It’s a brutal market out there, and LNG is already going through a glut as basically everybody, from Shell to Qatargas, has been greenlightning maxi-projects in a world awash in natural gas.

I am sure US energy companies are among the most generous sponsors of the “Russia ate my homework” and “Iran is Satan, literally” campaigns since they hope to get better prices for their wares by shutting them off energy markets. So far they seem to have mostly failed, and I hope they’ll keep on failing because the extra price is simply not worth paying.

///

Agreed, the glut of supply will only get worse, with transport cost becoming critical. I have never seen a study on comparison of transport cost, pipieline vs. rail vs. sea, so I can’t compare. Thanks for the articles, I especially liked the shipbuilding one.

///

“LNG is already going through a glut as basically everybody, from Shell to Qatargas, has been greenlighting maxi-projects in a world awash in natural gas.”

MC01, LNG supply won’t be in a glut until maybe 2021. Projects getting FID now will get their first LNG in 4 years if it’s a greenfield, less if it’s a brownfield.

“…export price for US-produced LNG has not yet recovered from the 2016 commodity burst and at last check stood at a miserable $5.33/tcf (thousand cubic feet).”

Actually, conditions for US LNG have been extremely favorable for pretty much all of 2017-2018. For evidence, take a look at volumes exported from Sabine Pass in Cheniere’s earnings presentations and the destinations involved. Their volumes are sold Free-on-Board, meaning the customers have to pay the shipping cost, so maybe that’s why it’s so appealing – but I don’t think so, given how overbuilt LNG shipping capacity has become.

US LNG also has pricing arbitrage built into it. Old Qatar-based LNG contracts are all oil-linked to Brent or some other heavy oil barrel benchmark. If Brent goes high while a hub price goes low, they are overpaying per unit of heating value compared to buying the same amount of gas from the hub. If instead, they purchase a cargo from Sabine Pass, whose gas is cheaper than the barrel of oil equivalent price (called “broken oil parity”), that’s arbitrage. If you netback the Cheniere contract and add maybe $1.00-$1.20/MMBtu for shipping fees, you still get a cheaper MMBtu than most current prices in Northeast Asia.

I’d also say lack of proper gas midstream infrastructure throughout the world and the need to improve air quality is behind much of the “new demand” for natural gas/LNG.

Lastly, why are you quoting the price in tcf? All quotes are in $/MMBtu. Sounds like you’ve got an axe to grind or something.

Time to buy some dirt cheap Russia ETFs. Good dividends too.

The entire futures market is manipulated by our government through their proxies behind the scenes.

The economy is slowing. Natural gas demand will crash, even in winter as so much is flowing from the fracking wells. So, the powers to be place a massive short squeeze to send a notice. The shorts then pile back in. Back and forth it will go.

The governement cannot tolerate deflation. They will fight it at all cost.

The main focus of all energy trading is to try and establish what other players’ position is. That is what it is critical in the OTC market to see what names are buying or selling. Then you try and create a facsimile of the overall position to see where the inflection point is.

The second stage is to hit the lunch circuit in London and New York to create a team of people that can work together (or stand aside) and force the identified (massive) short or long to puke the position when the market rips against them.

All fun and games.

I watched all it happening in past two days.

I’ve been gambling on UGAZ for two years and decided not to touch it again.

However, on Wednesday morning pre-market I saw the 30%+ gain on UGAZ and wondered why I didn’t look into it this year. In the afternoon when NG price hit $4.9 (UGAZ 60%) I added DGAZ into my watchlist.

Unfortunately or fortunately, at the end of day I didn’t have the courage to buy DGAZ. And, Thursday DGAZ 60%+ here we come!

It has been a wild ride. I wonder how much fortune was made or destroyed in past two days.

Bitcoin caught my eyes in past two days, too.

And think how much fortune has been extracted from the real economy by the long-oil, short natty speculators over the past 10 years.

I saw a news report recently, maybe it was on RT’s Boom Bust, that a large number of tankers are sitting off of Asia, unable to unload. As I recall, the reasons stated were that the Chinese economy has slowed and that the expected cold weather in that part of the world is taking a long time in coming. There’s no place to store it on land. However, that doesn’t explain daily volatility.

It wouldn’t be a tragedy anyway if fossil fuel consumption went down and the world’s obsession with growth showed signs of tapering.

Smells like a pump n dump. People with lots of money pumped on the report, especially if they had advance knowledge of it which is very possible for people with lots of money. Then they dumped.

As usual, the losers were the people not in on the game who bought on the upswing thinking its going to be a cold winter and the price is going higher and if I get in early (afternoon of the up day) then I’ll make lots of money. Nope.

“a sharp cold revision in the winter weather outlook”

Are we sure it wasn’t a measure of money laundering ??

One question that occurred to me on reading Wolf’s description of the lack of domestic pipeline infrastructure needed to bring natgas from the fracking fields to major cities far away: Why haven’t we heard anything about pilot programs involving production and road/rail transport of methane clathrates, which are the kinds of solid-ice molecular-cage methane-water complexes formed naturally at the pressures and low temperaturs of deep ocean water? Wikipedia on the basic physical properties and the obvious barrier to *ocean* transport of same:

OK, so the added mass of the water makes this a no-go for ocean transport – but I wonder if the calculus might be different for surface transport between points lacking a gas-pipeline connection. If the much-cheaper compression/refrigeration step and the ability to do it without the massive plant infrastructure of CNG offsets the added road/rail haulage cost due to the water weight … anyway, I was surprised not to have heard about even a US pilot program along these lines.

As far as I know Dongguk University (Seoul) developed a laboratory scale experimental pelletization plant for natural gas hydrates (NGH) with financial backing from the Korean government.

Plainly put while the experiment was successful in producing a few pellets strong enough for transportation, it wasn’t neither cheap nor easy.

The first main challenge is to manufacture NGH pellet strong enough to withstand transportation at a speed comparable with NG liquefaction plants, and that’s a problem because modern LNG plants are becoming faster and faster to load modern LNG carriers. In short NGH pelletization is playing catch with technology that’s still advancing at a rapid pace.

The second main challenge is that while the people at Dongguk thought their most resistant pellets could withstand transportation, they warned they have no idea how several thousand tons of the things would behave while being loaded and unloaded in a ship, let alone if said ship is caught in a storm.

The third main challenge is how to economically and safely sublimate the pellets at a fast enough pace to, say, feed a power plant. The US and Japanese governments have a joint small scale sublimation plant in Alaska to explore the feasibility of natural NGH exploitation, but that’s about as far as we go about our knowledge of the sublimation process on anything larger than laboratory scale.

The US government (chiefly through the Geological Survey) has been at the forefront of NGH studies since the mid ’90s and the Jet Propulsion Lab has a very impressive NGH program, but always remember that merely throwing money and brainpower at a problem is no guarantee of success.

If that were the case the “Hydrogen Economy” of the late 80’s and early 90’s would have long become a reality instead of being limited to a handful of rabidly expensive cars.

Thanks, MC01 – that was very helpful, exactly what I was looking for.

Optionseller–》 https://www.youtube.com/watch?v=-qGvPRX270A

Crazy..