Hot air is hissing out of this market.

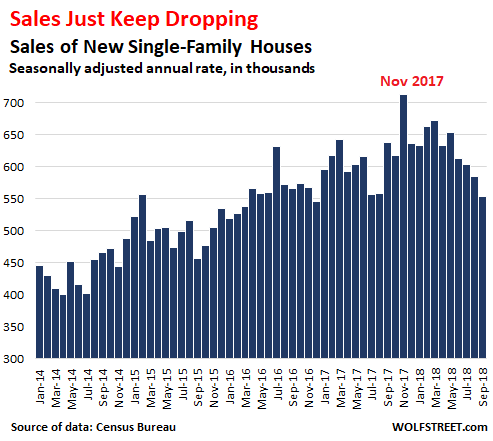

Sales of new single-family houses in September plunged 18% from September a year ago, not-seasonally adjusted, to just 41,000 new single-family houses, according to estimates that the Census Bureau and the Department of Housing and Urban Development jointly reported this morning.

In terms of the seasonally adjusted annual rate of sales, which projects what sales for an entire 12-month period would be based on the sales in September: It plunged 13% from September last year to an annual rate of 553,000 houses. Single-family house sales account for about 10% of total home sales. This data is volatile and is subject to big adjustments, but after a while, the trends are starting to be unignorable:

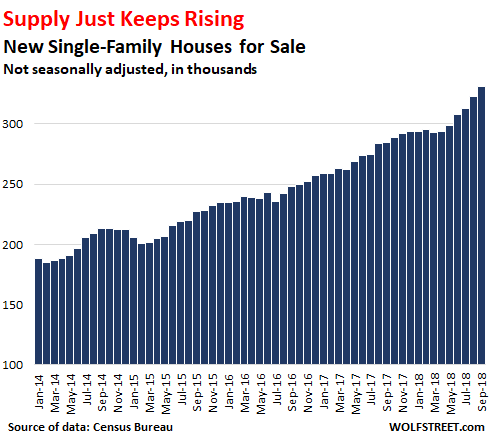

But the number of new unsold single-family houses on the market keeps surging and in September jumped 16% from a year ago, to 331,000 houses (not seasonally adjusted), the highest number since January 2009, during the middle of the housing bust.

This supply of unsold new single-family houses on the market, at the rate of sales in September, represents 8.0 months’ supply, the highest since February 2011, and up 40% from September a year ago.

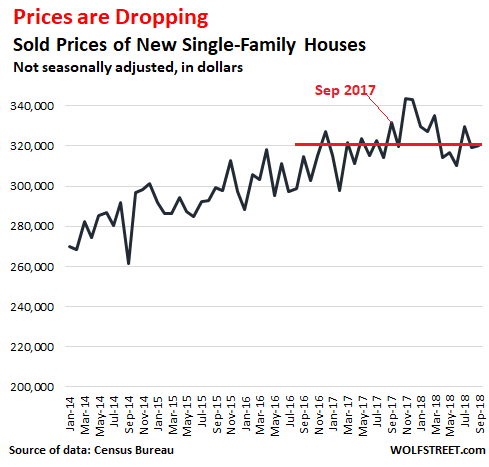

So, is it time to cut prices to move the unsold inventory languishing on the market? You bet.

In September the median sale price dropped, very embarrassingly, 3.5% from September last year, to $320,000. The median price is now down 6.8% from the glory days at the peak last November:

Homebuilders are pros. There are no emotions involved. They do this for a living. They have all sorts of data at their fingertips. They know how the market works, and where the market is headed, and they cannot sit on their unsold inventories for long, and they will sell what they have built, one way or the other, and if they have to cut prices and offer incentives, so be it.

By contrast, regular homeowners, trying to sell the home they’re living in, or used to live in, are often under all kinds of illusions about the market, and they have some aspirational price in mind that they want to get, and they’re still dreaming of bidding wars, and they take a lot longer to come to the realization that the market has turned, and that if they want to sell, they need to be where the market is.

And this data confirms that the hot air is coming out of the housing market, not all at once, but very gradually, with many up and downs in between.

Forget the hype about a shortage of supply. Read… US Housing Turns into Buyer’s Market

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The house across the street just sold for $85k more than the sellers ( who were apparently living in squalor as there has been a parade of construction vehicles) paid for it two years ago. Zillow just miraculously shows a value almost identical to what the Knife Catchers paid for it even as the Zillow value of my home across the street continues to fall

The value algorithms are not 100% real time. Usually sales at the lower prices have to pile up before they will start to adjust values. If there are no similar home sales from that area the algorithm probably wont alter the value much.

Very true.

Yet prices continued to plunge. In fact the declines are accelerating.

So much for “value”.

I am seeing lots of properties in SF now on Trulia and most of them seem to have price drops. There is still some insanity like $1,600 per sq foot remodeled in Noe Valley that just screams flipper stuck in the market. Haha good luck with that.

I look forward to buying in 2020.

Back before the last crash, a noted waiting-for-RE-to-collapse blog had a bunch of funny terms, like the DHO Index for Dudes Hanging out, for how many random people appeared in the photos in the listings, the number of “cawlumns” because everyone knows, columns always make RE worth more, and all kinds of funny terms that had us giggling our way to the hobo camps…

One was whether a place was in the Real Bay Area or RBA, depending on $ per square foot. I want to say the division was at $200 a square foot but that sounds so outdated and quaint now. Was it $400 a square foot? Even that sounds outdated these days.

So what would make a place part of the Real Bay Area now? $1000 a square foot? This might be grist for a thread all its own.

There must be some way to hedge these inflated values, some RE inverse leveraged ETF that tracks housing prices. It might make the difference between foreclosure at some point.

If it’s inverse-leveraged, your sustained ownership only lines the pockets of the issuers. All the inverse-leveraged funds are guaranteed long-term zeroes, useful only for short term trading (if at all).

What you could do as a hedge is to short homebuilder stocks, but it looks like others have already done that. And of course your upside is limited but your downside isn’t. Put options might do better but then you have to get timing right.

SRS DRV and REK. Depends on whether you think RE will decouple from stocks, how much you need to hedge and how much capital you can allocate. And how much you can get hurt on the upside.

Now plot the longer-term charts for any of those funds. They are not useful for hedging over timescales longer than a few weeks.

In fact, no one who held SRS for over 10 months ever made a profit. The sellers of those funds are ripoff artists. They’re no good for hedging a vague risk.

How is it that this discussion has failed to note the oppressive job market in the US and how it directly relates to home values?

The labor participation rate is still in the range of 2000.

Consider not only that fact, but also the gruesome rise in medical/auto/home insurance.

“By contrast, regular homeowners, trying to sell the home they’re living in, or used to live in, are often under all kinds of illusions about the market, and they have some aspirational price in mind that they want to get, and they’re still dreaming of bidding wars, and they take a lot longer to come to the realization that the market has turned, and that if they want to sell, they need to be where the market ”

Markets are all local. If you would like to give some teeth to your speculation I suggest you tell us exactly where the housing inventory is building up?

My guess is California and the other speculative markets are skewing the stats for the whole country. In my well to do suburb, there is nothing for sale for miles and the apartment complexes are full to bursting (tried to get a relative an apt- near impossible).

Theoretically, if there were no supply at all, the sales figures would plummet! So that’s what I think you’re seeing.

“Markets are all local. If you would like to give some teeth to your speculation I suggest you tell us exactly where the housing inventory is building up?”

Just because you didn’t read it doesn’t mean I didn’t write it. Here are two local examples, and a nationwide view:

https://wolfstreet.com/2018/10/08/sonoma-bay-area-housing-bubble-price-declines/

https://wolfstreet.com/2018/10/05/san-francisco-house-price-condo-price-bubble-trump-bump-peak/

Which includes: “Total listings reached 1,208 homes in September, which gives the city 3.8 months’ supply at the current sales rate.”

https://wolfstreet.com/2018/10/19/us-housing-turns-into-buyers-market/

If markets were all local. like for example the weather, then there could never be a general real estate boom, or a general drop in prices.

But there has been a general boom, fueled by a general availability of ultra- cheap money.

I first learned that a general real estate crash BEGINS in certain hot spots as a young realtor with a few properties of my own. I was shocked when the market turned without warning at ‘2 PM, August 1981’ (to slightly exaggerate the speed )

Out of a job a few months later I did some investigating and found there was actually lots of warning. I was working on Vancouver Island, Canada.

but the market had been weakening in the US up to year before.

Back to this market: the super-hot Miami condo market began its descent last year.

Speculators who’d been buying pre-builds off the plan, hoping to flip before after (or before) completion began either walking away or selling at a loss. I believe it WS that covered that, with a long list of sales at a loss.

London, one of the hottest markets in the world, also began its decline at the high end last year. A Russian who’d bought off- plan two years earlier couldn’t close and lost 500, 000 pounds.

Why are the speculative markets the first to predict a general decline?

They need the ‘oxygen’ of cheap money like the canary in the coal mine needed literal oxygen more than the miners. But if the miners don’t heed the swooning canary, and the air worsens, they are next.

The question for the general market: will liquidity (oxygen) continue to ebb?

Here in Nanaimo, Van Isle, no one doubts we have passed the peak but there is also very little for sale. We are in for a long stand- off between buyers and sellers. Sellers are notoriously reluctant to lower prices and buyers are reluctant to buy until they do.

PS: mortgage rates are not local, they are national.

I get the sense that this softening in the real estate market is actually an international phenomenon. My parents are from Ireland so I follow that market more closely.

An article from today (10/25/18) describes the following situation in the Dublin real estate market:

“In the upmarket areas of Dublin 4 and Dublin 6, high-priced homes are struggling to sell. A report by property portal MyHome.ie shows that 68 per cent of prime properties in Dublin 4 — the most expensive area in the country with an average price of €775,973 — and Dublin 6 have cut their prices.

‘For quite a few properties that are on the market for more than €1m, the asking prices are being pushed down,’ says Stephen Day, residential director at Lisney estate agents.Day has recently reduced a five-bedroom property in Ranelagh from €2.25m to €1.995m.

‘To be blunt,” he says, ‘agents are putting houses on for too high a price, and so they have been sitting on the market.'”

The article also suggests that the trend is global:

“We have long contended that London house prices would fall sharply and there are increasing signs that this is happening not just in London (see News today below) but in Sydney, Melbourne, Vancouver and other cities which have seen massive appreciation in their house prices in the last two decades.”

http://news.goldseek.com/GoldSeek/1540465200.php

(This article is not unbiased because the author recommends moving money into gold at the end, but I assume that the article’s data is correct.)

Yes, high end properties are taking longer to sell and selling for less in London (UK), Sydney, Toronto, Vancouver and, as the GoldCore article states, Dublin. It does seem to be pervasive in the West and probably just a matter of time before it trickles down to the less expensive housing sector. People are becoming worried about higher interest rates and, here in Canada, some provincial governments have introduced measures to cool the property market.

Sonoma County, the local paper even acknowledged it yesterday.

And we have NO shortage of demand.

It’s the price.

I spoke to two people yesterday who are pulling their homes off the market and planning to rent them until prices come up, they have plenty of equity and are comfortable waiting 5 years or more.

I also looked at three houses on today’s broker’s tour, one was priced well, one was iffy and one was priced at 20% more than it sold for a year ago (Now $3MM).

I dropped by because they had a catered meal and who doesn’t enjoy a free lunch?

The prices in Sonoma are ridiculous. My guess is your renting home owners will be worse off in 5 years.

I think buyers markets are better for everyone if they are more frequent. Most home sellers also need to trade up. So though they may have to sell at a lower price, they also get to trade up at a lower price with more options to trade up to.

Meanwhile first time buyers are always better off in a buyers market.

A sellers market screws new buyers and also takes all your gains on a sale and shoves them into an overpriced trade up.

The only normal risk to owners in this situation is, god forbid, you may have to own your home for more than just 2 years to build enough equity to sell and get a good amount of money back.

A house used to be shelter. The wheels came off when it became a commodity

A house used to be a home and was the bedrock of society. It mattered not if it was rented or owned, it was where people of importance lived. Individuals mattered. In a large centre it would have been an apartment but still reflected a community that people belonged to.

These days, everything…everything is a commodity. I was very pleased to hear my children’s opinions this fall. My son has decided not to sell his home and is now in it for the long haul. When he does improvements he just works more OT to pay for things. My daughter and son-in-law informed me their big planned renovation is now off. Not only have they decided to stay put, they have concluded their little bungalow is big enough for their family and that they don’t want to get on the ‘more stuff’ bandwagon. They are afraid of debt taking over their lives and have charted a course to avoid it.

I disagree with some on the site who say that a home is a declining asset; a liability. With care and attention, a purchased home can set a family up for life. This might not be the case right now where you live, but it can be for others in different areas and situations.

regards

They will have a problem if you are free. So you will lose our home or you will be in debt. If NOT rent, they will load you up with student loans. If NOT student loans, they will squeeze you on medical insurance premiums. If still can NOT squeeze you into a positions where they want you to be, there will be globalizations. If there is NO globalizations, they will let you work on robots to replace you so that you will be on universal income. Bottom line, you will NOT break free.

All the financial markets, policies, Fanny May and Freddy Macs, are the institutions to make sure you are under control. To break free, you will have to be extremely conscious about all the traps and be willing to risk your freedom to get to freedom. Change of habit on consumption is a start, but NOt enough.

I think Wolf is taking a macro view. It’s wonderful to hear individual stories but we’re discussing homebuilders and millions of homes trending in hundreds of markets.

The wheels came off when they dropped it off at the trailer park!

Sorry, couldn’t resist!

Saw a video this morning which reported some properties in Australia dropping as much as A$5K-10K a week. Their auction clearing rates are now worse than during the GFC. Another video talked about Toronto condo incentives now including a new BMW car, up to C$35K in value.

My local market is still “hot” only down 6% in Sept YOY. It’s getting interesting.

July 2018 inflation hits 2.95%! The 12 month moving average is now around 2.5%. How do all like them apples?

“gradually”

SP500 doesn’t seem too “gradually” today :)

Watch it bounce tomorrow :-]

I wonder if that’s what people thought yesterday. Look, it didn’t end nearly as bad as it began, it’s gonna really bounce tomorrow.

;-‘]

The pros are dropping out of the buy the dip routine. Now it is mom and pop using a strategy that worked for the last eight years… one year too late. They’ll get crushed, they always do.

The Plunge Protection Team is ON THE JOB!!!

Nah, it was pretty gradual in the scale of things, just barely over 600 points, not even breaching the level of what happened two weeks ago… never mind January… Let me know when it drops 10% in one day. Oh wait, I don’t think it can, there are curbs that will get slammed in place… right?

I cannot count the number of retired friends I have with significant money in the stock market or really all their money in the stock money and they are past 70. This down cycle will cause many a retired person to seek a part-time job to make ends met sooner then later.

On-line forums are filled with retirees with all their assets in the stock market. It’s a bad idea. I’m 50. I’ve decided to be out of the market when I’m 60 (well, perhaps mostly out of the market).

Gotta love the predictable response to FED monetary policy, keep rates too low for too long then hike mercilessly… rinse and repeat.

Enjoy the ride!

“they will sell what they have built, one way or the other, and if they have to cut prices and offer incentives, so be it.”

And you don’t want to be in a position trying to sell a used home when builders are unloading their inventory all around you in a new community. Pretty easy to get burned in this situation in certain Texas markets where land is plentiful.

As the CEO of PulteGroup pointed out this week, cuts to base prices are the easiest but least attractive option. Looks like the endless bid for bad dirt is evaporating about as fast as the Fed’s balance sheet, probably faster.

\\\

If the US wants to be competitive in the world job market, it is critical that the realestate prices adjust to significantly lower levels asap. This would alleviate the income stagnation, and increase the relative purchasing power of the same. Otherwise the country at large will suffer a gradual de-industrialization…something like England has seen in the last 40 years.

If I were the government I would immediately pass incentives to build even more housing units across the nation to bring the price even further down.

\\\

Malinvestment got us here and malinvestment will get us out ? I would rather

the policies facilitate long term stability without catering to special interests.

\\\

If you look at the cost breakdown of each employee, you can notice two major items that dominate the cost: the healthcare for the employer and the realestate for the employee. My point on incentivising building realestate is not tailored to any special interest group, but more towards the working family and lowering their cost of living. Now is this a bad or good idea, I don’t know…I will leave that up the public opinion. Nevertheless it’s an idea…Malinvestment? Maybe…but the cost of housing needs to go down!

\\\

If England were a U.S. state it would be one of the poorest. The U.S. is a powerhouse economy with endless wealth and opportunity. “If I were the government”? Well, that pretty much sums up your economic theory. Please don’t ever run for public office. Please, everybody, don’t pay attention to those NYC penthouses and LA estates trading at insane numbers. Those people have no relation to Mr. Wolf’s observations regarding the building and sales of new single family homes.

\\\

Don’t worry, I will not be running…I simply prefer using my bicycle or public transport in general. And running is bad for your knees.

\\\

This is a representative democracy, and as you enter office you can do as you please with little to no reprocutions from the public. Hence the term “If I were the government” is an appropriate statement. Now Swiss direct democracy…that is a different story.

\\\

You must all be living in the USA bubble. Believing that it is a powerhouse with endless wealth and opportunity. Maybe so if you want to work like a slave and get screwed in isolation in the bubble.

I have lived in both England for 27 years and the USA for the last 14 years. I’m done with America. As beautiful as it maybe to the eye, it’s not for me socially. It robs your time and dime. America is a business and not a country. It’s a big rat race to obtain a dream setup by the 1% to feed from.

I’m going home to where the grass is actually greener, where I don’t have to worry about copay and operations costing over 6 figures. Where travel and vacations are cheap and companies give you 5-6 paid vacation to actually enjoy your life. Who want’s to be the richest person in the graveyard?

The real estate sales artists always call them “homes”, but Wolf correctly calls them “houses”. One thing I absolutely love about Wolf’s writing is that he frequently picks the words correctly without being bamboozled by bankster “framing” of issues. We need a lot more of that in the media.

A building for sale is just a house. Only when someone is happy living in it does it become a home. It’s the owners (or long-term tenants) that make a house into a home – not the builders or sales people. So you can only buy a house, not a home.

Absolutely correct. A home, and a house are two vastly different animals….I could write a lot about this. But I believe most of us really know the difference….

I believe Burt Bacharach had you beat by about 50 years, and Luther Vandross rather eloquently spoke for Mr. Bacharach back in 1983.

Where is this oversupply? We’ve had two local (D.C. suburb) real estate agents call in the last week begging us to sell our house because they have no inventory!

It’s called prospecting, Bozo (no offense) and businesses ramp it up when things slow.

Recently received a seemingly hand-signed and hand-addressed letter from my local car dealership (mailed from a zip code several states away). Apparently they are desperate to have my ’04 Pilot with 280K miles for their lot because they have people clamoring for it. Just come in and let’s talk.

Suggest you don’t talk to strangers who come to your door or there may be a new religion in your future ;-]

“Suggest you don’t talk to strangers who come to your door or there may be a new religion in your future ;-]”

That right there is funny!

My prediction is that, if home prices significantly fall, the Banksters will further cut back on the money supply so only the wealthy will be able scoop up the bargains.

All the lemmings who piled in at the peak wailing “If we don’t buy now we will be priced out of home ownership forever” are regretting their purchase.

Any time you hear people saying these words, you know the peak is near.

QE unwind and rising interest rates are taking the air out of the housing market. The interesting group will be the vast number of rental houses purchased since the downturn waiting to be turned over by individuals and corporate. Large Profits have always been forecast on the turn cycle but maybe they have waited to long and now will watch as the market cycle moves against them.

From the lending world interesting changes are happening.

Conventional loans are tightening up while non-QM programs are loosening.

Today’s non-QM are nothing like the sub-prime of the previous decade, however, I don’t like this loosening trend.

Looking from the lens of the little guy (low income/small home) in the South I see and hear the following:

1) People are coming here (a lot of them) and prices over the past 48 months have ever increased up until August. Now people are still coming here but the prices of houses has peaked. Locals are priced out and people moving here are likely buying new…. lots of new DR Horton type homes vs. buying some old house. Old houses are now sitting.

2) Interest rates are causing people to freak the heck out. I know of and hear from people whom either sold or bought…with some of both starting late last year up until August again. Now everyone is at the level of “forget it” because the rates are too high. For our price range those quarter points added up to keeping that $150K house out of reach so we are all going to stay in our $85-100K house because we don’t have cash or enough of it to buy that other house.

I had purchased some land to build a house, but the cost of everything has that on hold. Commodity prices for near everything including labor have skyrocketed. All the builders are busy (40 plus homes with deposits down from folks not from here) and if you want to build… you are going to pay $155-$200/sq ft. That is Yankee money right there and for me…. my budget is $135/sq ft. Max. So we wait until something gives.

“2) Interest rates are causing people to freak the heck out. I know of and hear from people whom either sold or bought…with some of both starting late last year up until August again. Now everyone is at the level of “forget it” because the rates are too high. ”

I am old enough to remember Jimmy Carter, and 18% mortgage rates. Most of us children of the 70s have PTSD, from that.

On the other hand, if you were brought up to think that 8% is a normal and proper interest rate for a 30-year mortgage, then what is going on today looks like relatively easy money.

Your mileage may vary.

Yep… remember the 18% very well. But the cost of a home in the 70″s was between 50,000 to 90,000 not 280,000 to 300,000.

50,000 to 90,000 1980 dollars is roughly $150,000 to $275,000 in 2018 inflated dollars, so yes, the prices are roughly comparable.

Even NAR has come out with data showing that sellers are having to accept lower than asking to get the close. Once this is common knowledge, how long until buyers start to wait longer to see how far down the price will really go? And as rates rise, they get priced out anyway.

Absolutely the market is turning into a more balanced market. Not a crash (as of yet).

But, sellers that price high and expect 10 offers in the first 2 days are not happening anymore.

Mortgage broker here in CA, btw

Normal cycles of the market. Yawn. Keep calm and carry on.

To some extent, yes, but there is nothing normal about this period of ultra-low interest rates we’ve had and the level of debt it has led to.

As a non-RE person, I often get confused when I see the term “houses” used interchangeably with “homes.” I automatically consider the word “house” to mean a free-standing building, or maybe a fourplex or duplex. But the idea of telling someone you just moved into a new “house,” which is down the hall in #4B on the fourth floor of a high-rise condo, seems strange.

But I’m aware that over the last few years Wolf has noted the massive overbuilding of condos in places like San Francisco and Miami, which added his conclusion that they would eventually flood the market. So I wonder if that might be part of what’s happening with prices.

Being musically minded, it made me think of the song, “A House is Not a Home,” although in a different context, LOL.

https://www.youtube.com/watch?v=EF0c2so977A

A “home” is a catch-all for houses, condos, co-ops, etc. So when we talk about total sales of all types of dwellings, we often use the word “home sales,” because it’s easier.

Houses are always detached or semi-detached. Something like duplex could be a house. But a condo in a tower is never a “house”; it’s either a “home” or a “condo” or in Australia, deliciously, a “unit.”

This all gets pretty complicated. And the catch-all word “home” makes this easier. That’s why you see it so often. I use it too, instead of “all types of dwellings,” which I also use if I have enough ink left.

Of course, none of this has anything to do with the “home” you go to after work or get kicked out of if you’re not nice to your wife.

First time poster.

Please don’t life time ban if inappropriate post.

I’ve never been to San Francisco and probably never will be. But, thanks to Wolf, I have a new hobby – the S.F. real estate market! I don’t understand why but this topic interests me.

One question has been puzzling me. Looking at a map it seems SF might be at peak usage as far as available land is concerned. I’m from central Wisconsin and I normally don’t think in these terms. I wonder if I need to factor this in.

Now on to figure out that Donate button.

Thanks Wolf for the great site!

RedRaider,

Thanks for trying to figure out how to operate the Donation button!!

In terms of available land, SF has a very large amount of it. Much of it is in two areas, Treasure Island and the Naval Shipyards (Hunter’s Point). They were both federal property, used for military purposes during the Cold War. Now they’re infested with nuclear contamination. The clean-up of this land lurches from one corruption scandal to the next, and has been going on for years. If and when this land gets cleaned up sufficiently, it will be built up with tens of thousands of new apartments, condos, offices, retail, etc. (“mixed use”). The views will be gorgeous!

Plus, there is a lot of fill-in available, old warehouses, office, and industrial spaces that are now empty. These fill-in spaces have been getting redeveloped for years, but there are still plenty left. They just redeveloped an old 2-story office building with a big parking lot down the street from us: tore it down and built a condo complex on it from sidewalk to sidewalk.

Well, people are still flocking into my neighborhood. There was a Bloomberg article about it two days ago.

https://www.bloomberg.com/news/articles/2018-10-23/boise-and-reno-capitalize-on-the-california-real-estate-exodus

Ten thousand dollars here or there don’t seem to bother them, but the older homes are competing against new builds with all the bells and whistles. It’s still impossible to find contractors in Boise – one month lag just to get a quote. and 3 to 4 months to actually get on he job. They can pretty much quote what they like.

That said, my banker tells me the interest rates are slowing things down.

Wolf, thanks for this report,

Gives me hope affordability will eventually hit here in N.Texas as well and I’ll be able to have a home again.

I listed one of my rentals in So Cal a month ago and received 3 offers, all within 10% of asking. I believe 4 months ago I could have gotten asking price, but a lease is a lease. I am still looking at a gain of 329%, since purchasing in 2009 as an REO. This does not include all the rent I have collected since 2009, which after property taxes, insurance and upkeep averaged 46% over 9 years. Not so sure most stocks or precious metals could generate such a return. Real estate can be your friend, if you buy right. Scoop them up at or near the bottom.

Doubtful but post a link.