“101 new listings, 101 price reductions.”

This is what it looks like on the ground: The home on 1704 Hurlbut in Sebastopol, Sonoma County – a pricey area a little north of San Francisco, between the Pacific and Napa County – was listed for $980,000 on June 17. Then came the price cuts:

- July 19: cut to $935,000

- July 24: cut to $895,000

- August 7: cut to $850,000

- September 19: cut to $830,000.

In addition to the 15% price cut, they threw in a $15,000 credit toward the pest damage, explained Thomas Stones, a broker in Sonoma County. It still hasn’t sold.

“Places that were right around $1 million initially seem to be having the largest price reductions,” he said. “Oh, I mean ‘Fresh Prices’ and ‘Improved prices.’ I really have to work on my Realtorspeak!”

Another example is the home on ten acres at 1725 Sextonview Lane, a few miles west of Sebastopol. It was originally listed on August 27 for $1.995 million. On September 23, the asking price was cut by $296,000 (15%) to $1.699 million, and it still hasn’t sold.

Two months ago, we – Thomas Stone, the broker in Sonoma County, and I – stuck our necks out and said that the housing market in Sonoma County experienced its inflection point in June, and that the underlying dynamics have deteriorated since. This became visible in the raw data beneath the surface as well as other indicators, such as desperate fliers sent to brokers. So here is how things developed in September.

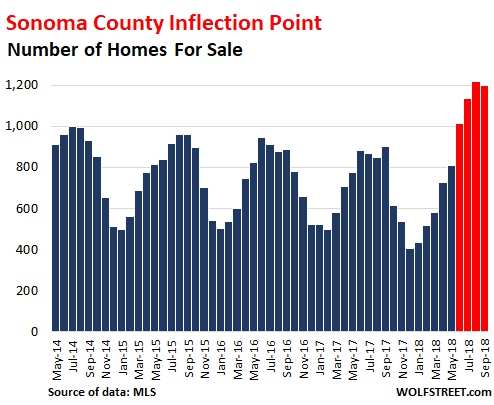

The supply of homes listed for sale in the county suddenly jumped in June and in September reached 1,198 homes, according to Multiple Listings Service (MLS), provided by Stone. The red columns indicate the moves since the inflection point in June:

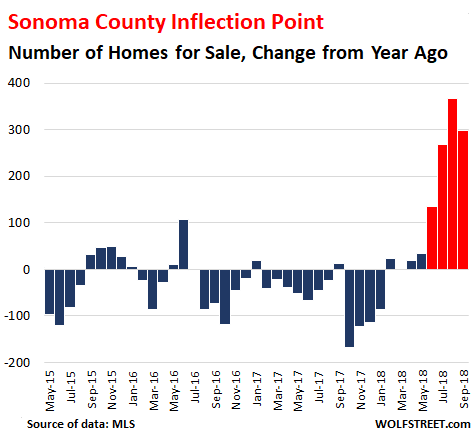

Home sales is a seasonal business. To eliminate the effects of seasonality, the chart below compares inventories to the same month a year earlier. In prior years, supply tightened, with inventories on a downward trend year-over-year. But over the past four months, that has drastically changed. In September, 299 more properties were listed for sale than in September last year, an increase of 33% (red indicates the moves since the June inflection point):

Even as supply has surged 33%, sales in September have plunged 25% year-over-year, to only 357 homes, the slowest September in the data going back through 2014.

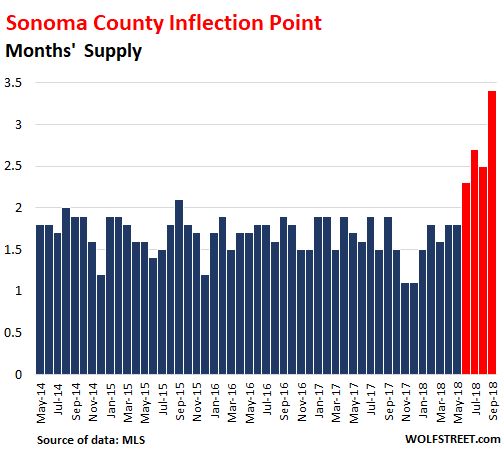

And months’ supply of homes for sale is soaring. This is the number of homes for sale divided by the number of homes that sold. It used to hover around 1.7 months. It began rising in June. By September, it had doubled to 3.4 months (red indicates the moves since the June inflection):

When there is no sale, no one gets paid. When sellers are asking for more money than buyers are willing to pay, sales volume falls off. If this stalemate continues, the market freezes up and doesn’t thaw until sellers start lowering their prices far enough. Brokers play a role in conveying this new market reality – after years of rising prices – to their clients to make deals happen. And now everyone is trying to figure out where the market is.

“101 new listings, 101 price reductions,” quipped Thomas Stone two weeks ago.

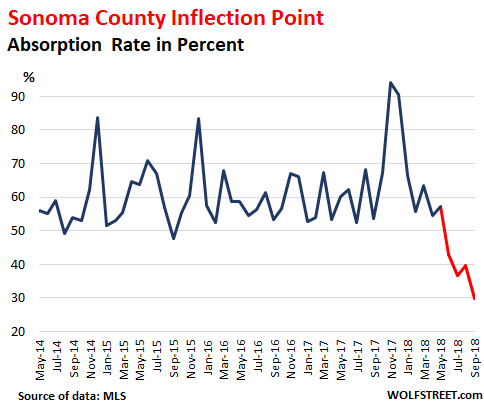

The chart below of the “Absorption Rate” (the number of sales divided by the number of homes for sale) shows the percentage of the supply that has been “absorbed” by buyers. The spike in the absorption rate late last year, peaking in November at 94%, was largely due to the fires, the most destructive on record in California. At the time, buyers – perhaps speculators hoping for a surge in prices following the fires – grabbed nearly every home that came up for sale. But then, the absorption rate fell back to normal, and continued to plunge. In September, it hit 30%, the lowest in years (red indicates the moves since the June inflection point):

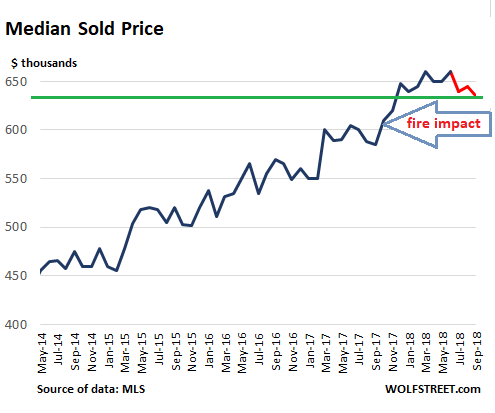

These metrics outline what has been happening beneath the surface of the housing market. But even on the surface, the deterioration is starting to show. In September, the “median price” – which means 50% of the homes sold for more, and 50% sold for less – dropped to $635,000, the lowest since November last year:

Prices in the county had surged in late 2017, largely due to the fires and perhaps the speculation following them. This impacts the year-over-year comparisons, and so the median price was still up 8.5% from September last year.

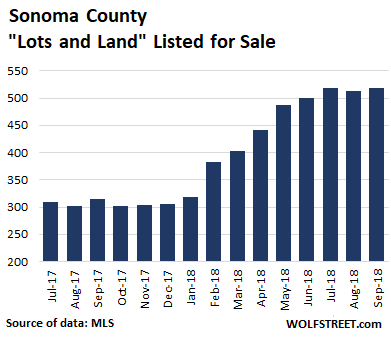

The data above is for inhabitable homes. “Lots and Land” is a separate category in MLS data; and these properties are not included in the above metrics. Homes that burned down during the fires and are now for sale are in MLS’s “Lots and Land” category.

Every month in the second half last year, there were just over 300 properties in the “Lots and Land” category listed for sale. But in January, as the burned-down homes came on the market, the listings began surging, reaching 519 listings in September, up 65% year over year. But only 23 lots sold in September:

How to deal with this market? “Condition issues are becoming more important as buyers become aware of how busy local contractors are,” Stone mused. “Local Contractors are booked out for two years or more. And out-of-the-area contractors are SOL if they want to use local subcontractors.” So potential buyers are starting to avoid homes that need work – now that the heat in the market has dissipated. And homes in great condition sell faster.

And there’s a side effect: “If you can swing a hammer without falling down too often, you can work as many hours as you want,” Stone says.

Even in San Francisco, the housing market isn’t that much fun anymore. Read… “Trump Bump” Peaked in San Francisco’s Housing Bubble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I really wish you weren’t using Sonoma county for the case study. I feel like it is too much of an outlier with the effects of the fires from 2017.

I believe the narrative to be true, but I find it hard to reconcile the hypothesis and the data from Sonoma due to the unique nature of the area.

With that said, keep up the good work. Love your analysis and commentary. I also appreciate the comment section.

Cheers.

I would love to get this level of detailed data for other cities. I also have access to similar data for San Francisco, which I posted a few days ago, with similar results. But that’s about it. If there are brokers out there willing to send me MLS data for their city, please do so!!

This type of data shows the principles at work in a real-estate downturn, long before the downturn shows up in indices such as the Case-Shiller. Brokers are fully aware of this.

And yes, in effect, every market is an “outlier” because real estate is local, and all markets behave differently — at least to some extent.

The MLS system sounds like a deliberate attempt to make the real estate market opaque to the general public. If any really good deals come up for sale, guess who gets the first chance to buy? The agents themselves! And it logically follows that if an agent is showing you a property to buy, it isn’t a good deal. They have already passed on the opportunity to buy it.

MLS is just a cooperative effort to show all listings and all sales by all brokers in one place. It has helped clear up some opacity in real estate.

Maybe I don’t understand the MLS system. I thought you had to have a real estate license and belong to a brokerage to access the data?

Ted Freeman,

Your understanding in that sense is correct: The MLS is not a free public data base that anyone can peruse. It’s a cooperative effort for brokers by brokers.

But it’s not a secret either. Brokerages and others, such as Zillow, get their data from it and send their data to it. The listings you see on Zillow are in part based on MLS data and in part on direct submissions that can include new construction and the like that might not be sold through a broker.

The MLS data base is the broadest data base of listings and sales.

But it doesn’t cover all sales. There are some properties that are never listed for sale, and so they never appear on the MLS, and when they sell, the sale does not show up on the MLS either. Years ago, I sold my condo that way. I sold directly without listing it and without broker. That sale bypassed the MLS or any broker data entirely.

Also, large developments that have their own sales offices and do not use brokers to sell the homes (houses or condos) don’t list their units on the MLS, and sales and prices do not appear on the MLS. This is part of the reason why true supply of condos for sale in cities with construction booms (Seattle) remains a guessing game — because they’re not on the MLS.

I used to live in Sebastopol (1987-2008), and it is pretty strange to see houses I know personally being used as market indicators.

I agree with your overall assessment. While there has been a bump in the market due to the fires, the real story is that interest rate are rising. Specifically:

-Many first-time buyers no longer qualify for a mortgage.

-People who were planning to sell their starter home and move up can’t find a suitable buyer.

-People who were thinking of downsizing find that the numbers no longer work out, since the monthly payment on the new place has increased.

I do not expect this to get better for at least 1-2 years.

It’s not just Sonoma County CA. Dallas-Fort Worth just saw the largest sales decline in 7 years. Various DFW submarkets are seeing even steeper sales drops, and this is happening with price points that are much cheaper than your California real estate. Everywhere you look there are inflection points popping up in various real estate markets across the U.S. because the housing echo bubble is just that…a bubble driven on the back of central bank/govt intervention. https://aaronlayman.com/2018/10/denton-county-home-sales-see-big-september-decline/

It would also make sense to step back and wait for the 3rd lanes to be finished on 101 N and S.

$980,000 to $830,000 in 4 months?! OUCH

Hopefully for the sellers sake, they bought 20 years ago and didn’t use the place like an ATM machine!

Yes, I always roll my eyes at ads talking about “tapping your equity.” It may be necessary if the alternative is worse – otherwise, bad idea.

“Tapping your Equity” makes good sense for about 20% of the people who do it.

It’s about the same for reverse mortgages.

Bebgie, it’s been in the same family since 1973 according to the tax records which also show an assessed value of $108K and change.

And as of 12:30 I’m showing 50 new listings and 49 price reductions along with 14 homes back on the market.

Buyers set the price and a property is always worth exactly as much as someone is willing to pay for it in cash, today.

What I believe we are seeing in my neck of the woods (Portland, Maine), MA., CT., NY., NJ. residents taking their equity off the table and buying here at MUCH lower prices but enjoying a much higher quality of life-although at equally lower incomes. Prices are crazy, though, as far as I’m concerned

I was in Portland, Maine in May and was shocked to see prices nearly as high as here in Seattle.. Not as high as the Seattle downtown core but almost as high as the Seattle suburbs and outlying neighborhoods.

My daughter and her husband are planning on buying in Portland or in the area and I’ve been nearly begging them to hold off because this is going to crack.. The last real estate bust happened first in Calif. and spread proving to me that real estate is not all local.. A financial crisis will hit all markets. It took a year or so to spread but once it got going it was a conflagration.

I believe the market has already turned. I live in a wealthy suburb of Portland and according to Zillow, the value of my house has decreased by $75k in the last six months. I would advise them to hold off on a purchase. They’ll be glad they did.

Portland is an awesome city but is getting crazy expensive and the taxes are the highest in the area

And freezing their Apple pies off!

How much are taxes on a value of $108K ?

In California that’s about $1500. What a deal! The American Dream!

My theory would be that the combination of the Sonoma County fires and realization that wines with the Sonoma and Napa valley labels are grossly overpriced (you can get some great reds from Argentina and Spain these days, super cheap, as their economies have tanked) have put a serious crimp on the wine industry there, adding to the economic woes and drop in housing prices.

Any data as to how the Sonoma/Napa wibe industry is doing?

Sonoma Grapes: Last time I asked, the vineyard developers were paying more for land than the condo developers. When you consider that vineyard prices are relatively insensitive to interest rates, I suspect that the relative condo sales are actually down.

People are still willing to pay $40/bottle for your basic Sonoma Pinot.

1-year anniversary of the North Bay Tubbs Fire, the most destructive wildfire in California history, burning parts of Napa, Sonoma, and Lake counties. Lots of anniversary coverage on the bay area news channels last evening, but one of the segments focusing on a selected fire victim’s rebuilding efforts really gave me pause – they showed an aerial drone-view shot of the fellow’s new home under construction on the same lot as the old, the new place’s wood framing was complete and the external plywood sheathing was about 2/3 done. Accompanying commentary: “One year later —-‘s new house is finally looking like a …” – the voiceover continued with ‘home’, but on seeing the wooden matchstick-looking assembly I just blurted out ‘tinderbox’.

I realize getting paid only replacement value for one’s home by the insurance company may not leave a lot of options as far as materials and dwelling style go, but seriously, one would hope that of all those folks rebuilding in wildfire country, one would see at least a few new dwellings of smaller, built-into-the-earth, less-flammable-materials (e.g. adobe with tile or living-garden roof) variety – but all the new construction I saw in the anniversary coverage was exactly the same kind as the old. If nothing else, I would’ve expected hefty fire-insurance hikes on that kind of structure to have incentivized folks to choose lower-risk alternatives.

Would appreciate any insight into the dearth of fire-resistant construction from Tom and any others – is it a resale-value thing? Lack of available builders for such homes? Simple greed-for-square-footage?

You can build a normal looking house with all Class A fire rated materials, steel frame, metal/clay roof, concrete cinder block walls, non flammable Air Krete insulation, etc. That’s what I did. It will just cost twice as much to build and you’ll never get your money back in the market value cuz nobody else will care. Insurance will not pay for this extra cost, you will have to out if pocket

EWMayer,

Most were substantially underinsured and only about a third of the burned out homeowners have settled with their insurance companies.

Some are rebuilding in a fire resistant style, and I’d like to see more of that, however it does cost more and it’s unaffordable for most.

It’s a mess.

It’s the outside that matters: ceramic tile roof especially, and stucco or stone exterior make a big difference. And cut the vegetation and trees around the home so that the fire doesn’t have fuel near the home. There are many other ways with which people can reduce the risks. But if your home is in the middle of a firestorm that is so hot it melts dirt into a glassy substance, I’m not sure anything outside a concrete bunker without windows would survive.

Stucco siding and clay tile roofs help, but in a firestorm with embers blowing everwhere, it’s the exposed flammable parts of the house that these embers latch onto that burn those types of houses down also. Thats why everything has to be Class A fire rated or better

Clay tile roofs are merely decorative- what actually keeps the roof dry is usually an underlying tar or asphalt based covering sheet which may have Class A fire rated properties or may burn better and faster than wood. Under that is usually plywood or particle board, also either fire rated or as flammable as kindling. Birds and small critters often get under the clay tiles and build nice flammable nests under clay tile roofs which can catch embers and start a roof fire

You could easily use a corrugated galvanized steel metal roof, either as the primary roof or as the structural board to hold the clay tiles, instead of this wood board, but few people do that. I did.

Under the roof, fiberglass insulation is the most commonly used. This is not fire resistant unless you spec for that, or use more fire resistant rock wool or inflammable Air Krete. Other common insulations used can also be highly flammable.

On the outside of the house, even with stucco siding, the wood in the eves will catch fire easily from these flying embers, unless spec’ed out to be Class A fire resistant. Same with wood frame windows. These small fires then spread to the structural wood frame of the house that the eaves and windows are attached to. Which is the reason to use steel framing and/or concrete/ cinder block in the structural frame of the house

Probably just dipping into their home equity to purchase more oversold Tesla stock.

Zillow is not a bad site to get a reasonable range of value. So I checked out the two houses in Sebastapol.

The one at 1704 Hurlbut Ave. was asking way above value. It had increased in value 10% since 2016 but they were asking 38% above the 2016 value.

The house on Sextonview is valued at 1 million, so it seems to be simply another case of greed/optimism. It’s only 1,470 sq. ft. after all.

You want a real reality check on prices? Check out the Redfin values. In my area, they are much lower than Zestimates, and probably reflect a buyers offer more accurately.

Meh, I checked their tax history, both these guys can afford to drop prices by quite a bit and still get away with it. Sextonview was purchased in 2004 from the looks of it at around $850K or so. The Hulbert one didn’t even have a record of sale, but from the tax history, looks like the base was at <$150K.

I think in both cases, they are doing fine even if they cut the prices down. The question I have is whether their original list price was the suggestion of their realtor, or their own idea. If it was the realtor, then the realtor isn't helping the situation. If it was the owner who insisted on the pricing, then they really should have listened to their realtor.

Usually a house with multiple price reductions would elicit the "What's wrong with this place question." Ultimately, not a good thing for the seller.

I think it’s great to see some air come out of the market. Not to mention, people are always the same – the higher the price of an asset seems to go, the more people line up to pay it. The lower the price goes, the greater value that is created.

You can see it everywhere. In the restaurant world in SF – people seem to enjoy standing on line at very marginal places at best. We live in an age of a very non-discerning populace.

Is a reduction in an aspirational price a real reduction?

Is a 25% discount on a Cartier watch a bargain?

The answer to both questions is no.

Yes, asking prices will fall, but I won’t hold my breath for a 50% off sale, which is a buyer aspirational price, that is not likely to happen.

I thought the same in 2006/2007 and the rest is history unless this time is truly different!

This time is different. No liar loans, zero down, and AAA rated MBS repackaged manure.

Only time would tell

California has seen many boom and burst and the effect is same all the time :: prices going down and the reasons were different all the time

We would see how does this any out this time.

In san Diego I m seeing homes staying longer in market and multiple price reductions which are unheard of last year

At the end of the day all it matters is if people are able to pay the house price either in cash or monthly mortgage

Typically, the hold off starts because of a trigger. Six months later, there are worse problems in the economy and a lot of people lose actual jobs, rendering a mortgage impossible.

So, it might actually fall 50%. Remember, we never structurally fixed any problem from 2008.

Great info, guys, but all real estate is local. Sonoma and Napa are quite a bit different from the valley, and even SF, or Oakland, how much of this do you think translate more broadly into the bay area markets?

There is also the issue of the wildfires affecting Sonoma area, I know it seems like there was an artificial effect in pricing, do you think this has been carried a little further along than it might have otherwise?

The crack in the market comes when buyers can’t come up with the asking prices. There are markets around the world where buyers put down deposits on new construction and can’t close because they no longer qualify for financing or the prices have dropped wiping out their equity. I saw stories on these scenarios coming out of Canada, Australia, and China.

One guy out of Vancouver was trying to figure out if the Chinese investors there were selling. He used an unusual method to try to ascertain the ratio of sellers who where Chinese. He counted up all the houses for sale listed by Chinese real estate agents. It was a big chunk of the market.

Rumour on a place down the road from me about 1/2 mile says an older couple bought the place sight unseen off a Facebook add. Not only is the house a complete shack with no heat source beyond an old beater wood stove in an annex, it is the worst construction I have ever seen; walls out of plumb, ceiling joists that don’t reach a supporting wall, unfinished drywall, headers at head cracking face smashing height, etc. The buyer guy says he plans to put in a small shingle mill. (no cedar available here…all sold). I reassured a friend of mine who lives across the street it won’t happen. Oh yeah, even the well is contaminated.

The renters, who wanted to buy it but don’t have a down payment, are freaking out because there is nothing to rent at all in our Valley. Meanwhile, chickens and a goat have taken over the solarium and have roosted/bedded down there for over a year. Apparently, the doo doo is 6 inches deep. $400,000 for 4.5 acres of gravel and swamp, sight unseen, all the manure you could hope for.

Crazy BC housing market and renters being forced out with nowhere to go. Downturn has hit Vancouver, but unfortunately we have been discovered and prices are adjusting to the fame.

An article in Sunday’s L.A. Times would seem to imply that the R.E. game of upward spiraling prices is due to reverse. We know that empty-nesters and seniors don’t need Macmansions. So one stat that made me gulp:

“Seniors will be California’s fastest-growing population. Between now and 2026, the number of Californians 65 and older is expected to climb by 2.1 million, according to projections by the state Department of Finance. By contrast, the number of 25- to 64-year-olds is projected to grow by just more than half a million; the number of Californians younger than 25 will grow by a mere 2,500.”

http://www.latimes.com/projects/la-pol-ca-next-california-demographics/

Any info on what closing prices were for the area in the last month? It could be that sellers just can’t reach for the stars any longer? YOY selling prices for comps?

“Closing prices?” Do you mean selling prices — the price at which homes sold? Yes, the answer to that is “median sold price,” which is represented by the second to last chart.

So remember when I said this was going to be the green year, green for US dollars?

Buying the same house for less money means a stronger dollar, right?

Not to mention a lot of currencies have lost value against the dollar this year.

Maybe inflation means the dollar purchase value has gone down in general from last year but look, houses are cheaper!

Not everywhere of course but you can’t have everything.

Real estate is local… ish? Rates, Federal law, taxes/incentives aren’t, hype and FOMO, developers/investers… Even Jobs and population move when the economics are persuasive. I find that axiom a bit suspect. Like, true, but only partially. Only locally. ;)

Also, it *seems* like RE prices are nuts everywhere. Some more than others, but I see remote not-bedroom-community-try-finding-a-job towns nearly matching city prices.

Why? Maybe because it’s been engineered that way to blow air back into the bull-shaped-parade-baloon that IS our financial infrastructure? To re-inflate assets that ended up flat, on the plate of “too big” organisms? Just a wild, uneducated guess.

Anyway, my friends own a vacay in Sonoma. They’ll survive. If you can sign a million-dollar mortgage, you can handle a 10% loss on your “investment”. Yachts depreciate pretty rapidly too, but no bailouts. Yet. No pun intended.

If you have to borrow it, you cant afford it regardless of price.

Hi Wolf,

Thanks for all the good work. Apologies if I’ve missed this but have you conducted any research and analysis that highlights when home values are historically inexpensive relative to other asset classes?