The inflection point was in June. This is how inflection points show up at the subcutaneous level in all housing markets.

The first obvious sign that something was up, that something wasn’t going the right way, came on June 6, 2017, when the housing market in Sonoma County was still booming, according to the data. Sonoma County is a little north of San Francisco, between the Pacific and Napa County. It’s wine and craft-brew country, sprinkled with beautiful cities and towns. And it’s pricy.

“I haven’t seen this one before,” Thomas Stone, a broker in Sonoma County, told me at the time. “Food and booze yes. But $1,000 cash seems qualitatively different.” He’d received the offer of a $1000 cash raffle by Sotheby’s for a broker’s tour of four homes in the city of Novato that Sotheby’s was trying to sell. The $1,000 would go to the winning broker. “Visit All Four Luxury Properties in Novato to Win!” the brochure said (I added the red marks):

These kinds of antics are an early sign that it’s getting tougher to sell homes at the prices sellers envision. But then came the horrific wildfires that spread across several counties in Northern California, including Sonoma and Napa, killing 43 people, and burning down thousands of homes, including entire neighborhoods in Sonoma County’s largest city, Santa Rosa. The destruction created a burst of demand in some zip codes, but it didn’t last long.

And a year after the $1,000 cash raffle flier had gone out, the inflection point of Sonoma County’s housing market became visible in the subcutaneous data from the Multiple Listing Services (MLS).

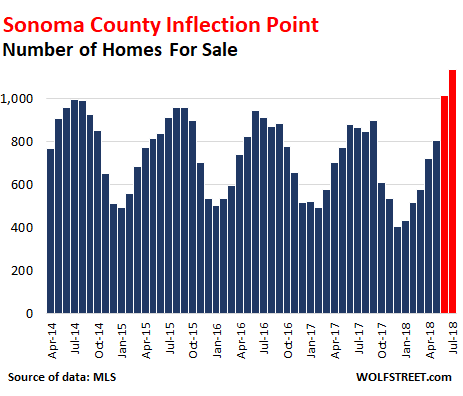

In June and July 2018, supply suddenly shot to the highest level in years. The chart below shows the number of homes listed for sale in the county. Both June (1,014 homes listed for sale) and July (1,135 homes listed for sale) hit the highest levels in the data going back to 2014:

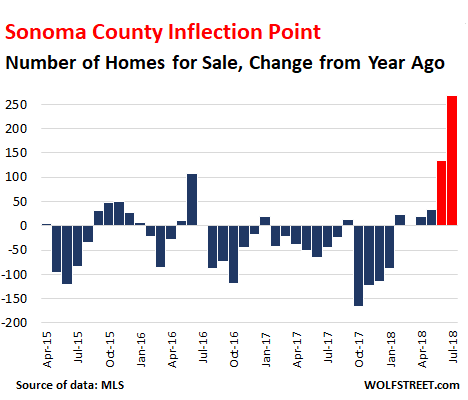

This inflection point becomes even more obvious in the year-over-year increase in the number of homes listed for sale:

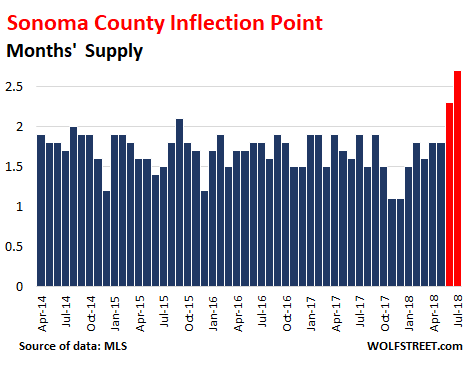

Months’ supply of homes for sale – the number of homes for sale divided by the number of homes sold – jumped from 1.6 months in June 2017 to 2.3 months in June 2018. In July, it jumped to 2.7 months:

Toward the end of July, Stone said: “The last three weekly office meetings have been focusing on the changing market, how to prepare sellers for lower prices when taking a listing and how to change your marketing to take advantage of the change.”

Brokers only make money when there is a sale. When sellers are asking for more money than buyers are willing to pay, sales stall, and the market grinds down, and volume falls off – until sellers start lowering their prices. It is the brokers’ job to convey a sense of reality to their clients — the sellers.

Stone added another data bit: Of the 114 “new” listings at the time, 30 had been listed before, and had been pulled because they didn’t sell, and now were back on the market as “new” listings.

And there were 94 price reductions. “Some days the price reductions alone exceed new listings,” he said.

However, this doesn’t include homes that had been listed at a higher asking price, pulled off the market, and later relisted at a lower asking price. If the home sells at the latest and lower asking price, it’s considered “at asking,” though at its prior listing, it had had a higher asking price but didn’t sell.

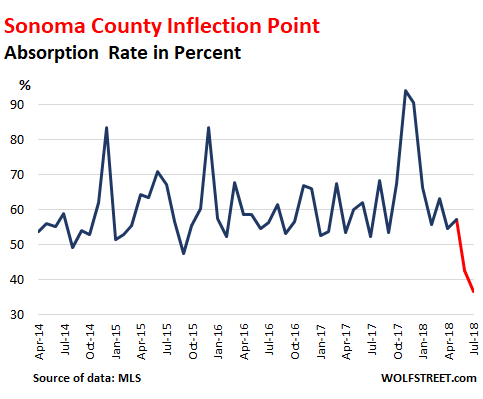

The chart below shows the “Absorption Rate” (the number of closed sales divided by the number of homes for sale). It shows the percentage of the supply that has been “absorbed” by the market. The spike late last year to 94% was in part due to the fires. But in June this year, the market only absorbed 43% of the supply, the lowest in years, and in July, the market only absorbed 37%:

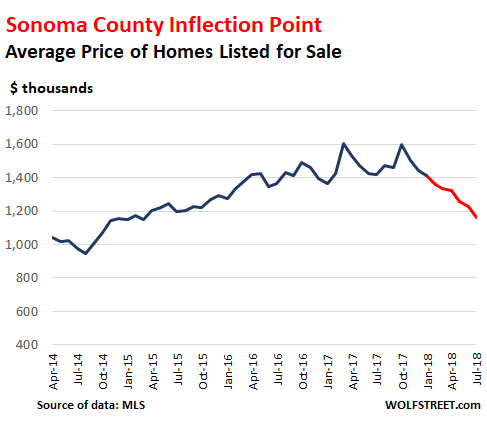

So in this kind of market where the inflection point has become visible to industry insiders, what should sellers do so that their house will sell? Lower the asking price. The chart below shows the “average asking price” of homes listed for sale:

The average “asking price” in July dropped 18% year-over-year to $1.16 million, the lowest since the spring of 2015. Some caution is advised: “Average” asking prices (sum of all asking prices divided by the number of all homes for sale) can be skewed by a small number of very expensive homes that might not sell for a long time and remain in the asking price data for a long time. So the “average asking price” is a lot higher than the “median” price of homes that actually sold. More on those in a moment. Nevertheless, this is a big and consistent move.

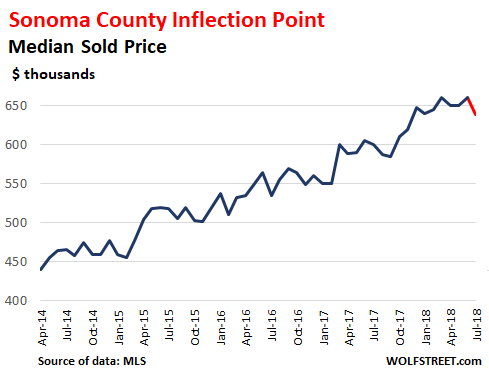

So, what about the median prices at which homes actually sold? The “median sold price” – which means 50% of the homes sold for more, and 50% sold for less – in July dropped to $639,000 – the lowest for the year. But it was still up 6.5% from July last year, and many stories in the media cite this number to show that the housing market is still hot:

A home is considered sold when the sale has closed. There is some delay between the signing of the contract and the closing of the sale, and the median price in July reflects many deals that were made in a prior month.

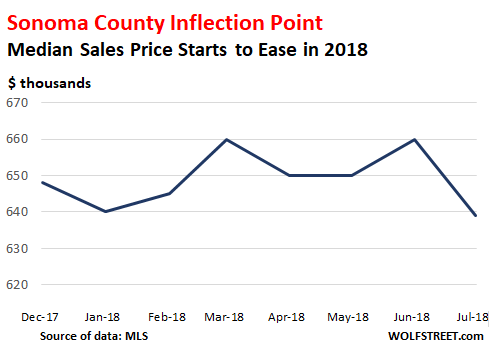

But to see what has been happening this year, let’s put the median prices for 2018 under the microscope. July was the low point so far this year, and the lowest since November 2017:

The median price is the last metric to move, and it has met its inflection point in July.

When I talked with Stone a few days ago, he mentioned that the weekly office meetings still focused on how to get sellers to be more realistic. This has now been the case for five weeks in a row. The “vast majority of brokers, except for a few eternal optimists,” expect prices to skid, he said. He expects a 25% correction over the next three years. And the above charts show how it starts at the subcutaneous level, for industry insiders to see, but before it turns into media-ready year-over-year declines in the median price that causes so much wailing and gnashing of teeth.

The Case-Shiller Home Price Index, the way it is designed, lags about three months behind the median price data. According to it, there is a historic spike in Seattle, sharp increases in other metros, but New York condos fall. Read… The Most Splendid Housing Bubbles in America

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank you, Wolf , for thisI illuminating analysis and commentary. Will you be extending this to integrate effects of population/household levels and changes plus supply changes, esp new housing unit additions?

Look forward to seeing you doing similar investigations of other NorCal markets, esp SF and Marin, both overall and the luxury segment.

The more pertinent question would be will it bite the banks? If yes, when? Because at that stage we can expect a bailout. if not, it is a non-issue. That is privatize profits, socialize losses for you.

It’s not hard to imagine the public completely turning on the banks and forceably banishing that species of parasite from the economy forever should they trigger just one more financial crisis on us.

Wishful thinking … the ‘public’ has the attention span of a flea (or a dog when you shout ‘squirrel!’).

Would there still be credit unions? I will need a mortgage after the crash asap but if credit dries up as banks are banished I’m gonna need you to sell me your house for less than $50,000. For the next generation I beg of you.

This can be done by an individual by not borrowing money or at least by speedily paying back loans.

I’m sure the NAR ( National Association of Rodents) will give us accurate information. Certainly they have only our best interests at heart.

I remember once listening to a radio show by a local real estate brokerage here in NYC. A caller was complaining that her house in New Jersey wasn’t selling and going into loving detail about all her home’s amenities and heaping abuse upon all the prospective buyers out there who didn’t appreciate how great her home was. The broker interrupted and said, “If you listed your home for one dollar, would it sell?” The caller said, “What’s your point?” and the broker said, “My point is that there is always a price at which a home will sell,” and the caller said angrily, “Well, I’m not giving my home away.”

I think realistic pricing does not occur until the homeowner becomes desperate to get out from under the property taxes, or desperate to get out of the neighborhood for any reason.

Good point.

MANY people are trying to get out of their house in NJ and Long Island and Westchester county where taxes have skyrocketed incredibly. Some 1000% in Scarsdale.

Good luck with that.

A yes, the good ol’ “I’m not giving it away!”. Always love that one. Sure sign of greed, sense of self-entitlement and detachment from reality,

As the saying goes…”Price cures all defects.” :)

You can see things shifting here in the formerly red-hot DFW area as well. Some sellers have hit the market late in the summer in what I will politely describe as a fishing expedition, only to find that demand isn’t quite as robust as they assumed.

The absorption rates are declining and inventory is growing, particularly as you move up the price bands.

I noticed that Sacramento also shifted recently with sales down and inventory sharply higher.

Did someone just ring a bell?

Simple. The markets owe you nothing

You get what the market is willing to give you. Always amuses me when sellers think the market “owes” them

After months of Seattle times headlines

Of the HOT housing market. Last week the headlines. Is the housing market finally cooling

https://www.seattletimes.com/business/real-estate/u-s-housing-market-may-be-headed-for-biggest-slowdown-in-years/

Comments:

– Even Texas seeing a slowdown ? I am both NOT surprised and surprised at the same time.

– Also throw in the new federal tax laws regarding the deductions for interest paid on those mortgages and the deductions for state and local taxes.

– The FED raised interest rates but people with a mortgage DO NOT pay a rate linked to the FED’s fund rate/short term rates. It’s the long term rate that determine the rate on a mortgage. And those have been drifting higher in the last say 2 years.

DFW was also building a crap load of affordable homes and demand there was clearly in response to people moving their for work.

When I looked out their for homes just on Redfin this spring, there were a fair amount of new homes in Allen, Mckinney and Frisco.

At some point building was bound to catch up with demand.

I can’t think of anywhere in SoCal within 1 hours drive of work that has new affordable home in a good school district…

Intersting Wolf. I do believe housing prices are peaking in most markets.

Sonoma may not be a good choice for analysis. I would suspect that the devastating fire of last year did two things: 1) Increase supply as some decide to move away from the fire prone area and 2) Decrease demand as buyers have no interest in suffering those kind of losses.

The Sonoma fire was bad news. More of these will occur throughout the west and even in my neck of the woods (North Carolina mountains), we saw the first wildfires in many years just two years ago after a long draught summer).

Thanks for the analysis.

That prediction of a 25% price correction ( Inflation adjusted) over about 3 years in the county wide median price is based on the assumption that this is a normal Real Estate cycle.

That’s a conservative prediction based on past cycles, it might be a bit more.

We don’t have the criminal loans of the last bust to deal with and buyers for the most part now have skin in the game, barring a significant exogenous event this looks like a “Normal” Real Estate cycle.

Keep in mind that we are talking about “Median price”, different market segments and different price tiers will react differently.

As “Jim the Realtor” is fond of saying “There’s nothing price can’t fix”.

To confirm for our readers: Long-time commenter Tom Stone is the Thomas Stone cited in the article.

2008 was about17 quarter point increases of short interest rates and the forecast of 4 more before end of 2008? The mortgages fell before the prices and massive job losses took all the press?

This time it will be a true opportunity to hold ones nose and wade into the blood soaked avenues?

I see one variable that is different from the the last bust , and that is the number/percentage of non resident owners . Will it make a difference ?

Check out the last 6 months of this data set and tell me if you think it looks like an inflection point.

https://fred.stlouisfed.org/series/MSPNHSUS

Its local until it isnt? How come the can is wrapping itself around my foot every time i kick? A grand! We have fallen far from glengary glen ross?

YOY change for both May and June on that chart are -4%. Yes????…. Although it would be nice to get a couple more data points. Housing is so damn slow!

Four more hikes in the next four months? Cadaver says yeah!

Excellent information:

Point 1. If one looks at the July period for the last 4 years it appears ( median prices ) that there has also be a decline or slump. The chart and data is very bumpy and not smoothed so more detail analysis would be required. Perhaps others could support or refute.

Point 2. A more relevant measure might be “dollars per square foot” as this works to equalize all the various differences. Realtor have these numbers in “listed / asking ” and “sold” and percent of asking the property sold for. This delivers much more granular data for trend analysis.

R Hughes,

As I said in the article: “The “median price is the last metric to move.” That’s why I showed the other metrics. They point in the direction where the median price is headed.

Here is the chart with median price per square foot in red, right scale:

I mentioned on this forum several years ago that my nephew bought a small rancher in Novato. I thought he was nuts buying as the purchase price was $750,000 at that time. A few months ago I commented to his mom that now might be a good idea to sell, capture some appreciation, and get off the hamster wheel by moving. (He hates his job and commute and she brought up the subject…..I didn’t). He could relocate and buy a house for cash and work even part-time or at something he likes doing. His mom thought my suggestion was crazy talk; crazy brother talk from Canada.

I watched these folks ride the Seattle 2008 bust to a loss and fear we are going to see the same thing again. I say what I think on Wolf Street, but on Family Street I usually keep my mouth shut as I understand solutions that worked for me doesn’t suit others. This time and place is different I suppose.

It’s frustrating watching the train gathering speed and making sparks while my family waves from the coach windows.

Paulo,

Good points. Although I am older and still running my business, I am a FIRE proponent. Was talking with GF how out of step I was in the 1980s; no debt, paid off house and basically worked first toward a point where I could flip burgers, then passive income from rentals supports me. I remarked that I think consumerism keeps people speculating. Sure, you can live in Midwest on $40k a year, but you cannot tap home equity for $125k car, $100k pool remodel, etc. Basically, mindset has to change.

I can see the same thing in Florida. There was a big run up in prices between July ‘17 and April ‘18 (after years of somewhat more moderate, but steady increases). Then in June prices flatlined and are now starting to come down just a bit.

Seems to me that we’ve probably hit the top of the real estate cycle, especially with interest rates rising. At this point, nationwide house prices are still about 15% below the 2006 peak in real terms (adjusting for median household income growth). However, I don’t think we’ll surpass the previous peak. As I’ve mentioned on this site before, I expect a correction of 15-25% in terms of real nationwide house prices in the next 2-3 years.

The house I lost in Florida is now worth about 20% less than it was in 2007, the peak for me. If you are correct and it drops another 25% that would put it at the price I paid in 2002.

The economics of real estate in Florida are really interesting these days. Someone we know, who bought at the peak in 2007, recently sold taking a ~15% loss. They traded up to an underwater property whose owners were taking a ~25% loss.

Yeah, my gut feel is that in two to three years we’ll see prices at about one third to 40% below the 2006 peak in real terms. In the long run prices will tend to mean revert to a certain long term range of income to price ratio, as do rental cap rates/yields.

Also, folks shouldn’t get too hung up on nominal price levels – they’re meaningless, especially when by the time the down cycle works its way we’ll be comparing a peak to a traugh with a gap of more than 15 years between them.

I still see real estate holding up.Most people I talk to would rather

have property than cash.They cite the rapidly declining

purchasing power of money.

It holds up until the value of the house drops to a point where they can no longer use their home as an asset for borrowing more money. Then the small return on cash looks much better than the loss in borrowing power.

Hurray for debt slaves!

This type of thinking will be the failure of the majority.

People have been led into the real estate corral because it has gone up and u do get the tax right offs.

But in a falling or flat market, u lose and it can be big. As an earlier poster stated, many / most in the Northeast are straining under >$8,000/yr property taxes.

What happens when/if they lose jobs / income decreases / they retire and go on pension/social security as the cycle turns down?

Then they will realize how as a “ property owner“ they are playing the role not of a “debt slave” but of a “government serf”.

I heard two retired ladies, both from PA, complain on a call in show that even though they had retired with adequate incomes, medicare costs and school taxes were driving them into hardship. My impression was they both knew they couldn’t hold on to their homes beyond the next few years.

After seeing my inlaws’ home taken by medicare, I would advise both these ladies to sell their homes and rent. Never mind waiting to sell into a declining market.

Can Medicare take a home that is fully loaned without mortgage?

What do you mean by “medicare took your in laws’ home”?

Max,

My mother in law was in hospice for a long time, medicare charged whatever benefits she received from them against her estate. When she died they took the little $50K condo she owned.

Most people don’t realize that if they get sick in retirement, their children will get nothing when they die.

I think it would be Medicaid not Medicare.

Medicaid makes you disperse all assets before you can take advantage of the benefits, i.e. nursing home.

@Petunia, that doesn’t sound like a hospice situation involving Medicare. It sounds like Medicaid and a nursing home situation.

Max & TX,

Everybody thinks it’s a mistake but it’s not. My mother in law had social security, a post office pension, plus medicare, so didn’t qualify for medicaid. Medicare charges back medical costs to the estates of patients with large payouts.

@Petunia, I have never heard of a cost recovery procedure for Medicare. I don’t think such a concept exists. I have even tried souring the interwebs and can’t find a single reference to such a process.

I am guessing one of two things really happened… either it was really Medicaid (or whatever your state calls it) or your in-law wasn’t covered under Medicaid but needed long-term nursing home care, which is not covered under regular Medicare and perhaps it was the nursing home which sought recovery.

@Petunia – to add to the above, the only way I know that the government might seek recovery in case of Medicare is if there a third party liability involved and an award or settlement in case of an injury. For example, if your in-law was injured and received an insurance settlement due to the injury and Medicare also paid for treatment that was required as a result of the same injury then Medicare can seek recovery from an estate. (This basically makes sense as the party that was at fault for the injury should be liable for costs associated with the injury.) Other than this narrow scenario, there is no process for cost recovery I know of from an estate under Medicare.

If you or your parents own property and are elderly and in need of care that exceeds Medicare benefits, you might contemplate a reverse mortgage, pulling all the money you can from your house and stashing it so Medicare can’t take it.

A house is a liability, which requires taxes, maintenance, operating costs, or utilities, and mortgage fees. The point of owning property is a nonstarter, when you don’t own anything but a liability.

I’ve seen some headlines on Zillow and Redfin stating the stocks have taken a hit. Another indication the trend may be down.

Depends on what country you live in. The formula in BC is a Govt. or subsidised care facility gets 80% of a resident’s income with no minimum. If someone earns $1,000/month pension income, the facility gets $800 of it with the balance made up by directed tax dollars. (Cheaper than seeing old folks decline in hospital). Assets are not touched and allowed to go to family as per situation. Obviously, rich folks choose fully private care which is almost resort-like, (Berwick by the Sea). My mom, who just passed away Saturday, was in an excellent facility for 8.5 years as she declined with Alzheimers. The facility was first class and the workers became as close as family over the years. My brother and I kept her at home until looking after her was impossible for us. Her GP made the call and was placed within 2 weeks after a bad fall and resulting crisis.

The remaining 20% was administered by my brother and I and went for canteen goodies, special supplies like body creams etc. All required medications supplied by BC Med.

All facilities are inspected and have to meet Govt criteria/standards of care.

Aging is hard enough on its own, let alone suffering from dementia or Alzheimers. The Govt taking acquired assets is criminal as they were accumulated with after-tax dollars.

regards

There are signs that housing is reaching at least a short-term peak, and in Sonoma County there may also be some concern that building to come and an expansion of units is providing an incentive to sell now (given the recent fires and a bet that people are looking to buy while rates are still relatively low and they are closing in on the end of FEMA and insurance subsidies for rental). Good growth also provides a profit incentive like any other market.

Wolf, If and When do you expect this to begin in the heart of Silicon Valley:

1. Santa Clara county

2. Alameda county

3. San Mateo County

4. San Francisco county

With all due respect, Novato and Sonoma are on the periphery of Silly-con valley.

I posit that the farther you are from job centers, the earlier and faster the decline begins.

But until it gets to the core, the fat lady ain’t singing.

I live in the Peninsula, and I see cracks starting to show in the SF-Peninsula-SJ market. There are houses sitting on the market, and you can even find some price reductions. The high-end markets (Atherton, etc.) also seem a lot slower to me.

For the first time in years, I’m hearing homeowners say they think the value of their homes has gone down. In fact, a friend just bought an investment (rental) property in East Palo Alto earlier this year and he thinks it’s probably down at least 5% already.

Redfin CEO Glen Kelman just said they’re seeing demand on the decline:

> “For the first time in years, we are getting reports from managers of some markets that home buyer demand is waning, especially in some of Redfin’s largest markets,” Kelman said, specifically calling out Seattle, Portland and San Jose as areas where inventory was still tight but did not seem to be pushing prices higher still.

That’s from https://www.marketwatch.com/story/housing-market-has-hit-a-significant-slowdown-in-recent-weeks-redfin-ceo-says-2018-08-09

You’re right about the job centers. But I think Facebook’s 20% post-earnings drop was a warning shot for those who are paying attention. An acquaintance’s spouse works at FB and he was complaining about their finances shortly thereafter. And this is a household with an income above $400,000/year when you include stock-based compensation.

What the average person doesn’t hear about Silicon Valley’s boom is that there are still a lot of leveraged households. People have high incomes, but a lot of it is tied to the stock market and a lot of money is required to maintain their lifestyles. If home values and stock values go down even 10-15%, I think many of them will be under a lot more strain than many expect.

The “average” U S household income is around $53,650. Households with $250K and above are in the top 5% of income earners.

Most of us do not live in SF, Seattle, NY and similar. To get a more “realistic” sense of this housing market, you’ll want to extend your thinking beyond the Bay Area. I don’t mean to be too rude, after all, for thousands of years, it was believed that the sun circles the earth.

The person I was responding to seemed to be suggesting that a decline isn’t apparent in the hottest Bay Area markets when, in fact, cracks are starting to show.

If demand is down in hot markets like Silicon Valley, where buyers need substantial down payments and multiples of the US median income to qualify for a mortgage, even as supply is increasing and prices seem to have stopped rising, that probably doesn’t bode well for the rest of the market.

When what’s happening in Turkey, Brazil,Argentina spills to US. POTUS Trump is smiling at this moment because when EM collapse, money flows back to US. There would be a point the world will drag US down. Where would money flow into at that time? If there is no place for money to go, the money will be slaughtered, destroyed by falling prices of everything which drags down debt amd drive up backrupcies. The D word which FED will NOT allow. Turn on printer again? Hmmmmm

Prior to the GFC in 2008-09…”….a ‘match'” was lit somewhere in the San Joaquin Valley around Bakersfield. Didn’t take but few months for a real estate sell firestorm engulfed most of the state and then the nation. One of my children (an adult even then) had his “mortgage wholesale money” territory down there….the stories that changed like a swift moving river from plus to real, real minus was incredible….almost day to day! The further you are from the “core” of the SF Peninsula the faster prices will drop and the steepest. Anyone who still believes today that the best “investment” is real estate for the purpose of quick ATM returns is batty.

Good to hear from Tom Stone again. It’s been

a long time since the old Calculated Risk days.

I lost of count of all the lots for sale around Santa Rosa on Zillow. Zillow has over 500 properties including various lots for sale in Sonoma county. One of the surprising area is Fountaingrove the wealthy subdivision in Santa Rosa that took the fire hit. Large number of lots for sale which is a good indication that many of these wealthy homes had large mortgages and the insurance company used the fire insurance money to pay off these mortgages leaving the owners with burned out lots for sale and hoping someone has the cash to buy them. These unlucky home owners need to get a construction loan to rebuild in a time frame of high construction costs along with having to go through the entire loan approval process which itself could eliminate many of them based on job and income verifications.

The other issue is the large number of cabins, studio’s and even large vacation rentals throughout Sonoma County dependent on the wine tourist business which has been hit hard by the fires, many of these properties depend on rental income to pay there mortgage. It’s my guess a significant number of these vacation rentals are on the market as they not only face a declining rental demand but higher overhead prices as fire insurance rates skyrocket in the local area.

Are any of the mega landlords taking a hit from all the CA fires?

Doubt it, they are more likely buying up established neighborhoods inside the zone. They have to buy insurance too.

Lots are going down in price because of increased regulations and costs to build and the fact that insurance will not cover the cost to rebuild

My insurance was quoting me a (cost to rebuild) rate higher than the market value. If you have the right insurance company.

Vacant land is dropping in price. Just about any remote hillside in E Riverside Co can become a million plus home overnight. Remote parcels without utilities already have HOA. LA sits in a basin so there are natural limits. Sellers have backed off a bit, the idea that it is all going to development is baked into the cake.

Fire insurance is becoming a real problem in the hi-fire risk areas (I live in one) especially if that property is not your primary residence. Most rejected prices from original insurers double when seeking out other companies that will cover. Sometimes only Lloyd’s of London will be the only insurers; it takes lots work to get others but they are there; the prices do escalate.

It’s always about the price. Doesn’t matter if it’s a house, a car, whatever. Price it well and it will sell. I saw peak bubble coming this spring and started getting my house ready to sell. Unfortunately it took me a bit longer than I hoped and didn’t put it up until late June. I missed the absolute peak by about 6-8 weeks. Nonetheless I priced it “aggressively” as the realtards love to say but still after 3 weeks, no offers, even though about 10-12 or so people came to look. So I dropped the price by 5% and 2 days after that price drop….TA-DAH…an offer. I am scheduled to close in 2 weeks.

Meanwhile some neighbors of mine are still asking 5-10% higher than what my house will sell for. And they sit and sit. But they won’t just GIVE IT AWAY!!! lol. Good luck with that guys.

I bought the house in 2011 and will end up clearing about $285K after all buying and selling costs, including real estate commissions are counted for. Add another $30K in renovation/repair work I did over the years and I’m walking out the door with a $250K tax-free profit. All the while spending less than I would have spent on a comparable house to rent every month.

There are never absolutes in life. Anyone who says real estate is ALWAYS a good bet is idiotic. And anyone who says real estate is NEVER a good bet is also idiotic. It’s all about timing. Buy low, sell high, rent, rinse and repeat.

Now the plan is to rent for a year and see what happens. I have a feeling this crash will accelerate a lot more quickly than the 07-10 crash. It’s amazing how fast it turned this time around, going from multiple offers with no inspections in April to price drops in July. At this rate, I’ll be ready to buy back in at a 30% discount next summer.

Interesting mentioning the speed of decline…

Last time around it was overextended homeowners with loans they never should have gotten with lenders operating as pass-thru entities and investors holding the bag on the securitized loans. Tightening lending standards precluded the market turn.

This time a lot of the money is still from investors, but in large funds purchasing to rent or foreign buyers looking to just hold.

There is pent up demand from locals, but they mostly can’t afford the current prices, so this will create a floor. However, once investors get skittish, their demand can simply disappear which is why stocks like Facebook can drop 20% in a day.

Will prices quickly fall to where enough locals can afford as new construction gets hot to move, or will they linger as patient sellers turn to renting or refuse to sell and occasional locals struggle to reach as much as possible to reach their big dreams of home ownership?

Interesting question and I really don’t know.

Personally, I live in LA and I don’t think I’ll ever own a home in the area. Sure I would love to at the right price, but I don’t want to be a debt slave so I am not tempted to reach past payments of 50% of my take home pay, which leaves a yawning gap in price.

You are smart.

Wondering where are you located ?

“2 weeks to closing”

A lot of things can happen in two weeks. Like a bad inspection report and contract cancellation. Just recently happened to my son in Texas.

Keeping my fingers crossed for you.

I am a recently retired Florida Claims Adjuster. The issue also surrounding Florida real estate is the very high cost of Homeowners Insurance, Windstorm Insurance ( with very high deductibles) & Flood Insurance. In coastal counties, Windstorm Insurance is only available through the State of Florida. Two relatives from NY did not believe me until they attempted to finance a home. I am certain this has a factor in Florida Real Estate.

Rural/wilderness areas have been strong real estate markets in Calif for years. Many of these are are sold as Tourist getaways and advertised as cute, secluded, quiet, away from the noise, affordable or close enough to commute to urban Calif work.

In some ways these areas have operated as investment havens for wealthy buying property in areas such as Sonoma, Tahoe, various mountain retreats and renting out the property when they are not using it to cover the mortages but with the continued fire threats in Calif these investment must be getting a closer look as bookings decline and the physical areas themselves become less attractive due to past and present fires.

Combine this with urban sprawl replacing Ag property that border forest and wildlife areas may come under increasing price pressure as demand to live near these high fire zones become less appealing.

Overall the non urban areas of Calif that have been both a safety value for people seeking lower cost housing willing to drive long distance to work and investment/vacation spots for the wealthy could be less appealing in the future changing the Real Estate landscape significantly in the state.

How much pain is there in a 25% drop in values? You can lose your home over a REFI, and having a mostly paid off mortgage is no guarantee that the bank won’t call the paper. What is the income demographic for these people? If FB lays off half its workforce, what does that mean?

In many cases, you don’t need your cushy job at Facebook to disappear. You just need the value of your stock, which you used to qualify for your mortgage, to drop by a double-digit percent.

Outside of the Bay Area tech scene, I’m not sure how many people know that there’s a cottage industry of lenders that have popped up to lend to employees of companies like Facebook and Google. They are willing to treat stock-based compensation as income to get borrowers qualified for large loans.

Here’s an example of deal in which a couple borrowed $876,000 on a five-year ARM with 30 year amortization from a lender who was willing to include restricted stock units as income:

https://www.sfgate.com/realestate/article/Stock-units-provide-mortgage-obstacle-3689226.php

The lender even did this deal despite the fact the borrowers hadn’t yet sold an existing primary residence they already had a mortgage on.

The real stupidity of counting stock-based compensation as income is that even if you assume the employers are stable, stock is typically granted on a 4 year vesting schedule. There’s no guarantee that folks are going to continue to get the same level of stock-based compensation. In a down market, the equity gets more expensive for companies and less attractive to employees.

Finally, there’s no guarantee that folks are going to work at these companies for anywhere close to 30 years. Ageism in Silicon Valley is real, as is burnout.

Bricks are made of literal horse shit and or concrete (but those last ones might have a different name in the USA), why does people who lives in wildfire country doesn’t live in brick houses?

Is like living in an inundation prone zone and not building the house in a high place or over a platform so water doesn’t reach it.

Heck my dad build a house over a dune, he made sure it was fixed in place first, they mocked him until that year with the sea quake when water level went over a meter…

Drywall palace is cheaper than concrete

Hey Wolf,

We are seeing this in Seattle as well. Number of listings has risen to above 4,000 now and continues to rise. Anecdotally, I see a lot of “For Sale” signs driving around my expensive central Seattle neighborhood – or maybe I just notice them more now. I’m still sitting on cash and not biting until the next recession.

I do think it’s interesting that this lull in the housing market is occurring outside of a recession in the real economy or a bear market in equities. I think equity prices and home prices are probably more tightly correlated than any point in recent history. That the RE market is softening now really shows the fragility in the market: once we start to see some bad economic data and a few layoffs, the number of listings is going to skyrocket.

– There’s a joke going around in the state California:

– Question: What’s the definition of a millionaire ?

– Answer: A homeowner.

Willy2, There is a joke about Oregon real estate.

Question: How do you make a million dollars in Oregon real estate

Answer: Start with two million

Wolf might appreciate this. My daughter told me a story about a couple who recently bought a house in Berkeley. The price was $850,000 for a 1300 sq foot house with 2 bedrooms. This couple have a 3 year old and a 9 month old. The plan is for the 3 year old to sleep in the 2nd bedroom and the 9 month old to sleep in a closet!

My daughter and her boyfriend make ~ 120,000 annually. This will jump to about 220,000 when he gets his PhD.They currently live in El Cerrito. Because of housing prices and too many people in the Bay Area, they will move out if Ca .

I recently sold my house in NJ. Although it was not an easy sale , I sold it relatively quickly for about %98 of my asking price.

During the last year, I paid $24,400 in property taxes. When I bought the house in 1983, I paid $3,400 in property taxes

Currently I rent a 2 bedroom apt in Pleasant Hill Ca for 2,700 month. This may seem high to many non Ca and non NYC readers , but I can assure that it is not. One thing that surprised me was my monthly water bill, which ran $ 90 last month. I might eventually buy a house in the Bay Area, but the housing market would have to decline considerably before I would consider it.

Ca would be a great place except for the traffic( plans are being made for some freeways to expand to 8 lanes each way), high prices ( the cheapest regular gas is 3.26 )the regulations and too many people.

In 1976 my rent in Pleasant Hill was $165.

In 1976 dollars, that was a lot of money.

$100 in 1976 →$442.89 in 2018

source:

https://westegg.com/inflation/

PS: Anyone else noticed how Google first results then to be spam and unsafe sites nowadays?

The 800 pound gorilla for the counties north of Sonoma is the legalization of marijuana and the concurrent drop in prices.

Lots of people paid top dollar for rural properties only to see prices for outdoor weed fall below $500 per pound, less than the cost of production

In concord Ca they will deliver grass to your door

The SF area has the highest ratio of median housing prices/ median household incomes of any place in the country

There are only 4 ways for to afford a house on the Bay Area

1. Have an income considerably higher than the median-this would include any bonuses

2 Be a current homeowner

3.Get the money from the bank of Mommy and Daddy

4 Pay all cash

4.

Good list – a few tweaks:

3a. Get the money from the bank of Mommy and Daddy but refuse to admit that to others, and just tell people they need to sacrifice like you did for a down payment.

4. This is the wild card; the China all-cash spigot will either hold the RE market up as rates go higher, or will exacerbate a decline if the rug gets pulled out and they need to sell. Right now, while new buyers are slowing, you have a ton of absentee owners/landlords around here. If the Chinese markets keep sucking wind, and they are overlevered, maybe we see an exodus like the Japan money of the early 90s.

5. Get a cushy Prop 13 hand down from Mom and Dad so you can pay 70’s era taxes for an asset that has appreciated 15x over….and then complain about how the school system is underfunded.

I was reading a Redfin aricle a couple of weeks ago that showed asking prices accross the country were rising as actual accepted offer prices are declining. Add increasing volumes of homes for sale and it’s looking like a peak may be here. I just sold some vacant lots and I’m really glad to have finally sold all the rental homes I’d bought over the last 5 years.

I think your also seeing the bulk foreclosure purchase buys for pennies by hedge, foreign PE and PE, banks dressed as PE etc. fall out of the 5 year hold window via the fed engineering

https://www.cnbc.com/id/45925851

Tom Stone is great guy..is Adorno around?

Yes, Adorno is still around, we’re in touch.

I hang my license at C21 in Santa Rosa, you can reach me through them or through the CA DRE.

We are about to enter the Mid-Cycle Recession. This is not the crash, but *a* deep recession. After it’s over, expect housing prices to soar – the final hurrah.

If hottest markets like Seattle can be dropping like this then not sure what can happen to other cities?

It’d get interesting for sure

Will Powell do a Trumpster Twist and Print Print Print???