Forget the hype about a shortage of supply.

In its report today on existing-home sales in September – they fell by 4.1% from a year ago to the lowest level since November 2015 — the National Association of Realtors blamed inevitably the “decade’s high mortgage rates.” This is no surprise. The Fed has been hiking its policy rates, and mortgage rates have been rising for a while and now average over 5% for a 30-year fixed-rate conforming mortgage. While this may seem high by 2016 standards, it remains low compared to rates in the pre-Financial-Crisis era.

And yes, after years of rampant home price inflation, touted by everyone in the media, at the Fed, and elsewhere as the greatest thing since sliced bread, the NAR finds that “affordable home listings remain low, continuing to spur underperforming sales activity across the country.”

Indeed, when home prices rise faster than wages year after year – in September too, the median home price rose 4.2% year-over-year to $258,100 – sooner or later, the choice of homes that are “affordable” to those worker bees having to make mortgage payments from their wages gets pretty thin.

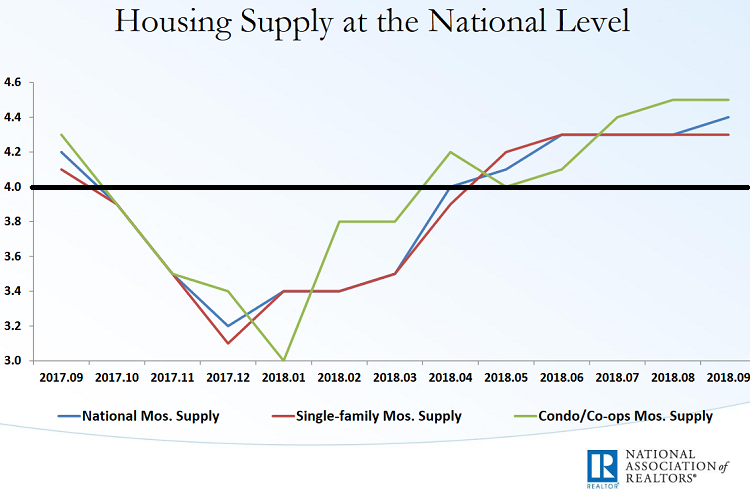

Inventory of existing homes for sale edged up 1.1% year-over-year to 1.88 million homes. Unsold inventory rose to 4.4 months’ supply. And this is where it gets interesting – because it breached a new line.

Housing market players are relying more and more on technology to make the purchase of a home and the approval or a mortgage much faster and more efficient. What might have taken months can now be done in days.

These technologies include online listings that are instantly viewable by everyone (rather than printed listings that took a long time to get to the potential home buyer), online research tools, drone-generated video of the home, automated income verification tools for lenders, automated credit approvals, and the like. These technologies are impacting every part of the market. And there have been big consequences.

“Technology has permanently taken two months off the time required to sell a home,” Rick Palacios Jr., Director of Research at John Burns Real Estate Consulting, wrote last year. And in a recent blog post, Palacios wrote:

Technology has shattered the balanced market months of supply conventional wisdom, shaving roughly two months off the time required to sell a home. Homes can enter escrow today within 24 hours of listing, compared to prior periods when it took at least 30 days for the first open house.

Because the time of the entire process, including the transaction itself, has been shortened by so much, the time from the moment that a home is put on the market to the moment the transaction is complete has shrunk, and these homes disappear from the market much faster. Hence, according to Palacios, “roughly 4 months of supply is the new buyer/seller equilibrium.”

Under this scenario, the unsold inventory of 4.4 months’ supply in September is now a buyers’ market.

The NAR’s chart below shows months’ supply for all types of homes (blue line), single-family houses (red line), and condos/co-ops (green line). I drew a horizontal black line at the level of four months’ supply. Everything above the black line is a buyer’s market (click on chart to enlarge):

Rick Palacios explains:

If we’re right, nationally we’ve already entered the early stages of a buyer’s market. Should supply levels cross above five months we’ll be watching for flat, possibly declining resale prices in some markets, especially where affordability is already very stretched.

So the beginnings of the buyer’s market, arrived gingerly at around April or May this year, based on national numbers. Real estate is local, and local results may vary, as they say, with some cities wallowing deeply in a buyer’s market and other cities still enjoying the endlessly sunny days of a seller’s market.

But whatever there is, there is no shortage of supply, though there is, after years of rampant home-price inflation, a shortage of affordable supply. But that mismatch can be fixed by a drawn-out housing downturn.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

At least in the condo market in San Diego, it looks like people are struggling to sell at expected prices.

It will be interesting to see if they pull the listing all together if they don’t sell soon.

You can tell a lot of homes are coming up for sale after being bought just 2 years prior. A sure sign some people were trying to cash in on rapid appreciation and the tax free gains after 2 years.

Generally this is the kind of gamble I like to see punished because this is unhealthy speculative behavior…

This is hilarious: I just clicked on the “Housing Bubble 2” tab in the menu above (it has all my articles on housing in the US), and when the page rendered it showed three ads for brand-new luxury apartment and condo projects in San Francisco, where I live, a city now drowning in overpriced luxury apartments and condos. Sign of desperation?

So I took this screenshot for your mild amusement (click on it to enlarge):

Yeah, I get a luxury living San Diego add on the left advert…

Algorithms are not without a sense of irony.

This is like the time I clicked on a news story about a terrorist bombing in Beirut, and got ads for Beirut hotels.

Looked online for small pressure cookers; for cooking artichokes.

Got ads for full figured bras for the next three months.

Thanks for the thought on artichokes. Great use for my pressure cooker that I hadn’t thought of!

Wolfstreet serves the most amazing ads, Wolf. When you were writing about the crisis/bankruptcy in shipping a year back or so, I even got an ad listing an ongoing auction for a ship being sold after the previous owner had gone bust.

Five minutes ago a lady from KellerWilliams rang my doorbell. Boise still supposedly has just 23 days’ supply. She wanted to know if I wanted to “cash in on the changing market before it becomes a buyer’s market”.

That’s a sign that it is one already.

Tell her you are about to sell, but Redfin only charges 1% commission as a seller’s agent.

I am betting the Boise area market is going to get hit hard by this next housing correction. Boise has a large number of construction related jobs which will go away with the correction, pushing many of the people working in those jobs into foreclosure on their own homes. I have watched the high end market in the Treasure Valley experience huge price gains in the past three years. I look for a major correction in that segment.

Prices are still sky high here in Seattle. You either cough up a kings ransom for a house or live in a van, man.

I don’t see any hint of a correction, unless rocketing higher at a slower pace counts as a correction.

forgot to add:

a lot of the saas/sw/related purchases made by most companies is currently decided by the IT departments. They overspend and buy things they don’t end up needing or using, and a lot of these products are useless hype. Budgets for this type of spending are going to be cut and these decisions are going to start be made more and more by the finance departments. expect the balance of power to shift, your departments are going to be getting it all for much longer. it’s in your best interest to prepare for that now instead of later.

the anger is strong with this one

Yoda: Not alone is he.

Not pleasant will be the damage when their days come.

Drove to Seattle downtown today (20th) to pick up a friend to go to Olympia with me and saw just as many cranes and just as many holes in the ground and just as many signs proclaiming some new high-rise and all I could think of was Wolf Street which almost made me feel sorry for those who wrecked a nice city. Almost..

You could buy yourself a fold/unfold house.

Youtube – These houses unfold in 10 minutes.

You could park it almost anywhere ??

RE would have to be cut by 2/3 for me to ever be able to afford a home in socal. My only option is to move. The only people I know who own a home inherited them or bought them 20+ years ago.

RE prices and incomes are so f’ing out of wack it’s not laughable it’s tragic.

You could buy in the county, and DIY the work, find someone with a contractors license you can “use”. My neighbor turned an abandoned home built in the 40s into a beautiful home with a metal roof, and he did almost all of it himself. He is “cheap”. You just have to leave the standard assumptiona about amenities, and be willing to live in a work in progress for a few years.

It’s a bit of a myth ‘using’ someone’s contractors license for DIY work. Why would a contractor sign off on work he/she won’t be doing? That is a sure-fire way to lose the license, but why would anyone shoot themselves in the foot with work they don’t do? Plus, people also believe that if they buy from a wholesaler, they get the contractor rate. No, they pay retail. They never even see the listed prices contractors pay, and even that rate varies as to how busy a contractor is and how much they purchase. Homeowners will be paying Home Depot prices at the wholesaler; it’s reality.

This just happened to my son, (people have stopped asking me). Son phoned me up and asked if I knew ___________ who lives across the river? The guy stopped by one evening and asked how to install a new electric furnace? He brought out his receipts and said “This is what I bought, but I’m not sure exactly how to safely install it”. So, my son was supposed to pull the permit with the BC Safety authority (lower rate being a contractor), tell they guy how to do the installation, sign off that the work was done to standards, and then be on the hook if someone gets electrocuted or the house burns down.

It varies to every locale, but homeowners can pull their own permits, do their own work, and pay the increased rates for homeowner inspections which have priced in call backs. I tell people it’s easy enough to do and to check out youtube videos.

As to your comment, I agree with everything else. Sweat equity is the way to get ahead for sure. With the internet there is absolutely no reason why people cannot learn how to do most work themselves. However, what can’t be learned except by experience are shortcuts, skills, and lurking pitfalls/mistakes. That is why a construction foreman is usually one of the ‘old guys’ on the crew.

I live rural and we do not need to pull building permits or have building inspections done. However, for electrical work and septic you have to be inspected and permitted. For insurance purposes I always take pictures of work and materials that will be hidden just to verify work was done to code or above. In fact, I just got done sending in a dozen jpegs to our insurance agent of a small rental I built.

regards

> I live rural and we do not need to pull building permits or have building inspections done.

Wow, where is that — approximately, even? Here in WA even the rural counties are permit driven (on both sides of the Cascades too).

> However, for electrical work and septic you have to be inspected and permitted.

That’s probably a good thing. Same here although mainly because electrical, well, and septic are the state level permits.

That part about 24hr escrows, at the top of the bubble buyers were asking for 90 days, in hopes they could flip the home before even owning it. No penalty for pulling out of escrow. That has to take out some spec, but how do you do due diligence? What about easements and liens, you should spend more time screening a new home than you would a new wife. No prenups in RE.

Diligence on a house, at least in California and other title insurance states, can be done in a week or less. Schedule your pest control inspector, roof, whatever other systems you want for the same day and get it all done – maybe pay a small premium for a quick turn-around on the written report. Get a preliminary title report within three days of opening escrow that spells out any title exceptions (easements, liens, etc.), and even get an environmental hazards report within minutes of ordering it online. If you discover issues that might take time to resolve, but most physical items can be quickly addressed with a credit in escrow. The big variable is how long it will take to get financing/appraisals, and if the down payment is large enough the appraisal mostly becomes a non-issue. A properly prepared buyer will have a loan lined up, subject to the specific property, so that can be done quickly too.

unsophisticated buyers are getting SCREWED. easement problems are not resolved by looking over the title unless you understand the implications. “a properly prepared buyer” is akin to caveat emperor. a 24 hr escrow is hardly time to find out what the CITY thinks about that too small easement. sometimes they grandfather, and sometimes they don’t.

title companies are a joke, and they should have ripped them apart after 2008. the best advice on RE is know your property, know your planning commission. or suffer buyers remorse….

> No penalty for pulling out of escrow.

Who would sell to a buyer offering zero dollars earnest money?

\\\

Now this is a storm: the stock market will deflate due to reverse QE and rising yields, on top of which the real estate market will “adjust”. There really is no place to hide any more…

\\\

Such a teaser headline. Houses are still selling for well over ask here in Silly-con Valley.

P.S. The ad I see on my page is for a reverse mortgage from Lending Tree. The company wants me to see how I can enjoy a stress-free retirement.

A “Buyer’s Market” means negotiating power shifts to the buyer. If you read the article, you’ll see that prices flatten and may eventually decline as you get deeper into the buyer’s market.

A buyer’s market is NOT a crash. It means the dynamics have changed. But if there is a market decline, there has to be a buyer’s market first.

Place across the street asking $1.4 million. Okay that sounds mad but is a one and a half flat with an empty permitted studio downstairs.

Had two weekends of showings back to back. Then another set back to back a month later. That was a month ago. Now ‘reviewing offers as they come in’

Okay anecdotal isn’t ‘data’ but with the amount of inventory in SF it’s anecdotal all the way down.

The dynamics have certainly changed alright. Denton County TX is one of the top inbound migration destinations in the U.S, but you will still have a challenge finding affordable starter homes. Doesn’t help when you have new home builders selling their affordable inventory directly to Wall Street landlords…

https://aaronlayman.com/2018/10/lgi-homes-beaver-creek-in-denton-tx-a-haven-for-wall-street-landlord/

I see rent control in their future. The peasants are fed up.

Really? SV is a big place. Prices dropping in San Jose, for starters

Just because someone wanted to sell a property for way too much, + a kidney does not mean the prices are falling in real value.

Dropping the price 25K from a 900-1.2M property is no big deal.

Seems like some people think that they are going to get that 900K house for 380K… after the crash. Yeah it’s silly. just like buying lotto tix.

I’m seeing drops in $100k steps.

It’s absolutely going to happen again. I purchased 121 acre farm/orchard for slightly above 1/3 of it’s original asking price before it was forclosed on it late 2010.

I also purchased a nice two owner, Victorian rental property for 55 percent of what is was refinanced for when the owner bailed out.

And the house next to that one sold for 25k, roughly the same time. They could get 110-125 righ now, going by recent valuations.

Wolf Richter is giving an assessment on what he hopes will happen — I think it will turn out much worse.

It may take a little time – but get your cash ready.

The last bubble, the steps were $50k, so yeah, $100k steps are about right for this time around.

This was/is for steps up and down alike.

I see “PRICE REDUCED” signs all the time in central San Jose.

And you can find houses in Silicon Valley that are selling at or under ask. It depends on the location and market.

I live in the middle of desireable area of SF and unit below is sold for $40K below asking. I have been keeping an eye on the market and it seems like almost every property in SF has a price drop recently. There are a lot of nice places on the market between $1.2 – $1.5 million.

Well I like that one better than my “Easy Climber Ad” for getting upstairs. Fortunately I can still climb the stairs………….

“The company wants me to see how I can enjoy a stress-free retirement.”

Disbelief,

The Mega Millions lottery is at …wait for it…1.6 Billion dollars. Even the cash out of $900,000,000 would provide for an adequate retirement, if you are careful.

Please do not tell me this is a sucker-bet…the odds are 600 million for one….they are paying way above even odds…almost 3X. Consider that the odds that most of us on this site becoming billionaires otherwise is…zero.

This is insane.

What if there are two winners? That “cash out” would be cut in half, below the “even odds” or better.

What if there are three?

HowNow,

How to express that mathematically? I would expect that the chances of multiple winners would hinge on the initial odds? If so, it would portend 2+ potential winners.

Considering this, one can never be presented with anything other than even odds as a probability.

Overpriced houses are not a good investment any more. Prices are falling. Even if you could get a 2% annual inflation return on the home price, the real estate tax will take that away. It’s a money losing proposition at this point in the cycle. People are much better off renting.

Overpriced cities are also not a good financial decision. They are good places to visit from time to time. Why buy the cow when you can get the milk for free?

I don’t see a buyer’s market because I don’t see any over supply sign in the housing market. There is no doubt that higher interest rates would hurt and sellers, investors and builder but it also hurts the buyers. Demand is strong but affordability is an issue. It will be interesting to see a condo boom in all metropolitan areas… LOL

It just doesn’t make sense to buy in Silicon Valley. In our neighborhood, which has shitty schools mostly free preschools because most are low income. Yet, the current house we rent would sell for 1.35 million, down from 1.6 million a few months ago. We pay $2950 less than half of the cost of mortgage plus property taxes.

The owner does not cover the mortgage. He bought the house 15 years ago for $600000 and pays $8k in property tax yearly, $3k/ month mortgage and maintance. Can anyone explain this insanity to me?

The owner could have refi’d it and/or might have an arm with an incredibly low rate. Maybe he’s breaking even on a cash basis but is able to take losses due to depreciation and has principal paydown. Real estate is a long term bet and your landlord has funded his retirement with the appreciation from that house. Sounds like he’s done pretty well.

When you think it is insane from the money perspective, you need search the answer in deep human emotions. Trust me, human emotions could be manipulated to do damage to him/herself. Think about fear, love, desire for certainty, look better than others, being accepted by others……

We have not sold a house over asking since April this year. Every listing since has gone below original asking after a price reduction or two or taken off the market after 4-6 months as the sellers think the market will be better in the spring. Yeah right! This is in Danville/San Ramon area of SF Bay Area a very strong high end market. Our latest is a newer tract home built in 2014. We have comps of the same exact home/floorplan selling for $1,250,000 and $1,288,000 in August 2018. 2 months later we are priced at $1,150,000 after a $100,000 price reduction. 5 weeks on the market yesterday. Buyer after Buyer we talk to at the open houses say “Bubble” “still overpriced” “rates are 5%”. An agent said “this isn’t August anymore that was two months ago the market is different”

If you don’t think this thing is going to crash 20% at least I got a bridge to sell you. Don’t ever underestimate the herd mentality once the headlines change the herd will be running the other way.

Oh and week one of the open house only one buyer asked “when are offers due”? We probably had 50 people though that weekend.

In March/April we would have 500 people through an open house and every last one of them would ask when offers were due.

We don’t even have offer dates anymore as the odds of not having an offer by the offer date is almost 100%.

50 to 500 . I guess that is a 90 % reduction in interest.

And many of the recent buyers will become long term (unwilling) landlords when a recession hits, jobs are lost, and they have to pack up and move but can’t afford to sell. The more unfortunate owners who bought at bubble prices will default during the next recession. Recession and unemployment is the wild card in all of this.

And what is that buyer getting in Danville/San Ramone for their $1.25 million? A 50-year-old-plus remodel/gut job for $500+ per square foot it appears. Nope, nothing insane about those prices. :)

This one is a 3/2 2300 sf single level built in 2011 by Toll Bros. Can’t even sell the new ones now!

I know of a 1.2 – 1.5 mil place in Fremont …. place was originally a single story built in the 1960s, upgraded from shit like aluminum wiring or suchlike things and a 2nd story installed in the 1970s, place has tons and tons of deferred maintenance haunting it. Uneven floors, periodic flooding, back lawn watering system drains to a pool of water under the house, termites are a thing, ground/foundation are settling …

One of the principal residents may not be able to make it up and down the stairs in another couple of years … where the bedrooms are. Then what do they do?

It’s a matter of simple age and poor maintenance, for the house and for the people living in it.

The people, and the house, are not special. I imagine this pattern repeated 1000s of times all over the place around here.

Sorry I meant our rent cannot even cover the owners mortgage, even though he bought 15 years ago. We just found this place, so it’s not like we’ve been living there forever.

It was on the market three months. The rental market has already slowed here. This ship going to sink like the titanic soon. So many have already moved away because of the inane cost of housing.

What? How do you even know what your LL pays for his mortgage? Do you have access to his social security to see his breakdown or financial status?

Besides he bought 15 years ago.

You’re talking non-sense.

Your right I have no idea. He could have bought in cash. My point is that is we tried to buy today at the same price he bought in 2001, we would still be in the hole collecting $2950 per month in rent.

Why he chooses to rent and not sell makes no sense to me. 30xs our annual rent is 1.06 million and he could sell for 1.35 million. This market makes no sense to me.

I don’t think that JK is “talking nonsense”. (By the way, Ehawk, that’s not exactly a nice way to communicate your point.) Even if the landlord bought the house for cash, there’s still the issue of opportunity cost. Assume the landlord nets $945,000 after paying capital gains tax, realtor fees, and other fees, can he/she get a better return than what he’s getting in rent? A 3% return on 945K is $23,350/year (or $$2,362/month). That’s less than what he’s getting in rent, but when you factor in property taxes and maintenance expenses, perhaps it’s a little better.

There are also considerations that the landlord may be mulling over:

1. He/she doesn’t understand stock market investing very well and prefers investing in real assets. The person may not know what to do with the money.

2. Some people just can’t stomach paying capital gains tax. And if he’s been renting the house for a number of years, he has to pay capital gains on past depreciation (which, I guess, is considered like income because it’s a benefit.) This rate is 25% which is higher than the regular capital gains tax rate.

By the way, I recently looked at selling my rental and ran through these numbers with my accountant so I feel like my estimations are within the ballpark. I was looking at cutting about 30% from the final sales price.

3. If the landlord has children, he/she may decide to hold onto the house until his/her death, thus avoiding all of the capital gains tax mentioned in #2. (This is because the property gets “stepped up” to current market price, so in effect, the property has no gain from original purchase date to date of death.)

4. In the Bay Area, many cities have strong eviction laws such that you can’t just require that the tenants leave in order to sell the house. Selling the house with renters in it can considerably bring down the sales price.

5. Selling a house is quite an undertaking. Some people just don’t have the bandwidth and would rather let things coast.

I agree, though, that the rental income does not represent some outstanding return on his investment. There are online calculators that help with determining whether to sell or keep renting, and I suspect that in this case, the advice would be to sell. But there are qualitative reasons for why people continue to remain as landlords.

I forgot to mention an important point. If the landlord has not resided in the home for 2 of the last 5 years, he/she no longer gets the benefit of excluding $500,000 of profit from tax. (For married couples it’s 500K; singles only get to exclude 250K.) So for example, on the sale of this home, this could amount to paying an additional 100K in capital gains tax. Given the current laws, landlords can feel locked into holding onto property.

Being a SF resident, I don’t think SV will be affected as much as some other places that went nuts with the low interest rates.

SV has so so many tech workers making $200k-300k that even a decline in prices has a very high floor. (barring a recession).

But I wouldn’t say the same about expansive cities in Socal, Seattle area, NYC area where availability is much higher and number of people with “wealth effect” are reducing by the day.

What is really sad in today’s world is that for some to win, others have to lose badly. Sure there were some speculators who bought in at low interest rates. But that’s what they were told to do and life circumstances make people buy them despite out of whack prices. If the market is kept propped up for those folks, newcomers struggle. For newcomers to be able to afford, these old speculating folks will necessarily have to suffer a drop in housing values.

For one to win, the other necessarily has to suffer. The politicians and central bankers get to decide who to throw under the bus. What a sad state of affairs!

I wonder if a different economic model is necessary!

Key is whether or not those 200-300k engineers keep their jobs and wealth. Job cuts in tech do happen. Businesses can also move out of SV. And if tech stocks suffer losses, so will stock holdings and stock options. SV is not immune to economic factors, in fact it may be more vulnerable.

Where I work, there are about 20 people with a household income around $300k in base salary (no stocks, bonuses)

They didn’t buy houses because:

1. Too expensive in the last few years

2. Unsure about living in this area

3. Immigrants unsure about living in the US

Barring impending mass layoffs, most of them would easily buy a reasonably priced house (say $700k-$800k: 3x their base income)

As prices are dropping, there are more and more people who can afford those homes. I don’t see that changing. SV is especially rich and that gives a lot of cushion (until a tech recession).

Sure, but can these people sustain 300k for 30 years. We live in Silicon Valley. Most are H1bs with salaries that are not that high around 120k. Together they’re making 250k, but houses are 1.3-1.7 million, not affordable to them. I don’t even see any other Americans most days. Most of the houses were being bought by Chinese investors, but I haven’t see one in months at the open houses.

We make 350k on a single income (total comp), but my husband’s employer already told senior management that bonuses and raises will be capped or declining in fiscal 2019 because the company is projecting a recession.

My husband’s company is a large supplier of parts (not going to share exact details), so the orders are sharply down. This is going to be fun. No way it’s even removing sustainable. 800k would be a 50% fall in our shitty neighborhood.

James, yes, there is a better economic model for housing. Ban mortgages. People need to use savings to buy houses. The current debt fueled purchases will only do one thing, which is wealth transfer as opposed to wealth creation. I can borrow 1 million to force you out of the place you want to live until you borrow 2 million to make me worth while to sell the house to you. I did NOT create 1 million wealth, I transferred it from you and you are thinking you can transfer 1 million from next guy.

I am totally supportive of capital markets to form capital and do “productions”. But these debt fueled consumptions need to stop. Ban mortgages, ban Fanny and Freddy. House should be lived in by the worthy ones who produced and saved more, but not by the ones who are good at Casino stuff.

Problem with that is YOU would never be able to buy a house. Wealthy people with large inheritance and generational family money would own most everything.

If you think by borrowing to cosume can “empower” you to be rich and enables you to compete with the rich, I think you misjudged the reason why the rich have generational wealth while the non-rich are NOT.

Even if what you think is going to happen actually happened, the mass will suddenly know who is their true enemy. Not the neighbor that is willing to borrow more to compete you out, but the 0.00001% if they DARE to own everything and rent squeeze everybody to death.

Right now, the common debt slaves are borrowing to kill each other while the rich are watching and collecting mortgages interest and fees.

@JZ I’m not sure what you are talking about. All anyone can do is make the best decisions available at any given time. I’m not sure what your definition of rich is but please tell me how you believe the rich became/become rich? Or do you think they are just chosen or it’s just luck?

I completely agree. The federal government shouldn’t be in the business of guaranteeing mortgages. Banks might actually have to lend to businesses rather than bidding up prices on existing assets (rent seeking). Without a gov’t guarantee, there is no way a 30 year fixed rate loan would exist in a free market.

@THE MAN, my thinking is there are two kinds of rich. The Henry ford, the Bill Gates, The Steve Jobs, when they get rich, they bring everybody rich with them. These are the wealth creators. If you want to compete with them in terms of buying houses by borrowing money, I don’t think you will have a shot. The 2nd kind of rich is the land lords, bankers, the insurance companies, education charging tuitions. These are the rent/interest/tuition squeezers that are the wealth transfer kind of rich. They thrive under Federal Reserve, the ZIRP, the QE, they make everybody else into debt slaves and thwart their social mobility/progress. If you want to compete with this kind of rich by taking on debt and do wealth transfer, you better be one of them and do a better job, but the better you do, the worst the society gets.

I agree with you everybody has to play the games under the given game rule. I am NOT suggesting otherwise. Jame’s post asked the question whether there is a better “game” that is set up benefiting most of people as opposed to the current housing situation where the debtors is at odd with the savers and they vote for government for their own conflicting benefit. This is part of the divide and James was asking whether there is a better game set up. I have my two cents on how the game can be set up better by banning debt fueld consumptions, and you brought up the idea that consumers will never be able to compete the rich without taking on debt. I disagrees with that.

@JZ you said “The Henry ford, the Bill Gates, The Steve Jobs, when they get rich, they bring everybody rich with them. These are the wealth creators. “…This is just celebrity worship.

Being a landlord is business and a job just like anything else. It provides housing for society. Many landlords lose their shirts if they take on too much debt and/or too much risk. .The same thing is true for banking. It is a service and society is better as a result. Clearly you have little or no knowledge of this business…

@THE MAN, the rent seeking rich always describe themselves as if they are the wealth creation kind. The Bill Gates, the Henry Ford build companies and lift up all the W2s of working people, and the 2nd kind always tries to squeeze maximum amount of portion out of the W2s of working people under the name of “providing services” like the mob providing “protection” services. In reality, people need places to live and people get sick. These parasites just take the positions of the land and insurance and raise rent/premiums until the W2 earners can NOT get by and then the bankers come in and provide another service to convert them into debt slaves and let them pay interest. I am fine with all of these since the capitalism is a dog eat dog world and let’s all compete and exploit each other to advance human civilization. But when bank fails W2 folks have to bail them out? When Fanny and Freddy is close to banrupt and W2 folks have to pay more TAX or suffer wealth transfer through money printing under the name of “saving” the economy? And they are still telling me they are “service” companies that “serve me”? Sorry, I do NOT need this kind of service. “It would take 25 years for the people to forget about 2008”— Jamie Dimon recently said. ANd I know what he wanted to say but he did NOT say it, “it would be f—-king 25 years before we can do it again, damn it!” Service company.

One word, pronounced like Milo: China!

Watch their housing crisis unfold.

The California Governor’s salary is about 190k. Amazing that so many tech workers are paid far above the Governor’s level. Just seems out-of-balance to me.

Obviously a very worthy man, doing great things that people value highly.

Concerning appraisals, once the market truly shifts downward Appraisers will get more conservative and if you don’t have the big down-payment, Sellers will find the going tougher.

I see prices starting to fall here in South Orange County CA.

> once the market truly shifts downward Appraisers will get more conservative

I can haz death spiral?

In the suburbs of Seattle, it is already happening.

Since de facto federal licensing of appraisers, the whole thing has become a gravy train. When the boys from Washington come and yell at the appraisers to tighten up, they tighten up.

Getting a refinance this July was a nightmare. Appraisals are definitely getting tighter.

South Orange county is one of the best and safest places to buy/own real estate. Great clientele, very little space left to build, an hard to get a zoning and permit to build. It will always also be a desired place to live, tucked away between the ocean, mountains, and camp Pendleton.

I’m really surprised that South OC cities aren’t priced higher as compared to Northern OC.

The traffic has gotten horrible. What used to be one of huge benefits of the area has turned into a weakness.

San Diego is same

Great place awesome weather.. we are truly different and real estate can never go down in prices

Just forget the last few crashes here

The sky is falling, the sky is falling! Who cares? If you’ve positioned yourself right, you stand to gain from the apparent impending downturn in RE (cyclical, is it not?). This is an opportunity, not a calamity and a time to increase your wealth by picking up properties as they bottom out, yet again. Let the carnage begin.

Agreed! This time is NOT different and opportunities are always available. In down markets there is lots of opportunity. When things are hot, less so. RE goes up and down in cycles. It’s not a fast moving market so there is time to see what’s happening and make bets accordingly.

You’re speaking from your position, and not the position of the average schlub. Certainly not from the position of the “General Welfare.”*

Yes, any situation has winners and losers. If there are a lot of losers and a few big winners, it’s usually not good for the society-at-large. Neoliberals love to celebrate big winners, papering over the condition of the numerous losers. Thanks for commenting from the Neoliberal pov.

* You may recognize this phrase. It’s one of the six objectives listed in the preamble to the United States Constitution.

I got a flyer from the second subdivision offering 5% to any agent who brings a buyer in…These ae $700K plus homes in both cases.

Rohnert Park and Santa Rosa.

I also spoke to a woman whose condo in Sebastopol has been on the market for 70 days without an offer, she just dropped the price again and would take less than asking.

It’s now priced at $35 K less than a similar unit that closed in mid August.

There is no shortage of “Fresh” prices,”New” prices, “Improved” prices and even Reduced prices.

If a property is in “Turn Key” condition and priced right it still sells in days.

Otherwise it sits.

30 year mortgage rates have risen to over 5%, but home prices haven’t dropped yet to any significant degree. Affordability is rock bottom. It won’t take long for prices to plummet from here.

I don’t think home prices are as sticky as many people think. Flippers, investors, builders, and others have to make transactions happen to make payroll. To make a transaction happen in this environment, they have to reduce the prices to keep things moving. Plus, we know here are gazillions of apartments and condos coming on line in the next few years.

Prices will fall but it’s very unlikely they will ‘plummet’. The demographics are good and a lot of the inventory that is coming on line makes up for years of very little development after 2008.

If prices rise 50% in 3-4 years, can you explain why they can’t fall just as fast, or faster?

OK, if the price rises 50%, so from $100 to $150, it would only take a 33% decline to bring it back to $100.

A 50% decline off $150 would bring the price to $75.

But I understand what you’re getting at, and the answer is yes, it could, but it might not, because the whole system is set up to support and inflate prices, so the down-trend could be slower, but if there is a real crash (credit freezes up), it could be faster…

:-]

Prices could fall by that much and they did after 2008 in some areas. Subsequentry the Fed, govt, banks, (society as a whole) decided to intervene and collectively decided to prop up the system and wait it out. So you are correct that prices can fall just as fast or faster. And usually price declines are much faster than increases. However, will prices stay at those depths? Not for long. We now know the Fed’s playbook pretty well. Place your bets accordingly. See my other comments for additional detail.

There is a term in economics called “Sticky Downside”, which describes the psychology of price movement.

The bottom line is that, when Real Estate come under pressure, a lot of property owners decide to hunker down and wait for prices to rebound. Usually this works. Sometimes it does not (2008-2011).

When confronted with lower prices and the belief that the long-term trend is upwards, rational people will refuse to sell. That is why, during a Real Estate downturn, the sales prices might drop 10% per year, but the number of sales might drop 50%-80%.

This is one of the reasons why many economists think that a small amount of inflation (2%-4%) is good for the economy: A small amounts of inflation means that people who are waiting for the price to get back to what they owe on the house don’t have to wait so long. (According to the theory,) this makes the recession shorter.

House prices will very likely adjust downward as they always do during a down period of the economy. Nothing new about that. But will prices be higher in 10 to 15 or 20 years? Sure they will. Everyone needs a place to live and the stability of owning a home is very attractive for most people. But some people prefer the flexibility to rent and that’s great too.

Just remember, no one gets younger and time marches relentlessly forward. If you want go buy a house and it makes sense for you and your family then great. Just plan to stay there for 7 years and you will very likely do well. If you pay attention to the economy then buy when the market is down thats even better. But don’t get stuck in analysis paralysis. Thats a waste of time and time is the most valuable asset, not money.

Depends entirely on whether people’s earnings outpace their basic cost of living and consequently whether they have more money to put into a mortgage – if that’s the case, then prices will be higher. If not – they won’t.

Saying ‘sure they will’ just because that’s what’s always happened during your [brief] lifetime, is daft. The USA’s post-war prosperity is now a past time, and its well-remunerated middle-class jobs based on artisan skills have been replaced mostly by no-skills, no-benefits, low-pay service jobs, due to its polity taking the easy option of debt rather than production.

Given that, it’s strange to be so cock-sure that prices will always be higher.

Wolf knows a bit about Japan; he can tell you about the housing market there for the last 30 years.

In bubbly places like central BC or Calgary, Re prices have barely recovered to where they were in 2006 peak. Great for buyers who bought post crash…. Not so good for many who were banking on that equity. After this next crash, there will be much opportunity for those with cash on hand.

All anyone can do is make the best decision with the available information. The post ww2 usa may be over, and China might be the next sole superpower, and rates might shoot to 20%, and and and…. you can play this game forever. But the Fed has shown it’s hand. It will not let the economy fail. The federal, state, and local governments also need prices to rise. Sure, anything can happen. But as I said, in 10 or 20 years it’s a very good bet that prices will be higher.

In the short term I would wait on the sidelines and until rates get where they are going. Longer term (my lifetime and into the foreseeable future) real estate is a good bet. And as you said, 70+ years of data back up my argument.

Although I think the Fed will eventually be induced to change monetary policy once a recession gets started, I think you’re overplaying the power they will have to cushion the blow. Who is to say monetary policy alone will be sufficient this time, and a fiscal policy response (increased government spending) will be likely face substantial resistance in Congress. Even if these policy responses work, they are likely to take some time to take effect and there could be a major dip in asset prices while the Fed and Congress put a plan together.

Another thing to thing about is US real estate, on average, increases in value only 1-2% over inflation since 1800. Some hot markets bubble up during the boom times, but in the US overall, it’s not a very productive place to park capital. When you count in the cost of holding the investment (prop taxes, depreciation, ongoing maintenance, utilities, unforeseeable one time costs) and the illiquidity/high cost of transacting in real estate it becomes even less attractive.

If I owned a home I would be selling now, and I’d be getting ready to cash in long term gains in stocks soon. Cash will soon be king again.

“But the Fed has shown it’s hand. It will not let the economy fail.” – There is a massive embedded assumption in this statement. One that will, most likely, turn out false,

New to Wolf Street – really enjoying the reports AND the comments.

A technical question: If days to close declines (due to technology shifts) should months of supply increase or decrease all other things being equal?

Decrease. Because the average home is on the market for a shorter period.

I no longer have a mortgage and I usually get asked if I am investing the equity in my home. I always say no. They ask me why and I tell them, because I tell them it is paying the rent.

After paying a mortgage and giving upfor years I will not put my home at risk for any investments because now it is one.

This might sound like it’s off topic but I don’t think it is.

If the fed is normalizing the banking sector by increasing rates. They are both kicking banks off their welfare stipend(interest on excess reserves) and limiting credit for everybody with higher rates. If left unchecked this will ultimately lead to a tighter market for lenders and borrowers. Leading to lower prices.

BTW, in my southern flyover country town, home sales are down 6% in September YOY. The story made the local paper which usually leads with a football headline.

Petunia,

That’s interesting. When that stuff starts showing up on the front pages of local papers, something is changing in the mindset (and a good part of market dynamics is psychological).

Here are some real estate local news from San Diego CA:

slowing housing market http://www.sandiegouniontribune.com/business/real-estate/sd-fi-case-shiller-20180925-story.html

record high median home price

http://www.sandiegouniontribune.com/business/real-estate/sd-fi-home-median-20180926-story.html

supposedly slowing rental market http://www.sandiegouniontribune.com/business/real-estate/sd-fi-alexan-trip-20180906-story.html

The economic door was already starting to swing shut. Wolf’s great reporting on various key aspects of the economy validated that and most of his readers who are pretty savy keeping “an eye” on economic conditions have concurred from their vantage point.

All I can conclude is that Fed Chair Powell is fighting the last war. If I’m right, he will succeed in not only closing the door, but slamming it shut.

The US economy cannot withstand higher interest rates. Too much debt.

Regarding housing, as prices drop you will have some step in buying by people that had waited. Countering this will be negative wealth effect on those that bought in at the top and are seeing their paper gains erode.

If the economy tanks hard as I suspect it will, job loss will be significant and this will put further pressure on housing as people that are financially stretched will be forced to sell. That’s when things will get dicey.

Everyone is expecting it to fail: Deteriorating infrastructure. Prohibitive health care prices, high debt and perpetual war.

It could swing either way. No one has a crystal ball. Lots of debt loathing kids coming online. Young to middle aged adults finally having kids getting forced out of their parent’s basements. Immigration providing cheap labor and growth.

US economy is driven largely by consumer spending. As long as consumers are spending money,, all is good.

I don’t see it slowing down.

Everything is expensive but people are still lining up for $1K ipHone..

I’d like to believe that the economy is going bad.. but the consumer spending is telling me other wise.

Stock market is not economy and stock market going down does not mean economy / real estate going down..

I used to live in LA, but have lived in an area for years now where an average house is about $100-$120/ft. Seeing this article about such concerns over people’s housing assets presents an interesting contrast to my world, where most of my assets are in CD, bonds and equities. First, I am glad to see rates to finally go up so I get a better return on fixed income. Most of my assets are very liquid with low fees, so I can easily rebalance as times change. I contrast this to housing that can become very illiquid, has relatively high transaction fees, and for most is a leveraged asset. (I couldn’t possibly imagine taking out a margin loan to buy equities, which would make me as nervous as some of what I am seeing in the comments here.) Add to this, I pay no taxes or upkeep fees on my assets, and because of corporate laws, I can’t be sued if my investments cause problems for other people.

“But whatever there is, there is no shortage of supply,”

In many areas in the metro Northeast there is virtually nothing for sale below 500k. And what’s above 500k is like 700, 800k homes that are quite posh (and not many of those).

So I think your statement can be proven false. When there exists only a few hundred homes for sale in an area of several million. I think you’re being overally dramatic on the reasons for the housing slump.

I think people are broke, and sales are plummeting for that reason. But an excess of housing supply is not the reason. If you have no money and are deep in debt, any amount is too much.

There is a very real shortage of supply!

I wrote:

“But whatever there is, there is no shortage of supply, though there is, after years of rampant home-price inflation, a shortage of affordable supply.”

Note the second part of the sentence that you conveniently and willfully chopped off. People chopping my sentences and quoting them in fragments to fit a false narrative pisses me off.

There are like a billion homes and condos for sale in SF. Problem is everyone with a shitty two bedroom condo now thinks they are going to realize 100% in five years and all those condos are minimum $1.2 million for anything we want to live in. We make plenty and could afford it but we are not suckers. Sellers are going to have a reckoning.

So… how much more prices are gonna drop? I would say to wait a few more months unless is urgent.

I think most people are wrong. We are entering a period of stagflation. We will be seeing rising rents with a slowing economy. That means real estate will be strong. Absolutely no, and I mean no deals on SoCal beach properties. If you think prices on SoCal beach prices are falling, you are delusional.

Do you own socal beach properties ?

During last downturn, people said the same thing… but we all know what happened.

No area is immune. Never say never

I do own 2 properties in SD.. not beach properties. Both properties are in used by family members

Right ON Wolf! There is a tremendous supply of homes here in North Texas, BUT they just aren’t affordable for the average worker. Most Americans are having trouble saving for the 20% down, when a home on average in Frisco, Plano, McKinney, Prosper, if you’re lucky starts at $300,000. The buyers here are people coming from states that received a large profit from their last house and are moving here, to get more bang for their buck. Thus Locals that have been here for 20 to 40 years (both young and old alike) and were hurt in the last recession are priced out of the current home market. We’re just saving and hoping for a another down turn to get back in a home.

In San Diego, I am seeing homes staying longer in the market and multiple price reductions for both condo and sfr.

There is no dearth of inventory here if you have money but the problem is affordable inventory.

Theres so much inventory here in the northeast I don’t think you could give away a house. Prices are falling at a pretty good clip too.