What many in 2016 thought would never happen again is now reality.

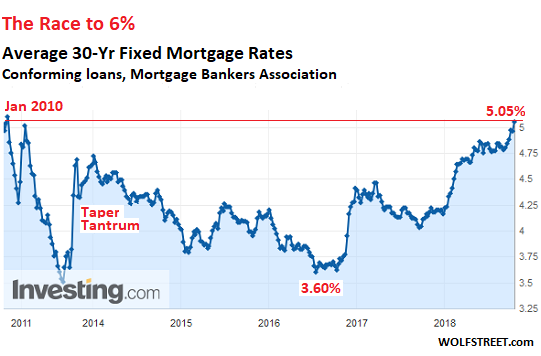

It finally happened – a line in the sand has been breached. The average interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) and a 20% down-payment did what people had thought in 2016 we’d never see again: It breached 5%.

It hit 5.05%, to be precise, for the week ending October 5, according to the Mortgage Bankers Association (MBA) this morning. This is the highest average rate since January 5, 2010 (chart via Investing.com):

This is likely not the pain-threshold for the housing market, though it is already putting pressure on it at the margin, with some potential buyers being scared off and other potential buyers finding the inflated home prices of today with the current mortgage rates outside their range of affordability. As interest rates have risen, some potential buyers have fallen by the wayside – though not a huge number just yet.

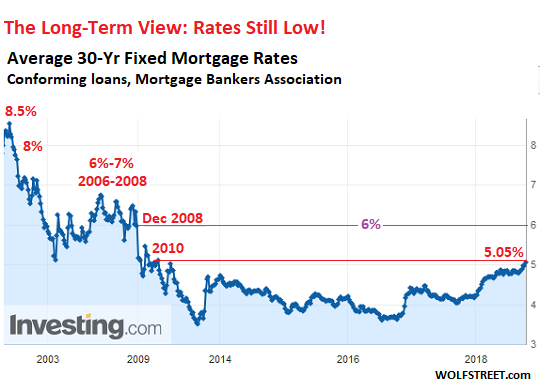

But 6% will likely be the pain threshold, in my estimates. It will block a considerable number of potential buyers from buying at current prices. Home prices would have to fall first.

If the maximum a household can afford is a mortgage payment of $1,720 a month, they can finance $320,000 over 30 years with a 5% fixed rate mortgage. But if the mortgage rate rises to 6%, they’re maxed out at $287,000. In other words, the price they can afford would drop by about 10% if the rate rises by 1 percentage point.

This principle goes for all budget-constrained buyers.

And 6% has moved into view. This is still historically low. It would take rates back to December 2008, when the Fed was kicking off its first round of QE to repress long-term rates and inflate asset prices. Beyond that are the now unimaginably high rates of 7% and 8%:

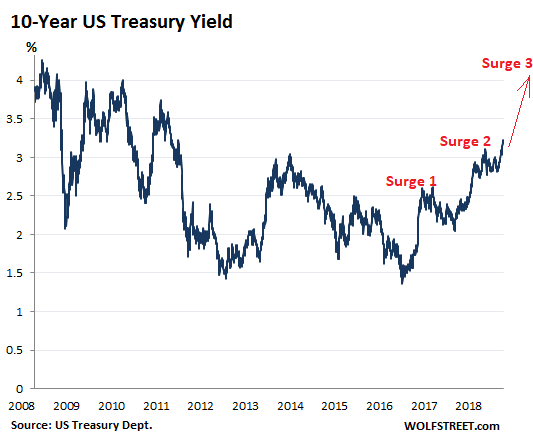

Mortgage rates move more or less in tandem with the 10-year Treasury yield, but are higher. The spread between the MBA’s average 30-year fixed mortgage rate and the 10-year yield runs around 1.5 to 2.0 percentage points over time. With today’s 10-year yield at 3.22%, the spread is 1.83 percentage points.

The 10-year yield has moved in two surges so far in this rate-hike cycle, each of them over 1 percentage point, with some back-tracking in between. It appears to have launched “Surge 3.” If it plays out, this surge would push the 10-year yield beyond 4%. And this would bring the 30-year fixed rate into the neighborhood of 6%.

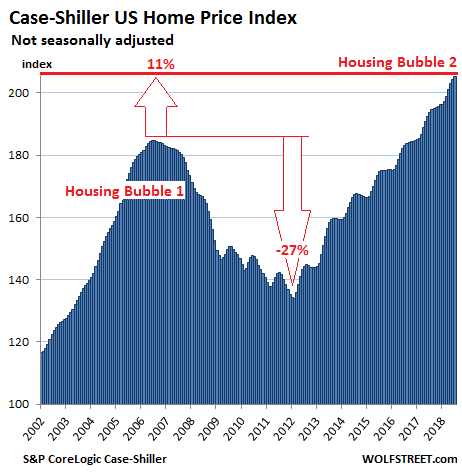

This new mortgage rate environment is meeting home prices across the US that have surged over the past years. Affordability issues, already tough to deal with at 4% and 4.5% and even tougher to deal with at 5%, are going to be much tougher at 6%.

But the Case-Shiller National Home Price Index averages out the booming housing markets with the lagging ones. Housing markets are local. And in many metros, home prices have surged far more than the national average. For example, according to my Most Splendid Housing Bubbles in America, these metros have seen the Case-Shiller index surge from the peak of Housing Bubble 1 in 2006/2007:

- Seattle, by 35%

- Denver, by 55%

- Dallas-Fort Worth, by 48%

- Portland, by 26%

- San Francisco Bay Area, by 41%

These price increases came on top of the crazy peaks of Housing Bubble 1. So a 6% average 30-year fixed mortgage rate in these inflated markets will likely change the equation a lot more than in some of the less inflated markets.

“101 new listings, 101 price reductions.” Read… Red Ink: Housing Inflects Further in Bay Area’s Sonoma County

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Housing Bubble 2.0 is doomed for the same reason Housing Bubble 1.0 was doomed: speculators binged on cheap credit supplied by the Fed’s ultra-easy monetary policies to drive up housing beyond all logical limits, and then suddenly the supply of Greater Fools dried up and the market tanked.

Common misconception. When rates were going up during Volcker era, real estate didn’t crash, but it kept going up.

From 60s-00s, interest rates were above 7%. Interest rates were actually rising during many bubbles, including the late 70s and late 80s housing bubbles.

So there are more important factors than just interest rates, like lax lending standards and, more importantly– population surges.

Population surges increase demand on housing, with many forced to live in overcrowded conditions to prop up high rental prices.

The last 2 decades experienced unprecedented population growth from “Open Borders” globalisation policies. Overcrowding housing always leads to higher prices. Many landlords pack 10 renters to a room and collect rent. Foreigners are used to these conditions– Americans are not.

That era did not come after a decade of ZIRP, NIRP and QE in a coordinated effort by all central banks. You have not idea what higher interest rates will do this time around. In my view higher rates mean people like me can’t bid up the price as we could have when financing was cheaper.

Population surge is a wash when you have a huge segment of the population retiring and dying off, and the millennial generation that follows them with far fewer children in tow and massive student debt is all that’s left to buy that housing inventory.

Population surge doesn’t mean much if the prices are still out of reach of that population.

But these rates will have no effect on housing prices in most of the Bay Area because so many houses are bought without mortgages

Wonder how much of this Chinese cash will dry up with this trade war heating up? Will those Chinese rolling their lucrative business profits into US real estate be more concerned now w/ tariffs and how that will affect their businesses? Interesting…

It has already dried up. China imposed capital controls to stop dollars fleeing the country. That means, less dollars propping up markets in Australia, Canada, California and Washington.

Holders of assets in these states and tax revenues in these states are in for a shock.

Disagree. Those supposed controls were put in place 12-24 mos ago and the money kept flowing.

I wonder if even more cash will flee China because the unpatriotic wealthy don’t believe China will come out of a trade war on top.

I think foreign money will only stop from the fear that US gov. will punitively tax or take their real estate.

Interesting opposite take.

That’s a remarkably naive understanding of how capital moves around. Most Chinese money isn’t fleeing China because they don’t believe in China. It’s fleeing for lack of investment vehicles in China. Some individuals have too much “extra” money that they want to put somewhere. Some rich Chinese have some visas to live in the US and want to make US their home. It completely makes sense when you look at it from the lens of the rich.

To put things in perspective, Trump has properties all around the world. Is that because of lack of faith in US?

The world is bigger than just the US, hot China money is flowing into other parts of Asia, middle east, Africa, and Europe. It’s a big world out there. China silk road is also spurring FDI.

James – $500k put into property in the US gets you instant citizenship. The US is not unique in this; other countries have plans similar to this, ranging from millions of dollars to tens of thousands.

If you thought your county was going to have a crackdown on certain kinds of crimes, financial; acts of treason, etc., wouldn’t you want a pied-a-terre somewhere else?

No, $500K does NOT give you “instant citizenship.” All it does is it allows you to apply for an EB-5 visa which may or may not lead to a Green Card. You must invest $1 million to finance a business (not buy a house) unless the investment falls into a rural area or a high unemployment area, which cuts the minimum to $500k. There are a lot of tricks being played, and usually $500k works.

But the only thing this investment does is it allow you to apply for an EB-5 visa. It’s a long and iffy process that can take years. Many Chinese investors have gotten ripped off. Google EB-5 visa fraud.

If you don’t get ripped off and if you get the EB-5 visa, you can apply for a green card, and after you get the green card, it takes at least 5 years to get US citizenship.

The number of all-cash deals has been dropping as prices have increased, and the all-cash deals are much more common for houses above $2 million.

Historically, the all-cash buyers in the Bay Area are typically either wealthy foreigners (often Chinese) or tech lottery winners. These folks are being hit too.

The situation in China is deteriorating (just look at a chart of the yuan) and this means you have far fewer Chinese willing and able to drop millions on US housing. Chinese investment in the US has dropped 92% this year.

As the market is finally starting to accep the reality of the rate-hike cycle and Fed balance sheet unwinding, tech stocks are leading the sell-off and the wealth that is being lost is significant. For example, in late July, FB hit a 52-week high above $218. It closed today at under $152. That’s already a 30% drop, but if key support levels don’t hold, look out below.

Bottom line: the Bay Area will not be immune from pain. In fact, it’s far more vulnerable than many people think.

How do you know Chinese investment in the US has dropped 92%? That seems very high.

https://money.cnn.com/2018/06/20/investing/chinese-investment-united-states-falls/index.html

I believe the 92% drop relates to Chinese M&A activity in the US, not RE money coming in.

That said, I agree with the premise that Chinese money flow into US RE is facing an uphill battle with Chinese currency devaluation, Chinese stock market declines, capital controls, and Chinese RE declines. They simply aren’t as rich as they were last year, and they have less money to throw around.

Only time would tell never say never

My gut feeling is .. bay area is not immune and it would be clear in next few years

Everyone think we are special and this time is different

Bay Area housing is already going down. Especially in the periphery. Check out most parts of San Jose, Milpitas, Fremont. Even Santa Clara and Sunnyvale are getting hit. Houses are sitting in the market weeks, in many cases for months. Often, price is reduced or even the list price is significantly less than what it would be just a short 6 months ago. Zillow has the robot picture for many if not most houses in the periphery to indicate that the house price is way different (lower) than their estimate.

What is funny is that in most neighborhoods, they show an expected 20-30% increase for the next year all the while prices are already dropping big time.

I’m seeing just what you describe in my Union City neighborhood.

I’m seeing “PRICE REDUCED” on signs in central San Jose.

Most all-cash purchases are investors chasing maximum returns. When the balloon is inflating, they buy. Once prices show a downward trend, they sell to do their profit-taking. This pops the bubble, and prices drop quickly as people try to sell without taking a loss.

The problem is housing prices are sticky – if you can’t sell without taking a big loss, you tend to hang on as long as you can. Bankruptcy filings are on the horizon…

Yeah, some people will hang on but inventory will increase in some way, shape or form, driving the prices lower until we reach equilibrium. I have been waiting to buy in SF and looking at the homes and condos and the appreciation in the past five years, you would have to be crazy to buy now. Interest rates will have a double whammy in the Bay Area, both for the actual cost to finance and the impact on high flying tech stocks that are used to finance residential real estate purchases.

If the price of lumber is any indication (below link) I’d say we’ve been in a housing correction since June 2018.

https://www.finviz.com/futures_charts.ashx?t=LB&p=d1

On a long-term chart, you see that the price of lumber, after a ridiculous spike, is now back to something like normal. There were other causes for the spike in lumber prices in 2017, including the hurricanes in the summer and trade issues:

Wolf,

Isn’t the price of lumber one of the more significant Canaries in the coal mine?

I don’t think so. There are too many other factors involved that muddy it up. However, when lumber gets to expensive, home builders are screaming and yelling, as they did last year and earlier this year.

Tom McClellan uses lumber in his forecasts. https://www.mcoscillator.com He is a bit eccentric, but worth following

Just some anecdotal intelligence. My company sells to Georgia Pacific across their business units. A recent meeting with a GP Reliability Engineer for their Building Products Division said for them, lumber is booming. They have several hundred $$MM slated for new equipment at brownfield sites as well as developing greenfield sites across the country but mainly in the Southeast.

Other anecdotal evidence. I am in the Charlotte market and have several friends building homes on lots and they have struggled to find lumber for these projects at any price.

I live in logging country that supplies a big portion of the US softwood market. The trucks are hauling….7 days per week. The booms are towed out, every few days. In this one region alone the forecast cut is several million cubic meters.

Mind you, having lived here all my life and had most of my work based on a healthy forestry industry, I have seen it shut down in a few weeks…sometimes for several years. One day everything is going gangbusters and then the industry just doesn’t start up again after Christmas shutdown. Hurricanes are good for the lumber market, though. It’s boom times on Vancouver Island for sure.

To complicated matters further, I just read about the softwood “glut” in the Southeast (this is timber not lumber). Quote:

“There are far more ready-to-cut trees than the region’s mills can saw or pulp. The surfeit has crushed timber prices in Mississippi, Alabama and several other states.”

https://www.wsj.com/articles/thousands-of-southerners-planted-trees-for-retirement-it-didnt-work-1539095250?ns=prod/accounts-wsj

My story, two houses (1976 and 1987) from two marriages and both lost in divorces. They were both purchased with 20% down, 15 year duration, and at 8% interest.

Before the new normal of FED operating out of fear, (Zero Interest, QE, and other Tweaks), the market set the operation and the cards fell as they must for proper functioning.

It will be interesting to watch action during the next contraction and how the fear in the FED (and the banking industry) plays out.

I think it will again chew more from the formerly great Middle Class, but this time aim for the Upper Level as the Lower End has already been beat up badly.

The money control is stricter in China.

The control of Hong Kong is even stricter by the Chinese communist government.

All money want to go out China and they don’t prefer Hong Kong anymore.

They will try very hard to land in other countries futher away.

US is China’s enemy and is the best place.

Estate asset in SF, NY is a good starting.

thank you. it’s good to hear it from an asian perspective.

I think that this is what we call “Not Economically Motivated”.

I had a Chinese guy ask me a very interesting question a few years ago: “What good does it do you to have a Billion Dollars, if the Secret Police can just take it away from you any time they want?”

When I see PRC-flavored money buying houses in the USA, I do not see people buying Real Estate. They are buying Life Insurance.

I don’t see the 10yr yield pushing up the 30yr yield to the 4.5% or so needed to reach the 6% 30 yr mortgage rate

https://www.zerohedge.com/sites/default/files/inline-images/886b9f26717685a83c7a4f8680afb98c.png?itok=d-rHwtcb

but then I don’t know what the fed has on its books to play with the long end of the curve, nor how important the longer debt is to anchoring finance. Just first instinct so not trying to counter or confuse.

The 30-year yield is already at 3.35%. It just needs 1.15 percentage points to get to your goal. 2-3 rate hikes and a slightly steepening yield curve will do that, for example. So by mid-2019.

The 30 yr mortgage is not priced off the 30 yr bond, because the mortgage amortizes and has a much shorter effective duration. Especially if rates drop and the borrower refinances or pays the loan off early! Not to mention the median owner will sell the house much more frequently than every 30 years. This is why the 10 yr Treasury (not the 30 yr) is the standard benchmark for the 30 yr mortgage.

Yes, I understand that (better now). The “trouble” is that for the 10yr to rise enough to give a 6% mortgage rate, unless the curve inverts, it will have to push up the 30yr yield at the same time to a level that stands a good way out from the decades long 30y trend. I just don’t know if that is feasible because I don’t know the effect that would have on long term positions using the 30yr bond as anchor, and I don’t know if they can actually force 30yr bond prices lower if it is sought as refuge in an uncertain market. For example the 30yr yield dropped these last 24hrs, it seems to surge and then retrace a bit each time after. I am NOT a market analyst, but I do like to know what a few of the fundamental readings are up to. I guess it is all part speculation because there is no sure way to say what the markets or anything else will be doing in a day or a weeks time.

I believe that Wolf is saying (exactly ) that the trendline you reference is being broken. I think that’s the entire point!

Well it has to change unless the US joins EU and Japan, but is it going to be broken or is it just being tested (as now) and then going to edge sideway for a while or even reverse ? The whole way the fed talks, which is really the only reference besides trying to figure what will happen if rates are lifted, is sort of ” We will tell you gradualy what the change will be “. Maybe they have decided that rates are going up or they are going up. The whole equation, including global rebalancing, is just way to big for me to picture…so I am just glad that I am somewhere near the sidelines watching and not too caught up in it.

I don’t think Wolf is saying definitely what rates will do, I think few would, he is pointing out the style that they trend higher and what the next target would seem to be.

I’m working with a group of Chinese nationals of which have green cards. They have bought $8 Mil in real estate here for all cash. Some of it is land to build spec SFR’s. They planned to build with cash but are now getting a construction loan as they can’t get $6Mil cash out of China due to government crack down on capital leaving China.

I’d say good luck to them :-)

Indeed. They’re going to need it. Talk about bad timing.

“if the mortgage rate rises to 6%, they’re maxed out at $287,000” (rather than $320k).

I think that will change quite a lot. Here in Portland OR that 1% difference would basically equate to a 30 minute longer commute. $320 is bottom end in “Portland Proper”. But that change does even more damage as you move up in price, which would maintain demand on low-end housing, no?

Mortgage rates are already above 6%. Lights out.

Fannie Mae added MASSIVE loan level pricing adjustments in 2012. IF you have less than 740 score, add a quarter point, less than 700, add a half point, less than 680, well, that’s a full point. AND if you are putting less than 20% down, well, add PMI and you are looking at APR’s well into the 6’s. Self employed, putting 20% down, 6% is a decent rate.

Home ownership at lowest level since 1964 for a reason. Buying a house isn’t fun and exciting anymore, it is anxiety and stress. Qualifying can be difficult, even for the best borrowers.

Asset based lending should be easier than it is. Dodd Frank really messed things up. (yes, something had to be done as mortgage lending was out of control in 2004, BUT that’s what the Federal Reserve is supposed to do. The Maestro should have been doing his job and regulating mortgages, looking for 125% ltv stated income loans and flushing them out. Instead, he preferred the cameras, the press, and being labeled “the man who saved the world”.

If you’re putting less than 20% and your score is below 700, you’re going FHA.

You are right the LLPAS are high and lower FICO stuff will now have APRs in the 6s.

Paradoxically as a mortgage broker, I’m super busy. Lower prices and lack of cash buyers would expand my volume significantly.

@Broker Dan. Not necessarily so, you can say we are outliers as we are dealing with local community credit union but we are presently doing Conventional, 20 year, <700 credit score (long story), high dual income empty nesters, 6.5% for an anecdotal data point.

Fro,

At what LTV (loan to value) is that? In other words, how much loan are you taking vs the value of the property?

Welcome back – ba da bing

Literally everything financial is falling flat on it’s collective face.

The global bond market is in convulsions and everything financial (especially interest rates) starts and stops in the bond market.

The Fed continues to tighten with a worsening global liquidity drought.

International political tensions are being stretched to breaking.

Same place – ba da boom! Welcome back to 08.2 on steroids.

6% Yawn, call me when it makes 16%.

I have seen and worked with higher rates than that also.

We still have the same long term issue we have had since 2004, House prices must come down, or wages must rise .

NIRP ZIRP policy’s have simply put off that day of reckoning.

The FED and Employers do not want WAGES to rise, and are taking actions to prevent realistic needed wage increases.

Hence there is only 1 option that remains long term, unless the cities are to die due to residence unaffordability.

Cities and nations have been killed by residence unaffordability before in History. It has suited those who publish history, to avoid this fact and topic.

I’ll state it again. The US economy can’t withstand the 10 year much above 3.5%. It certainly can’t withstand the 30 year over 6% without a major housing correction, not to mention stocks.

If this continues it will become obvious that the Fed IS intent on crashing the markets. The only rationale I can think of for them doing that is to get rid of Trump.

#Mike R: Trump appointed the Fed President. Privately, he wants the Fed to raise the interest rates. Publicly, he states it is a mistake to raise interest rates. He wants to interest rate to go up and the real estate market to crash. Even before he got elected, he has said the market is a bubble and he wants the interest rates to go up. Trump is a realty TV star and is awesome in telling people what they want to hear. Just that the people are foolish to believe everything he says.

I simply can’t imagine the FED would want markets to crash so they can bail out their friends again at the expense of taxpayers and savers (sarc).

6% mortgages are historically normal. Shouldn’t be hard for ordinary buyers to handle, if house prices were also normal.

What’s truly ABNORMAL now is 0% interest on savings. In an honest economy, savings interest would be 3% when mortgages are 6.

an important point. when will savings rates start going up?

If interest rates go up, doesn’t that inherently mean savings rates are going up?

Not necessarily. Banks pay as little as they can. If people (and more importantly, businesses) still keep their money with them without demanding higher yields, there’s no reason to raise rates.

They have, although slowly. Check CDs and treasuries. Or do you mean savings account rates at banks? If so, I expect the banks will fight it kicking and screaming. It will be the same as credit card rates being pinned high despite generation low rates everywhere else.

Perhaps, but the purchasing power of most American households has not for many years, and is not now, rising against inflation, so a 6% mortgage in 2018 is a very different animal than it was in 1970 or 1950.

Purchasing power yes, but, also I wonder about this stagnant wages vs exponentially higher housing prices over the past 30 yrs.

How does the changing role of dual income family earners play into this wage stagnation statistics? Meaning; in the 70’s, 80’s and even 90’s majority of families had 1 breadwinner and 1 parent that stayed home w/ the kids. The past 30 yrs that has changed whereby both parents are now contributing to the household; so, even if both income earners wages separately cannot afford current housing; the two together can.

So, when I see the stat that avg income is 60k and avg house is 500k and that wages are out of whack and housing is 10 times avg income; this doens’t really take into account most families now have double the income than in decades past. So, 120k/yr income can afford a 500k house.

Broker Dan,

Minor correction to your last paragraph: In 2017, median HOUSEHOLD income in the US was $61,372. This includes income from all earners in the household, plus other forms of income, such as interest, dividends, Social Security, etc.

https://wolfstreet.com/2018/09/12/real-earnings-of-men-women-income-distribution/

We are not living in an HONEST economy. That went away when the dollar was separated from gold.

To keep our “standard of living” high while our productivity dropped, America borrowed. That is the crux of the issue. Too much debt, too little opportunities for real productivity growth. Stagnation. The Fed will bail us out again and the US dollar will inch closer to loss of faith/desire on the part of all holders. That is when the rubber hits the road.

In the meantime, higher interest rates spell doom for our debt ridden economy.

Maybe housing will simply reflect a more normal reality than the hyped up orgy of recent history.

As a long-time carpenter I always check out construction trends and practices. I have been astounded at the recent changes to the industry. My first house was on a 1/2 acre lot and was around 900 sq feet with a full basement. It was 65 years old. The 2nd house was about 25% bigger to accomodate 2 kids, but still was situated on 1/2 acre and was 20 years old. Mortgage payment was 25% of net take home pay (single/sole wage earner). Over a few years, lots went down to .25 acre, and now .14 acre seems common. The buildings went from small bungalows to bling-filled monstrosities. Small lots and larger homes with no overhangs to protect against the weather contributed to ‘condo-disease’ rot problems and very poor (modern) but over-regulated building codes. Cut backs in municipal services saw building inspections farmed out to private engineering companies with sign-off authority. Regulations increased….service fees increased…taxes increased…and all the while home accoutrements became ever more expensive and were rolled into the financed purchase.

Now, here we are with slowly slowly normalizing rates and people are freaking out at 5-6%. My mortgage rates ranged between 9% -17% but the houses were modest and simple.

If aspirations and purchases don’t return to reality people’s financial situation will only become more desperate. Are we entering a great unwind of sane interest returns for savers and a collapsing Stock Market casino? I sure hope so. The last 20 years has been hard on people, families, and the environment. I attribute it to lower interest rates and rampant consumerism.

warning….one swear word, but I love this analogy. (30 seconds)

https://www.youtube.com/watch?v=i37uttMA6Mc

regards

Paulo – Sorry but even your running an ad against Prop 10 won’t convince me. There’s so much money being poured into those ads that I’m voting yes on it.

You might really need to rethink your financial situation if you feel the need to drive around town looking for .01/gallon cheaper gas or if an extra $50/month puts a mortgage over budget

I did mean to imply that SF Bay Area prices were not vulnerable ; on the contrary I think that they are going to crash.Just that housing prices are so high that 6% mortgage rates will not be the nail in the coffin

Much more important would be a tech stock crash and or intensification of the trade war with China. I consider this to be inevitable , given that politically the Trump administration has little to lose given Chinas aggressively response. Further it also looks inevitable that this trade war will spread to small military confrontations over Chinas militarized islands in the South China Sea.How much would the market open down if China sunk a a US warship. I will give you a little hint. It would not be a measly 800 points but nearer 10 times that

Infact for all over the usa.. 6 percent won’t cause any crash but definitely decrease the price

It would take events of bigger magnitude for the crash to happen e..g recession with big job loss

Wonder what the price of Gold would then do ?

As a saver glad to see rates going up, and not having to load up on ever riskier stocks. On the other hand, not sure how the up and comers can afford these mortgage rates and home prices on the jobs and salaries they get. However, my guess is as soon as there is even a little downturn, the powers that be will goose things again, and drop rates like a stone. People won’t take any short term pain if they can avoid it. Then the question becomes how long before the easy money drug works no more and real pain sets in.

The mortgage market is okay, you buy at these rates, they go down in two years, you refi. Housing is in a bubble sure. There is probably oversupply in housing, short of opening the hole in the wall where Mexico used to come in, and saying Chinese only, it will take some time to work it off.

Where do you see an oversupply of housing? Looking at a population adjusted housing starts graph from FRED:

https://fred.stlouisfed.org/graph/?g=lyer

shows we should expect the constrained supply. That matches your other statement that housing is in a bubble.

8 million vacant held off market by Wall street landords (EOFFMARUSQ176N)

https://fred.stlouisfed.org/graph/?g=lf3U

From your link:

“Included in this category are units held for occasional use, temporarily occupied by persons with usual residence elsewhere, and vacant for other reasons.”

Ok; so this includes 2nd homes or vacation properties, foreigners, or cash buyers that “invest” and let sit. You are aware that many properties in CA are bought cash by asians and remain unoccupied, right? I think the shadow inventory idea was applicable in 2010-2013; but, since the banks have rode the wave up unloading to the consumer.

There is plenty of living space mostly misallocated. Boomers have more living space than they need, working poor need to be close to their jobs. The first group moves into assisted living, the second group moves up the economic ladder. Birthrates are down, do you need five bedrooms? The market creates more accessible housing, location, price, on top of the square footage in the burbs.

Rents have really ramped up since 2008. At 6%, the monthly PITI is $600 per $100,000 in mortgage debt. At $3,000 per month rent, that is $500k FTD. Subject to economic changes. I think the housintg market may have more support that some might think. Also, I imagine some millenial couples have been putting off starting a family. This would tend to indicate that luxury apartments, particularly newly built, might see some softness in occupancy and rents. BTW, $3,000 a month is a Studio in Brooklyn & maybe more in Manhattan.

Cities and municipalities are getting more extractive on new construction, so costs to build new are not likely to decrease, particularly with higher interest carry.

And tangentially, I still think flyover areas and areas like SE USA with relatively cheap housing will see an inmigration of companies and their employees will be home buyers. Its funny, many people in Cali are trying to figure their way out and many people are trying to figure out how to move here.

As someone in the SE USA (Mississippi), I have been seeing more and more California license plates in the area. I just hope they keep passing through and not land here, paying cash for houses after selling off at peak back home, thus rocketing our prices up further. As it stands, trying to buy a home nearer to work is already a fairly high % of take-home pay. I’ve been saving for years and have enough for down payment and 6 months emergency but really don’t want to pay $115/ft when 4 years ago it was probably around $90… not to mention this area of the state has wonderful foundation-destroying “Yazoo clay” that causes huge expenses for a lot of people. Most everyone is “how much a month” vs caring about the overall cost of carrying the loan (total paid by end of loan, scheduled and unplanned maintenance, tax increases, HOA, etc). LOTS of SFR rentals available at silly prices by “entrepreneurs” and various LLC. “Entry level” homes are selling for stupid premiums while higher end (250k+) often sit on the market for months.

Deleveraging is a brutal, involuntary experience for the overextended spec crowd.

Not my problem. I have no skin left in the game, so meh.

As for asset deflating, the strong dollar is the cause. Assets no longer have a return, just a spec gain value.

And that is why we are not going to be able to bail out this mess.

America is now a bigger Sears….

Would that make Mexico KMart and Canada JCPenny’s ?

I am ignorant immigrate from China and have no idea about the economics, but I agreed with you about that the strong dollar could cause the asset deflating and I think it would cause price cut almost on everything. I have to say there are only a few Chinese could afford million assets in US. We know the properties are extremely overvalued in China and Hong Kong but not many will sell the assets and exchange to US dollars even without the government control. But Chinese ordinary people would like to have some US dollars (cash) on hand just because they don’t have much confidence in the officials. No matter the US dollar strong or weak, they will keep buying it. So, if the Feb will not print much money, I think the US economy will deflation.

In addition, talking about the house, if house price continues going down until builders can’t make money, who will build houses for us. I don’t have a statistic table here, but I heard Americans should have built a lot more house in the past 10 years if there was not 2008 financial crisis. There are so many 50 years old houses now and I don’t think millennials want to live in these buildings. If the inventory is going even lower after next crisis, the house price will rebound much higher than today’s peak.

I think housing problem is very difficult and I found even the geniuses in Silicon Valley are still looking for a solution. I know the wage growth is awful over the past 10 years, but there are also lots of high paying tech (IT and biotech) jobs created during this period. I don’t want to say the house overpriced or undervalued but I want to say it is controlled by the growth (population, wage, start-up, economy, material and government control and so on…)

Keep reading these web sites.

Soon, you will not be ignorant.

;-)

Meanwhile, you got this right:

“Chinese ordinary people would like to have some US dollars (cash) on hand just because they don’t have much confidence in the officials”

LOLOLOL

And on cue… here come the no down payment, sub prime loans :-)

https://www.cnbc.com/2018/10/12/thousands-line-up-for-zero-down-payment-subprime-mortgages.html

They say they have not had a foreclosure in last 6 years! Although they should get some credit and the lending is not as predatory as in 2000s.

But Of course, 6 year ago was the bottom of home prices. Once prices slide foreclosures will start.

That was the stupidest article I have ever read. There was 0 information on the program and a 90% approval ratio for lower income / lower credit score buyers it’s a joke.

Willing to bet there’s an extra 0 on there and it’s more like 9%.

There is actually a down payment assistance program in California with many restrictions. 90% won’t qualify.

I am pretty sure the 90% approval is what they meant. It’s the way the sentence is worded. The BOA VP is actually bragging.

I assume these are private mortgages? Anyway they are very small in number overall. I doubt housing is where the next blowup will happen. It’s too soon after 2008.

Ok, so I looked up the guides briefly.

31% debt to income ratio for the mortgage

43% debt to income ratio for all debts

It’s defacto good credit bc even though they say no credit score required they review the credit history and require no lates in the past 12 months.

Also there are payment shock guidelines and reserve requirements basically meaning that your new mortgage cannot be too much higher than your current rent and you should also have money in the bank post closing.

All collections charge-offs and other derogatory debts need to have a zero balance or be paid off prior to approval which in the low-income sphere is rare to see.

Low income levels as well.

In summary, in order to qualify you must have:

good credit history as well as rental payment history

Reserves in the bank

A new mortgage not much higher than current rent

Total debt to income below 43%

I think the vast majority will not qualify for this program, so the few that do probably will have a pretty low default ratio.

Thanks Dan. Yeah it’s seems nothing like the old sub prime mortgages. I agree we are unlikely to see a repeat of what happened in 2008 nationally anytime soon.

By 90%, I assume that the applicants need to meet all these things before they can apply under this program.

AS,

You are correct, today’s “non prime” is not in the same Galaxy as the sub-prime loans written back in the day.

I’ve seen them then and now.

House prices need to come down – back to 2 or 3 times gross income.

A friend of mine is a neurosurgeon in California. Shouldn’t he be able to buy a house in Laguna? HE spend hundreds of thousands on education, he is one of the tops in his field…but Laguna Beach “starts” around $10m. 2200 SQ FEET!) The 3 friends we know with houses on the water – hedge fund, private equity, and VC. People living in the fiat/investment world. You can’t get into the 1% (or 5%) working anymore – LABOR ISN’T WORTH THAT MUCH. it has to be leveraged, investment, speculative, gambling.

WE are all working for peso’s. It takes a million of them to buy a decent house. Ridiculous.

I am for currency appreciation through housing deflation.

I was talking with a realtor recently and she said that it was quite common for people to put down as little as 5% for a 30 yr mortgage.

She didn’t elaborate how that was done (I thought 20% down was the norm) but she claimed that pricing my house a little higher wouldn’t effect the buyer traffic all that much.

Anyone know what’s going on with mortgages today?

Minimum down is 3% for conventional and 3.5% for FHA.

That is depending upon the loan amount limit however. When the loan amount is greater than $453,100 the minimum down increases to 5% for conventional.

This time is different b/c the FED continues paying interest on excess reserves (paying banks to not lend)

“housing bubble 2.0” Seriously?

You’re a smart enough person to know Housing bubbles are not a new thing. They didn’t originate in 2008.

2008 was simply one in a LONG line that goes back Centuries.

Would be better to call a housing bubble by the year or region that it happened. 1991, 1980, Florida bubble of 1925, etc.

As I have pointed out many times, I start counting housing bubbles starting in 2000 AD, not in 3000 BC: Housing Bubble 1 was the first housing bubble this century. Housing Bubble 2 is the second one this century. That’s what that means.