A fiasco threatens to spiral out of control.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

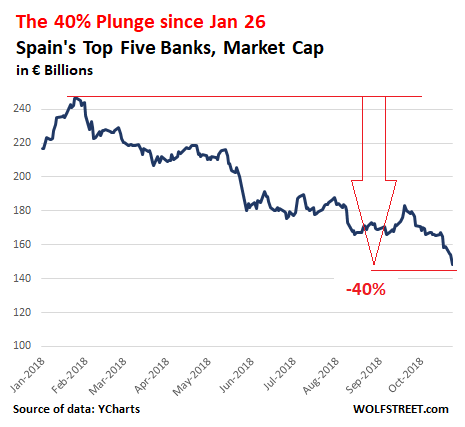

In the last five trading days, the shares of Spain’s five largest listed banks have re-energized their plunge that had started at the end of January and now amounts to 40%. The cause for the recent drop? A shock ruling by Spain’s Supreme Court that lenders, rather than mortgage borrowers, should pay the contractual tax on mortgage loans, on the grounds that the lender is the only party with an interest in getting the loan certified by a notary, since this is what enables the bank to begin foreclosure proceedings if the borrower defaults on payments.

Even the Supreme Court’s desperate decision last Friday to suspend its own ruling a day after it had announced the ruling, a historic flip-flop that left everything in limbo and its reputation in tatters, failed to stop the rout (data via YCharts):

On Monday, the Supreme Court announced that it won’t decide who has to pay the tax on mortgages — the banks or the borrowers — until November 5. In other words, there will be two more weeks of acute legal uncertainty.

This has plunged Spain’s mortgage market into chaos. For years Spanish banks and builders have been desperately trying to breath new life into the market — including, in some cases, by resurrecting 100% mortgages, a high-risk instrument that helped fuel Spain’s madcap property boom. But now, thanks to the pervading legal uncertainty, the market has all but seized up.

On Tuesday, sources from a number of large banks told the financial daily Cinco Dias that the only mortgages being signed are with clients who had already arranged to sign the contract before last week’s furor and who don’t mind paying the mortgage tax. “We’re not signing any new ones,” the sources said.

Banks have said they will continue to apply the previous legislation: i.e., it will be the clients who pay the tax. If they refuse, the banks will offer to postpone the signing until the situation is cleared up. Some banks have even included a new clause in their contracts stipulating that in the event that the Supreme Court rules that the bank must pay the tax, the customer will be reimbursed.

Meanwhile, a group called Association of Judges for Democracy is calling for the head of Luis María Díez-Picazo, the senior judge that suspended Thursday’s ruling. As a result of Díez-Picazo’s “dire mismanagement” of the situation, the association says, concern has grown “among citizens, who don’t know what to do with their mortgages […], and has cast doubts about the impartiality and independence of judges, creating a deplorable image of judges among the public.”

To try to repair that image, the Supreme Court is expected to ratify rather than overturn its previous ruling on Nov 5, while limiting the extent to which it can be applied retroactively, thereby minimizing the banks’ financial pain. According to credit rating agency DBRS, the most likely scenario is that the banks will end up having to pay the tax from now on but without having to reimburse mortgage users the taxes they’ve already paid. Such an outcome could end up costing the banking sector around €700 million a year.

In the second most likely scenario, customers will be allowed to reclaim their tax fees going back four years, which would end up costing lenders an estimated €2.3 billion — roughly equivalent to a quarter of the net domestic profits Spanish banks generated over the last four quarters. In other words, painful but bearable.

In the third, least likely and worst-case scenario, the ruling will be applied retroactively to the past 15 years, the maximum limitation period for civil claims. In such a case, the total bill for Spain’s banks could reach €16.9 billion, according to DBRS — almost the equivalent of 2 years of the banks’ net domestic profits.

The hardest hit lender so far has been Banco Sabadell, Spain’s fifth largest bank, which has seen its stock slump 18% since last Thursday. For Sabadell, 2018 has been an authentic ano horibilis. Besides its mind-boggling and costly IT blunder at its UK subsidiary TSB, Sabadell is also suffering the side-effects of being one of the most exposed European banks to Italian sovereign debt. It is one of the weakest capitalized banks in Spain.

Now add to it the growing uncertainty about its mortgage business. If the Supreme Court’s final ruling, scheduled for November 5, comes out in favor of the mortgage customers and against the banks and the law is applied retroactively, Sabadell’s capital ratio would take another hit. Since Thursday, its shares have plunged 18%, to €1.04, its worst daily close this century.

Sabadell won’t be the only lender to suffer the consequences of an anti-bank ruling. The core capital of other domestic lenders, such as Bankinter and state-owned Bankia, is likely to be hit even harder, while the fallout for Spain’s two largest banks, Santander and BBVA, which are much more globally diversified, is likely to be less pronounced. By Don Quijones.

Plunging bank stocks got the Court’s attention, or something. Read… Spain’s Supreme Court Flip-Flops on Mortgage Ruling After Just 1 Day Amid Bank Stocks Bloodbath, Legal Shitstorm Erupts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

After the Spanish Supreme Court’s “floor” ruling, banks should have grabbed the opportunity for lawyers to crawl all over the mortgage closing process and ensure each step’s basis in law (including identifying ambiguous laws).

Politicians and banks have been fighting over who is the most disgraced in the current environment; looks like the Spanish Supreme Court decided to join the mud-wrestling.

This level of incompetence is truly impressive – hard to pick a winner. All European countries should go back to using Monopoly money as their “sovereign currency”.

Maybe we can loan them Brett Kavanaugh

I see no humor in this comment, only ignorance.

It wasn’t a joke.

Every time I go to Spain, my uncle asks me to look for a “retirement property”, so I have formed an impression of the Spanish real estate market, at least outside of the tourist meccas like Palma de Mallorca.

The impression I have formed is about the same as Italy: a massively overbuilt country where nobody (starting from the government and down to ordinary landlords) want to see real estate prices balance with both the massive stock and the very tepid demand. Spain is already a nation of homeowners (77.1% ownership rate, the second highest in the EU after Romania) and, after very strong population growth in 2000-2010 (due to immigration), population has been declining at a yearly rate of around 0.1% since 2016.

In spite of the truly mind-boggling unsold stock, Spanish construction firms keep on building and adding new stock: I’ve been told they are like “tiburones”, sharks, an apt metaphor as these creatures lack a gas bladder and hence have to keep on swimming or sink to the bottom, albeit I suspect the metaphor was originally used in another equally apt fashion.

Massively overpriced real estate is one of the cornerstones the Spanish economy is built upon, just like Italy, and I have zero doubt this court ruling had been politically motivated. After all monthly mortgage originations in Spain struggle to hit the magic 30,000 number, a far cry from the 120,000/month average of Housing Bubble 1.0 (this is 1.2) but still deemed absolutely necessary to keep the all-important construction sector afloat.

However in so doing the Spanish government overestimated their own banks’ health. It’s a classic case of believing one’s own propaganda, as European banks are if possible in even worse shape than they were in 2010. Eight years of complete impunity, free handouts and accomodating monetary policies aren’t bound to make them any better.

So now the juggling act has started, proving once again that one can have the cake and eat it too only for so long.

The impression I have formed is about the same as Italy: a massively overbuilt country

The other thing is: Spanish regulations are rarely enforced until suddenly they are, and, when that happens, very much to the letter.

It is not uncommon for people buying retirement property in Spain to discover that their house was built illegally, they don’t actually own the land, the local council did not know that the property was connected to water, waste and electricity for years … et. cetera.

One needs to hire a good Spanish conveyance lawyer to downgrade the risk of Spanish property investment from “certain ruin” to “potential” :)

Italy and Spain have some of the tighest regulations on real estate and construction in Europe, far tighter than Germany.

Yet these laws go almost invariably non-enforced. Local authorities always complain “lack of personnel”, rather strange given it’s never an issue when commercial activities are concerned, but the truth is they are afraid to spook those real estate speculators upon which so much rests, from GDP growth to their own budgets. Impact fees allow all those useless sports centers to last one more year and local “artists” to dump their monstrosities upon councils which perpetually complain the most abject poverty. But I am digressing.

What you are mentioning is basically the time-old mugging of non-residents, who don’t vote locally (eh eh) and are always assumed to have more money than common sense, hence they will just pay whatever’s asked from them and shut up.

Problem is it doesn’t work anymore.

Spain and Italy have batallions of lawyers who are only too happy to offer their services to foreigners, from pre-purchase legal work (checking for mortgages and other nasty surprises, checking contracts and translating them etc) to threatening greedy councils with 6-7 figures lawsuits. The threat of years of legal battles, with nothing certain but big bills is usually enough to put the highwaymen back in their place.

Spain has secure property rights (once you’ve got them) but doesn’t have a modern Torrens system of land registry.

Under this system, which we take for granted, the land registry issues an indefeasible title, i.e., the title you obtain cannot be challenged by some long- lost relative, who claims they were cheated etc.

In Spain the process resembles the previous system under English law centuries ago, the Doctrine of Notice.

This meant the buyer had to take notice of potential claims or ‘buyer beware’

He had to investigate the title to prove there no such claims.

In Spain (and Uruguay etc.) the transfer of property that a notary or land agent could do in Canada in a couple of days,

(in an all cash deal) can take more than a month. Your notary or lawyer has to investigate the title.

A friend who bought an interesting century- old house in Spain

was nearing completion when his notary found an unexpected covenant. A lady (not the owner) had the right to stay overnight when she was in town. This was from forty or so years ago and no one had seen or heard of her since.

My Canadian friend was taken aback but went ahead anyway.

She never showed up while he owned the house.

Uruguay is similar. To convey a 100, 000 piece of property would cost about 6% split between buyer and seller.

The cost is based on the value of the property.

You might think that once this has been done,the next time will be much cheaper, but no, it all happens again.

Around here there is make-work trend in survey certificates, to make them expire after each transaction,

Far too much property, too few buyers, shrinking, impoverished population. Not much for a shark to feed on….

I’m looking for a nice house in my ancestral Pyrenees – but not too isolated – and I’ve noticed significant price reductions to sell and quite reasonable prices.

All very encouraging for a cash buyer trading down who really doesn’t care what the property is worth when they die.

Younger families and individuals just can’t buy these -very suitable – properties, and are having to make do with cheaper apartments, often just rented, or living with the family (which is, of course, simply a reversion to pre-boom patterns in Spain).

And yet, in the regional capital, one reads that ‘130,00 new apartments have to be built, now!’

The same local Socialist government is talking about subsidies to enable young people to ’emancipate’themselves. Even Socialists have to prop up the rental market.

Who needs 13,000 apartments in Spain? You have whole abandoned villages, with nobody living there but foxes and kites. I am sure whoever owns them would be happy to let them go for a nominal sum.

Unless of course this is yet another variation of the Underpants Gnomes principle: 1) Steal underpants 2) ? 3) Profit!

I’m sure the banks in Spain are exactly like ours. Certainly, they have only our best interests at heart.

Spain, Italy, Venezuela, Argentina….

I was going to risk possibly offending DQ by asking if there was a Latin correlation here, but then I remembered Ireland, where the RE excess exceeded Spain.

One difference however. The Irish bubble had an end, a vicious one, with the main three banks being nationalized, and a painful return to reality. (An Irish banker, after years of litigation has been sentenced to a jail term.)

But the RE thing in Spain seems to drag on and on.

Or are we nearing a point where the cans can’t be kicked any further?

Politically motivated courts which country does not have them ….lol……also canadians as can seem by local political winds if change are demanding a social housing type platform…marker driven Is out get ready for the collapse here in Richmond bc prices are down 20 percent already and yet everyone is killed into believing its s sellers economy …..would be nice to the monopolist Canadian banks face a tax that would straighten them out but I forgot……Canadian banks own the governments and courts in Canada……..perhaps 11 percent interest rates will help let’s see. In canada the banks have free reign yo do anything they want anything….

On a rare good day for banking stocks in Europe, Sabadell and Deutsche bank continue to go lower in share price. Something not good is going on with these two.

Most European banking stocks are really penny stocks: while we lack a precise definition like the one the SEC adopts, I think €5 is a good upper valuation limit for a penny stock these days.

Deutsche Bank was around €9 last time I checked, meaning it still has a long way to go.

And like Wolf always say “Things never go to heck in a straight line”.