The chart that makes me scratch my head.

Tesla reported earnings today – a profit, its third quarterly profit ever, and its first profit based on operations rather than the sale of taxpayer-funded pollution credits. So it’s time to reflect.

I have always given Elon Musk full and extra credit for putting electric vehicles on the map and making them cool, after others have tried for about 150 years and failed.

But I have never been a fan of Tesla’s financial performance, which has been rock-solidly abysmal until today’s report. I’ve never been a fan of the incessant falsehoods propagated by Tesla’s fearless leader for the sole purpose of manipulating up the share price, and very effectively so. And I have never been a fan of Tesla’s share price, which has been – and continues to be even today – ludicrously overpriced. But today’s quarterly earnings report had a lot of good stuff in it though it left me scratching my head.

Sales growth has always been strong at Tesla. And it should have been, given how investors and governments have subsidized those sales to the tune of many billions of dollars. Total revenues in Q3, including automotive and energy, jumped 128% from a year ago to $6.8 billion. Nearly all of that growth came from automotive sales as Model 3 sales ramped up.

Cost of revenues jumped 109% to $5.3 billion.

Gross profit – revenues minus cost of revenues – more than tripled from a year ago to $1.5 billion.

Operating expenses rose only 12% to $1.1 billion.

Income from operations – as a result of the surge in revenues minus the lesser increases in costs and expenses – reached $417 million, compared to a loss of $621 million in Q3 last year. That’s a $1-billion swing.

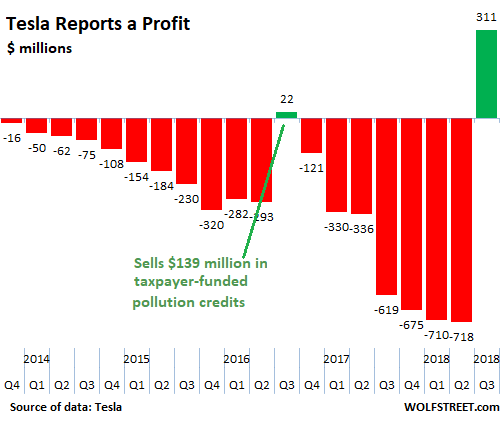

After interest income and expense, other income and expense, and taxes, the company generated a net profit of $311 million, compared to a loss of $619 million a year earlier, and a loss of $718 million in the prior quarter:

But this chart is a head-scratcher. It’s funny-looking for anyone who has been around business for a while. There is a total and sudden break in trend, without gradual reduction in losses, and without transition of any kind. It just jumps from a sea of record losses to a profit. A magic wand comes to mind.

This was only the third quarterly profit ever. Tesla has never made an annual profit. This chart which goes back to 2014 shows two of them. The one in Q3 2016 was triggered by the sale of $139 million in taxpayer funded pollution credits. It was followed by an even bigger sea of losses.

Digging into the asset side of its balance sheet, comparing Q3 to Q2 (ended June):

Cash galore, suddenly. Tesla reported positive free cash flow of $881 million, after having burned through billions of dollars in the prior quarters. Cash and cash equivalent increased to $2.97 billion at the end of Q3, from $2.24 billion at the end of Q2.

This is good stuff. At this pace, if it continues to generate cash like this, Tesla will not need to raise funds.

Accounts receivable more than doubled, not year-over-year, but from Q2 to Q3, to $1.16 billion in Q3, from $569 million in Q2, after having mostly been flat for a few quarters. These are the amounts Tesla is expecting to get paid by the recipients of its merchandise or their lenders. But doesn’t it sell its cars on a cash basis, meaning that it gets paid at around the time of delivery, either from an auto lender or the customer? And its leases are tracked in a separate line item (see below).

Inventories remained flat from Q2 to Q3, at $3.3 billion

Outstanding operating leases of vehicles at $2.2 billion were down a smidgen from $2.3 billion in Q2. And in terms of its solar business, outstanding leases were $6.3 billion, about flat with Q2.

Which takes us back to the doubling of accounts receivable. So who owes Tesla suddenly $586 million more in Q3 than in Q2? And how did that impact revenues? I would like to know.

On the liability side of the balance sheet, accounts payable – money that Tesla owes its suppliers – jumped to $3.6 billion from $3.0 billion in Q2. This makes intuitive sense, given the surge in production, and the bigger bills it has to pay its suppliers.

I’m still scratching my head about the chart above. While I’m at it – wife is watching me askance, wondering if I have lice – I’m thinking about the abrupt departure of Tesla’s chief accounting officer in early September; and the sudden departure of its CFO last year, upon which Tesla brought back its old CFO, and all the turmoil these personnel changes engendered. These are the folks responsible for the financial statements we just looked at.

So I’m a little nervous. There are lot of big changes in these financial statements, largely due to the surge in sales and production, which triggers big changes in the balance sheet. I just need confirmation for a few quarters before I see where this is going.

The confirmation could be that Tesla will or will not have to raise new money – and if it has to raise new money, what it will use it for. According to the growth of its cash balance, it would not need to raise new funds. However, if Tesla does suddenly need to raise new funds without a compelling reason, such as building a mega-factory or something, and if it uses these financial statements to butter up potential investors, all kinds of alarm bells will go off in my head.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

This is all in keeping with Elon’s promise that he doesn’t have to raise cash this year. Now, it seems like this will come true. No need to raise this year, we’re profitable. See. Move along. Then WHAMMM, on January 1st, Elon will raise a Bajillion dollars.

Although I’m curious if Elon will be able to keep his mouth firmly shut for the next three months to allow TSLA to find stability. Come on, Musk, tweet, you know you want to. Just do it. It’s entertainment for the masses.

Sure, your chart looks funny. But it’s almost Christmas, it’s time for miracles.

Just because you change the way you count the beans, does not change the actual number of beans…. Lipstick on a pig comes to mind.

B

You plainly have zero understanding of crooks, incompetents and beans.

The perverse effects of smoking hopium in non-GAAP Utopia.

Great article! A head-scratcher for sure.

The famous short-seller Jim Chanos has been shorting Tesla since 2015. He is cautious about calling Tesla a fraud. “There’s a lot of questionable activities, questionable accounting. But fraud needs intent.” He says that Tesla might turn out to be a legal fraud, which is more common. In such cases, “there’s lots of intent to deceive, even though it might be covered by safe-harbor provisions and accountants and lawyers have signed off. And by the way, those things never get prosecuted.”

“But doesn’t it sell its cars on a cash basis, meaning that it gets paid at around the time of delivery, either from an auto lender or the customer?”

A lot of people on Twitter have complained about paying in full for their Model 3 at the end of Q3 while not having received their car by the end of the quarter. The delivery rep setting a delivery date a few days ahead, the customer paying in full, and that delivery date is suddenly cancelled. Some have had 3 delivery dates cancelled by Tesla. Some have had their assigned VIN In Texas in particular, people were complaining of making their first loan payment for a car they weren’t in possession of.

People have also said their assigned VIN was removed and even told their car was sold to someone else. Makes you wonder if that 17% Q/Q drop in COGS per vehicle was helped from having the same car sold more than once.

“…drop in COGS per vehicle was helped from having the same car sold more than once.” If this really happened, and it can be proven as a purely financial strategy to pretty up the Sept 30 balance sheet, Musk is even more of a genius than I thought. It reverses itself this quarter, but not before the evil genius has raised another few $ billion.

Musk IS a genius. How many people (including myself until recently) believe that he invented the electric car and founded Tesla? Classic genius conman.

Don’t forget that people love their cars. I haven’t met a single owner that regrets their purchase.

The model 3 could be the top selling car for 2019.

If demand continues to increase and oil goes to $250/barel due to geopolitical events , Tesla could be printing money for years to come.

The top selling car in America in 2017 sold something like 400,000 vehicles. And I’m trying to skip the trucks at the top of the list.

400,000 vehicles is making 33,333 a month.

Elon Musk might have figured a way to juggle some numbers quickly to make it seem like he made a profit just when he needed to do so when the board was grumbling, but making over 30,000 cars every month is something you can’t do with fancy footwork on the accounts.

“Love their cars”. Cognitive dissonance?

Wolf

I agree with you. This profit graph you showed is very abnormal. One other strange event was the Famous short seller, Andrew Edward, announcement of covering his shorts and becoming Tesla’s sudden fan right before the earnings. Tesla has huge amount of convertible bonds meaning the company has to return lots of cash to the bond investors if the stock price doesn’t stay above certain value. Tesla can’t afford to pay that cash back and that’s why Elon is trying everything to make sure the stock price won’t go down. One example is his famous 420 tweet. I am not sure if you are a believer of technical analysis but if you look at Tesla’s price chart, $280 is an important price and every time the stock breaks down this support, Elon does something to squeeze the shorts. Never the less, I do like and respect him as a genius .

I suppose at some point in simply comes down to whether you trust Elon Musk.

Items that suddenly jump from one Q to the next usually involve some fine print that they’ve started accounting for something differently than they did before. And a sudden claim that more people owe them more accounts receivable than before gets at least a Vulcan eyebrow raise with an ‘interesting.’

Fascinating how ‘manufacturing hell’ which bled money all over the joint suddenly turned into an efficient organization that makes lots of money. My grey hairs agree with Wolf that this usually does not happen overnite or even within one quarter. Seems a bit like when the kids clean the house really quickly, but there are big lumps under the rugs.

Makes one wonder… With numbers like these why did Musk want to take it private? Why did the CAO leave after just one month? These happened during “their best quarter ever”

Tesla broke ground with their new China factory last week. Elon is going from strength to strength.

There isn’t a single global automaker that hasn’t had factories in China for years. Tesla is just trying to catch up. Tesla’s sales in China are minuscule. China is the largest market in the world. If you want to sell a larger number of cars in China, you have to make them in China.

I also understand that China’s electrical network does have some issues as well.

Wolf,

Is there any other auto manufacturer that has a factory in China that is 100% owned by that manufacturer? And doesn’t have to share IP?

https://money.cnn.com/2018/07/10/news/companies/tesla-china-factory/index.html

“Tesla said it will be the sole owner of the factory. Until now, China has always required foreign companies to enter joint ventures with domestic companies.”

Yes, this is a new thing — thanks to the pressures of the trade war, the Chinese caved on that point.

BMW is buying out its Chinese partner. Going forward, the Chinese will approve foreign automakers to set up shop without joint-ventures. And they will allow automakers to buy out their joint venture partners on a case by case basis.

In the past, technology transfer via JV was required, in addition to the unofficial technology transfer that happens in China anyway. The official technology-transfer requirement will likely disappear, but the unofficial technology transfer will continue hot and heavy.

The Chinese will transfer out plenty of technology from Tesla’s factory, whether Tesla wants to or not. That’s the price you pay for operating in China.

By the time Tesla’s factory is up and running, it will be one of several foreign automakers operating without JVs.

In my opinion there is deterioration of balance sheet:

(In thousands)

Inventory increased to 3,314,127 from 2,263,537

Current portion of long-term debt and capital leases :

increased to 2,106,538 from 896,549

Long-term debt and capital leases, net of current portion

increased to 9,672,613 from 9,418,319

Shares used in per share calculation,

number of shares increase to 170,019 from 164,897

I cast my mind back about the furore over Tesla asking their suppliers for retrospective discounts. Could the $600m come from that arena?

If Tesla was disposing of surplus production equipment (say, all the industrial robots it ripped out of its production lines and stored out the back of its factory) would these appear on the regular Accounts Receivable line?

Perhaps they sold these back to Fanuc on rather generous credit terms?

Just read through the report. This seems to be the explanation: “our accounts receivables also increased by a similar magnitude since the quarter ended on a Sunday, which limited our ability to collect cash from the banks financing our customer loans.”

So accounts receivable more than doubled from Q2 to Q3, to $1.16 billion in Q3, from $569 million in Q2, because the quarter ended on a Sunday??????? Lots of quarters for lots of companies ended on a Sunday over the years, and that doesn’t cause AR to double, from one quarter to the next. Tesla’s explanation is just hilarious.

In Tesla’s case, it would have meant that it collected over $500 million on Monday. If that is what Tesla meant to say, it can be classified as fiction.

Friday afternoon + Saturday + Sunday = 8k cars a.k.a. delivery hell, remember?

Yep, all believable. And only one drop of blood required to do all the tests you need.

The real genius is EM’s ability to get fans to live with cognitive dissonance.

Hay ho. The story has some way to run yet.

There was a case in the UK of some financial fraud (money conned from people they would never see again). The uproar from the ‘losers’ of said money was towards the police, who should have left the scammers well alone because it was all fine. ie they blamed the police for the loss of their money not the scammers.

This is my best guess of how this story will end.

That’s exactly why the SEC was so lenient. They didn’t want the blame if TSLA came crashing down.

And that drop of blood will PROVE youre 1/1064th Native American!

New financial folks wanting to make a good impression?

Worked at GE and Enron for years….

*****

I’m thinking about the abrupt departure of Tesla’s chief accounting officer in early September; and the sudden departure of its CFO last year, upon which Tesla brought back its old CFO, and all the turmoil these personnel changes engendered. These are the folks responsible for the financial statements we just looked at.

Sales jumped 128%. COGS sold jumped 109%. I recall Musk pushing suppliers to cut prices in August. So that relationship could be legit. Lots of stories of Tesla finally getting it bearings on manufacturing the Model 3.

Cash should jump based on the gross margin. Divide the total sales by number of cars sold. If it is within the range of car prices, the whole thing should be good.

Reminds me of the fable of the pencil and the paint.

In a few years EV’s will be ubiquitous and sold by every automotive manufacturer….IMHO it’s time for Mr. Musk to “fold up the tent” on Tesla and devote his time/abilities/finances toward development of Ion Drive for serious space travel to Mars and beyond…Musk and Space-X would have an eternal place in history “far beyond” anything Tesla in now doing.

Meh – “Accounts Receivable” could be the good-ole Vendor Financing.

Company Execs needs to boost the last quarter for Christmas Bonus Time, so they push the (unfinished) product stock onto vendors, then book it as “Sold, Delivery in 3 months”. Those expected payments in Jan/Feb will be “Accounts Receivable”.

The product doesn’t actually have to leave the yard, and they can f.ex. have an option in the sales agreement for non-recourse cancellation.

The “other side” gets maybe a case of good whisky, a seminar held at a sunny luxury resort or a set of golf clubs with Club Membership for the inconvenience.

When a company is actually crooked, those vendors will of course not need to know about their recent purchase and the future cancellation of their orders. Since one can compare books on both sides, that would be reckless and is usually the last gasp for air before Chapter 7.

We already have legalized non gaap accounting, mark to market suspension, buyback accounting where everbody looks at eps rather than dollars of earnings.

Reserve accounting and standard cost accounting has been a huge area of fluff accounting since the beginning of time. The potential is limitless especially as a company moves from startup status.

And nobody outside the accounting staff knows the difference till the year end audit which should compare financial statements on a consistant basis.

Auditors (in Tesla’s case – PricewaterhouseCoopers LLP) just don’t show up on the last day of the year to conduct the audit. With significant change in finance senior staff, they’ve probably been heavily engaged in the 3Q results.

It’s unfortunate auditors have so debased their credibility, but this looks like an interesting story; it’ll be interesting to see how it plays out.

I don’t pretend to be able to read manufacturing financials.

Enron anybody?

For years the accounting and reporting was faked. It was a con game from the get go. When it all collapsed it seems so obvious..

Why would the financial staff quit just before such an impressive quarter?

They know what’s coming down the pike.

The “staff” didn’t quit, a couple very short-term senior leaders did (not a good thing, to be sure).

Presumably, lots of others in the finance department have licenses they’d have to be worried about.

“I’ve never been a fan of the incessant falsehoods propagated by Tesla’s fearless leader for the sole purpose of manipulating up the share price, and very effectively so.”

What if he is pulling a fast one again. It won’t be the first time.

Time will tell.

I wouldn’t scratch my head over this based on Musk’s character and the terrible financial condition of the company. His “wrist slap” by the SEC for the major short squeeze he engineered is all you need to know about this.

The numbers are phony and he’s counting on any government response to be slow and dragged out.

Don’t short the stock unless you are prepared to first take some heavy losses (on paper) and can ride out the bumps.

The company is toast sooner or later. Other electric cars are coming into production but the big factor is when the economy hits the shitter (coming soon to a theatre near you). When that happens, sales will crash.

Game over.

Wolf, The account receivable increase was explained in the CC as related to Fleet sale to enterprise. Tesla used to own a bunch of cars for service loaners (since they do not have a dealership model) and they sold it to enterprise on the very last day/days. They said that funding did not come through in Quarter ending time since it was a bank holiday.

These are all one time tricks not sustainable.

If they sold a fleet to Enterprise, wouldn’t that have pumped up profit for the quarter as well? If so, why didn’t they back that out as a one-time item in the non-GAAP accounting? Companies are quick to back out write-offs as one-time items.

This is why the SEC shouldn’t allow companies to highlight non-GAAP accounting.

Non GAAP accounting is essentially fantasy accounting. No serious person believes in it. Execs go to jail (well if law is upheld. These days seem to be different…) if they lie in GAAP. They can do whatever they want in non GAAP without going to jail.

Also, the fact that they sold the fleet at the very last minute is negative in my opinion. It is as if “Enterprise asked for a very sweet deal, they did not want to do it unless it was really necessary and at the end of quarter they really needed to do it…”

Simple answer, I have seen this: note sales and A/R are up for a company where sales are essentially cash. The obvious answer is they booked either fictitious sales or sales in advance which would not result in cash but rather an increase in A/R.

->What I Think about Tesla’s Financials

Tesla’s investors do not care what you think. I think Tesla’s financials are . . . questionable. Tesla’s investors do not care what I think either. At this moment, TSLA shares are up 25+ pts, 8%+.

To win the sympathy of the masses, you must tell them the crudest and most stupid lies. This is a great quote, and it works on many levels.

It is just as well. A triggering event will occur in twelve days, followed by others in quick succession. I still will not discuss The Year of the Jackpot.

Are you expecting the election results to cause some sort of market turmoil? Or some other event related to it, such as outbreak of politically motivated violence? I’m curious.

For What It’s Worth, I’m an historian, sponsored by an art critic, and I don’t give financial advice any more, and I don’t discuss politics.

On my drive to work in San Diego I am starting to see a notable uptick in the number of model 3s. The model X is also rather popular but now I more frequently see model 3s than anything else.

But it is a bit of a head scratcher how in this moment of great need we have a full 180 from large loss to large profit.

I also have seen a few new Model 3s on the streets of Minneapolis and St. Paul. I was surprised that I didn’t see them until this past month or so.

Are you sure they weren’t Saturn sedans that you saw? The front end of the Model 3 looks very much like the Saturn. Also, they both have that one-piece plastic look and the moon wheels.

If I were going to spend $30k on an automobile, I would get something decent looking.

Didn’t TSLA announce a chinese factory deal awhile ago?

https://money.cnn.com/2018/07/10/news/companies/tesla-china-factory/index.html

Did the chinese throw some money TSLAs way for a technology transfer – I mean partnership?

I don’t know, just sayin’

Hi Wolf – love your work!

Call me a paranoid trader, but I’ve survived the markets for nearly 40 years,

20 trading at some of the big houses on Wall St. Seen a lot of manipulation and nothing surprises me. An extreme example was JOHN Delorean doing a coke

deal to keep his new car company alive.

Could some of the investors have gotten together and fictitiously bought cars to

to buy time for the Tesla Ponzi?

Maybe that was why Merlin was so confident that he would be cash flow

positive. The turnaround just seems fake to me. The numbers are too good.

Would love your opinion.

Best,

Phil

Phil,

“Could some of the investors have gotten together and fictitiously bought cars to buy time for the Tesla Ponzi?”

If they actually bought cars with real money, it would be legal. So no problem. If an investment fund wants to buy 1,000 Model 3s and give them away for Christmas, fine, no problem.

But if they engineered some kind of “fictitious” transactions to increase sales, that would be very illegal. If that kind of thing comes out, TSLA would likely collapse Enron-like. And these investors would know this too. So I doubt they would try something like that.

But they’re buying more TSLA shares every time TSLA sells off (and they announce it so we know, it’s part of the hype). And that’s probably all they’re willing to do.

If the accountants, auditors, executives and board are fictitiously running up sales, they are taking a heck of a risk. Enron did this, that is creating fake sales to subs, and their President, CFO and Auditor went to jail. So I’m finding it hard to believe that insiders, whether investors or management want to play footsie with the SEC and DOJ over Related Party Transactions or Conflict of Interest rules, no matter how good the Legal Opinion. Still, a half a billion increase in A/R, means a lot of cars sold. Like many, I am having a hard time swallowing this turn around, which has to be one of the great quarter to quarter swings from loss to profitability of all time. The answer for me, I wouldn’t touch this company with a ten foot pole. They say major market crashes are frequently triggered by a scare, sudden loss of confidence with a major fraud being the source. Could this be the fraud that breaks the market’s back. Time will tell.

Wolf,

I think you have your eyes on the right things here- the accounts receivable and the fact that the claimed cash flow should diminish the need for additional borrowing/equity sales. Like you, that chart would worry me if I were a Tesla shareholder- it is something that is pretty much never seen in a company that is transitioning into a mature money maker from the startup phase. I strongly suspect you will see Tesla go to the markets within the next month or so to raise additional capital.

If I had to make a guess about the accounts receivable, I would wager that Tesla has booked a lot of additional car sales to the people on the waiting list, but haven’t yet actually delivered the cars to those customers. You are right- the cars are sold usually on a cash basis- you get the car when your payment has been received from someone.

I will be watching for Tesla’s expect capital raise- it will have to be brought to the market within 6 weeks if our suspicions are correct.

Both theTesla and Microsoft reports were good yesterday. Amazon will probably report strong results this afternoon. The market is short term over sold. If history is any guide, a Santa rally thru thanksgiving (perhaps beyond) looks quite likely.

We can go back to worrying about global macro, autos, housing, etc. in the new year.

The only thing I can think of is maybe they quietly sold the defective stored units?

If I were on the save-the-company committee, I’d vote for a plan that traded a future initial-quality hit for survival now (i.e.: ship now, use customers to do QC). An alive Tesla with a PR problem to solve is way better than a dead Tesla with no problems.

The people behind Tesla are obviously doing the right thing, get him out of the way, paint the tape. (45 needs these guys) Is there any there, there? Is the EV viable, or will other automakers get there first? A lot of us thought Apple could not maintain dominance in the iphone market. What happened to Blackberry? Polaroid cameras? (instant photos went electronic). It’s a matter of timing, and money and image.

It’s simple – the Model 3 has arrived!

Now TSLA can go into the red again.

Then go green again when Model Y and the pickup arrive!

Each green will be bigger than the last.

The reds between new models might be deeper too – but probably not.

In the end, no matter, TSLA will simply crush the legacy auto industry.

This is a company on a mission. Green spikes are incidental and automatic.

->Then go green again when Model Y and the pickup arrive!

Revenue recognition policies should not reflect projected orders for non-existent products.

It’s thinking like this that keeps me off the short lists of CEO search committees.

I heard that tesla has gotten quite indebted. A new factory in China and now showing a “profit”…..hmm , looks like someone is looking to sell.

adventuresincapitalism.com did an interesting write up on Tesla’s results:

http://adventuresincapitalism.com/2018/10/25/q3-results-secured

AS Wolf and others alluded to: The final test will be the integrity of the Balance Sheet.

Wolf, I’ll wait for your next chapter on the balance sheet. Should be very interesting and telling……….

Associated Press International.

Tesla’s new consultant, Elizabeth Holmes, had no comment when asked about her role in the company’s remarkable third quarter performance.

As Sgt. Shultz would say to Col. Hogan——Jolly Joker!

Thanks, this made me smile.

Just think of Teslas in terms of boxed software sales, which customers have already put a deposit on. Once boxed, you can invoice in full because the sale has been consummated. Then you just extend the same accounting logic into the replication process itself. If it’s on the production line, why not invoice? Voila, you have just stuffed your future sales into the present quarter. Thereby temporarily reducing the COGS of each box to @$25k per copy, showing a profit of $24k per sale.

One common way of juicing gross profit in the manufacturing business in a given quarter is to overstate the value of both raw material inventory on hand and work in process inventory on hand at the end of the quarter. This decreases cost of goods by the amount these two are inflated. This is a very hard one to catch in real time as valuing these two types of inventories is tricky and detailed. Of-course you have to pay the piper eventually and have a quarter with high C.O.G. when you burn your inventory back down to its real value.

‘A magic wand comes to mind.’

A wand like, ‘going private at 420, funding secured.’

Mind the GAAP!

Long time reader in Bellevue, WA. There is a closed Sears that has a big parking lot. I went there yesterday and it is FULL of new, wrapped Teslas, mostly model 3s. I was very very surprised to see all this unsold inventory.

People here are confused because they can’t wrap their head around the idea that Tesla is making a net profit on cars sold.

two words: accounting fraud.

While we don’t have access to the real data for the numbers at Tesla, we do have the SEC data.

The following numbers I think are ok, but people can correct them.

According to the information out from Tesla and other sources, they had Auto sales of $5.8 billion this quarter and $3.1 billion last quarter.

Total deliveries were about 70,000 units in this quarter and 41,000 some last quarter. (Ignore leasing which is a small part of the business.) Cost of auto sales this quarter was $4.4 billion and last quarter was $2.5 billion.

So average revenue per car for this quarter was almost $83,000. Last quarter was $75,600 or so.

Now do those numbers make any sense?

No, as the the increase in sales was mostly a result of Model 3’s which are supposedly priced lower than Tesla’s other cars………….

Let’s look at costs. Auto sales costs this quarter were $4.4 billion and last quarter were $2.5 billion. Average cost per car this quarter was about $63,000 and last quarter was $76,000 or so.

The average increase in cost per car was a little over $63,000 as well.

Well the numbers appear to at least be in the right direction as model 3’s are cheaper cars to produce and there were more cars produced as well.

What about inventories?

To ramp up production Tesla went from an inventory amount of $2.2 billion at the end of 2017 to $3.3 or so at the end of Q2 and Q3.

Are the numbers telling us anything?

Well, I find it interesting that the ramp up to increase production was some $1.1 billion from the end of 2017 to the end of Q2, but no change at all to increase production by 30,000 units or so from Q2 to Q3.

That change either indicates that they had very few if any ‘finished’ cars in that inventory and most was parts and supplies or something is off.

What about deferred revenues?

At the end of Q2 and Q3 ST revenues were about unchanged. LT deferred revenues fell by about $150 million from Q2 to Q3 and about $200 million from the end of 2017.

Obviously, the company is working off some of their LT ‘orders’ and not much changed on ST deferred revenues.

This indicates that the company is filling these types of orders faster than they come in. A slow down in demand perhaps. As production has increased up these deferred revenue accounts will tell us about actual demand – if they fall to much lower levels then it is a clear sign that demand has fallen.

I do wonder how they account for the reversal of the deferred items on the balance sheet though when product orders are filled though.

So what does all that tell us about the Accounts Receivable number jumping by over $500 million from Q2 to Q3?

I haven’t a clue as I have no idea where the numbers could have come from looking at the above data.

However, when I first looked at the Tesla material on the SEC web site I found a $500 million reduction adjustment to “Other operating……” and a $60 million reduction adjustment to “Other…..” on the balance sheet but, no matter how many times I look now, I can’t seem to find them again…………..

These two items would account for the change in Accounts Receivable increase if moved from these two.

What they could be I have no idea and no idea why I can’t find them again.

Sorry, you got one number wrong: car deliveries in Q3 were 56065 model 3 plus 270710 models s/x = 83775, instead of your number 70000.

And that’s the big story this quarter that is that changes everything: they almost doubled sales revenue and became more efficient in production. Huge achievement, simple explanation.

27710, typo sorry

So the numbers can be adjusted, but even when I look at those numbers and the blurb put out by Tesla:

http://ir.tesla.com/news-releases/news-release-details/tesla-q3-2018-vehicle-production-and-deliveries

it makes the other numbers even funnier.

For example, they state that they produced 80,142 vehicles. But when you add the numbers in the release (53,239 +26,903) it only comes out to 79, 548.

Deliveries totaled 83,500 which means that around 4000 or so vehicles were taken out of inventory from somewhere.

Adding to the mystery is another factoid in the release:

“8,048 Model 3 vehicles and 3,776 Model S and X vehicles were in transit to customers at the end of Q3, and will be delivered in early Q4.”

So they produced either 79,142 or 80, 142 vehicles during the quarter, delivered 83,500, and then also had another total of 11,824 in transit.

Where did those 11, 824 cars come from?

At a value of say $65,000 per vehicle that amounts to some $750 million of cars.

If you add the additional cars delivered over production of about 4000 cars at the same value that brings up another $260 million.

Sorry, but no matter how I look at the numbers, something isn’t right and I can’t figure it out.

Take out:

“For example, they state that they produced 80,142 vehicles. But when you add the numbers in the release (53,239 +26,903) it only comes out to 79, 548.”

my mistake.

I find it curious Musk tweeted he was taking Teska private last quarter and now this quarter posts unbelievable numbers.

I would not know where to start to break down Tesla’s earnings report. But I have to give Musk and Co credit for actually making a product, and mostly a domestic product.

In a point where a lot of the hot stocks are still measuring things that reckon back to the 2000 bubble of “eyeballs” or whatever acronym they are putting on it now. Even if they are profitable, companies such as FB, and SNAP, and TWTR…. etc are all just advertising.

At some point, the advertising conduits should be worth a fraction (in whatever metic, P/S – P/E, you would like to apply) of the true product companies that are using them to make actual goods.

Stock is flying, looks like the pros disagree.

Gonna wait for the FBI probe concerning the Tesla production data.

Mike R (above) may have nailed the answer “Accounting Fraud” ?

If you see lots of FBI Tesla vehicles on the road soon, I figure EM made another deal like his SEC one……………

Guess that makes our current Predident the Crybaby-In-Cheif

While the price Tesla stock has been trading at may give the impression Musk may eventually get past his recent problems reality indicates otherwise. Electric Vehicles continue to make up only a small part of auto sales. however, it is estimated that over 100 different electric cars are expected to hit markets by 2025.

The problems before Tesla are about to become overwhelming. Many of these “Tesla crushers” are months away from hitting showrooms.