“People are concerned about all that capital chasing limited opportunities.”

After a decade of “emergency” measures such as QE and zero-interest-rate policy designed to pump up asset prices – now ended – we get this:

“Everyone is worried where things are headed,” explained Matthew Anderson, managing director at Trepp a data firm focused on commercial real estate and commercial mortgage-backed securities (CMBS), speaking with The Wall Street Journal. “The basic complaint is that there’s a surplus of capital and a shortage of product.”

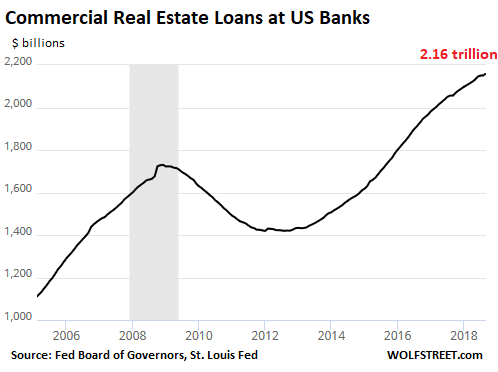

There are about $4.2 trillion in commercial real estate loans outstanding. Regulated banks hold just over half of it: $2.16 trillion, according to the Fed Board of Governors, with a majority of it concentrated at smaller banks (less than $50 billion in assets):

The other $2 trillion in CRE loans are held by non-banks, such as insurance companies, Government Sponsored Enterprises (such as Fanny Mae), and commercial mortgage-backed securities guaranteed by the GSEs.

Boston Fed President Eric Rosengren, who’d been warning about CRE and the risks it poses to the banks since 2016, gave a presentation in March 2017 on CRE’s risk to “financial stability.” His concerns over CRE was one of the factors that turned this dove into a rate-hiker and one of the first proponents of unwinding QE.

Other Fed pronouncements have also fingered repeatedly CRE loans as one of the risks to financial stability.

But since then, CRE loans have further ballooned, and a new force — private equity firms — has muscled into the space, heating up competition and leading to further lowering of loan underwriting standards – as all this capital is chasing product.

Private equity firms are trying to raise large amounts of money from pension systems and endowments, but also other investors, for these “debt funds” that then provide construction loans, bridge loans, and other types of often risky commercial real-estate loans.

There are now 106 funds trying to raise a total of $40 billion, according to the WSJ, citing data firm Preqin. In addition, real-estate debt funds already have $57 billion to invest, a new record.

Last year, CRE loan volume at PE firms jumped by 40% to $60 billion, according to the WSJ, citing Green Street Advisors. This gave those firms a market share of 10% in the CRE loan space, up from near zero in 2014.

And they’re all trying to chase product and deploy this capital they have already raised or are planning to raise. And they’re competing with each other and with everyone else. As result, risky lending has surged.

Back in 2012, interest-only CRE loans accounted for 30% of all CRE loans that were turned into CMBS. Because these loans don’t amortize, they’re considered riskier than regular mortgages. This was down from the peak of 60% before the Financial Crisis. For the first nine months this year, they accounted for 73%.

The waning credit quality, loosening lending standards, and rising interest-only loans that are packaged into CMBS have triggered a warning on Monday from Moody’s, which rates CMBS. While at it, Moody’s threw in a warning about falling collateral values:

- The credit quality of these loans “deteriorated.”

- “Leverage rose.”

- “Exposure to interest-only loans and single-tenant occupancy hit new highs.”

- “Underwritten-implied capitalization rates fell to their lowest average on record.”

- “Rising interest rates leave substantially more room for collateral values of recent vintages to fall than to rise.”

- “Rising rates also coincided with declines in debt service coverage ratios for the fourth quarter in a row.”

The latest numbers are “concerning to me,” Ricky Cipko, a Morningstar assistant vice president, told the WSJ. Now that the commercial property market is slowing, there are concerns borrowers may not be able to repay those loans.

“We’re seeing a lot more loans with cash flow that has crept down,” Steve Jellinek, a Morningstar vice president, told the WSJ.

Morningstar Credit Ratings had $25.4 billion of CMBS on its “watchlist” of securities that might face problems, up nearly 50% from the post-crisis low.

But it may get tougher for PE firms to raise the funds they aspire to raise. Treasury securities with maturities of seven years or longer now offer yields of over 3%, with near-zero credit risk. High-grade corporate bonds offer higher yields with relatively low risks, such as Apple’s 3.45% notes due in May 2024, which currently trade at a yield of 3.6%, according to Finra.

The record low cap rates in commercial real estate – the implied market cap rates used for underwritten property values fell to a record low of 5.87% in Q2, according to Moody’s – just aren’t that appealing anymore, given the big risks involved and the available alternatives.

So interest in real-estate debt funds “has plummeted,” with just 6% of investors in June saying the strategy “presented the best opportunities” over the next 12 months, down from 26% a year earlier, according to a Preqin survey released this month and cited by the WSJ.

“People are concerned about all that capital chasing limited opportunities,” Tom Carr, Preqin’s head of real estate, told the WSJ.

When investors stop chasing CRE deals at record low cap rates, and when pension systems stop plowing money into risky loan funds for very little return, it would mark a milestone in what the Fed calls a tightening of financial conditions, which is precisely what it wants to accomplish with its rate hikes and its QE unwind. So far, it has had only very limited success. But now it seems, the Fed’s medicine is ever so gradually starting to work.

High-end apartments is where the money is, on paper. But it’s not where the market is. Read… “High End” Apartment Construction Totally Dominates, Creates Mismatch of Supply & Demand

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Has there ever been a time in history when a speculative mania has been “gradually” brought to a soft landing? (CRE or otherwise?)

Has Moody’s ever provided a ratings downgrade for a trillion-dollar sector before it was too late for the bagholders to exit?

Is credit really “capital” just because a financier calls it that?

Does the Federal Reserve still honestly think that they’ve gone from policy “accommodation” to neutrality?

No.

History teaches us that we learn nothing from history.

Financiers are particularly impervious to experience.

I don’t think financiers are impervious to experience. I think they have learned from history. They’ve learned that when they blow bubbles, they come out the winners.

History teaches us we should fear financiers proportionately more than armed robbers and arsonists, and for the same reasons.

They don’t sell Jamie Dimon masks at Halloween party stores because it’s supposed to be fun, not genuinely terrifying. Lloyd Blankfiend brand chainsaws would be in bad taste.

Besides the rhetorical questions, I have some opinion on this:

> Does the Federal Reserve still honestly think that they’ve gone from policy “accommodation” to neutrality?

Does anyone else think that the economists at fed are just erds playing simcity with the whole world? They seem to not realize what inflation of assets mean in the first place.

It’s like the old saying, “How did you go bankrupt? Two ways. Gradually, then suddenly.”

For all of their models and supposed market stabilizing policies, the Fed is essentially a cabal of Wall Street tools, a glorious PR machine. Boom, bubble, bust. Rinse, repeat. And who benefits? It certainly isn’t main street. This is a feature, not a bug.

Wolf – Similar situation in Canada.

The commercial real estate sector is in dire straights.

Downtown Calgary high rise towers have high vacancy rates.

Commercial retail space is like wise suffering high vacancy rates.

See the link below for the New Horizon Mall (ghost mall)

http://www.youtube.com/watch?v=ZJ1wbDJkn58

Now the Bank of Canada is raising rates again. Look out below!

Some of the excess money needs to be drained out of the system by the U.S. govt issuing 5% bonds just for U.S. based pension plans. This will not only protect U.S. pension plans but also cause a gradual decrease in asset prices and keep the bubble from (hopefully) bursting.

Pension fund benefits are bloated, I agree that government would like to put a floor under these funds, they have obligations, they also run the pension guaranty fund, and the Feds do not want to see the state general funds raided to pay benefits. Still there is a lot of political blowback, the healthy funds are in blue states mostly. I also agree that reallocating from stocks to bonds will keep new issues and government spending at a comfortable level. POTUS thinks rates are too high, the gop Congress is angry angry angry.

I heard there are so many empty storefronts in New York City they are considering a bill to institute commercial rent control. The landlords are forcing small business owners out, then keeping the stores empty. The bill will guarantee owners lease renewals at reasonable rates and institute an arbitration board to mediate.

Rent control is coming everywhere.

->Rent control is coming everywhere.

And will be ruled unconstitutional, if not prohibited by decree. Huis clos. Sorry.

Rent control has been in America since WWII when all prices were frozen during the war.

That was when the US was electing Democrats and at war with the Reich, instead of the other way around.

Taxes are for little people, not for empty buildings, in deference to NYC real estate tycoons. Hey, I don’t make the rules.

Rent control has been in America since the Federal Reserve was created to set the rent on borrowed money.

/FIFY

[say it ain’t SO: Petunia and Unamused…TOGETHER AT LAST! on one thread!… be still my beating heart!!!!]

—

“That was when the US was electing Democrats and at war with the Reich, instead of the other way around.”

and man that line was SO good hairline cracks appeared in my skull and i had to repeat it in my mind like melting chocolate on the roof of my MOUTH….

The big Rent Control kaboom will be when market on vacancy is ended. Talk to anybody from the old days regarding WeHo (West Hollywood) and Santa Monica.

One issue that is rarely discussed.

Each successive cycle has gotten more and more corrupt in terms of lending and banks wishing to “retain relationships” with borrowers, mortgage brokers, whales, etc. Market Values are based on market indicators with a deduct for under-market rents. You get say 10% too aggressive lease rates, a too skinny vacancy/collection loss allowance, squeezed expenses and a too skinny Cap Rate (OAR) and the “real” LTV is way above the stated 70%. Looking back over 30+ years, even if the appraisal was say 10% too high, there was a greater probability of problems. The system evolves and works, but not when the people in involved are unethical and driven by bonuses, production and retaining their seats at the table. There are lots of peeps in CRE that have never seen a bear market and certainly never seen a “no bid” market such as RTC/S&L Crisis c. 1990-1994. The newbies don’t know what they don’t know, which will be costly – atypically low OARs (Cap Rates) magnify the results.

Don’t need rent control, just need to tax empty buildings.

I heard Paris wants to raise the new vacancy tax to 60% because there are still too many vacant apts. Other cities around the world are now either doing it too or considering it.

Whoa… i was wondering about that. People in NY say SF was “smart” regarding commercial real estate not being allowed to lie fallow, but that’s not true: just on one corner, i think 21st/Folsom, had thriving businesses until the rents were jacked up enormously for the successful restaurant that had lines and the thriving flower shop– now leaving the entire corner empty, dead and for lease.

These REITs are brutal all around.

I’ve heard this thing so many times it stopped being funny.

When a town, or even a city, sees empty storefronts “greedy landlords” are always blamed for them. It’s a good story: local politicians and newspapers love a simple story where they can blame those money-grabbing capitalists driving little Mom and Pop types out of business. People love it as well, as it’s a classic case of “the government must do something about it” and blaming monocle-wearing cigar-smoking financiers.

And like always we should mistrust such simple stories.

Greedy landlords don’t last long for the simple reason an empty store generates zero income and a lot of expenses. Just think about taxes. And nobody wants to rent an office coated in cobwebs and with flaking paint. Unless he plans to convert it in a meth lap, of course.

Sure, you can keep some new supply off the market to manipulate prices, but how long can you keep it up? It’s a short-term game that can only be fueled by desperate investors who now have alternatives and who will cash out at the first whiff of troubles.

Retail is an absolutely brutal game, especially when the competition increases the way it’s doing: most of the world is seriously overmalled (just go to Manila, Jakarta or Kuala Lumpur) and Ali Baba, Amazon, Etsy, eBay etc are everywhere these days. Want a new Huawei smartphone? A genuine Louis Vuitton handbag? Just need some new socks? There are literally hundreds of sellers ready to take your business.

The only reason casualties aren’t piling even higher is debt is cheap to service these days, but that’s about to end, if it’s not already over.

Rent control is not solving anything, but that never stops politicians and their voters from trying.

“Politics is the art of looking for problems, whether they exist or not, diagnosing them incorrectly and applying the wrong remedy”

-Groucho Marx-

That’s the kind of Marxism I can embrace. :-D

->When a town, or even a city, sees empty storefronts “greedy landlords” are always blamed for them.

Because we do know that it does happen.

But not all of them. Sometimes those store fronts are empty because they lost their customers when their jobs were offshored, which is something you could blame on greedy industrialists, not greedy landlords.

->Greedy landlords don’t last long for the simple reason an empty store generates zero income and a lot of expenses.

The trick is to gouge tenants short of putting them under. Some Chicago and NYC slum lords have been in business for generations. Sometimes they go too far, and then their victims have to bail them out.

-> Just think about taxes.

CRE tax breaks and grants for redevelopment that never happens ha been a common problem across the Rust Belt.

->Sure, you can keep some new supply off the market to manipulate prices, but how long can you keep it up?

Let’s not avoid including existing supply, okay? CoreLogic says five million homes were foreclosed by 2015 after the 2008 RE bust, and many of those have been strategically kept off the market to support prices. Blackrock has been manipulating supply in southern CA and elsewhere for years. It’s been a very profitable business model. It’s why they do it.

->Rent control is not solving anything, but that never stops politicians and their voters from trying.

It holds off rentiers determined to gouge tenants. Tenants vote for officials to protect them from predators, and you haven’t been able to buy them all off yet.

->And they’re all trying to chase product and deploy this capital they have already raised or are planning to raise. And they’re competing with each other and with everyone else. As result, risky lending has surged.

And since they can’t make performing loans, they will make non-performing loans. In other words, they can’t have it all because they have no place to put it.

They could just put the money into the stock market. People constantly call to assure me that stocks always goes up, and email me charts going back ten years which prove it. But I’m more than ten years old.

I tell them that if they’re really desperate they could invest the money in projects to save the world, but they complain the ROI is too low and they want to make the big bucks. So I guess they’ll put it into non-performing loans, since that’s where the real money is at.

These people have more money than they know what to do with. Have you noticed they always end up wasting it and still crave more, as much as they can get? A rehab specialist would prescribe income taxes, substance abuse treatment, and training to acquire useful life skills.

“The credit quality of these loans “deteriorated.””

question on deteriorating CRE loans:

Is there simply too much CRE out there, are the commercial ventures are starting to decline in a slowing economy, are rising interest rates affecting the ability to operate a business, or all of the above? Is it just that there is too much empty product or is it that business is declining? In short, have builders chased a falling market or just overbuilt?

There sure has been a lot of ‘the economy is great’ hype this past decade.

I’m over my limit, but you deserve an answer. Finance is too important to leave to Larry Summers.

Briefly, in answer to question 1, all of the above. Question 2, both. Question 3, both. More or less. It’s complicated.

Forgive me if I seem condescending, but I make mistakes too. I perceive you yourself are not a professional finance guy. Otherwise you would not be asking these questions. This article, along with other articles, do answer your questions, and the nature of your questions suggests you understand the answers better than you may think.

Give yourself some credit. So to speak.

Also give WR credit for being a pretty good explainer for the non-professional.

I’m not really a finance guy either. I’m an historian. If I can figure it out, so can just about everybody else, at least enough to keep themselves from being easy pickings for the sharks. Most articles on this site show that even finance guys have trouble with finance, as big as it gets. Really, if they’re so smart, why do the rest of us always have to bail them out when their boneheaded scheming goes pear-shaped? It’s not just stupidity. It’s malice. There’s a lot of them out there, and they run the show.

I’ll get off my soapbox now.

– Question: How is this commercial real estate financed ? With short term rates ? with 5 year rates ? or say 10 year rates ? That would give me a better understanding what rising rate (e.g. 10 year rate) pricks this bubble

JM –

It is not as much the financing although a concern. It is about the valuations. Construction loans are based on short term but permanent financing is generally 10 year fixed loans which takes the risk out of it.

If you consider the 10 year Treasury to be the base line of risk. As it goes up, then investors are willing to pay less for commercial real estate assets. For Example:

McDonald’s trade at approximately 4% Cap rate or 4% unleveraged return on investment. Therefore, a McDonald’s with $100,000 in rent is worth $2.5M but if the treasury goes up to 4%, no one will buy at the same return.

Now that McDonald’s with $100,000 in rent will trade around 5% Cap rate and worth around $2M for the exact same investment.

The scary part as a developer is that from the time that you find a property, build it and the tenant is paying rent takes about 18 months

Hope that helps, David

David as you are aware, financing and values are related. Using your example, a 70% loan on $2.5MM is $1.75MM; the LTV after a decline to value of $2MM is 87.5%. But say you hit a recession and due to lower lease rates and higher vacancy, the NOI is reduced to $80,000; at a 5% cap rate, the value is $1.6MM and the equity has gone poof! and the bank is underwater.

I’ll tie this back to my prior post – say the value NOI was never $100,000; say it was $90,000 and the $100k NOI was inflated by the appraiser – the value at 4% was $2.25MM, so you started out at 90% LTV on real numbers. That is the point I was trying to make in the prior post… Problems are already baked in the cake, and the impact from a recession, higher yield requirements, higher financing costs, etc., will be worse than they should be. You take the $90,000 to $70,000 NOI and the value is $1.4MM or 20% below the $1.75MM loan amount… and worse, this type of cycle is self-reinforcing because higher risk requires higher yields which means high cap rates. Plus, when values are declining potential buyers shoot lower to pad their potential price. There are old broker on this site – ask them what happens in a “no bid” market.

That’s why all the foreclosed homes were blown out to Blackrock – had they hit the market offered for sale rather than being rented out, the housing market would have tanked further and increased the number of NPLs on the already BK banks’ balance sheets. The higher values allowed homemoaners to refi as rates were lowered.

Many, many participants have only seen investing as a 1-way street.

– So, it’s the 10 year yield that matters for commercial real estate. OK, thanks.

Many of these notes have a balloon payment at the end.

Shouldn’t you invest in stuff there’s going to be less of? And so long as we have Qt, isn’t that the $? Doesn’t QT mean deflation? Or have I got it all wrong?

“I heard there are so many empty storefronts in New York City they are considering a bill to institute commercial rent control. The landlords are forcing small business owners out, then keeping the stores empty”

Could someone explain to me the point for a landlord of doing that? In my otherwise well off residential area (in Paris), a couple of small shops have been sitting empty for months on end, probably because rents were too high relative to the foot traffic and business potential.

I mean unless you are super filthy rich, you generally want to have a return on your assets, at least to cover the costs. Capital appreciation potential at this point of the cycle is minimal to say the least, so really, what is the point? Honest question.

There isn’t. Greedy landlords never last long. If stores stay empty is because it’s not profitable to have a commercial activity there for a myriad reasons ranging from a saturated market (just how many mattress stores do we need?) to dwindling foot traffic. High rents don’t remain high for long if months pass by without a tenant.

It’s a completely different market from residential real estate in countries like Spain, where owners will cling to fanciful valuations like a mussel to a rock no matter how much money it costs them.

It’s possible that when there’s a lot of new supply coming into the market owners will keep part of that new supply off the market for a while to artificially inflate prices, but it’s always a short-term gamble that rarely pays off. In fact these days lenders may force the developers/owners to put all units up for rent right away, even if this means giving big incentives such as one month free rent.

But a lot of people are very much convinced it’s never the “small” guy’s fault and there’s some Wall Street-type financier (possibly wearing a monocle and smoking a big cigar) behind every economic/financial trouble and if those financiers are “removed” we’ll go back to some mythical Golden Age. Mais où sont les neiges d’antan…

Down here(EM) in perpetual GFC. One month free has been the norm this decade. Rent prices drop significantly with every new tenant. No rent increases since 09.

Empty retail space to the horizon(dense urban). Locations without tenants for years. Astronomical property taxes.

I told the company owner what I read here about cities raising taxes on empty CRE to promote lower prices. He said when a commercial activity chokes it’s time to migrate to something else.

Consider for the moment that in the coming years, few will actually go out to shop for anything. It will all come from online sources.

That said, local economies can only support so many bars, restaurants, yoga studios, and gyms. With every big new development incorporating street level commercial, and an ever increasing inventory, sooner or later the market will have to adjust to reality.

That reality is that fact that opportunities for long term viability in retail are rapidly evaporating. Regardless of the location, ground level retail is of rapidly diminishing value. Worse, no one wants to live on the ground floor.

The entire economy in this area needs a serious rethink.

Hard to get the gist here, money is pouring into CRE from all sides, what’s not to like?

Check toward the bottom when it talks about the difficulties of raising funds going forward.

I replied a few weeks ago, but wondered how much these ‘new’ financing vehicles are wrapped in pension fund REITS , Dark Pool, Anonymous hedge funds? Sold as seemingly stable bundles, but largely unknown risk assets?

Anecdotal observations here on the Gulf Coast is we saw a flurry of TX , Ca. plates, Many huge 10 million plus new mixed use shops & living above places being developed and prices rising , now tons of ‘for sale’ signs and none selling the last few months. Changes are palpable, and just wondering how this next unraveling turns out…

The landlords in NYC are only part of the problem. I live and run a successful small business in Manhattan. My landlord is a professional re operator, had a vacancy rate close to zero. Start looking at the $15.00 minimum wage, pass along re tax increases and a greedy city writing $150.00 summonses for a gum gum wrapper on your sidewalk. There is where you will find a big part of the answer to the vacancy issue.

Retailers are closing stores all across America and the impact will be huge. Online retailer Amazon is by far the chief offender causing such grief. Over the last few years, stores such as Target and Macy’s have even had to face a slew of dishonest shoppers trying to sneak defectives products purchased online back as exchanges and trading them for a fresh unbroken product. I have seen this costly abuse recommended by several online shoppers that see this as an “easy fix” while simply brushing aside the ethical issues it creates.

As stores close much of this space located in the large shopping malls that once flourished in commercial zones of suburbia will grow empty and abandoned.

B Wilds,

FYI: When you try to promote your own blog in a comment and link it, I delete the link and the promo. But when you comment, you can put your blog’s URL in the box that says “Website.” This will highlight your name in blue and link your blog under your name so that when people click on your name, they’re taken to your blog. You can use this feature with every comment you make.