Red indicates the moves since the inflection point in June.

“Having a legal cannabis grower near your property has a significant negative effect on value due to the odors,” explained Thomas Stone, a real estate broker in Sonoma County, California. “This is the first legal harvest in the County, and while better than having a pig farm next door, an acre of flowering cannabis can be pretty overwhelming. You don’t want to show those properties on a warm afternoon.”

Just another wrinkle in the shifting landscape of the housing market in Sonoma County, an expensive San Francisco Bay Area market between the Pacific and Napa County – wine country interspersed with beautiful cities and towns.

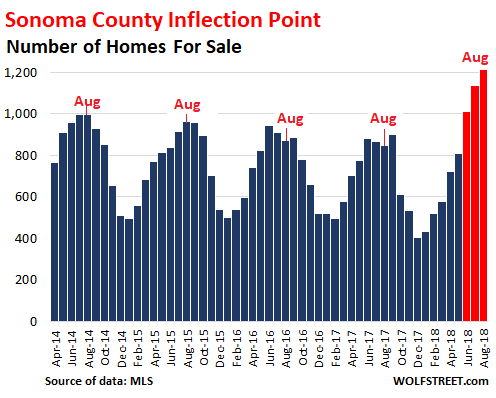

A month ago, Thomas Stone and I stuck our necks out and said that the inflection point in the housing market in the county had appeared in June. Housing markets deteriorate beneath the epidermis first, before the deterioration becomes visible in median prices. So here is an update of our anatomy of this housing market, based on August data.

In June and July 2018, supply of homes listed for sale in the county had suddenly jumped to the highest level in years. And in August, supply rose further to 1,216 homes (red indicates the moves since the inflection point in June):

“Inventory continues to grow at a time of year when it usually slows,” Stone said.

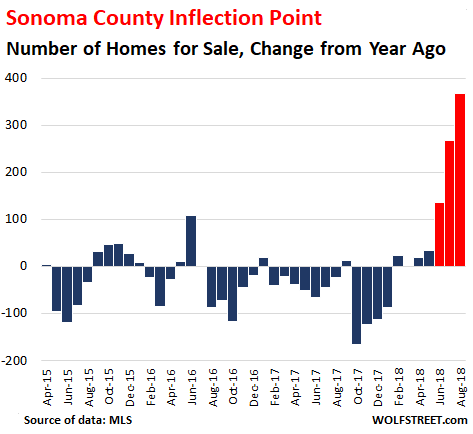

This surge in inventories – a first sign of the inflection point – becomes even more obvious when compared to the same month a year earlier. In prior years, supply tightened, with inventories on a downward trend year-over-year. But over the past three months, that has drastically changed. In August, there were 367 more homes listed for sale, up 43% from a year ago (red indicates the moves since the inflection point in June):

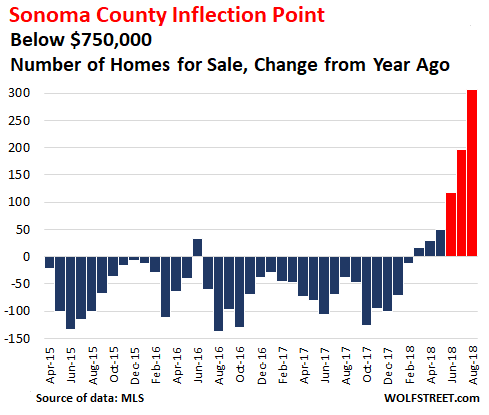

Most of the surge in supply happened at the bread-and-butter end of this market, with homes that are listed below $750,000, which covers 66% of the homes sold. And here, the supply surged by 84% (by 306 homes) year-over-year (red indicates the moves since the inflection point in June):

But even as supply surged, total home sales dropped 17% in August, compared to August last year, to 483 homes, the slowest August in the data going back through 2014.

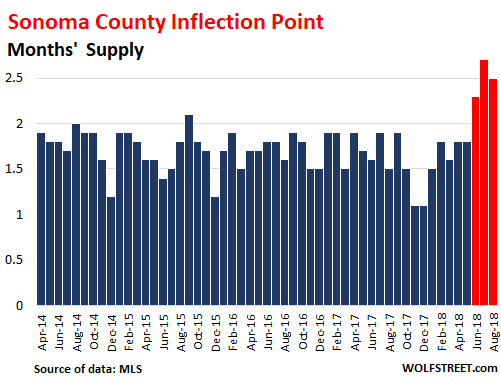

Months’ supply of all homes for sale – the number of homes for sale divided by the number of homes that actually sold – has been mostly between 1.5 months and 1.8 months. But since June, it jumped. In August, it was 2.5 months (red indicates the moves since the inflection point in June):

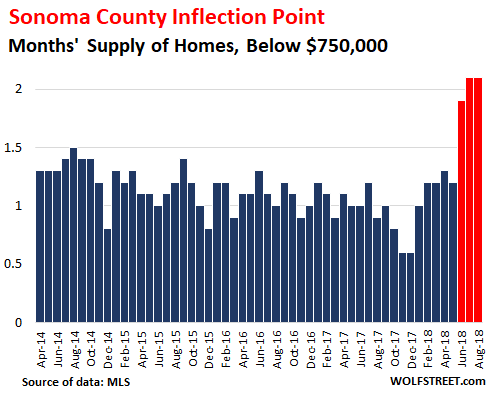

In the bread-and-butter tier of homes listed below $750K, the surge in months’ supply was even more striking, having jumped from a tight supply between 0.6 months and 1.3 months in recent years to 2.1 months, about double the prior midpoint (red indicates the moves since the inflection point in June):

In the mid-tier of prices ($750,000 to $1.3 million), supply reached 3 months. And at the top tier (above $1.3 million), supply jumped to 7.9 months. But in both these lofty price tiers, months’ supply had been higher during the slow months in the winter a few years ago. In the bread-and-butter tier, however, months’ supply shot past all recent high points.

When there is no sale, brokers don’t get paid. When sellers are asking for more money than buyers are willing to pay, sales volume falls off – until sellers start lowering their prices. It is the brokers’ job to convey a sense of reality to their clients – the sellers – to make deals happen. It’s not an easy job, after years of surging prices, which sellers are now taking for granted.

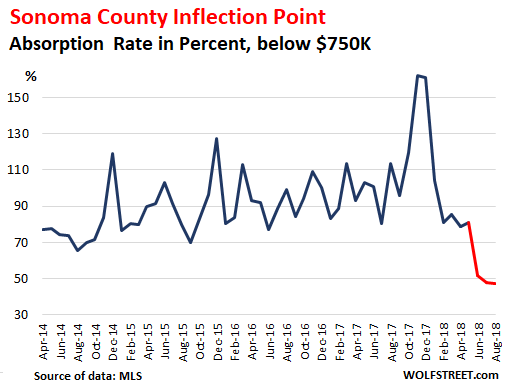

The chart below shows the “Absorption Rate” (the number of sales divided by the number of homes for sale) for homes below $750,000. It shows the percentage of the supply that has been “absorbed” by buyers. The spike in the absorption rate late last year, including in November to 162%, was largely due to the fires – the most destructive on record in California. At the time, buyers grabbed every home for sale. By February absorption had dropped back to 81% and continued to drop. In August, it was down to 47.2%, the lowest in years (red indicates the moves since the inflection point in June):

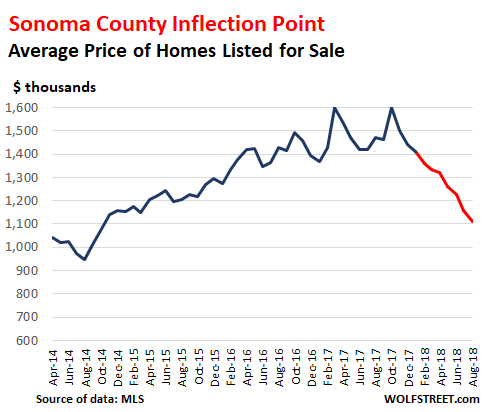

Average price of all homes listed for sale dropped to $1.11 million in August, the lowest since October 2014, down 25% from a year ago. This “average active price” (sum of all asking prices divided by the number of all homes for sale) can be skewed by a small number of very pricy homes. And it is a lot higher than the “median” price of homes that actually sold (more in a moment). Nevertheless, this is a big and consistent move (red indicates the moves since the inflection point in June) :

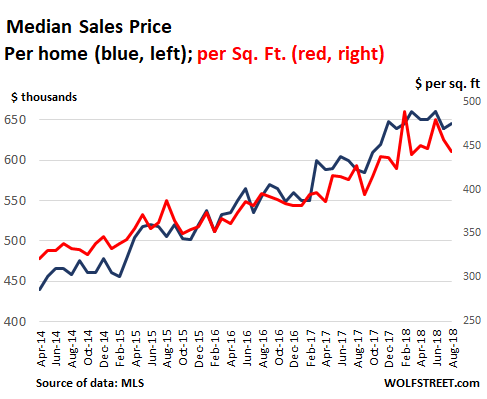

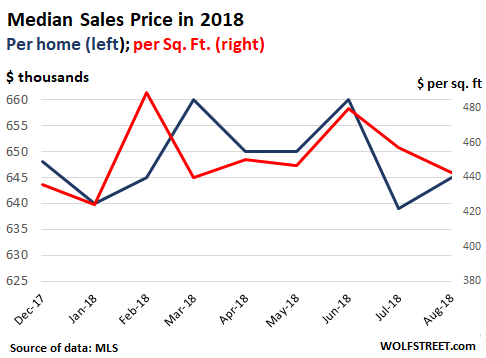

This and similar metrics are visible beneath the epidermis of the housing market. On the surface are the prices at which homes actually sold. The “median sold price” – which means 50% of the homes sold for more, and 50% sold for less – in August, at $645,000, was the second lowest for the year. But it was still up 9.6% from August last year. A slightly different measure, the median selling price per square foot dropped to $443, up 3.7% year over year:

Prices in the county had surged in late 2017, largely due to the fires. This impacts the year-over-year comparisons at the moment. But in 2018, the weakness in prices is becoming apparent, with August prices being at the low end of the range so far this year, as sellers and buyers are trying to figure out how to make the next step in this dance:

“Prices are dropping slowly,” said Stone, who has to deal with this phenomenon every day. The median price is one of the last metrics to change direction because there is a lot of resistance from sellers who are not yet in a rush to sell. Yet the median price, and other price measures such as the Case-Shiller index, which lags even further behind, are our primary housing market indicators outside the profession.

And based on the Case-Shiller index, New York condo prices fell again. Historic spikes slow in Seattle and other metros. Read… The Most Splendid Housing Bubbles in America

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Excellent article.

Possible issue with last 2 figures – they are identical at the moment. Intent was to put in a different final graph?

Also, surprised Months’ Supply is still so low… I thought under 3 months supply is normally considered a tight market, historically at least? Prices don’t normally drop (much) with supply still that tight…

Yes, you beat me to it. You must have read the article within seconds of publication because a few minutes after publication, I saw it and fixed it :-]

The correct chart is now in place.

They’re still identical.

Similar, not identical.

The first of the two charts is for ALL homes listed for sale (Aug = 367)

The second of the two charts is for homes listed for sale under $750K. (Aug = 306).

It shows that most (83%) of the homes for sale are in that “below $750K” category. Over the past 12 months, 66% of the homes sold were in that category.

I mean the very last two charts. I do not see a difference. They even have identical titles.

Oops. Thanks. Fixed.

Months of supply can be misleading, particularly when that metric has been depressed by a sea of central bank liquidity searching for yield. Many markets across the U.S. have been extremely distorted because market interventions favored existing asset holders over traditional first-time buyers and owner occupants.

Investors have been buying up every affordable home in sight to either flip or join the landlord boom. As a result, prices are well above historical norms. Inflection points can be subtle at first, and prices often take a while to correct. That doesn’t mean the inflection points are not readily visible. Sonoma County is just one example of many. I was running stats here in the DFW area yesterday, and even in our relatively affordable locale, we’re seeing cities with inventory increases of over 40 percent from last year, while sales are stagnating.

This is a testament to just how intertwined the Fed has become in the U.S. housing market. Instead of reforming the system and allowing true price discovery with the Great Recession, they made a Devils bargain to recapitalize the wealthy and well-connected at the expense of the broader public. Best govt (and housing policy) money can buy. :)

https://aaronlayman.com/2018/09/denton-county-home-sales-slide-7-in-august/

Nice recap, do you think that the exposure of speculators and carpetbagger landlords represents a threat to the mortgage system? I follow analysts who believe the mortgage system is not going to be a catalyst in a crisis (and that banks are rock solid)

I think you will see that biggest increase is in the 500,000-plus price bucket.

There’s really no change in the under 200,000.

There are not enough jobs in the DFW area to support all the 500,000 houses.

“It is the brokers’ job to convey a sense of reality to their clients – the sellers – to make deals happen. It’s not an easy job, after years of surging prices, which sellers are now taking for granted.”

The brokers have a vested interest in accelerating the sale, obviously. The actual buyers and sellers have an opposite interest: to get the best price possible even if the deal takes months to close. At the end of the day, the agents make sales happen by conniving behind the scenes and applying pressure to the buyer and seller to adjust their expectations.

Not surprisingly, brokers love people who have to buy/sell and become demotivated by buyers/sellers who aren’t in a hurry. Which means that RE prices are driven by the margins. Then the margins drag the center up or down after a lag.

Good comment. However, despite the accuracy of the rear-view mirror charts I would value more the honest assesment (gut feeling/opinion) of an experienced local realtor. I’m not sure how an outsider and potential buyer always gets that information, but I am sure a couple of brews between friends would be a first start….kind of like a WS post. :-)

Seriously, I have bought and sold two properties without an agent and two using an agent. I did not do any worse using an agent in either example. In fact, the commision was priced into the asking price and the agent had the experience to hold out and reject first offers when I might have been inclined to accept them. They know the local market. They know buyers and people. This article is very interesting and the charts verify. However, they are lagging behind what a good realtor already knows and may not be so helpful for active buyers and sellers.

Another point. I am sitting in a house right now that I own solely because a realtor called me up two years after my initial search for riverfront ended in a 2nd place offer. She filed my name away and one day called me up and asked if I was still interested in buying? After looking at a few unsuitable properties she remarked that a rumour was circulating a particular place might come on the market in the next 6 months. We had a look and began negotiating. Our offer was accepted before the place was even put on the market. After we moved in no end of peope came to visit and asked how we had come to buy the place? (It is, in my opinion, the best piece of riverfront in the valley, bar none). We were oh so lucky to have met that realtor and it helped that I knew her father from old logging/flying days. It also changed our life 100% for the better and every so often I contact her and let her know it (with renovation pics). Cynical people will be quick to call this event a scam, but over the years I became good friends with the sellers family and found out ‘his story’. The price at the time was fair, and selling his place allowed him to move away and start over. It was a win win.

My point, it pays off to work with a knowledgeable and honest realtor. They are not always the ‘top producer’ or recognized hot shot. Laymen 2nd guessing the Market is akin to researching health symptoms and telling your GP what needs doing. Just my opinion and experience. regards.

One more thing…our purchase ended up being at the bottom of the cycle. Sure, I renovated because I am a carpenter. However, in the last 15 years it has appreciated 500%, and this is in a realtively depressed rural market. It wasn’t a scam because no one actually has a crystal ball beyond indicators that everyone else is privvy to.

When we sold the place in town to move here full time my friends used to hum the theme from ‘Deliverance’ whenever I walked into the pub to see them. I haven’t heard that one for the last 10 years. In fact, I’m meeting them for lunch in two hours and the only thing they’ll ask is, “How’s the fishing”?

Just wanted to say I do appreciate the personal stories you post in the comments. Thanks for taking the time to write them. (BTW, I’m contemplating a similar lifestyle change for myself.)

Surely all market prices are set at the margin? We work out the value of all a company’s shares in existence by multiplying them by the last sale price.

Indeed – and the highest bid wins, so prices are set by the most optimistic market participants.

You could do a whole twenty minutes stand up sketch with this material. And the fact is real makes it better.

Much better that my crayon drawing of a gun coming out a computer monitor with the caption “Don’t worry, real cybercrimes rarely use guns”.

With realtor tricks such as delisting and relisting homes that do not sell surely months on hand statistics are useless.

They’re very useful as an indication of trend. But they’re not a numerically accurate description of how long it takes to sell a home. If the number is twice as high, it means that it takes a heck of a lot longer to sell the home than before. That part is very reliable :-]

“In the bread-and-butter tier of homes listed below $750K”

That really is a laugh out loud line of text for me……what does “bread and butter” mean? Certainly not affordable at $750K

RE prices have completely disconnected from the incomes of the underlying economy IMHO…….well at least my measly income.

Agree and thought to share this reality affecting Baby Boomers who sold their homes to Downsize…https://www.cnbc.com/2018/09/11/baby-boomers-are-struggling-to-downsize–and-it-could-create-the-next-housing-crisis.html

Yes this is funny in a state with more normal homes prices. In Californias major cities, under $750k is in the range of being “affordable” by most dual income families making a median wage. Somewhere around $60-$70k a year. I put affordable in quotes because most frugal people would not find a $700k home affordable on a $120k salary, but it is pretty normal here.

Keep in mind our property taxes are around 1% pretty much everywhere. And home insurance is cheap. Though companies are harshly reevaluating fire zones so they are getting worse.

Prop 13 really screwed the current generation by freezing property taxes, and then we all complain that the schools are underfunded.

Not to make a tangent in the discussion, but I read that only 13% of homeowners have earthquake insurance. As a renter who is looking to buy a home, I am not an expert by any means, but when one of these faults goes (not even the Big One, but more like Loma Prieta) and tangible damage occurs, what happens?

I have heard everything from “it doesn’t cover much and its expensive” to “I would probably hope a gas line bursts so I can torch my home and have it covered under a homeowners policy”.

I just find it amazing that the biggest risk (literally a fault under your most significant asset) is only addressed by a minority of homeowners. What is the order of payment for damages? If the average home here is $1.25MM (in SF), I cant imagine people have a healthy “rainy day earthquake repair” pile of cash sitting around.

California is one of only 12 “non-recourse” states. Which means the mortgage lender can only go after the collateral (the home) in case of default. If the Big One destroys an uninsured home or the insurance company itself, the homeowner can do the math whether it’s better to walk away from the loan and the property and let the bank take the loss, or whether there is enough equity in the home to try to work something out.

This is a crucial consideration and calculation for homeowners in non-recourse states after a disaster like an earthquake or a hurricane.

Here is my article on recourse v. non-recourse mortgages:

https://wolfstreet.com/2018/06/20/us-style-housing-bust-mortgage-crisis-in-canada-australia-recourse-non-recourse/

I own my house free and clear so Earthquake insurance is required. For 600K and 80K deductible I am spending around $2400. I am going to increase both my fire insurance level and Earthquake given the higher building cost today due to all the fires in Calif. Before I could use $250 a sq ft but now I am going to $400.00 due to labor shortages and wood prices from Canada that have increased due to Trump tariffs.

The California Earthquake Authority policy IS overly expensive and does NOT cover much. High deductible and low benefit above the deductible. Doesn’t cover vehicles, landscaping, fences etc. Note also that the CEA policy doesn’t cover fire damage, since that’s already covered by a regular homeowner’s policy even when an earthquake triggers the fire.

If you live right atop a fault line that is overdue for a big one, it probably makes sense. If you live on stable ground many miles from a fault line, it probably doesn’t. Especially if you have the option to walk away thanks to a non-recourse loan. (Note that California expanded the eligibility for non-recourse status so that it now includes many refinance situations as well!)

GSW: “Prop 13 really screwed the current generation by freezing property taxes, and then we all complain that the schools are underfunded.”

Prop 13 didn’t freeze property taxes. It merely put a limit on how fast property taxes can be raised while a house is owned. The property taxes are re-evaluated when ownership changes hands. This was designed to prevent people from being kicked out of their houses merely because the tech industry has bid the price up.

I used to live in Sonoma County. It is expensive.

$750k is a somewhat-above-average house.

It is very rough on the first-time buyers, but that’s not

who are driving the market.

There was an article in the Seattle Times last week saying prices dropped $70k over the last three months in Seattle. It looks like inflection points are not limited to Sanoma CA. That drop in Seattle was over 5%.

I saw that too. I’m not disputing the numbers but I haven’t seen the same thing (yet) on Eastside. We have been watching the Eastside market closely and going to a ton of open houses. Many asking price drops, much less foot traffic than a year ago, and houses are sitting a month now, instead of a week. However, the overall impression is that many buyers are still jumping in quickly because of their glee at having a bit of choice. Next Spring should be fascinating.

I am seeing prices coming down on the Eastside (with the exception of West Bellevue) at all price points.

My best guess based on looking at daily zillow data is that if someone bought a SFH on the King County Eastside last september – and tried to sell it today they would do well to just about break even – after one factors in the 8% closing costs.

I’m am seeing some anecdotal evidence that potential buyers are now walking away from the market to wait it out. I know two couples that had a fear of missing out six months ago, but now they have fear of being a bagholder. It’s a lot more tolerable to rent when you see home prices coming down.

Over the past year, my wife was putting tons of pressure on me to buy a million dollar home or more, saying things like – “the prices are what they are” and “that’s what you have to pay”, as if the prices were set in stone and couldn’t change year over year. Now that I’ve pointed out the change in trend, she’s been excited enough to follow the status of aspirational homes that she thinks are going to drop 30% or more next year.

The point is that market mentality reverses at inflection points like this. Once the negative data starts coming in, suddenly everyone expects things to drop. They turn like a group of sardines that sees the whale coming. The slow turning ones get gulped up.

Could be too that sellers are sensing the top of the market and listing their homes in an attempt to cash out before the bust? I just listed one of my rentals in SoCal for this very reason.

That sounds plausible to me.

Here in Texas, real estate prices are still going up. Up 6.7% in the last year and they are expecting a further rise this next year. Prices have really appreciated since ~ 2013.

It’s almost as if a massive fire destroyed the community. Know your data. Even if you are excluding the 690 burned out lots under $750k (are you?) on Redfin there are tons of homes standing in annihilates communities. I’m not arguing that Bay Area homes are underpriced, just that your implication that this is some unexplained magic leading indicator and not the result of an obvious catastrophy is mystifying.

The results of the fire are very visible in Oct-Jan in the chart. The aftermath of a big fire should be an increase in demand, a decrease in supply, shortening of days on the market, etc. That’s what we see in the charts for Oct-Jan. Then the effect fades. Now it’s gone. Thomas Stone — quoted in the article — lives and sells homes in that market. His anecdotal stuff, in many ways, is even more convincing than the actual data.

Not that I agree with Mark, but could it be that the latest round of fires finally convinced people to not buy there anymore?

You need proof that another county is rising in sales and prices with limited supply left to show people leaving this county to go to a different location away from the fires.

If natures wrath was ever an indicator, no one would have moved back in to Houston after Harvey. No one would have went back to New Orleans after Katrina.

Prairies: your point is good but better made without mentioning Katrina and NO. The latter has never recovered in house prices and insurance is out of reach for rebuilding.

It is exceptional. It is also amazing how a US city could depend on such cheapo barriers as those earthen levies that are like something a farmer would make.

They need to go to Holland and see how it’s done.

Sonoma county does not represent the Inner Bay Area very well as it has been a Tourist driven market with excessive vacation rentals, weekend retreats and a lower income resident population working in the Wine and restaurant jobs. It also has some history as a large over 55+ housing hub with both residential housing tracts and mobile home parks.

The country has significantly upgraded its requirements for building in the more rural and forested areas. They are requiring homeowners and builders to remove all dead trees on their property. My contractor told me he is rebuilding a home on 11 acres and they had to remove 300 trees. The very wealthy are not having any issues as they had enough insurance and money in the bank to weather this crisis but everybody else is hurting.

Mark, the numbers don’t include “Lots and Land”, just single family detached homes.

As to the very few surviving homes in burned over areas most of them had severe smoke damage and quite often damage from the heat.

One home I’m familiar with was untouched by fire, however the estimate for the heat and smoke damage was $400K for a home that would bring $1MM or so updated and in good shape.

You seem to be arguing that the inventory of homes for sale is up and sales are down due to the overall supply of homes declining due to the fires?

What I am seeing so far looks like a normal cyclical price correction, these usually take a few years to play out.

Mark,

As Tom Stone pointed out, Lots and Land are not included in the MLS data. But here is the separate data for Lots and Land for Sale, going back to June 2017. And you can see the impact of the fire in the surging listings since Feb this year:

I got an e-mail a few days describing a “beautiful build-able lot in Fountaingrove”, with a very nice view. (Fountaingrove is one of the neighborhoods is Santa Rosa which took a lot of damage.)

No word yet on how the listing is going. . .

Another reason could be connected to the marijuana world, which Santa Rosa sits almost dead in the middle and being the biggest urban location for the growth and trade. Over the past 3-5 years as other states have legalized marjuana, Northern California growers have taken a deep hit in the return for thier product. Many people from Willits down to Santa Rosa are leaving. Most are renters but Im sure some bought home while times were good in the trade.

I talked to a friend he used to put on big music shows in Northern CA and were heavily attend by people in the trade, he tells me the shows, are cut in half. People are showing up like they used too. Not sure how much weight this has in inventory and price, but it could be a factor.

My observations are that prices of residential real estate in the emerald triangle counties are at or slightly lower than the 2006 peak still. Rural land on the other hand was in an enormous bubble that started to burst about a year and a half ago, due to cannabis speculation. Inventory has exploded and buyers have completely dried up. Lots of land was sold for way more than it was worth over the last few years, most owner financed, things will get interesting when growers begin defaulting. Legal cannabis is not as lucerative as many hoped and competition is fierce. I hear all over that local business across the counties aee down 50% or more from years past. Things are going g to get interesting for sure.

– Canadian realtor Ross Kay told Howestreet.com that his model told him that there was already a trend change in the US real estate markets in mid to late 2015.

I can’t help but think that there might also be a bit of the yearly impending forest fire season. Last year devastated a lot last year in Sonoma County. Life changing events such as loss of employment (destroyed either in the fire or as a ripple effect). Who knows, maybe it is the weed. Most of the folks I know from Sonoma County couldn’t care less about grow operations.

We used to have many articles about the doomed Miami condo market . Nothing no more?

Fear porn?

I lost my data source, that’s all. These articles were largely focused on the pre-construction market. This is very specialized data that you cannot get from the MLS because these units are not listed on the MLS but are sold directly by the developer.

They don’t call them NAR (National Association Of Rodents) for nothing :

sell ’em a multi-million dollar property with pre-meditated deception-

“while better than having a pig farm next door, an acre of flowering cannabis can be pretty overwhelming. You don’t want to show those properties on a warm afternoon.”

Next, look at how many agents and brokers are failing to renew their licenses. The marginal agents will drop out when it is too hard to make a living.

Wolf, Bonjour, your gmail is bouncing my email msg sent.

Pls check.

Thanks & Regards,

Bill

Strange. All my email systems seem to be working fine. Are you using the email listed on the “Contact Us” page ([email protected])?

These numbers are only for detached single family homes.

Burn lots are classified under “Lots and Land” and are not broken out separately by the MLS.

And Cannabis grows affect nearby home values both due to odors and due to the fact that it is a cash business which attracts violent criminals.

A nearby grow is a material fact which MUST be disclosed to buyers.

>> a cash business which attracts violent criminals.

Wall St criminals are next. Less overtly violent, but even more dangerous.

Great article Wolf, it must take a lot of your time to research this information and graph it all up for the blog. I’d love to see the same for So Cal/ San Diego as I see many of the same ‘warning factors’ in my community as well. I suspect that we have the same thing going on here, only to possibly get worse as the southern part of Calif is now beginning their real fire season, when the Santa Ana winds perk up ala 2003 when the Cedar Fire destroyed 300K acres of the Cleveland National Forest and a couple hundred homes here in SD County. We’re quite ripe for another inferno as 6 years of drought have had a major impact on the chaparral and all the makings are in place. I think our RE market is beginning to inflect as well, and if we get a Sonoma style fire going into one of the rural communities, well, there are lots of implications. We’ll see….

Tom Stone, a broker in Sonoma County and a commenter here, provides me with the MLS data for Sonoma County. If you find a broker in your bailiwick who is willing to send me the MLS data I’d be happy to look at it.

Insurance companies are reluctant to cover homes on the edge of open space, or only do so at prohibitive rates. RE growth is coming back into incorporated areas, and high density projects. While we have a property tax cap, it doesn’t help much if you don’t have an older property to sell and therefore transfer the base rate. HOA, Mello Roos, county restrictions on development, insurance blackout zones. (transportation: Carmaggedon) No longer a buyers market, and the Fed can’t keep levitating prices indefinitely.

I am in San Diego and anecdotally I can see sales down yoy long listing time and multiple reductions although prices are not down a lot

These exact charts would be very helpful for other cities, such as San Diego and Orange county :)

2018 started out looking like the RRE market was going to flatten, but then in the spring it shot up to new highs. I think what happened in N. Cal is that folks who were on the fence saw the astronomical prices in spring and spent the summer getting their properties ready for sale – and now in Aug/Sep, the inventory is spiking. And prices are leveling and falling.

It’s inflecting in Vancouver rapidly; house prices down, even in condo prices. Action and multiple offers way down. The buyers are no longer in a panic and can’t be intimidated into an auction.

This will strike some as odd, but the crashes in Turkey and Argentina have the same fundamental cause as our slowdown: liquidity is leaving the game.

The weak members of the herd and the canaries in the coal mine will feel it first, but this tide is going out for all boats.

I think the ebbing mainland China money is a root cause for a lot of weakness in the markets mentioned in this site (especially Oz/Vancouver/Toronto). These three were exacerbated by actual legislation, but Seattle is starting to feel the pinch too. Whether that hits the US west coast markets rapidly could dictate the pace of normalization.

For a few years, any property on the market in the SF area was met with at least one all-cash mainland offer above asking with no contingencies, and it was off to the races from there. If those buyers are gone, then you can maybe start looking at actual fundamentals and see that it’s still out of whack. Will be interesting to see what happens.

You hit the bullseye, I’m up in Canada and Canadians are generally quite stupid so it will take a couple more years for them to figure it out. Of course Brampton will be the last city to figure it out as always.

The best part is, the prestidigitatorial FED tightening so late into the cycle they themselves yet once again, instigated.

Congratulations!

It’s not interest rates its killing off the Chinese demand on the west coast via stiff tariffs on China. Meaning the yuan buys nothing outside of China as the value of the yuan continues to fall. Interest rates don’t affect anything when the Chinese pay all cash. Trump figured out how to kill Chinese demand by killing off the yuan.

– Falling sales & real estate prices in California are a BIG deal for the US and the world. Because if Ca. would have been an independent country it would have been the 10th largest economy in the world. The financial pain will spread beyond state and national borders. (think: the US running a Trade Deficit).

– Weren’t the people in Washington DC aware that they are playing with Dynamite when they introduced the changes in the new tax code. Especially when it come to the deductability of state and local taxes ? It simply came on top of the already weakening US housing markets. I fear DC hasn’t got a clue what they have done to the stability of our US in the near future.

– The current administration could have phased in these new taxlaws over the next say 10 years. The current plans give (more) credibility to the ideas floating around on the internet that this was a deliberate move to punish the Blue states (like Ca.). Still don’t know what to make of it.

If either the US or world economy depends on Cali real estate then you could argue that is unhealthy in the first place.

Everywhere we see these economic disasters: US 2008, Ireland, Spain, now Turkey. there is a bloated real estate sector.

It wasn’t always like this. The US has had periods of prosperity with a much smaller role for housing. The Industrial Revolution in the UK, with the first railroads, steam ships, etc. did not see house prices rise or house building become a linchpin of the economy. But now it supposedly depends on London house prices. As does Australia’s on its urban centers.

In Germany the most successful economy in the Western world, if not the world. they remain largely a nation of renters, and not a nation with a bunch of credit card debt.

What about the problems with rebuilding houses that were destroyed by the fires last fall. The cost of rebuilding has been complcated by additional governmental requirements that even builders have not been able to estimate with good cofidence. Add this to the fact that many destroyed homes were not fully insured and you have an increase in the number of lots for sale. This does not show up in the number of houses for sale , but ultimately will result in more homes for sale

How things change in a hurry when Trump slaps stiff tariffs on China and the yuan collapses in value vis-a-vis the U.S. dollar. Looks like Trump has found the answer to deflating the housing bubble on the west coast. Kill off China and the value of the yuan and it kills the U.S. housing bubble.