New York condo prices fell again. Historic spikes slow in Seattle and other metros.

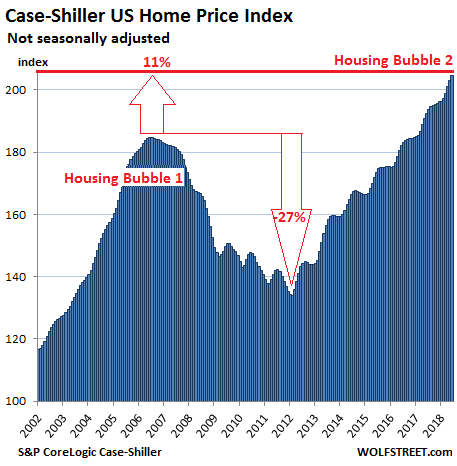

On a national basis, home prices surged 6.2% in June compared to June last year (not seasonally-adjusted), and 0.8% from May, according to the S&P CoreLogic Case-Shiller National Home Price Index released this morning. The index is now 11% above the July 2006 peak of “Housing Bubble 1” — the first housing bubble in this millennium. After its collapse, it was called a “bubble” and “unsustainable.” But by now, this peak of the collapsed bubble has been transformed into the new-normal rock-solid base of the current housing market. The index is now 53% above the bottom of “Housing Bust 1”:

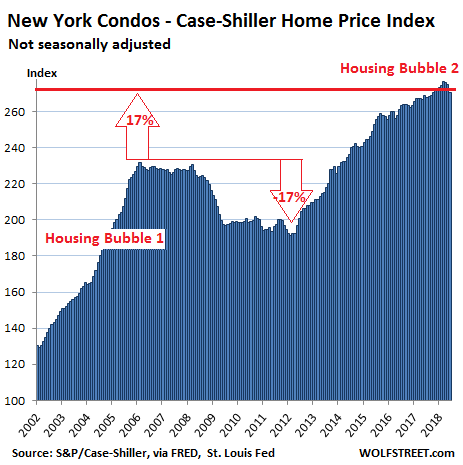

There have been some indications that some local housing markets are experiencing deteriorating fundamentals: declining sales volume, rising inventories, less foot-traffic, increasing number of days on the market, etc. [here is an example], though prices are slow to react. These dynamics are not yet visible in the some of the bubbliest markets as depicted by the Case-Shiller Home Price index — except in the New York condos category where the index has dropped to the lowest level since October 2017.

The Case-Shiller Index is based on a rolling three-month average; today’s release is for April, May, and June. The index is based on “home price sales pairs,” comparing the sales price of a home in the current month to the last transaction of the same home years earlier. The index incorporates other factors and uses algorithms to arrive at each data point. It was set at 100 for January 2000; an index value of 200 means prices as figured by the index have doubled. It’s an alternative to median-price indices (half of the homes sell for more, and half sell for less).

The index is not inflation adjusted. It’s itself a measure of inflation: of asset price inflation, specifically of home-price inflation, where the dollar is losing purchasing power with regards to housing; in other words, it takes more dollars to buy the same home.

So here are the most splendid housing bubbles in major metro areas in the US:

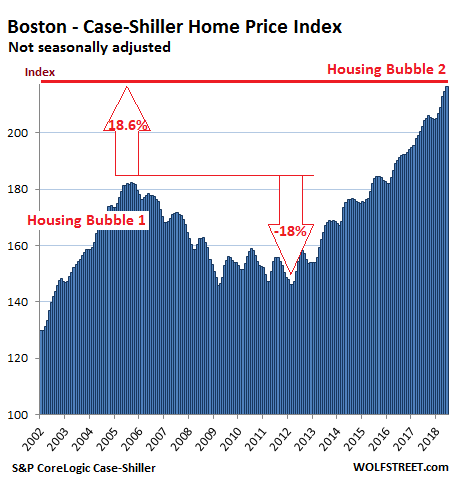

Boston:

The Case-Shiller Home Price Index for the Boston metro jumped 7.1% from a year ago. During Housing Bubble 1, from January 2000 to October 2005, the index soared 82% before dropping. It now tops that crazy peak by 18.6%:

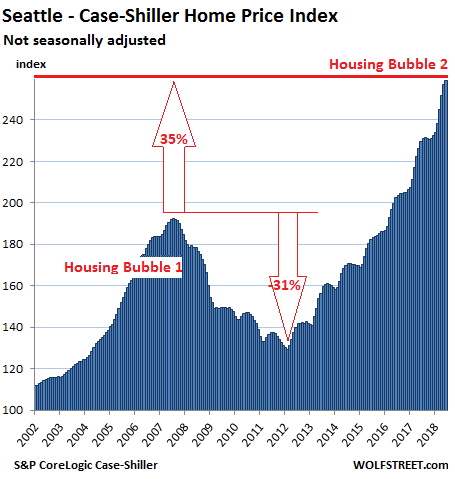

Seattle:

Home prices in the Seattle metro rose 0.7% in June from May. This is a slow-down from the historic spike in prior months. Over the past 12 months, the index has jumped 12.8%. It is 35% above the peak of Seattle’s crazy Housing Bubble 1 (July 2007):

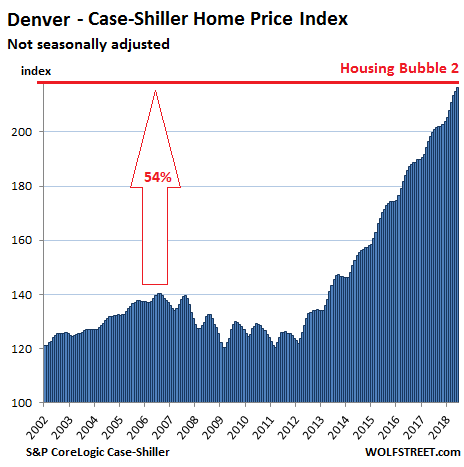

Denver:

The index for the Denver metro booked its 32nd monthly increase in a row in June, adding to the historic spike over the past few months. It’s up 8.3% from a year ago and 54% from the peak in July 2006:

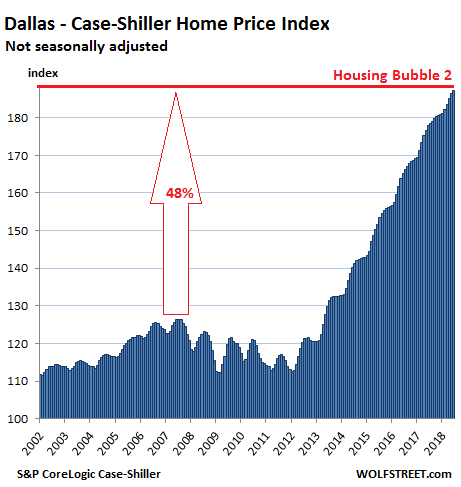

Dallas-Fort Worth:

The Case-Shiller index for for the Dallas-Fort Worth metro rose for the 53rd month in a row, and is up 5.2% from a year ago. Since its peak during Housing Bubble 1 in June 2007, the index has surged 48%:

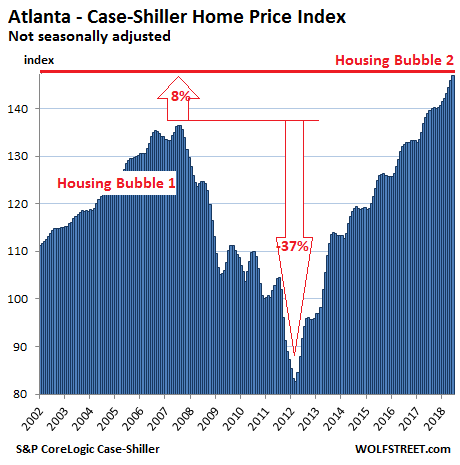

Atlanta:

Home prices in the Atlanta metro rose 0.7% in June from May, according to the Case-Shiller index, and 5.7% over the 12-month period. It now exceeds the peak of Housing Bubble 1 in July 2007 by 8%:

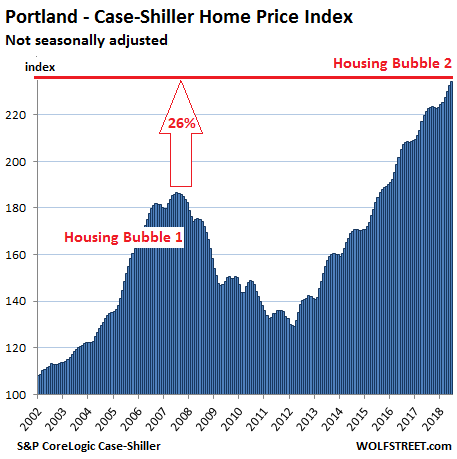

Portland:

Home prices in the Portland metro in June rose 0.7% from a month ago, 5.9% from a year earlier, and 26% from the crazy peak of Housing Bubble 1 in July 2007. It has ballooned 134% since 2000:

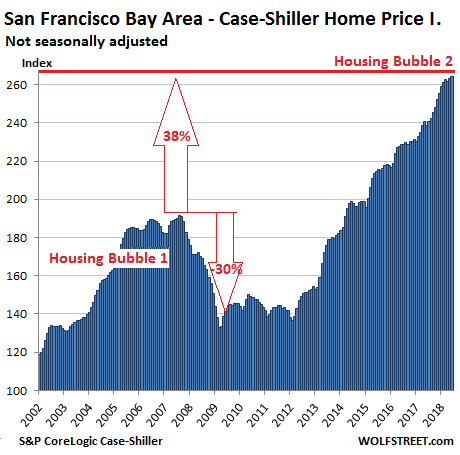

San Francisco Bay Area:

The index for “San Francisco” includes five counties: the city and county of San Francisco, the northern part of Silicon Valley (San Mateo County), part of the East Bay (counties of Alameda and Contra Costa), and part of the North Bay (Marin County). In June, the index rose 0.4% from the prior month and 11% from a year ago. It’s up 38% from the crazy peak of Housing Bubble 1 and up 164% since 2000:

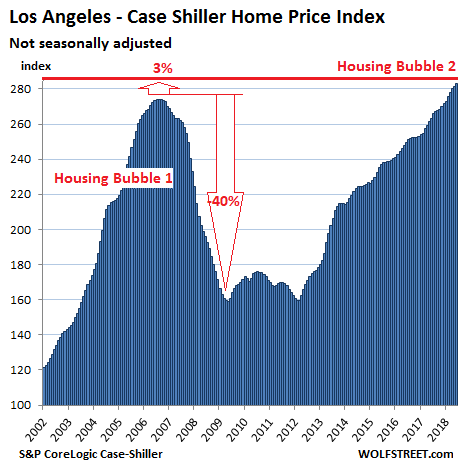

Los Angeles:

The Case-Shiller index for the Los Angeles metro in June rose 7.4% year-over-year. Between January 2000 and July 2006, the index had skyrocketed 174% before its epic collapse. The index now exceeds the complete nut-job of Housing Bubble 1 by 3%:

New York City Condos:

Prices for condos in the New York City metro fell — yes, fell — 1.6% from the prior month, the third month in a row of monthly declines, according to the Case-Shiller index for condos. The index is now down 2.2% from the peak in March and is up only 0.6% year-over-year and at the lowest level since October 2017:

This dip in condo prices is either the first visible sign of a deflating housing bubble on this list of the most splendid housing bubbles in America, or it’s just a temporary dip. Once the index is down year-over-year — at this rate, in a month or two — it would establish a trend.

Real estate is local. But prices are also impacted by national and global factors, such as monetary policies and offshore investors for whom “housing” in the US is not only an asset class used for diversification, but also in many cases an exit route for their family and wealth away from their own governments. These factors combined inflate local housing bubbles. When enough local housing bubbles come together, they turn into a national housing bubble (see the first chart), though some other markets may lag behind or never get into a bubble status.

The first wave in the buy-to-rent scheme, where private equity firms buy hundreds of thousands of single-family houses in a small number of markets, got started during the housing bust. Now comes the second wave, by a different set of private-equity firms, at the peak of the market, as brokers constantly blame low inventories of single-family houses for sky-high prices. Read… Here Comes the 2nd Wave of Big Money in the “Buy-to-Rent” Scheme

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

For interest and comparison purposes regarding Vancouver BC home prices….

A recent Angus Reid survey discovered the following:

For Vancouver, “Those numbers were even higher in Vancouver, where nearly three quarters of owners said the cost of a home was “unreasonably high” — 20 per cent said prices should drop by 30 per cent or more, and 29 per cent by at least 10 per cent.”

and: “People in Vancouver and Toronto would like to see more government intervention to help curb prices — despite skepticism that anything can be done to keep costs from rising, the study suggests. ”

Except for those who recently entered the housing market, the vast majority would like to see a substantial housing price drop. For those recent purchasers, they are very afraid of falling prices. The study also mentioned how misreable recent buyers were with their nightmare payments, long commutes, and feeling/realization of being stuck. Many said they wished they had moved away instead of buying into the Vancouver market.

From the hinterlands, we are really being pressured by relocating retirees. Just 1 hour drive east of where I live there is a non-stop housing construction boom. My in-laws home has increased in value by 25-30% in just the slast 2 year. A friend of mine down the road is selling his house privately…to someone from Texas. The buyer was a drive by lookie loo.

I can understand Canadians from other parts moving in for a better climate, but a Texan? The Okanagan valley prices must have gotten to completely unbearable levels for these people to start look at other options, such as your inner Vancouver Island.

Good fishing, I guess and t is beautiful. People who can’t take the rain and wind last about 2 years. Texas is windy, though so maye that’s why :-)

Prices rise when too much money chases too few of what’s being chased. I don’t get it. Wages must be rising or some form of desperation for housing must be off the scale.

In the heartland by me, I just read an ad for a house for a little over $1million. It has lake views from most rooms, lake access, an indoor pool – large, with a large balcony deck overlooking the pool, 10,000 sq ft in the house. The house sits on a park like lot with an expansive brick stair landscape going to the front door. Upscale everything, although the stove did not have an outdoor facing hood – bummer. Taxes would be an extortionate $35,000 a year or maybe a few thousand more.

NY NY and other places sound like Hell to live in.

Re the stove: it did have a custom brick flame grill with outdoor venting in the kitchen. I forgot. The stove must be to fry eggs.

Standard housing for $1million in lots of places will get you a place to live that’s nicer than where many others in the area live – only. Fortunately, not where I live. It’s lots cheaper for normal housing like my place.

Put it this way: really expensive cities to live in such as Boston and Seattle are where the real good wages are. These wages tend to grow faster than those in flyover country, sometimes even far faster, for a variety of reasons.

But the downside is when you combine a limited housing supply with fast-growing wages you get spikes as extreme as Seattle’s in the chart above, which in turn lead to the now infamous “affordability crisis” even for people earning good money.

On top of this mortgages are still cheap to service by any historical standard. Costs have moved upward a tiny bit, but not as much as you’d expect. Same as with US Treasuries.

For all the PR spin, companies do not like wage inflation, especially when due to competition they cannot pass it all on to customers. I know I don’t and I know several companies with US-based subsidiaries are already fretting about wage inflation and I can assure you if they could move operations to Mexico, Turkey or Vietnam they’d do it in a heartbeat. But they cannot.

The US Federal Reserve seems to have got the message by spending a lot of time talking about an optimum unemployment rate higher than the present one and that’s good, for the companies. Now everybody is waiting for the facts.

However companies may be put in front of a choice: lower wage inflation or higher debt servicing costs. The time of having the cake and eating it too is over.

If theres a shortage of housing in Seattle, why are listings up 44%you? This is central bank fueled speculation, my friends. And it’s beginning to unravel.

[Full Disclosure: I live in King County (Seattle Suburbs) and have a Real Estate Broker’s licence, but my real job involves Computer Stuff.]

The short answer to your question is this: When you increase a tiny number by 44%, you still get a tiny number.

The listing numbers early this year were absurdly low. It was something like one or two weeks of sales for a while there. Two or three months of inventory is usually considered a strong market.

There has definitely been a slowing of the market since the Fed started raising interest rates, but we are a long way from “affordable”. Most of the reduced demand comes from people who could just barely afford a starter house with a 4% mortgage, and who can’t afford anything at 5%.

A secondary issue is Chinese money. After Vancouver cracked down on non-resident Real Estate purchases, Chinese flight capital started buying in Seattle. (Notice that I say Seattle proper, not King County.) Recently, the Chinese government has made it harder for people to export money, and there has been a modest reduction in demand because of that.

The bottom line is that things have become slightly less crazy, but the Greater Seattle Area still has a lot of buyers.

Buyers are rushing to get into a house before interest rates get too high.

Prices are slow to turn but I just got back from Las Vegas and checked Zillow for prices in the area I was staying. The inventory was huge. I also noticed quite a few houses with recent price reductions. I don’t know if this is an indication that things are starting to change but it was alarming seeing the amount homes for sale.

I’ve noticed the same thing on Zillow in many areas on the East coast Price reductions and houses not selling for longer periods It sure looks like a top to me

Yep. As I mentioned in a comment in an earlier article… price cuts are starting to show up in Florida as well.

I still believe that we’ll see a 15%-25% decline in average nationwide house prices over the next 2-3 years.

There are reports on the internet that foreclosures are up in LA, Miami, Houston and other cities. I can’t recall them all now. It’s not everywhere but it’s trending up.

Saw some interesting videos on Australia where the refi process has been changed. Now borrowers have to account for normal expenses, not just other debt, and many are not qualifying.

I live in south central Texas. In our county, there were only 14 recorded foreclosure postings for July 2018. My neighbor sold his house in 8 hours for the full asking price. For my other neighbor it took only 4 days to sell. I don’t see this as a bubble but simple supply and demand at work. Our area has remained stable in prices since the great recession since over building was not an issue and never had explosive growth. But I have to say, I have seen this type of market before when I lived in Las Vegas in 2005 and we now know what happened a few years thereafter! Staying alert!

Yes Petunia big problems in Australia. Not just expenses being accounted for but the fact the banks are now willing to loan you a lot less based on your earnings than before. Interest only mortgages still a massive issue also around 40% of total mortgages.

Petunia,

Yes, they’re up in some cities but from very low levels — and they’re still at very low levels (these are new foreclosures, not those left over from the crisis… which are STILL getting dragged through the system in some places).

ATTOM sent me the data. It’s something to keep an eye on, but it’s not very meaningful yet. Where home prices have soared recently, foreclosures are rare because the home can be sold at above the loan amount and the loan can be paid off from the proceeds. When home prices decline, this becomes a real issue very quickly.

Absolutely correct, Wolf. Foreclosures only start picking as more homeowners start experiencing negative equity in their properties. We’re definitely not there yet in the current cycle.

Wolf, I’ll be sending you an update on Sonoma County when the numbers come out 9/10.

It will be more of the same, despite low inventory.

Buyers are no longer in a hurry, and sellers are not yet in a hurry either.

Not yet.

Spring will be interesting.

Thanks. Looking forward to the data.

A reminder: Among well-to-do homeowners, there often is not a lot of pressure to sell when the market sours, and they may try to sit it out. It’s when forced selling starts, that prices get hit at the high end, but that may not start for long time.

This is not the case with homes priced closer to the median or below. Most of those households don’t have a lot of financial flexibility and may not be able to wait out anything. This becomes a real issue when one of the earners in that household loses their job. But the job market is still very strong here, so forced selling is not yet on my horizon.

What about the fact that the last bubble and collapse are still fresh in many peoples minds? Is it possible when houses start sitting that many on the fringe will be quick to pull the trigger?

It’s possible. But housing moves so slowly, that “quick to pull the trigger” has a different meaning than in most asset classes.

Edwin,

What is also fresh is the FED & gubbermint have your back. People that sold at the lows must be seriously depressed and folks that bought in 2012 have crushed it. What used to be a cash purchase amount is now a decent down-payment in some instances. hard to sit on the sidelines and see fortunes made and have your purchasing power decline.

I grew-up in LA and was up there midday on Saturday. Jeez, the traffic is unreal.

“Among well-to-do homeowners, there often is not a lot of pressure to sell when the market sours, and they may try to sit it out.”

True perhaps for most owner-occupied houses of the “well-to-do.” However, it has been shown that middle to upper income housing speculators were the principal cause of the last housing bubble and collapse. When prices turn, there is not only no incentive to hang on to an ‘investment’ property, there is a big incentive to “jingle mail” in the keys to the bank, especially in a non-recourse state like California. This time it should be very interesting, with large numbers of houses now owned by REITs and private-equity speculators, not only “mom and pop” house flippers.

Yes, I totally didn’t mention speculators and investors :-]

And there are more of them than ever.

In California they will have a referendum on the ballot to repeal a law that prohibits rent control of single family homes. My bet is that rent control is coming to CA which will discourage SFR REITs from investing there in the future. I also think rent control is coming to other states.

Yes, but remember that for a lot of real estate investors, yield may be more important than the price of the asset. Once you smooth out the month-to-month gyrations, rent tends to be much more stable than house values. As such, RE investors may tolerate a reduction in price (as opposed to say stock investors who are much more reliant on price appreciation than dividend yield).

Of course, I am not talking about house flippers though, who generally hold the asset for a reliatvely short time. They are not real estate investors, they’re real estate speculators.

Here on the olypen (Olympic peninsula )

Rarely is a house sold in less than two weeks. Now I see houses that went in a week sit for months. It went from White hot to this in less than 12 months. Now about 60% or more of my daily Zillow updates are price drops. Hmmmm

Peak to trough Case Shiller for LA & Dallas pretty much tell the story of the BIG Short where the RE Agent tells Mark Baum that they are merely in a bit of a gully with respect to turnover & sales. Predicting the inflation between 08 and 2018 was easy. Now that QE has halted and liquidity is not sloshing around like it was a few years ago we can see that the smart money has moved on from places like Manhattan NYC. Given the decade since the last crash in the housing market it looks like another crash is sitting right on our collective doorsteps right this instant.

Expectation has it that the Stock Market is overvalued by at least 50% now and climbing on towards peak irrational exuberance again. With trough to peak increases in the range of 40 to 50% on housing inflation since 08 we can now expect that this asset bubble will implode at any second. No analysts believe in the productivity of the markets much anymore. Analyst skepticism is at peak too from what I have been selectively reading.

This analysis is following the same trend of analyst predictions that I am seeing on average so I would hazard a guess to conclude that the Cassandras of Wall Street should be receiving their long overdue accolades anytime now.

MOU

mid term election years are usually bullish until November and can carry forward. Definitely not anywhere near dot com bubble. Valuations are 19 Forward PE SPX…earnings driving market now..XLF heads to 30 and 3K is definitely in play….foreign money pouring into equities instead of emerging markets…

A lot of real estate price data like Case Shiller is trailing by a few most. On top of that buyers also go into contract 45 days before they close and the price shows up in data. We probably won’t see a price slowing show up in the data until earliest Nov – if not early 2019.

It can take a while for house prices to fall. Inventory started rising and things started slowing in spring of 2006 but the free fall in prices didn’t happen until 2008.

People will realize once again that its not as much fun to own a house that is falling in price or flat. Yet you still have a big mtg payment, property taxes, insurance and very expensive upgrades and repairs.

These periodic updates serve to document housing bubble 2.0 for posterity. Thank you for providing this service. The Case-Shiller index is an extremely lagging indicator, and so won’t show the turn until after it’s already happened. Anecdotally, from various comments and inputs, including this blog, this turning appears to now be well underway. Someone with the inclination can check the leading indicators, such as declining new and pending house sales, and rents to confirm.

A couple of 30k ft. view questions about this whole thing. Doesn’t anyone stop and marvel at the absolute insanity of these data sets? Doesn’t this market behavior seem just a little like an episode out of “The Twilight Zone”? C’mon! These used to be houses for shelter, but now thanks to the “genius” of financial engineering at the “wizards” running the central banks, it’s become just another commodity; another financialized asset. People, this isn’t normal market behavior. Adam Smith would be spinning in his grave.

Dare we ask “Why”? Because TPTB needed to “save” us all from the bad bets of bankers and financiers leading up to the GFC. Oh, we were “saved” alright, by the bailouts, QE and other interventions, financial repressions, and debt monetizations that were foisted upon the taxpayer. Whether outright bailouts, inflation, or growing income inequality, the taxpayer is picking up the tab, one way or another. If this is the best Keynesian economics and our betters have to offer, we ought to try something else. Like free markets and sound money, for example.

Recall that none of the responsible parties – up to and including the Fed and the other nefarious central banks – suffered any consequences. No one went to jail, with the exception of the responsible bankers in Iceland, the fact of which is relegated to a minor footnote in the archives of history. In the aftermath of the GFC, they just made up some whoppers, and yet again pulled the proverbial wool over everyone’s eyes, and doubled-down with yet more money printing and historic interventions, leading to the current “Everything Bubble”, which includes housing bubble 2.0.

Sure, it seems good on the way up, but bubbles have a nasty habit of bursting rather than dying by slow leak.

“A bull market is like sex. It feels best just before it ends.” – Warren Buffet

Finally, debt is not wealth. Go back to Econ. 101. Running a business or a country goes back to the balance sheet. Assets and Liabilities. Assets minus Liabilities is available capital or wealth. If this is a negative number, then, well, you get the idea.

My 53 year old sister-in-law is building a home and will be about $450,000-$500,000 in debt upon completion. They are ecstatic that their property has doubled in value before they even started construction.

Did I say anything about their debt? No. They aren’t prepared to listen and I won’t create a rift in our relationship.

Investing with debt has worked well and sometimes fabulously for decades. Rich man Poor man thinking has worked well and it is stuck in peoples minds as a sure fire way to get rich. I think the popularity in this way of investing is coming to an end. Cash will be king for the near term at least. The multitude of IOU’s that are piled on each other will come crashing down. I don’t think any action done by central banks will be able to stop it once it gains momentum.

“The index is not inflation adjusted. It’s itself a measure of inflation: of asset price inflation, specifically of home-price inflation, where the dollar is losing purchasing power with regards to housing; in other words, it takes more dollars to buy the same home.”

The Case-Shiller index has outpaced CPI for at least the last 25 years, only briefly approaching it in early 2012, using 1992 as the starting point. By my calculations, it would have to drop 30%+ just to meet CPI over that period. You (probably) can’t sell a bag of potato chips you bought in 1992 for multiples of the purchase price, but you can a house in some cities in the U.S. On the other hand, while CPI tends to slowly rise over time, asset prices go through boom/bust cycles with regularity. Hoping for a mere 30% drop in the Case-Shiller would be naive. I could see median prices dropping 50%+ in some cities in the U.S. over the next several years, even quicker if interest rates rise significantly. Peter Schiff is on record calling for a 50-70% drop in prices from current levels. Take that for what it’s worth, but I trust him more than CNBC’s talking heads and he is on record predicting the last housing collapse in 2007.

Todd Those talking heads on the boob tube sure gave it to Peter good when he starting predicting the last crisis He obviously had the last laugh and knowing Peter he will once again

He has also been calling for dollar devaluation and gold to the moon. He may eventually be proven right, but following his advice thus far would be financially damaging. It seems the can is being kicked further than he imagined possible.

It may eventually happen but it will take another decade or two. In the meantime following his advice leaves you in a big hole. The central banks are doing everything they can to blow this bubble as big as they can for as long as they can.

mid term election years are usually bullish until November and can carry forward. Definitely not anywhere near dot com bubble. Valuations are 19 Forward PE SPX…earnings driving market now..XLF heads to 30 and 3K is definitely in play….foreign money pouring into equities instead of emerging markets…

Here in Los Angeles, in order to sell a million $ average home, 2 sellers I know dropped their prices after 60 days with both only getting one offer.

One listed at $1,195,000 is in escrow for $1,075,000 and the other listed at $1,100,000 is in escrow at $980,000. These and other similar sales figures won’t show up until they close in Sept 2018. The shi* appears to be hitting the fan!

The house that sold for 980k is probably a small ranch on a postage stamp size lot and in a sane market would probably be realistically worth maybe 650k so they should be happy with what they got and that they got out early

Been hearing and seeing articles about this bubble yet nothing chances. Every time we think we’re going to revert back to the mean, several months pass and then it’s back to the races. I’m starting to believe something has fundamentally changed and it truly is different this time.

If Case Schiller index was set at 100 in 2000, and is now above 200, but is NOT inflation adjusted, what is the true per year increase in the index, after 18 years? By using these same metrics, could we also be in a Corvette and Big-Mac bubble as well?

Assuming true inflation is 2 percentage points above the publishe FED rate, is real estate since 2000 in a bubble at all, or just a normal 4-5% annual rate of return?

That’s what I keep pointing out as well on these articles. I like to use median household income growth rather than inflation to adjust the index (since income is subject to less gaming than CPI). Since 2006 it’s up about 30%. As such, the 11% nominal gain in the Case Shiller has not caught up with the peak of the previous bubble yet in real terms.

To me, the real splendid bubble is in stocks — which are up 85% in nominal terms since their late 2000 peak. Makes housing’s 11% gain seem like small potatoes.

The Case-Shiller IS a measure of inflation: asset price inflation. If the same house costs twice has much after 18 years = 100% price inflation for that particular asset.

Yes because do you really believe people’s incomes have doubled since 2000 because mine surely did not and I doubt many others did either It’s unsustainable and therefore a bubble People are living in their cars who have so-called good jobs in some places in California That’s Insane

Seems like a definitive ten year cycle with a five year mini cycle or mid point. Though your data points are indexed to 100 it would be interesting to see what the graphic pooks like including all in purchase price (rather than bid/offer on acquisition).

I am starting to see similar things mentioned by others in the DC area. Houses that use to go in days are not sitting for weeks or months, many now have price drops. On top, there is A LOT of inventory of new “luxury” apartments and condos coming on line in the next year. This is definitely the top around here. The only thing that might “save” prices is if Amazon HQ2 comes here. If not, 2-3 years should see 20-30% reduction imho.

Doing the math, if you compound Case Schiller starting at 100 in year 2000 up to today, 18 years later, the index should be about 239 using a 5% return. Now, has the ride been a roller coaster between those dates? Yes, without a doubt….but hardly a Magnificent Bubble. As a matter of fact, by the time you include inflation, and other expenses such as utilities, insurance and maintenance, I would say that it is a rather poor investment. Looking at the last 18 years appreciation the “bubble” is about where it should be, and if inflation is included, real estate is appreciating at a rate similar to historical averages.

The one thing I can say for sure is that if I bought a stock index fund back in 2000 at $100 per share, and I only made a 220% profit AFTER 18 YEARS, I would consider this return to be lackluster at best, especially when factoring in inflation.

Correction: 120% return over 18 years, not 220

You are hilarious!

Wendy,

Who says that a home, which doesn’t get bigger or better or nicer, should rise in price 5% a year? This is the same principle that the price of a gallon of milk should rise 5% a year. It’s just INFLATION. All this means is that dollar is losing its purchasing power with regards to those items.

A house is NOT a company with rising revenues and earnings. People keep confusing this. A house is an expense with a utility (living it it) and zero revenues (unless it’s rental property and than it’s a different story entirely).

Sir, I absolutely concur with you. People don’t realize that a house is a depreciating asset ( because of wear and tear ) and that only the appreciation in land prices is what should lead to increase in value of the house.And land appreciates mainly because of speculative investments and not merely because of increase in population.Thus, although land price will naturally appreciate over time, there will be checks and balances on the price.Thus, the appreciation in price of housing seems to be disconnected from reality and indicative of a “bubble”.

That may be true, but some markets are appreciating way ahead of the averages, while others are way below. The averages are deceiving.

You can’t really speak of a “return” in the context of a house you buy to live in.

And with the stock market, you can’t just compare the value of the index across time to compute “return”, you also need to include dividends (i.e., compute total return).

If you buy a house as an *investment* then you need to include rent proceeds in “return” calculations.

You can then use total return figures to compare different asset classes. If you do that you’ll see that over the very long run the stock market and the real estate market have provided roughly the same total return.

Interesting. So we should be able to overlay a graph of REITs and SPY for the last 30 years, and they would show similar returns? I need to try this.

REITs and SPY over the long term are identical.

As someone considering ‘retiring’ to a less expensive region and possibly investing in rental income real estate, the Case Shiller trends interest me very much.

One thing I have trouble getting my head around is that the data is based upon comparing the current month sale transaction of a specific property, to the previous sale transaction on the exact same property.

If such dramatic ups and downs are happening in periods of 6 years, wouldn’t the index be skewed to reflect speculators more than long term owners? And if so, in addition to higher highs and lower lows, wouldn’t that also compress the trends time-wise?

I understand that the current house price ‘is what it is’…It doesn’t care if you’re expecting to flip or stay 50 years. But assuming the days of ‘asset inflation’ are shifting to ‘everything else’ inflation, what would that mean for CS trends in dollars and time-wise?

Why do you want to invest in something that is not an investment? Buy some stock and bond indexes and call it day.

True price discovery, when it finally comes around, is going to be a bitch for the fools who massively overpaid for their real estate.

Heckova job, Ben & Janet.

Turning everything in the US into a “commodity” for profit will eventually destroy our economy/society. Housing is just one example. Of course, health care is another…….There will be no room for the “Commons”.

If everything is done online, why stay in New York anyway?