OMG! Another laugh-out-loud, gut-buster of an investor call. Come on guys, you’ve gotta stop it.

By Deep Throat IPO:

Let’s take a look at what happened once Alibaba’s YUGE! “61%” number hit the street at 7:30 AM on Thursday August 23rd. Pre-market generally went nuts, pushing the opening number up $7, to $184 from the prior day close of $177. Once the market opened,BABA average daily volume (20 million shares +/-) was traded in roughly the first hour of the trading day at about $184, occasionally caressing $186.50 with 2x average daily volume traded by 11:00AM.

The links to the folderol that caused all of the initial hubbub Alibaba’s earnings Press Release, Webcast, Presentation, and 6-K (Filed with the SEC on 2018-08-23 “end of day”).

Once “professional” investors and commentators had a chance to analyze the presentation, and most importantly the Q&A of the investor call, the mood evolved from euphoria to “what the hell?” and BABA ended the day down $5.75, a $15 swing from top to bottom. Of the 990 prior trading days since the IPO, Thursday, August 23rd, at almost 78 million shares, was the fifth highest volume day on record.

The reason this happened (among other things) has to do with the difference between professional investors and amateur investors.

I also want to acknowledge that the Analysts on the call did a fantastic job of probing the inner meaning and real implications of management’s comments. Based on what’s expected from analysts today, they did an awesome job of signaling the markets and professional investors as to what’s actually going on!

First, not once — with the exception of Alicia Yap at Citi and her “congrats on solid results” comment — did any analyst offer any adulation regarding the quarterly results. Note: In today’s vernacular, the term “solid results” usually refers to a business teetering on bankruptcy which managed to somehow reduce the quarterly loss.

Second, the Analysts bravely and cleverly walked, and never crossed, the ever-so-thin line between pissing management off, getting tossed off the call, risk being referred to as “that asshole analyst” on Twitter forever, and actually doing their job. Bravo!

We live in a world where everything is a “strong buy.” Today, a “strong buy” can mean anything from “Hey, this stock is actually a strong buy! No kidding!” to “Run for the hills!” That said, it has become all the more important to understand the nuances buried in the dialogue between analysts and management on these investor calls, to differentiate the levels and gradations of “strong buy.”

To that end, as a public service, we deploy my patented Dick Fuld Banker-Speak Translator [BST], to fully analyze the implications of the analyst Q&A on the Alibaba investor call. The BST will read between the lines, probing what the analysts were “really” asking. As usual, management’s responses were largely irrelevant, so we’ll ignore them for now (earnings call transcript via Seeking Alpha).

Here are the eight hard-hitting, laser-focused questions the eight analysts asked:

Eddie Leung, Merrill Lynch: Good evening. Thank you for taking my question. Could you share your thoughts first on the e-commerce competitive landscape given the fast growth of some of your peers in the lower price point market so to speak? Just — many years ago, if you remember, Taobao also started more in the lower price point market then developed into today’s scale. So just wondering, how you think about the difference today versus many years ago?

And then if you guys can — could you also comment a little bit on the outlook of your customer management business. There has been a bit of deceleration, of course, we know there is a high base affect. But any color going into second half of this year would be helpful. Thank you.

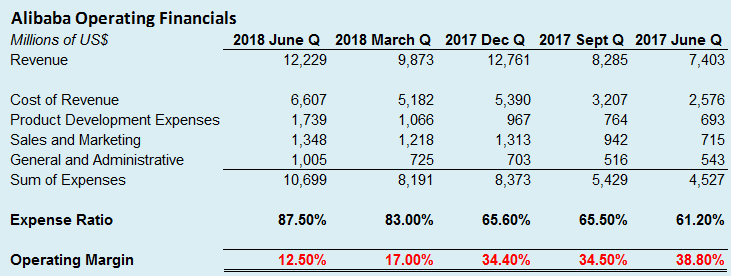

BST Translation: Hey guys, I don’t mean to be so harsh here, but what the hell is going on with your margins? When I compare your operating metrics from a year ago by quarter, I see that you’re operating margins have decreased from 38.8% all the way down to 12.5%….and since you don’t break anything out by business segment I have no way of knowing what’s going on.

From what I can see, “New Retail” means “No profit.” Are you following the model where we can expect that you won’t make any real money for a couple of decades?

Alicia Yap, Citi: Hi, good evening, management, Joe, Daniel and Maggie. Thanks for taking my questions and congrats on solid results. I have some follow-up on these combined online core commerce. So with GMV growth and commissions lightly to experience potentially high base as well from last year, we see CMR also lapse out a tough comp. I think management previously commented about the increasing page view and time spent on the numbers of the recommended feed pagers. So are we still on track to introduce new potential some additional add lows to those second lending pages later this year?

And also second question quickly is just, can you reconcile — help us reconcile the 34% physical GMV versus the 55% commission revenue growth. Is that implying the take rate actually increasing? Thank you.

BST Translation: Even though you don’t disclose GMV on a quarterly basis anymore, you put a growth rate in the press release (even though we don’t know what it’s grown from), and for some reason Maggie talked about it growing 34%, so even though you’ve already told me in the dress rehearsal before the call that the take rate isn’t actually increasing, I thought I’d go off the reservation and ask it again so you could again explain to the investing public how sales “commissions” apparently have no relationship to the amount of goods sold on the platform.

Grace Chen, Morgan Stanley: My question is about the New Retail business. Alibaba has been doing several mergers and acquisitions, and also has been sending out Hema and partnerships with various companies to lay out the foundations for the New Retail business. So I’m wondering is there any — is there still any missing parts in your business portfolio to implement your New Retail strategy? And after the recent merger and acquisitions, what is your critical next step to execute the New Retail strategy? Thank you.

BST Translation: Hey, from the latest 20-F (page 118) we know that you’ve created about 600 new legal entities over the last two years under your “Enhancement” program, getting more friends, family and political cronies involved in the dilution of the Capital Structure. So, I guess my question is “how long is this bullshit going to go on?”

Thomas Chung, Credit Suisse: My question is about food delivery business. Can management comment about the competitive landscape and our strategies and becoming the number one in this segment? Thank you.

BST Translation: Geezzz….I need to talk about something irrelevant so as not to tick off management, while at the same time, signal to the market that I don’t want to talk about the financial results. And now, my boss told me I couldn’t call in sick so I actually have to ask a question on this fu@#!ing call. Let’s see… Food delivery!… Yeah! That’s the ticket. Never mind that the Ele.me/Starbucks/Hema/Koubei thing is an insignificant part of their business, probably generating losses and is mentioned only in passing, without numbers on page 3 & 4 of the press release, and I only have one question to ask!

Mark Mahaney, RBC: I wanted to ask about the sustainability of the digital media revenue growth. It seems like you had a nice impact from World Cup there. Could you talk about whether some of the newer customers or some of the newer business that came out of that event whether that looks like its sustainable, whether you — those are new customers that will stay with the service. Anything you can tell about what their activity has been like post the World Cup? Thank you very much.

BST Translation: Now I’ve gotta follow Tom’s lead… I gotta let the market know that I don’t want to talk about this mess. Maybe I should talk about Share Based Compensation (SBC), maybe it has decreased significantly in the quarter in a relentless effort to control costs? Oh Crap! Outstanding shares have actually increased another 15 million shares (US$ 2.7 Billion @ $180/share). I can’t talk about that.How about “digital media” and the World Cup? Yeah, hat’s it! Tere are no actual numbers released and it’s a touchy-feely topic. Everybody loves sports, right? Oh wait, Digital Entertainment Revenue only increased US$63 million (7%) since the March Quarter so the World Cup couldn’t have had that much of a revenue impact. Professional Investors will see what I’m doing. They will see that I’m signaling that this is a god-awful cluster-filing. I can’t believe I’m in this mess. After that Facebook thing at Citi blew up, I really needed this gig. And now I’m stuck in the middle of this….

Gregory Zhao, Barclays: My first question is about your international — some international brands, which, during the quarter, more international brands coming on to your Tmall marketplace. So how shall we expect the advertising and the commission revenue contribution from these new players? And how shall we expect growth trends going forward? And very quick follow-up is on your 88 VIP. So how do we expect the membership to integrate your existing services and improve user engagement? And can you share some initial metrics of the business? Thank you.

BST Translation: US Shareholders should love it when we talk about “international shit” that they understand. I’m really hoping, even though there’s very little in the press release talking about International Brands, that maybe management will talk about something interesting. Maybe they’ll disclose some of the sales of the brands listed in the TMall “Luxury Pavilion”. They mentioned household names like MCM, Moschino and Giuseppe Zanotti in the filing. Of course, I’m not a fashionista, but I have no idea who these retailers are. I tried to look these companies up in Wikipedia, but the Wikipedia pages indicated that “This article contains content that is written like an advertisement. Please help improve it by removing promotional content and inappropriate external links, and by adding encyclopedic content written from a neutral point of view.” Which usually means that there’s some sort of issue verifying the veracity and background of these International Fashion Icons.

When I go to the websites, Moschino.com (an Italian designer that’s a public company listed in Hong Kong?) and GiuseppeZanotti.com (which oddly enough has a few storefronts scattered all over the world but only three in Italy), they look a little, well, funny. I’m sure everything’s OK, it would be really weird if Alibaba Management allowed fake businesses to be listed in an SEC filing.

Oh man, I know why I’ve never heard of Moschino. Per their website they only have two stores in the US, in LA at 8933 Beverly Blvd, West Hollywood, and their flagship store in New York City at 73 Wooster Street. I was really expecting that an International Fashion Icon listed in an SEC Filing from one of the largest businesses the world would be up on Fifth Ave over by Tiffany’s, Prada, and the Trump Tower. Probably just that “new retail” concept kicking in.

I think it would be really interesting to know how much volume MSM, Moschino and Giuseppe Zanotti are doing at these flagship stores since, by definition, it must be material as these businesses are listed in the filing. But sadly, it wasn’t disclosed. Anyway, I don’t see stuff like this when I google Prada or Armani, so I suppose it couldn’t hurt to ask about it.

Wendy Huang, Macquarie: Two very quick questions. The first, your revenue growth is very strong yet the adjusted EBITDA growth was only the 13% this quarter. And given that you’ve mentioned the New Retail’s margin was structurally different from previous. So should we expect the EBITDA growth to stay at the current level for extended period of time? And second, very quickly, on your overseas strategy so there has been some new reports talking about US$5 billion investment in the Indian market, in the Reliance Retail. So can you give us update on your overseas expansion and investment? Thank you.

BST Translation: Hey guys I want to elaborate on Eddie’s question above re: the erosion of margins, but I’m going to coyly rephrase it as a reduction in EBITDA growth. How long is this going to go on and how bad will the margins eventually get? I also know that you don’t have any interest in Reliance India, but since your PR department keeps releasing these little nuggets to generate enthusiasm from Amateur US Investors, I at least want to hear you deny it in the Investor Call. (Note: Wendy clearly went off the grid on this one. She wasn’t copied on my email, is new to the group, and most likely won’t be invited back for the next call. It’s a shame, we’ll miss her.)

Alex Yao, JP Morgan: Okay. So number one, for the formation of the local service holding company, why do you want to seek external investors and the funding source? Number two, in light of the consolidation of Koubei, and more investment in Ele.me, can you talk about the financial impact in FY 2019 from this local service holding company? Thirdly, in addition to investments in Ele.me, are there any other areas that you think it will worth investing in terms of the local delivery? Thank you.

BST Translation: Yet another “Enhancement”? Softbank AGAIN? Other than the future write-ups and associated/expected future valuation gains, why do you need to get Softbank involved on a deal like this? I know Masa Son’s, ummm, “advice” will add all sorts of valuable insight to the transaction. He’s done an amazing job personally redesigning Sprint’s 5G Network on the back of a napkin, refrained from self immolation in public forums and no longer lies about his golf score, but that doesn’t make him an indispensable part of this fire drill. This type of consultation is, of course, not unprecedented. It happens all the time in China. As I recall, as a parallel to Western financial transactions, Al Capone routinely sought the counsel from both the Gambino and the Genovese crime families before ordering a “hit.” It’s important, in business, to look at transactions from different angles and build a consensus.

So What Happened Next?

As I mentioned earlier, it was a wild ride once investors deciphered the analyst-speak and took a look at the numbers. A $15 swing from top to bottom, and the fifth highest volume-day on record. Presumably, with $14 billion in shares traded in one day, people who knew what they were doing must have made a lot of money. Again, those who didn’t know what they were doing… didn’t.

Of course the SEC has all sorts of tools to monitor “suspect” trading activity, but even the most sophisticated software would most likely fail to detect a coordinated Whac-a-Mole offshore effort, funded by at least US$3 trillion of CCP money through thousands of various legal entities, protected by Caymans Banking/Privacy laws. I’m guessing that “Hey I’ve got a hunch” wouldn’t be probable cause for a Caymans/BVI Banker or CIMA Official to hand over records. The SEC might have been able to track and figure out what Bud Fox was doing with Blue Star, but I doubt they would get very far with Alibaba.

We also learned another thing, as I’ve opined in previous posts, since, when you are trading BABA stock and the Chinese Communist Party (CCP) has the other side of your trade, Thursday August 23rd has established and confirmed a benchmark. We now understand that the CCP, through Cayman’s and BVI Shell Corporations, will have no problem, going forward, supporting a share price on volumes of at least 80 million shares or US$14 Billion, on any particular trading day.

My guess would be, since this is a brilliantly diabolical CCP plan, that they have developed and maintain some sort of model that determines how many shares of BABA “they” own collectively throughout their Caribbean Professional Investor ecosystem. They will keep supporting the share price as long as they (in aggregate) can continue to generate enthusiasm from US Investors through their PR effort. They can “sell high” and “buy it back” at a lower price. If there ever comes a point where US investors aren’t participating at acceptable levels, the CCP will most likely cash out.

We can expect an increasing number of fantastic, incredible take-your-breath-away, not-to-be-believed-for-a-second press releases and statements from richly compensated interviewees extolling the virtues of Alibaba and the China dream, when, in reality, this is the greatest wealth grab and tool for capital flight/conversion in history. By Deep Throat IPO

In the best-case scenario, Alibaba is the goofiest, most convoluted, opaque, mismanaged accounting mess and business structure in history. Read… Alibaba’s 20-F Annual Report… Financial Comedy Gold!!

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The world is awash with low cost cheap and easy credit.

Especially to those first in the credit access line.

It will find some place to die.

If you want to speed read it, just skip to BST Traslations. I am sure Alibaba will be fine, and make a ton of money if they copy Amazon, and charge $10 for something that cost $5 at Home Depot (just a recent experience). Never mind the auction style price movements. /s

BTW, when is BABA coming to NA, and not just with a stock listing.

Any progress report on the CCP’s takeover of America?

How’s that vaccine scandal going? Or the P2P bust? You think that’s another CCP’s ploy? How about the recent outburst of Ebola? You think Xi is behind that?

Thanks Rates….really enjoy hearing from you…..So you thought that was a normal, every-day, transparent Investor Call? What did you find to be particularly informative?

When you speak about just Alibaba, I have the utmost respect. Seriously. No sarcasm. I want this company to blow, but then I also want Tesla to blow. I don’t care whether a company is Chinese, British or “name your country here”. Fraud is fraud.

But then you just have to bring in the CCP and how 3 trillion is somehow enough to do a variety of Mission Impossible plots. They can’t even use their bond holdings to threaten us because we’ll just swallow everything they sell. Heck Wolf himself made the same argument. I suggest reading a book called “The Party” to expand your horizons. It presents a more nuanced view of the politics in China.

Ok…. Thanks…….I’ll try to read it over the next couple of weekends…I always try to learn something when I can……this is the one? McGregor?

https://www.amazon.com/Party-Secret-China8217-Communist-Rulers/dp/0061708763/ref=sr_1_1?s=books&ie=UTF8&qid=1535571576&sr=1-1&keywords=the+party+china&dpID=51VjrKu7mdL&preST=_SY291_BO1,204,203,200_QL40_&dpSrc=srch

Even though I am personally sceptical of the claim that CCP is behind this BABA fiasco, I don’t think that deep-throat is suggesting it as a plot to destroy US. I believe it is suggested as a way of getting rich rather than destroying US.

P.S.:- I recommend watching documentary , if you haven’t already ,named “The China Hustle” which covers similar topic ,i.e. frauds committed by US listed chinese companies to dupe US investor (apart from BABA).

Not sure if you’ve had a chance to read the USCC Annual Report…..it’s pretty lengthy….I’ll probably do something on it in a future post…..but the Comission does a nice job of describing the CCP issues for the most part, although they’ve skirted what I believe is the most serious issue, the pegged currency & exchange rate…..thus the genesis of a future post.

https://www.uscc.gov/sites/default/files/annual_reports/2017_Annual_Report_to_Congress.pdf

Then there’s Josh Rogin’s recent piece….referencing the above..

https://www.washingtonpost.com/opinions/global-opinions/its-time-to-end-the-china-hustle-on-us-stock-exchanges/2018/08/30/50137c1a-ac8d-11e8-8a0c-70b618c98d3c_story.html?utm_term=.ac35a96e62de

And Marco Rubio’s response….

https://twitter.com/marcorubio/status/1035493152910704640

DT: Have you read or seen Ann Stevenson-Yang on Youtube?

She founded her firm that specializes in getting the real numbers out of China. I believe she was first to realize that electricity consumption was a way of checking on the 7, 7. 7. every year GDP growth. But now that stat is also manipulated.

She is eloquent on the SOE s and their ties to the CCP.

China is drowning in aluminum capacity. One plant tried to shutter but the SOE bank wouldn’t let it because it would have to report a loss.

Good point about electricity consumption. I’ve read that statistically every percentage point in GDP growth usually requires 3-4% growth in electricity production. With China growing at 10% for a decade or so, where does it leave the electricity production? This might, of course, be leveling off, but not for a rapidly developing country.

Always remember the Chinese economy behaves accordingly to a phenomenon somewhat similar to the Quantum Zeno Effect: you will affect its growth merely by measuring it.

Both the National Bureau of Statistics (NBS) and provincial governments seem to keep a very close eye on what foreign analysts say about specific sectors of their economy. Rail traffic, electricity consumption, container movements… each time a different indicator is found to behave differently than macro data it’s immediately “corrected”, even if this means different data from different departments do not add up. Literally.

The same applies to Chinese companies, both privately and State owned. What they engage into makes our non-GAAP, EBITDA and ex-bad-items antics look like childish pranks next to arson and armed robbery.

One particular thing that keeps on troubling me is how their iron ore imports keep on growing at the pace they do. In my opinion this has more to do with an ongoing qualitative (and possibly quantitative) collapse in domestic iron ore production than anything else, but here’s the astonishing thing. While we know that the average iron ore grade from Chinese operations collapsed rather spectacularly in the 90’s (meaning to increase production the way they did they had both overeploited high grade deposits and started exploiting commercially unsound ones), Chinese authorities have time and time again attempted to artificially reinflate it by either cherry-picking samples or flat out inventing data. Let’s just say their perfectly flat graphics do not look like those for, say, Brazilian iron ore. Or any iron ore mining operation on this planet.

I know Anne well…..I met her through a mutual friend and she actually inspired my writing on BABA when I was researching the stock prior to the IPO….I was actually considering buying some shares……until I dug into the filings.

Anne is sharp, educated, articulate, thinks outside the box and is doggedly relentless…..everything I admire in a person.

So if I understand it correctly than you are saying that BABA is a CCP vehicle to get rich by duping US investor not a conspiracy for destroying US. Though BABA clearly looks like a fraud , involvement of CCP seems a little outlandish. For reasons you claim CCP’s involvement?

Read more hallucenigenic “financial statements” based on fake data and false assumptions, signed off on by captured regulars and clueless auditors?

I can’t…I just can’t.

Priceless.

You need to update your translator to translate “shares” into “synthetic derivatives: check the internet for current definitions.”

As for the mumbo jumbo produced by the financial elites, it was exquisite in it’s incomprehensibility.

Full Disclosure: I recognized all three brands mentioned in your article. Two of them are still in my closet.

Thanks Petunia….I am not a fashionista…..never claimed to be…I’ve been roundly taken to task for it by Moschino and Katy Perry fans…..my point was that these “wins” (without figures) were far too small to be listed in a quarterly report of one of the largest businesses in the world (by market cap). It would be like Walmart announcing in their 10-K that they just signed on to stock Rolex watches and they expect to sell a few dozen a year….

Moschino is cool once more, was always too edgy for me, now too expensive to be mass market.

MCM is the most popular and mass market of the three.

Zanotti is a true hardcore fashionista brand.

All are considered luxury brands and can be found in high end department stores around the world.

getting clever and learning fast CCP.. playing an innovating game.

I recall the Canadian PM promoting to Canadian businesses to invest in Chinese businesses at an Alibaba event last year. He couldn’t be wrong or misguided, he is an art major after all.

Yeh right! FDR, Jack Kennedy Bill Clinton were also Arts majors as was Obama. & we have a finance major in the White House! Oh, did you know that Herbert Hoover was an Engineer!

I’d just like to bring to the attention of the Powers That Be that in the links provided above the Chinese Communist Party has morphed into Care Capital Properties Inc, a REIT… a delicious irony considering the Chinese government is possibly the greatest enabler of real estate bubbles in the history of mankind.

I am also enthralled, and I am not using this word lightly, by Alibaba’s operating financials. What new and revolutionary products are they developing to justify that insane increase in development costs? Perhaps they are studying some slick filter to avoid counterfeit products from showing up for sale on their websites?

Thank you, I’ll be here all week.

LOL LOL….I’ll be sure to tip the wait staff…

Nothing new about analysts experiencing great difficulty capturing enthusiasm, lol.

China is a huge economy though, it just seems likely a copycat Amazon has undeniable potential, given the circumstances.

Priceless, or fraud?

I read the other day a list of the top ten favorite stocks of hedge funds. Surprisingly apple was not on that list but

Alibaba was. After reading wolf’s article last week on Alibaba’s report my hair stood up just a bit….

Alibaba makes Enron look like amateurs. But don’t worry guys; Spain and or Italy are likely to crash before China.

Every single analyst except one was Chinese. Are only Chinese people allowed to cover Chinese companies? Or are all analysts Chinese these days? Just curious.

I’m sure it’s a coincidence and none of them have any ties to China.

The yantze tribe uses its worldwide tentacles to promote the potemkin village fraud that is China. Lies, fraud and theft permeates everything in their society – down to their food.

You mean to say people in year 2018 actually attend the investors’ conference calls and hear the analysts do meaningful work with their oral apparatus?

Ever heard the old joke, on why you call them analyst?

They are called ANAL-lyst for a reason. lol.

Look, if a stock market analyst or their fanciful analysis were any good, they would all have been fabulously rich, instead of still working in their ANAL-lyst job; which they know deep down within themselves to be self-evidently pointless.

The quarterly dog and pony show of analyst jousting with management has now become an elaborate oral performance elevated to a fine art of farting through their oral canal rather than the one mother nature intended. Pardon my language here, but I really can’t describe it in more accurate terms with the English language. lol.

Interesting article…And love the format. Question…Translation and significance…Skip the useless time-consuming BS response–Brilliant!

If only, only Deep Throat I could wake up tomorrow to find similar coverage written by you on Square (SQ).

Great format. One of the few times I have read with interest anything uttered by anal-yeses. Thanks

I’ll put SQ on my list….for now I’m focused on the big fish & saving Western Civilization….so much to do…..so little time….. :)