Refinancing activity plunges to the lowest level since 2000.

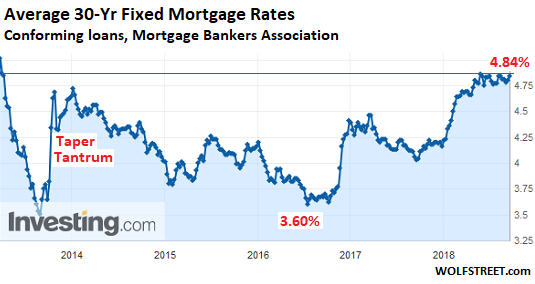

On its way to 5% and higher: The average interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) and a 20% down-payment rose to 4.84% for the week ending September 7, 2018, the Mortgage Bankers Association (MBA) reported this morning.

Mortgage rates – which move roughly in parallel with the 10-year Treasury yield – surged in two big bouts in this rate-hike cycle: First, from the near-historic low in July 2016 to March 2017; and after backtracking some, from September 2017 to mid-May 2018, when MBA’s measure of the average 30-year fixed rate hit 4.86%. Since then mortgage rates have vacillated in the same range – the highest since May 2011 (chart via Investing.com; red marks added).

The MBA obtains this data from weekly surveys of over 75% of all US retail residential mortgage applications handled by mortgage bankers, commercial banks, and thrifts.

The rising interest rates make it more challenging for potential homebuyers to be able to afford the inflated home prices prevailing in many US housing markets. These higher rates have already begun impacting the housing market, but only barely, and only at the margins. The real pain threshold is likely north of 5% and perhaps closer to 6% by the MBA’s measure.

But there is another impact of rising mortgage rates: Refinancing activity — whether as cash-out refinancing to fund some sorely needed consumption, or as an effort to lower monthly payments via a lower rate.

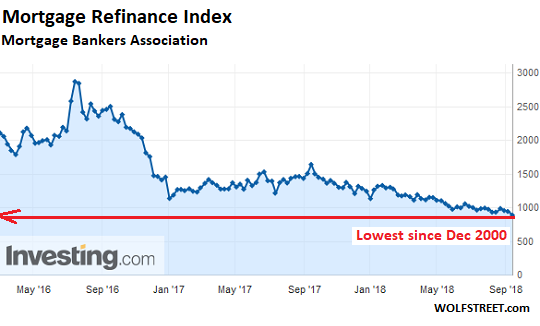

The MBA reported today that its Refinance Index, which covers applications to refinance existing mortgages, fell this week to the lowest level since December 2000. At 884, the index has plunged about 65% from the prevailing range in early to mid-2016 (chart via Investing.com; red marks added):

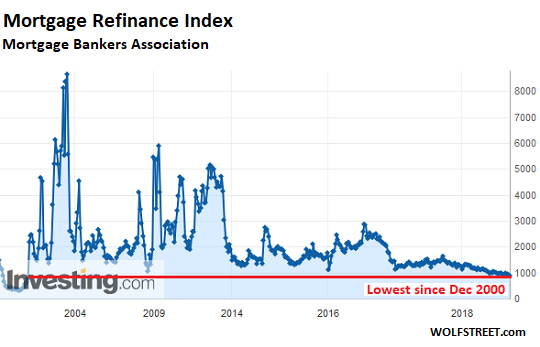

The chart below (via Investing.com) shows the long-term view of the Refinance Index going back to 1999. There are a number of factors at work to produce this type of spiky behavior, including:

- Refinancings spike when interest rates drop sharply or are low, in combination with rising home prices, such as in the post-2002 period leading to Housing Bubble 1 and Housing Bust 1.

- On the other hand, refinancings decline when interest rates rise.

- Broadly declining home prices also make refinancings difficult.

- Then there is the fear of approaching higher interest rates that motivates homeowners to refinance to lock in a lower rate before it’s too late.

This has implications.

For mortgage lenders, refinancing existing mortgages is a big and profitable part of their business. In the reporting week, the share of refinance activity versus all mortgage originations fell to a very low level, but that share was still 37.8% of all mortgage originations.

Wells Fargo – until last year, the largest mortgage lender in the US and now behind Quicken Loans, the largest of the “shadow banks,” – has been going through a series of layoffs in its mortgage units in response to the decline in refinancing activity. Other lenders too have trimmed their mortgage divisions – though purchase mortgage activity has remained stable.

For homeowners, rising rates make refinancing tougher. Cash-out refinancing, driven by surging home prices and low rates, has fueled some portion of consumer spending but is now starting to burn out. Refinancing to obtain a lower payment as mortgage rates have dropped over the past years has been helpful to household budgets. But this too is getting more difficult to pull off.

Even very gradually rising interest rates – rising slowly enough to where the economy can easily adjust without shock, which is the Fed’s stated plan – impact the economy in a variety of ways, in bits and pieces spread out over time. But eventually, homeowners, mortgage bankers, and all other participants in the economy can feel these rising rates.

How? Take a look. 9 charts. Red indicates the moves since the inflection point in June. Read… Anatomy of a Housing-Bubble Inflection Point in the Bay Area’s Sonoma County

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The big banks in fact seem to be licking their chops waiting for the crash. They stand at the ready to buy foreclosures and crash-priced stocks. One can only hope that sufficient QE-unwind has been accumulated so that banks will be prevented from benefiting to greatly from the crash.

It is also not fair that none of these bankers went to jail during the last crisis.

The problem is that if we jail some of these bankers, that will dampen the enthusiasm for the economy, and “kill the engine for growth”

Banks should do ok with rising interesting rates though. More returns loaning cash out to people.

Are you sure?

That’s what Democrats did in response to the financial crisis – not prosecute bankers during their 8 years in the Presidency, and the results were the weakest recovery of the last 70 years or so and the loss of a record shattering 1,000 elective offices of Democrats to deeply unpopular crazy people – all all time record in American history for a President of any party.

Results like can happen from just accidents, they usually require concentrate effort and deliberately crafted policy – against working people and for the rich and privileged.

The big banks are not in the business of buying foreclosures.

They may end up with a few foreclosures on their books (mainly from properties they haven’t managed to pack up and and securitize yet) but since the govt. has guaranteed nearly all the mortgages issued since the last crisis, then as long as they haven’t played shenanigans with appraisals, people’s incomes as such then Fannie, Freddie, the FHA or VA will end up eating the loss.

In any case, a downturn in the housing market is definitely coming but generally speaking, it won’t be as bad as the previous one for a whole host of reasons.

Max,

I think you will find that the coming downturn will DWARF the 2008 gyrations (which was more a market hiccup rather than a cold or maybe just a canary in the coldmine)….rather than be milder. Interest rates are now rising GLOBALLY while they were still falling before and after the 2008 crisis due to the manipulations of the Fed and other global central banks. The room for manipulation has run out (which is why the Fed has been raising rates the past year) without crashing the entire insurance industry and triggering the (inevitable) global pension crisis. Due to rising socialism (and destruction of family units which socialism promotes) over the past three decades, this pension crisis will trigger very large social unrest and gov’t upheaval and uncertainty….all of which push interest rates HIGHER.

With little labor rate inflation…people cannot afford the 40% of existing housing whose pricing expectations (by their owners) have been set under the assumption of 3-4% rates and gradually increasing housing prices….when in fact the only mortgages they will be able to obtain/qualify for are at 6-7% in an environment where housing prices are FALLING. This will cause the same seizing up of the employment market that the 2008 crisis did as people cannot AFFORD to move to where the jobs are being created because of the existing baggage of their underwater mortgages. CA and IL home owners are going to be especially hard hit due to the ridiculously high taxes and population and job OUTFLOW expected to be experienced in the next decade.

When it came to housing, the 2008 was most definitely not a hiccup.

Based on what the 10 bond is signaling, no way will prevailing mortgage rates reach 6-7%.

However, while housing values are more than 15% lower today (in real terms) than the 2006 high, the stock market’s value (again, in real terms) is more than 50% above the 2007 highs. So, I definitely agree with you on the oncoming pension crisis thing. It’s going to be severe.

One way states have been preparing BTW is by significantly reducing defined benefits for new pension system entrants since the early 2010s.

Wall Street landlords (REITs) are cronies of the Fed and are on the road to monopolize the entire real estate market

The banks don’t have the properties after 30-60 days. By then the financing is resold and they get the money back to lend again. They don’t benefit from foreclosures.

The Fed creates asset bubbles and then directs Wall Street Hedge Funds to swoop in and buy all the foreclosed properties after the bubble pops

If I were a lender, and someone wanted to put down 1/5 of the money to buy a house and wanted me to put down the other 4/5s, I ‘d want more than a 5% interest rate.

Is there a way to short granite counter tops, stainless steel appliances, European sports cars, vacations to Europe and boob jobs for the wife?

There were a few bankers that went to jail. Here’s one:

https://www.naplesnews.com/story/news/archive/2018/02/08/orion-ex-ceo-jerry-williams-sentenced-6-years-bank-fraud-case/320160002/

As to the increasing mortgage rates, there are many people in the US(me included) that have very low loan rates. As a result, they will stay in their homes longer. I believe the average length of homeownership has increased from roughly 7 years to 10 years. With a current rate of 2.5%, I am one of those people staying in my house.

Timothy, you have a lot of company.

I ran the numbers for some friends whose children have grown up and moved out, they are rattling in a house that’s much bigger than they need.

They bought at a good time and at a very good price, then refinanced (Rate/Term, not cash out) at a sweet rate.

Between Prop 13 and rates at 5% it makes sense for them to keep the place as long as they can keep it up.

Right now, if they sold and paid cash for a smaller place just the taxes would equal their current combined cost of the loan and taxes.

It’s California, enough said.

Depending on which county they are in, and the county they buy in, they may be able to carry over their real estate tax base.

The refi industry always seemed to me to prey on financially unsophisticated types that believe they’re really paying less by getting a new loan with a lower rate.

A new 30 year loan resets the amoritization schedule to year one where the borrower is again making a payment that is nearly 70% interest. Plus, fees. What a scam.

Besides, even in my neck of the woods where the median home is very expensive, changes in interest rates has been a matter of $100-200 more on a $4000-6000/month house payment. IMO, not enough to make someone with that kind of income balk.

You forget that you can also change the term in a refi. I refinanced my 30 year (with 23 left) to a lower rate and a 15 year term. Paying 100$/month more, but i’m paying 93000$ less in the long run.

Rock bottom interest rates drive prices up, higher interest rates will bring a Rice’s back down. It’s all about the size of the monthly payment.

I would like to see an interest rate and home price graph laid on top of one another to test that theory.

If this chart is anything to go by then it just looks like rates are slowly headed towards zero while house prices don’t want to do more than go sideways now

https://activerain.com/blogsview/4246663/mortgage-rates-affect-you

Notice that in the last thirty years rates have never been hiked more than a couple of % before continuing down. As rates near zero then there are maybe some other factors that might shift in… probably not though, you would have to look at… was it Swedish or Danish… markets where there is heavy state subsidy or guarantee …not remember what exactly… involved that sets a different picture.

…should read “in the last twenty five years”, not thirty years.

And notice that the author doesn’t even understand what the chart implies. Hilarious Realtor spin. Every day is a great day to buy a home. There’s something for everyone. LOL!

That is one of the advantages of searching a theme at random, you end up on all kind of sites and get a glimpse of different ideas and what people are making of any data. Now I am so used to this that I can place what school ( the great school of sales , the higher college of empirical state management etc.) each site falls into within the first paragraph usually, if not by just looking at the layout of the page…and I still find many of the sites amusing :-) .

Your instinct is correct Broker Dan. Monthly payment “affordability” predicts surprisingly little of subsequent housing price changes. There is an impact (of course) but not as much as common sense would tell us.

House prices are almost as sensitive to duration risk as bond prices. However the effect is somewhat delayed, and house prices are currently in a major bubble that will burst regardless of what interest rates do. The other question is how an interest rate rise will affect major holders of bonds such as insurance companies, pension funds and university endowments.

I know I’m an old fart, but I have to chuckle at articles that express concern of 5% mortgage rates. My first mortgage was in 1983 and it was 12 3/4%, and I was glad to get it. It was a private mortgage when most mortgages were 18%. I became a Realtor in 1986. At that time home loans were about 12%. The market was brisk, the economy was very good. Later, rates eventually came down into the high single digit range.

People these days have a short memory. They have become acclimated to artificially low interest rates, and freak out about anything normal.

The problem with higher mortgage rates this time around is the current price level of homes, inflated by historically low mortgage rates. An average rate of 7% on 30-yr fixed-rate mortgages is going to crush the housing market. Buyers will simply evaporate. Investors will disappear. It would be worse than the last housing bust. And that’s only 7%. My mortgage back in 1988 was 8%, and that was considered “below market,” offered by a failing bank to get rid of a property it had foreclosed on.

For a 30 year fixed interest mortgage, every 1% increase in the interest rate increases the principal and interest portion by 12%. That’s just math, and doesn’t include taxes and insurance.

Based on this, payments have already increased by nearly 15% since the low in interest rates.

Payments not including taxes and insurance.

Ya, 7% would be crushing to buyers. I know, I write mortgage loans for a living…..

Agree, although the 10-year bond is most definitely not signaling that mortgage rates will get quite that high.

Low rates allow high prices, at an extreme it would verge on perpetual debt by interest payment only on a total sum not likely to ever be repaid, basically renting from finance where first liability is on the owner due to the penalty of foreclosure and eviction.

If rates increase and prices drop, then many owners will go underwater, choosing bankruptcy and throwing more property on the market. That is a downwards spiral, traditionally you end up with dollar auctions! That affects even home owners who think they are pat, because depression may accompany this shrinking of money supply. I’ll post a view on that in a moment.

In the meantime these charts show how buyers leverage income to buy property – income/house price ratio. There are different sets that don’t match so I will include them all. Fortunately for US you almost all buy at fixed rates… in Spain for example they are mostly variable…rates go up and there goes anyone’s salary in repayment.

This is European data said heterogeneous to a degree to a wider set

https://voxeu.org/article/home-prices-1870

US and Canada

https://financialinsights.wordpress.com/2011/02/04/more-on-the-capital-economics-house-price-report/

However this data

https://www.longtermtrends.net/home-price-median-annual-income-ratio/

puts prices/income returning to the level of the fifties.

Someone more knowledgeable will explain which series is more correct maybe.

Test – just looking for a lost comment…

Nice try old fart .you might have had 12.75 % but you paid 40 000 for your house maybe less .today people are loaded to the hilt with debt on the cheap with high valuations the exact opposite of what you had .todays scenario has never been tried to the best of my knowledge and im sure the big boys have no problems raising interest rates for more monthly payments into their pockets but that was the plan all along ..?….load em up on cheap credit then come around the backside and raise the interest ..it’s almost as if it’s deliberately designed this way

Yep; not too hard to afford double digit rates when the amount borrowed is significantly less due to lower prices back then that are minascual compared to today.

Also; property taxes significantly lower as well as most other things that have skyrocketed due to inflation. Wonder what health insurance back then was for a family of 4? Today I pay 1500/mo + co-ins/co-pay/co-everything…….

My first job I paid nothing for my health insurance.. this was the Mid 90’s. When they finally got us to pay 10% it was $25 for the month in 1999.. this was for a single person. So quadruple that for a family.

Yeah, but old fart also made less money too. Don’t forget that.

The median home went from 2x family income to nearly 20x family income.

Back them, typically people saved as much as possible and bought a cheaper, smaller house with as little financing as possible. this “starter home” was lived in for several years at which point as their incomes and equity increased they would upgrade to a better house because they could pay for it.

Ummm, in what universe is the median home 20x the median income?

The median home (US$220K) is currently about 3.5x the median income (62K).

The upcoming housing market correction will drive this ratio to around 3x.

Max Power,

The median home price in the US in July was $269,600 (NAR).

In many cities in the Bay Area, $269,000 won’t even cover the 20% down-payment — and other cities are not far behind. Granted, the median household incomes here are around $100K. So a $1.4 million median home price, would be about 14x median income, give or take, depending on location. It’s not a different planet exactly, though sometimes it feels like it :-]

I paid $47,500 for a 3-family with positive cash flow, even though I borrowed the down payment, too. I had NO personal debt of any kind. The next year, I bought the house I was renting on a no-money-down, 5 year balloon deal with a mortgage heald by the seller.

About 5 years later I sold both at a very good profit. That was the Eighties.

It all fell apart in 1993 when my home mortgage was VERY upside down due to falling prices. I couldn’t sell or give my home away. Add in an expensive divorce. And then bankruptcy. Fun is…

Lesson to be learned–know when the market is going up, when it is near the peak, and when it is going down. Sell EVERYTHING before the peak. Rent a nice place and watch everything tumble around you.

How do you know the peak? This is the most important. Look at the median home price divided by median household income. This article explains it:

http://www.mybudget360.com/the-magical-2-housing-ratio-between-median-nationwide-home-prices-and-household-income/

All real estate is local, so the ratio will be different around the country. Find the one for the area you are in. It is not different this time. The prices always revert to the mean, as surely as gravity makes things fall down.

People starting a family have it most difficult. Usually they are buying with intent to keep, and as it is going to be long term home plus they want to “make it count”, they will look slightly above what they can afford. To access even anything just reasonable nowadays means you have to mortgage to a high level to just access the market. With stagnating wages many who bought earlier will be releveraging their houses like cash machines. I suppose that has placed a looooot of people in untenable positions if prices drop much, they will have no way out. Add to that that your plan to sell early (wise) will work for a small number of people, if everyone tried that prices would fall through. I can only imagine how many people have put off household formation because of the housing market.

In 1985, I bought a house in LA for $50,000. My entry-level salary was $45k. Like most people in those days, I would buy with savings, which would require 3 years to accumulate. Other people would buy with 90% down and take out a mortgage for the rest (10% of the price).

The interest rate on my savings account was 16%.

Historically, a house in any metro area in US cost 2X median income. That all changed in 2000, with the Fed’s “wealth effect” scheme.

“You should thank God for bank bailouts— absolutely required to save your civilization. So I think when you have troubles like that you shouldn’t be bitching about a little bailout. You should have been thinking it should have been bigger. You should thank God the government saved the big banks and their investors.

Now, if you talk about bailouts for everybody else, there comes a place where if you just start bailing out all the individuals instead of telling them to adapt, the culture dies. Suck it in and cope.”

Charlie Munger

It wasn’t the bail-out per se that angered much of the public; it was the attitude of our president at the time to let all the leading bankers off the hook when he and the leading politicians could have insisted on sharp haircuts for both CEO’s and their entourage plus the stockholders. It was a complete clusterf$#% of policy. The leading bankers went to Washington to meet with then President Obama girded for being taken to the woodshed and Obama gave them a chocolate sundae instead. A total disaster!

Charlie likes being a parasite. Luckily he isn’t young

Well. People are going to have to adapt.

https://www.svd.se/lilians-mardrom-det-ar-som-kafka

Lilian’s nightmare is that she has signed a contract for a soon to be built flat costing 4.5 M. SEK, planning to sell the one she is living in to pay for it.

Then the project company drop the price of the next lot of flats by 500 kSEK, the new amortisation rules come into effect (yes dearie- you really do have to pay off on the principal, no interest-only mortgage above 50% of the valuation anymore).

Her own flat of course is also not selling for 4 M SEK. So now she cannot borrow 4.5 million SEK and she has a contract for an appointment with a guaranteed 500 kSEK loss.

My question is: Why is a regular pensioner borrowing 4.5 millions on top of still owing 2 millions on her other home?

It’s like people are blind to their position.

One key point in Wolf’s article is the Cash Out refinance. Rising interest rates and falling house prices stop that nonsense. I know of a neighbor that did that multiple times and finally the house went into foreclosure. Said he forgot to make the payments. His parents are also doing the same cash out thing, it is public information in the county records, and using the cash out to live beyond their means. Another foreclosure in work?

ReFi ATM Machine. Is that healthy?

This is not occurring now or in the past few years.

HELOCs today go to 80% ltv, some local credit unions may go to 90% Max.

FHA 85% Max

Conventional 80-85% Max

VA was the only outlet that could go to 100% ltv.

So, no, people aren’t using their homes as ATMs bc you need to have a ton of equity left over. Oh, and don’t forget you must still qualify via income and credit.