A very crowded trade goes begging for a contrarian reaction.

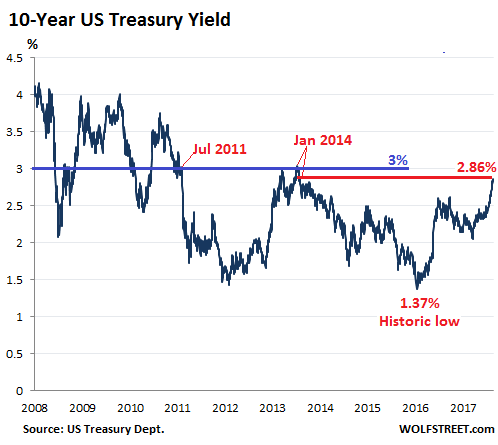

The 10-year Treasury yield closed on Monday at 2.86% the highest since January 16, 2014, after briefly kissing 2.89% during the day. At the moment, it is holding at 2.85%. Bond prices fall when yields rise – and being short the 10-year Treasury, and thus betting on a rising yield, has become a very crowded and profitable trade for hedge funds and other speculators.

Short bets in 10-year Treasury futures rose to 939,351 contracts, the most ever, according to Commodity Futures Trading Commission data through February 6, cited by Bloomberg yesterday.

This record came even after the market turmoil on February 5, when the Dow plunged 4.6% and when, briefly, Treasuries soared, with the 10-year yield dropping 13 basis points, which would have made shorts very nervous. But apparently, they hung on, as their record short positions through February 6 shows, when the 10-year yield rose again and closed at 2.79%.

The next step is 3%. The last time the 10-year yield was 3% was in early January 2014, and then only for a few days at the end of a brief spike. In May 2013, it got close, but no cigar (2.98%). And before then, it was at 3% in July 2011.

That 3% is a key level for another reason. At around 3%, the 10-year becomes very alluring for long-term holders, given today’s dividend yields and other yields, and it will bring out more buyers.

The emergence of these additional buyers may coincide with short-sellers trying to take profits, which may conspire to pump up the price and push down the yield. And this, fired up by speculators trying to get out of a short position, would turn into a sharp snap-back rally for the 10-year Treasury, and a sharp drop in yields. This could take off even before the 10-year yield hits 3%, and it could catch some speculators by surprise.

Tomorrow, those speculators will get to deal with the Consumer Price Index. If it comes in “benign,” it could trigger a buying spree of Treasuries with longer maturities and push down their yields. If it comes in on the upside, yields could jump on their way to 3%. For highly leveraged shorts, this will be a white-knuckle moment.

The chart above shows how smooth the one-way bet against the 10-year Treasury has been since September last year. The market, just when it gets this crowded on one side of the boat, is setting up for a downward jag in that smooth spike. With speculators suddenly switching sides, we could see some wild gyrations over the next few weeks.

But on March 21, the FOMC will likely announce the next rate hike and might give clues on what lies ahead. The yield curve has been steepening gently from its dreadfully flat slope late last year, and this is a trend I expect to continue; so in this scenario, over time, the 10-year yield would rise faster than yields of shorter maturities.

The fire under the 10-year yield will be fueled also by the Fed’s QE Unwind that has now accelerated and by the surge in new issuance of bonds to cover the ballooning deficits. These new bonds need to find buyers just when the Fed is whittling down its own pile. And they will have to have juicy yields to lure buyers into the market.

So I expect some wild gyrations that will likely give some shorts a bloody nose. But then, the 10-year yield will respond by rising slightly faster than shorter-term yields. And when it clearly and for good breaks above the 3% level, the 10-year yield will once again give confidence to shorts that it’s ready for the next leg up. But just because this is one of the seemingly most logical bets at the moment doesn’t mean it will be a smooth and pain-free ride.

The chorus is getting louder. But no one will be ready for those mortgage rates. Read… Four Rate Hikes in 2018 as US National Debt Will Spike

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The article references short bets on treasury futures being very crowded.

Futures, by definition, have an equal number of short and long contracts as they are issued in pairs.

If the short bets stand at 939,351 contracts, the most ever, then don’t the long contracts have to be the same???

Am I missing something??

Yes. The concept of market and price dynamics.

short bets can be hedges too.

playing the convexity fiddle and dancing the duration jig.

but the operative question is: should i lend uncle sugar money for 10 years at 3 per? he’s good for it, but he’s not the only game in town.

“Am I missing something??”

Sort of. The question to be answered – “is the fix still in?”.

This is the horse race. Today, it looks like no, but only a true believer in fair markets would put their own money down.

We are in the middle of a central bank bubble that affect the entire world. The fix not being in is like a floating pin searching for bubbles to prick. But, the fix can not last forever. The real bet is ‘are we reaching the end of forever now, or not’.

But, pricking one bubble, without a repair kit standing by, pricks all bubbles like slow falling dominoes. That’s the motivation to keeping all bubbles intact.

That’s the real question. It’s far more than a question of contracts and offsets.

Might be missing what they had to spend to get short and the price they get during an unwind

Unless the federal reserve are buying up the supply of debt and/or cutting short term Interest rates then they are a leech on both capital and labor!

What happens when the Fed is no longer monetizing debt who is going to buy all the U.S. Debt ??? Unfortunately that means higher rates to attract new buyers and with every 1/4 point $50 billion in interest will be added to our National Debt .

The new rate only applies to newly issued debt. I believe the average maturity of new debt issued runs about 7 years?

So any increase phases in over a very long time.

In other words, to put it in words my own brain understands, you recognize the “crowded trade” by the high price the people paid to get and maintain their position.

The crowded side of a trade doesn’t have more people but it has an unusually low reward for the price paid.

The case most people know well is betting on the favored horse at the track. Lots of bets (“crowded trade”) lowers the payoff/price ratio.

Bond buyers have options, if the perception is that yields are rising buyers tend to move down the curve to shorter maturities. The seller sets the yield which implies the level of risk. On those two counts higher rates might scare buyers out of the market, particularly foreign buyers who redeem their profits in a falling currency. Since government funding relies mainly on the 30yr the problem for buyers is can I collateralize these bonds, and is the stock market offering good returns? The Treasury can always intermediate the size of the offering, so they might be selling at a higher rate, but they aren’t selling as much. It’s a shell game and the ten year is where the right hand distracts you from what the left hands doing.

Either someone has a early look at CPI or credit is spooked about something more tangible? Credit is having a rough week and short credit is a kick in the solar plexus? The plumbing has been ripped out ? (Big blue has a full supply of cardboard boxes) Tax cut and a 4.4 trillion dollar budget? Speechless!

I wouldn’t short ANYTHING in these “markets”. I think the smartest thing I’ve read all week is:

But then, why even have markets? Why can’t(fill in central bank) just set the price of each (fill in the product) and make it go up at regular intervals, at a (fill in rate or price) deemed to be appropriate by authorities? It would offer true risk-free investing in (fill in product). It could become a national wealth builder.

There will also be supply from Uncle Sam looking to cover its deficit and to refinance its existing debt. With the yield curve flattish, the treasury may look to issue more longer dated debt. Fed is not selling anything but it is not buying anything either.

Greenspan said recently that in 500 years of Bond Yield history, interest rates have never been so low.

https://www.youtube.com/watch?v=h4iuwK4DL0k

So the shorts may be on to something.

Sell the tax cut and buy 100 year treasury bonds? Sir you are genius!

Neither the Fed’s balance sheet nor this economy can withstand a sustained rise above 3% (let me just say 4% is way too high) on the 10-yr.

The Fed doesn’t “mark to market” the Treasury securities it holds. And it gets rid of its Treasury securities by allowing them to mature, at which point it gets paid face value for those Treasuries by the US Treasury Department. It could make a loss if it acquired those securities in the secondary market during QE at a premium and then would get paid face value when they mature. Its loss would be limited to that premium. Overall, this is not a huge risk for the Fed. Also, since it can create its own money, it cannot go broke.

So far, its portfolio has been very profitable (which is easy to do: print your own money and invest in Treasuries). Most of its profits get remitted to the Treasury Dept. For 2017, the Fed remitted $80 billion to the US Treasury:

https://wolfstreet.com/2018/01/10/fed-pays-banks-30-billion-on-excess-reserves-for-2017/

Why short the ten year when the thirty year’s duration is longer and hence by theory the price moves should be more violent?

bond volatility= duration/(1+yield to maturity)

Anyone?

“Greenspan said recently that in 500 years of Bond Yield history, interest rates have never been so low.”

This man is responsible for pulling demand so far forward we could see the backs of our heads on the distant horizon. I pray for the day he and his globalist business partners rightfully receive credit for tipping the scales of climate change.

“This man is responsible for pulling demand so far forward we could see the backs of our heads on the distant horizon”

As we age, we want people to remember us as we wish we were and not as we actually were. This is Mr. Greenspan’s motivation today. He, Bernanke, Yellen, their international counterparts, and perhaps the new bunch at the Fed will have to deal with History. Since some are probable sociopaths and some were academics who were educated far beyond their intelligence, distant History will probably see them accurately.

Hopefully, the new bunch at the Fed will do what should have been done in 2010 and normalize US finance. Had they done this in 2010, the world would be a more idyllic place today. The fix today will cost much more than it would have cost then, but it will be far less than if the bubbles continue to grow for a few more years.

Poltergeist bonds?

@cdr

“He, Bernanke, Yellen, their international counterparts, and perhaps the new bunch at the Fed will have to deal with History.”

They will probably be referred collectively as “MONETARY GANGSTERS” or “MONETARY MAFIA” in the history books.

Instead of guns they used interest rates and control of money to create economic destruction, not to metion usurping of powers they did not have without a by your leave. For me, the surprising element is they are able to get away with it.

“to create” should have been “for”

If the DOW will start to crack, that will determine the fate of

the 10Y, not the Fed, or speculators.

:(yep)

We will most likely have rate hikes for at least two years counting this one. And the FED will continue to make their imaginary money disappear This and next year will probably be horrible for those with debt So a lot of zombie unicorns might finally die for good or be bought.

Then again the only zombie unicorn that might be worth to buy is Twitter.

Or maybe not since the company rep is down the drain thanks to russian bots, revenge porn and so on.

Although the reputation is still way better than Uber, so that’s something.

Amazon might have trouble due to all the debt their took but is likely to not die soon unless they takeover of the Brick and mortar Food business goes horrible wrong.

Nextfix is very likely to have serious cash issues by the end of the year.

Uber… well I have no clue when will they finally die.

Facebook and Google are doing well. Although Facebook is losing not users, but the time expend using it is decreasing because no one will a brain takes it as a place to get news anymore. So people is visiting other places for that.

Google smart phone project seems doomed but Microsoft videogame console project was doomed and then came the Xbox 360.

Google can afford a few years of loses in the phone market like Microsoft did with the original Xbox when it comes to videogames.

And Bitcoins or at least Monero will eventually be banned in the US due to mining it literally melting phones. And government computers worldwide getting infected with malware that mines bitcoins.

I’m trying to picture this as imbalances.

The government needs a lot more capital than it did even last year and it has to come from somewhere… Not out of thin air as the rules are that it has to borrow its capital, not just run a printing press.. The FED says it is not only not going to help out but is actually going to reduce its holdings of notes.. Making the imbalances even greater..

AND the government’s need is ultimate.. It will pay whatever it has to in order to get capital. Right?

I am holding stocks that pays around a measly (according to google) 2.2% dividend. But I own stock because they have been going up in price.. Asset value increase has been much greater than dividends. Good for me..

Now the government needs capital and it has to come from some where… Where is the most logical place for that capital to come from? Not real estate, not existing bonds, not savings.. so from the stock market.. Unless it can get foreigners to loan our government capital on the cheap at a sufficient amount as to maintain the balance..

So shorting the treasuries makes lots of sense.. Maybe shorting everything makes sense.

What happens if the capital comes from foreign CBs or even foreign SWFs? Or even wealthy foreign investors. Is that possible/probable? I mean we’re talking over a trillion$? Would that affect our balance of trade making our GDP greater? Make us look like we have a bigger and stronger economy than we actually do?

So much to know and understand…

Mildly off topic but should be noted: Many media reports are taking quotes from the Jerome Powell (new FRB Chairman) ceremonial speech today out of context.

“We will also preserve the essential gains in financial regulation while seeking to ensure that our policies are as efficient as possible. We will remain alert to any developing risks to financial stability.”

The 2nd sentence has been oft quoted. The 1st sentence is essential. Powell is talking about financial regulations and their impact on market stability. He is not invoking the prospect of valuation-based market intervention.

Thanks. I’ve noticed that too. It’s like they’re trying to force the “Powell Put” on him. Glad I wasn’t the only one … for a while I thought I was going nuts.

Danielle DiMartino Booth feels that Powell is no pushover. The real test is when market starts falling. At least he refrained from saying anything during this market tantrums.

Jim Rickards has an article on just this topic, he feels Powell won’t ‘taper’ on the rate hike policy and that markets would have a ‘tantrum’. Buy gold as always blah blah

[there is a lot more at work here, trying to assign blame for the pullback which ignores global liquidity and tepid economic growth should be considered as the real reasons]

I think people misimterpret the role of the treasury market.

During the Clinton years, the entire financial system of the world changed. The treasury department started to issue short duration bills , just as Clinton undid Glass-Steagel.

The purpose was to create a bill that could be used as a defacto trade nore, similar to trade notes that used to be issued by merchant banks. This new note was called a “reserve currency,” It’s value was that it could be used as a trade note between the US and say, china, then china could use it with Indonesia who could use it with Singapore, yada yada.

The thing was, this could only work if the US ran trade deficits and in fact, Bernanke said so on many ocassions. The Fed then created , an inflation guage that was detached from the cost of living. Today, housing, food and health care are not parts of the cost of living.

This gave them the ability to run inflation at 5% per annum abd call it 2%. Today, the average person can’t afford a house, car or health insurance and yet, inflation is under control.

In 2009, the Fed did it’s bailout. This had nothing to do with jobs, or wealth. It was to create asset inflation to keep the banks solvent. This is why they created maiden Lane securities, an illegal fund, annouced a “backstop” to fannie and freddie.

Tomorrows inflation number, like all of them, will be a fantasy. They will probably keep it benign to make their exit from the treasurymarket smooth.

>>The purpose was to create a bill that could be used as a defacto trade note, similar to trade notes that used to be issued by merchant banks. This new note was called a “reserve currency,”

This is outright incorrect. From treasurydirect.gov:

The first bill issued on a regular basis was the 13-week bill, beginning in December 1929.

By 1972, there were regular issues of 13, 26, and 52- week bills. Cash management bills are issued to bridge seasonal low-points in the Treasury cash balance. They were first introduced in 1974 to raise cash for a few days or several months. Four-week bills were introduced in 2001.

—–

Further, the word “trade note” is not in common usage. And the concept of a “reserve currency” existed long before 1992. It simply means the preferred currency for debts and payments. Banks from almost all countries keep a significant amount of their reserves in USD because reserves are the currency of interbank payment settlement.

The rest of what you say is not too far off from reality, but the other inaccuracies really detract from your credibility.

The Fed is attempting to engineer a “soft” transition in rates. Ultimately, they want money to come out of the stock market and into bonds and higher yields will certainly encourage that. It just needs to be orderly and the Fed has plenty of behind the scenes tools to accomplish that.

Those shorting either market will have their heads handed to them on a platter if the need arises.

10 year will settle around 3%, Anything over that and the economy tanks. It might very well tank at 3%; although the plan is to stimulate with higher deficits (fiscal policy).

There is a possibilty that the Fed is on the side of “crash Trump”, in which case disregard the above. I consider it small but definitely possible. There is a powerful force in D.C. that wan’ts Trump out sooner than later.

The major problem with going short or long is getting the timing correct. You can get the direction 100% correct but still lose your shirt.

If everybody decides to lean to one side of the boat at the same time, the manipulators simply change the timing. If that doesn’t work, they simply use their power to change the rules of the game!

Completely agree that Inflation numbers accepted by the Fed, and what the middle class is experiencing are detached. On most financial outlets seems like there is a big push for wage growth. A mixology of gender gap issues, lower class suffering and tighter labor market.

Do any of you see a way, for the fed to turn this real estate and stock bubble into a “new normal”? The only way to keep these assets up, is to increase peoples earnings. Personally, i believe if wages go up, unemployment will increase unless earnings somehow increase as well but on a recent interview Greenspan commented he didn’t believe in the Phillips Curve (could have been meant sarcastically). Is it possible for the gov to put the last nail in the “saver” coffin? They already stripped deposit/savings yield from us.

Inflating the cost of living could also save them from addressing pension insolvency, social security and other gov programs. I hope that eventually people who have saved and are conservative with their earnings will be recognized, but hope and reality sometimes don’t go hand in hand.

Interesting article as ever.

It would be beneficial to know which yield rate spells serious trouble for America Inc.

National debt is the accumulation of budget deficit. America’s national debt currently stands at $20.6 trillion https://www.usgovernmentdebt.us/

If bond yields hit a given percentage, how much of $20.6 becomes unsustainable?

As yields increase, more and more taxes have to be ringfenced to pay the interest on $20.6 trillion debt. This means that services which are tax funded cannot be provided unless more taxes are created and/or higher rates of taxes get applied.

So at what yield is national debt sustainable/unsustainable?

Right as The Bond Market & Dollar were going south for them last year, the Controlled Opposition convinced everyone to get into Crypto’s – Which They Then Crashed.!!!!!

It should have been Silver & Gold shooting to the Moon – Not Crypto’s.

Silver is an Asset that is way Undervalued compared to the other Metals that bypassed their 1980 Highs

What Changed on September 8, 2017

https://www.sgtreport.com/articles/2018/2/14/what-changed-on-september-8-2017-craig-hemke

“Three new recently published scientific papers seem to confirm what many have claimed for years: the “efficient markets” are not only

inefficient – from an informational standpoint – they are also badly

rigged.

Of the three papers, the Economist reports,

one argues that well-connected insiders profited even from the

financial crisis, while the other two go so far as suggesting the entire

share-trading system is rigged”

https://www.zerohedge.com/n…

John I agree Silver is WAY undervalued I own quite a bit and I’m buying more here