At taxpayer expense: easiest, risk-free, sit-on-your-ass profit ever.

The Federal Reserve’s income from operations in 2017 dropped by $11.7 billion to $80.7 billion, the Fed announced today. Its $4.45-trillion of assets – including $2.45 trillion of US Treasury securities and $1.76 trillion of mortgage-backed securities that it acquired during years of QE – produce a lot of interest income.

How much interest income? $113.6 billion.

It also made $1.9 billion in foreign currency gains, resulting “from the daily revaluation of foreign currency denominated investments at current exchange rates.”

For a total income of about $115.5 billion.

Those are just “estimates,” the Fed said. Final “audited” results of the Federal Reserve Banks are due in March. This “audit” is of course the annual financial audit executed by KPMG that the Fed hires to do this. It’s not the kind of audit that some members in Congress have been clamoring for – an audit that would try to find out what actually is going on at the Fed. No, this is just a financial audit.

As the Fed points out in its 2016 audited “Combined Financial Statements,” the audit attempts to make sure that the accounting is in conformity with the accounting principles in the Financial Accounting Manual for Federal Reserve Banks. Given that the Fed prints its own money to invest or manipulate markets with – which makes for some crazy accounting issues – the Generally Accepted Accounting Principles (GAAP) that apply to US businesses to do not apply to the Fed.

This annual audit by KPMG reveals nothing except that the Fed’s accounting is in conformity with the Fed’s own accounting manual.

Here is what the banks Get:

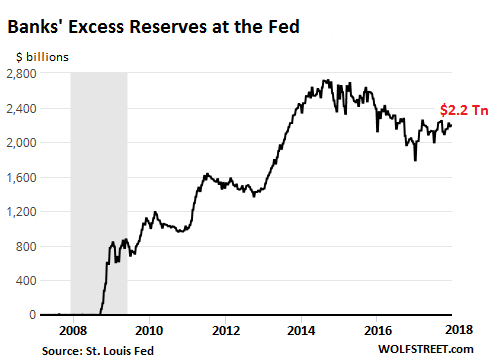

The Fed pays the banks interest on their “Required Reserves” and on their “Excess Reserves” at the Fed. Excess Reserves are the biggie: As a result of QE, they jumped from $1.7 billion in July 2008, to $2.7 trillion at the peak in September 2014. They’ve since dwindled, if that’s the right word, to $2.2 trillion:

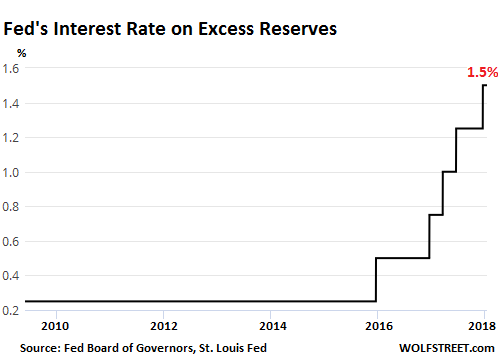

When the Federal Open Markets Committee (FOMC) meets to hash out its monetary policy, it also considers what to do with the interest rates that it pays the banks on “Required Reserves” and on “Excess Reserves.” In this cycle so far, every time the Fed has raised its target range for the federal funds rate (now between 1.25% and 1.50%) it also raised the interest rates it pays the banks on “required reserves” and on “excess reserves,” which went from 0.25% since the Financial Crisis to 1.5% now:

So the amount of excess reserves has fallen since 2014. But the interest rate that the Fed pays on them has been ratcheted up since December 2015. And so has the amount that the Fed pays the banks. In 2017, a year with three rate hikes, the interest that the Fed paid the US banks and foreign banks doing business in the US jumped by $13.8 billion to $25.9 billion.

That $25.9 billion is the easiest, most risk-free, sit-on-your-ass profit that banks ever made in the history of mankind. More on that in a moment – particularly out of whose pocket this comes.

The Fed also paid banks $3.4 billion in interest on securities sold under agreement to repurchase.

What else needs to be taken care of?

The 12 Federal Reserve Banks cover their own operating expenses of $4.1 billion. Plus, there are these items, among others:

- $724 million for the costs related to producing, issuing, and retiring currency.

- $740 million for expenses associated with the Fed’s Board of Governors.

- $573 million to fund the operations of the Consumer Financial Protection Bureau

Oh, and the dividend…

The Fed paid $784 million in statutory dividends to the financial institutions that own the 12 Federal Reserve Banks.

US Treasury gets most of the rest.

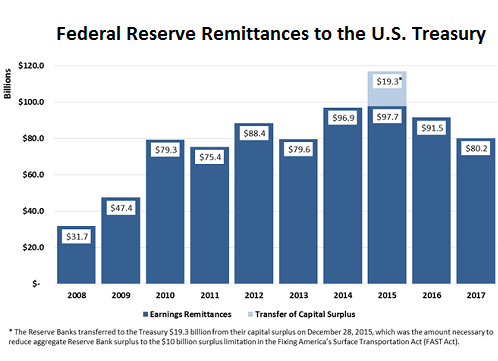

After everything has been taken care of, the Fed had a net income of $80.7 billion, which is tax free, of which it remits an estimated $80.2 billion to the Treasury:

In the chart, note how the surging interest payments to the banks slashed into the remittances to the Treasury. If the Fed hadn’t decided to pay interest on excess reserves, to benefit the banks, it could remit this money to the Treasury. In other words, every dime the banks receive comes indirectly out of the pocket of taxpayers.

The Fed will likely raise rates further this year. There is talk of four rate hikes. This would push the rate on excess reserves to 2.5% by the end of the year. Excess reserves will likely shrink as QE is being unwound, but not fast enough. And the amount that the Fed pays the banks this year might surge to $40 billion or more — a glorious and hidden subsidy extracted from taxpayer pockets.

At the same time, the Fed is shedding its income-producing assets as it unwinds QE and will make less income in 2018 than in 2017. With less money coming in, and paying more to the banks, the amounts remitted to Treasury and therefore the taxpayer will likely plunge. But at least megabank CEOs will be happy. Ka-ching.

First decline in the Bank of Japan’s colossal balance sheet since 2012! Read… QE Party Over, even by the Bank of Japan

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

They get paid $30 billion on “excess reserves” for 2017? That’s a heck of a deal. Where can the hoi polloi sign up?

The banks own the Federal Reserve, that’s the way the system works.

From the feds own: https://www.stlouisfed.org/In-Plain-English/Who-Owns-the-Federal-Reserve-Banks

The fed never gets audited, so do you think the people of the US would benefit in any way?

MikeB –

That link that you posted is put out by the Fed itself. It’s self serving.

It would like you to believe that the Fed is government controlled.

It is not. It is a private for profit organization.

Exactly

Thank You OUTLookingIn!!!! It never ceases to shock me how clueless people are still to this day, that the FED is a private For Profit Organization, total conflict of interest with the American Public…..Just who is Fused and who interests do you have at heart MikeB@Fused?

Dude, the banks ARE the Federal Reserve

Begin by applying for a bank charter. You’ll need some capital, which probably excludes the less entrepreneurial hoi polloi, but it is entirely feasible.

Who actually represents the people in this country of ours ? Anyone ?

We ARE the 99% ! When will WE hold THEM accountable ?

Got an action planned?

I know a few million interested.

Do they have lots of guns and ammo? We could put together an action plan.

VERY good question Bobby Probably not for awhile

Do community banks participate in this program? Or is it just for the ones that do things like treasury auctions?

The correct terminology for what you are trying to express are

1. primary dealers (PD)

The banks that are primary dealers are a very small number, around 23 at the moment.

https://www.newyorkfed.org/markets/primarydealers.html#primary-dealers

2. federal reserve system members (FRSM)

There are ~2400 of FRSM banks, but there are even more non-member banks, including many banks that perhaps one would call “community banks”. Worthy of note is that any bank that is a “National Bank” must also be a FRSM bank.

I could not find the exact number of FRSM banks, but wikipedia has an older figure from 2008/08/14 which is 1574+877 = 2451 FRSM banks.

https://en.wikipedia.org/wiki/Structure_of_the_Federal_Reserve_System#Member_Banks

The surprising thing is that half of the PDs are subsidiaries of non-American banks. Wonder how separated they are from the head office, e.g. it makes sense to BNP Paribas to keep excess reserves with the FED rather than ECB.

RRPO throws a net over ALL lending between banks, this is why the Fed chose to use it. Its a tool of financial repression, or a sort of deux ex machina. It’s been suggested that we might do a number on gold, set the price at $5000 (promise to buy all gold at prices lower than the threshold) and then back the currency. To me they might do better to defend the dollar in that way. Desperate measures for desperate times by desperate men.

Yes, community banks do participate in this. My bank held excess reserves at the KC FRB due to a rash of loan payoffs (our clients had a profitable year), and we used those balances to enhance our safety and liquidity. It detracted from our profitablility because we would rather have loans at, say, 4.5% than the 1.5% we got from the FRB.

“statutory dividends”

Paid to the “owner’s of the Federal Reserve Bank, who own the Fed stock.

And just who are these owner’s? No one knows. They are secret.

Oh, and about those “statutory dividends”? They are paid at a rate of 6 percent, plus they are indexed! In other words, they get a cost of living inflation allowance! How’s that for rubbing salt a into wound?

All the stock is owned by the member banks. This is not a secret. The FRB is ruled by its charter, a document you can find on the internet.

Petunia –

Yes. That is the stock answer that is trotted out each time the ownership question arises. But WHO really are the owner’s?

To say the “banks own the Fed” does not really provide an answer to the question. That is saying other institutions own a particular institution. So who is behind these institutions? Who are the major stock holders? What are their names?

The answer to these questions will prove ‘conflict of interest’ at the very least and most probably, criminal financial behavior at the worst.

This is why this information is a tightly held secret.

Here’s the super secret federal reserve stockholders formula for allocating federal reserve stock to member banks:

https://www.federalreserve.gov/aboutthefed/section5.htm

Petunia –

The “Section 5” link that you posted, put out by the Fed, is nothing more than terms and conditions of stock purchase/ transfer. It answers nothing.

Look dude. Petunia is right, and her link answers the question. The stock ownership of banks (and therefore the Fed/FRB) is no more or less secret than the ownership of any publicly traded US corporation, be it Microsoft, General Motors or Bank Of America.

The problem is not exactly who the owners are, but that the FRB generally puts the interest of the owners/banks ahead of the interest of the people. You do not need fancy theories about secret owners to know that, and in fact you are detracting from the argument by turning it into a conspiracy theory when it is in reality a conspiracy FACT. All the evidence indicates that FRB cares much more about WallSt than about MainSt. Stop muddying the waters by insisting that not knowing the name of every big shareholder of every bank is somehow essential. Yeah, sure, it would be fun to know, but it is not essential.

Mister Justme –

http://www.en.wikipedia.org/wiki/History_of_the_Federal_Reserve_System

I have to believe most folks are honest and they don’t intentionally HARM other people. On the other hand, the FED and the member banks have done much harm to so many people. Really sickens me to see so many panhandling at intersections. I have to believe there is a special place in hell for these folks in “crony finance”. Brings to mind one of the messages from Fatima: “If men only knew what eternity is, how they would make all possible efforts to amend their lives . . .” noodle on that one for a while.

When millions of American jobs were being shipped to China, no one at the Fed cared how China was financing such an expensive operation. Millions of families suddenly having no income was not the Feds concern, because the banks were making big profits helping China out. It didn’t become a crisis for the Fed until American bankers started to suffer.

After QE unwind taxpayers will no more pay interests on excess reserves, and will no more get the interests from bonds. They will not be better off. Am I right?

Sounds about right. QE unwind reduced the excess reserves dollar for dollar.

When will Americans get sick of private bankers ruining their lives and being above the law or any audit ( thanks Ms. Warren …).

The money (gold?) is ours, not theirs . Why is the Fed owned by the War Party Of The Rich (Demopublican and Republicrat multi- millionaires and their banker friends).

Why is the Fed above the law, or any audit?

Because honest politicians stay bought. Otherwise they get smeared and replaced by people who understand loyalty.

Marco, I have a feeling the Fed has been shovelling money into China to help out its banks too, because if China’s banks go, so do American and European banks. There might be a slight public relations problem if people were to find out that their money was being used to prop up China, which is in the shape it is because of the way it financed the “insourcing” of so many American jobs.

The banks worked hard and took big risks to earn that money. It’s easy for lazy people to be jealous of somebody else’s success.

I’m taking the libertarian line here. Did I get it right? I’m new at this.

If not, I’m sure there’s an easy way to dismiss it as fake news.

So let’s see, since only about half of folks pay federal taxes, I guess the half that is sitting on the wagon is not too sympathetic to the other half that is pulling the wagon. If 10,000 baby boomers retire each day, and are hopping on the wagon, it’s going to get much harder to pull.

Add to this scenario several increases in interest rates, and you compound the problem, unless you are willing to fire up the printing presses….but wait, no need to print paper when you can just pay interest to the banks on their “reserves”. I always wondered how the fed would deftly add money to the economy, knowing that dropping it out of helicopters was just a metaphor, but now we know. Thank you Wolf.

The latest news is that China may abandon purchasing US govt bonds. Looks like they have figured it out sooner than the wagon pullers.

Hey Wendy I thought us Boomers had paid into a fund and therefore we did our own “pulling” during our working years Where do you get off saying we are a burden just because we want what we were promised and paid for Give it a Rest will you

you would be misinformed if you think that lowering taxes and financing wars on your childrens backs were doing your own pulling.

“I guess the half that is sitting on the wagon is not too sympathetic to the other half that is pulling the wagon.”

Are you comparing the workers who enrich the wealthy to draft animals, or is this a cryptic reference to the Panama Papers?

I’m talking about the workers who pull along the entitled slackers who have no assets, but are still voters, and often speak with the most decibels.

I should not criticize the wagon riders, since I am getting ready to ride, and I weigh a ton, with my part D meds, and my non-means-tested Medicare benefits. Wheeee haw! Pull harder you indebted college graduates!

Just kidding. I have the means, but clearly the system is broken, we just haven’t seen the brunt of it yet.

Libertarians and Conservatives (versus what we call RINO Republicans) are opposed to the government picking the winners and losers.

Remember Bernie Sanders voted with the Freedom caucus against the import-export bill that provides a subsidy for large companies. It was the Freedom Caucus and Bernie Sanders vs rest of Republicans and Democrats.

Nothing like a little libertarian-bashing, eh?

Turn the clock back to November 1910 at Jekyll Island where Senator Aldrich, President Wilson, Mr. Warburg, House, Morgan Vanderbilt, Schiff and Rockefeller got together and engaged in a duck hunting excursion (wink, wink-nudge, nudge).

Then, in 1912, three prominent bankers named Benjamin Guggenheim, Isa Strauss and Jacob Astor drowned in the Atlantic when the Titanic sunk. These three men had opposed what was in the works from Jekyll Island, and their deaths cleared the way for Congress to move forward.

The Federal Reserve Act was passed by Congress in 1913, and signed into law by President Wilson, but there was one little glitch for permanent control. A twenty-year charter was included in the original Act just as in 1791 for the First Bank of the United States, and in 1816 for the Second Bank of the United States.

That charter was set to expire in 1933, but on 25 February 1927, Congress solved this by amending the Act of 1913: “To have succession of the approval of the Act until dissolved by Act of Congress, or until forfeiture of franchise for violation of law.”

Got that Walter? Only Congress can dissolve the Fed, and it’s been written in stone that way for over nine decades. If the Libertarian party could break the two party duopoly in Congress, there’s a chance that the issuance of currency could be returned to the Treasury, but until then, we are, fiscally speaking, all pawns in the hands of the global banking cartel that runs the BIS, IMF and the Fed.

P.S. On 4 June of 1963, President Kennedy signed Executive Order 11110 which authorized the Treasury to: “Issue certificates against any silver bullion, silver, or standard silver dollars in the Treasury.” This gave the U.S. government the power to issue currency without going through the Fed.

Dan –

We all know how that turned out for JFK.

“Nothing like a little libertarian-bashing, eh?”

A mallet won’t work on this site.

“If the Libertarian party could break the two party duopoly in Congress, there’s a chance that the issuance of currency could be returned to the Treasury”

Replacing bankster pirates with libertarian pirates. Now that’s ambition.

Dan,

You are one of the wise ones here. I enjoy your posts. I used to be a Libertarian until I finally started delving deep into economic and political history. This may be of interest to you.

https://www.salon.com/2014/05/18/libertarians_reality_problem_how_an_estrangement_from_history_yields_abject_failure/

Thank you for the compliment. I consider myself to be a Moderate Libertarian, and I agree that the ‘mainstream Libertarian party’ is a bit (OK, maybe quite a bit) off the deep-end.

We do need federal, state and local governments in order to function as a society without total anarchy. I live a few hundred meters from Minneapolis Fire Station 21, and I’m damn glad they’re close by, and I happily pay for them through my property taxes. Also, we do need to have safety-nets to take care of those who’re unable to do so themselves.

However, the U.S. government is broken and corrupt. Bill of Rights? Nah, we need to give up liberty and freedom for the sake of fighting the never ending war on terror. Speaking of wars, when will the next ‘War of Lies’ occur? From VietNam to our current military occupations of Iraq and Afghanistan, the NSA and MSM have pushed us into conflicts that have killed millions of innocent human beings – with your tax dollars paying the way.

Attorney General Jeff Session’s war on legalized cannabis, both recreational and medicinal, is another example of this nation’s corruption and persecution of liberty.

The list goes on, but as Wolf has reminded commenters, this website is about business and finance, not politics. The Fed is a political creation though, and its continuance which is set to be forever unless Congress dissolves is also in the realm of politics as much as finance.

I was a libertarian too! Then I realized that it meant liberty from government but slavery to the market.

Yes, the FED is a creature of congress. And congress, my dear friends, is a creature of US. The unfortunate truth is that it is not the “banksters” ultimately that are the problem, it is us. No one wants to be forced out of their “lifestyle”. A central bankers job is printing money – loaning it to government. We stop that, then a whole lot of people may have to live within their means, and that would last about 2 days until everyone would scream about their “entitlements”, “lifestyle being effected” etc. The creature from Jeckyl Island is ultimately our greed, and lack of financial education, which is simply exploited by those in control.

30 billion right off time top before Walmart gives its supervisors and greeters a grand just to stand around? That is OK because I got this store exactly were I want it , shedding over paid pole scanners!

If one thinks about it, the banks should be paying the Fed for the risk-free storage of their fiat in demand accounts there.

My bank pays transaction fees to the FRB system monthly. Every check that clears, every ACH that posts, and fees to access the payments system itself. FWIW, the fee schedule is posted on the FRB’s website.

My comment was wrt risk-free fiat storage at the Fed. Imagine how popular bank robbery would be if banks had to store all of their fiat in physical form? So why are banks allowed to store their fiat FOR FREE, much less receive IOR (interest on reserves), at the FED?

Moreover, why can’t ALL US citizens have demand accounts at the FED and thus be able to USE THEIR NATION’S FIAT in risk-free, convenient form? Why must any US citizen ever have to deal with a bank, credit union, etc. or be limited to grubby, unsafe, inconvenient, physical fiat, a.k.a. “cash”?

So not only is the Fed incompetent, it’s sleazy too. And remember, these handouts are only the ones we know about. There has to be a very good reason why all those brilliant economists at the Fed are terrified of being audited. Who else is the Fed handing out money to that they don’t want us to know about?

“So not only is the Fed incompetent, it’s sleazy too.”

Don’t look now, Drango, but those incompetents in the global bankster cartel are sleazing their way to world domination. Quigley suggested they were going to over 60 years ago. And they only seem incompetent because your interests have been sacrificed to serve their avarice. It takes some skill to rob entire populations and get them to sit still for it.

One wonders why the banksters bother with a piddling $30 billion here and there when they could simply write themselves checks for any amount and be done with it, until you realize that billions and trillions simply wouldn’t be anywhere near enough.

Walter, what you say is probably true. I use the term incompetent because the Fed says it wants to improve the economy, which it hasn’t, all cheerleading to the contrary. But I don’t think the Fed really cares about the larger economy, as long as the banks are doing well.

Conjecture aside. The Fed is a building, ME, and in that building are computers with software which begins, ENTER CUSIP NUMBER HERE. The Fed is not the only group using the building. There is an inbox on the Fed desk. Monetize new bonds, thank you Steve M. Send money to moderate rebels in Syria, signed CIA. Send pallet of hundred dollar bills to Baghdad, signed DOD. Wire money to Bangladesh, signed Men in Black. Ooops something went wrong. Not my fault.

This is why Paul wants to audit them, if you want to do illegal things in government you need a banker, the Fed is that banker all the way back to Nixon’s CREEP slush fund check written on the Mexico City bank.

Corruption in America is endemic, it was the cause of the 2008 crash and populist straw men like Trump will never touch the problem, because they made their fortune gaming it.

The worst part about interest on excess reserves paid to the banks is that the banks don’t have to lend to make money. It removes the primary reason for their existence, lending. It also guarantees them a profit margin and an income. This is no small point. The first and largest guaranteed income in America goes to the largest banks.

“It removes the primary reason for their existence, lending.”

Nonsense. The primary purpose of any business is to maximize the wealth of those running the business. In point of fact that is the only purpose. It is not to lend money, or to provide a product or service. It is not to provide employment, contribute to the economy, or support society. Social responsibility is in no way a consideration, corporate propaganda to the contrary notwithstanding. Wall St. has increasingly insisted on this model since Jack Welch propounded it in the 1980s and can sue successfully if it’s not followed. Financiers have the power to enforce it and have done so for centuries, and they can ruin any who won’t play ball, from Napoleon to Greece.

“The first and largest guaranteed income in America goes to the largest banks.”

Libertarians could inform you this is perfectly justified because they take the largest risks, presumably including the risk their livestock will revolt again, except on this count they prefer to pretend to be populists on the side of the victims.

WM,

You are obviously in rant mode today, so I will indulge you by disagreeing.

One of my degrees is in economics and in those days we were taught that businesses had social responsibilities, like selling products that don’t harm the customers, because you need them to keep making money.

Good business is based on a fair exchange and the distortion of this exchange is what got us where we are today. Which naturally leads me to Jack Welch and GE.

The legacy of Welch at GE was that nobody doing business with GE was going to get a fair deal. But even distorted markets tend to somewhat work and this leaves you with the GE you see today, totally diminished.

“One of my degrees is in economics and in those days we were taught that businesses had social responsibilities”

And yet, ten times a day you see businesses operating as if they had no social responsibility whatsoever. That’s the norm, and not the exception. I could load up the comments section of this site with thousands of heinous examples, and would never finish.

“Business ethics” isn’t taught in US MBA programs – what is taught is how to avoid it. What is taught is MSV, because that’s what Wall St. wants, the customers of MBA programs.

“selling products that don’t harm the customers”

At least until they can roll back the tort laws. That’s still to come. Until then, honey, enjoy your glyphosate and your endocrine disruptors. It’s what’s for dinner.

I, unlike Petunia, am enjoying your rants Walter.

Thanks, Kent.

Walter, that’s true about glyphosate. My family had a wheat seed genetics company, and many wheat growers in the Red River Valley desiccate their non-GMO crops of hard red spring wheat with Roundup four or so days before combining them.

The farmers have an economic incentive to do this for a few reasons, but when they bring their harvest in to the elevators, that glyphosate is on its way into the food chain. Much of the recently harvested canola crop has also been sprayed with Roundup and will be served up in the canola oil that’s so prevalent.

Does it really count as a “social responsibility” to avoid killing your customers so they can buy another? ;-)

On the other hand, I really do believe that this kind of example might be given out in B school. I know they teach classes on how to manage outsourcing, which is responsible to society only to the degree it’s responsible to shareholders alone.

Walter –

Spot on!

How is it possible that I totally agree with your rant while also agreeing with Petunia’s statement of issues with these interest payments?

Guess there are many layers to an onion. Your statement is True. Her statement is true, once you accept the rules of the game as they’re generally understood by compliant people, media, Congress, etc.

I wasn’t totally disagreeing with WM, just with his more extreme positions, pointing out these guys have to do good things once in awhile just to survive.

I am a libertarian, I will tell you that you are absolutely correct in my response – IF – and this is the clincher with today’s crony capitalism – IF the banks were not backstopped by the US government. See, you may not like a libertarian POV, but the problem, at least from my point of view, is that in order for libertarianism to work, the Government’s role has to change. NOONE gets a backstop, not the welfare queen, and not GE. Not GS or the small business down the road. Charity comes from private charities, NOT public IRS enforcement. That is when libertarianism actually works. If there is not real capitalism, then libertarianism is hopeless. That simple. Liberty only comes from freedom, and with freedom comes failure and success earned on its OWN MERITS. Not at gun point by Government coercion.

Even more perplexing is the fact that the rate on excess reserves is the same as the rate for interbank lending. This removes any incentives to do something with the reserves. But I guess in a post QE world nothing makes any sense.

As a bank CFO I’d rather make money making loans. Our average loan rate is 4.818% across our portfolio, and keeping excess balances at the FRB detracts from our income. We are currently experiencing insufficient loan demand, and have had excess deposit growth, mostly due to our clients having very profitable results. Note that this is the experience of a small community bank.

What I want to know, is this dividend part of the RRPO that was built into the rate hike policy. The first rate hike was accompanied by 105B subsidy, and since then the amount is only referenced by a disclaimer at the bottom of the page, some outrageous number per day, which each rate hike is costing the taxpayer to enable financial repression. Why (and I really want to know this) does anyone think levitating interest rates in defiance of free market gravity, is somehow going to turn out well.

Higher interest rates never turn out well. The Bank of England historically established a rate of 3% as the stable rate. This was a rate at which prices were stable. I tend to think it is still about the right rate.

Higher interest rates are going to hurt the working class once again. Having fallen into dire straights I have gotten a close look at higher rates in the shadow banking world. It is really good for bankers and really bad for customers. Since customers have little push back in the financial arena, they fight back where they can, at the ballot box. So eventually, the bankers, investors and the professional class will feel the pain too.

Never? Paul Volcker would argue otherwise.

I was around then and 21% was painful to most people. Even people holding 12% bonds were not happy.

What you are leaving out is that inflation was 14.8%. The bond holders at 12% had been unhappy anyway, but they would get compensated afterwards when inflation peaked and rates started to fall.

I am not sure why consumers would be happy with inflation running at 14.8%. Let’s say the Fed had stuck with 3%, are you telling me consumers would be happy with inflation at 20% plus?

Just seems to me you are confusing cause and effect.

Well for sure bears salivate at the prospect of higher rates.

This is why the USA is the greatest country in the world.

China, Japan, Europe? Who cares? They will all implode because they don’t have such a system.

Banks being paid to not lend. Guaranteed net interest margin.

The Fed: looking everywhere for inflation but paying for deflation.

Another example of the scam called economics. Yet there’s no public pressure to not continue paying banks to not lend.

No, my bank is willing to lend, but lacks loan demand. I’d much rather make the spread on a loan than what the FRB pays. I am foregoing income by parking money at the FRB. My cost of funds is .48% roughly, and my average loan is 4.8%. I’d much rather earn a spread of 4.32% vs. 1.02%.

Exactly as we should anticipate from the psychopathic face of criminal enterprise. Nice work if you can get it, the FED is well paid for all their hard work.

Hope and change, Indeed!

Maybe putting a criminal private banking cartel in charge of our monetary policy wasn’t such a hot idea.