Oh, and the unintended consequences of trying to regulate a monster.

Economists at the New York Fed included this gem in their report on a two-day conference on “Derivatives and Regulatory Changes” since the Financial Crisis:

Though the notional amount [of derivatives] outstanding has declined in recent years, at more than $500 trillion outstanding, OTC derivatives remain an important asset class.

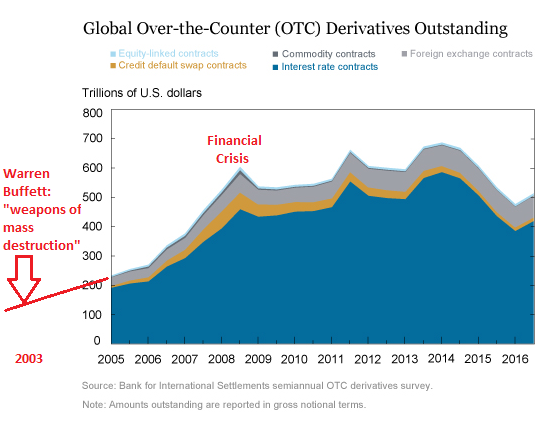

An important asset class. A hilarious understatement. Let’s see… the “notional amount” of $500 trillion is 25 times the GDP of the US and about 7 times global GDP. Derivatives are not just an “important asset class,” like bonds; they’re the largest “financial weapons of mass destruction,” as Warren Buffett called them in 2003.

Derivatives are used for hedging economic risks. And they’re used as “speculative directional exposures” – very risky one-sided bets. It’s all tied together in an immense and opaque market interwoven with the banks. The New York Fed:

The 2007-09 financial crisis highlighted weaknesses in the over-the-counter (OTC) derivatives markets and the increased risk of contagion due to the interconnectedness of market participants in these markets.

This chart from the New York Fed shows how derivatives ballooned 150% – or by $360 trillion – in less than four years before the Financial Crisis. They ticked down during the Financial Crisis, then rose again during the Fed’s QE to peak at $700 trillion. After the end of QE, they declined, but recently ticked up again to $500 trillion. I added in red the Warren Buffett moment:

The vast majority of the derivatives are interest rate and credit contracts (dark blue). Banks specialize in that. For example, according to the OCC’s Q4 2016 Report on Derivatives, JPMorgan Chase holds $47.5 trillion of derivatives at notional value and Citibank $43.9 trillion. The top 25 US banks hold $164.7 trillion, or 8.5 times US GDP. So even a minor squiggle could trigger some serious heartburn.

In 2003 already, famously, when there were less than $200 trillion in derivatives outstanding, Warren Buffett, who himself doesn’t shy away from them, warned in Berkshire Hathaway’s annual report:

I view derivatives as time bombs, both for the parties that deal in them and the economic system. Basically these instruments call for money to change hands at some future date, with the amount to be determined by one or more reference items, such as interest rates, stock prices, or currency values.

Unless derivatives contracts are collateralized or guaranteed, their ultimate value also depends on the creditworthiness of the counter-parties to them.

But before a contract is settled, the counter-parties record profits and losses – often huge in amount – in their current earnings statements without so much as a penny changing hands. Reported earnings on derivatives are often wildly overstated. That’s because today’s earnings are in a significant way based on estimates whose inaccuracy may not be exposed for many years.

The errors usually reflect the human tendency to take an optimistic view of one’s commitments. But the parties to derivatives also have enormous incentives to cheat in accounting for them. Those who trade derivatives are usually paid, in whole or part, on “earnings” calculated by mark-to-market accounting. But often there is no real market, and “mark-to-model” is utilized. This substitution can bring on large-scale mischief.

As a general rule, contracts involving multiple reference items and distant settlement dates increase the opportunities for counter-parties to use fanciful assumptions. The two parties to the contract might well use differing models allowing both to show substantial profits for many years. In extreme cases, mark-to-model degenerates into what I would call mark-to-myth.

The derivatives genie is now well out of the bottle, and these instruments will almost certainly multiply in variety and number until some event makes their toxicity clear.

In my view, derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.

That was in 2003. Five years later, it all came apart. Since the Financial Crisis, there have been some regulations globally to improve the functioning of OTC derivatives markets and manage “the risks associated with these products,” as the NY Fed’s report put it. But even today, there are still conferences on derivatives – for regulators to figure out how to regulate them, and for market participants to figure out how to get around these regulations. Hence “unintended consequences,” according to the New York Fed:

Some of the unintended consequences:

[W]hile the new trading, clearing, capital, and margin requirements have not generated the expected levels of derivatives market standardization, these requirements may be driving new market behaviors. For example, higher margin requirements for bilateral contracts may incentivize different types of institutions to become CCP [Central Counterparty] members, while higher capital requirements may lead to fewer traditional intermediaries providing clearing services. [S]ome CCPs are evaluating the possibility of allowing direct access for buy-side firms to mitigate the impact of capital regulation on the market. [R]egulations have disparate impact on different types of financial institutions. For example, mandatory clearing and higher margin requirements for non-cleared derivatives are having unintended consequences for end users of derivatives. In particular, institutions that use derivatives to hedge unexpected changes to their liabilities engage in bilateral contracts to match their exposures; the higher margin requirements for non-cleared trades thus increase their hedging costs and may reduce their willingness to hedge.

The report concludes with this zinger: “Possible further innovations to market practice and regulatory landscapes warrant consideration, given that OTC derivatives remain a significant part of the financial landscape.” Again, this hilarious understatement concerning the $500 trillion monster.

Clearly, it’s not all careening downhill, at least not for everyone. “The new 1%” of the S&P 500 stocks gained $260 billion since March 1, while the 99% of the S&P 500 lost $260 billion. Read… “The Great Narrowing” of the S&P 500

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good God I need a drink after reading this

Derivatives are “hedging tools?” Geez I hope you don’t actually believe that… Take this example..

I go long on Euro/USD to break 1.25 during the summer of 2016 and it doesn’t break 1.25 so I lose my money….But because Im a major bank, I dont actually have to take the loss, I can just make a DERIVATIVES play in the opposite direction and paper my losses…..If my next bet doesn’t work out (the derivative), lets say the day after I exit my Euro/USD it DOES break 1.25, then I have to make ANOTHER DERIVATIVES PLAY, and so on and so on….These Jerks dont want to take a loss on their 2008 bad bets so they’ve been laying down DERIVATIVES bets for the last 10 years until now, when the worlds derivatives market is 7x the world GDP..

For the umpteenth time the finacnial system is completely fraudulent…Act accordingly…

I am getting tired of those who always predict the end of our capitalistic system, “one day its gonna crash and burn”, maybe, but it will be last economic system to go down, which means it the best system to utilized resources. Leave it alone.!!!!!!!

Too bad that industrial capitalism is not the same thing as financial Casino capitalism. At least you could make this distinction.

By the way, do you really think that manufacturing a t—shirt in China and shipping it to the USA is a good example of capitalism allocating scarce resources efficiently?

Of course it isn’t, particularly when it is done in a state subsidised bankrupt factory.

With the deliberate intention, of keeping unemployment high, and small business opportunities scarce, in the destination nation.

Hey, what do you mean leave it alone ? That’s BS ! If the Wall Street wise guy were risking their own money, that would be one thing. But when that “system” buckles, the losses will be foisted off on the public. So the wise guys get the profits and the public get the losses.

At the rate that we’re going, we are all going to end up as Marxists, not Karl, Groucho.

Best system to utilize resources. LOL You may be right. Just not the “best system to wisely utilize resources”.

“Capitalism”?? This article is about financial engineering, not capitalism. Good God, capitalism is about taking earnings after paying your taxes, depreciation, interest, and principal, and investing into new strategies for products and services. The currency that organizations borrow to start businesses comes from savings or excess currency from labor. Buying up the derivatives in 2009, 2010, 2011, (it hasn’t stopped) by central bank morons only created an idiot institution that is holding the bad derivatives. THE PROBLEM IS THAT THIS INSTITUTION CREATES THE CURRENCY THAT OUR CAPITALIST SYSTEM RELIES UPON. We are now far worse off than any state-run, banana republic because the holders of our capital are going to take it when the “crash and burn” happens…

Go back to sleep, it is much more comfortable there anyways

Corruption. Derivatives are effectively being guaranteed by the U.S. and other governments, because of corruption. Otherwise, except for commodities futures and put and buy options, derivatives have no realistic social benefits: thus, only those entities that are not effectively subsidized by the government should be allowed to trade in them.

That is the problem with modern cronyism, which is what remains of the “capitalism” that we had in the eighteenth century. That is reason why the current system will have to change sooner or later. Like former president Salinas De Gortari in Mexico, who did everything to transfer to his cronies the assets of Mexico, since and including Clinton, U.S. presidents have been allowing similar, unjust transfers (thefts) of wealth.

For example, credit card and other debt carries interest rates of 8% to 25% for the majority of Americans. Meanwhile, the financial parasites (banksters) that plague America can borrow from the “Federal” reserve, the private banking cartel that can create money using the credit of the U.S. government (i.e., all Americans) with a name meant to confuse Americans, at below 2%. Of course, as to banks’ depositors’ funds, banks rarely even pay that much. Why are banks not taxed on those government (TARP) or “Federal” reserve subsidies and on the “fractional reserve” banking privilege-subsidy, which tactic other businesses are not allowed to do on threat of criminal punishments?

Other transfers of TRILLIONS of U.S. dollars continue. Junior and “The Snake” Paulson gave banksters $700 billion and “The Special Inspector General for TARP summary of the bailout says that the total commitment of government is $16.8 trillion dollars with the $4.6 trillion already paid out.” See https://www.forbes.com/sites/mikecollins/2015/07/14/the-big-bank-bailout/#4b5f3b772d83

Due to the influence of Geithner and Holder (who now openly represents the banks), apparently, the banks were also given get out of jail cards for their members, after they had defrauded thousands. See “Eric Holder Returns as Hero to Law Firm That Lobbies for Big Banks”; https://theintercept.com/2015/07/06/eric-holder-returns-law-firm-lobbies-big-banks/

As a result, the majority (bottom 80%) of our population is over taxed, while the top 20%, whose “reported,” “known” wealth now is far greater than the wealth of the bottom 80% of Americans, DO NOT HAVE TO PAY TAXES (on foreign investments that they naturally choose to keep in other countries) unless they want to pay them or (until Trump repeals the estate tax) they die. Of course, those wealthy people often under-report their wealth.

See some very conservative estimates: “The richest 10% hold 76% of the wealth”; http://money.cnn.com/2016/08/18/pf/wealth-inequality/.

See “20 People Now Own As Much Wealth as Half of All Americans:; https://www.thenation.com/article/20-people-now-own-as-much-wealth-as-half-of-all-americans/

To clarify, these derivatives are effectively guaranteed by the U.S. government, because the next time that the banksters are close to collapse, because of their derivatives (effectively gambling) debts, they will demand a government bail out. If no bailout occurs, they will make the stock market collapse, so the U.S. government (as in 2008-2009) will be coerced into bailing them out.

Thus, as to their gambling with derivatives, the banksters have a great deal: if they bet and win, they keep the money and pay huge dividends and gigantic salaries/gifts of options. If they lose, the U.S. and other governments are forced to bail them out.

Andrew, please clarify how your described scheme works. First of all, there has to be a willing counterparty at some usable price. Is there always one? Second, how can a new bet (that will not be settled for some time) paper over the loss of a bet that got settled yesterday?

If there really is a Ponzi scheme of derivates bets, then I would REALLY like to know EXACTLY how it works, with accounting rules considered.

Are you saying that the scheme is similar to buying a call option, then losing all of the purchase price, then selling a put option on the same stock to get some cash into my account to hide the previous loss, although in reality you still need to have other collateral if the market moves against you.

One way to do this, for example, is to enter a new swap with an upfront fee to offset the loss.

Not good to drink alone. I’ll hoist one with you.

Lol

Don’t like the growth in the forex derivates. At all.

The Warning: Brooksley Born’s Battle With Alan Greenspan, Robert Rubin And Larry Summers to have derivatrd regulated. She lost in the 90’s and so did the everyday person

It needs to be emphasized that derivatives, as they seem to me, are not so much a future threat. Their toxicity has already happened as it mostly consists in that they absorb, the real investment money from any economy they suck. They are not tools for hedging but a bet to maximaze profits, just as like your banker goes every night to the local casino with your deposits.

When the bankers can win $millions each and every day and never lose by virtue of their HFT algos, its not gambling. Maybe there is no risk for them anymore.

More specifically, derivatives are used to not have to take a loss on a previous bad bet….A banks balance sheet can always be “evened out” by papering over more and more derivatives over the previous bad bets so it seems as though assets balance out liabilities..

You’re right to say the toxicity has already happened, but to say there is no “future threat” is ignoring the fact that the players in question still HAVE NOT taken their losses from 2008 and after and until they take their losses their will always be a future threat…..I think the TPTB would rather just annihilate half the population with a war with Russia than actually admit criminal activity but what do I know….

Waw! Agree with you, the crisis (of the “financial post-industrial” capitalism) seems just entering its second phase.

And I, like you, didn’t like idea of the “50% annihilation” in a war with “West”.

TPTB is for “too powerful to bust”, isn’t it?

Derivatives are a form of insurance, backed by the assets to those underwriting them. When Lehman fell, it was very obvious the underwriter was under-capitalized. Who expected a large number of houses (trillions of $) to burn down all at once?

The notational value is like the sum of all the insured house values in the world, unlikely to all burn at once–unless built on the same faulty interest rate assumptions.

The bulk of OTC derivatives are interest rate swaps. These contracts need a notional value to calculate the contracts interest rate. It is not the amount of liability imposed between the parties nor is this notional amount exchanged between the parties. The trillions of dollars of interest rate swap contracts executed are reported at ”notional” value. This value does not represent the counter party risk. Unless i am missing something i don’t see the systemic risk inherent in issuing this type of product. This meme of trillions of dollars going up in smoke via derivatives may be overly hyped. Here is a overview of interest swaps.

https://www.khanacademy.org/economics-finance-domain/core-finance/derivative-securities/interest-rate-swaps-tut/v/interest-rate-swap-1

You’re right regarding the interest rate swap composition. While growth in derivatives sounds awful what are the complexities and risks of the interest rate swaps? Are there any more details regarding the types of interest rate swaps?

With CB’s pegging low interest rates for so long, why has this market grown so much? What’s the scheme?

How does an interest rate swap scenario become a nightmare vs the CDO meltdown we previously experienced?

The problem with them, is there is a group underwriting them, who are pure gamblers, who do not have the ability to pay, and no intention of ever doing so, if required to. This group are not “Bank’s”.

The “Head’s I win, tails you loose” People.

Those forex and commodity D’s are scary, as they deal with Very Volatile Components.

You can’t as some claim, write out another derivative, to cover a loss. Once the payment is due.

Many Forex and Commodity derivatives, can come due IMMEDIATELY.

A small division of AIG in Curzon Street, Mayfair thought selling CDSs were a license to print money.

House prices could only go up and they would never have to pay out on their CDS insurance contracts, needless to say they put no money aside for pay outs.

When the tide turned, this was what bought down the largest insurance company in the world.

Exactly

D’s as instruments, are not the problem. Some of the people, writing, buying, and selling them, are a huge problem.

The 1 bad apple thing.

Derivatives were and still are considered to be a crucial element to support the spread of dollar assets around the world and help keep the US the dominant player in world finances. “They” didn’t want a lot of transparency with these instruments and we got the result of 2008. It is likely their use is somewhat better managed/regulated now but I agree that another time bomb will likely occur. “They” consider this all part of the game to keep the US on top, so they are not going away any time soon.

Saw ‘THE BIG SHORT’ Last night. Nope no one learned a damn thing especially pension funds and the general public.

Meme, some of us have never used any of the “instruments” of the big-time financial system. By design, not because of financially ineligibility.

” Todays mistakes and errors are yesterday’s history forgotten “

I can’t bring myself to watch that movie…….I fear my head will explode.

Derivatives are the biggest threat to the financial system.

James Rickards in Currency Wars gives some figures for the loss magnification of complex financial instruments/derivatives in 2008.

Losses from sub-prime – less than $300 billion

With derivative amplification – over $6 trillion

It was the derivatives that really did the damage; derivatives were the mechanism that allowed a housing bust in one nation to infect the global economy.

Derivatives were used as leverage to increase bonuses on the way up and losses on the way down.

The derivatives market is now bigger than ever, no sensible regulations have been put in place since 2008.

Where does the real danger come from with derivatives?

Jim Rickards was at the top of LTCM when it collapsed in 1998 and saw how the collapse in a link of the derivative chains turns losses, from nett to gross within the system.

Everyone panicked as it was impossible to gauge the size of the losses.

When Lehman Brothers collapsed in 2008, everyone panicked as it was impossible to gauge the size of the losses.

The same problem ten years later and the same problem will happen next time as no regulations are in place. Everyone still believes the risk with derivatives only comes from their nett value as they have learnt nothing from experience.

LTCM as the poster boy for what can go wrong. The Gramm-Leach-Bliley Act, also known as the Financial Services Modernization Act of 1999 ( Merry Christmas America) opened the doors for crimes. But, who cares, right? Read up on it and the same names pop up as in LTCM.

The new derivatives game for mom and pop is the ETF. Now with ETFs based on other ETFs and 3x and 5x derivatives ETFs, what could go wrong here? There are more ETFs than their are underlying stocks, but the money flows. Why isn’t that the way the crash of 2007/2008 started.

The dark bets, the side bets, the off-the-book bets are not even in the mix. Those most likely can’t even be measures or tallied. Just think of it as you and all your buddies making side bets on sports games, and you get the idea.

I have the same idea about ETFs, its just another way of leveraging up that rather small real world with another type of financial product.

You have to build an inverted pyramid of financial products on top of any real world assets as there are just aren’t enough of them.

“It’s nearly $14 trillion pyramid of super leveraged toxic assets was built on the back of $1.4 trillion of US sub-prime loans, and dispersed throughout the world” All the Presidents Bankers, Nomi Prins.

Like that.

…and then promptly bailed out by Fed money printing, lending, direct investment, bail outs and financing.

Free money for rich people.

No lessons learned, no one went to jail, fines were smaller than Sunday collection plates, so the crimes continue. Blame government or the lack of one, blame greed from the perpetrators, the rating agencies, the lazy fund managers, and the to god to be true suckers.

What these statistics don’t tell are the dark bets, the side bets, the off the books bets. Just like the bets you make with you football buddies, some one wins all. These off the book bets will be the real threat. The FED whistles in the wind on the impact.

When such things as ETFs ( which are derivatives) out number the underling stocks they are based on, one can only see dominoes waiting for a nudge.

There is no tax money to bail out these crimes again, just hard assets.

Why can’t the Fed print their way out again? They made such YUUUGE profits last time around in their estimation. The Bernanke method is certain to be used again, probably at three times the balance sheet.

Meme, all the lessons were made clear and learned by many…The financial system is run by Organized Crime….It’s a Cabal…They know what they’re doing is fraudulent but instead of people pulling their money out of the fraudulent system most people rather just complain about it than actually remove their assets,withdraw from the fraud and rearrange their life in a manner that is not dependent on a system run by gangsters…

NY Geezer’s comment is dead on, there is NO risk…The equity markets have been on autopilot (smash vix spoof SP minis/QQQQ) since 2012…In December of 2013 Congress passed a bill making the US treasury responsible for all Derivative losses that MAY happen to major US banks….Its tax payer backed…This has been in the works for years..

What bill was that, Andrew? Bill number and paragraph, please.

Was it this – in 2015? This would be via the FDIC….

http://www.politifact.com/wisconsin/statements/2015/jan/07/mark-pocan/new-law-means-taxpayers-must-back-banks-incredibly/

I vaguely remember the controversy over it. If someone could dig up more on this – including the bill and paragraph(s) – that would be great.

Wolf and Justme,

I believe what you are talking about is what some refer to as the Citi Amendment. This ZeroHedge article talks about it.

http://www.zerohedge.com/news/2014-12-07/wall-street-moves-put-taxpayers-hook-derivatives-trades

The bill was H.R.83 – Consolidated and Further Continuing Appropriations Act

https://www.congress.gov/bill/113th-congress/house-bill/83/text

The amendment is under Sec. 630

Thanks.

It’s part of Dodd Frank. I think it was part of the SIFI designation. Andrew is totally right.

Now that I think of it Greenberg lost his case again this week so the Fed can perfect print, seize, and profit. Treasury is supposedly piling up vast sums from Fannie and Freddie.

The Weimar printer was probably out of his mind. That was vandalism and our Fed bobbins are now proven technicians. It appears they even know how to smooth stock prices.

Greenberg and the management at AIG are lucky not to be in prison. In a just world their heads would be on sticks.

For every seller there is a buyer. I’m not sure what kind of event would upend the system. The net result of a crisis would be a break-even since many players are betting in opposite directions on an asset. class.

Or are there rules for collateral here that I don’t understand?

If 2008 didn’t collapse the system I don’t know what would. As far as I know pension funds and govts can’t buy such risky assets.

Waco: The problem as I see it is it will be a lot worse, with lots more derivatives involved than the 6 Tr. referenced by Wolf here. There IS counterparty and contagion risk. It’s not that things net out as much as how we get there (contagion, hard landing), and how long it takes to get there. I think there’ll be massive displacement in that process. Think about how long it took the US to pull out of the Grat Depression.

Yep. Rickards says it’s basically a pyramid scheme with nothing reported so that the risk management desk remains clueless.

Damn Waco I dont even know where to start when you begin your statement based on a false assumption…”for every buyer there’s a seller” really!?

I see you fail to grasp that margin will let people go BELOW zero net worth if their margin isn’t cut off in time and they continue to make bad bets…And Deutsch Bank has 60 trilllion in derivatives and no cutoff since at the highest levels of this fraud there ARE NO checks and balances….They cheat to win….

——–So 2008 didnt “collapse” the system because there was still money in pension funds and at the municipal level….That changed when the FED purposely lowered interest rates to the lowest EVER so companies managing pension and municipal funds could no longer make sufficient money collecting interest on Bonds and other fixed income because their interest rate was so low. This forced these companies to put their money into a Ponzi scheme(equities) with a built in skimmer (HFT algos) to drain the liquidity day by day (take a lookf at Virtu, 1 loss in 2 years of trading, refer to NY Geezer’s comment)..So this next crash wil leave NO money at the local level and your retirement funds, aaaaaaand its gone!

The problem, Andrew, is not with derivatives, but the collateral and ability of a counter-party to a derivative to settle when things go wrong.

If Lehman or AIG had enough collateral to cover the difference in the derivatives that fell outside their calculated value then nothing would have happened.

If you want you can expand the universe of ‘derivatives’ to things as simple as a person buying a house with a mortgage.

If you don’t have the ‘assets’ to cover the difference in value of what you put down and the mortgage, then your ‘derivative’ goes belly up. You lose the house. Those assets can be other assets you own or another ‘derivative’ the future value of your earnings.

As there is very little or no regulation of these markets and the ability of the entities involved in the derivative market to skimp on the collateral to back up the ‘bet’, as collateral costs money, it invites excess risk which people now know will be picked up by others.

Very simple.

“The problem, Andrew, is not with derivatives, but the collateral and ability of a counter-party to a derivative to settle when things go wrong.”.

Ummmm Lee, I think thats exactly what Andrew is implying….Redundant…

Happy Mother’s Day

Collateral is an illusion since it depends of what someone else values that specific collateral item.

One day a beanie baby is worth $100 the next year $5. In 1990 Enron stock was worth around $10, 10 years later over $90, two years later nothing.

Good luck on loaning money based on collateral alone. The Merchant Bankers of the 19th used to do it based primarily on a person’s character and reputation. They found that system far more reliable.

What you don’t SEEM to understand with D’s, is that a group of the buyers, DO NOT HAVE THE MONEY TO PAY.

If called upon to do so.

They are effectively selling insurance with out the income, or money, to cover a payout on the policy. Further they have no intention of paying, if there is a claim.

That, as we know, is fraud.

A few fraudsters are all it takes to break a system.

In the US there are many Fraudsters, (they are not Banker’s) it is a legalised profession.

I cannot buy life insurance on people I do not know and have no relationship with or do not know even if I have a reasonable suspicion they may die soon. The insurance company would suspect I am operating on information they do not have and that the risks are greater than their models assume yet the big banks will sell CDS and other derivatives to ‘investors’ willing to make just such bets.

Banks need to ask why someone with no direct interest in the underlying security is interested in buying insurance on it. They aren’t operating a casino where the odds are entirely mathematical and in favor of the house. They are operating in the human world where someone somewhere can be operating on superior information and seeking to profit from it.

Beadblonde, you don’t really believe the FED can overcome the proven history of fiat currency collapse, do you? Maybe you’re being sarcastic.

I don’t know what the Fed can overcome. I don’t know if I’m being sarcastic or not. At what point do people lose belief?

Now for starters

I quit believing when Congress passed TARP, against the will of the public, and allowed FASB to make Big Financial asset reporting changes from mark to market to ‘Mark to Unicorns’ !!

…. and we continue, to this day, to roll downhill towards that rocky precipice, picking up ever more snow !

“according to the OCC’s Q4 2016 Report on Derivatives, JPMorgan Chase holds $47.5 trillion of derivatives at notional value and Citibank $43.9 trillion.”

This is interesting because JPMorgan Chase has $2.49 trillion in assets, and Citigroup has $1.79 trillion in assets. The Volcker Rule supposedly bans proprietary trading by deposit taking banks, with an exemption for ‘hedging’ activities. If banks are only allowed to hold derivatives for ‘hedging’, but JPMorgan Chase holds derivatives with a notional of 19X their assets, and Citigroup holds derivatives with a notional of 24.5X their assets, then what are these banks hedging? My guess is these are really highly profitable proprietary derivatives trades collateralized by FDIC insured bank deposits. It’s well known that most bank derivative trades are collateralized by bank deposits. According to the NY Times “Wall Street firms locate derivatives trades in bank subsidiaries backed by government-insured deposits. As a result, these subsidiaries have higher credit ratings than the parent companies. Citigroup, Bank of America and JPMorgan Chase have more than 90 percent of their derivatives in such subsidiaries.”:

https://dealbook.nytimes.com/2012/06/22/a-sober-new-reality-in-credit-downgrades-for-banks/?_r=0

With regard to the potential profit to banks from derivative transactions, just ask Harvard University how they lost more than $1.25 billion on a wrong way interest rate swap:

https://www.bloomberg.com/news/articles/2013-11-08/harvard-swap-toll-tops-1-4-billion-ending-deals-in-2012-2013

The thing about derivatives is that they are often a zero sum game, and banks can just as easily be on the wrong side of one of these trades. Except bank losses are backed by FDIC insured deposits.

Was that when Larry “don’t regulate derivatives” Summers was President of Harvard?

The governments should tax every transaction with a small tax of about 0.5%. Such a tax would stabilize the financial system, because it would kill the useless high-frequency trading and it would bring down the volume of speculative transactions and derivatives.

If $500 trillion were to change hands, would mean that the government gets $2.5 trillion in taxes. Besides stabilizing the financial system it would have another benefit: you as a normal person would pay much less in federal taxes.

The time has finally arrived to convert Emerald City’s digital 1s and 0s into, ironically, OZs.

Ground Zero for Derivatives.

The Depository Trust and Clearing Corporation, which is privately owned by banks and brokers, announced on Wednesday February 10 2010, that the Federal Reserve Board had approved their application to form a subsidiary of the Federal Reserve System, to be known as the “Warehouse Trust Company” responsible for over-the-counter derivatives, and operate under the umbrella of the Trade Information Warehouse.

So, what are derivatives?

They are structured investment products that are financially engineered, combining underlying shares, bonds, indices, commodities, options, forwards, swaps, etc. The value of which is determined by the prices of the underlying “assets”.

They come in many forms;

ABS – Asset Backed Securities

MBS – Mortgage Backed Security

CDS – Credit Default Swap

CDO – Collateralized Debt Obligation

CMO Collateralized Mortgage Obligation

CBO – Collateralized Bond Obligation

CLO – Collateralized Loan Obligation

CFO – Collateralized Fund Obligation

SSL – Senior Stretch Loan

Well over 50% of OTC derivatives now being issued are based on leveraged loans. What could go wrong?

If it does go south the taxpayer picks up the tab, since the “Warehouse Trust Company” responsible for the derivative sphere, is part of the Federal Reserve System and is backed by Uncle Sammy!

BASIC PRIMER ON DERIVATIVES

A.While the total amount of derivatives (~500 T is huge ,most are really plain vanilla type derivatives with very little risk (i.e short term interest rate hedges).That said ,the amount of derivatives that are more risky probably total in the tens of trillions.So if the amount of risky derivatives total 50 T,then just a 2% loss on these positions will total 1 T. Will a loss of 1 T crater the financial system.I do not know ,but we shall find out if there another major financial crisis

B.Simply put derivatives can be thought of as combination of options and futures,which offer a way to hedge a position(lock in profits).Credit default swaps are a type of derivative in which the buyer is paid if a company( or government) defaults on its obligations in the future..

The difference between the futures and options that individuals trade and OTC derivatives is that exchanges require higher margin (collateral) requirements and “supposedly” segregate these funds.I use quotes because of the problems involving the bankruptcy of MFGlobal in 2011.No segregated monies were eventually lost ,but that were some troubling questions because MF Global had illegally commingled company and customer accounts .

When markets move sharply (i.e 1987 and the Long Term Capital Management of 1998). the amount of margin(even at exchanges) may not be enough to cover losses.

The OTC derivatives ARE MUCH LARGER AND have no such requirements.While there are collateral requirements for banks,these rules can vary by country and are lower than exchanges require.And there are different rules for non banking entities.All financial institutions have a financial incentive to minimize the amount of collateral used for a trade in order to increase returns.

C. Not all participants in the OTC derivative markets are hedging.Some are hedge funds who use OTC derivatives to make money.In simple terms they can be thought of as making side bets.

D. Yes, for every entity buying derivatives there has to be another one selling that same derivative.

HEREIN LIES THE REAL RISK .If a financial institution hedges a trade by buying a derivative ,it is dependent on the the institution who sold them the derivative to pay off.Everything is fine if the seller can pay.But if the seller somehow runs into financial problems and can not pay,then that can create financial problems for the buyer also .In essence the buyer who thought he had hedged a position was really unhedged ,because the seller failed to pay up .

THIS CAN THEN RESULT IN A DAISY CHAIN OF DEFAULTS

THIS RISK IS CALLED “COUNTERPARTY RISK ” AND IS AT THE CENTER OF ANY FUTURE POTENTIAL PROBLEMS.

1 Trillion in losses will not crater the system. The Central Banks will step up and fill the hole. That is why these derivatives are allowed to continue.

And it will happen again.

Two words:

Exter’s. Pyramid.

Money is trust in the narrative, the promise of more in the future, even if it is impossible, since the interest is non-existent, and, if existent, worthless.

Some good, coincidental insight into the Derivatives issue from Doug Noland:

http://creditbubblebulletin.blogspot.pt/2017/05/weekly-commentary-vix-and-scheme.html

The implications of narrowing of the SP, (the rally is a lot longer in the tooth than we thought) and derivatives (the fed needs some transparency because sorry, if moving rates, or shrinking their balance sheet, or reducing liquidity, one way or another blows a big hole in the outstanding derivative book, they are going to follow the safe path, or the path determined by the flow of money in capital finance markets, hence over time there should be less risk, of the Fed always meets that risk with the appropriate policy, and less need for derivatives. (Then why does the outstanding nominal number keep going up? wrong fed policy?)

(Then why does the outstanding nominal number keep going up? wrong fed policy?)

No not wrong fed policy.

The majority of the D’s are interest rate swaps.

The more money lent/borrowed in the larger economy = more need of interest rate swaps.

The one I dont like in that chart, as I wrote before, is the growing FX Swaps, as at the bottom on them, is large pile of gamblers without the ability, or intention, to pay, if called.

Read the chart think about the volume of money pushed into the economy, and when.

But with FX, global trade is very down, yet there is a lot of speculation in FX trading. And a growing FX D volume, in a particularly volatile area.

I thought tear-ups were supposed to reduce the notional monster. (At least that was the hope 10 years ago….) If tear-ups have been happening in the background, the rate of new contract generation has been truly obscene.