In the land of NIRP refugees and “Reverse Yankees,” who will get crushed?

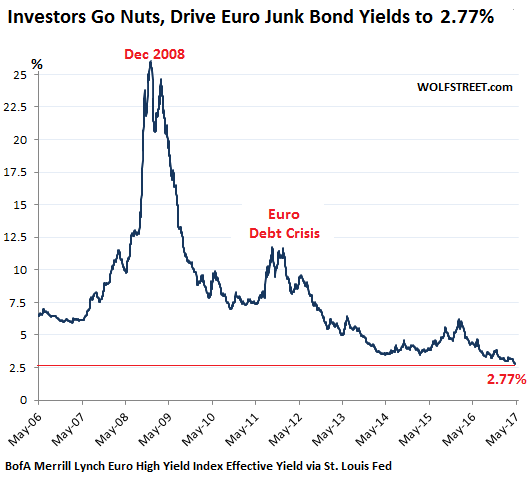

At the end of the week, something special happened, something totally absurd but part of the new normal: the average yield of euro-denominated junk bonds – the riskiest, non-investment-grade corporate bonds – dropped to the lowest level ever: 2.77%.

April 26 had marked another propitious date in the annals of the ECB’s negative yield absurdity: the average euro-denominated junk bond yield had dropped below 3% for the first time ever.

By comparison, what is considered the most liquid and safe debt, the 10-year US Treasury, carries a yield of 2.33%; the 30-year Treasury yield hovers at 3%.

This chart of the BofA Merrill Lynch Euro High Yield Index (data via FRED, St. Louis Fed), shows just how crazy this has gotten in the Eurozone:

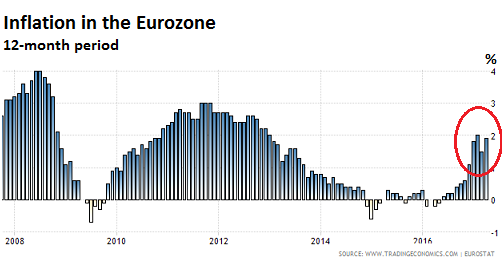

It’s not like there’s deflation in the Eurozone, despite rampant scaremongering about it. The official inflation rate in April was 1.9% for the 12-month period. As this chart shows, it’s not likely to go away any time soon (via Trading Economics):

In other words, the average “real” junk bond yield (after inflation) according to the above two indices is now 0.87%. That’s the return bond-buyers get as compensation for handing their money for years to come to non-investment grade corporations – as per an average of the ratings by Moody’s, S&P, and Fitch – with an appreciable risks of default looming on the horizon.

Issuing junk bonds in euros is not just the prerogative of European companies. It includes issuance of junk-rated US companies that seek out this cheap money. “Reverse Yankees,” as these bonds are called, have become a large factor in euro-bond issuance.

And investors that accept a “real” compensation of only 0.87% per year to deal with these risks – have they gone nuts? You bet.

The Wrath of Draghi.

As part of its now reduced €60 billion-a-month QE program, the ECB buys government bonds, “covered bonds,” investment-grade corporate bonds, and asset-backed securities. It also cut its deposit rate to negative -0.40%. All of this with the explicit goal of driving up all asset prices and repressing all yields across the corporate and sovereign spectrum, from the best to the worst.

What the ECB doesn’t buy is junk bonds. That doesn’t mean it can’t end up with junk bonds on its balance sheet, if for example, a country or a company whose bonds it holds gets downgraded to junk.

As a result of the QE program and the negative-interest-rate policy (NIRP), numerous government bonds are now trading at a yield below zero. For example, the German five-year yield is -0.33%. This hounds investors with a return after inflation of -2.23%! Investors who seek any kind of positive return in euro-denominated bonds have to flee into riskier assets, such as junk bonds. Or they have to flee to other currencies, such as dollar-denominated bonds. These are the NIRP refugees.

Why are NIRP refugees risking so much for so little?

Many are institutional investors that have to buy euro bonds, such as life insurance companies and bond funds. Ultimately they don’t care because it’s not their money. It’s other people’s money (OPM). Institutional investors get paid to manage it. All they have to do is go with the market. If it blows up in their face, and everyone is in the same mess, they’re just fine. It’s OPM that blows up.

As the ECB buys more and more bonds, repressing yields in the process, investors have to bid against the ECB, further pushing down yields. But a central bank like that is special. It’s the relentless bid. It’s bidding high on purpose because the purpose is to drive up bond prices and push down yields. Institutional investors, such as pension funds and life insurance companies that have to buy bonds don’t have a choice. They have to play.

What’s the outcome?

Someone is going to take the loss. When companies default on their debt, investors get stiffed – usually pension-fund beneficiaries and the like whose money this is. The OPM. They should have been compensated for taking this risk. What the Wrath of Draghi accomplished is that they are forced to take these risks without compensation.

So companies are issuing euro bonds no-holds-barred. From Spanish banks that have unleashed a flood of bonds to Mexico’s teetering state-owned oil company Pemex which sold a €4.3 billion of euro bonds in February.

But bonds aren’t like stocks. Bonds get redeemed (if they make it that long) at face value. If held to maturity, the only capital gains occur if the bond was bought at a discount. But in the current environment in which yields have plunged, bonds are acquired in the secondary market at a premium. But the premium evaporates as the bond gets closer to the maturity date. Traders and hedge funds can make a buck if they unload the bonds early enough and if yields continue to drop. But for institutional investors that hold bonds to maturity because their business model requires them to, there’s no good exit.

And that’s really crazy, what this central bank has wrought, when you think about it long enough.

Oh, and the unintended consequences of trying to regulate a monster. Read… $500 Trillion in Derivatives “Remain an Important Asset Class”: Hilariously, the New York Fed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wake me up when it blows .then we can point the finger even if it is way way to late bloody good job Europe you deserve everything that comes your way. The rest of the world don’t want to hear you moaning because you sat on your ass and did nothing for far far to long

We are deaf anyway. Eyesight ain’t so good either. But they, Europe, are politically correct so lets see how that works out.

This is what happens when you let bankers, who own the politicians, run the world. Then after they lose the public’s money, they come crying to the government, who then makes them whole with taxpayer funds. So the people get screwed twice. Find a banker and get a rope.

+1

They will not see it coming and “couldn’t have seen it coming” when it does.

Super bailouts to stop the system imploding….. before the system implodes.

The game has changed, in a sense. In the sense that it didn’t use to be a game. It used to be work. Investment used to be in some enterprise which performed some activity, and hoped to produce something useful and turn a profit. Now the game is nothing but a game.

Great Article:

I have come to believe that ‘the debt’ of the European Union Member Countries is a fabrication .. a lie .. a scam perpetrated on the 28 European Union Member Nations.

By the old & seasoned, geriatric, financial, pilfering professionals that we call the EU Leadership & our clever little Italian friend Mario Draghi & his mafiosi groupo.

To appropriate into private possession, the vast wealth of 28 European countries in their charge.

Come pay day & they are all over us like a rash ..

How many “must’s” have been compulsorily taken out of the salary packet of descent & hard working citizens .. too bloody many.

Superannuation is literally theft ..

* 1.000.000 citizens have $10 extracted from their weekly pay packet = $10.000.000 a week ( $520.000.000 free money / OPM; to play with a year ) delivered to a company to do with as they wish .. “forced to take a risk with out compensation” .. for the most part it is monies that will never be seen again by their rightful owners.

I wonder if – The Wrath of Draghi – Is not – In reality –

The act of shooting himself & his ravenous buddies in the foot.

Because, to my mind, the sooner the superannuation monies are all gone – the sooner the superannuation funds will shut down for good, labelled – FAILED & NON VIABLE.

In an article KTG – some guy suggested – in jest most likely ha, ha, aha ha. that Greece give over it’s gold reserves & real estate to help Greece with it’s debt burden – & I knew, it’s all fa scam, a grab for as much as the looters can get.

But I heard the Greece has no gold Boating accident I believe they said

Micheal Milken was able to create the junk bond business at Drexel because he was able to convince investors that the companies could generate the profits to pay off the high yield bonds.

What the junk bond yield you describe is saying is, these companies can’t squeeze out enough profit to pay more. In a sense, the low yield of the junk bonds is a signal to the market of future profitability or the lack thereof.

No, the low yield junk bond is a desperate search for income where little is available. It’s the result of competition for funds where massive liquidity exists. Or just a fix by the biggest investor (ECB) who pays above market prices for debt and this influences the entire market. The FED does this at the long term today and has for years with operation twist.

Your argument doesn’t make any sense.

When Milken was underwriting junk bonds at 5%+ over prime, there was massive liquidity going into the junk bond market. And normally prudent investors followed the yield into the market then too. The difference is, then there was more confidence about the “economy” being able to produce the profitability, which isn’t there now. I think the historically low yields now point out the lack of confidence in the economic environment.

No search for yield back then. Apples and oranges.

‘lack of confidence’ is a sales pitch to keep rates low by popular opinion. Low rates have little relationship to ‘lack of confidence’ in reality. Rates have historically, in hundreds of years, never been this low. It’s a public finance scam. The public buys into it due to ignorance, apathy, and by having given control to others who control the agenda regardless.

and, finally, low rates for saver hinder economic growth because they would spend what they earned. Parasites who live off abnormally low rates would scream bloody murder and claim the end of the world is nigh if rates normalize. In actuality, normalized rates will fix much at the expense of economic parasites.

“forced to take these risks without compensation”

This is not even close to Capitalism.

One of the most fundamental mechanisms in capitalism is that risk is used to price all forms of capital (equity and debt). So higher risk capital gets more expensive. Markets decide how much risk is involved and what that price level should be. But central banks have destroyed that fundamental pricing mechanism.

Yes, Wolf, markets now serve only to transmit the will of the Elite.

Another fundamental, ultimately fatal flaw in whatever you want to call the present experimental system is a private central bank printing “money”, literally out of thin air, and using that “money” to “compete” with ordinary people to buy REAL things, thereby “setting the price” at whatever the central bank desires.

This “system” is increasingly becoming nothing more than a herd-management operation run by the “private” central banks. Unfortunately for the Elite central bankers, just exactly Whom this system benefits is becoming more and more obvious to an increasingly-LESS-bewildered herd, who will at some critical-intellectual tipping point, rebel against that system in unpredictable ways — perhaps metaphorically “ramming their vehicles” into the Elite pedestrians walking down Their yellow bricked roads.

No Offense please…but the kids running the market have a poster on their hot rod pickups with some arrant squat kid taking a pee in our face. The are no markets, period. There is no intelligence running the markets. IA runs the markets and some kid changes the batteries every so often in-between puffs and moving the antenna closer to the source.

And the Fed, if they had to make a jelly sandwich, half would ‘trickle down’ the cabinet and spread all over the floor and then giggle, wondering who would clean up the mess.

Conservative Libertarian RECENT convert from ultra liberal Democrat must tell you volumes. The wake up call is not getting louder, why should it, no one is listening. A spade is no longer being called for what it is….a spade.

It is all about fear now. That… is so heavy in the air that scrubbers are being left with out anyone to change their batteries.

enough…I am on the way to the hospital…really.

‘Following the binary choice’ is a great thought exercise. For example, the ECB can stop QE or continue QE. For either event each consequence follows a binary choice. After each trail is followed a bit, the most likely course in the near future and far future becomes obvious.

For example: ECB stops QE: Rates rise or fall (rise)

Rising rates help / hurt the borrowers (hurt)

Rising rates help / hurt debt owners due to capital gains risk (hurt)

Public likes / hates rising rates for public debt (hate)

Public likes/hates higher interest income (likes)

Debt levels rise/fall (fall to neither, probable default due to rising costs and massive debt requirements just to keep the plate spinning)

Free government benefits actual cost rises/falls (rises to due higher cost of money and hoards of refugees)

Risk of EU ending now/later (now)

OR

ECB retains QE indefinitely: rates rise or fall (fall)

falling rates help / hurt the borrowers (help)

falling rates help / hurt debt owners due to income risk (hurt, savings earns nothing and may have actual cost from negative rates)

Public likes / hates falling rates for public debt (like, somebody else is paying the way, they think)

Debt levels rise/fall (rise)

Free government benefits actual cost rises/falls (rises, but paid for with debt so you can afford more now, so rates kept low to lower)

Risk of EU ending now/later (later)

The EU will end either way. The EU public is paying their way with low to negative rates which indirectly consume savings either via debt that will eventually default or forgone income from normalized rates. Benefits only look free, but the worst effects will be much further down the road if QE remains until it can’t. The people of the EU did this to themselves and continue to embrace it. They ostensibly have all agreed to live on borrowed and printed money until they can’t. They just don’t talk about it openly.

Binary logic clears muddled thinking.

Basically, everyone in the EU has agreed to live on the credit card and feels special because they can control interest rates and never be cut off unless the entire world gets tired of it. Anyone who doesn’t like it, such as savers, don’t matter because the system slowly confiscates their savings over time. Borrowers are the thrifty ones in this plan since someone else is paying their way … the systems is designed to do it that way.

Germany is indirectly supporting the southern countries via negative rates and savings.

Thinking obliquely, Petunia above got me thinking about financial parasites and how they like to convince the Fed to keep rates low to prevent the world from ending … being sarcastic. Those who need low rates would feel pain if rates rose while most people would start to feel normal again. The US economy would prosper with unicorns and flowers abounding after rates went up to normalized levels.

The Eurozone is a different story. In the US, our oligarchs discovered low rates and how to get rich with them artificially low. ECB clients, both big and small, including the biggest, smallest and most indigent … have discovered how to use the central bank to promote living off the credit card.

Draghi spins a story that implies salvation if successful and world ending events if not successful. Low rates and unimaginable quantities of printed money and debt monetization are involved. The salvation of an entire continent depends on him doing his thing. Unimpeded. Squalor and worse are the alternatives.

The result … the world permits the ECB to monetize everything in sight. Debt levels rise. Negative rates confiscate savings. Locals are living on the credit card and the credit card is paid off with printed money. Low rates make it look like a good deal.

Yet it’s the same as our oligarchs, only it’s less stratified. In the eurozone, everyone gets a piece of the action. Everyone’s in on the scam. Borrow and print or the world ends. Take someone’ else’s savings. Stiff the Germans with negative rates to offset target 2 imbalances

The Euro-Utopia in full flower. As log as the Fed isn’t sucked in to keep our rates low to indirectly subsidize theirs, let them continue their circus. I won’t buy eurodebt. Not my problem. Fun to watch.

All clear to see if you ignore the econ-babble and pr flacks.

In some ways, it’s a myth that “little people” are necessarily victims of the international financial/corporatocracy cabal.

Some are not.

For example Lee Bank offers financially sound individuals a checking account that pays 1.5% on a balance up to 15K (graduated downwardly above that) in return for some transactions in the account each month that are ordinary anyway, and not onerous.

Some credit unions offer 2%, but these institutions generally perform like government bureaus (your friendly state driver’s license agency, for example) and putting up with their service deficiencies is not worth the extra .5%, IMO. This is not true of all credit unions, but the ones that offer 2% demonstrate why they have to do it. Try and get one on the telephone – see what happens (more exactly, what doesn’t happen).

The Keys: enough genuine liquidity to be able to take advantage and an excellent credit rating.

There is nothing to prevent the ECB from changing their rules and buying junk bonds in the future..Interest rates have nothing to do with risk or inflation ,but all to do with the PERCEPTION that the Central Banks are all knowing and all powerful.

Imagine another scenario.

All Euro countries start issuing zero coupon bonds with maturities of at least 50 years.Obviously no interest is paid on these bonds.The ECB then buys these bonds with money printed out of thin air.Each country then uses the money raised from these bonds for any purpose they like,including lending to corporations with low credit ratings and slashing taxes .After 5 years the ECB starts writing off these zero coupon bonds resulting in no payments from any country to the ECB. The result is that each country gets monies to use as they wish and the ECB theoretically losses a bunch of money.But since this money was conjured from thin air no losses are taken.

Zero coupon bonds sold at a premium are a real possibility. In other words, the bond is for $1000, you pay $1100 instead of $900. Then it gets refinanced at maturity with more negative rate debt. You pay $1100 and get repaid $1000.

Actually, that may be a reality now since I have no idea how to service negative rate debt.

Re ECB default: yes, but not until the game is over. Years from now.

Zero coupon long maturity debt is the the logical extension of current ECB policies.No interest payments and no defacto repayment of principal .NO PROBLEM,RIGHT!!!

Your example is a good,simple mathematical representation of what negative interest rates represent Refinancing such bonds with more bonds avoids any default issues .

The only argument for buying bonds with negative interest rates(other than to quickly flip them to the ECB) is the collapse of the Euro to be replaced by each countries individual currencies.And even under this circumstance only those currencies with the strongest finances would benefit.

If low interest rates mean lack of demand for money, negative interest rates undoubtedly mean force feeding of money. It’s the helicopter drop with the only difference being you have to go to the bank to sign up for it.

I have to smile when all my neighbors think they’re millionaires because they ‘own’ a house …

If you have capital in Europe, you can invest it in new business and lose it quickly, or you can sit on the capital it and lose it slowly. Either way you lose it.

Prices of everything must drop before any real investment will occur.

Bobber sounds like you are describing the US housing market to me

The ECB is yet another example of the correctness of Lord Acton’s observation “Power corrupts, and absolute power corrupts absolutely.”

While civil control of the central banks has indeed resulted in problems in the past, including collapsed economies, e. g. hyper-inflation http://www.businessinsider.com/worst-hyperinflation-episodes-in-history-2013-9 , it appears “independent” central banks cause even more problems.

The maxim “what the state (taxpayers) pays for, the state should control,” for example the military, appears correct. While this does not eliminate problems, it does seem to minimize them.

What is incomprehensible to me is how middle-class taxpayers keep voting for the Oligopoly status quo and its captured political marionettes, then whine about how things just keep getting worse and worse.

You can’t fix stupid.

Just another day in the globalist Oligopoly.

Central banks exist for one purpose: to facilitate the looting and asset-striping of the middle and working classes, and to concentrate all wealth and power in the hands of a corrupt and venal .1% in the financial sector.

Understand that, and everything the Fed and central banks do becomes perfectly predictable.

A looming tsunami of loan debt repayment requirement.

HELOC – Home Equity Line of Credit.

A majority of HELOC’s issued prior to the 2008 financial crises, have ten year draw periods. Many with interest only payment requirements. At which time the HELOC principle amount is due, either as a lump sum balloon payment, or according to the loan amortization schedule. The majority of these loans are recourse debt, for which the borrow is personally liable, even after a property is foreclosed.

Derivative portfolios are riven with these “asset backed securities” either as CDO’s or CLO’s, in the event of an unforeseen financial shock, such as higher interest rates or a bond market “event” these financial “products” will implode. Taking the house of credit cards down with them. Junk bonds compose part of the mix of “assets” in these weapons of massive financial destruction.

I think most of the people who took out HELOCs prior to 2008 have already foreclosed on their home which included the Mortgage and the HELOC. The Fed probably holds all of those HELOCS anyway and guaranteed the payout to the investors?

Just thinking out loud.

So companies are issuing euro bonds no-holds-barred. From Spanish banks that have unleashed a flood of bonds to Mexico’s teetering state-owned oil company Pemex which sold a €4.3 billion of euro bonds in February.

This is just unbelievable to me. How is this not theft? Forcing institutional investors to invest in worthless companies like Pemex. How else can one look at it, if not as theft?

I read this article twice just to let it sink in. I’m incredulous (tho not surprised) at the level of grift going on in the finance world today, perpetuated and held up by our own central banks. Such an utter shame. AMOT we say in Armenian. AMOT!

Kasadour,

In the eurozone, the residents see this as a combination of screw-your-buddy and living on the credit card, which is paid off using printed money and negative rates which confiscate German savings. Default is a tool yet to be used. Not doing things this way would cost real money to real people in ways that affect real cash. Continental kick the can. It’s in the euro-genes, apparently.

Grift is a good word. You get it. It’s always been there but now it runs the system. A world wide big store being built as we watch … parts already complete. The Euro-store is the most blatant. Japan is mostly self contained and a curiosity. China is a caged monster … pray the cage holds.

The scam is to get new, real money into the system.

Want to join the Eurozone or use you college savings to buy Greek debt?

Exactly. Grift certainly runs the system, and to stop it now would spell disaster in every conceivable way. People will die. The central banks know this, but they won’t publicly admit it. We aren’t stupid- we all know why the elephant is in the room, and what the eventual outcome will be.

The central banks are right in the middle and totally captured.

Trump might have moved to get the Fed back to something more normal. My fingers are crossed.

The ECB runs the Euro-game. It IS the big store. The eurozone is in a death spiral – the speed is up for debate. ‘Grift’ defines the landscape. Now is the time to think of cost containment regarding the after-effects.

China has thousands of years of being in serfdom. A ‘free’ Chinese population is a terrifying concept. A billion or more screaming Chinese who want equality – to be defined ad-hoc- would be world ending. China has my permission to do whatever they want to keep things level.

The BOJ will tell the Japanese Treasury to ‘forget about it’. After a brief scandal, Japanese finance will be in much better shape.

The Fed raising rates to normal is the key to saving the world. And running off the balance sheet.

Kasadour,

For me, it’s far less confusing when you don’t call the Fed, “the Fed”, but rather, “The banks”. There’s nothing independent about it or the ECB. They’re run by the International FIRE sector cabal.

I’m incredulous (tho not surprised) at the level of grift going on in the finance world today, perpetuated and held up by our own central banks.

You’re incredulous? Really? Have you not been paying attention since 2008?

I’ve been reading this blog for about six years. I use the term as an idiomatic expression, like one would say “hold your tongue”. One would not literally hold their tongue, but rather stop speaking or responding, esp. in protest.

When I say “I’m incredulous” I’m saying, I can’t believe it! I do believe it, I’m just expressing complete disgust and disapproval of the aforementioned theft-based system.

The Troika is truly a living, breathing beast in need of a dragon slayer…Think the ECB and NIRP is destructive? The IMF is talking about imposing a 10% tax(capital levy) on all bank deposits in Europe to help with the sustainability of the debt…The IMF also wants Germany to raise property taxes to help balance incomes with the poor…It seems the only salvation at this time is to be a destitute debt slave…

German taxpayers will bend over and grab their ankles on demand for their globalist masters and their bankster partners in crime.

Funny that these posts regarding how dire the European financial system is keeps coming up, and yet the American progressives keep worshipping Europe as an ultimate socialist Utopia.

Takes two hands to clap. The ECB can lower rates and lead the horse to water, but the decision to drink the water is mostly the horse’s. I would suggest changing the title to “It’s Really Crazy What ECB and Yield Chasers Have Wrought”.

No doubt it’s the fault of the government again ….

Given the substantial accumulation of rather questionable assets in the ECB balance sheet, I am curious as to who is likely to incur the losses as these positions over time revert to their realizable value. The Federal Reserve would appear to have made substantial gains to date on assets accumulated during the various QE’s. This seems a very unlikely outcome in the case of the ECB. Unless you are of the opinion that Southern European Long term sovereign debt issued at near negative yields and nominated in Euros has a very high expectation of positive returns in the long term. A number of very bleak alternative scenarios appear likely. Are ECB losses ultimately to be transferred to the tax payers of the Euro Zone countries in general as I strongly suspect? In this case Northern European taxpayers will ultimately be paying for the fiscal adventures of their southern neighbours.