Something is afoot.

The overall figures of relatively sanguine year-over-year rent increases in the US hide the drama playing out city by city, with rents plunging in the most expensive markets while they’re soaring in less expensive markets.

If you’re looking to rent an apartment today in San Francisco, the most ludicrously expensive market in the US, you will run into something that rarely occurred in the past: incentives. Big incentives, not just a gift card.

A search on Craigslist for apartments in San Francisco offering incentives brought up this:

“1 month free” produced 503 results. They include some flukes, like “1/2 month free.” But mostly, the offers of one month free rent sound tantalizing: from “amazing one bedroom in Nob Hill” (one of the more expensive neighborhoods) to “beautiful Hayes Valley” (one of the cooler neighborhoods), and “great walkability” (one of the most important features in a city with nerve-wracking traffic).

“6 weeks free” produced 96 deals, from the “Sweetheart special” to “ideal floorplan” and, desperately, “lease today get six weeks free.”

“8 weeks free” produced 31 results from “gorgeous 2 bedroom” to “love your space” and even more desperately, “don’t miss out!” Then there’s “2 months free” which produced 345 results but included a lot search flukes.

This is like so un-San Francisco. Landlords are actually trying to market apartments and rope in potential tenants. They’re offering deals instead of fighting off throngs of bidders that are jostling for position to submit a whole dossier of how great they are, along with a signed application, without having even looked at the place.

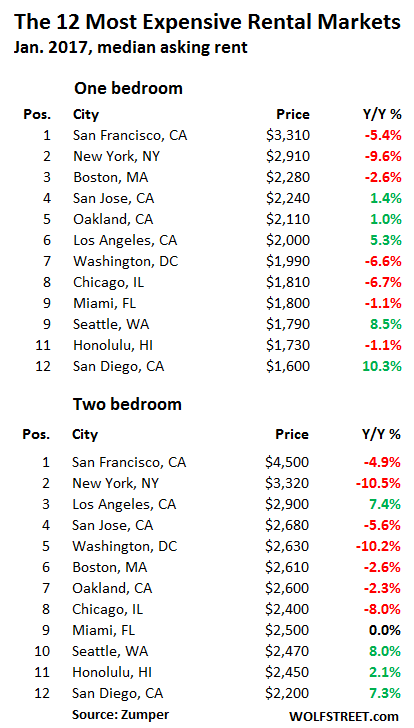

And it shows. In January, the median asking rent for a one-bedroom – not including any of the above incentives – dropped 5.4% from a year ago to $3,310, according to Zumper’s National Rent Report. And median asking rent for a two-bedroom dropped 4.9% to $4,500, which is down 10% from the crazy peak in October 2015.

The last time rents declined year-over-year was in April 2010 as the housing bust was bottoming out.

Zumper tracks asking rents in multi-unit apartment buildings. Single-family houses for rent are not included. And incentives are not included either, nor are actual rents that might have been negotiated down from asking rents.

So add the incentives: If you get “1 month free,” that median two-bedroom rent of $54,000 a year will drop 8.3% to $49,500. On that basis, the rent has plunged 17.5% from its peak in October 2015. Now, if a potential tenant with patience and a willingness to do so in this climate can negotiate two months free….

And there are a lot of units on the market, with a flood of new supply on the way, the result of a historic and still ongoing construction boom of both apartments and condos. Many of these condos have been bought by investors who will either try to sell them at a profit (good luck these days) or rent them out while waiting for better days to help reduce the pain of the stiff carrying costs.

Craigslist has shown its maxed-out number of 2,500 apartments for rent for months. San Francisco is small, a rough square of about 7 by 7 miles. Apartments.com currently lists 2,245 apartments for rent.

“There are signs of hope for Bay Are renters,” says Zumper in the report.

Similar scenarios are playing out in other top rental markets. In New York City, the median asking rent for a one-bedroom, not including incentives, has plunged 9.6% year-over-year and for a two-bedroom 10.5%. The number of apartments listed for rent in Manhattan alone on Apartments.com has doubled since November, when I last wrote about it, from 12,486 then to 25,419 at the moment.

The tables below of the 12 most expensive large rental markets in the US show a lot of red ink where there used to be thick verdant green for the past six years. Note the rental la-la lands of Seattle and Southern California (LA and San Diego).

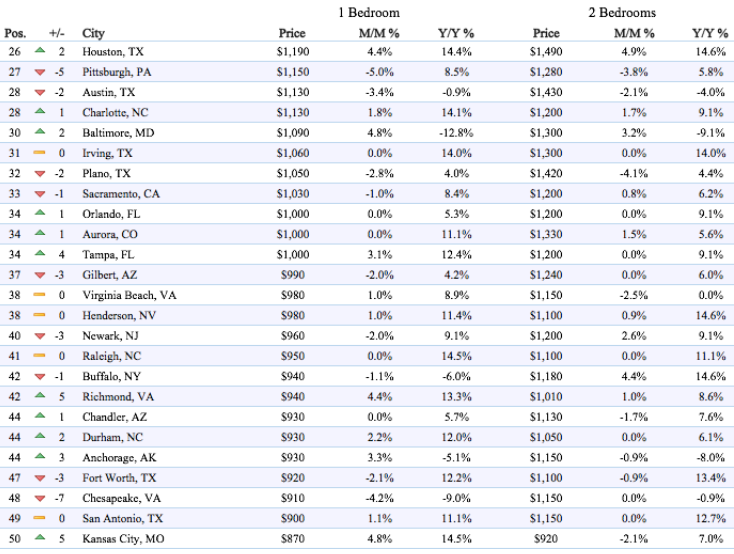

But in many large mid-tier cities – “mid-tier” in terms of the magnitude of rents – rents are surging well into the double digits. Here is a selection year-over-year rent increases based on Zumper’s top 100 most expensive markets:

- #15 New Orleans (1BR +14.4%)

- #17 Philadelphia (1BR + 14.2%)

- #18 Long Beach (again Southern Cali – 1BR +14.4%)

- #20 Minneapolis (1BR +14.9%)

- #21 Dallas (1BR + 14.2%)

- #22 Nashville (1BR +14.3%)

- #26 Houston (1BR +14.4%)

We’re talking a lot about the rising costs of living these days. So if you live in Dallas, and your rent jumped 14% from a year ago, your cost of living surged far beyond what the national averages might suggest.

These plunging rents in some markets and soaring rents in many other markets – the real drama playing out on the ground – are averaged away in the national numbers. According to Zumper, on a national level in January, the median asking rent for a one bedroom apartment rose a practically boring 2.4% year-over-year to $1,143, and the median two-bedroom rent rose 2.3% to $1,358.

Construction booms impact markets with a delay. In Miami, one of the cities with a huge construction boom of apartments and condos, rents have begun to decline just a wee bit on a year-over-year basis. But the condo market is in turmoil [read… Condo Speculation Collapses in Miami-Dade’s Condo Glut].

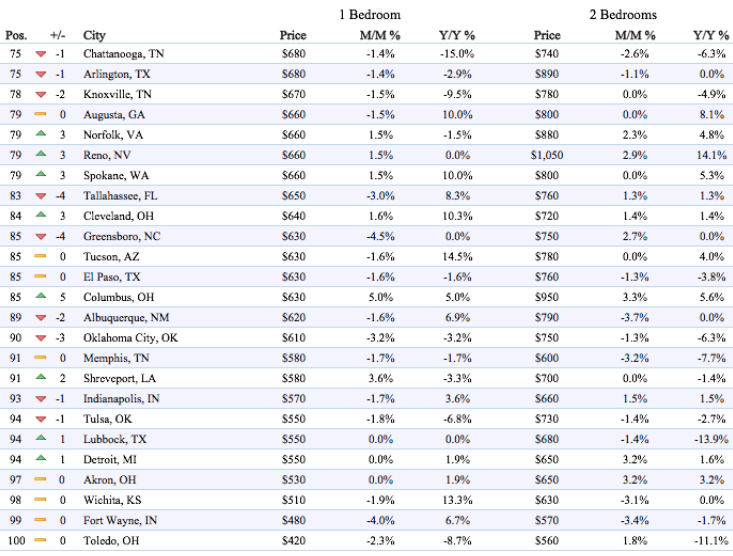

So below are the top 100 rental markets in January, in order of the amount of rent for one-bedroom apartments. Note how in some of the most expensive cities rents are coming down hard year-over-year (Y/Y%), while in many somewhat less expensive cities, rents are surging. Find your city (tables by Zumper, click to enlarge):

And here’s a microcosm of the condo boom-and-bust cycle. Read… The Granular Detail of Miami’s Preconstruction Condo Flipping Bloodbath

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

In Dallas these rents are rising despite building more apartments than any other City in the US. This includes cities that are much larger such as New York Chicago and LA.

Even with this excessive building, demand is still about 30% higher than the new supply coming on board.

A big part of the problem is that there have been extremely few affordable and starter homes being built over the last 8 years. And virtually no new affordable apartment complexes have been built because of scandals and fraud.

Plus, now several local cities, including the city of Dallas, are getting greedy and are increasing regulations tenfold to try to convert rental housing to owner occupant housing.

I say greedy, because as things have developed the truth has come out. For example the City of Dallas publicly shamed the 10 largest “supposed” slumlords and threatened to take their houses away in an administrative move.

The truth is, the city wants the cheap housing destroyed and replaced with yuppie urban duplexes and apartments costing 10 times more. And of course generating 10 times the tax revenue.

And at the same time getting rid of all the social costs of the poor people that were living in the small existing houses.

Even worse, I personally heard at the first public forum the city lawyer respond to the question of “where will the poor people go” with an answer saying “we don’t know… perhaps to one of the further outlying cities.”

One of these landlords, with over 300 houses, does have crappy houses, but he can’t afford to make them picture perfect unless you raises the rent for beyond the current $400 per month. And this economic bargain works for the vast majority of his tenants who stay with him for an average tenancy of 10 years.

His rents are $400 less than one third of the going rate for even dirty and crime infested apartments.

The good, new Class-A Apartments generally run $1600 to $2,000 per month for a one bedroom, and $1,800 to $2,500 for a 2 bedroom.

As I said, the truth came out with the greedy city leaders when he brokered a deal with Habitat for Humanity to replace ALL 300 houses with brand new basic starter homes, for about $80,000 each and the city wouldn’t even listen.

This would also have the benefit of keeping all those 300 families in the same neighborhood in West Dallas, among with their friends and extended families.

Instead, the city wants these houses torn down and replaced with units that range from $250,000 to $500,000 each. And of course populated with professionals that can buy and pay sales tax on a commeasuerate amount of goods and services.

This model, of forcing out landlords and forcing out poor families, is happening in many different cities in the Dallas area.

So beneath the numbers showing great increases in home values and rents, is a quagmire of misery for ordinary people.

The ultimate plan is to house all those displaced people in their for profit prison system, also paid for by those high earners. I already saw this in Florida.

Yup.

CoreCivic (CXW), formerly known as the Corrections Corporation of America, is the largest for-profit prison company in the world. It’s also one of the single biggest corporate blights on humanity… profiting off imprisoning people (and doing so in some of the most corrupt ways possible– bribing judges to imprison people, etc.)

It’s up about 110% since President Trump was elected. Not too shabby.

Petunia, you need to come to Key West as see the show. Rents last year for a matchbox 2 bed, 1 bath walk up at 2,500 a month is now 3,500 a month. Storefront on Duval was 8,000 now 12,000 a month for 1,000sf. net, net, net. A dinner entre at $25 is now $35, a beer at $4 is now $7. You need three jobs and still can’t afford to go to the movies.

How about a Motel 6 style room at $1,400 for 3 nights, not even on the water. A boat dock for 30 foot, from $500 to 950 in one year and it does not even have PIERS but is Euro style with an anchor holding you off.

Greed? Well not if you are so rich you can walk into town and buy 8 houses at 1 to 3 million, and let them sit empty as ..drum roll please…..investments.

Golden geese and angels have a way of flying off. It has happened 8 times in the last 110 years here, it will happen again. The buyers market becomes the rat trap in a heart beat. No one to sell to, no one to rent to, no one to fix a damn thing.

Blackrock sees the writing on the wall, with or without the get-out-of-jail card that Obama gave them last month.

Rinse and repeat.

I was there 2 years ago for 2 days and couldn’t wait to leave. It broke my heart to see how crowded and totally uninteresting it had become. Missed all the key lime pie stands and Fast Buck Freddies (best tee shirts I ever owned).

Thanks for the details of what’s going on beneath the surface. I imagine this is similar in other cities.

It’s basically the ‘white flight’ of the 50s and 60s in reverse. Urban areas are becoming trendy again and the current inhabitants are being pushed out.

It’s interesting seeing this happen, quite literally, before my eyes (I live in Boston). For a few years you get mixed communities in the trendy neighborhoods, before eventually the gentrifiers have totally taken over and there are no true ‘locals’ left. On the flip side, with those higher income earners come better bars and restaurants, nicer shops, etc.

Jd. To meet DJT at WH on Friday to swap brief cases?

Will DJT give back the blackmail warrants to Chase? (Obama’s leverage?)

And for how much?

How did they get away with that in an Obama Administration where low cost multifamily is crammed down the throats of local municipalities. I live in Lafayette / Walnut Creek, CA area (a high end suburb of San Francisco). Both cities have had large apartment projects forced on them by the Obama Administration. This has changed the schools here greatly.

They got caught by Obama’s HUD director for taking $30m for affordable housing and not building it.

Seems like every 5-8 years there is a big scandal where the Good Ol Boy Developers get caught bribing City Council Members (the mayor has very little power) and suborning the planning commission members.

Previously, in the mid 2000s, one big developer got pissed because he got out-bribed by another big developer for tax increment financing for affordable apartments.

He blew the whistle leading to a big FBI sting. It ended up shutting down most of these types of projects in Dallas.

I could go on and on. I really wish I was just making this stuff up.

Even worse, the actual City of Dallas is heavily Democratic and if they hadn’t screwed up so bad Obama would have made tremendous improvements here.

Short memories and no media coverage by choice.

Obama gave an executive order to HUD to cut the language about lenders and FRAUD convections or no contest fines being forbidden to make any loans. Never mind about Congress or the tax payers who are now once again on the hook for these bums.

So much folks do not know about and who benefits.

So many gifts he left us with.

Chris,

In heavily democratic Boulder here.

Can you tell me more about this scandal in affordable housing? How it worked. Can’t imagine the same thing isn’t happening here in Denver/Boulder.

The corporate landlord’s that own large swaths of the residential rental space, have used this “collateral” to leverage their currently held positions in the derivatives sector, all in the name of hedging.

As their higher end holdings begin failing to deliver, they must pressure their mid-tier tenants to take up the slack. Or risk a tranch failure in their derivative holdings.

They are walking a tight rope and know it, as the commercial real estate space has deflated, when they rotated into residential properties and can’t risk a double whammy of reduced income.

wolf,

Quite frankly, i thought the numbers would be weaker in this report, especially in San Francisco and Seattle. I went back and looked at an article you wrote at the end of October last year titled something like ” What the heck just happened to rents” ?

Rents from October 2015 to October 2016 posted very similar YOY changes as rents from Jan 2016 to Jan 2017 in those 2 markets.

Maybe a strong Nasdaq since the elcection prevented a further deterioration, you think ? Do you think that there are clearly more incentives and freebies now compared to last October ?

Dollar is on a weeks holiday and is logically soft?

Let us see how the dollar reacts next week. We may get another lower down spike in rates?

One more time would not be much of a surprise since bond rally is 30+ years young?

Tom,

In the media, the US dollar is presented as very strong. However, it is only strong versus the Euro, Yen and the British Pound. Year over year the USD is down -20% versus the Brazilian real, the ruble and down -15% against the South African Rand. There is currently a massive commodity rally going on as exports from Brazil http://www.tradingeconomics.com/brazil/exports are up 32 percent yoy. Soybean, oil, fuels, sugar…. all up an incredible over 100% year over year. Australian exports soared as well and the trade surplus is the highest ever swinging from AUD -4.3 bn to +3.5 bn – an incredible AUD 8 bn change. I wonder how his could happen when the dollar is so strong against the Euro. Maybe companies finance in Euro and sell their products in dollar.

Well, I have lived within a minutes walk of the Bellevue Square mall in Bellevue, WA since 1995 and i have never seen anything like it.

They built high rise Apartment buildings here like crazy since 2013.

Apartment rents have gone up 50% in 3 years, I’m guessing that it’s because of Chinese and East Indian immigrants coming here to supply the growing tech need.

I wonder if we will follow NY and SF down or if we side step it. Will be interesting

Don’t forget, these are asking rents, and the incentives are strong. All this data is volatile. Last time (2008), the rent downturn took about four years before the Fed’s QE started boosting the SF housing markets. So don’t expect one sudden huge move. But incl. incentives, it has been a pretty good move so far from its peak.

Seattle is on a different timeline. I did mention in a prior article that cracks are appearing, and rents are about flat with September. The big surge in rents was earlier in 2016, and now there’s sort of a loss in momentum. But YOY, rents are still up a lot.

The process is like watching paint dry … that’s why I don’t write about it on a monthly basis :-)

I agree. Sherwin Williams day in and day out.

I still think as long as FB,AMZN, GOOGL, CRM et al. continue to post impressive growth there will be tech hiring and therefore supporting the buoyant rental market here in the Seattle area. And as long as ORCL, CSCO, MSFT, et al don’t announce layoffs.

Salesforce.com will occupy a brand spanking new building in downtown Bellevue. It’s almost ready for move in.

All in all it’s difficult to forecast 12 months out. This tech led economic expansion is the 2nd longest since (95 months) WW2. Nuts Oh hazel nuts !!

It takes time to play out like the last bubble crash. My assumption is while new units come on line the prices are sticky as the landlords hope for a positive change in the market. Having units sit empty for a few months finally motivates incentives. Once jobs begin to roll over and vacancies grow this is going to really get interesting,

The whole downward spiral started probably 3-4 month; so, this is just the starting point; once this gets momentum, they have to decrease their rent demands by at least 40%; if the economy tanks, they will have to go even lower.

So many buildings have apartments which have been vacant for months, but they don’t advertise it since many are run by large property management companies.

But whether they compete for a share of market now, or later, they will eventually have to try to rent those apartments.

Also, I think there are many unadvertised layoffs in tech sector, and no one in their right minds would stay in Bay area when they can’t get another job. Way too expensive in comparison to other locations. So, they move to other cities.

My comment above is only about Bay area; I have no idea what other markets are like.

I actually moved away from the Bay Area this summer. I wasn’t laid off, but was part of a re-org in which a chunk of people left voluntarily. Some of those people did to move Austin, Seattle, etc.

I cashed out since I saw what happened to those that were hit in ’08. When your home value tanks, and jobs are hard to come by it becomes a miserable situation. I saw people that were normally happy become beaten down by the pressure of keeping up a mortgage payment and undertaking a 3 hour round trip commute.

Both my wife and I work, but we wanted to move somewhere that one income was feasible…just in case something happened. Now live somewhere where our mortgage payment is 1/4th what it was in SV, our commutes are just a few minutes, and our kids don’t need to share a bedroom.

Yes, good move; Bay area and SV are really more hype than anything else; and as tech spreads to other cities, it is preferable to live in other areas.

Just a short funny story; whenever I fly back to SF and the plane has stops in other cities, I get depressed when it gets to SF airport.

Plane stops in other cities such as L.A., Denver, Dallas, and the women dressed up as if they are going to a party get off; then the plane gets to SF airport, and all these passengers who look like hobos get off; they seem as if they haven’t taken showers for days, and of course forget about how they are dressed; we are lucky they don’t wear their PJ’s on the plane. And this is the tech center of the world!

San Francisco

We escaped form SOMA last year and moved to the financial district because SOMA became to disgusting. For over a year now the City has way too much filth, human waste, crazy people, junkies, violent “youths” and incompetent governing. Without a major change in local governance, this city will fail big time and all that wealth invested here will simply disappear, like Detroit.

Even if rents dropped by 70%, I am leaving. It has become disgusting.

In summary, there are more than just economic factors working here.

There is the QUALITY OF LIFE and it keeps crashing at a fast rate.

You guys fail to understand the massive stealth immigration going on in the USA. Obviously this drives up rents and housing prices.

In my area on the urban East coast I am astounded by the number of Chinese who have flocked here over the last 5 years. From virtually none, to virtually everywhere. Saw the same thing happening in cities I work in the Midwest.

Students, visitors and temp visa holders buy up homes then the whole family moves in from abroad. The notion that people actually need visas once they get here is quaint.

I see this getting worse with Trump as sanctuary cities double down on their ‘open door’ policy.

This is bad news for young people who have to compete for homes and apartments with foreigners. I think back to my own youth and realize how lucky I was not to have to compete with the whole world for every last nickel.

Immigration over here can’t get more massive than this in Bay area; and the immigration card is played by real estate agents in all countries from Australia, to Canada, to US, to even Uganda.

According to Ozies, everyone wants to live in Australia, and all they have to do it to open the door and a 100 million will go to Australia to buy houses.

dunno where this is headed, but real estate tends to fluctuate in long waves, punctuated by volatility up, and slides down.

or as a friend of mine once observed “they all say that.”

I am not seeing rent declines at all in Chicago. Nowhere. I’m seeing the opposited. Higher rent places going up and being filled immediately.

I think I read it somewhere, maybe one of Wolf’s articles, that Chicago has huge pension problem. So, they have to increase property taxes. Maybe that tax increase is being channeled to the renters.

I walk in downtown Seattle daily. All I see is cranes & construction as far as the eye can see. Most of the land application signs say >40 story residential tower slated for construction. Not sure if they’ll all be apartments or condos…? I’ve never seen anything like this, even during the dot com bubble. It doesn’t seem sustainable to me.

Seattle Times had an article with a great graphic of the number of cranes in cities across the US – Seattle has most in nation, with only Chicago even close. Almost 3x NYC; similar in comparison to SF. Amazingly, here in PDX there are actually slightly more than either SF or NYC.

http://www.seattletimes.com/business/real-estate/seattle-is-again-crane-capital-of-america-but-lead-is-shrinking/

Welcome to my world. No land, no bucks, on my way into a cold Canadian crate. Say good bye to everything that made Seattle special -places, people and things.

High priced homes feed high salaried civil servants. Do you really think they’d be destroying the city if every politician, paper pusher and cop wasn’t getting a piece? People talk about these projects like unexpected weather, when they’re a planned wealth transfer from the poor to the rich.

The investors make out and so does your local police (who will be arresting you for loitering).

https://thetyee.ca/Opinion/2017/01/30/Vancouver-Plutocrat-Playground/

What is the on the ground situation like in New York City? It looks like it has suffered the most dramatic of these declines, with less than 10% year over year. Still way overpriced, but IMO it probably shows that the Big Apple has lost its lustre.

The job market in NYC is probably weak, and I’d be interested if the same is true in many major metropolitan areas in the US.

The rents in second tier cities are increasing, as shown in the reports. Why are they increasing? Is it because people are moving out of the costliest cities and moving in to these second tier cities? How do these officials know people are flocking to these second tier cities? Is this the way it goes… Former new york city renters flocked to philadelphia. City officials notice this increase of wealth, so they feel they can get more money for rent.? Second question is how do these “city officials” know people moving into their cities? It seems like they have their eyes on every piece of Data*. Which f’n scary.