Going down the drain, putting this wondrous stock market at risk?

Companies in the S&P 500 spent about $3 trillion since 2011 to buy back their own shares, often with borrowed money. It’s part of a noble magic called financial engineering, the simplest way to goose the all-important metric of earnings per share (by lowering the number of shares outstanding). And it creates buying pressure in the stock market that drives up share prices.

With buybacks, you don’t need to sell one extra iPhone to boost your earnings per share. So the amounts have grown and grown. With ultra-cheap money available to borrow endlessly, companies take on debt and hollow out shareholder equity. It has worked like a charm. Stock prices have soared. Declining revenues and earnings, no problem. But something is happening that hasn’t happened since the Financial Crisis.

Share buybacks in the third quarter plunged 28% year-over-year, to $115.6 billion, the biggest year-over-year dive since Q3 2009, according to FactSet. It was the second quarter in a row of declines, from the glorious Q1 this year, when buybacks had reached $168 billion, behind only Q3 2007 before it all came apart.

From that great Q1 2016 to Q3, buybacks plunged 31%, or by $52 billion.

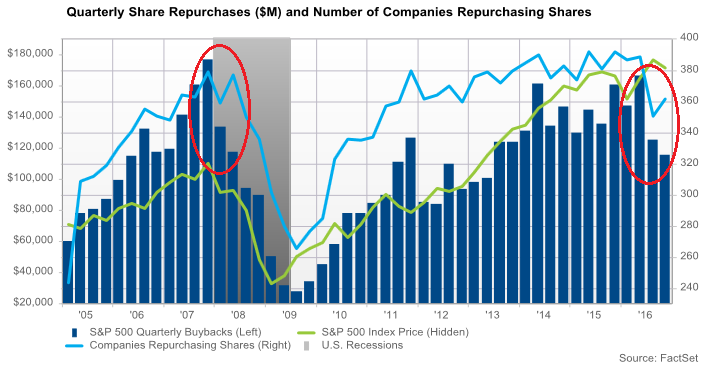

“Only” 362 of the S&P 500 companies bought back shares in Q3, the second lowest number in three years, with Q2 having been the lowest number (blue line in the chart below).

However, the third quarter has historically produced the most buybacks as companies are feverishly trying to put some lip gloss on their annual earnings per share. But not this time.

In this chart by FactSet, I circled the phenomenon of that $52-billion two-quarter plunge (blue bars). Only the $58-billion two-quarter plunge in 2007/8 was bigger:

Even the near-record share buybacks in Q1 could not overcome the plunge in Q2 and Q3 and pull out the tally for the trailing 12 months, which declined 2.6% from a year ago to $556.6 billion. That’s still a lot of moolah dedicated to nothing but propping up their shares.

The number of S&P 500 companies making buybacks of $1 billion or more dropped from 43 a year ago to 33 in Q3.

Apple retained its crown in this elect field with $7.2 billion in buybacks in Q3, followed by GE, distantly, with $4.3 billion. Over the past 12 months Apple repurchased 31.1 billion of its shares, GE $21 billion. Here are the ten biggest buyback queens:

- Apple: $7.22 billion

- GE: $4.29 billion

- Microsoft: $3.55 billion

- Allergan: $3.19 billion

- McDonald’s: $2.77 billion

- Citigroup: $2.53 billion

- JP Morgan: $2.29 billion

- AIG: $2.26 billion

- Home Depot: $2.14 billion

- Yum! Brands: $2.09 billion

Tech, thanks to Apple and Microsoft, remained the largest “buyback sector” – this sort of financial engineering lingo grows on you after a while – with $27 billion, or 23.4% of total buybacks. Financials are in second place with $25 billion, or 21.7% of total buybacks.

But buybacks by all major “buyback sectors” declined. Major excludes the Real Estate, Telecom, and Utility sectors, which averaged less than $2 billion a quarter in buybacks. Buybacks among Financials declined only 3.6%. The remaining “buyback sectors” experienced double-digit plunges. There are the most magnificent “buyback sector” dives, in Q3, year-over-year:

- Energy: -62%

- Materials: -55%

- Information technology: -41%, dragged down by new-found stinginess at Oracle, Intuit, Motorola, and Apple.

- Industrials -36%, dragged down by Honeywell, Quanta Services, and Caterpillar.

Despite the decline, buybacks remained a huge buying force in the market. At the end of Q3, trailing 12-month buybacks ate up 66% of net income, about the same as a year ago, with 119 companies in the S&P 500 blowing more on buybacks than they generated in earnings. And 109 companies blew more on buybacks than they generated in free cash flow. As ludicrously high as this sounds, it’s the lowest count since Q2 2013.

And much of it is funded with debt. Over the past three years, aggregate debt of the S&P 500 companies has grown 1.7 times faster than aggregate cash and short-term investments, according to FactSet.

Even Apple, which is swimming in cash, has borrowed megatons because much of its cash is registered “overseas” and represents profits that have been sheltered from US corporate income taxes by being registered “overseas” though much of the “cash” is already invested in US securities but it can’t be used for buybacks [read… Come on Moody’s, Spare us these Falsehoods: That $1.3 Trillion “Overseas Cash” is Already in the US].

This is a nasty wrinkle in the buyback scenario. But there’s hope. Trump has pledged to change the corporate tax code, and/or give corporations a tax holiday on this “overseas” cash so that they can “repatriate” it, by selling their US Treasurys and other investments and using the proceeds to buy back their own shares. That’s what happened last time the government granted this kind of tax holiday in 2004. And everyone is hoping that it will happen again. I suspect that’s one of the reasons for the surge in stock prices since the election.

If not, and if this major stock-buying force continues to wheeze like this, our eternally wondrous stock market might be in serious trouble.

GM has been reacting to its fabulously ballooning inventory glut by piling incentives on its vehicles. But that hasn’t worked all that well. Now it’s time to get serious. Read… “Car Recession” Bites GM: Inventory Glut, Layoffs, Plant Shutdowns

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“This is a nasty wrinkle in the buyback scenario. But there’s hope. Trump has pledged to change the corporate tax code, and/or give corporations a tax holiday on this “overseas” cash so that they can “repatriate” it, by selling their US Treasurys and other investments and using the proceeds to buy back their own shares.”

Yeah but I think we know the above will happen so Dow 30K soon?

exchange rate risk?

So does this mean I, a little peon, get to be the beneficiary of a ‘tax holiday as well ….. because I, and many millions more, could sure as hell use one !

If the next four years turn into the last four years .. then i’ll bet dollars to donuts we’ll have our civil war 2.0

Why would there be a civil war? Game of Thrones is still playing on TV.

Rule No 1 in Murica: “You can’t rely on muppets.”

Trump is the biggest con in American history. I expect nothing to change and actually potentially get worse. Conflicts of interest all over the place, his family sitting in on meetings, his Gilded Age cabinet. There won’t be a Civil War. His followers will go back under the rock from where they came. Automation is what is killing blue collar jobs. And the fact that America was a hub of manufacturing was a byproduct of World War II and the fact that Europe and Asia were destroyed. The fixes for unemployment are much more complex than a stump speech by either party.

I’m a novice. Can you explain what you means when you say ” With ultra-cheap money available to borrow endlessly, companies take on debt and hollow out shareholder equity” How does this erode shareholder equity?

Thanks!

They take on loans, a liability. They then buy back shares with the loan money. Balance sheet increases debt while reducing equity. Pretty easy..

When Wolf says Balance Sheet, what he means is the following:

Assets = Liabilities + Equity

This is Accounting 101 and is literally the first thing you learn if you take classes/read books on the subject.

To put that in concrete terms, let’s assume your “business” is a rental house, worth 100,000, of which you owe 50,000 in mortgage loans. In this case, you would have 50,000 in equity.

Taking it a step further, a real business might issue shares to raise money (let’s assume you issued 50 shares at 1,000 each to friends and family) to raise money (they gave you 50,000 and you gave them shares). So, 50,000 came from the bank and 50,000 came from share holders.

All we did here is assign the equity to someone at some value (share price). To summarize:

100,000 = 50,000 + 50,000

If you followed this far – there are all sorts of metrics (some of which might trigger bonuses for management) that are share price driven – so a HIGHER share price means rewards for certain folks.

So, if you took out a loan, for say, 25,000 and bought back 25 shares at 1,000 each, now it looks like this:

100,000 = 75,000 + 25,000

The number of shares outstanding went DOWN, thus any metrics based on shares (such as EARNINGS PER SHARE) change accordingly.

Reality is a lot more complicated – for example as companies attempt to buy back shares to prop up share based performance metrics (because reality isn’t all that great), they force their share price higher. What Wolf is doing is tracking how MUCH money in aggregate is being blown on buybacks and highlighting that as it slows down, the buyers keeping prices up also might disappear – and stock prices will then reset lower.

And the company will still have cash going out the door on all those loans they took out to buy shares back at inflated prices.

Hope that helps.

Regards,

Cooter

It’s very simple. If you make a 100,000.00 dollars a year and you rack up debt of 75,000.00 your equity is now only 25,000.00. This is what he means by eroding share holder equity. it always gets back to your balance sheet.

Maybe this is part of the upward pressure of late? More money will be allowed to be used for buy backs in the near future. It doesn’t make much sense that all of the sudden people will have more money to buy products.

They’d be dumping treasuries to do this as others are dumping them for other reasons as well. uh oh.

The recent selling of credit eliminates the liability and results in credit destruction.

The gain or loss has been realized and use is no longer necessary and gain is increasingly likely win win

Does anyone have access to the customer flow reports from baml.com, by analysts Subramanian and Hall?

They used to be freely accessible on the web but now BAML has locked them up. These reports had great information on buyback as well as about 4 other categories of flows .

While buying back some shares can steadily improve EPS, what is the effect if a company’s EPS turns negative?

They’ll stop buying back shares long before the losses set in. Reducing the share count makes negative EPS look even worse.

That’s one of the reasons money-losing companies like Tesla like to ISSUE new shares (in addition to needing more money to burn through): more shares outstanding reduce negative EPS.

But TESLA is a WONDERFUL electric vehicle manufacturer, best thing since sliced bread?

At what price? ;-)

Regards,

Cooter

would venezuela’s and india’s stunning demonitisation be a reason for reduced buybacks?

when is facebook’s 6 billion in buybacks supposed to happen?

I don’t do FB so I can only speak to the other topic.

Indians and Venezuelans usually invest in tangible assets like businesses they actually run, real estate, even gold and silver. The stock markets have generally not been their thing. They are also big holders of cash, which is why the govt is forcing them to exchange notes.

You’re forgetting that capital gains taxes will be slashed next year. Trump’s infrastructure plan is the least likely part of his agenda.

Hence ‘cash repatriation’+Lower capital gains+ no infrastructure plan + no more SEC= low rates forever

The stock market is a perpetual motion cash machine. Don’t like it, but that’s just the way it is. There will never be a chance to buy the dip or clean up again. Just buy an index on margin and watch the money roll in!

I heard the Russell 2000 is trading at near a 1000 P/E ratio or maybe even negative P/E you include all the 2000 companies in the ratio (and don’t kick out the losers to make it look better – like Russell does).

Those companies will have to buyback a lot of stock to improve the P/E.

Of course, people get fired on Wall Street for mentioning these things.

IWM is biggest joke index eva

Is FULL EMPLOYMENT fake news? I mean I’ve followed Japan’s employment rate for decades and it’s rarely been over 3%, much better than US and look where they are (Is their economy really so bad?)

Oh, isn’t all the “smart” corporate debt denominated in those depreciating currencies such as Euro (which might actually disappear?), while $US denominated debt has become an anchor to corporate profit?

So while for instance AAPL may have sold tons of bonds, were they denominated in pesos and euros?

dollars and euros.

“U.S. issuance has risen since 2011, totaling $92.49 billion last year, a number also topped only in 2007. The four biggest U.S. corporate Eurobond offerings over the past six months include an €8.5 billion ($9.5 billion) issue from Coca-Cola Co., a €3.8 billion issue from AT&T, a €3 billion offering from Berkshire Hathaway and a €2.8 billion issue from Apple. McDonald’s sold $2.3 billion of euro-denominated bonds.”

Whistle blowers fired.

http://www.financial-planning.com/news/ex-federal-investigators-supported-rias-whistleblower-claim-against-jpmorgan

There seem to be some really smart people commenting on this site. I would like to know what they think about the stock market and its current valuations. Seems to me like it is has been over inflated by “free” money and now has no way to correct. Please feel free to respond, especially Wolf!

The over valuation of the markets have both a structural aspect and an economic aspect. Structurally the stock buybacks have created a shortage of available paper to bet on (buy). The shortage pushes prices higher. The economic aspect is that, cash made both in the markets and outside, has nowhere else to go right now. Real estate is just as over valued and much less liquid. This is also pushing the price of the paper higher.

As far as the new administration is concerned, Trump has committed himself, by word and deed, to spend. They will slash from here and spend there, with an upward bias. This too will push the markets up.

Having said this, all the momentum will come from financial engineering. I don’t expect the earnings to be all that different, until employment is expanded.

Thank you for your reply, you seem to very knowledgeable based on your past posts.

It is my understanding that the stock market has been or should be based on a company’s performance, the better a company does the more valuable the stock. Since there really hasn’t been any outstanding performances in the corporate sector in the past 8 years the market appears to have been buoyed by the buy backs via “free” money, which has caused a rise in value/pricing. This all seems artificial to me and unsustainable long term. I would think somewhere along the line the “piper will need to be paid”. Am I way off base on my thoughts?

The value of companies listed on exchanges have been disconnected from their business activities for decades now, definitely since the 80’s. Most of the money these companies used to expand didn’t come from operations, it came from Wall St. When big box store X built more stores in your area, it wasn’t because profits were exploding, it was because they raised more money on Wall St. Most of the earnings and valuations are creations of the accounting world, but everybody is willing to go along to get along, until they’re not.

It’s important to note that from a financial theory perspective share buy backs do not create economic value. Look at it this way: If I buy one share of Intel then my net worth did not change given that I bought that share at fair value. If I can buy a share of Intel and create zero value then why would Intel create value by buying that same share? Simple…it can’t and doesn’t. The only way value is created is if the share was bought at a price that was less than fair value. If we are in a stock market bubble then by this measure companies are destroying value by buying back shares at a price that is greater than fair value. In this market share buy backs destroy value not create it.

Precisely, which is why I never chase buybacks, I rather consider them an opportunity for exit. One exception though, additional to your more obvious point, is on the side of the capital raise. Say for instance the fine print of conversion to common equity in case capitalization falls below some predetermined level or results work in disfavor of the bond buyer, no?

There are two sides to every trade, insiders are paid to make good decisions or maybe they’re paid to protect their best interests such as distributing their stock options into strength.

Gotta do your homework, this is one aspect I don’t see being stressed by bloggers criticizing something they don’t understand in detail and it explains how people miss out on opportunity.

Didn’t Carl Icahn push for the Apple buybacks? And then dump all of his stock mid-2016? And now he’s set to influence the SEC directly?