Their bone-chilling chart.

Everyone is fretting about the Canadian house price bubble and the mountain of debt it generates – from the IMF on down to the regular Canadian. Now even the Bank for International Settlement (BIS) and the Organization for Economic Co-operation and Development (OECD) warn about the risks.

Every city has its own housing market, and some aren’t so hot. But in Vancouver and Toronto, all heck has broken loose in recent years.

In Vancouver, for example, even as sales volume plunged 45% in August from a year ago – under the impact of the new 15% transfer tax aimed at Chinese non-resident investors – the “benchmark” price of a detached house soared by 35.8%, of an apartment by 26.9%, and of an attached house by 31.1%. Ludicrous price increases!

In Toronto, a similar scenario has been playing out, but not quite as wildly. In both cities, the median detached house now sells for well over C$1 million. Even the Bank of Canada has warned about them, though it has lowered rates last year to inflate the housing market further – instead of raising rate sharply, which would wring some speculative heat out of the system. But no one wants to deflate a housing bubble.

During the Financial Crisis, when real estate prices in the US collapsed and returned, if only briefly, to something reflecting the old normal, Canadian home prices barely dipped before re-soaring. And this has been going on for years and years and years.

The OECD in its Interim Economic Outlook warned:

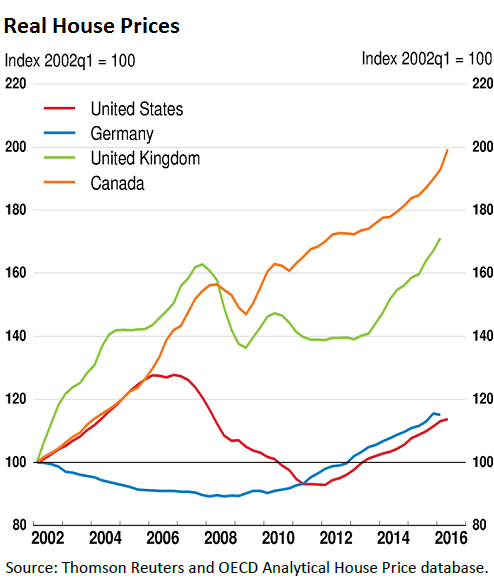

Over recent years, real house prices have been growing at a similar or higher pace than prior to the crisis in a number of countries, including Canada, the United Kingdom, and the United States. The rise in real estate prices has pushed up price-to-rent ratios to record highs in several advanced economies.

Canada stands out. Even on an inflation-adjusted basis, Canadian home prices have long ago shot through the roof. The OECD supplied this bone-chilling chart. The top line (orange) represents Canadian house price changes, adjusted for inflation:

In the US, several national indices have now exceeded the crazy prices of the Housing Bubble that started blowing up in 2006. In some cities, the median price has shot way past the prior bubble highs – in San Francisco, by over 50%! But other cities have lagged behind, and the national averages paper over the local bubbles.

In Canada, real estate is more concentrated. The Canadian market is about one-tenth the size of the US market. But the two largest local markets, Toronto and Vancouver, together make up 54% of the Teranet National Bank House Price Index. So when these two local bubbles begin to deflate – or implode – they will create enormous havoc across Canada.

Real estate is highly leveraged. It’s funded with debt. Many folks cite down-payment requirements in rationalizing why the Canadian market cannot implode, and why, if it does implode, it won’t pose a problem for the banks. However, an entire industry has sprung up to help homebuyers get around the down-payment requirements.

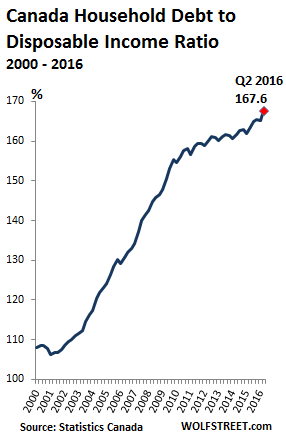

So household debt has been piling up for years, driven by mortgage debt. Statistics Canada reported two weeks ago that the ratio of household debt to disposable income has jumped to another record in the second quarter, to a breath-taking 167.6%:

The BIS now too, in its Quarterly Review, jumped on the bandwagon of issuing ineffectual warnings about this pile of debt, fingering particularly China – and in the same breath Canada:

According to the BIS early warning indicators, which are intended to capture financial overheating and potential financial distress over medium-term horizons, credit growth continues to be unusually high relative to GDP in several Asian economies as well as in Canada.

Estimated debt service ratios, which attempt to capture principal and interest payments relative to income, appear to be at manageable levels at current interest rates for most countries, although they point to potential concerns in Brazil, Canada, China, and Turkey.

The BIS developed a metric – the “credit-to-GDP gap” – that compares current credit levels to long-term trends and serves as an early warning indicator for financial crises.

Everyone wants to know when the next financial crisis happens. It will happen, but once again, it will surprise the economic establishment because, in the eloquent words of the BIS, debts always “appear to be at manageable levels” – until suddenly, they’re not.

The country with the highest credit-to-GDP gap is China (30.1), and the second highest is Canada (12.1). When it comes to debt creation, it’s not a good idea to be mentioned in the same breath with China. Turkey (9.6) is next in line. Then Mexico (8.8). And Brazil (4.6). Oh, and Australia (4.4)! So housing-bubble Canada is in excellent company!

The only saving grace is the permanently near-zero-interest-rate environment. Because that’s what it takes to keep this thing from deflating, according to the BIS, and even then there are “concerns.” But these countries, particularly Canada, are going to be in trouble when rates rise even a little.

So have central banks painted themselves and their entire bailiwicks into a corner with their ingenious emergency policies that have been dragging on for eight years? You bet. Is there a way out? Nope. Not a good one, at least. It’s just a question of when and how – and who gets to pay.

But the Fed is steadfastly blind to bubbles and their consequences. Read… OECD Warns Fed, BOJ, ECB of Asset Bubbles, “Risks to Financial Stability,” Pinpoints US Stocks & Real Estate

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am contemplating a job offer in Toronto but I currently live outside the Toronto/Vancouver bubble zone. Even with a significant raise, the prices of housing and electricity in Toronto make the move pretty daunting. I’ll probably remain on my one acre lot with my reasonable mortgage and a 15 minute commute to work every day. I feel like I would be buying in at the top of the market and even then I could only afford a town house or condo.

Toronto is fine if you haven’t succumbed to the psychosis which treats a stickframe house and a stamp of land as the summit of all asset classes and a necessity. I live downtown with a wife and daughter, we pay $1100/mo. I’m a 10 min streetcar ride from Bay Street. You could easily sell, rent until the bubble pops (6-12mo, depending on whether we tax/ban the mainlander criminals doing the buying), and then use your cash from the sale to buy one of the thousands of cheap investment properties gullible Shenzhen money launderers are desperately trying to dump.

amen.

Most are fleeing now as Vancouver is overrun by criminal mainland trash.

Hopefully extradition and Operation Fox Hunt stops my city from being the chinese scumbags #1 destination for hiding out and dumping there dirty money.

Given the lax lending criteria, and market based, rather than replacement based building (less actual depreciation due to fair wear and tear, (e. g. roofs, water heaters) appraisals, why would anyone expect anything different?

The lenders have major accountability for this R/E asset bubble.

First they must limit the fixed rate, amortizing, max twenty year term mortgage size such that interest, principle, and escrow payments are not more that 1/3 the annual income of the borrower(s).

Second *ALL* the borrowers debts/payments must be considered in this era of usurious credit cards, and 84 month car loans. (Student loans are a big factor in the US, don’t know about Canada)

Third, the mortgage must not be based on inflated “bubble” valuation, but rather on replacement cost of like kind and quality, less fair wear and tear depreciation.

Forth, the economic sectors in which the borrowers are employed should be determined because this may be in the boom/bust sector, which is driving the asset bubble.

Yes this will significantly restrict home ownership, but the alternative is repeated R/E asset bubble and crashes, and we do people who are unlikely to be able to repay a mortgage no favors when one is made.

Almost all politicians, home owners and potential buyers are going to disagree with your proposal. Zero chance of ever happening although I agree that these are good suggestions (there are plenty more that would be needed …) that would work out much better in the long run.

However, in the short run these suggestions would be so painful for many homeowners, housing speculators and bankers that politicians chose to kick the can down the road again, and hope the market doesn’t crash while they are in office.

Just imagine what would happen in Netherlands where most buyers start out with a 103% mortgage, based on ridiculous home valuations. Most who purchased in the last years are already under water to start with, all your proposals would lower the value of the home (severely) and mean they are so far under water that they will never recover in a lifetime and have a fatal problem when the mortgage runs out (if they are even able to keep paying, good luck with that as the current mortgages often have 0.5-1% interest rates so they can only go up).

Which in the Dutch situation would mean that the Dutch state is bankrupt too, because they more-or-less guarantee over 90% of the mortgages (mortgage debt around 800 billion) against financial loss when selling the home. Most other countries are in less dire situation but in most of the West there is no way back without causing the biggest RE crash in history. And think of all the social and political upheaval when people find out that all the things they were promised by politics were lies (like getting rich quick with RE, and living far beyond your means thanks to the home piggy bank) or that all the stuff they feel entitled to is suddenly out of reach (like buying your own home, even if you have never worked and have loads of student debt etc.).

Germany went crazy over the dot.com boom, in the bust its version of the NASDAQ lost 97%,, to help Germany the ECB lowered interest rates.

Housing bubbles blew in Greece, Spain, Ireland and Holland.

Holland is the last bubble still inflated with the desperate measures you mention.

no, the ECB didn’t lower rates to help Germany. The dot.com boom was relatively unimportant for the German economy and most of Europe (I worked in the tech sector then, I know …).

One of the ECB’s first objectives in lowering interest rates was to keep Spain with its huge RE problems above water. Many Spanish home owners had mortgages directly tied to Euribor, Mario Draghi made sure that they could stay in their home for little (way too little …) money to keep the housing market inflated. If Euribor really goes back to a normal 5% or more, the pain in Spain will start for real.

There currently are housing bubbles in many EU countries, but often mostly in the metropolitan areas (where the international money arrives first) and tourist areas (speculator homes). Much of Scandinavia has housing bubbles as well.

It is difficult to tell what is a bubble because organizations like OECD usually only look at home prices for the last 10, 15 years. If you do that for Netherlands there is hardly a bubble to be seen, the big gains happened in the nineties and those prices have become ‘the new normal’.

I have seen a graph of the German version of the NASDAQ it fell by 97%.

It had a massive effect on the German economy.

It’s in this video:

https://www.youtube.com/watch?v=8YTyJzmiHGk

55.44 mins.

Before that he shows the effect on the German economy as they repaired there balance sheets.

The Neuer Markt, it was so bad they changed its name to TecDAX.

“The lenders have major accountability for this R/E asset bubble.”

I agree, in principle, but in practice, the CMHC insures most of the domestic mortgages, and are going to have to do the actual “accounting” in most cases..

George Mcduff…. Your appraisal theory is way off because you aren’t considering real estate is both land and buildings combined. Appraisals are based on market evidence first and further supported by a cost approach which takes a replacement cost new less all forms of depreciation(physical,functional and economic). What you are failing to realize is the underlying land value the home is built on is what is appreciating due to scarcity of supply relative to the overwhelming demand from foreign investors and the artificially low interest rate environment. A house is always depreciating but you forgot to consider that the land the house is built on is still appreciating (for now) through supply/demand factors. Overpriced real estate none the less but blame low interest rates and uninformed buyers.

There are local websites that give actual data. The soaring prices are yoy, they are down quite sharply since February fyi..

The Canadian government has floated the idea of a deductible when the government insurer of mortgages CHC has to reimburse a bank for a sour loan. They figure it might make the banks more cautious.

The banks don’t like the idea.

BIS and OECD warned about the Dutch housing bubble several times over the last 10-15 years; nothing happened, except that OECD changed some of their statements later on under heavy pressure from the Dutch government (or from the banksters, more likely).

And if that chart is correct the Canadian bubble is a joke compared to the Dutch one; just 100% increase in 12 years, what are we talking about??

The Dutch had 500% price increase (median home price for the whole country) between 1985 and 2002, and prices have increased 2-3x since then in many areas. Also the REAL price increases are bigger than the median numbers suggest, because the statistics severely underestimate the price gains in many ways. This is primarily because the homes that the statistics track keep changing (e.g. during the nineties many big canal houses were split into 4-6 ‘cheap’ apartments, and around 2000 a flood of old former rental housing was sold by housing corporations). The median home of 2015 is far less home (smaller and lower quality) than the median home of 1985; this might apply in Canada as well, but I doubt it.

The chart is inflation adjusted – that’s why I posted it. Makes a HUGE difference over the years and decades, especially during times of higher inflation, such as the 1980s.

OK, thanks for mentioning that because I hadn’t noticed; that explains part of the big difference.

But even in this case the price gains are small compared to Netherlands. Dutch household income has roughly doubled from the start of the housing bubble, mostly because we now have far more two-income households. Official inflation is probably far below 100% over the last 20 years (5-10% in the early nineties, but after that always in the 0-3% range).

I know, I keep coming back to this axiom.

The first rule of economics;

All debt will be paid.

Either with dollars worth pennies, or with pennies worth dollars.

It will be paid.

A reset must occur. It will occur. This is another axiom.

Just a matter of timing.

“I know, I keep coming back to this axiom. The first rule of economics; All debt will be paid.”

Hooey, I say, hooey. Debts that can’t be paid, won’t be paid. And aren’t paid. People do get haircuts and it’s not all long blond tresses, you know.

When houses start looking like tulips to you it’s time to get out of the residential market.

Those lucky Canadians, all getting rich selling overpriced houses to each other with money conjured up on disposable phones. Someday it will all fall apart and they can blame Putin. Or it is Obama? I forget.

TRUMP…… I think

walter –

As in all financial contracts when a debt is defaulted on, who is the loser and who is the winner?

The debtor has the underlying asset seized and the creditor loses the balance of their investment, that the seized asset does not cover.

In today’s upside-down financial investment market, when this debt is ‘serialized’ into derivative packages and sold on to other entities, guess who these “other entities” mainly are? If you said pension funds, or insurance companies you would be right.

Do you receive a pension? How about a retirement insurance policy such as “Freedom 55”? Now guess where they get their income from? If you said bonds and the market you are right.

Now guess what happens when the income stream dries up because of debt defaults. Ding! Ding! Now you get it!

In the end – all debt is paid. One way. Or the other.

“Now guess what happens when the income stream dries up because of debt defaults.”

But how can there be debt defaults if “all debts get paid”?

Are houses starting to look like tulips to you?

Walter –

Use your thinking cap, other than keeping your head warm!

The debt is paid. Either with dollars worth pennies, or with pennies worth dollars. What is not to understand?

In each instance the debt is discharged.

And the payer is ALWAYS the same: the taxpayer.

Good subject, but has the superficial tone of double speak begging to be ignored.

No, what cannot be repaid, will not be repaid. Simple, but not without consequences. It could be through bankruptcies, or the infamous idea of a debt jubilee, but the debt “numbers in accounts” will be reset. The wider the net the less onerous it will be.

About 10 years ago the Canadian dollar was 10% more valuable then the

American dollar. Since then it has fallen off a cliff. If the chart were

to reflect prices in constant American dollars I don.t think Canada would be to far out of line.

I’ve noticed on ebay many Chinese sellers were quoting in Canafian dollar recently. Not sure if there’s any correlation.

On ebay.com, or ebay.ca? The listings are separate unless the seller pays to have them cross-listed (free for smaller sellers, but most of the Chinese sellers are high-volume)

All the nations that didn’t get blown up by 2008 and the US housing bust, spread internationally with derivatives, have engineered their own housing booms to blow themselves up.

Ireland, Spain – now dead ducks

Norway, Sweden, Canada, Australia – still waiting.

Japan started the trend back in 1989, it has never recovered.

many countries in Europe had housing bubbles WAY before the US bubble of 2005 or so.

The Dutch housing bubble started around 1990 (1985-1988 in the big cities, 1991 was the first year with double-digit price increases for the whole country), it is still growing. Several other EU countries like UK had housing bubbles that faded and came back thanks to ever more government support. It is also obvious that many of the bubbles started around the financial centres (in the eighties London, Paris, Amsterdam; only Germany escaped the bubble trouble due to the re-unification). The root cause is central banking and the economic policy that goes with it.

Spain may be a ‘dead duck’ in the sense that the RE market isn’t healthy, but prices are still extremely rich in most of the coastal areas. People who purchased a bit longer ago are still sitting on huge paper profits (but I guess most of them don’t want to sell with a 30-40% haircut because they feel entitled to more).

Bankers relaxing lending criteria into a boom and tightening into a bust doesn’t help .

This is what they do in the UK anyway.

The broad brush of monetary policy doesn’t help either.

Really low interest rates – great – I can get a really big mortgage.

Many years ago when Alan Greenspan first started using interest rates to control the economy, the critics said it was far too broad a brush, they were right.

Dutch politics has been debating for 30 years how they could defuse the bubble (there was a prior bubble that burst in 1981 which caused minor financial damage but major political upheaval). They haven’t made any progress because of course it is NEVER a good time to tighten lending standards, remove subsidies and tax incentives etc. The only thing that has been accomplished is that the mortgage tax deduction will be slightly limited over the course of 30 (!) years (and still be the most generous in the world).

Similar to Alan Greenspans policy of serial bubble blowing.

The best time to buy a home is when interest rates are sky-high; I like small mortgages (and I like buying without a mortgage even better, but again only when interset rates are sky high and money has value). Buying a home at really low interest rates is only clever if you have no money and never expect to have any (in case rates go up, home values plunge and the lender decides they want their money back).

Greenspan used to say if you understood what he just said, you’re wrong (paraphrased).

My take is Greenspan had no idea and was admitting he didn’t know what he was talking about. Sounds pretty dangerous to me.

Recall, he touted adjustable rate mortgages and that was great until he began raising rates the house of cards toppled and many people lost their homes to guess who…, bank owned.

The entire charade was arranged for the purpose of transferring wealth, the largest ripoff in human history. Federal Reserve was at the epicenter, making certain banks had plenty of capital to take advantage of the panic created by, on purpose, the federal reserve.

I was nearly the biggest fool on my first house purchase, once bitten twice shy.

I kept thinking this can’t go on, but it did.

Before I got priced out altogether I got in.

When the most hardened cynic capitulates that is the end of the bull run, been there, done it.

Commercial real estate in the big Japanese cities has been doing very well, thank you. Residential real estate in the big cities is just as expensive, if not more, than it was years ago. Huge price tags for new high rise condos.

However, in many places outside the big Japanese cities it is cheaper to buy than to rent.

In fact many places in Japan have cheaper houses than in Australia or even in the USA.

You can get a nice place within an hour train ride of Tokyo for around $US$250,000. And that is for a place with 1/4 acre of land.

Here in Melbourne you can not even find a dog house for that price within an hour of the CBD by our pathetic, overcrowded, late as usual train system – when it runs.

Go out to the real ‘country’ areas in Japan and you’ll find huge houses and huge tracts of land for unreal prices.

The problem with much real estate in Japan now is that population in many smaller places is falling and as that happens the real estate values continue to fall.

Latest estimates I’ve seen are that about 15 to 20% of the housing stock in Japan is vacant.

The key is to find a decent sized city with good transport that has had a stable or increasing population and where number of people using the rail system has remained the same or increased.

It’s interesting that nobody ever bothers to comment on Japan’s unemployment metric.

There’s nothing more forlorn than an unemployed workaholic.

There really is no employment problem in Japan.

There are more than enough jobs for people there now – a situation that has changed from when there were more job seekers than jobs.

The problem is that wages for the jobs that are available are either low or falling.

Too many what we would term casual or part time jobs with low wages.

For foreigners wanting to work in Japan the situation is even worse.

For example, university positions.

I look at jobs for foreign teachers at Japanese universities about once a week.

In reality there are no more real university lecturer or professor positions there anymore.

They are more like wage slaves.

I saw one post doc position for a foreigner at a national university for a whopping 275,000 yen per month income. (Less than $2500 a month once tax, health insurance, and pension costs are taken out!!!)

Another national university was paying the amazing amount of $3000 a month for a PhD – full time 5 days a week at the university, etc., etc.

Compare that to 30 years ago: 6 classes at your full time university, no limits on adjunct teaching, free once you put in a few hours of office hours, meetings, and classes, 2 month summer breaks and winter breaks.

And the pay? Well……………a hell of a lot more than that!!! (I paid twice as much in Japanese income tax as I make now.)

There were also opportunities for consulting and translating.

Not much so anymore and if you do find them the pay is peanuts.

That’s why Sydney and probably Melbourne as well are still booming.

We are having a housing shortage, in Sydney at least 100,000 houses short. So as long as people want to move to Sydney the boom will get oxygen. My friend in Sydney was offered $5 Mil recently for her terrace – double what its market value is and more than 5x what she bought it for less than 10 years ago. The boom is still booming.

I have read many reports about trophy cities (Vancouver, Toronto, Sydney, San Francisco…) claiming or showing that non-resident investors, particularly foreign investors who want to get money out of their countries, are buying residences in relatively large numbers and leave them unoccupied. That can create an artificial shortage. This is an investment that they hope they can sell for more money down the road. When prices begin to fall enough, they’ll try to sell them – and SUDDENLY the shortage turns into a glut.

These are not always high-dollar homes either. A lot of them are mid-range.

There is a condo tower in San Francisco that has been marketed entirely to Chinese investors. Hardly anyone actually seems to live there.

I think this is very similar in many other countries, RE prices are local. If you can work from home and don’t need the facilities of a big city or a strong employment situation, you can usually buy much cheaper.

If this is a realistic option when you are still working (compared to people who are retired) is often questionable. In the nineties quite some Dutch IT entrepreneurs and managers decided to start living in France (where at the time you could buy a complete castle for the price of a small Dutch home, plus you enjoy the French ‘lifestyle’ instead of the stress, pollution, bad food etc. that the Netherlands had to offer). The idea was that you could drive to your clients or office for face-to-face contact e.g. one day a week (takes a few hours by car). But almost everyone returned after some years, apparently working from a French residence didn’t work out.

From what I have heard, there IS an employment problem in Japan e.g. Hokkaido seems to have way too little work for the young generation, with the result that most of them leave. I bet RE prices are quite low there. Again, if you are self-employed, can work from home and enjoy rural life that could be great, but otherwise …

Also in Oz: although prices in the big cities like Sydney are ridiculous, farther out in the country (sometimes even in the suburbs of the big cities ) you can buy homes for prices that look like a joke in my country (nobody would believe it is really so cheap). I have family who live in a small town in Oz (not too far from Melbourne) and their home would be about 3x more expensive in Netherlands, of course taking exchange rates into account.

In my own country there are a few areas that are significantly cheaper too, e.g. a small part of my province can only be reached from Netherlands nowadays through a tunnel, which is a psychological and financial barrier. If you start living there, you become almost a citizen of Belgium in practice ;-) Also, there is little work there with the result that home prices can be much lower (but not everywhere, because neighboring Belgium has pushed up prices along the border over the last ten years or so).

If will be interesting to see what happens when we get some ‘disruptive technologies’ that make working from home much easier. Not just IT technology, but also things like homes that are self-sufficient for energy/water, affordable small planes or quadcopters than can touch down everywhere without special facilities or maybe delivery drones that can supply everything you need on demand and for reasonable cost. But for now, there are many practical issues.

Canadians who do not live in these overpriced markets really don’t care if they go under or not. Canadians who are not overly in debt do not care about impetuous people in personal debt up to their eyeballs, either. It’s all relative. If pensions take a haircut people will lower their purchasing and prices will drop to accomodate who can buy and what they deliberately choose to buy. Debts will be paid, one way or another, and maybe people will take heed and listen to common sense instead of rushing to get into the market at any cost.

To be honest, as this real estate stampede has progressed I have developed an embarassment to being Canadian. I simply find it hard to believe it has happened to the extent that it has. We are in a desperate need of a correction before it gets worse.

RickRod, good decision. Smart way to view a job prospect. How can one put a price on ‘quality of life’?

Well, off to siphon/rack some wine.

The housing bust spreads out into the general economy.

The sensible lose their jobs too, this is why they are so dangerous.

yes, and even before the bubbles burst they already severely distort the economy because most of the money flows to activities related to the bubble and not to productive investments.

When everyone is basking in the potential capital gains from housing they do not question the price.

When the capital gains stop, reality hits and the collective insanity moves to the harsh reality of fundamentals.

When house prices rise the owners (especially those with the maximum mortgage) are brilliant; when house prices decline they have been cheated and government has to do something to help them, and make sure that prices go up again.

If you read all the requests from the Dutch home owners association after 2008 (when Dutch home prices declined 15-20%, after a prior runup of about 1500%) it was equivalent to demanding from politics that they throw all renters and savers under the bus in order to make them rich again. And of course politics did just that, because renters and savers are a minority in my country and the elite (the real housing speculators) likes the bubble too.

My country (Sweden) is reportedly one of the worst in the world when it comes to housing prices:

https://www.imf.org/external/research/housing/

Personally, I can vouch for this. The apartment I paid under a million for in 1993 is now worth ten times that.

FWIW, My apartment rent in Italy was one million Lira/month, many years ago.

The home that I purchased in 1992 and had to sell in 2001 with about 500% in paper gains is now valued at 15x the 1992 price (without any improvements, and all prices converted to euro currency). This is typical for many better quality homes in Netherlands, but also for many small homes in the cities that appreciated by over 1000%. Only for apartments (excluding the luxury market) the price gains have been much smaller, about 500-600% from the early nineties.

In 1990 less than 1% of the homes in my city cost more than 100K euro; nowadays there are possibly a few homes (small apartments) available below 100K euro but these are the proverbial needle in the haystack and probably in such bad shape that you have to add 50-100K before you can live there …

In 1992 mortgage rates in Netherlands were around 12% and you needed a 20-25% down payment; today rates are below 1% and a downpayment is only required is special cases – 103% mortgages are the standard so even closing costs etc. are covered. That simple fact explains most of what has happened (in addition to the countless other government measures to keep the bubble growing).

100k?

The cheapest free standing house in my suburb located 45 klicks from the Melbourne CBD is currently listed at $A380,000.

It needs work and is on 631 square metres of land. The next cheapest is listed at “over A$400,000 plus buyers”, and the next one after that at “Negotiation over A$430,000”.

The cheapest townhouse is listed at A$430,000………..

So much for cheap housing here.

There’s no housing Bust unless major recession hits and people lose their jobs. Calgary housing has gone down a tad 5-10% after oil fell a year ago.

Vancouver and Toronto ain’t coming down. The government will pay the mortgage of those unemployed via programs.

In San Francisco Bay people keep waiting for a bust, meanwhile there’s still people making bank in this recovery. Top End went down a bit, but lower end gets more expensive as we speak.

LOL! Must be your first rodeo – that is one of the best signs that the market has topped – the smart money bails first, while the weakest hands continue to step in, thinking now or never. Couple that with lending standards getting whittled down to nothing and you know game over is just around the corner, just not everyone has got the memo yet.

OutLookingIn

“The debt is paid. Either with dollars worth pennies, or with pennies worth dollars. What is not to understand?”

How you can insist that “all debts are paid” when every bankruptcy court in the world, every lein holder who has ever written down a bad loan, and every loan shark who has ever been stiffed disagrees with you.

First of all, Vancouver and Toronto are two of the best cities to live in… on the planet. It is natural that these cities attract foreign buyers and the influx of foreign $ has been going on for decades.

In addition, the C$/US$ dropped ~35% from mid-2014 to Jan/16 effectively giving a large price discount in many currencies. Why? Crude crashed to 50%??). However, ‘trading up’ to a larger/better home is an important part of the real estate market. Those ‘trading up’ will greatly increase their mortgage but also have a big chunk of equity.

Thirdly, the ordinary Canadian has very few tax-free or low-tax savings options except their home. Mortgage interest is not income tax deductible in Canada. The ‘savers choice’: Pay down your 2-3% mortgage (after tax) or get 1-2% on a CD (as taxable income). Canadians tend to pay off their mortgages. (Go look at the stats, I didn’t bother comparing Can/USA).

Fourth, student loan debt in Canada is much lower. Fewer Cdn graduates graduate with student loans (by about 10% with USA =~71%) and the average debt is lower (approx. C$26k? vs $US 37k?, I didn’t look up the latest data nor check for apples-vs-orange stats). This is a big chunk of the pool of first time home buyers 5-10 years from now. Think about that for a while. Just how long will it take your kid & spouse to pay off their student loans and save $70k-$100k for a reasonable down payment in a non-prime market?

Bottom line: IMHO, the Canadian ‘crash potential’ is low without a very nasty global event (upon which everyone, everywhere is in deep s%^t ). Is a ‘frenzy’ correction or extended ‘flat’ period possible? Maybe/Likely.

Another old axiom that I seem to have forgotten, that was gifted to mankind by Mark Twain. “Never argue with a stupid person. They drag you down to their level, then beat you with experience”.

Watched yellen on Wednesday. Still coming up with jargon to avoid a rate increase. I wonder if they’re concerned about the USD gain too much strength?

Well, the market thinks there’s a 68% chance of a December hike. Up from 55%. So I guess my interpretation was not in agreement with the market.

IMNSHO what we are seeing is a rerun of Disney’s “The Sorcerer’s Apprentice,” where Mickey invokes forces he cannot understand, and certainly cannot control.

The big central bank fear seems to be they may collapse the global socioeconomic “house of cards” if they make ANY changes, the main problem being that the “house of cards” is going to collapse at some point, and building it higher cannot prevent this.

It is worthwhile to remember that more than 95% of what circulates as “money” is actually bank credit, which will vanish when the “house of cards” collapses.

Doesn’t Canadian mortgages have interest rates that adjust every 5 years? So it is worse there because they dont get fixed rates like the us.

Have you seen the new zealand property market in auckland? the chinese have caused such unprecedented asset inflation there! House prices increased from 100% through to 150% from 2008 just because of chinese speculators. The NZ market is in a huge mess!

they destroyed Vancouver, our city overrun by dirty chinese offshore money

For all the Americans reading this- you know how foreclosure ends mortgage recovery there? Not here- if you’re foreclosed on, and the house doesn’t cover the value of the mortgage (eg underwater due to housing bust), they can garnish your paycheque until the full value is repaid. No jingle mail here- the underwater are literally debt peons.

That’s a very common misconception about the US – and thus about Canada. There are only about a dozen states in the US that are “non-recourse,” which is what you’re describing. The rest are recourse – same as in Canada.

In recourse states, when people run out of money and can’t make the mortgage payment, the bank can go after the borrower until hell freezes over or until the borrower files bankruptcy, whichever comes first. Bankruptcy means, “Game over” for the bank. Mortgage debts will be discharged. No garnishment, no nothing.

So why throw more good money after bad? Same is going to happen in Canada. Banks aren’t stupid. When something becomes uncollectible, they stop throwing money at it and cut bait.

Thanks for the clarification Wolf! I have clearly been misinformed. So in all US states, bankruptcy discharges mortgage debt? My understanding is that in Canada, as mortgages are secured debt, they are not discharged in bankruptcy, and the bankrupt person must surrender equity- so they can continue to garnish your wages if the house doesn’t cover the mortgage debt in full.

The only consumer debt – secured or unsecured – that cannot be discharged in US bankruptcy court are student loans. That does not mean that ALL debts are discharged. The court can decide what payments you can reasonably make … on say some credit card debt. And so not all debts may be discharged.

Note: you cannot keep the house if your mortgage is discharged.

I really would like a lawyer who knows how bankruptcy works on both sides of the border to weigh in and do a little compare-and-contrast. This comes up all the time, and I would love to have some clarity.

‘Bankruptcy means, “Game over” for the bank.’

Try reasoning with OutLookingIn about that. He insists that ‘all debt will be paid’, strangely unaware of bankruptcy courts and bad loan writedowns.

Maybe its just an attempt at gaslighting. It can be an effective propaganda technique, and one does see rather a lot of it these days.

Walter, I think what OutLookingIn is trying to say is that when there’s a debt default, the creditor loses money and therefore is “paying” the debt.

CV Myers wrote the book The Coming Deflation in which he said the same thing, that the debt is always repaid, one way or another. He meant that national debts will be paid by inflation, ie., dollars worth pennies, or by deflation, ie., pennies worth dollars. Myers came down on the side of deflation, hence the title. He wrote the book in 1979. Still waiting.

Since deflation would be deadly for the FED and their handlers, it seems unlikely that it will occur. Those who say that they can’t make money fast enough to avoid deflation are not explaining how the FED et al made money fast enough in 2008, or 2000, or all other times. The money supply never contracted.

There could be a short deflationary period, but if deflation appears to be truly recalcitrant, the FED will change the rules for money and start inflation all over again.

IMWO, inflation is in our future, foreva.

Marty –

Thank you for the clarification.

However some are just not able to see the forest, because of all the trees blocking their view!

What OutLookingIn means is either the lender or the debtor will pay.. If a loan is discharged at bankruptcy then it was the lender who lost (paid) his money.. If a bad loan is written down then the person(s) who put up the money lose (paid)..

With all of this ZIRP and NIRP making money is next to impossible for those who are trying to live off their capital which means dangerous stuff is being funded looking for any yield. If all debts get paid by some means then we are in for a poo storm of unfathomable proportions.

My response to urban real estate bubbles in any country…..

https://www.youtube.com/watch?v=MAJPjPf9sLI

Does it matter that Canadian mortgages are mostly recourse loans? I doubt it because if the borrower can’t pay, they just can’t pay. You can threaten that they will never be able to borrow again but if I were in the hole by $250,000 or $500,000 I’d say too bad. Try garnishing my wages, I’ll work off the books in the gig economy. Tarnished credit history when renting a home, I’ll leave an extra months rent as deposit. And in many cases you can just use your spouse or kids name to purchase with credit in the future. You can’t bleed a stone. Having recourse means nothing. The banks and the government by extension are going to take a bath on this for many years to come. But they caused this mess so I don’t feel too bad for them.

And now we are getting much closer to not being able to ‘work off the books’ as we go cashless.

You WILL be assimilated.

Canada and US are not as clever as the Netherlands: we have a National Mortgage Guarantee that guarantees (with government backing) that you can never make a loss when you have to sell your home due to loss of work, divorce, serious health issues etc. This is a major bubble factor because most mortgages start out at 103%, so home owners have NO skin in the game apart from virtual gains through recent home prices rises.

So: the home owner can pocket all the gains if the property appreciates (tax free!) and dump all the loss on the taxpayers in case the house depreciates (just make sure you argue with your boss or your wife first …). Privatize the gains and socialize the losses, small capitalist edition. Great isn’t it, except that of course this is a super Ponzi, the guarantee has a backing of just 0.4% of the insured mortgage amount. As soon as there are serious price declines the guarantee fund will go bust and after that probably the Dutch state because of all the leverage, which means bad news for all those clever (previous) home-owners.

nhz, your posts are very valuable. thank you.

It seems to me that in the US fascist state, the hoi polloi will NEVER be given the safety net that the Dutch gov’t gave homeowners. The gig is to strip wealth away from the 99% not only through taxes, regulation and inflation, but also actively bankrupting them, taking what’s left and handing it to corporations.

Tptb did that relentlessly with farmers, for example, encouraging them to load up with debt to buy equipment and bankrupting them in the inevitable ensuing lean years. They did it with housing 2002-2008 and they are continuing to do it with student loans.

There appears to be no need to throw ‘Merikans a bone such a guaranteed floor on their assets. We’ll all just move into tiny houses and shiver in the dark. As long as the Miller lite and NFL are piped in, nobody will even make a peep.

but … the Dutch ‘safety net’ is not a safety net at all. It’s a scam that gets the 99% into even more debt. Fanny and Freddie are a bit similar to the Dutch mortgage guarantee system, except that they insure only a small part of the market while the Dutch system covers basically 90% of the mortgages, and a large majority of all home owners.

IMHO the Dutch system is more perverse than the US system because when the Ponzi ends the cost will be shifted to those who were NOT responsible and still have some money (renters and savers) while all the irresponsible home owners will walk away free. In the US that would be less obvious and primarily those who took on too much debt will feel the pain – which is honest to me, nobody put a gun to their head and demanded that they buy a bigger home than they could really afford.

Of course it is difficult to predict what politics would do if there is a massive housing crash, both in Netherlands and the US. People are getting used to bailouts for everyone …

Marty

‘Walter, I think what OutLookingIn is trying to say is that when there’s a debt default, the creditor loses money and therefore is “paying” the debt.’

So ‘not paying the debt’ is somehow equivalent to ‘paying the debt’.

I smell a semantic tactic that reeks of doublespeak with a dishonest agenda.

Note that banks have become notorious for not writing down bad loans so as to avoid ‘paying the debt’, so that once again ‘not all debts are paid’, as Don Quijones, Michael Hudson, and financial realities have assured us, and despite obfuscatory definitions.

I cannot speak for OutLookingIn, but I think he is just trying to make you think about who actually gets to absorb the losses when debt is defaulted upon, whogets to prfit, and how it happens.

Basically, the Powers That Be (banks, wall st, the top 1%, cronies in government, the central bank (FRB in the US), etc) will collude to shift the losses onto main street through inflation, bailouts (taxpayers fund it), monetary policy (manipulating interest rates down takes money from savers and pensioners and turns it into higher bank profit margin on existing fixed-rate loans), and selectively making credit availalble only to the top 1% when getting credit is VERY valuable.

He is not gaslighting you. He trying to make you think. I agree he is being a bit obtuse, but I think he means well ;-).

As Marty hinted above, inflation means debt gets paid with money worth less than before (dollars worth pennies). On the other hand, asset inflation as in the housing bubble, followed by a bust, followed by defaults, followed by lending cheap funds (ZIRP and QE) to Hedge Funds and Private Equity to buy up 6% of the US housing stock in 2009-2013 (circa) at firesale prices (pennies worth dollars), is the other method. It is all about privatizing the profits and socializing the losses.

I hope it is making sense now.

It amounts to redefining words to mean their opposites. You’re bringing in inflation as a red herring.

Gaslighting is a favorite tactic of con artists in the financial industry. We do research on them and get a lot of leads on this site.

Well, when there is nothing else happening in the Canadian economy, having foreigner come in to launder money in your real estate sector is the only way to go.

Well, looks like I need to step in and help Walter out. I believe both Walter and OutLookingIn (OLI) had valid points, except Oli is speaking through the lens of a central banker, whereas Walter speaks through a more personal point of view. If your nephew had borrowed 10 000 from you 10 years ago, to buy his first house, and never pay you back, then that debt wasn’t pay, whether it is now worth pennies or not. Or you can try using Oli’s quote, in a bankruptcy court, to argue you should stay in your own home, even though you haven’t make your mortgage payment in the last two years, see if they will accept your reasoning.

As a Country, that quote might mean something when you have to negotiate with your creditors.

Cheers, and have a good night.

Its been said that debts will always be repaid either by the borrower or by the lender. If its the lender then the lender ends up taking the loss. Isn’t that the reason we used to have interest rates once upon a time. The riskier the loan the higher the interest rate used to be.

I’ve given up advising my fellow Canadians to sell and rent before the bubble pops, but no one is listening. Look up ‘Cognitive Dissonance’ and you’ll see a picture of a Canadian homeowner.

As Wolf described in a previous post, the US Government, as a result of the financial crisis, now effectively insures all US home mortgages. Banks, which can’t make money via loan spreads, are happy to make mortgage loans and sell them into collateralized mortgages, keep the fee, spread and servicing income and dodge the value bullet. Brokers don’t care about the value because they just earn a fee for the sale. Appraisers are just working stiffs who get hired by lenders/brokers, both of which are ambivalent to value, so appraisers don’t care about value either.

Its the sheep who are the problem. I get it, sheep need to live somewhere, and sheep get worried that they are going to miss out (FOMO) so they follow the other sheep, pay 50% of their income to the mortgage and feel worried/overjoyed over their piece of the American dream. If things don’t work out they can default, rent and start over, so they don’t worry too much about value either.

The only ones who really pay are savers, retirees, pensioners (current or future) and high end taxpayers whose investments and savings are eroded by the sheep’s bad judgement and the government’s desparation to inflate asset values to support their monetary policy decisions. High end taxpayers, the scourge of the sheep, will be the only ones able to bail this out.

If sheep had discipline about buying houses (20% down and 33.33% of income to mortgage), demand would decrease and prices would drop. Instead of FOMO a little financial discipline might be in order.

I’m not sure how we all think there is no inflation. There have been hundreds of trillions of dollars, yen, euro, yuan created since 2008 ($13 trillion in the US alone?). At some point, and maybe only hypothetically, all of that sovereign debt becomes currency deflating the s&#t out of your retirement savings. Its either that or your annual tax liability doubles and the 33.33% you spend on housing becomes 66.6% and you are a sheep again.