Jobs, labor force are declining; housing construction in epic boom.

The San Francisco housing bubble – locally called “Housing Crisis” – needs a few things to be sustained forever, and that has been the plan, according to industry soothsayers: an endless influx of money from around the world via the startup boom that recycles that money into the local economy; endless and rapid growth of highly-paid jobs; and an endless influx of people to fill those jobs. That’s how the booms in the past have worked. And the subsequent busts have become legendary.

The current boom has worked that way too. And what a boom it was. Was – past tense because it’s over. And now jobs and the labor force itself are in decline.

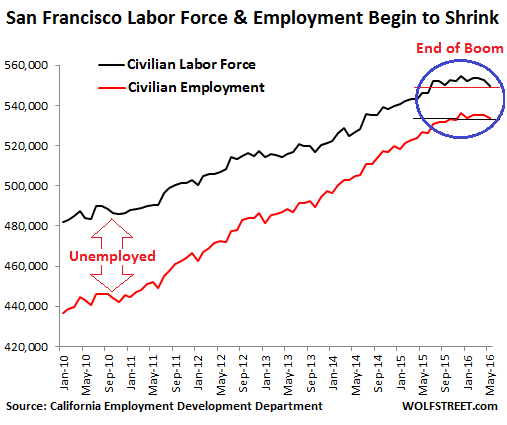

Until recently, jobs and the labor force (the employed plus the unemployed who’re deemed by the quirks of statistics to be looking for a job) in San Francisco have been on a mind-bending surge. According to the California Employment Development Department (EDD):

- The labor force soared 15% in six years, from 482,000 in January 2010 to its peak of 553,700 in March 2016.

- Employment skyrocketed 23%, from 436,700 in January 2010 to its peak of 536,400 in December 2015. That’s nearly 100,000 additional jobs.

This increase in employment put a lot of demand on housing. Low mortgage rates enabled the scheme. Investors from around the world piled into the market. And vacation rentals have taken off. As money was sloshing knee-deep through the streets, and many of the new jobs paid high salaries, the housing market went, to put it mildly, insane.

But the employment boom has peaked. Stories abound of startups that are laying off people or shutting down entirely. Some are going bankrupt. Others are redoing their business model to survive a little longer, and they’re not hiring. Old tech in the area has been laying off for months or years, such as HP or Yahoo in Silicon Valley, where many folks who live in San Francisco commute to.

So civilian employment in May in SF, at 533,900, was below where it had been in December. The labor force in May, at 549,800, was below where it had been in July 2015. Some people are already leaving!

The chart shows how the Civilian Labor Force (black line) and Civilian Employment (red line) soared from January 2010. As employment soared faster than the labor force, the gap between them – a measure of unemployment – narrowed sharply. But now both have run out of juice:

During the dotcom bust, the labor force and employment both peaked in December 2000 at 481,700 and 467,100 respectively. Employment bottomed out at 390,900 in May 2004, a decline of over 16%!

The workforce continued falling long past the bottom of employment. SF is too expensive for people without jobs to hang on for long. Eventually, they bailed out and went home or joined the Peace Corp or did something else. And this crushed the SF housing market.

But by the time the labor force bottomed out in May 2006 at 411,000, down 15% from its peak, the new housing boom was already well underway, powered by the pan-US housing bubble. In SF, this housing bubble peaked in November 2007 and then imploded spectacularly.

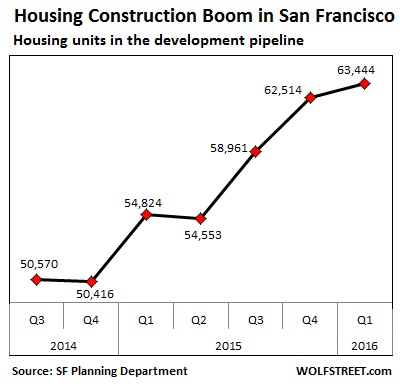

So now, even if employment in San Francisco doesn’t drop off as sharply as it did during the dotcom bust, in fact, even if employment and the labor force just languish in place, they will take down the insane housing bubble for a simple reason: with impeccable timing, a historic surge in new housing units is coming on the market.

According to the SF Planning Department, at the end of Q1, there were 63,444 housing units at various stages in the development pipeline, from “building permit filed” to “under construction.” Practically all of them are apartments or condos.

This chart shows that the development boom is not exhibiting any signs of tapering off. Planned units are entering the pipeline at a faster rate than completed units are leaving it; and the total number of units in the pipeline is still growing:

Many units will come on the market this year, on top of the thousands of units that have hit the market over the last two years. Once these 63,444 units are completed – if they ever get completed – they’ll increase the city’s existing housing stock of 382,000 units by over 16%.

If each unit is occupied by an average of 2.3 people, these new units would amount to housing for 145,000 people. This is in addition to the thousands of units that have recently been completed as a result of the current construction boom, many of which are now on the market, either as rentals or for sale.

This surge in new, mostly high-end units has created an epic condo glut that is pressuring the condo market, and rents too, to where mega-landlord Equity Residential issued an earnings warning in June, specifically blaming the pressures on rents in San Francisco (and in Manhattan).

Manhattan’s condo glut also has taken on epic proportions. Sales of apartments in the second quarter dropped 10% year-over-year, to the lowest since 2009. And condo prices plummeted 14.5% in 3 months. Ugly! Read… It Gets Real: Manhattan Apartment Sales Plunge

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think this is not happening fast enough. At the same time, I think a lot of startups are better financed nowadays. I am not saying that they have a better business model, but a bunch of them have a lot of cash in the bank. I regularly read stories of even small ones confident of weathering bad times for the next couple of years.

This assumes demand remains steady. A lot of the startups serve other startups (cloud services, food delivery, job recruiting, etc) so any effect will be multiplied.

Yes, everything is at a safe level, until it isn’t. Then it’s time to hit the panic button, realizing that the Big Bang Theory isn’t confined to universes. We’re watching as the entire world gets ready to crash and burn. It’s going to be really ugly, but until then there’s every confidence that everything is okay.

Time to stock up on popcorn :-)

Don’t forget the beer

I’ll stock water and storage food, too.

No worries, FB, Google, Apple and the likes will just raise every workers wage to 15 an hour so they can afford all that housing in the “golden city” .

Or not.

You think 15 an hour can support living in SFO area ? You must no something I’m not aware of. That’s chump change !

15 an hour wouldn’t pay for rent in the garage of a suberb out here… lol

Hey Wolf when this thing hits bottom you can probably pick up posh new digs for the price of a premium doublewide trailer, er excuse me I’m showing my age, MANUFACTURED HOME. With everyone fleeing California you could probably insulate yourself like Zuckerburg by buying the surrounding units. Oh I’m sorry you aren’t a hypocrite. My bad!

You buy low and sell high. That’s the goal. SF will never be cheap. But it will be cheaper. And there will be a time to buy. But now is the time to sell.

I have a gut feeling this may also be the case in Denver.

Depends on where in the Denver metro area you’re talking about. We’ve seen a tapering off in the southern suburbs, but the northern subs are still popping.

The convergence of the Broomfield tech center, Boulder, “Silicon Flatirons,” and some huge players like DigitalGlobe and Google making some big moves in the surrounding areas are fueling a fever-pitch housing frenzy.

I think we’ll see another 1-2 years sustained growth minimum. Optimistically, due to the influx of jobs, I’m hoping that we see a taper off rather than a burst, but we’ll see what happens.

In consideration that it took years for this bubble to build, it will take years to fail. Wolf is giving us a great week by week view of the events that will culminate in the the inflection point that will lead to that failure.

All one has to do is look around your home and wrok to see the signs. The bubble extends to commercial and residential real estate as well as internet nonsense.

The Dutch housing bubble has been building from about 1985, and except for a small blib after 2008 it is still going strong: more than 30 years of bubble economics. I see very few of the desperate measures that the Dutch government is using for supporting the housing market in the US, so if politicians really want there is plenty of upside potential. RE is a cat with many lives.

Even though new production is relatively high in SF (it’s a lot more than the Netherlands is building in a year …) there are simple solutions for that. Just make Angela Merkel the new mayor, let her invite the whole of Africa and Asia to SF for free homes (paid by the taxpayers, of course) and a juicy entitlement package for life, and they will come. The whole condo glut can be absorbed within a month and even if that doesn’t work, a few IS supporters included among the migrants would do the trick. I just think Soros may be a little bit less enthusiastic in supporting this migration route ;-)

No, you’re wrong there! It’s like what Hemingway said when asked about how his bankruptcy had happened. “Slowly at first, and then quite suddenly”. Bubbles may take a long time to build up, but can burst almost over night! Just look at the Dutch tulip craze! It took a solid 6 months to build and peak, then just a few weeks to fall back down again, from what I’ve read.

I don’t doubt a bubble can burst suddenly, my point is that the bubbles can keep growing much longer than most imagine.

Around 2000 many clever people thought the Dutch housing bubble would burst, and it should have without all the government and central bank interference. In my area home prices increased about 5x between 1990 and 2000 with little income growth, home prices relative to incomes were higher than at any time in the previous 400 years. But after 2000 prices still increased by 2-3x, while inflation was relatively low and wages hardly increased. Everyone who sold around 2000 expecting a crash has lost tons of money due to skyrocketing rents (you have to live somewhere and government does everything they can to drive up rents, because that supports home prices) and almost zero return on their cash. I doubt they will ever be able to buy back into the market for anything close to their 2000 sales price …

The tulip craze indeed crashed by 90% in about a week, and that was when news traveled by horse and pigeon, not telephone and internet ;-)

The previous Dutch housing bubble was from 1975-1980 with about 100% gains in 5 years. It crashed by 40-50% (AVERAGE sales price, individual losses were bigger) in 1.5 years. So in a little more than a year almost all the bubble gains evaporated, and that’s without considering inflation which was very high at the time. In the next 5-10 years home prices went nowhere.

However, the current situation is completely different with massive government intervention and guarantees, close to zero mortgage rates etc. Politics decides what happens, if they want I don’t doubt they can keep the bubble alive for many more years – of course there will be very bad consequences :-(

My impression is that CA politics isn’t much different from the idiot ‘socialist’ policies in the Netherlands …

There is no comparison to dutch and california economy or politics. Even with a rainy day fund, we are at the mercy of the ups and downs of the stock market and housing assessments. Once those start to drop, so does the budget and all the freebee programs that are offered here. Thanks to prop 13, the schools will get cut first followed by government programs. NO SUSTAINABILITY in the housing market. Been through four of these ups and downs, wont be the last.

San Francisco’s government is already fretting about the huge deficits coming its way amid the now acknowledged “slowdown.” They’re going to try to put another sales tax on the ballot to fill the holes and avoid some cuts. Good luck!

Prices in real estate is made on the edge, last comp. You better have a clear line of site and unabated path to the exit door, it’s going to get very crowded in and around that doorway. Been through these in the Bay Area since 1985.

Only thing different today is the epic front running by our Central Bank who area trying desperately to eliminate the business cycle and change from a capitalist monetary system to a socialist monetary system.

I have been thinking about the mal-investment and unsustainable debt generated demand sponsored by government around the world.

My opinion is that United States will not go cheap before other countries have no money to buy.

I suspect this is the strongest force for all countries and their controlling governments.

Us, Japan, China, Europe, all are waiting others to bust first.

Reason is simple. I ate your lunch and gave you 1$ IOU, and when you come to my place that 1$ IOU will not buy you the same lunch because here it is more expensive.

If you believe the elites have not lost control over the sheeple, the only conclusion I can draw is which ever country is the strongest will bust last.

So SF/NY and the rest of US will bust AFTER you see other counties go FUBAR (F***ed up beyond recognition) because US is still the strongest.

My opinion is that this force is the strongest and can overwhelm all other local supply/demand imbalance.

True. The least ugly girl in the Whore House gets most of the attention.

US policies make sense in this light : sponsor a coup in Ukraine , overthrow dictatorships that kept the Middle East stable(er) , have NGO’s enourage mass migration into Europe, ratchet up tension with Russia a bit more, get the Eurominions to apply sanctions on Russia and Iran (avoid them yourself when it suits you), facilitate a soft coup in Brazil, declare both China, Russia and ISIS threat no 1 – all this chaos is good for the dollar and it will appear to be the safe haven.

I don’t know how large of a factor the Chinese have in the SF RE market, but there’s another “perfect storm” in overpriced RE starting elsewhere.

The NYC real estate market is about to crash

28 Mar 2016

http://www.cnbc.com/2016/03/28/this-real-estate-market-is-about-to-crash-commentary.html

Excerpt:

The U.S. Treasury Department’s recent mandate that the identity of foreign buyers be made known, for purchases above $3 million, could be discouraging overseas investors from buying pricey real estate. And that could have a dramatic impact on sales going forward.

Chinese bank claims fugitive bought luxury B.C. real estate

B.C. Supreme Court order freezes Shibiao Yan’s assets while bank tries to get back $10 million loan

Jun 27, 2016

http://www.cbc.ca/news/canada/british-columbia/china-real-estate-vancouver-fugitive-1.3655136

Excerpts:

“The lawyer who represents the bank, Christine Duhaime, would not comment on the proceedings, but tweeted that the case was of “global significance for China”.

The court case comes amid ongoing speculation about the role of offshore money and cash from wealthy Chinese investors in particular, in driving the out-of-control Lower Mainland real estate market.

——

Those two factors should help reduce the Chinese demand in real estate markets previously hot because of their monetary flight induced demand since both the Chinese government and the US Treasury are now interested in the buyers’ identities.

“The NYC real estate market is about to crash. 28 Mar 2016”

Here’s June:

https://wolfstreet.com/2016/06/30/manhattan-apartment-sales-condo-prices-plunge/

$3 Million? All a “rich” Chinese guy has to do is spread the money around to more than one home. $3 Million can get you some really nice homes across America.

If the intent is to get the money out of China, put is someplace where you have something left, then buy nice properties away from the Right and Left Coast. Homes on golf courses and retirement communities retain some value and one can get a hell of a home at these gated communities for $3 Million.

At $3 Million a home, the buyer may have more security and value by buying in “central” America and not pay inflated coastal prices. Even then, why buy a home? Why not purchase shopping centers, high end apartments or even vacant land? Commercial Land? Farm land?

IF the coasts are bubbles and if they look at any purchase above $3 Million, just avoid all that.

Which I’m sure they will, but the point made is about the inflated high end markets in the mentioned cities. The artificial inflation of markets will be spread out, thereby leading to less extreme overpricing in the white hot RE markets.

I was watching morning tv last week and the Clinton surrogates were out with an open and rather large goodie bag.

As a result, I expect any residential real estate projects that run aground to be bailed out by the govt, as workforce, or section 8 housing. I think this was what Zell was trying to avoid when he bailed out of his bad projects. While these govt programs may stem the initial problem, they cap rents over time and are not so great for the investors.

BTW, I was checking out rentals in South Florida and while rents have gone even higher, they are now openly accepting section 8 vouchers in their ads.

yes, that’s the situation in my country: RE bailouts forever, real investors in the housing market have been marginalized for years so effectively the government controls almost the complete market – the low end through housing corporations and social housing subsidies, the high end through mortgage subsidies and endless guarantees.

Despite skyrocketing rents, the housing market is hardly profitable for real investors because private homeowners are heavily subsidized, with the taxpayers effectively paying over half the cost, while investors get nothing – it’s difficult to get more than a few % gross return on investment, while the risk is pretty big because the whole market (both homes and land) is seriously overpriced.

Just today our ‘TV News’ (government propaganda channel) voiced concerns that young and/or single people are unable to buy a home despite the lowest mortgage rates in 400 years (of course, home prices have risen by 10-20% again last year in the big cities, thanks to Mario and his gangsters).

Those ‘potential buyers’ complain that it is not fair to expect them to rent, because renting outside the social housing sector is 2-4x more expensive than buying, and for buying you nowadays sometimes need a downpayment of about 5%. The country was used to getting at least 5-10% extra from the bank when you ‘buy’ a home, so a downpayment is a ridiculous idea. Fortunately, the TV News has the solution for this problem: the government should again provide the downpayment for young and single buyers (and migrants, and all other disadvantaged people who want to buy but don’t have any money), just like they did in the nineties (when interest rates were 10x higher than today, and banks still checked if you would be able to pay off your home).

So rich developers use the Gov again to save their investments and its Clintons fault. Hello Republican Congress approving the funding. You always forget who actually appropriates funds.

The Developers have not. Its not a Repub or Demo thing. Its business buying the access and votes it needs. Try again.

While both parties waste our money, the democrats are the ones openly offering bribes for votes. I can already see the use of section 8 vouches being a big deal in the new deluge of south FL rentals, they solicit them in their ads.

The republicans would do it differently thru lower taxes, lower interest, or direct subsidies to the owners or bondholders. The parties cater to different interest but the taxpayers always land up with the bill.

SF is the ultimate cesspool. I live in the East Bay and have to commute into and through SF all the time. The amount of streets torn up due to construction activity and traffic congestion paralyzing movement through the city is unbelieveable. I don’t inderstand why anyone would want that kind of work and living scenario. In addition the freeway situation in, out and through the city is horrific, and I’m from L.A. so I know bad traffic but this is a whole different level of bad.

The city is massively overbuilt in a a very odd mixture of very old decrepit buildings and infrastructure. And they keep shoe-horning more and more into a beyond overloaded saturation point. It spells disaster and the increasing supply glut is a real precursor to the coming economic collapse.

and when “the fault” finally moves? How is 911 response in SF?

It’s been quite a while since I’ve been to the SF Bay, but these are interesting observations in your last paragraph. The Calaveras and Hayward Faults are storing a lot of pent up energy. When a quake rattles, how will this shoe-horning survive?

We’re all waiting for Musk to give us the Hyperloop for getting around town and across the Bay.

Backed by taxpayers obviously.

Double D has a low tolerance for change & progress, and the poor dear is “inconvenienced” by traffic & infrastructure activity.

Imagine that: one of the most desirable cities in the world AND IT HAS TRAFFIC! WHO KNEW?

San Francisco is not massively overbuilt – most of the housing stock is old (post 1906 quake & post WW2) units of less than 5 stories. The tall buildings seen in pictures are, for the most part, confined to what used to be called the financial district – the northeast corner of the city. As large an area (the Sunset district) is primarily 2-story single family homes with tiny lots (and grass, the kind you mow).

Depending on your faith in earthquake building codes (me, not so much), the housing capacity of the city could easily be doubled by simply replacing old single unit housing with taller multi-unit structures. Real problem is traffic – excluding the laughable Muni street bus system, SF has very little city-wide municipal transit.

Here’s someone who moves through SF fast. Do NOT try to do this yourself:

https://wolfstreet.com/2012/07/12/fastest-drive-through-san-francisco-ever/

That was wild! But I don’t get how they cleared the route for the guy without a single living person watching. Even first thing in the morning. I guess Ford paid for it.

Some tires are for sale now.

Would you ride along?

THAT WAS TRULY EPIC!

How did they ever get SF approval to do that? It makes BULLET look like a Cub Scout project.

SF has a special office to deal with film makers. They close off streets, disallow already scare street parking, organize police traffic controls, and the like. They were filming in front of our place the other day. Cities love to be in the movies (it’s a form of “product placement”), and so they spend a lot of money to make it possible. And I guess/hope the film making activity brings in some money too.

“Imagine that: one of the most desirable cities in the world AND IT HAS TRAFFIC! WHO KNEW?”

Nah, Melbourne, Australia is the world’s most liveable city:

“Melbourne has topped The Economist’s liveability rankings for a fifth consecutive year.”

SEE:

Read more: http://www.theage.com.au/victoria/melbourne-named-worlds-most-liveable-city-for-fifth-year-running-20150818-gj1he8.html#ixzz4DlN3tX9j

Oh, I forgot, housing affordability and traffic congestion are not part of the survey.

I wonder if we will make it six years in a row?

And the final event to himself has been, that, as he rose like a rocket, he fell like the stick.

Thomas Paine (1737 – 18090

So many “Minsky Moments” on the horizon.

Australia is experiencing the calm before the storm, its “Minsky Moment” is near.

Neoclassical economics says debt doesn’t matter with its very simplistic assumptions about money and debt.

I am not allowed to see bubbles as a neoclassical economist, they don’t exist. Capitalism heads towards stable equilibriums (but it doesn’t).

Irving Fisher looked at the debt inflated asset bubble after the 1929 crash when ideas that markets reached stable equilibriums were beyond a joke.

Fisher developed a theory of economic crises called debt-deflation, which attributed the crises to the bursting of a credit bubble.

Hyman Minsky came up with “financial instability hypothesis” in 1974 and Steve Keen carries on with this work today.

Of course it as totally at odds with stable equilibriums and has to be ignored by neoclassical economics.

“Minsky Moments”

1929 – US (margin lending into US stocks)

1989 – Japan, UK (real estate)

1999 – US (margin lending into US stocks)

2008 – US (real estate bubble leveraged up with derivatives for global contagion)

2010 – Ireland (real estate)

2012 – Spain (real estate)

Coming soon – Australia, Canada, Sweden, etc …… (real estate)

China is saturated in debt too, perhaps that will implode and many commentators seem to think so.

I’ve always said that job matter in the San Francisco housing market. But one can’t overlook the fact that there is a lot of money printing going on by CBs all over the world translating into a lot of debt being dolled out by banks. Stacy Herbert of the Kaiser Report float an interesting hypothesis that the Chinese government is encouraging it’s wealthy businessmen and bureaucrats into buying up RE assets in trophy cities throughout the world using money borrowed from failing Chinese banks. So when the shit hits the fan, and all fiat currencies start to tumble, the select few in Chinese society will be safe owning RE abroad.

This is why I have always ” believed” only a citizen of a country should be able to buy land in that country. Especially a home.

That’s just the kind of observation I’d expect from KR.

Have you been able to figure out where or what Keiser is politically?

The costs of attracting competent employees has skyrocketed ,partly due to sky high housing costs.My daughter who works and lives in Berkeley hopes that her company will relocate to Colorado ,where overall costs are much lower

r chon

The cost of hiring competent dot.com employees in the silicon valley is high because workers who actually conceive and deliver Google/Facebook/Apple quality products are literally worth more than their weight in gold (FYI about $3-4M). Yes, these employees do pay more to live exactly where they want (high density, hip metropolitan areas with lots of Starbucks), and less powerful earners do get squeezed out. (I’m not justifying this; just explaining facts).

Only an itsy-bitsy minority of the 2016 cutting edge hi-tech superstar workforce would even consider moving to some idyllic pasture in Colorado. This does not mean it’s not a great option for less-than-superstar earners.

Chip,

You have definitely been drinking the Kool Aid.

Petunia

As a retired Fortune 500 CFO from San Francisco, I had to hire talent in that environment. Didn’t give a damn how expensive housing was; only cared how much shareholder value the talent could deliver.

You appear to have a different experience.

Please let me know exactly where I am incorrect so I at least know what flavor Kool Aid you’re accusing me of drinking.

As a techie who traveled extensively while on the job, I can tell you that it really doesn’t matter where you live, because you spend all your time staring at a screen. If you have a stationary job it is still the same. I remember taking a Sunday off, after working every day for months and wandering around my house aimlessly because it felt foreign.

The people who have time to spend their paychecks and go out for expensive coffee are not the real superstars.

Cough cough Boulder….Marijuana is legal and just a bit North is one of the cheapest and best places to send your kid to college.

And there you have it. Advertising, telephones and gossip dressed up as leading edge high tech. Geez, what did we do without these geniuses all these millennia? We are so indebted to you superior human beings.

Silly con valley would be nothing without usg military and spy money. You’re a bunch of whores constructing the US panopticon. SF can’t crash soon enough.

Amen.

I do not work in the tech industry and do not live in CA.I was just stating what my daughter has told me.Evidently she is hardly the only one with this idea

http://www.bloomberg.com/news/articles/2016-04-05/san-francisco-tech-firms-see-workers-flee-from-4-500-rents

Your daughter is smart to get out of the CA tech bubble. She should look for a job in other tech communities in TX, MA, PA, or DC. The list is long and gets longer if she considers going overseas where US degrees are highly valued.

As a kid in the 80s I as shocked to learn that the Japanese pension fund of Osaka bought the local golf course in Oregon. Besides worrying about Russians (ie. Red Dawn movie), I was fascinated by the Japanese, post their Minsky moment. That golf course got re-sold back to Locals for about $.50/dollar in 1993.

American RE will always be desirable to the world….sell high to the Chinese now….let them have their Minsky moment….buy it back later. But you have to be patient.

Now I live in Sydney (parallels to SF are striking) I can’t wait for the bottom to fall out.

Well the median Sydney house is price around A$1,000,000.

Why did you go to Sydney?

Melbourne is better, has cheaper housing, and better people as well…………………….

People have been waiting for the ‘bottom to fall out’ for a long, long, time……………..

64k units in the pipeline. I’m guessing that’s about a 5 year time line.

Yes.

Is that just for San Francisco? There is a lot of appartment complexes being built all around, along Lawrence, Central, Camino Real, ie the core of Santa Clara, Sunnyvale and Mountain View. Very dense, very close to highways and Caltrain noise – not the most attractive housing estate. Is being built very fast in the US style (steel frame+plywood).

You’re right, the building boom is all around the Bay Area. In some places perhaps similar to what’s going on in SF.

Anyone have an estimate how much engineering for potential (probable) seismic events adds to SF building costs?

My understanding is that retrofitting “soft-story” buildings (a floor that has wide open spaces, such as for retail or garages, in a multistory building) is very expensive. But they’re the ones that caved during the 1989 earthquake. If an older building has a bad foundation, it gets even more expensive.

https://en.wikipedia.org/wiki/Soft_story_building

The additional cost of building according to the new code from the beginning isn’t nearly as much as retrofitting.

S.F. luxury market takes a hit as tech buyers and foreign investors pull back

“It looks like the full-steam-ahead San Francisco market is finally slowing down, with overall inventory rising to levels not seen since 2012, when the market was still recovering from the financial meltdown of 2008, according to Redfin data. The segment of the market taking the hardest hit seems to be the luxury market, where the typical buyers (namely tech and foreign investors) are taking a step back, said Redfin agent Miriam Westberg, who specializes in high-end sales.”

http://blog.sfgate.com/ontheblock/2016/07/06/s-f-luxury-market-takes-a-hit-as-tech-buyers-and-foreign-investors-pull-back/

Something doesn’t add up here.

Many units will come on the market this year, on top of the thousands of units that have hit the market over the last two years. Once these 63,444 units are completed – if they ever get completed – they’ll increase the city’s existing housing stock of 382,000 units by over 16%.

382,000 units of housing stock? Really?

Just in your graph which includes this number of 63,444 and only includes a total of 7 quarters – in the preceding 6 quarters I count approximately 320,000 units being in the development pipeline. Add in that 60 odd thousand and you have over 380,000 units in the development pipellne in under 2 years.

So basically you are saying the development pipeline is doubling the housing stock in under 2 years?

Really?

Something here doesn’t add up.

OK, maybe I should have been clearer. So here’s the lingo:

Housing stock is the total number of residential housing units now in SF (houses, condos, TICs, rental apartments). That’s where everyone here lives, and it includes the vacant units. But it does not include units deemed “under construction.”

The development pipeline (chart) measures a fluid number (it’s a “pipeline,” after all). New units enter it during the early stages of the planning process, and completed units leave it (when they become part of the housing stock). That 63,444 units is the total number of units in the process of development as of the end of Q1. Each quarter, that number changes, up or down.

These numbers are NOT additive. It’s like a stock chart taken each quarter. You cannot add up the numbers. Each represents a value at a point in time.

For example, theoretically: If developers pull back sharply and few projects are started, then few units enter the pipeline. As more units are being completed, they leave the pipeline. The net effect is that the total number for that quarter would shrink and the line in the chart would show a downward slope.

Hi Wolf,

It seems as though your analysis assumes a strong correlation between the labor force and the population of San Francisco, and also a correlation between this labor force and employment.

However, a non trivial amount of the population are employed by large tech firms outside of the city such as Apple, Google, Facebook and Linked-in and the tech shuttles allow large numbers of people to make the long commute possible. These shuttle buses did not exist during the last dot com boom and are a significant factor in contributing to the decrease in housing supply.

The majority of tech startups in San Francisco have high cash burn rates, poor management, questionable business models and depend entirely on free flowing venture capital and are likely to contract in number in the next few years as their cash hoard dries up. However, the 5 major tech companies in the Peninsula are far more stable and are quite happy to absorb a lot of the slack in the labor market, particularly engineers, and even more so without a bidding war.

Although over crowded city living and long commutes may not be desirable for workers with families (3 hours a day on a shuttle) , there is still a large millennial workforce and thirty something demographic who desire to live in the city.

So do you think the affect of these mega tech companies will be muted on housing prices?

I just took the SF county data. Silicon Valley is approaching a similar situation but every county is different. I already know of people who lost their jobs on the Peninsula and haven’t found another one (they’re in the 50s, so good luck!).

As you know, many people who live elsewhere work in SF (that’s the main commuting route). People who live in SF and work elsewhere is the (busy) counter-commute.

The correlation between jobs/labor force and housing is pretty strong. The growing number of people working in SF and their high salaries were always bandied about as reason why this was NOT a housing bubble. Now that the numbers are declining, everyone is fretting.

SF Home prices, according to Corelogic, have dropped 2% in June YOY.

San Francisco is already struggling with a budget deficit….

Wolf as it starts it ends. Atherton is epicenter, the grey market in Real Estate post 2008, evaporated there first. It’s already topped out and is rolling over.

I know multiple spec builders, some that had three or more APN’s who have sold everything already.

Secondary markets, Carmel, Healdsburg are still ramping up, they won’t know what hit them when the mid peninsula lets go.

Atherton?! That’s interesting. That’s like the most expensive zip code in the US.

When you say “crushed” do you mean a decline of 15-20%? B/c that’s what happened during the worst downturn in history.

I’m hoping the ~$3M houses drop to around $2.5M by winter 2018 so I can buy. These downturns are great for homebuyers moving up and great for existing mortgage holders who get to refinance.

May I ask when the OP bought his home?

Regards,

Sam

I gave up on my $3,000 a month one bedroom apartment in San Francisco and moved one hour east to eastern contra costa county. I now own a 4 bedroom, 3 bath 3,000 sq ft home on a large lot. I pull into my own driveway and park in my 2 car garage. Yeah, I know it sounds very middle class, but I like owning my own house with plenty of room. My tiny apartment in the city was a dump. MY mortgage on my new house is $1,900 a month.

Home prices up 300% in 3 years … this is normal. Keep buying into the craze so bubble gets bigger. Give me a call when you are dying to get out of your ridiculous mortgage a couple years from now, i might give you 30% of what you paid for the property.